Are Bitcoin and Gold a Safe Haven during COVID-19 and the 2022 Russia–Ukraine War?

Abstract

:1. Introduction

2. Literature Review

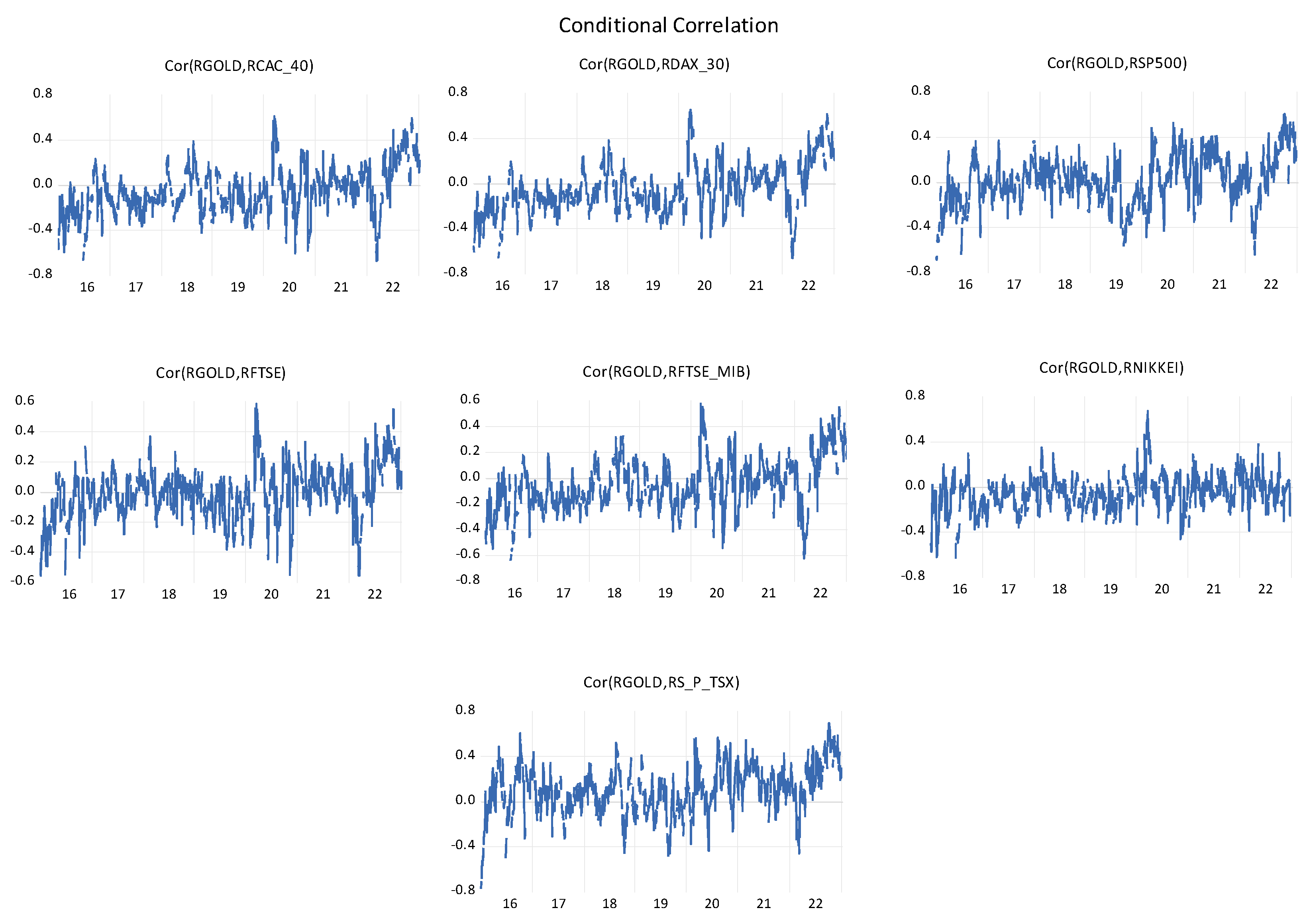

3. Methodology

3.1. Diagonal VECH-GARCH (DVECH-GARCH) Model

3.2. Hedge Ratio

3.3. Hedging Effectiveness (HE)

4. Data and Results

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

| Covariance specification: Diagonal VECH | ||||

| GARCH = C + A1 × RESID(−1) × RESID(−1)’ + B1 × GARCH(−1) | ||||

| Transformed Variance Coefficients | ||||

| Coefficient | Std. Error | z-Statistic | Prob. | |

| C(1,1) | 0.0002 | 1.64 × 10−5 | 9.3843 | 0.0000 |

| C(1,2) | 1.13 × 10−5 | 5.67 × 10−6 | 2.0025 | 0.0452 |

| C(1,3) | 1.06 × 10−5 | 5.07 × 10−6 | 2.0916 | 0.0365 |

| C(1,4) | 3.72 × 10−6 | 1.58 × 10−6 | 2.3625 | 0.0182 |

| C(1,5) | 8.38 × 10−6 | 5.43 × 10−6 | 1.5435 | 0.1227 |

| C(1,6) | 8.42 × 10−6 | 4.34 × 10−6 | 1.9405 | 0.0523 |

| C(1,7) | 6.16 × 10−6 | 1.44 × 10−5 | 0.4264 | 0.6698 |

| C(1,8) | 6.37 × 10−6 | 2.33 × 10−6 | 2.7311 | 0.0063 |

| C(2,2) | 9.75 × 10−6 | 5.68 × 10−7 | 17.1547 | 0.0000 |

| C(2,3) | 9.24 × 10−6 | 3.19 × 10−7 | 28.9931 | 0.0000 |

| C(2,4) | 5.35 × 10−6 | 5.71 × 10−7 | 9.3740 | 0.0000 |

| C(2,5) | 6.92 × 10−6 | 4.78 × 10−7 | 14.4862 | 0.0000 |

| C(2,6) | 9.90 × 10−6 | 6.95 × 10−7 | 14.2314 | 0.0000 |

| C(2,7) | 4.53 × 10−6 | 1.32 × 10−6 | 3.4413 | 0.0006 |

| C(2,8) | 4.29 × 10−6 | 5.08 × 10−7 | 8.4418 | 0.0000 |

| C(3,3) | 1.03 × 10−5 | 1.50 × 10−7 | 68.7691 | 0.0000 |

| C(3,4) | 5.44 × 10−6 | 5.82 × 10−7 | 9.3524 | 0.0000 |

| C(3,5) | 6.24 × 10−6 | 4.26 × 10−7 | 14.6616 | 0.0000 |

| C(3,6) | 9.94 × 10−6 | 5.61 × 10−7 | 17.7344 | 0.0000 |

| C(3,7) | 4.30 × 10−6 | 1.28 × 10−6 | 3.3532 | 0.0008 |

| C(3,8) | 4.14 × 10−6 | 5.06 × 10−7 | 8.1952 | 0.0000 |

| C(4,4) | 5.30 × 10−6 | 5.51 × 10−7 | 9.6172 | 0.0000 |

| C(4,5) | 4.05 × 10−6 | 5.15 × 10−7 | 7.8739 | 0.0000 |

| C(4,6) | 6.08 × 10−6 | 7.81 × 10−7 | 7.7828 | 0.0000 |

| C(4,7) | 2.44 × 10−6 | 1.03 × 10−6 | 2.3765 | 0.0175 |

| C(4,8) | 3.09 × 10−6 | 3.56 × 10−7 | 8.6831 | 0.0000 |

| C(5,5) | 7.60 × 10−6 | 7.52 × 10−7 | 10.1075 | 0.0000 |

| C(5,6) | 6.47 × 10−6 | 5.86 × 10−7 | 11.0431 | 0.0000 |

| C(5,7) | 3.76 × 10−6 | 1.31 × 10−6 | 2.8668 | 0.0041 |

| C(5,8) | 3.26 × 10−6 | 4.28 × 10−7 | 7.6276 | 0.0000 |

| C(6,6) | 1.33 × 10−5 | 1.19 × 10−6 | 11.1172 | 0.0000 |

| C(6,7) | 4.33 × 10−6 | 1.37 × 10−6 | 3.1525 | 0.0016 |

| C(6,8) | 4.84 × 10−6 | 6.60 × 10−7 | 7.3334 | 0.0000 |

| C(7,7) | 1.30 × 10−5 | 1.83 × 10−6 | 7.0877 | 0.0000 |

| C(7,8) | 2.86 × 10−6 | 1.16 × 10−6 | 2.4695 | 0.0135 |

| C(8,8) | 3.58 × 10−6 | 4.90 × 10−7 | 7.3086 | 0.0000 |

| A1(1,1) | 0.1673 | 0.0177 | 9.4333 | 0.0000 |

| A1(1,2) | 0.0768 | 0.0216 | 3.5642 | 0.0004 |

| A1(1,3) | 0.0651 | 0.0213 | 3.0608 | 0.0022 |

| A1(1,4) | 0.0783 | 0.0194 | 4.0459 | 0.0001 |

| A1(1,5) | 0.0514 | 0.0236 | 2.1793 | 0.0293 |

| A1(1,6) | 0.0530 | 0.0221 | 2.3965 | 0.0166 |

| A1(1,7) | 0.0198 | 0.0518 | 0.3830 | 0.7017 |

| A1(1,8) | 0.0730 | 0.0221 | 3.3000 | 0.0010 |

| A1(2,2) | 0.1816 | 0.0122 | 14.8709 | 0.0000 |

| A1(2,3) | 0.1580 | 0.0104 | 15.1995 | 0.0000 |

| A1(2,4) | 0.1712 | 0.0135 | 12.6501 | 0.0000 |

| A1(2,5) | 0.1635 | 0.0116 | 14.1222 | 0.0000 |

| A1(2,6) | 0.1625 | 0.0111 | 14.6545 | 0.0000 |

| A1(2,7) | 0.0893 | 0.0216 | 4.1275 | 0.0000 |

| A1(2,8) | 0.1699 | 0.0136 | 12.5238 | 0.0000 |

| A1(3,3) | 0.1411 | 0.0106 | 13.3482 | 0.0000 |

| A1(3,4) | 0.1497 | 0.0126 | 11.8470 | 0.0000 |

| A1(3,5) | 0.1344 | 0.0103 | 13.0799 | 0.0000 |

| A1(3,6) | 0.1463 | 0.0104 | 14.0216 | 0.0000 |

| A1(3,7) | 0.0852 | 0.0204 | 4.1879 | 0.0000 |

| A1(3,8) | 0.1484 | 0.0126 | 11.7470 | 0.0000 |

| A1(4,4) | 0.2472 | 0.0215 | 11.4902 | 0.0000 |

| A1(4,5) | 0.1477 | 0.0141 | 10.4550 | 0.0000 |

| A1(4,6) | 0.1572 | 0.0147 | 10.6687 | 0.0000 |

| A1(4,7) | 0.0805 | 0.0277 | 2.9061 | 0.0037 |

| A1(4,8) | 0.2182 | 0.0186 | 11.7094 | 0.0000 |

| A1(5,5) | 0.1594 | 0.0144 | 11.0501 | 0.0000 |

| A1(5,6) | 0.1379 | 0.0113 | 12.2322 | 0.0000 |

| A1(5,7) | 0.0789 | 0.0241 | 3.2788 | 0.0010 |

