Towards a Truly Decentralized Blockchain Framework for Remittance

Abstract

:1. Introduction

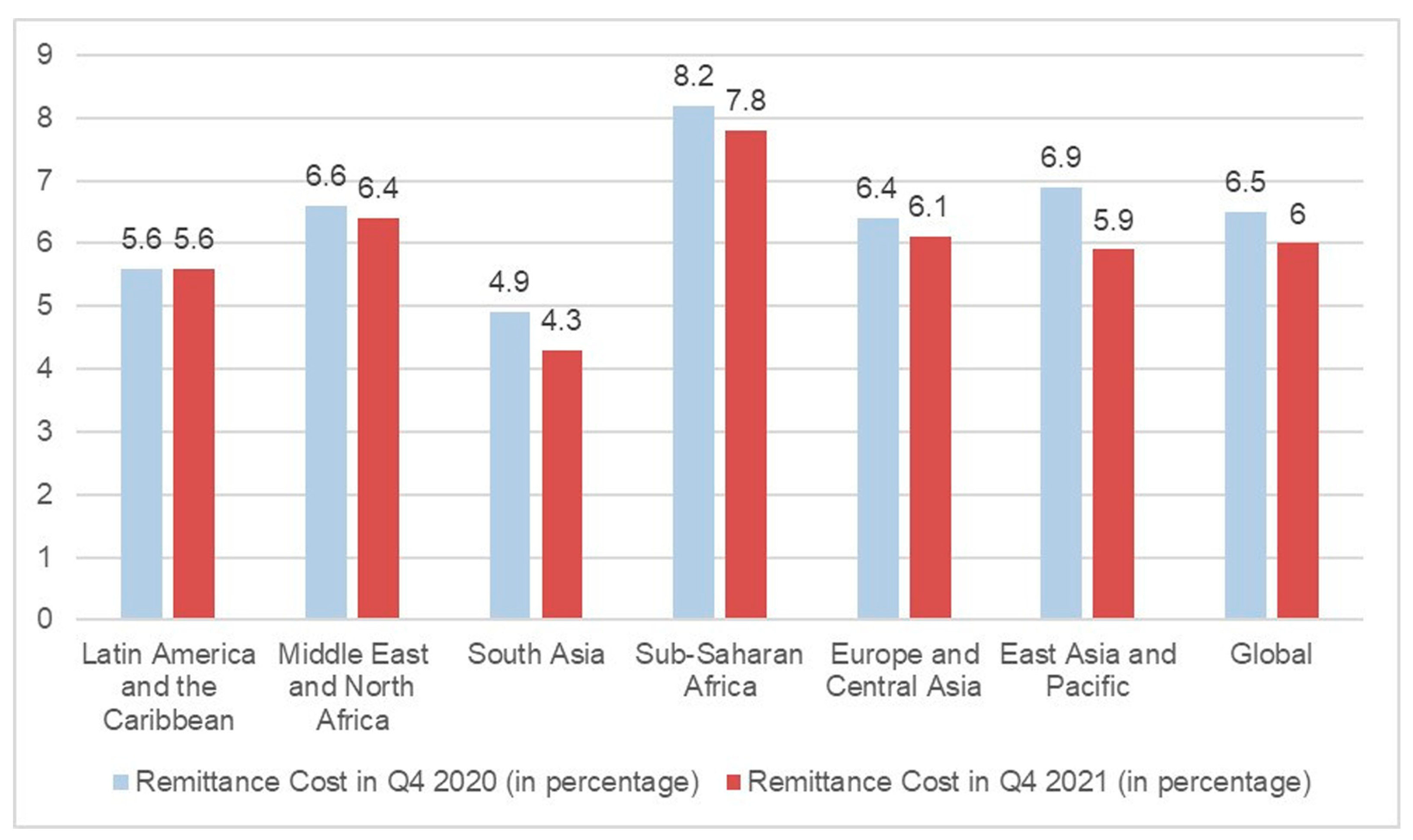

2. Remittance: A Global Economic Flywheel

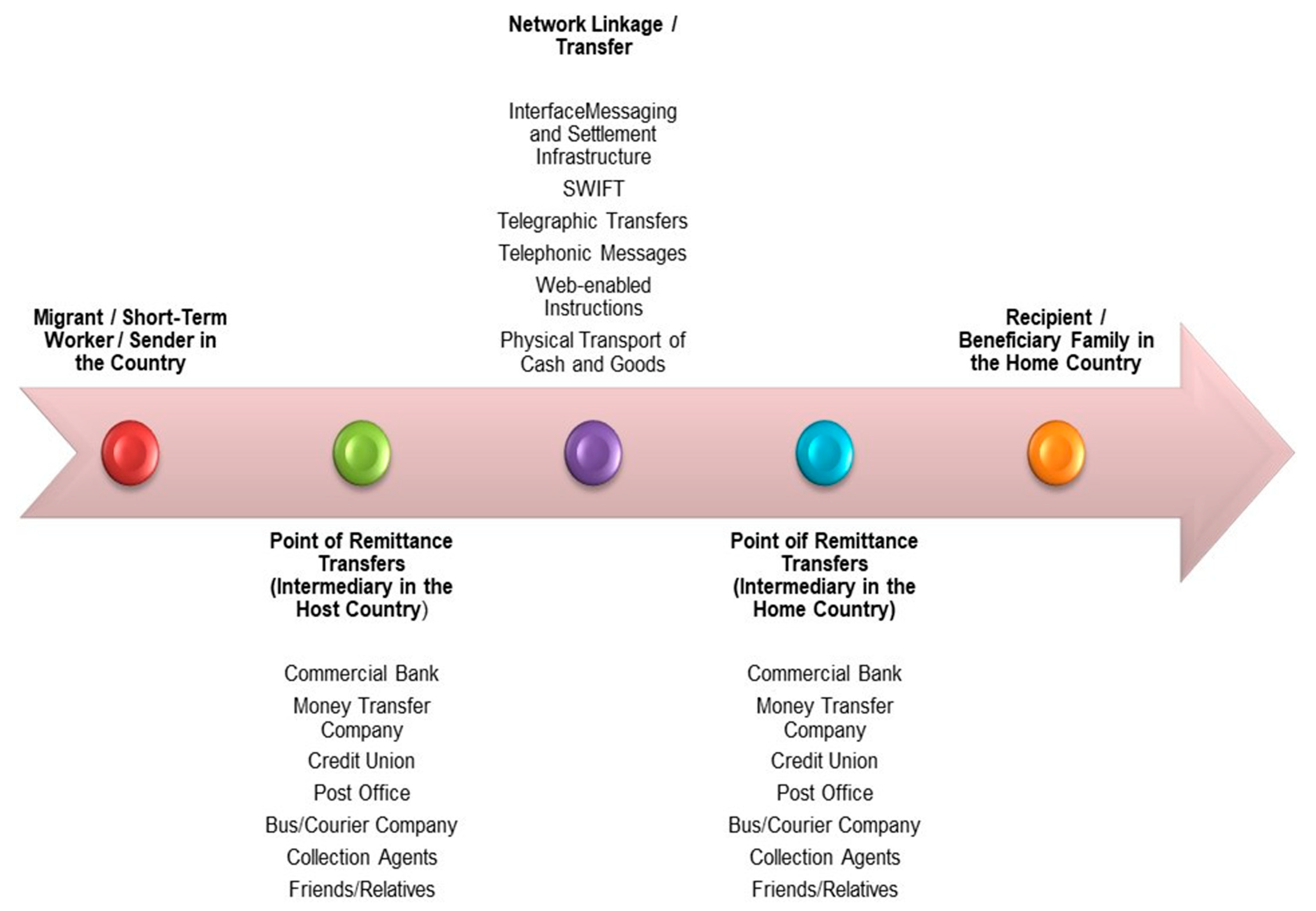

2.1. Remittance Mechanism

2.2. Remittance Drivers

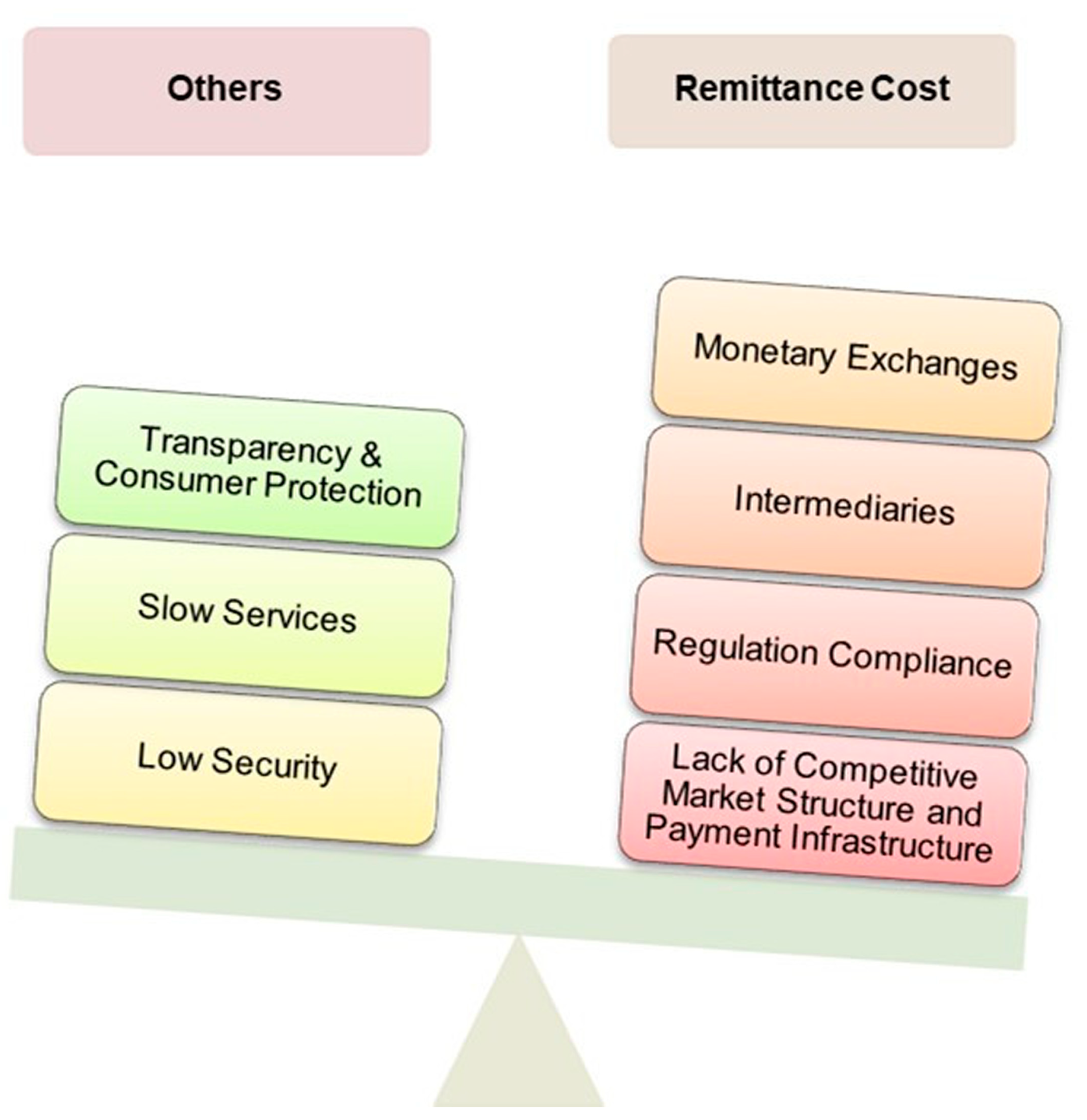

2.3. Remittance Market Characteristics

