Coupling the Empirical Wavelet and the Neural Network Methods in Order to Forecast Electricity Price

Abstract

:1. Introduction

2. Literature Review

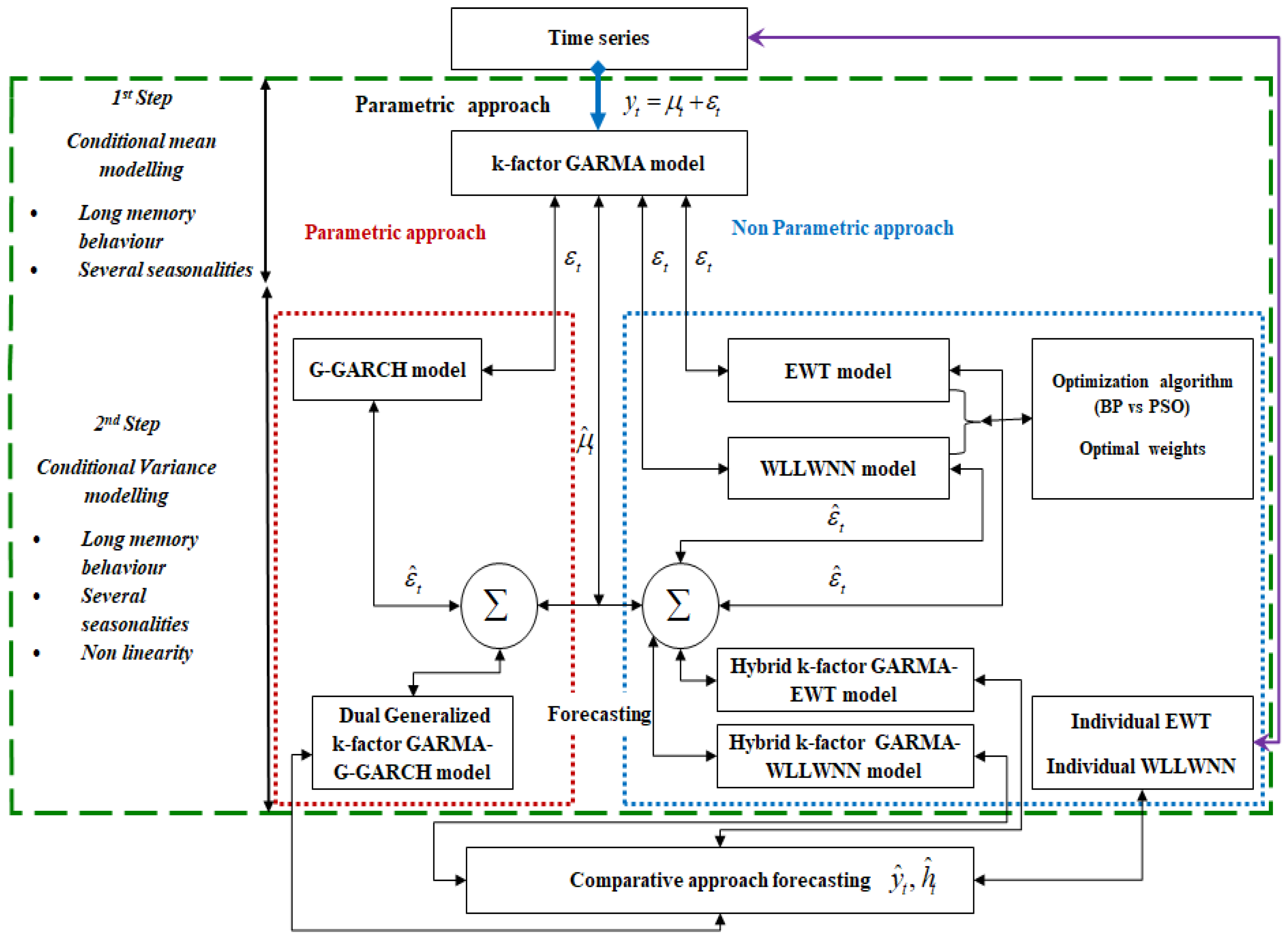

3. Econometric Methodology

3.1. The k-Factor GARMA Model

3.2. The Wavelet Local Linear Wavelet Neural Network

3.2.1. Theoretical Concepts of Wavelet

3.2.2. Empirical Wavelet Transforms

3.2.3. The Local Linear Wavelet Neural Network

3.3. The Hybrid k-Factor GARMA-WLLWNN Model

3.4. The k-Factor GARMA-G-GARCH Model

4. Empirical Methodology

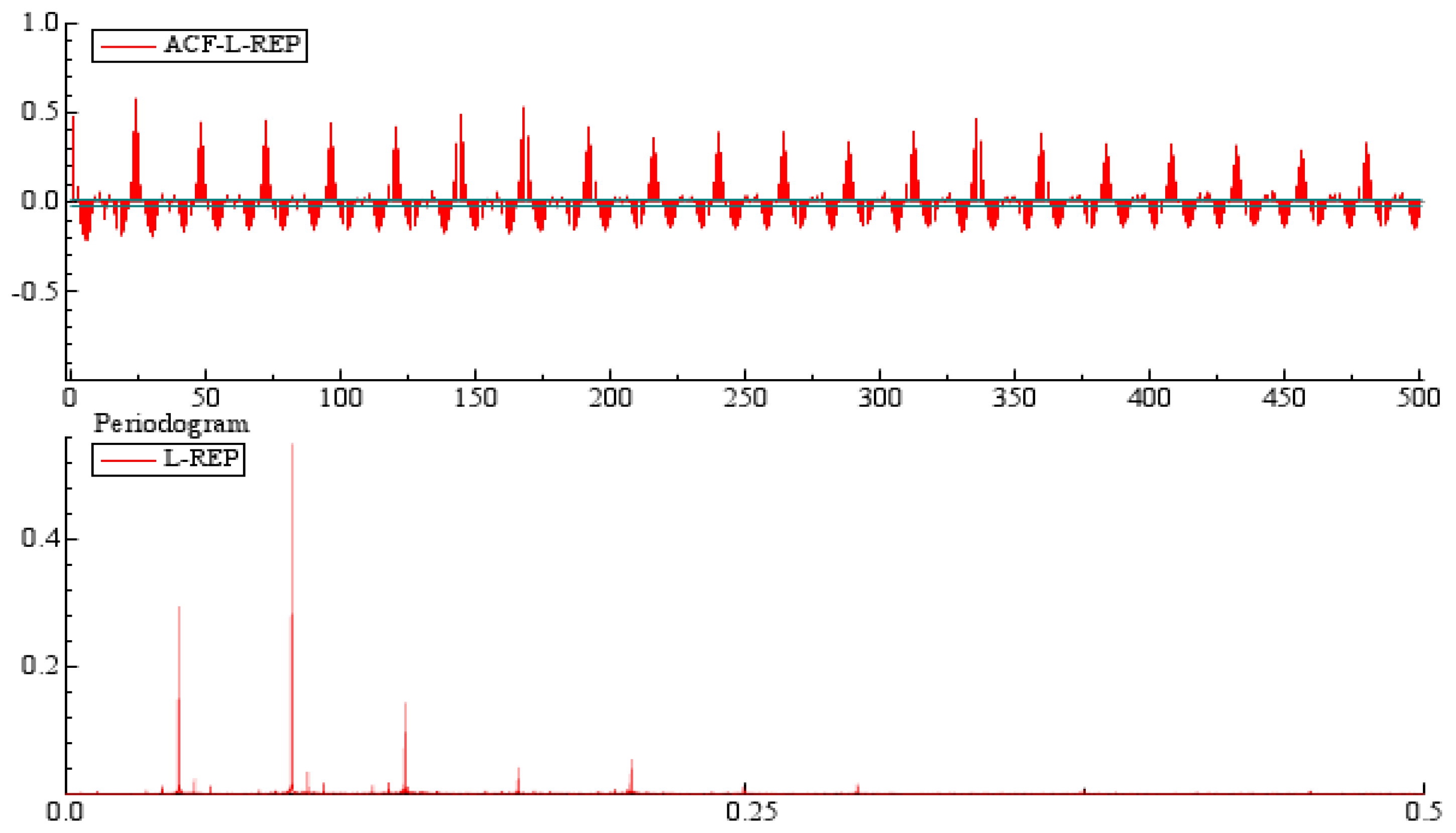

4.1. Data Description and Preliminary Study

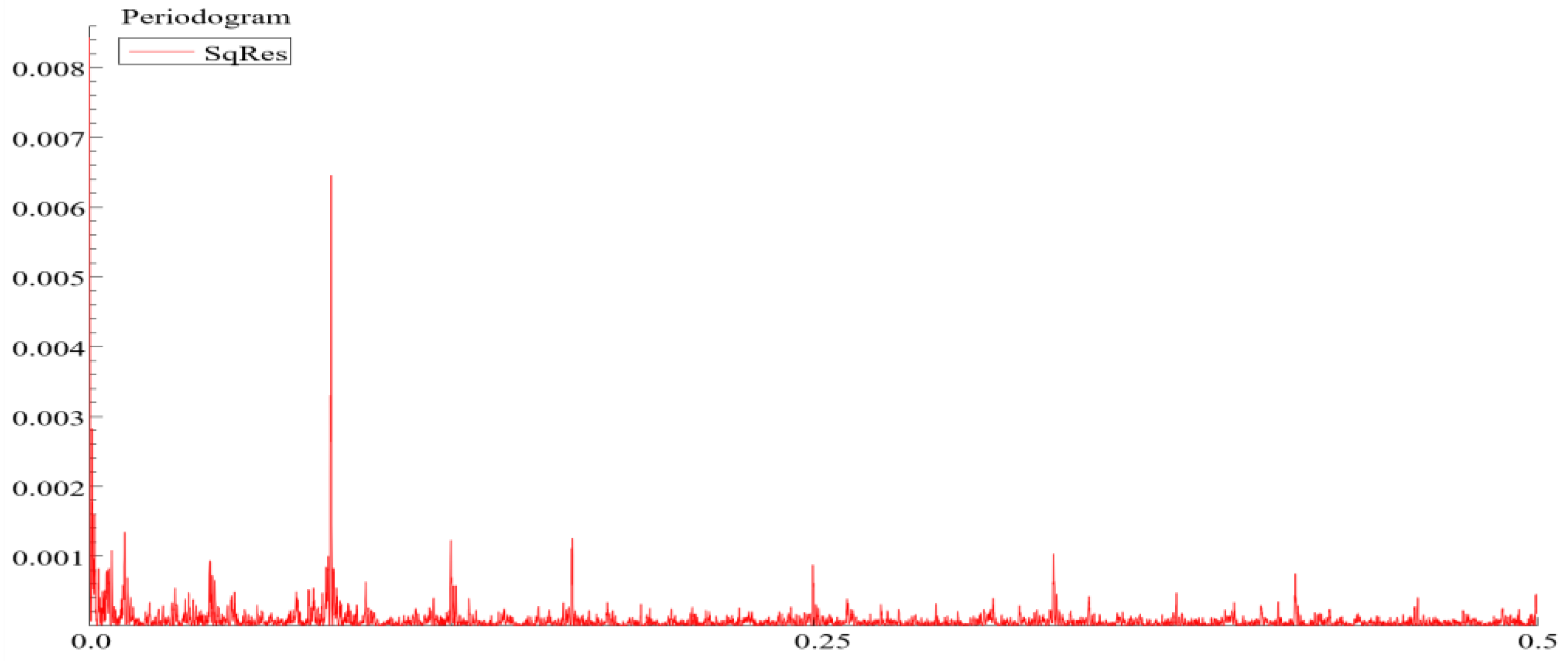

4.2. Estimation Results

4.2.1. The -Factor GARMA Estimation Results

4.2.2. The EWLLWNN Estimation Results

4.2.3. The LLWNN Modeling

4.2.4. The -Factor GARMA-G-GARCH Estimation Results

4.3. Forecasting Results: A Comparative Approach

5. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