| A1(5,8) | 0.1600 | 0.0145 | 11.0421 | 0.0000 |

| A1(6,6) | 0.1635 | 0.0122 | 13.4494 | 0.0000 |

| A1(6,7) | 0.0892 | 0.0212 | 4.2090 | 0.0000 |

| A1(6,8) | 0.1525 | 0.0133 | 11.4414 | 0.0000 |

| A1(7,7) | 0.2519 | 0.0274 | 9.1856 | 0.0000 |

| A1(7,8) | 0.0851 | 0.0275 | 3.0969 | 0.0020 |

| A1(8,8) | 0.2299 | 0.0214 | 10.7601 | 0.0000 |

| B1(1,1) | 0.7888 | 0.0169 | 46.6692 | 0.0000 |

| B1(1,2) | 0.6066 | 0.1231 | 4.9297 | 0.0000 |

| B1(1,3) | 0.6888 | 0.1034 | 6.6610 | 0.0000 |

| B1(1,4) | 0.8452 | 0.0345 | 24.5295 | 0.0000 |

| B1(1,5) | 0.6579 | 0.1817 | 3.6203 | 0.0003 |

| B1(1,6) | 0.7684 | 0.0849 | 9.0545 | 0.0000 |

| B1(1,7) | 0.3689 | 1.3507 | 0.2731 | 0.7848 |

| B1(1,8) | 0.7841 | 0.0584 | 13.4368 | 0.0000 |

| B1(2,2) | 0.7858 | 0.0093 | 84.7881 | 0.0000 |

| B1(2,3) | 0.7968 | 0.0073 | 108.6502 | 0.0000 |

| B1(2,4) | 0.7593 | 0.0166 | 45.7590 | 0.0000 |

| B1(2,5) | 0.7855 | 0.0104 | 75.2647 | 0.0000 |

| B1(2,6) | 0.7936 | 0.0096 | 82.9526 | 0.0000 |

| B1(2,7) | 0.6811 | 0.0742 | 9.1751 | 0.0000 |

| B1(2,8) | 0.7618 | 0.0172 | 44.3395 | 0.0000 |

| B1(3,3) | 0.8073 | 0.0074 | 109.0195 | 0.0000 |

| B1(3,4) | 0.7747 | 0.0163 | 47.4583 | 0.0000 |

| B1(3,5) | 0.8082 | 0.0097 | 83.4686 | 0.0000 |

| B1(3,6) | 0.8017 | 0.0083 | 96.2105 | 0.0000 |

| B1(3,7) | 0.6944 | 0.0692 | 10.0282 | 0.0000 |

| B1(3,8) | 0.7766 | 0.0175 | 44.4442 | 0.0000 |

| B1(4,4) | 0.7502 | 0.0167 | 44.9456 | 0.0000 |

| B1(4,5) | 0.7639 | 0.0201 | 37.9954 | 0.0000 |

| B1(4,6) | 0.7613 | 0.0213 | 35.8015 | 0.0000 |

| B1(4,7) | 0.6765 | 0.1000 | 6.7675 | 0.0000 |

| B1(4,8) | 0.7580 | 0.0164 | 46.0973 | 0.0000 |

| B1(5,5) | 0.7841 | 0.0149 | 52.4669 | 0.0000 |

| B1(5,6) | 0.8057 | 0.0117 | 68.7610 | 0.0000 |

| B1(5,7) | 0.6727 | 0.0920 | 7.3081 | 0.0000 |

| B1(5,8) | 0.7667 | 0.0180 | 42.5071 | 0.0000 |

| B1(6,6) | 0.7925 | 0.0107 | 73.8906 | 0.0000 |

| B1(6,7) | 0.7138 | 0.0655 | 10.8950 | 0.0000 |

| B1(6,8) | 0.7690 | 0.0196 | 39.2040 | 0.0000 |

| B1(7,7) | 0.6650 | 0.0303 | 21.9254 | 0.0000 |

| B1(7,8) | 0.5979 | 0.1309 | 4.5694 | 0.0000 |

| B1(8,8) | 0.7535 | 0.0187 | 40.3032 | 0.0000 |

| Covariance specification: Diagonal VECH | ||||

| GARCH = C + A1 × RESID(−1) × RESID(−1)’ + B1 × GARCH(−1) | ||||

| Transformed Variance Coefficients | ||||

| Coefficient | Std. Error | z-Statistic | Prob. | |

| C(1,1) | 1.42 × 10−6 | 3.26 × 10−7 | 4.3426 | 0.0000 |

| C(1,2) | 1.38 × 10−7 | 1.78 × 10−7 | 0.7740 | 0.4389 |

| C(1,3) | 5.77 × 10−8 | 1.64 × 10−7 | 0.3510 | 0.7256 |

| C(1,4) | 1.45 × 10−7 | 1.29 × 10−7 | 1.1239 | 0.2610 |

| C(1,5) | 3.81 × 10−8 | 1.44 × 10−7 | 0.2637 | 0.7920 |

| C(1,6) | 1.50 × 10−7 | 1.96 × 10−7 | 0.7695 | 0.4416 |

| C(1,7) | 1.43 × 10−7 | 1.58 × 10−7 | 0.9044 | 0.3658 |

| C(1,8) | 2.77 × 10−7 | 1.10 × 10−7 | 2.5245 | 0.0116 |

| C(2,2) | 7.17 × 10−6 | 3.19 × 10−7 | 22.4768 | 0.0000 |

| C(2,3) | 6.30 × 10−6 | 3.25 × 10−7 | 19.3919 | 0.0000 |

| C(2,4) | 2.82 × 10−6 | 1.78 × 10−7 | 15.8706 | 0.0000 |

| C(2,5) | 5.00 × 10−6 | 2.37 × 10−7 | 21.1195 | 0.0000 |

| C(2,6) | 7.01 × 10−6 | 3.90 × 10−7 | 17.9937 | 0.0000 |

| C(2,7) | 2.41 × 10−6 | 2.55 × 10−7 | 9.4738 | 0.0000 |

| C(2,8) | 2.60 × 10−6 | 1.59 × 10−7 | 16.3154 | 0.0000 |

| C(3,3) | 6.29 × 10−6 | 3.90 × 10−7 | 16.1159 | 0.0000 |

| C(3,4) | 2.63 × 10−6 | 1.87 × 10−7 | 14.1152 | 0.0000 |

| C(3,5) | 4.46 × 10−6 | 2.58 × 10−7 | 17.3072 | 0.0000 |

| C(3,6) | 6.45 × 10−6 | 4.13 × 10−7 | 15.6071 | 0.0000 |

| C(3,7) | 2.20 × 10−6 | 2.59 × 10−7 | 8.5009 | 0.0000 |

| C(3,8) | 2.37 × 10−6 | 1.62 × 10−7 | 14.6537 | 0.0000 |

| C(4,4) | 3.25 × 10−6 | 2.06 × 10−7 | 15.8234 | 0.0000 |

| C(4,5) | 2.36 × 10−6 | 1.69 × 10−7 | 13.9304 | 0.0000 |

| C(4,6) | 2.88 × 10−6 | 2.28 × 10−7 | 12.6097 | 0.0000 |

| C(4,7) | 1.45 × 10−6 | 2.01 × 10−7 | 7.2044 | 0.0000 |

| C(4,8) | 1.97 × 10−6 | 1.29 × 10−7 | 15.2092 | 0.0000 |

| C(5,5) | 5.36 × 10−6 | 3.11 × 10−7 | 17.2332 | 0.0000 |

| C(5,6) | 4.97 × 10−6 | 3.02 × 10−7 | 16.4371 | 0.0000 |

| C(5,7) | 1.92 × 10−6 | 2.16 × 10−7 | 8.8654 | 0.0000 |

| C(5,8) | 2.18 × 10−6 | 1.50 × 10−7 | 14.5525 | 0.0000 |

