1. Introduction

With more than 300 million estimated (verified) users worldwide, the phenomenon of cryptocurrency has reached a state of non-negligible societal relevance (

Crypto.com 2022). It has the potential to disrupt traditional financial systems and has already begun to change the way we think about money and transactions (

Cong and He 2019;

Cong et al. 2021). While still representing a relatively new and rapidly evolving technology, cryptocurrency has gained a significant following and is being increasingly accepted as a legitimate form of payment by merchants and other organizations (

Holotiuk et al. 2017;

Jonker 2019), even in nation states such as El Salvador (

Alvarez et al. 2022). However, cryptocurrency has also faced controversy and regulatory challenges, and its future remains uncertain (

Chokor and Alfieri 2021).

The adoption of cryptocurrency as a means of payment and store of value varies widely around the world (

Bhimani et al. 2022;

Saiedi et al. 2021). Some countries have taken a positive approach to cryptocurrency and have implemented regulatory frameworks to support its use, while others have taken a more cautious or negative approach and have imposed restrictions or outright bans on its use (

Silva and da Silva 2022). In general, the adoption of cryptocurrency has been driven by a combination of technological innovation, increasing awareness and understanding of cryptocurrency, and the potential benefits it offers, such as reduced transaction costs, faster transaction times and promoted financial inclusion.

Cryptocurrency markets are permeated with ideological statements and narratives constituting alternative, decentralized and censorship-resistant financial and economic systems (

Steinmetz 2023). One of the most important narratives in recent years was that cryptocurrency in general, and Bitcoin in particular, may serve as “safe-haven” assets to protect against inflation. While Bitcoin itself is subject to volatility and showcases pronounced correlations with other established financial markets (e.g.,

Ha and Nham 2022), it may still be perceived as trustworthy or the lesser evil in comparison to domestic fiat currency suffering from severe inflation.

Despite the Turkish government having banned cryptocurrency payments as a measure to protect the sovereignty of the Turkish lira in April 2021 (

TCMB 2021), Turkey stands out from other geographies with a very high cryptocurrency ownership rate between 16 to 25%, which is double the European and US average (

de Best 2022;

Exton and Doidge 2018;

Paribu 2021). This makes Turkey a particularly interesting case to study cryptocurrency owners and their motivations. Furthermore, in December 2021, Turkey announced plans to further regulate cryptocurrencies, for, among other things, combating capital flight by restricting access to foreign cryptocurrency exchanges. However, a corresponding bill to that plan was postponed (

Tamac and Öz 2022).

Turkey is considered an emerging market (

MSCI 2022) and has experienced high growth rates between 2002 and 2017 causing a growing upper-middle-income class and attracting foreign capital investments (

The World Bank 2022). In political terms,

Öniş and Yalikun (

2021) describe that Turkey has experienced significant economic and democratization reforms during 2002 and 2007, followed by a turn towards a more centralized and top-down system since 2018. Furthermore,

Öniş and Yalikun (

2021) outline that the Turkish government is increasingly seeking to shift partnerships from the West towards China, which are perceived to embody an important political dimension with regards to manifesting the Turkish government’s domestic political power and international legitimacy. The Turkish lira has experienced phases of high inflation in the past and its value, i.e., against the US dollar, has depreciated extraordinarily since 2016 (

Guler 2020), resulting in increased currency risks for investors and citizens. As of September 2022, Turkey’s inflation rate soared to 83.5%, which is the highest rate since July 1998 (

TUIK 2022a). Potential reasons for the prevailing negative investment sentiment and consumer confidence in the country include Turkey’s domestic monetary policy (

Daragahi 2018) and the erosion of central bank independence in Turkey (

Demiralp and Demiralp 2019). While Turkey’s economy grew by 11% in 2021,

Orhangazi and Yeldan (

2021) highlight that several domestic and external factors have caused financial and economic turbulences and disclosed systematic vulnerabilities. They further argue that Turkey’s economy suffers from structural problems and intrinsic instabilities by its economic growth model, which depends on foreign capital inflows and increasing indebtedness. The political, fiscal and economic situation in Turkey has negatively affected consumer confidence since 2018 with the lowest ever recorded indicator in early 2022 (

TUIK 2022b). It is conceivable that the comparably high ownership rates of cryptocurrency in Turkey are the result of the high inflation of the Turkish lira (

Sivrikaya 2020) and general economic insecurity causing Turkish consumers’ confidence to erode, despite cryptocurrencies often being fairly volatile themselves (e.g.,

Walther et al. 2019).