| 1 | We refer to Bunn and Karakatsani (2003) and Huisman et al. (2007), among others, for an overview on (hourly specific) day-ahead price characteristics. |

| 2 | To check the stationarity, we apply the unit root tests without and with structural breaks. We find evidence of stationarity. These results are not reported here but are available upon request. |

| 3 |

References

- Abbass, Hussein A., Ruhul Sarker, and Charles Newton. 2001. A Pareto-frontier Differential Evolution Approach for Multi-objective Optimization Problems. IEEE Congress on Evolutionary Computation 2: 971–978. [Google Scholar]

- Aggarwal, S. K., L. M. Saini, and Ashwani Kumar. 2008. Price Forecasting Using Wavelet Transform and LSE Based Mixed Model in Australian Electricity Market. International Journal of Energy Sector Management 2: 521–46. [Google Scholar] [CrossRef]

- Anbazhagan, S., and N. Kumarappan. 2014. Day-Ahead Deregulated Electricity Market Price Forecasting Using Neural Network Input Featured by DCT. Energy Conversion and Management 78: 711–19. [Google Scholar] [CrossRef]

- Armano, Giuliano, Michele Marchesi, and Andrea Murru. 2005. A Hybrid Genetic-Neural Architecture for Stock Indexes Forecasting. Information Sciences 170: 3–33. [Google Scholar] [CrossRef]

- Athanassios, Kintsakis, Antonios Chrysopoulos, and Pericles A. Mitkas. 2015. Agent-based Short-Term Load and Price Forecasting Using a Parallel Implementation of an Adaptive PSO-Trained Local Linear Wavelet Neural Network. Paper presented at International Conference on the European Energy Market, Lisbon, Portugal, May 19–22. [Google Scholar]

- Baillie, Richard T., Bollerslev Tim Mikkelsen, and Hans Ole Mikkelsen. 1996. Fractionally integrated generalized autoregressive conditional heteroskedasticity. Journal of Econometrics 74: 3–30. [Google Scholar] [CrossRef]

- Bashir, Zidan, and M. E. El-Hawary. 2000. Short Term Load Forecasting by Using Wavelet Neural Networks. Paper presented at 2000 Canadian Conference on Electrical and Computer Engineering. Conference, Halifax, NS, Canada, May 7–10; vol. 1, pp. 163–66. [Google Scholar] [CrossRef]