| C(6,6) | 8.92 × 10−6 | 6.34 × 10−7 | 14.0687 | 0.0000 |

| C(6,7) | 2.33 × 10−6 | 3.13 × 10−7 | 7.4589 | 0.0000 |

| C(6,8) | 2.69 × 10−6 | 2.06 × 10−7 | 13.0605 | 0.0000 |

| C(7,7) | 7.26 × 10−6 | 6.88 × 10−7 | 10.5584 | 0.0000 |

| C(7,8) | 1.18 × 10−6 | 1.54 × 10−7 | 7.6740 | 0.0000 |

| C(8,8) | 2.14 × 10−6 | 1.50 × 10−7 | 14.2812 | 0.0000 |

| A1(1,1) | 0.0448 | 0.0050 | 8.9266 | 0.0000 |

| A1(1,2) | 0.0902 | 0.0061 | 14.8814 | 0.0000 |

| A1(1,3) | 0.0784 | 0.0057 | 13.8914 | 0.0000 |

| A1(1,4) | 0.0975 | 0.0074 | 13.1735 | 0.0000 |

| A1(1,5) | 0.0814 | 0.0062 | 13.1340 | 0.0000 |

| A1(1,6) | 0.0825 | 0.0058 | 14.1276 | 0.0000 |

| A1(1,7) | 0.0819 | 0.0070 | 11.7103 | 0.0000 |

| A1(1,8) | 0.0966 | 0.0069 | 13.8997 | 0.0000 |

| A1(2,2) | 0.1817 | 0.0071 | 25.5267 | 0.0000 |

| A1(2,3) | 0.1580 | 0.0062 | 25.6121 | 0.0000 |

| A1(2,4) | 0.1963 | 0.0068 | 28.8162 | 0.0000 |

| A1(2,5) | 0.1640 | 0.0068 | 24.2592 | 0.0000 |

| A1(2,6) | 0.1661 | 0.0061 | 27.1445 | 0.0000 |

| A1(2,7) | 0.1650 | 0.0073 | 22.5519 | 0.0000 |

| A1(2,8) | 0.1945 | 0.0069 | 28.2070 | 0.0000 |

| A1(3,3) | 0.1374 | 0.0061 | 22.4792 | 0.0000 |

| A1(3,4) | 0.1707 | 0.0062 | 27.7446 | 0.0000 |

| A1(3,5) | 0.1426 | 0.0060 | 23.5920 | 0.0000 |

| A1(3,6) | 0.1444 | 0.0057 | 25.2061 | 0.0000 |

| A1(3,7) | 0.1435 | 0.0066 | 21.8106 | 0.0000 |

| A1(3,8) | 0.1691 | 0.0063 | 26.9917 | 0.0000 |

| A1(4,4) | 0.2121 | 0.0095 | 22.4028 | 0.0000 |

| A1(4,5) | 0.1772 | 0.0065 | 27.1272 | 0.0000 |

| A1(4,6) | 0.1795 | 0.0064 | 27.9984 | 0.0000 |

| A1(4,7) | 0.1783 | 0.0089 | 19.9917 | 0.0000 |

| A1(4,8) | 0.2101 | 0.0082 | 25.5651 | 0.0000 |

| A1(5,5) | 0.1481 | 0.0076 | 19.5028 | 0.0000 |

| A1(5,6) | 0.1500 | 0.0061 | 24.7480 | 0.0000 |

| A1(5,7) | 0.1490 | 0.0076 | 19.7058 | 0.0000 |

| A1(5,8) | 0.1756 | 0.0066 | 26.6188 | 0.0000 |

| A1(6,6) | 0.1519 | 0.0064 | 23.7560 | 0.0000 |

| A1(6,7) | 0.1509 | 0.0066 | 22.9162 | 0.0000 |

| A1(6,8) | 0.1778 | 0.0062 | 28.5054 | 0.0000 |

| A1(7,7) | 0.1499 | 0.0108 | 13.8856 | 0.0000 |

| A1(7,8) | 0.1767 | 0.0086 | 20.5936 | 0.0000 |

| A1(8,8) | 0.2082 | 0.0089 | 23.3227 | 0.0000 |

| B1(1,1) | 0.9365 | 0.0078 | 119.4844 | 0.0000 |

| B1(1,2) | 0.8512 | 0.0088 | 97.3101 | 0.0000 |

| B1(1,3) | 0.8769 | 0.0089 | 98.7774 | 0.0000 |

| B1(1,4) | 0.8513 | 0.0106 | 80.6946 | 0.0000 |

| B1(1,5) | 0.8613 | 0.0102 | 84.5252 | 0.0000 |

| B1(1,6) | 0.8696 | 0.0096 | 90.2320 | 0.0000 |

| B1(1,7) | 0.8625 | 0.0143 | 60.1847 | 0.0000 |

| B1(1,8) | 0.8496 | 0.0106 | 80.1649 | 0.0000 |

| B1(2,2) | 0.7735 | 0.0055 | 140.3956 | 0.0000 |

| B1(2,3) | 0.7969 | 0.0052 | 154.5904 | 0.0000 |

| B1(2,4) | 0.7737 | 0.0051 | 151.8311 | 0.0000 |

| B1(2,5) | 0.7828 | 0.0056 | 141.0820 | 0.0000 |

| B1(2,6) | 0.7903 | 0.0054 | 145.3758 | 0.0000 |

| B1(2,7) | 0.7839 | 0.0078 | 100.9599 | 0.0000 |

| B1(2,8) | 0.7721 | 0.0052 | 147.2636 | 0.0000 |

| B1(3,3) | 0.8210 | 0.0056 | 146.0587 | 0.0000 |

| B1(3,4) | 0.7971 | 0.0052 | 153.1472 | 0.0000 |

| B1(3,5) | 0.8064 | 0.0055 | 146.1735 | 0.0000 |

| B1(3,6) | 0.8142 | 0.0056 | 146.6485 | 0.0000 |

| B1(3,7) | 0.8076 | 0.0082 | 97.9905 | 0.0000 |

| B1(3,8) | 0.7955 | 0.0052 | 153.5707 | 0.0000 |

| B1(4,4) | 0.7738 | 0.0069 | 112.5035 | 0.0000 |

| B1(4,5) | 0.7829 | 0.0056 | 140.7238 | 0.0000 |

| B1(4,6) | 0.7905 | 0.0059 | 133.1670 | 0.0000 |

| B1(4,7) | 0.7840 | 0.0091 | 86.1304 | 0.0000 |

| B1(4,8) | 0.7722 | 0.0061 | 125.8899 | 0.0000 |

| B1(5,5) | 0.7921 | 0.0073 | 109.0117 | 0.0000 |

| B1(5,6) | 0.7997 | 0.0058 | 137.2994 | 0.0000 |

| B1(5,7) | 0.7932 | 0.0084 | 94.3148 | 0.0000 |

| B1(5,8) | 0.7813 | 0.0057 | 136.7357 | 0.0000 |

| B1(6,6) | 0.8075 | 0.0067 | 120.0668 | 0.0000 |

| B1(6,7) | 0.8009 | 0.0085 | 94.1766 | 0.0000 |

| B1(6,8) | 0.7889 | 0.0056 | 140.0178 | 0.0000 |

| B1(7,7) | 0.7943 | 0.0115 | 68.9509 | 0.0000 |

| B1(7,8) | 0.7824 | 0.0084 | 93.0574 | 0.0000 |

| B1(8,8) | 0.7707 | 0.0069 | 112.3783 | 0.0000 |

| 1 | Bitcoin is a strong hedge for most of the developing markets but only an effective diversifier for the developed markets. |

| 2 | Only for Canada. |