At this point, however, it is unclear whether Turkish consumers buy into cryptocurrencies for speculating, investing, means of payment or capital preservation. Although the current literature already covers diverse aspects of cryptocurrency adoption, e.g., cryptocurrency users in different countries, usage patterns and motives (see

Steinmetz et al. (

2021) for an overview), none of these studies focus on Turkey in particular. Given the diversity of influential factors for cryptocurrency adoption (

Alnasaa et al. 2022;

Bhimani et al. 2022), it is inauspicious to draw conclusions on cryptocurrency users in emerging markets based on research that is predominantly focused on Western economies. Against the backdrop of Turkey’s outlined situation, addressing the research gap about Turkish cryptocurrency users and use foreshadows unique insights about the diffusion and adoption of this technology among emerging markets in general.

Based on a dataset of 715 Turkish cryptocurrency owners from 2021, we applied exploratory factor analysis to identify and differentiate user profiles and then empirically analyze the extent to which characteristics, such as demographics, ideology, purchase intention and the use of domestic or foreign exchanges, drive respective user groups. The methodological approach resembles existing studies with similar research questions but other thematic areas (e.g.,

Fisch et al. 2021;

Pierrakis 2019).

From a theoretical point of view, our study can be placed in the context of the self-determination theory (SDT) (

Deci and Ryan 1985), a framework that assesses the extent to which human behavior is driven by internal (e.g., ideological beliefs) or external (e.g., financial returns) motivation. SDT explains how people’s inherent growth tendencies and psychological needs for competence, relatedness and autonomy contribute to their well-being and personal development. The theory asserts that the satisfaction of these basic psychological needs leads to increased intrinsic motivation, which in turn leads to better overall functioning, well-being, and performance. In contrast, the frustration of these needs leads to decreased intrinsic motivation and poorer functioning (

Deci and Ryan 1985). The SDT has been widely applied in a variety of contexts, including education (e.g.,

Niemiec and Ryan 2009), sport (e.g.,

Vlachopoulos et al. 2000) and healthcare (e.g.,

Ng et al. 2012), and has been shown to be a robust predictor of a wide range of positive outcomes. By unraveling different ownership profiles, we can assess to what degree the actual use cases (e.g., payments, lending, short-term speculation or long-term investment) drive certain groups and the degree to which ideology or national and foreign cryptocurrency exchange usage drive group affiliations.

Furthermore, this study aims to contribute to the literature on individual investors in general (e.g.,

Barber and Odean 2013) and on cryptocurrency users in particular (e.g.,

Ante et al. 2022). Because cryptocurrency is still considered a novel phenomenon which is, despite its rapid innovation capacities, at an early development stage, we contribute to research on the diffusion of innovations, i.e., how, why and at what rate new ideas and technologies spread (

Rogers 2003). More precisely, our results contribute to the understanding of lead users and markets, where Turkish cryptocurrency users may pioneer the use of cryptocurrency for their needs and similar emerging markets follow (

Beise and Cleff 2004;

von Hippel 1986). Lastly, the results may provide informative regarding the current regulatory debate in Turkey and help cryptocurrency service providers to better understand their customers.

This article proceeds as follows. In

Section 2, data and samples, as well as the empirical approach, are described.

Section 3 includes correlations and the results of factor analysis and subsequent regression analysis.

Section 4 contains a discussion of the results and

Section 5 concludes.

2. Materials and Methods

2.1. Data and Sample Description

The survey data analyzed in this study were collected by cryptocurrency data provider CoinGecko (

coingecko.com) between 27 January and 8 February 2021, via computer-assisted self-interviewing (CASI). It was distributed via CoinGecko’s geo-targeted website, the website and social media channels of Turkish cryptocurrency news website Kriptokoin and the Turkish YouTube channels of key opinion leaders (KOLs) Alp işik (

youtube.com/@Alp) and Kripto sözlük (

youtube.com/channel/UC5rV0QEGbv0Y-umDwshs_HA). The data were used to publish a market report named

Cryptocurrency Awareness in Turkey 2021 (

CoinGecko 2021) that provides descriptive statistics on demographics, usage and attitudes with regard to cryptocurrencies. In addition, a methodology document describes the survey questionnaire, as well as the processes of quality assurance and data preparation (

Azmi 2021). A total of 1124 people participated in the survey, of which 745 (66%) completed the questionnaire. Of these 745 respondents, 715 stated that they currently own cryptocurrency.

The survey data include information on self-assessed internal and external motivations of individuals, as well as data describing their technical and financial literacy. Based on the data, we created a set of eight variables that were used for exploratory factor analysis with the goal of reducing complexity in the data and uncovering previously hidden connections between individuals. The variables included dummy variables if respondents used cryptocurrencies for investment/trade or payments/buying items, a variable indicating their technological literacy proxied via the respondents’ affirmation about the ability to read computer code, as well as a variable indicating their financial literacy proxied via the number of different asset types they owned. Furthermore, it included respondents’ cryptocurrency experiences proxied via the first time an individual purchased cryptocurrency (i.e., the number of years since the first purchase), their cryptocurrency knowledge in terms of the number of different cryptocurrencies known, their trading frequency (i.e., how often they manage their portfolio) and finally a self-assessed score of their risk-taking attitude.