- Ben Amor, Souhir, Heni Boubaker, and Lotfi Belkacem. 2018. Forecasting Electricity Spot Price for Nord Pool Market with a Hybridk-Factor Garma-LLWNN Model. Journal of Forecasting 37: 832–51. [Google Scholar] [CrossRef]

- Benaouda, D., F. Murtagh, J.-L. Starck, and O. Renaud. 2006. Wavelet-Based Nonlinear Multiscale Decomposition Model for Electricity Load Forecasting. Neurocomputing 70: 139–54. [Google Scholar] [CrossRef]

- Beran, Jan. 1994. Statistics for Long Memory Processes. New York: Chapman & Hall. [Google Scholar]

- Bollerslev, Tim. 1986. Generalized autoregressive conditional heteroskedasticity. Journal of Econometrics 31: 307–27. [Google Scholar] [CrossRef]

- Bollerslev, Tim, and Hans Ole Mikkelsen. 1996. Modeling and Pricing Long Memory in Stock Market Volatility. Journal of Econometrics 73: 151–84. [Google Scholar] [CrossRef]

- Bollerslev, Tim, and Robert Hodrick. 1992. Financial Market Efficiency Tests. Cambridge: National Bureau of Economic Research. [Google Scholar] [CrossRef]

- Bordignon, Silvano, Massimiliano Caporin, and Francesco Lisi. 2007. Generalised Long-Memory GARCH Models for Intra-Daily Volatility. Computational Statistics & Data Analysis 51: 5900–12. [Google Scholar] [CrossRef]

- Bordignon, Silvano, Massimiliano Caporin, and Francesco Lisi. 2008. Periodic Long-Memory GARCH Models. Econometric Reviews 28: 60–82. [Google Scholar] [CrossRef]

- Boubaker, Heni, and Mohamed Boutahar. 2011. A Wavelet-Based Approach for Modelling Exchange Rates. Statistical Methods & Applications 20: 201–20. [Google Scholar] [CrossRef]

- Boubaker, Heni, and Nadia Sghaier. 2015. Semiparametric Generalized Long-Memory Modeling of Some MENA Stock Market Returns: A Wavelet Approach. Economic Modelling 50: 254–65. [Google Scholar] [CrossRef]

- Boubaker, Heni, Souhir Ben Amor, and Hichem Rezgui. 2020. A New Hybrid Wavelet-Neural Network Approach for Forecasting Electricity. Energy Studies Review 24. [Google Scholar] [CrossRef]

- Boubaker, Heni. 2015. Wavelet Estimation of Gegenbauer Processes: Simulation and Empirical Application. Computational Economics 46: 551–74. [Google Scholar] [CrossRef]

- Boubaker, Heni. 2016. A Comparative Study of the Performance of Estimating Long-Memory Parameter Using Wavelet-Based Entropies. Computational Economics 48: 693–731. [Google Scholar] [CrossRef]

- Bunn, Derek W., and Nektaria Karakatsani. 2003. Modeling and Forecasting Electricity Prices. London: London Business School. [Google Scholar]

- Burton, Bruce, and Ronald G. Harley. 1994. Reducing the computational demands of continually online trained artificial neural networks for system identification and control of fast processes. Paper presented at 1994 IEEE Industry Applications Society Annual Meeting, Denver, CO, USA, October 2–5; vol. 2, pp. 1836–43. [Google Scholar]

- Cao, Liangyue, Yiguang Hong, Haiping Fang, and Guowei He. 1995. Predicting Chaotic Time Series with Wavelet Networks. Physica D: Nonlinear Phenomena 85: 225–38. [Google Scholar] [CrossRef]

- Caporale, Guglielmo Maria, and Luis Gil-Alana. 2014. Long-Run and Cyclical Dynamics in the US Stock Market. Journal of Forecasting 33: 147–61. [Google Scholar] [CrossRef]

- Caporin, Massimiliano, and Francesco Lisi. 2010. MISSPECIFICATION Tests for Periodic Long Memory GARCH Models. Statistical Methods and Applications 19: 47–62. [Google Scholar] [CrossRef]

- Chakravarty, S., Maya Nayak, and R. Bisoi. 2012. Particle Swarm Optimization Based Local Linear Wavelet Neural Network for Forecasting Electricity Prices. Presented at 2012 International Conference on Energy, Automation and Signal, Bhubaneswar, India, December 28–30. [Google Scholar] [CrossRef]

- Chen, Yuehui, Jiwei Dong, Bo Yang, and Yong Zhang. 2004. A local linear wavelet neural network. Paper presented at Fifth World Congress on Intelligent Control and Automation (IEEE Cat. No. 04EX788), Hangzhou, China, June 15–19; vol. 3, pp. 1954–57. [Google Scholar]

- Cheng, Hangyang, Xiangwu Ding, Wuneng Zhou, and Renqiang Ding. 2019. A Hybrid Electricity Price Forecasting Model with Bayesian Optimization for German Energy Exchange. International Journal of Electrical Power & Energy Systems 110: 653–66. [Google Scholar] [CrossRef]