| 3 | Bitcoin, Ripple, and Stellar are safe havens for all US equity indices. |

| 4 | An asset might be suitable for investment from a risk perspective. If the asset is negatively correlated with another asset, putting them together decreases risk significantly. In line with Baur and Lucey (2010) we differentiate between a diversifier, hedge, and safe haven. A diversifier is an asset that has a weak positive correlation with another asset on average. A weak (strong) hedge is an asset that is uncorrelated (negatively correlated) with another asset on average. A weak (strong) safe haven is an asset that is uncorrelated (negatively correlated) with another asset on average during times of stress, Bouri et al. (2017b). |

References

- Albulescu, Claudiu Tiberiu. 2021. COVID-19 and the United States financial markets’ volatility. Finance Research Letters 38: 101699. [Google Scholar] [CrossRef] [PubMed]

- Al-Khazali, Osamah, Elie Bouri, and David Roubaud. 2018. The Impact of Positive and Negative Macroeconomic News Surprises: Gold versus Bitcoin. Economics Bulletin 38: 373–82. [Google Scholar]

- Baig, Ahmed Suleman, Hassan Anjum Butt, Omair Haroon, and Syed Aun R. Rizvia. 2020. Deaths, panic, lockdowns and US equity markets: The case of COVID-19 pandemic. Finance Research Letters 38: 101701. [Google Scholar] [CrossRef]

- Baur, Dirck, and Brian Lucey. 2010. Is gold a hedge or a safe haven? An analysis of stocks, bonds and gold. The Financial Review 45: 217–29. [Google Scholar] [CrossRef]

- Baur, Dirck, and Kristoffer Glover. 2012. The destruction of a safe haven asset? Applied Finance Letters 1: 8–15. [Google Scholar] [CrossRef] [Green Version]

- Baur, Drick, and Thomas McDermott. 2010. Is gold a safe-haven? International evidence. Journal of Banking & Finance 34: 1886–1898. [Google Scholar]

- Baur, Drick, and Thomas McDermott. 2016. Why is gold a safe-haven? Journal of Behavioral and Experimental Finance 10: 63–71. [Google Scholar] [CrossRef]

- Beckmann, Joscha Berger, and Robert Czudaj. 2015. Does gold act as a hedge or a safe haven for stocks? A smooth transition approach. Economic Modelling 48: 16–24. [Google Scholar] [CrossRef] [Green Version]

- Będowska-Sójka, Barbara, and Agata Kliber. 2021. Is there one safe-haven for various turbulences? The evidence from gold, Bitcoin and Ether. The North American Journal of Economics and Finance 56: 101390. [Google Scholar] [CrossRef]

- Bekiros, Stelios, Boubaker Sabri, Duc Khuong Nguyen, and Gazi Salah Uddin. 2017. Black swan events and safe havens: The role of gold in globally integrated emerging markets. Journal of International Money and Finance 73: 317–34. [Google Scholar] [CrossRef] [Green Version]

- Bollerslev, Tim, and Jeffrey Wooldridge. 1992. Quasi-maximum likelihood estimation and inference in dynamic models with time-varying covariances. Econometric Reviews 11: 143–72. [Google Scholar] [CrossRef]

- Bollerslev, Tim, Robert Engle, and Jeffrey Wooldridge. 1988. A capital asset pricing model with time varying covariances. Journal of Political Economy 96: 116–31. [Google Scholar] [CrossRef]

- Bouoiyour, Jamel, Refk Selmi, and Marck El Wohar. 2019. Safe havens in the face of Presidential election uncertainty: A comparison between Bitcoin, oil and precious metals. Applied Economics 51: 6076–88. [Google Scholar] [CrossRef]

- Bouri, Elie, and Rangan Gupta. 2019. Predicting Bitcoin Returns: Comparing the Roles of Newspaperand Internet Search-Based Measures of Uncertainty. Finance Research Letters 38: 101398. [Google Scholar] [CrossRef] [Green Version]

- Bouri, Elie, Brian Lucey, and David Roubaud. 2020a. Cryptocurrencies and the downside risk in equity investments. Finance Research Letters 33: 101211. [Google Scholar] [CrossRef]

- Bouri, Elie, Konstantinos Gkillas, and Rangan Gupta. 2020. Trade Uncertainties and the Hedging Abilities of Bitcoin. Economic Notes 49: e12173. [Google Scholar]

- Bouri, Elie, Naji Jalkh, Peter Molnár, and David Roubaud. 2017a. Bitcoin for energy commodities before and after the December 2013 crash: Diversifier, hedge or safe haven? Applied Economics 49: 5063–73. [Google Scholar] [CrossRef]