2.3.1. Monetary Exchanges

2.3.2. Intermediaries for International Payments

2.3.3. Price of Regulation and Compliance

2.3.4. Lack of Competitive Market Structure

2.3.5. Transparency and Consumer Protection

2.3.6. Payment System Infrastructure

2.3.7. Slow Services

2.3.8. Low Security

3. Remittance Models: Conventions and FinTechs

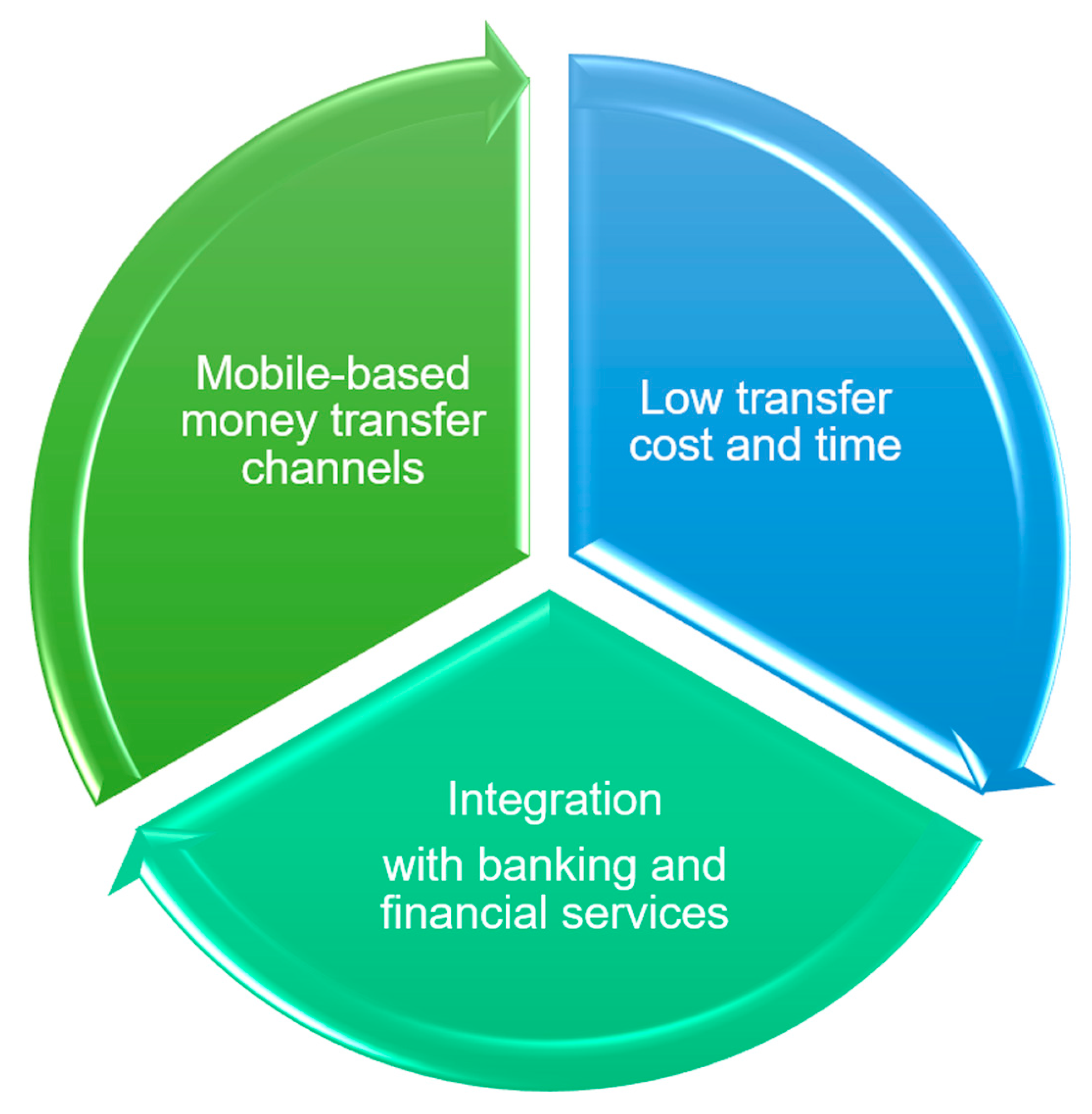

4. Remittances in the Era of Blockchain Technology

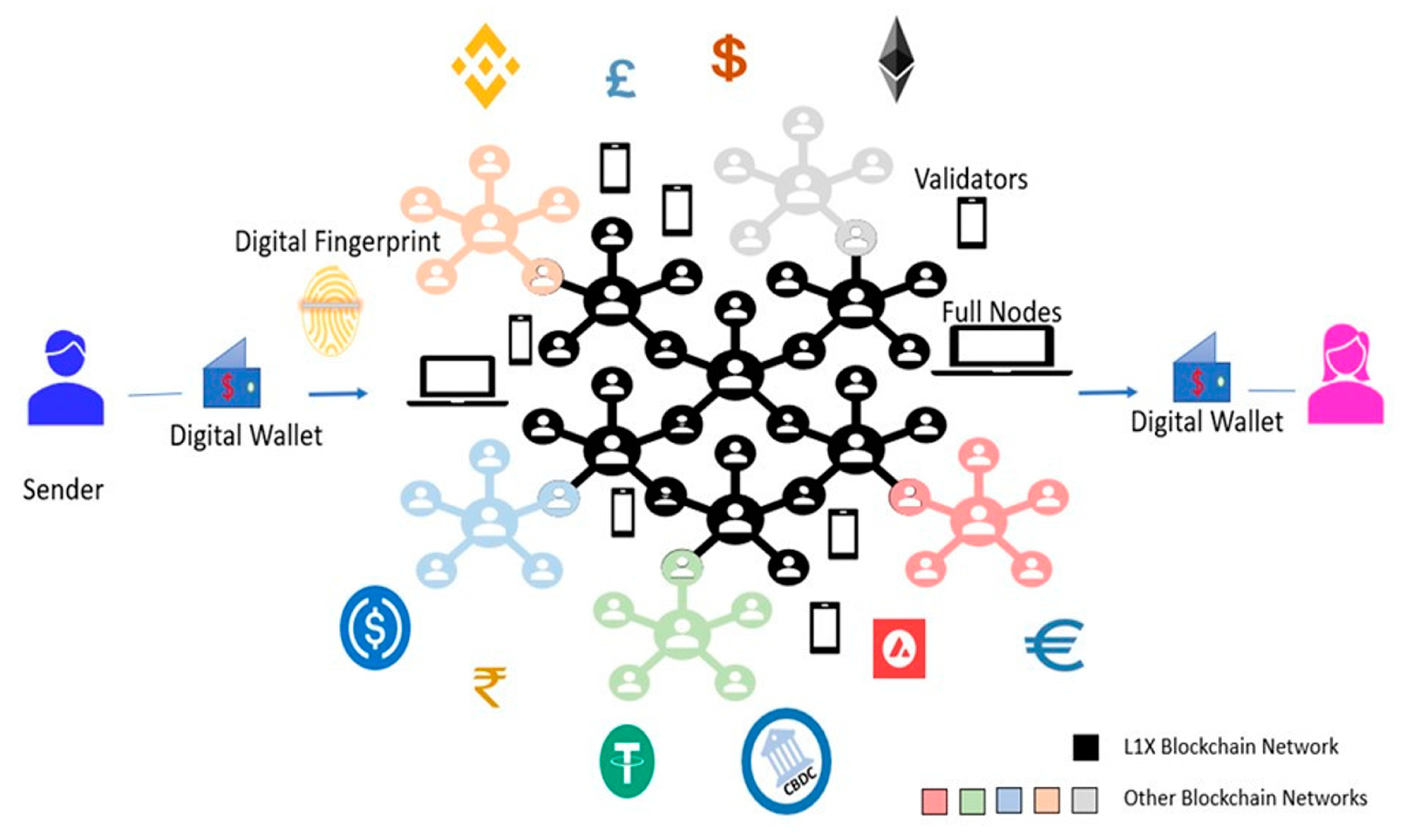

5. Conceptual Framework

- True Decentralization: Since the dependence on foundation-driven nodes for validation and consensus reduces the security and availability of the network, a truly decentralized network is the next big challenge.