- Cheung, Yin-Wong. 1993. Long Memory in Foreign-Exchange Rates. Journal of Business & Economic Statistics 11: 93–101. [Google Scholar] [CrossRef]

- Contreras, Javier, Rosario Espinola, Fransicico J. Nogales, and Antonio J. Conejo. 2003. Arima Models to Predict next-Day Electricity Prices. IEEE Transactions on Power Systems 18: 1014–20. [Google Scholar] [CrossRef]

- Cristea, Paul, Rodica Tuduce, and Alexandra Cristea. 2000. Time Series Prediction with Wavelet Neural Networks. Paper presented at 5th Seminar on Neural Network Applications in Electrical Engineering, NEUREL 2000 (IEEE Cat. No.00EX287), Belgrade, Yugoslavia, September 27. [Google Scholar]

- Daubechies, Ingrid. 1992. Ten Lectures on Wavelets. Philadelphia: Society for Industrial and Applied Mathematics. [Google Scholar] [CrossRef]

- Diebold, Francis X. 2015. Comparing Predictive Accuracy, Twenty Years Later: A Personal Perspective on the Use and Abuse of Diebold-Mariano Tests. Journal of Business and Economic Statistics 33: 1–9. [Google Scholar] [CrossRef]

- Diebold, Francis X., and Roberto S. Mariano. 1995. Comparing Predictive Accuracy. Journal of Business & Economic Statistics 13: 253–63. [Google Scholar] [CrossRef]

- Diongue, Abdou Kâ, Dominique Guégan, and Bertrand Vignal. 2009. Forecasting Electricity Spot Market Prices with a K-Factor GIGARCH Process. Applied Energy 86: 505–10. [Google Scholar] [CrossRef]

- Dragomiretskiy, Konstantin, and Dominique Zosso. 2014. Variational Mode Decomposition. IEEE Transactions on Signal Processing 62: 531–44. [Google Scholar] [CrossRef]

- Engle, Robert F. 1982. Autoregressive Conditional Heteroscedasticity with Estimates of the Variance of United Kingdom Inflation. Econometrica 50: 987. [Google Scholar] [CrossRef]

- Escribano, Alvaro, J. Ignacio Peña, and Pablo Villaplana. 2011. Modelling Electricity Prices: International Evidence*. Oxford Bulletin of Economics and Statistics 73: 622–50. [Google Scholar] [CrossRef]

- Gao, Rong, and Lefteri H. Tsoukalas. 2001. Neural-Wavelet Methodology for Load Forecasting. Journal of Intelligent and Robotic Systems 31: 149–57. [Google Scholar] [CrossRef]

- Garcia, Reinaldo C., Javier Contreras, Macro van Akkeren, and João Batista C. Garcia. 2005. A GARCH Forecasting Model to Predict Day-Ahead Electricity Prices. IEEE Transactions on Power Systems 20: 867–74. [Google Scholar] [CrossRef]

- Gençay, Ramazan, Faruk Selçuk, and Brandon Whitcher. 2002. An Introduction to Wavelets and Other Filtering Methods in Finance and Economics. Waltham. Cambridge: Academic Press, pp. 1–14. [Google Scholar] [CrossRef]

- Geweke, John, and Susan Porter-Hudak. 1983. The Estimation and Application of Long Memory Time Series Models. Journal of Time Series Analysis 4: 221–38. [Google Scholar] [CrossRef]

- Ghosh, Sajal, and Kakali Kanjilal. 2014. Modelling and Forecasting of Day-Ahead Electricity Price in Indian Energy Exchange—Evidence from MSARIMA-EGARCH Model. International Journal of Indian Culture and Business Management 8: 413. [Google Scholar] [CrossRef]

- Gilles, Jerome. 2013. Empirical Wavelet Transform. IEEE Transactions on Signal Processing 61: 3999–4010. [Google Scholar] [CrossRef]

- Girish, Godekere P. 2016. Spot Electricity Price Forecasting in Indian Electricity Market Using Autoregressive-GARCH Models. Energy Strategy Reviews 11–12: 52–57. [Google Scholar] [CrossRef]

- Granger, Clive W. 1989. Invited Review Combining Forecasts—Twenty Years Later. Journal of Forecasting 8: 167–73. [Google Scholar] [CrossRef]

- Granger, Clive W., and Roselyne Joyeux. 1980. An Introduction to Long-Memory Time Series Models and Fractional Differencing. Journal of Time Series Analysis 1: 15–29. [Google Scholar] [CrossRef]

- Gray, Henry L., Nien-Fan Zhang, and Wayne A. Woodward. 1989. On Generalized Fractional Processes. Journal of Time Series Analysis 10: 233–57. [Google Scholar] [CrossRef]