- Bouri, Elie, Peter Molnár, Georges Azzi, David Roubaud, and Lars Ivar Hagfors. 2017b. On the hedge and safe haven properties of Bitcoin: Is it really more than a diversifier? Finance Research Letters 20: 192–98. [Google Scholar] [CrossRef]

- Bouri, Elie, Rangan Gupta, Marco Lau Chi Keung, David Roubaud, and Shixuan Wang. 2018. Bitcoin and Global Financial Stress: A Copula-Based Approach to Dependence and Causality in the Quantiles. The Quarterly Review of Economics and Finance 69: 297–307. [Google Scholar] [CrossRef] [Green Version]

- Bouri, Elie, Syed Jawad Hussain Shahzad, and David Roubaud. 2020b. Cryptocurrencies as hedges and safehavens for US equity sectors. The Quarterly Review of Economics and Finance 75: 294–307. [Google Scholar] [CrossRef]

- Bouri, Elie, Syed Jawad Hussain Shahzad, David Roubaud, Ladislav Krištoufek, and Brian Lucey. 2020c. Bitcoin, gold, and commodities as safe havens for stocks: New insight through wavelet analysis. The Quarterly Review of Economics and Finance 77: 156–64. [Google Scholar] [CrossRef]

- Bredin, Don, Thomas Conlon, and Valerio Potì. 2015. Does gold glitter in the long-run? Gold as a hedge and safe haven across time and investment horizon. International Review of Financial Analysis 41: 320–28. [Google Scholar] [CrossRef]

- Brière, Marie, Kim Oosterlinck, and Ariane Szafarz. 2015. Virtual currency, tangible return: Portfolio diversification with bitcoin. Journal of Asset Management 16: 365–73. [Google Scholar] [CrossRef]

- Cheema, Mohamed, Robert Faff, and Kenneth Szulczuk. 2020. The 2008 Global Financial Crisis and COVID-19 Pandemic: How Safe are the Safe Haven Assets? Covid Economics, Vetted and Real-Time Papers 34: 88–115. [Google Scholar] [CrossRef]

- Choi, Sangyup, and Junhyeok Shin. 2022. Bitcoin: An inflation hedge but not a safe haven. Finance Research Letters 46: 102379. [Google Scholar] [CrossRef] [PubMed]

- Chrétien, Stéphane, and Juan-Pablo Ortega. 2014. Multivariate GARCH estimation via a Bregman-proximal trust-region method. Computational Statistics & Data Analysis 76: 210–36. [Google Scholar]

- Conlon, Thomas, and Richard McGee. 2020. Safe haven or risky hazard? Bitcoin during the COVID-19 bear market. Finance Research Letters 35: 101607. [Google Scholar] [CrossRef]

- Corbet, Shaen, Andrew Meegan, Charles Larkin, Brian Lucey, and Larisa Yarovaya. 2018. Exploring the dynamic relationships between cryptocurrencies and other financial assets. Economics Letters 165: 28–34. [Google Scholar] [CrossRef] [Green Version]

- Corbet, Shaen, Charles Larkin, and Brian Lucey. 2020. The contagion effects of the COVID-19 pandemic: Evidence from gold and cryptocurrencies. Finance Research Letters 35: 101554. [Google Scholar] [CrossRef]

- de Almeida, Daniel, Hotta Luiz, and Esther Ruiz Ortega. 2015. Mgarch Models: Tradeoff Between Feasibility and Flexibility. UC3M Working Papers Statistics and Econometrics 15–16: 1–42. [Google Scholar] [CrossRef] [Green Version]

- Ding, Zhuanxin, and Robert F. Engle. 2001. Large scale conditional covariance matrix modeling, estimation and testing. Academia Economic Papers 29: 157–84. [Google Scholar]

- Dyhrberg, Anne Haubo. 2016a. Bitcoin, gold and the dollar–A GARCH volatility analysis. Finance Research Letters 16: 85–92. [Google Scholar] [CrossRef] [Green Version]

- Dyhrberg, Anne Haubo. 2016b. Hedging capabilities of bitcoin. Is it the virtual gold? Finance Research Letters 16: 139–44. [Google Scholar] [CrossRef] [Green Version]

- Feng, Wenjun, Yiming Wang, and Zhengjun Zhang. 2018. Can cryptocurrencies be a safe haven: A tail risk perspective analysis. Applied Economics 50: 4745–62. [Google Scholar] [CrossRef]

- Ghorbel, Achraf, and Ahmed Jeribi. 2021a. Contagion of COVID-19 pandemic between oil and financial assets: The evidence of multivariate Markov switching GARCH models. Journal of Investment Compliance 22: 151–69. [Google Scholar] [CrossRef]

- Ghorbel, Ahmed, and Ahmed Jeribi. 2021b. Investigating the relationship between volatilities of cryptocurrencies and other financial assets. Decisions in Economics and Finance 44: 817–43. [Google Scholar] [CrossRef]

- Ghorbel, Achraf, and Ahmed Jeribi. 2021c. Volatility spillovers and contagion between energy sector and financial assets during COVID-19 crisis period. Eurasian Economic Review 11: 449–67. [Google Scholar] [CrossRef]

- Ghorbel, Achraf, Wajdi Frikha, and Yasmine Snene Manzli. 2022. Testing for asymmetric non-linear short- and long-run relationships between crypto-currencies and stock markets. Eurasian Economic Review 12: 387–425. [Google Scholar] [CrossRef]

- Gourieroux, Christian. 1997. ARCH Models and Financial Applications. New York: Springer. [Google Scholar]

- Guesmi, Khale, Samir Saadi, Ilyes Abid, and Zied Ftiti. 2018. Portfolio diversification with virtual currency: Evidence from bitcoin. International Review of Financial Analysis 63: 431–37. [Google Scholar]

- Gürgün, Gözde, and Ibrahim Unalmis. 2014. Is gold a safe haven against equity market investment in emerging and developing countries? Finance Research Letters 11: 341–48. [Google Scholar] [CrossRef]

- Hafner, Christian. 2003. Fourth moment structure of multivariate GARCH models. Journal of Financial Econometrics 1: 26–54. [Google Scholar] [CrossRef]

- Hafner, Christian, and Arie Preminger. 2009. On asymptotic theory for multivariate GARCH models. Journal of Multivariate Analysis 100: 2044–2054. [Google Scholar] [CrossRef] [Green Version]

- Hood, Matthew, and Farooq Malik. 2013. Is gold the best hedge and a safe-haven under changing stock market volatility? Review of Financial Economics 22: 47–52. [Google Scholar] [CrossRef]

- Hillier, David, Paul Draper, and Robert Faff. 2006. Do Precious Metals Shine? An Investment Perspective. Financial Analysts Journal 62: 98–106. [Google Scholar] [CrossRef]

- Iqbal, Javed. 2017. Does gold hedge stock market, inflation and exchange rate risks? An econometric investigation. International Review of Economics and Finance 48: 1–17. [Google Scholar] [CrossRef]

- Jeribi, Ahmed, and Yesmine Snene-Manzli. 2021. Can cryptocurrencies be a safe haven during the novel COVID-19 pandemic? Evidence from the Tunisian stock market. Journal of Research in Emerging Markets 3: 14–31. [Google Scholar] [CrossRef]

- Jeribi, Ahmed, Dhouha Chamsa, and Yesmine Snene-Manzli. 2020. Emerging Stock Markets’ Reaction to COVID-19: Can Cryptocurrencies be a Safe Haven? Journal of Management and Economic Studies 2: 152–65. [Google Scholar] [CrossRef]

- Jeribi, Ahmed, Sangram Keshari Jena, and Aymen Lahiani. 2021. Are Cryptocurrencies a Backstop for the Stock Market in a COVID-19-Led Financial Crisis? Evidence from the NARDL Approach. International Journal of Financial Studies 9: 33. [Google Scholar] [CrossRef]