- Scalability: Given the demand for massive remittance transactions worldwide, a scalable protocol to reduce transaction processing time and fees is required.

- Interoperability: Amalgamating across borders through cross-blockchain communications to facilitate seamless remittances.

- Digital Fingerprint: A unified digital identity recognized globally across blockchain networks, banks, and financial institutions.

- Wide Alternatives: Use of cryptocurrencies, stablecoins, or central bank digital currencies as an intermediary currency.

5.1. Prominent Features of Proposed Framework

- Blockchain-based cross-border payment architecture and framework, incorporating various needs of the remittance economy on L1X blockchain;

- L1X blockchain-powered payment solution (utilizing L1X scalable and interoperable solutions) that will improve transaction processing time and reduce transaction fees while keeping decentralization and security uncompromised;

- A digital wallet mechanism and cross-border payment channel that accepts, pays, and interoperates with multiple digital assets;

- Blockchain-based remittances that allow transfers using cryptocurrencies or stablecoins;

- An interoperable protocol that allows the use of intermediary currency in the background to facilitate remittances;

- Utilizing L1X technology to store digital fingerprints, enabling identification applicable to KYC for onboarding requirements.

5.2. Novel Features of Proposed Framework

5.3. Contribution of Proposed Framework

6. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- About MoneyGram International, Inc. 2022. MoneyGram. Available online: https://corporate.moneygram.com/about-moneygram (accessed on 20 September 2022).

- Andoni, Merlinda, Valentin Robu, David Flynn, Simone Abram, Dale Geach, David Jenkins, Peter McCallum, and Andrew Peacock. 2019. Blockchain Technology in the Energy Sector: A Systematic Review of Challenges and Opportunities. Renewable and Sustainable Energy Reviews 100: 143–74. [Google Scholar] [CrossRef]

- Anti-Money Laundering Principles for Correspondent Banking. 2014. The Wolfsberg Group. Available online: https://www.wolfsberg-principles.com/sites/default/files/wb/Wolfsberg-Correspondent-Banking-Principles-2014.pdf (accessed on 20 September 2022).

- Ardic, Oya, Hemant Baijal, Patrizia Baudino, Nana Yaa Boakye-Adjei, Jonathan Fishman, and Richard Audu Maikai. 2022. The Journey So Far: Making Cross Border Remittances Work for Financial Inclusion. Bank for International Settlements 2022, World Bank Group. June. Available online: https://www.bis.org/fsi/publ/insights43.pdf (accessed on 20 September 2022).

- Azzi, Rita, Rima Kilany Chamoun, and Maria Sokhn. 2019. The Power of a Blockchain-Based Supply Chain. Computers & Industrial Engineering 135: 582–92. [Google Scholar] [CrossRef]

- Beck, Thorsten, and María Soledad Martínez Pería. 2011. What Explains the Price of Remittances? An Examination Across 119 Country Corridors. The World Bank Economic Review 25: 105–31. [Google Scholar] [CrossRef]

- Become a Western Union Agent. 2022. Western Union Money Transfer. Available online: https://www.westernunion.com/li/en/become-agent.html (accessed on 20 September 2022).

- Bermeo-Almeida, Oscar, Mario Cardenas-Rodriguez, Teresa Samaniego-Cobo, Enrique Ferruzola-Gómez, Roberto Cabezas-Cabezas, and William Bazán-Vera. 2018. Blockchain in Agriculture: A Systematic Literature Review. In Technologies and Innovation. Edited by Rafael Valencia-García, Gema Alcaraz-Mármol, Javier Del Cioppo-Morstadt, Néstor Vera-Lucio and Martha Bucaram-Leverone. Communications in Computer and Information Science. Cham: Springer International Publishing, pp. 44–56. [Google Scholar] [CrossRef]

- BitPesa|Africa’s Crypto and BTC Exchange—Access the Deepest BTC Liquidity in Africa. 2022. Available online: https://www.bitpesa.co/ (accessed on 20 September 2022).

- Bitspark’s Bankless Ecosystem. 2023. Bitspark ZEPH. Available online: https://whitepaper.io/document/486/bitspark-whitepaper (accessed on 20 September 2022).

- Bodkhe, Umesh, Sudeep Tanwar, Karan Parekh, Pimal Khanpara, Sudhanshu Tyagi, Neeraj Kumar, and Mamoun Alazab. 2020. Blockchain for Industry 4.0: A Comprehensive Review. IEEE Access 8: 79764–800. [Google Scholar] [CrossRef]

- Brilliantova, Vlada, and Thomas Wolfgang Thurner. 2019. Blockchain and the Future of Energy. Technology in Society 57: 38–45. [Google Scholar] [CrossRef]

- Chase, Brad, and Ethan MacBrough. 2018. Analysis of the XRP Ledger Consensus Protocol. Ripple Research. arXiv. Available online: https://arxiv.org/pdf/1802.07242.pdf (accessed on 20 September 2022).

- Coins.Ph. 2023. Available online: https://coins.ph/ (accessed on 20 March 2023).

- De, Nikhilesh. 2020. Bitspark Fades Out Following COO Maxine Ryan’s Departure. Available online: https://www.coindesk.com/markets/2020/02/04/bitspark-fades-out-following-coo-maxine-ryans-departure/ (accessed on 20 September 2022).

- Demestichas, Konstantinos, Nikolaos Peppes, Theodoros Alexakis, and Evgenia Adamopoulou. 2020. Blockchain in Agriculture Traceability Systems: A Review. Applied Sciences 10: 4113. [Google Scholar] [CrossRef]

- Deng, Qing. 2020. Application Analysis on Blockchain Technology in Cross-Border Payment. In Advances in Economics, Business and Management Research. Amsterdam: Atlantis Press SARL, vol. 126, pp. 287–95. [Google Scholar] [CrossRef] [Green Version]

- Distributed Ledger Technology and Blockchain. 2017. World Bank Group. Available online: https://documents1.worldbank.org/curated/en/177911513714062215/pdf/122140-WP-PUBLIC-Distributed-Ledger-Technology-and-Blockchain-Fintech-Notes.pdf (accessed on 20 September 2022).