- Grossi, Luigi, and Fany Nan. 2019. Robust Forecasting of Electricity Prices: Simulations, Models and the Impact of Renewable Sources. Technological Forecasting and Social Change 141: 305–18. [Google Scholar] [CrossRef]

- Hansen, Peter Reinhard, Asger Lunde, and James M. Nason. 2003. Choosing the best volatility models: The model confidence set approach. Oxford Bulletin of Economics and Statistics 65: 839–61. [Google Scholar] [CrossRef]

- Hosking, J. R. 1981. Fractional Differencing. Biometrika 68: 165–76. [Google Scholar] [CrossRef]

- Huang, Norden E., Zheng Shen, Steven R. Long, Manli C. Wu, Hsing H. Shih, Quanan Zheng, Nai-Chyuan Yen, Chi Chao Tung, and Henry H. Liu. 1998. The Empirical Mode Decomposition and the Hilbert Spectrum for Nonlinear and Non-Stationary Time Series Analysis. Proceedings of the Royal Society of London. Series A: Mathematical, Physical and Engineering Sciences 454: 903–95. [Google Scholar] [CrossRef]

- Huisman, Ronald, Christian Huurman, and Ronald Mahieu. 2007. Hourly Electricity Prices in Day-Ahead Markets. Energy Economics 29: 240–48. [Google Scholar] [CrossRef]

- Jabeur, Sami Ben, Salma Mefteh-Wali, and Jean-Laurent Viviani. 2021. Forecasting Gold Price with the XGBOOST Algorithm and Shap Interaction Values. Annals of Operations Research. [Google Scholar] [CrossRef]

- Jiang, Manrui, Lifen Jia, Zhensong Chen, and Wei Chen. 2020. The Two-Stage Machine Learning Ensemble Models for Stock Price Prediction by Combining Mode Decomposition, Extreme Learning Machine and Improved Harmony Search Algorithm. Annals of Operations Research 309: 553–85. [Google Scholar] [CrossRef]

- Jiang, Ping, Feng Liu, and Yiliao Song. 2017. A Hybrid Forecasting Model Based on Date-Framework Strategy and Improved Feature Selection Technology for Short-Term Load Forecasting. Energy 119: 694–709. [Google Scholar] [CrossRef]

- Kennedy, James, and Russell Eberhart. 1995. Particle Swarm Optimization. Paper presented at Proceedings of ICNN’95—International Conference on Neural Networks, Perth, WA, Australia, November 27–December 1. [Google Scholar]

- Khashei, Mehdi, and Mehdi Bijari. 2010. An Artificial Neural Network (p,D,Q) Model for Timeseries Forecasting. Expert Systems with Applications 37: 479–89. [Google Scholar] [CrossRef]

- Knittel, Christopher R., and Michael R. Roberts. 2005. An Empirical Examination of Restructured Electricity Prices. Energy Economics 27: 791–817. [Google Scholar] [CrossRef]

- Koopman, Siem Jan, Marius Ooms, and M. Angeles Carnero. 2007. Periodic Seasonal Reg-Arfima–GARCH Models for Daily Electricity Spot Prices. Journal of the American Statistical Association 102: 16–27. [Google Scholar] [CrossRef]

- Liu, Heping, and Jing Shi. 2013. Applying Arma–GARCH Approaches to Forecasting Short-Term Electricity Prices. Energy Economics 37: 152–66. [Google Scholar] [CrossRef]

- Mallat, Stéphane. 1999. A Wavelet Tour of Signal Processing. New York: Academic Press. [Google Scholar]

- Mallat, Stéphane G., and Zhifeng Zhang. 1993. Matching Pursuits with Time-Frequency Dictionaries. IEEE Transactions on Signal Processing 41: 3397–3415. [Google Scholar] [CrossRef]

- Nicolaisen, James D., C. W. Richter, and Gerald B. Sheble. 2000. Price Signal Analysis for Competitive Electric Generation Companies. Paper presented at DRPT2000. International Conference on Electric Utility Deregulation and Restructuring and Power Technologies. Proceedings (Cat. No.00EX382), London, UK, April 4–7. [Google Scholar]

- Panapakidis, Ioannis P., and Athanasios S. Dagoumas. 2016. Day-ahead electricity price forecasting via the application of artificial neural network based models. Applied Energy 172: 132–51. [Google Scholar] [CrossRef]

- Pany, Prasanta Kumar. 2011. Short-Term Load Forecasting Using PSO Based Local Linear Wavelet Neural Network. International Journal of Instrumentation Control and Automation 1: 163–68. [Google Scholar] [CrossRef]

- Percival, Donald B., and Andrew T. Walden. 2000. Wavelet Methods for Time Seriesanalysis. Cambridge: Cambridge University Press. [Google Scholar] [CrossRef]

- Rana, Mashud, and Irena Koprinska. 2016. Forecasting Electricity Load with Advanced Wavelet Neural Networks. Neurocomputing 182: 118–32. [Google Scholar] [CrossRef]