- Ji, Qiang, Dayong Zhang, and Yuqian Zhao. 2020. Searching for safe-haven assets during the COVID-19 pandemic. International Review of Financial Analysis 71: 101526. [Google Scholar] [CrossRef]

- Ji, Qiang, Elie Bouri, Rangan Gupta, and David Roubaud. 2018. Network causality structures among Bitcoin and other financial assets: A directed acyclic graph approach. The Quarterly Review of Economics and Finance 70: 203–13. [Google Scholar] [CrossRef] [Green Version]

- Junttila, Juha, Juho Pesonen, and Juhani Raatikainen. 2018. Commodity market based hedging against stock market risk in times of financial crisis: The case of crude oil and gold. Journal of International Financial Markets, Institutions & Money 56: 255–80. [Google Scholar]

- Klein, Tony. 2017. Dynamic correlation of precious metals and flight-to-quality in developed markets. Finance Research Letters 23: 283–90. [Google Scholar] [CrossRef]

- Klein, Tony, Hien Pham Thu, and Thomas Walther. 2018. Bitcoin is not the new gold-A comparison of volatility, correlation, and portfolio performance. International Review of Financial Analysis 59: 105–16. [Google Scholar] [CrossRef]

- Kliber, Agata, Marszałek Pawel, Ida Musiałkowska, and Katarzyna Świerczyńska. 2019. Bitcoin: Safe haven, hedge or diversifier? Perception of bitcoin in the context of a country’s economic situation—A stochastic volatility approach. Physica A: Statistical Mechanics and Its Applications 524: 246–57. [Google Scholar] [CrossRef]

- Korovkin, Vasily, and Alexey Makarin. 2019. Conflict and Inter-Group Trade: Evidence from the 2014 Russia-Ukraine Crisis. SSRN. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3397276 (accessed on 25 February 2022).

- Kroner, Kenneth, and Jahangir Sultan. 1993. Time-varying distributions and dynamic hedging with foreign currency futures. Journal of Financial and Quantitative Analysis 28: 535–51. [Google Scholar] [CrossRef]

- Kroner, Kenneth, and Victor K. Ng. 1998. Modeling asymmetric comovements of asset returns. Review of Financial Studies 11: 817–44. [Google Scholar] [CrossRef]

- Ku, Yuan-Hung Hsu, Ho-Chyuan Chen, and Kuang-Hua Chen. 2007. On the application of the dynamic conditional correlation model in estimating optimal time-varying hedge ratios. Applied Economics Letters 14: 503–9. [Google Scholar] [CrossRef]

- Kumar, Anoop. S. 2020. Testing Safe Haven Property of Bitcoin and Gold during COVID-19: Evidence from Multivariate GARCH analysis. Economics Bulletin 40: 2005–15. [Google Scholar]

- Lahmiri, S., and S. Bekiros. 2020. The Impact of COVID-19 pandemic upon Stability and Sequential Irregularity of Equity and Cryptocurrency Markets. Chaos, Solitons & Fractals 138: 109936. [Google Scholar] [CrossRef]

- Liu, Weiyi. 2019. Portfolio diversification across cryptocurrencies. Finance Research Letters 29: 200–5. [Google Scholar] [CrossRef]

- Lorenzo, Luis, and Javier Arroyo. 2022. Analysis of the cryptocurrency market using different prototype-based clustering techniques. Financial Innovation 8: 7. [Google Scholar] [CrossRef]

- Mazur, Mieszko, Man Dang, and Miguel Vega. 2021. COVID-19 and the march 2020 stock market crash. Evidence from S&P1500. Finance Research Letters 38: 101690. [Google Scholar] [CrossRef] [PubMed]

- McCown, James Ross, and John R. Zimmerman. 2006. Is Gold a Zero-Beta Asset? Analysis of the Investment Potential of Precious Metals. July 24. Available online: https://ssrn.com/abstract=920496 (accessed on 25 February 2022). [CrossRef]

- Ming, Lei, Xinran Zhang, Qianqui Liu, and Shenggang Yang. 2020. A revisit to the hedge and safe haven properties of gold: New evidence from China. Journal of Futures Markets 40: 1442–56. [Google Scholar] [CrossRef]

- Narayan, Paresh, Seema Narayan, and Xinwei Zheng. 2010. Gold and oil futures markets: Are markets efficient? Applied Energy 87: 3299–303. [Google Scholar] [CrossRef]

- Polasik, Michal, Anna Piotrowska, Tomasz Piotr Wisniewski, Radoslaw Kotkowski, and Geoffrey Lightfoot. 2015. Price fluctuations and the use of Bitcoin: An empirical inquiry. International Journal of Electronic Commerce 20: 9–49. [Google Scholar] [CrossRef] [Green Version]

- Popper, Nathaniel. 2015. Digital Gold: The Untold Story of Bitcoin. London: Penguin. [Google Scholar]

- Reboredo, Juan Carlos. 2013. Is gold a safe-haven or a hedge for the US dollar? Implications for risk management. Journal of Banking & Finance 37: 2665–76. [Google Scholar]

- Salisu, Afees, and Idris Adediran. 2020. Gold as a hedge against oil shocks: Evidence from new datasets for oil shocks. Resources Policy 66: 101606. [Google Scholar] [CrossRef]

- Salisu, Afees, Ibrahim Raheem, and Umar Ndako. 2020. The inflation hedging properties of gold, stocks and real estate: A comparative analysis. Resources Policy 66: 101605. [Google Scholar] [CrossRef]

- Salisu, Afees, Ibrahim Raheem, and Xuan Vinh Vo. 2021a. Assessing the safe haven property of the gold market during COVID-19 pandemic. International Review of Financial Analysis 74: 101666. [Google Scholar] [CrossRef] [PubMed]

- Salisu, Afees, Xuan Vinh Vo, and Adedoyin Lawal. 2021b. Hedging oil price risk with gold during COVID-19 pandemic. Resources Policy 70: 101897. [Google Scholar] [CrossRef]

- Sherman, Eugene J. 1986. Gold Investment: Theory and Application. Hoboken: Prentice Hall. [Google Scholar]

- Shahzad, Hussain, Syed Jawad, Elie Bouri, David Roubaud, and Ladislav Kristoufek. 2020. Safe haven, hedge and diversification for G7 stock markets: Gold versus bitcoin. Economic Modelling 87: 212–24. [Google Scholar] [CrossRef]

- Shahzad, Hussain, Syed Jawad, Elie Bouri, David Roubaud, Ladislav Kristoufek, and Brian Lucey. 2019. Is Bitcoin a better safe-haven investment than gold and commodities? International Review of Financial Analysis 63: 322–30. [Google Scholar] [CrossRef]

- Smales, Lee. 2019. Bitcoin as a safe-haven: Is it even worth considering? Finance Research Letters 30: 385–93. [Google Scholar] [CrossRef]

- Smiech, Sławomir, and Moni Papiez. 2016. In search of hedges and safe havens: Revisiting the relations between gold and oil in the rolling regression framework. Finance Research Letters 20: 238–44. [Google Scholar] [CrossRef]

- Stensås, Anders, Nygaard Magnus Frostholm, Kya Khine, and Sirimon Treepongkaruna. 2019. Can Bitcoin be a diversifier, hedge or safe haven tool? Cogent Economics & Finance 7: 1593072. [Google Scholar]

- Tauhidul, Islam Tanin, Ashutosh Sarker, Robert Brooks, and Hung Xuan Do. 2022. Does oil impact gold during the COVID-19 and three other recent crises? Energy Economics 108: 105938. [Google Scholar]

- Miyazaki, Takashi, and Shigeyuki Hamori. 2013. Testing for causality between the gold return and stock market performance: Evidence for ‘gold investment in case of emergency’. Applied Financial Economics 23: 27–40. [Google Scholar] [CrossRef]

- Wang, Pengfei, Zhang Wei, Li Xiao, and Shen Dehua. 2019. Is cryptocurrency a hedge or a safe haven for international indices? A comprehensive and dynamic perspective. Finance Research Letters 31: 1–18. [Google Scholar] [CrossRef]

- Wiseman, Paul. 2022. Economic Dangers from Russia’s Invasion Ripple across Globe. AP NEWS. Available online: https://apnews.com/article/russia-ukraine-vladimir-putin-coronavirus-pandemicbusiness-health-9478a9825c9abfde5f6505bd34b2998c (accessed on 4 March 2022).