- Dorri, Ali, Salil S. Kanhere, and Raja Jurdak. 2017. Towards an Optimized BlockChain for IoT. In Proceedings of the Second International Conference on Internet-of-Things Design and Implementation. Pittsburgh: ACM, pp. 173–78. [Google Scholar] [CrossRef] [Green Version]

- FAQ Your Questions about XRPL, Answered. 2022. XRP. Available online: https://xrpl.org/faq.html (accessed on 20 September 2022).

- Fernández-Caramés, Tiago M., and Paula Fraga-Lamas. 2019. A Review on the Application of Blockchain to the Next Generation of Cybersecure Industry 4.0 Smart Factories. IEEE Access 7: 45201–18. [Google Scholar] [CrossRef]

- Flore, Massimo. 2018. How Blockchain-Based Technology Is Disrupting Migrants’ Remittances: A Preliminary Assessment. EUR 29492 EN vols. JRC Publications Repository JRC113484. Luxembourg: Publications Office of the European Union. Available online: https://publications.jrc.ec.europa.eu/repository/handle/JRC113484 (accessed on 20 September 2022).

- Future of Cross-Border Payments: Blockchain Remittance Explained. 2022. Liquid-Technology, Industry (Blog). Available online: https://blog.liquid.com/remittance-blockchain-crypto#TheProblemswiththeCurrentRemittanceChannels (accessed on 20 September 2022).

- General Principles for International Remittance Services. 2007. Committee on Payment and Settlement Systems, The World Bank. Available online: https://www.bis.org/cpmi/publ/d76.pdf (accessed on 20 September 2022).

- Hasselgren, Anton, Katina Kralevska, Danilo Gligoroski, Sindre A. Pedersen, and Arild Faxvaag. 2020. Blockchain in Healthcare and Health Sciences—A Scoping Review. International Journal of Medical Informatics 134: 104040. [Google Scholar] [CrossRef] [PubMed]

- Hölbl, Marko, Marko Kompara, Aida Kamišalić, and Lili Nemec Zlatolas. 2018. A Systematic Review of the Use of Blockchain in Healthcare. Symmetry 10: 470. [Google Scholar] [CrossRef] [Green Version]

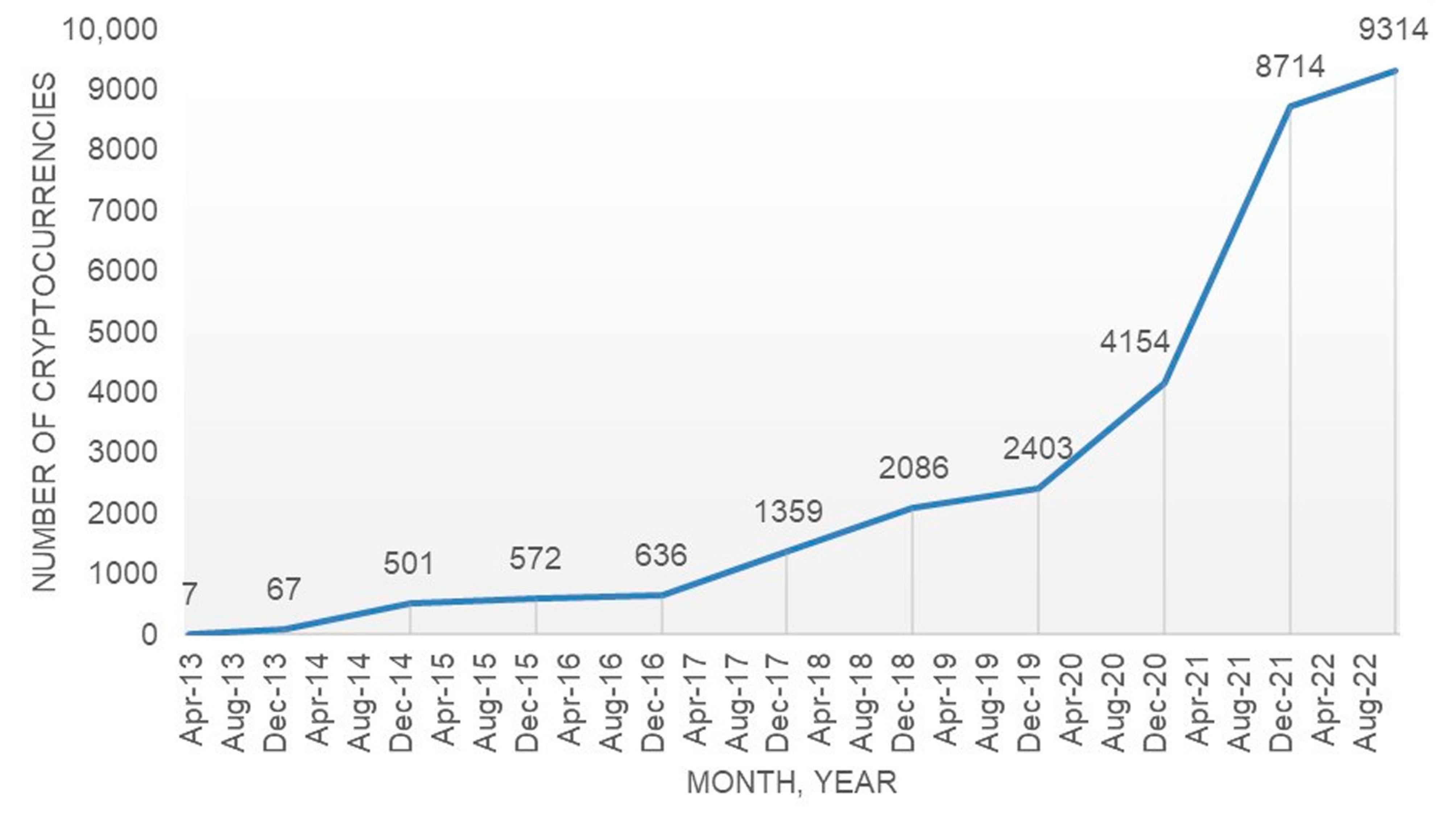

- Howarth, Josh. 2022. How Many Cryptocurrencies Are There in 2023? Exploding Topis (Blog). Available online: https://explodingtopics.com/blog/number-of-cryptocurrencies (accessed on 30 November 2022).