- Robinson, P. M. 1995. Log-Periodogram Regression of Time Series with Long Range Dependence. The Annals of Statistics 23. [Google Scholar] [CrossRef]

- Shafie-khah, M., M. Parsa Moghaddam, and M.K. Sheikh-El-Eslami. 2011. Price Forecasting of Day-Ahead Electricity Markets Using a Hybrid Forecast Method. Energy Conversion and Management 52: 2165–69. [Google Scholar] [CrossRef]

- Sharkey, Amanda J. 2002. Types of Multinet System. In Multiple Classifier System. Berlin/Heidelberg: Springer, pp. 108–17. [Google Scholar] [CrossRef]

- Soares, Lacir Jorge, and Leonardo Rocha Souza. 2006. Forecasting Electricity Demand Using Generalized Long Memory. International Journal of Forecasting 22: 17–28. [Google Scholar] [CrossRef]

- Szkuta, Boguslaw R., L. Augusto Sanabria, and Tharam S. Dillon. 1999. Electricity Price Short-Term Forecasting Using Artificial Neural Networks. IEEE Transactions on Power Systems 14: 851–57. [Google Scholar] [CrossRef]

- Tan, Zhongfu, Jinliang Zhang, Jianhui Wang, and Jun Xu. 2010. Day-Ahead Electricity Price Forecasting Using Wavelet Transform Combined with Arima and GARCH Models. Applied Energy 87: 3606–10. [Google Scholar] [CrossRef]

- Tseng, Fang-Mei, Hsiao-Cheng Yu, and Gwo-Hsiung Tzeng. 2002. Combining Neural Network Model with Seasonal Time Series Arima Model. Technological Forecasting and Social Change 69: 71–87. [Google Scholar] [CrossRef]

- Valenzuela, Olga, I. Rojas, F. Rojas, H. Pomares, L. J. Herrera, A. Guillen, L. Marquez, and M. Pasadas. 2008. Hybridization of Intelligent Techniques and ARIMA Models for Time Series Prediction. Fuzzy Sets and Systems 159: 821–45. [Google Scholar] [CrossRef]

- Wang, A. J., and B. Ramsay. 1998. A Neural Network Based Estimator for Electricity Spot-Pricing with Particular Reference to Weekend and Public Holidays. Neurocomputing 23: 47–57. [Google Scholar] [CrossRef]

- Weron, Rafał, Ingve Simonsen, and Piotr Wilman. 2004. Modeling Highly Volatile and Seasonal Markets: Evidence from the Nord Pool Electricity Market. In The Application of Econophysics. Tokyo: Springer, pp. 182–91. [Google Scholar] [CrossRef]

- Whitcher, Brandon. 2004. Wavelet-Based Estimation for Seasonal Long-Memory Processes. Technometrics 46: 225–38. [Google Scholar] [CrossRef]

- Woodward, Wayne A., Qin C. Cheng, and Henry L. Gray. 1998. A K-Factor Garma Long-Memory Model. Journal of Time Series Analysis 19: 485–504. [Google Scholar] [CrossRef]

- Wu, Zhaohua, and Norden E. Huang. 2009. Ensemble Empirical Mode Decomposition: A Noise-Assisted Data Analysis Method. Advances in Adaptive Data Analysis 1: 1–41. [Google Scholar] [CrossRef]

- Yao, S. J., Y. H. Song, L. Z. Zhang, and X. Y. Cheng. 2000. Wavelet Transform and Neural Networks for Short-Term Electrical Load Forecasting. Energy Conversion and Management 41: 1975–88. [Google Scholar] [CrossRef]

- Yu, Lean, Shouyang Wang, and Kin Keung Lai. 2005. A Novel Nonlinear Ensemble Forecasting Model Incorporating GLAR and Ann for Foreign Exchange Rates. Computers & Operations Research 32: 2523–41. [Google Scholar] [CrossRef]

- Zhang, G. Peter. 2003. Time Series Forecasting Using a Hybrid Arima and Neural Network Model. Neurocomputing 50: 159–75. [Google Scholar] [CrossRef]

- Zhang, Jinliang, Yi-Ming Wei, Dezhi Li, Zhongfu Tan, and Jianhua Zhou. 2018. Short Term Electricity Load Forecasting Using a Hybrid Model. Energy 158: 774–81. [Google Scholar] [CrossRef]