- Wu, Shan, Tong Mu, Yang Zhongyi, and Abdelkader Derbali. 2019. Does gold or bitcoin hedge economic policy uncertainty? Finance Research Letters 31: 171–178. [Google Scholar] [CrossRef]

- Zaremba, Adam, Renatas Kizys, David Y. Aharon, and Ender Demir. 2020. Infected markets: Novel coronavirus, government interventions, and stock return volatility around the globe. Finance Research Letters 35: 101597. [Google Scholar] [CrossRef] [PubMed]

- Zhang, Dayong, Min Hu, and Qiang Ji. 2020. Financial markets under the global pandemic of COVID-19. Finance Research Letters 36: 101528. [Google Scholar] [CrossRef]

| Variables | Descriptives | Period | ||

|---|---|---|---|---|

| Pre-COVID-19 | During COVID-19 | During Russia–Ukraine War | ||

| Bitcoin | Mean | 0.0027 | 0.0030 | −0.0037 |

| Median | 0.0027 | 0.0028 | −0.0002 | |

| Maximum | 0.2218 | 0.1937 | 0.1024 | |

| Minimum | −0.2474 | −0.4973 | −0.2821 | |

| Std. Dev. | 0.0463 | 0.0485 | 0.0401 | |

| Skewness | −0.0777 | −1.9580 | −1.8464 | |

| Kurtosis | 7.0432 | 23.7102 | 13.6797 | |

| Jarque–Bera | 700.5574 | 10,291.6800 | 1191.7990 | |

| Gold | Mean | 0.0004 | 0.0004 | −0.0002 |

| Median | 0.0004 | 0.0011 | −0.0001 | |

| Maximum | 0.0394 | 0.0430 | 0.0309 | |

| Minimum | −0.0324 | −0.0589 | −0.0284 | |

| Std. Dev. | 0.0075 | 0.0103 | 0.0097 | |

| Skewness | 0.2594 | −0.7645 | 0.0595 | |

| Kurtosis | 5.0364 | 7.1580 | 3.5585 | |

| Jarque–Bera | 188.9692 | 454.6780 | 3.0429 | |

| S&P500 | Mean | 0.0005 | 0.0005 | −0.0005 |

| Median | 0.0005 | 0.0013 | −0.0015 | |

| Maximum | 0.0484 | 0.0897 | 0.0540 | |

| Minimum | −0.0418 | −0.1277 | −0.0442 | |

| Std. Dev. | 0.0080 | 0.0160 | 0.0153 | |

| Skewness | −0.6390 | −1.0155 | −0.0615 | |

| Kurtosis | 7.8328 | 18.3487 | 3.5200 | |

| Jarque–Bera | 1069.3360 | 5553.2350 | 2.6651 | |

| CAC40 | Mean | 0.0003 | 0.0002 | 0.0002 |

| Median | 0.0004 | 0.0011 | −0.0004 | |

| Maximum | 0.0406 | 0.0806 | 0.0688 | |

| Minimum | −0.0838 | −0.1310 | −0.0509 | |

| Std. Dev. | 0.0095 | 0.0156 | 0.0140 | |

| Skewness | −0.8525 | −1.3654 | 0.3920 | |

| Kurtosis | 10.7762 | 16.4670 | 5.9162 | |

| Jarque–Bera | 2711.9660 | 4374.3020 | 85.1119 | |

| DAX30 | Mean | 0.0003 | 0.0002 | 0.0001 |

| Median | 0.0007 | 0.0008 | 0.0005 | |

| Maximum | 0.0345 | 0.1041 | 0.0762 | |

| Minimum | −0.0707 | −0.1305 | −0.0451 | |

| Std. Dev. | 0.0097 | 0.0157 | 0.0146 | |

| Skewness | −0.5903 | −1.0315 | 0.4801 | |

| Kurtosis | 6.9719 | 16.8962 | 6.0780 | |

| Jarque–Bera | 734.7256 | 4572.1840 | 97.0288 | |

| FTSE100 | Mean | 0.0002 | 0.0000 | 0.0003 |

| Median | 0.0004 | 0.0006 | 0.0008 | |

| Maximum | 0.0352 | 0.0867 | 0.03844 | |

| Minimum | −0.0352 | −0.1151 | −0.0354 | |

| Std. Dev. | 0.0080 | 0.0138 | 0.0100 | |

| Skewness | −0.1409 | −1.2332 | −0.1421 | |

| Kurtosis | 5.3644 | 16.6258 | 5.1374 | |

| Jarque–Bera | 242.6107 | 4442.0700 | 43.3944 | |

| FTSEMIB30 | Mean | 0.0001 | 0.0002 | −8.05 × 10−6 |

| Median | 0.0007 | 0.0013 | 0.0006 | |

| Maximum | 0.0491 | 0.0855 | 0.0672 | |

| Minimum | −0.1333 | −0.1854 | −0.0644 | |

| Std. Dev. | 0.0129 | 0.0171 | 0.0156 | |

| Skewness | −1.1287 | −2.8930 | −0.2834 | |

| Kurtosis | 15.5474 | 33.2730 | 5.6318 | |

| Jarque–Bera | 6955.0070 | 22,006.7500 | 67.6462 | |

| Nikkei | Mean | 0.0003 | 0.0002 | −2.59 × 10−5 |

| Median | 0.0004 | 0.0003 | 0.0010 | |

| Maximum | 0.0691 | 0.0773 | 0.0386 | |

| Minimum | −0.0825 | −0.0627 | −0.0305 | |

| Std. Dev. | 0.0115 | 0.0137 | 0.0122 | |

| Skewness | −0.4538 | 0.1016 | 0.1036 | |

| Kurtosis | 10.5439 | 7.3376 | 3.5394 | |

| Jarque–Bera | 2470.5290 | 436.8313 | 3.1159 | |

| SP-TSX | Mean | 0.0003 | 0.0004 | −0.0003 |

| Median | 0.0006 | 0.0013 | 0.0002 | |

| Maximum | 0.0290 | 0.1130 | 0.0329 | |

| Minimum | −0.0249 | −0.1318 | −0.0315 | |

| Std. Dev. | 0.0059 | 0.0150 | 0.0104 | |

| Skewness | −0.3594 | −1.7967 | −0.1019 | |

| Kurtosis | 5.3593 | 31.9811 | 3.4354 | |

| Jarque–Bera | 260.2983 | 19,756.9600 | 2.1572 | |

| Indices | Period | Pearson’s Rho | Spearman’s Rho | Kendall’s Tau |

|---|---|---|---|---|

| S&P 500 | Pre-COVID-19 | −0.0381 | −0.0372 | −0.0252 |

| During COVID-19 | 0.3703 | 0.2617 | 0.1757 | |

| During Russia–Ukraine War | 0.5586 | 0.5696 | 0.4017 | |

| CAC40 | Pre-COVID-19 | −0.0010 | −0.0050 | −0.0038 |

| During COVID-19 | 0.3250 | 0.1672 | 0.1126 | |

| During Russia–Ukraine War | 0.3685 | 0.3194 | 0.2225 | |

| DAX30 | Pre-COVID-19 | 0.0052 | 0.0059 | 0.0035 |

| During COVID-19 | 0.3321 | 0.1615 | 0.1084 | |

| During Russia–Ukraine War | 0.3715 | 0.3124 | 0.2139 | |

| FTSE 100 | Pre-COVID-19 | −0.0252 | −0.0170 | −0.0122 |

| During COVID-19 | 0.3202 | 0.1440 | 0.0970 | |

| During Russia–Ukraine War | 0.3175 | 0.2568 | 0.1774 | |

| FTSEMIB30 | Pre-COVID-19 | −0.0074 | 0.0085 | 0.0053 |