- International Money Transfer—Send Money Online|WorldRemit. 2022. Available online: https://www.worldremit.com/en (accessed on 20 September 2022).

- International Money Transfers, Western Union India. 2022. Western Union Money Transfer. Available online: https://www.westernunion.com/in/en/home.html (accessed on 20 September 2022).

- Jain, Rajeev, Dhirendra Gajbhiye, and Soumasree Tewari. 2018. Globalising People: India’s Inward Remittances in 2016–2017. Division of International Finance, Department of Economic and Policy Research (DEPR), Reserve Bank of India. Available online: https://rbidocs.rbi.org.in/rdocs/Bulletin/PDFs/1AR_14112018071B9474B5D74DDC91FC8AA015C5A360.PDF (accessed on 20 September 2022).

- Kaarmann, Kristo. 2021. Modern Slavery and Human Trafficking Statement for Wise. WISE. Available online: https://wise.com/public-resources/assets/public-navigation/modern_slavery_statement.pdf (accessed on 20 September 2022).

- Kagan, Julia. 2022. What Is a Wire Transfer? How It Works, Safety, and Fees. Investopedia. August 17. Available online: https://www.investopedia.com/terms/w/wiretransfer.asp (accessed on 20 September 2022).

- Kim, Minjeong, Yujin Kwon, and Yongdae Kim. 2019. Is Stellar As Secure As You Think? In Proceedings of the 2019 IEEE European Symposium on Security and Privacy Workshops (EuroS&PW), Stockholm, Sweden, 17–19 June. [Google Scholar] [CrossRef] [Green Version]

- Know Your Customer Surveys Reveal Escalating Costs and Complexity. 2016. Thomson Reuters. Available online: https://www.thomsonreuters.com/en/press-releases/2016/may/thomson-reuters-2016-know-your-customer-surveys.html (accessed on 20 September 2022).

- Lu, Cindy. 2022. Cryptocurrency and Digital Assets: A Positive Tool for Economic Growth in Developing Countries. SSRN Electronic Journal. [Google Scholar] [CrossRef]

- Lumens-Stellar. 2022. Stellar. Available online: https://stellar.org/lumens (accessed on 20 September 2022).

- McGhin, Thomas, Kim-Kwang Raymond Choo, Charles Zhechao Liu, and Debiao He. 2019. Blockchain in Healthcare Applications: Research Challenges and Opportunities. Journal of Network and Computer Applications 135: 62–75. [Google Scholar] [CrossRef]

- Money without Borders. Annual Report and Accounts 2022. Wise. 2022. Available online: https://lienzo.s3.amazonaws.com/images/2aeb66e27009d06acbd6f46f746feae2-WIS001_Book.pdf (accessed on 20 September 2022).

- Moos, Mitchell. 2020. Is XRP Decentralized? Ripple’s Involvement in the Cryptocurrency. Crypto Briefing (Blog). March 31. Available online: https://cryptobriefing.com/is-xrp-decentralized-ripples-involvement-cryptocurrency/ (accessed on 20 September 2022).

- Nakamoto, Satoshi. 2019. The White Paper. Edited by Ben Vickers. IGNOTA. Available online: https://ignota.org/products/the-white-paper (accessed on 20 September 2022).

- Panarello, Alfonso, Nachiket Tapas, Giovanni Merlino, Francesco Longo, and Antonio Puliafito. 2018. Blockchain and IoT Integration: A Systematic Survey. Sensors 18: 2575. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Products and Services. 2022. MoneyGram. Available online: https://corporate.moneygram.com/products-and-services (accessed on 20 September 2022).

- Qiu, Tianyi, Ruidong Zhang, and Yuan Gao. 2019. Ripple vs. SWIFT: Transforming Cross Border Remittance Using Blockchain Technology. In Procedia Computer Science, Science Direct. Amsterdam: Elsevier, vol. 147, pp. 428–34. [Google Scholar] [CrossRef]

- Queiroz, Maciel M., Renato Telles, and Silvia H. Bonilla. 2019. Blockchain and Supply Chain Management Integration: A Systematic Review of the Literature. Supply Chain Management: An International Journal 25: 241–54. [Google Scholar] [CrossRef]

