J. Risk Financial Manag., Volume 16, Issue 4 (April 2023) – 43 articles

Cover Story (view full-size image):

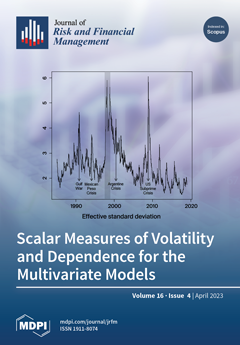

Variance and correlation matrices contain a multi-dimensional array of numbers, representing all the information about individual variabilities and pairwise covariabilities; however, it is difficult to interpret them in a concise way. We propose a scalar measure of summarizing the volatilities and correlations in the variance (or correlation) matrix into a single number, which is desirable for easy interpretation of the overall variance (or correlation) in the multivariate system. The scalar measures can be useful tools in many research areas of economics. They can be applied to the issue of regional market comovements during the financial crisis, and they can also be practical tools for fund managers to produce clear measurements of portfolio diversification effects and risk. View this paper

- Issues are regarded as officially published after their release is announced to the table of contents alert mailing list.

- You may sign up for e-mail alerts to receive table of contents of newly released issues.

- PDF is the official format for papers published in both, html and pdf forms. To view the papers in pdf format, click on the "PDF Full-text" link, and use the free Adobe Reader to open them.

Previous Issue

Next Issue