- Zhang, Qinghua, and Albert Benveniste. 1992. Wavelet Networks. IEEE Transactions on Neural Networks 3: 889–98. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| The Log-Returns Electricity Price | |

|---|---|

| Mean | |

| Standard Deviation | 0.1079 |

| Skewness | −0.2634 |

| Excess Kurtosis | 37.2358 |

| Jarque–Bera | 2.9826 × 105 *** |

| L-REP | Bandwidth | GPH | LW | ||||

| Standard error | p-value | Standard error | p-value | ||||

| = 169 | −0.51683 | 0.0558 | 0.0000 | −0.5588 | 0.0403 | 0.0000 | |

| = 397 | −0.61336 | 0.0372 | 0.0000 | −0.5775 | 0.0269 | 0.0000 | |

| = 934 | −0.4786 | 0.0253 | 0.0000 | −0.5892 | 0.0178 | 0.0000 | |

| Parameters | -Factor GARMA Model Estimation |

|---|---|

| 0.5132 *** | |

| - | |

| - | |

| 0.1687 *** | |

| 0.2349 *** | |

| 0.4137 *** | |

| 0.0417 *** | |

| 0.0834 *** | |

| 0.1262 *** |

| L-REP | Bandwidth | GPH | LW | ||||

| Standard error | p-value | Standard error | p-value | ||||

| = 169 | 0.5275 | 0.0523 | 0.0000 | 0.4982 | 0.0381 | 0.0000 | |

| = 397 | 0.3678 | 0.0329 | 0.0000 | 0.3874 | 0.0246 | 0.0000 | |

| = 934 | 0.2379 | 0.0218 | 0.0000 | 0.2453 | 0.0249 | 0.0000 | |

| -Factor GARMA Model Estimation | The G-GARCH Model Estimation | ||

|---|---|---|---|

| 0.6327 *** | 0.7156 *** | ||

| - | 0.5139 *** | ||

| - | - | ||

| 0.1698 *** | 0.1497 *** | ||

| 0.2568 *** | 0.2678 *** | ||

| 0.3978 *** | 0.4319 *** | ||

| 0.0405 *** | 0.0411 *** | ||

| 0.0838 *** | 0.0854 *** | ||

| 0.1289 *** | 0.1197 *** | ||

| Models | Criterion | ||||

| WLLWNN-based BP algorithm | |||||

| 1.1545 | 1.2874 | 1.3786 | |||

| EWLLWNN-based BP algorithm | |||||

| 1.2334 | 1.2982 | 1.4684 | |||

| WLLWNN-based PSO algorithm | |||||

| 1.3566 | 1.5562 | 1.6414 | |||

| EWLLWNN-based PSO algorithm | |||||

| 1.3751 | 1.5875 | 1.7486 | |||

| The hybrid -factor GARMA-WLLWNN-based BP algorithm | |||||

| 1.9874 ** | 2.3536 ** | 2.7861 *** | |||

| The hybrid -factor GARMA-EWLLWNN-based BP algorithm | |||||

| 2.0143 ** | 2.5462 ** | 2.8871 *** | |||

| The hybrid -factor GARMA-WLLWNN-based PSO algorithm | |||||

| 2.6716 *** | 2.9873 *** | 3.5728 *** | |||

| The hybrid -factor GARMA-EWLLWNN-based PSO algorithm | |||||

| 2.7861 *** | 3.0837 *** | 3.7981 *** | |||

| The -factor GARMA-G-GARCH model | |||||

| Models | Criterion | ||||

| WLLWNN-based BP algorithm | |||||

| 1.4932 | 1.6133 | ||||

| EWLLWNN-based BP algorithm | |||||

| 1.5623 | 1.7593 | ||||

| WLLWNN-based PSO algorithm | |||||

| 1.9645 ** | 2.2514 ** | ||||

| EWLLWNN-based PSO algorithm | |||||

| 20342 ** | 2.3436 ** | ||||

| The hybrid -factor GARMA-WLLWNN-based BP algorithm | |||||

| 2.9784 *** | 3.4836 *** | ||||

| The hybrid -factor GARMA-EWLLWNN-based BP algorithm | |||||

| 3.1426 *** | 3.7625 *** | ||||

| The hybrid -factor GARMA-WLLWNN-based PSO algorithm | |||||

| 3.7633 *** | 3.8921 *** | ||||

| The hybrid -factor GARMA-EWLLWNN-based PSO algorithm | |||||

| 3.9562 *** | 4.1201 *** | ||||

| The -factor GARMA-G-GARCH model | |||||

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Boubaker, H.; Bannour, N. Coupling the Empirical Wavelet and the Neural Network Methods in Order to Forecast Electricity Price. J. Risk Financial Manag. 2023, 16, 246. https://doi.org/10.3390/jrfm16040246

Boubaker H, Bannour N. Coupling the Empirical Wavelet and the Neural Network Methods in Order to Forecast Electricity Price. Journal of Risk and Financial Management. 2023; 16(4):246. https://doi.org/10.3390/jrfm16040246

Chicago/Turabian StyleBoubaker, Heni, and Nawres Bannour. 2023. "Coupling the Empirical Wavelet and the Neural Network Methods in Order to Forecast Electricity Price" Journal of Risk and Financial Management 16, no. 4: 246. https://doi.org/10.3390/jrfm16040246