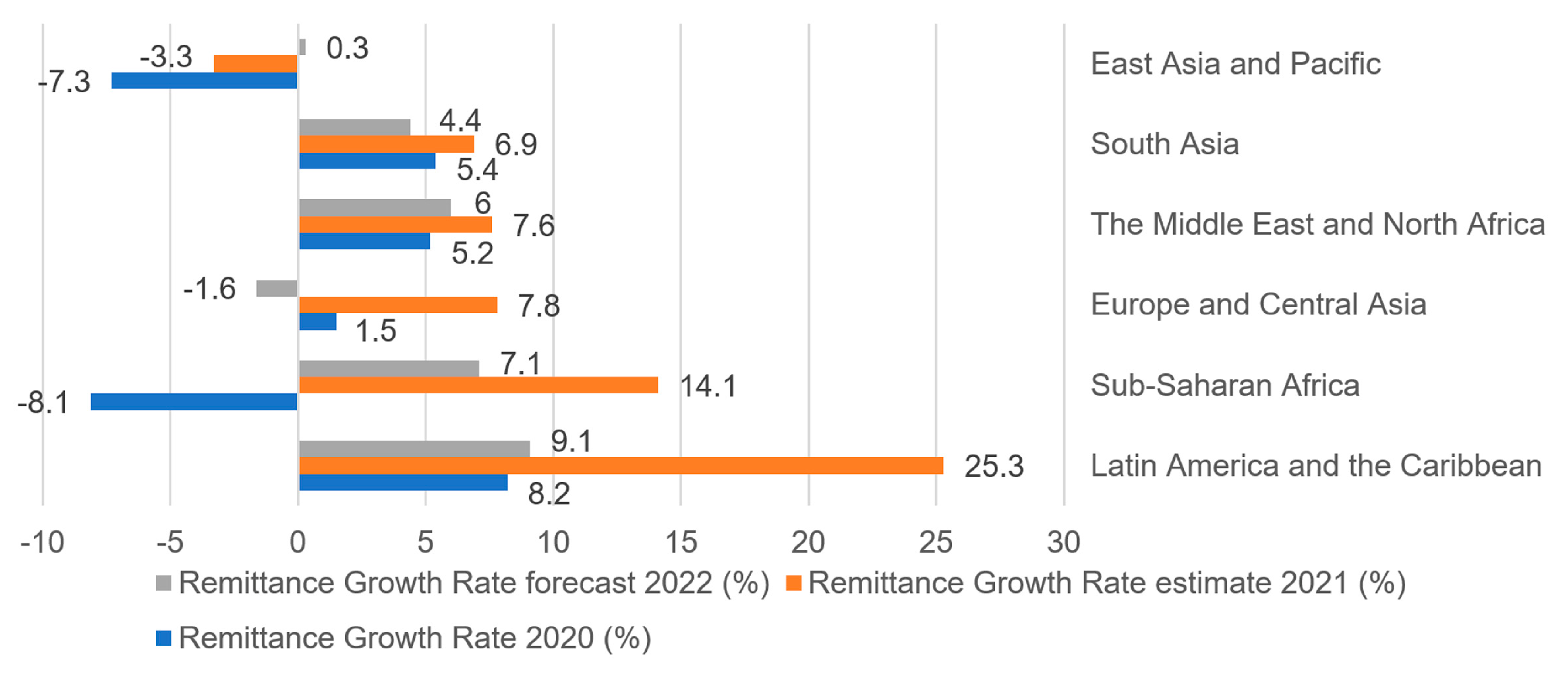

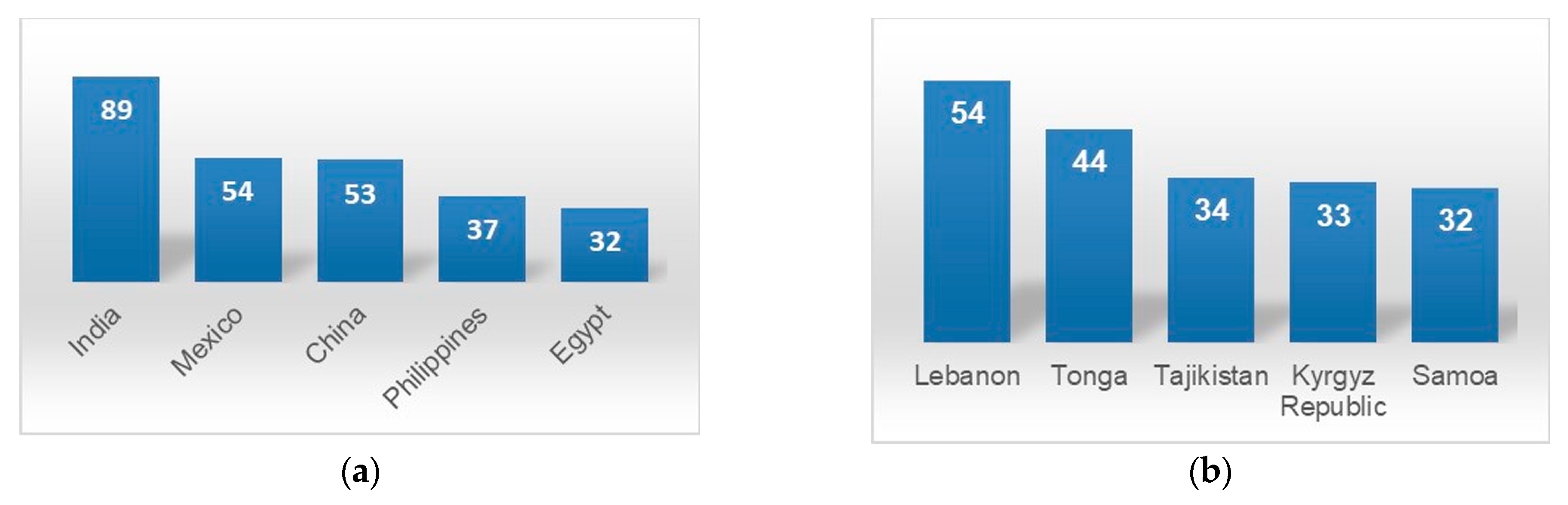

- Ratha, Dilip, Eung Ju Kim, Sonia Plaza, Elliott Riordan, and Vandana Chandra. 2022. Migration and Development Brief 36: A War in a Pandemic: Implications of the Russian Invasion of Ukraine and the COVID-19 Crisis on Global Governance of Migration and Remittance Flows. KNOMAD-World Bank. Available online: https://www.knomad.org/publication/migration-and-development-brief-36 (accessed on 20 September 2022).

- Rebit—Crunchbase Company Profile & Funding. n.d. Crunchbase. Available online: https://www.crunchbase.com/organization/rebit-2 (accessed on 20 March 2023).

- Rebit.Ph. 2023. Tracxn. Available online: https://tracxn.com/d/companies/rebit.ph/__n4cHrmD3KFLuyjrcjW3CSCTsTTVP4i1auTObd8sFnY0 (accessed on 20 March 2023).

- Recent Trends in Correspondent Banking Relationships: Further Considerations. 2017. IMF. Available online: https://www.imf.org/en/Publications/Policy-Papers/Issues/2017/04/21/recent-trends-in-correspondent-banking-relationships-further-considerations (accessed on 20 September 2022).

- Reducing Remittance Fees. Global Economic Prospects 2006. World Bank. 2005. Available online: https://documents1.worldbank.org/curated/fr/507301468142196936/841401968_200510319014045/additional/Global-economic-prospects-2006-economic-implications-of-remittances-and-migration.pdf (accessed on 20 September 2022).

- Rella, Ludovico. 2019. Blockchain Technologies and Remittances: From Financial Inclusion to Correspondent Banking. Frontiers, Frontiers in Blockchain 2: 14. [Google Scholar] [CrossRef] [Green Version]

- Remittance Flows Register Robust 7.3 Percent Growth in 2021. Text/HTML. 2021. World Bank. Available online: https://www.worldbank.org/en/news/press-release/2021/11/17/remittance-flows-register-robust-7-3-percent-growth-in-2021 (accessed on 20 September 2022).

- Remittance Market: Global Opportunity Analysis and Industry Forecast, 2019–2026. 2020. Allied Market Research, April. Available online: https://www.alliedmarketresearch.com/remittance-market (accessed on 20 September 2022).

- Remittances Matter: 8 Facts You Don’t Know about the Money Migrants Send Back Home. 2019. United Nations Department of Economic and Social Affairs. Available online: https://www.un.org/development/desa/en/news/population/remittances-matter.html (accessed on 20 September 2022).

- Ria Money Transfer—Send Money Online to over 165 Countries Instantly. 2022. Ria. Available online: https://app.riamoneytransfer.com/en-us/ (accessed on 20 September 2022).