| During COVID-19 | 0.3990 | 0.1588 | 0.1066 | |

| During Russia–Ukraine War | 0.3918 | 0.3545 | 0.2475 | |

| Nikkei | Pre-COVID-19 | −0.0535 | −0.0207 | −0.0139 |

| During COVID-19 | 0.1222 | 0.0382 | 0.0263 | |

| During Russia–Ukraine War | 0.1275 | 0.0295 | 0.0160 | |

| SP-TSX | Pre-COVID-19 | 0.0355 | 0.0311 | 0.0206 |

| During COVID-19 | 0.4009 | 0.2387 | 0.1615 | |

| During Russia–Ukraine War | 0.5257 | 0.4842 | 0.3394 |

| Indices | Period | Pearson’s Rho | Spearman’s Rho | Kendall’s Tau |

|---|---|---|---|---|

| S&P 500 | Pre-COVID-19 | −0.1683 | −0.1262 | −0.0846 |

| During COVID-19 | 0.1457 | 0.0802 | 0.0548 | |

| During Russia–Ukraine War | 0.2631 | 0.2225 | 0.1537 | |

| CAC40 | Pre-COVID-19 | −0.2693 | −0.1991 | −0.1349 |

| During COVID-19 | 0.0834 | 0.0200 | 0.0141 | |

| During Russia–Ukraine War | 0.1195 | 0.1841 | 0.1303 | |

| DAX30 | Pre-COVID-19 | −0.2667 | −0.2163 | −0.1475 |

| During COVID-19 | 0.1327 | 0.0365 | 0.0262 | |

| During Russia–Ukraine War | 0.1188 | 0.1779 | 0.1236 | |

| FTSE 100 | Pre-COVID-19 | −0.1462 | −0.1044 | −0.0704 |

| During COVID-19 | 0.1059 | 0.0264 | 0.0177 | |

| During Russia–Ukraine War | 0.1113 | 0.1378 | 0.0978 | |

| FTSEMIB 30 | Pre-COVID-19 | −0.2382 | −0.1778 | −0.1208 |

| During COVID-19 | 0.0878 | 0.0174 | 0.0127 | |

| During Russia–Ukraine War | 0.1397 | 0.2018 | 0.1396 | |

| Nikkei | Pre-COVID-19 | −0.1619 | −0.1073 | −0.0724 |

| During COVID-19 | 0.1083 | 0.0352 | 0.0237 | |

| During Russia–Ukraine War | 0.0306 | 0.0382 | 0.0240 | |

| SP-TSX | Pre-COVID-19 | −0.0427 | −0.0183 | −0.0132 |

| During COVID-19 | 0.1902 | 0.1438 | 0.0990 | |

| During Russia–Ukraine War | 0.4356 | 0.4262 | 0.2937 |

| Indices | Period | β | HE | |

|---|---|---|---|---|

| S&P 500 | Pre-COVID-19 | 0.0111 | 0.0343 | 0.0376 |

| During COVID-19 | 0.0529 | 0.0440 | 0.2908 | |

| During Russia–Ukraine War | 0.1025 | 0.0496 | 0.1322 | |

| CAC40 | Pre-COVID-19 | 0.0173 | 0.0516 | 0.0754 |

| During COVID-19 | 0.0243 | 0.0734 | 0.1826 | |

| During Russia–Ukraine War | 0.0352 | 0.0762 | 0.0710 | |

| DAX30 | Pre-COVID-19 | 0.0206 | 0.0506 | 0.0615 |

| During COVID-19 | 0.0292 | 0.0684 | 0.1195 | |

| During Russia–Ukraine War | 0.0414 | 0.0715 | 0.0665 | |

| FTSE 100 | Pre-COVID-19 | 0.0143 | 0.0331 | 0.0533 |

| During COVID-19 | 0.0194 | 0.0526 | 0.1843 | |

| During Russia–Ukraine War | 0.0227 | 0.0365 | 0.0722 | |

| FTSEMIB 30 | Pre-COVID-19 | 0.0226 | 0.0837 | 0.1475 |

| During COVID-19 | 0.0337 | 0.0788 | 0.2337 | |

| During Russia–Ukraine War | 0.0489 | 0.0872 | 0.1549 | |

| Nikkei | Pre-COVID-19 | 0.0062 | 0.0612 | 0.1415 |

| During COVID-19 | 0.0046 | 0.0616 | 0.1624 | |

| During Russia–Ukraine War | 0.0057 | 0.0529 | 0.0269 | |

| SP-TSX | Pre-COVID-19 | 0.0185 | 0.0131 | 0.0106 |

| During COVID-19 | 0.0369 | 0.0282 | 0.3302 | |

| During Russia–Ukraine War | 0.0523 | 0.0202 | 0.0325 |

| Indices | Period | β | HE | |

|---|---|---|---|---|

| S&P 500 | Pre-COVID-19 | −0.0640 | 0.4698 | 0.6696 |

| During COVID-19 | 0.0965 | 0.5337 | 0.7129 | |

| During Russia–Ukraine War | 0.3019 | 0.7632 | 0.6426 | |

| CAC40 | Pre-COVID-19 | −0.1660 | 0.5734 | 0.7266 |

| During COVID-19 | 0.0089 | 0.5936 | 0.6974 | |

| During Russia–Ukraine War | 0.1178 | 0.6452 | 0.6237 | |

| DAX30 | Pre-COVID-19 | −0.1721 | 0.5983 | 0.7295 |

| During COVID-19 | 0.0536 | 0.6178 | 0.6822 | |

| During Russia–Ukraine War | 0.1319 | 0.6795 | 0.6529 | |

| FTSE 100 | Pre-COVID-19 | −0.0617 | 0.5040 | 0.6084 |

| During COVID-19 | 0.0441 | 0.5302 | 0.6187 | |

| During Russia–Ukraine War | 0.0833 | 0.4810 | 0.4749 | |

| FTSEMIB 30 | Pre-COVID-19 | −0.2042 | 0.6747 | 0.8048 |

| During COVID-19 | 0.0176 | 0.6489 | 0.7282 | |

| During Russia–Ukraine War | 0.1650 | 0.7252 | 0.6810 | |

| Nikkei | Pre-COVID-19 | −0.1314 | 0.6011 | 0.7541 |

| During COVID-19 | 0.0326 | 0.5792 | 0.6044 | |

| During Russia–Ukraine War | −0.0200 | 0.5272 | 0.5727 | |

| SP-TSX | Pre-COVID-19 | 0.0157 | 0.3605 | 0.4368 |

| During COVID-19 | 0.1508 | 0.4072 | 0.7047 | |

| During Russia–Ukraine War | 0.3403 | 0.5622 | 0.3699 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Kayral, I.E.; Jeribi, A.; Loukil, S. Are Bitcoin and Gold a Safe Haven during COVID-19 and the 2022 Russia–Ukraine War? J. Risk Financial Manag. 2023, 16, 222. https://doi.org/10.3390/jrfm16040222

Kayral IE, Jeribi A, Loukil S. Are Bitcoin and Gold a Safe Haven during COVID-19 and the 2022 Russia–Ukraine War? Journal of Risk and Financial Management. 2023; 16(4):222. https://doi.org/10.3390/jrfm16040222

Chicago/Turabian StyleKayral, Ihsan Erdem, Ahmed Jeribi, and Sahar Loukil. 2023. "Are Bitcoin and Gold a Safe Haven during COVID-19 and the 2022 Russia–Ukraine War?" Journal of Risk and Financial Management 16, no. 4: 222. https://doi.org/10.3390/jrfm16040222