- Rühmann, Friederike, Sai Aashirvad Konda, Paul Horrocks, and Nina Taka. 2020. Can Blockchain Technology Reduce the Cost of Remittances? OECD Development Co-Operation. Available online: https://www.oecd-ilibrary.org/docserver/d4d6ac8f-en.pdf?expires=1676616987&id=id&accname=guest&checksum=BCF1F8BD7F580120355A7683265D99FB#:~:text=The%20characteristics%20of%20Bitcoin%20enabling,systems%20including%20speed%20and%20cost (accessed on 20 September 2022).

- Run a Core Node Overview. 2022. Stellar. Available online: https://developers.stellar.org/docs/run-core-node (accessed on 20 September 2022).

- Sajja, Guna Sekhar, Kantilal Pitambar Rane, Khongdet Phasinam, Thanwamas Kassanuk, Ethelbert Okoronkwo, and P. Prabhu. 2021. Towards Applicability of Blockchain in Agriculture Sector. Materials Today: Proceedings. [Google Scholar] [CrossRef]

- Scott, Brett. 2016. How Can Cryptocurrency and Blockchain Technology Play a Role in Building Social and Solidarity Finance? UNRISD. February 10. Available online: https://www.unrisd.org/en/library/publications/how-can-cryptocurrency-and-blockchain-technology-play-a-role-in-building-social-and-solidarity-finan (accessed on 20 September 2022).

- SEC Charges Ripple and Two Executives with Conducting $1.3 Billion Unregistered Securities Offering. 2020, U.S. Securities and Exchange Commission. Available online: https://www.sec.gov/news/press-release/2020-338 (accessed on 20 September 2022).

- Sending Money from Tanzania to Kenya—Remittance Prices Worldwide. Remittance Prices Worldwide. 2021. December. Available online: https://remittanceprices.worldbank.org/corridor/Tanzania/Kenya (accessed on 20 September 2022).

- Soufaih, Amine. 2020. Revolutionizing the International Remittance Payment Industry Using Cryptocurrency and Blockchain-Based Technology. Social Impact Research Experience (SIRE), 75. Available online: https://repository.upenn.edu/sire/75 (accessed on 20 September 2022).

- Stellar Development Foundation. 2019. May 15th Network Halt. Stellar Developers (Blog). Available online: https://medium.com/stellar-developers-blog/may-15th-network-halt-a7b933103984. (accessed on 20 September 2022).

- Stellar Network Visibility. 2022. Stellarbeat, September. Available online: https://stellarbeat.io/?network=public. (accessed on 20 September 2022).

- Suki, Lenora. 2007. Competition and Remittances in Latin America: Lower Prices and More Efficient Markets. Organization for Economic Cooperation and Development and Inter American Development Bank. Available online: https://www.oecd.org/daf/competition/prosecutionandlawenforcement/38821426.pdf (accessed on 20 September 2022).

- Swift—About Us. 2023. Swift. Available online: https://www.swift.com/about-us (accessed on 17 February 2023).

- The Decline in Access to Correspondent Banking Services in Emerging Markets: Trends, Impacts, and Solutions. 2018. Working Paper. Washington, DC: World Bank Group. [CrossRef]

- The Digital Currency Shift—September 2021. 2023. PYMNTS. Available online: https://www.pymnts.com/study/the-cross-border-remittances-report-cryptocurrency-digital-payments/ (accessed on 20 March 2023).

- Uddin, Md Ashraf, Andrew Stranieri, Iqbal Gondal, and Venki Balasubramanian. 2021. A Survey on the Adoption of Blockchain in IoT: Challenges and Solutions. Blockchain: Research and Applications 2: 100006. [Google Scholar] [CrossRef]

- Wang, Qiang, and Min Su. 2020. Integrating Blockchain Technology into the Energy Sector—From Theory of Blockchain to Research and Application of Energy Blockchain. Computer Science Review 37: 100275. [Google Scholar] [CrossRef]

- What Cryptocurrencies Are Available on Coins.Ph? 2023. Coins.Ph Help Center. Available online: https://support.coins.ph/hc/en-us/articles/900006877303-What-cryptocurrencies-are-available-on-Coins-ph- (accessed on 20 March 2023).

- WorldRemit About Us. 2022. WorldRemit. Available online: https://www.worldremit.com/en/about-us (accessed on 20 September 2022).

- XRP Overview Your Questions About XRP, Answered. 2022. XRP. Available online: https://xrpl.org/xrp-overview.html (accessed on 20 September 2022).

- XRP Price Today, XRP to USD Live, Marketcap and Chart. 2022. CoinMarketCap. Available online: https://coinmarketcap.com/currencies/xrp/ (accessed on 20 September 2022).

- XRPL Explorer|Network. 2022. XRP. Available online: https://livenet.xrpl.org/network/nodes (accessed on 20 September 2022).

- Yen, David. 2017. Blockchain-Based FX/Treasury Solution in Africa. BitPesa. October. Available online: http://www.gtreview.com/wp-content/uploads/2017/03/Classroom-style-breakout_How-is-technology-enabling-African-trade.pdf (accessed on 20 September 2022).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Ripple | Stellar | |

|---|---|---|

| Cryptocurrency | XRP | XLM |

| Model | Deflationary | Inflationary |

| Governance | Centralized | Decentralized |

| Network | Permissioned | Permissionless |

| Consensus Protocol | Ripple Consensus Protocol | Stellar Consensus Protocol |

| Consensus Mechanism | Probabilistic Voting | A decentralized version of Practical Byzantine Fault Tolerance |

| Target Group | Bank and financial institutions | Individuals |

| Target Market | International Bank Transfer | Micro Payments, Remittances |

| Focused on | Improving international transactions among financial institutions | Inexpensive financial services for people in the developing nation |

| Organization | Profit-driven | Non-profit driven |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Coutinho, K.; Khairwal, N.; Wongthongtham, P. Towards a Truly Decentralized Blockchain Framework for Remittance. J. Risk Financial Manag. 2023, 16, 240. https://doi.org/10.3390/jrfm16040240

Coutinho K, Khairwal N, Wongthongtham P. Towards a Truly Decentralized Blockchain Framework for Remittance. Journal of Risk and Financial Management. 2023; 16(4):240. https://doi.org/10.3390/jrfm16040240

Chicago/Turabian StyleCoutinho, Kevin, NeerajKumari Khairwal, and Pornpit Wongthongtham. 2023. "Towards a Truly Decentralized Blockchain Framework for Remittance" Journal of Risk and Financial Management 16, no. 4: 240. https://doi.org/10.3390/jrfm16040240