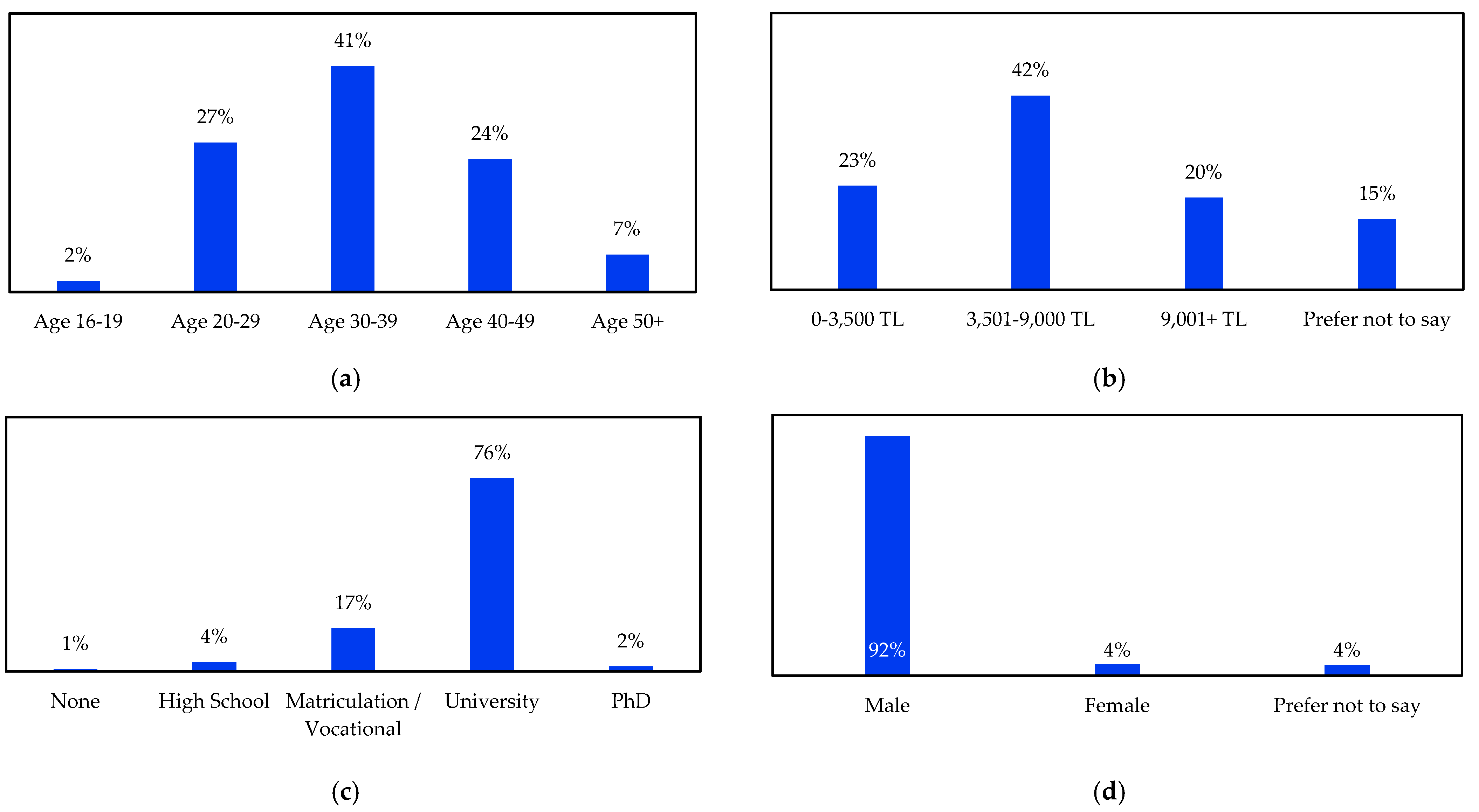

Of the 715 Turkish cryptocurrency owners, about 92% were male, 4% were female and the rest did not provide any information (cf.

Figure 1). The largest percentage of respondents (41%) were between 30 and 39 years old and had a university degree (77%). The most commonly owned cryptocurrencies were Ether (56%) and Bitcoin (50%), and 68% of respondents said they were active in the cryptocurrency space to invest, among other things.

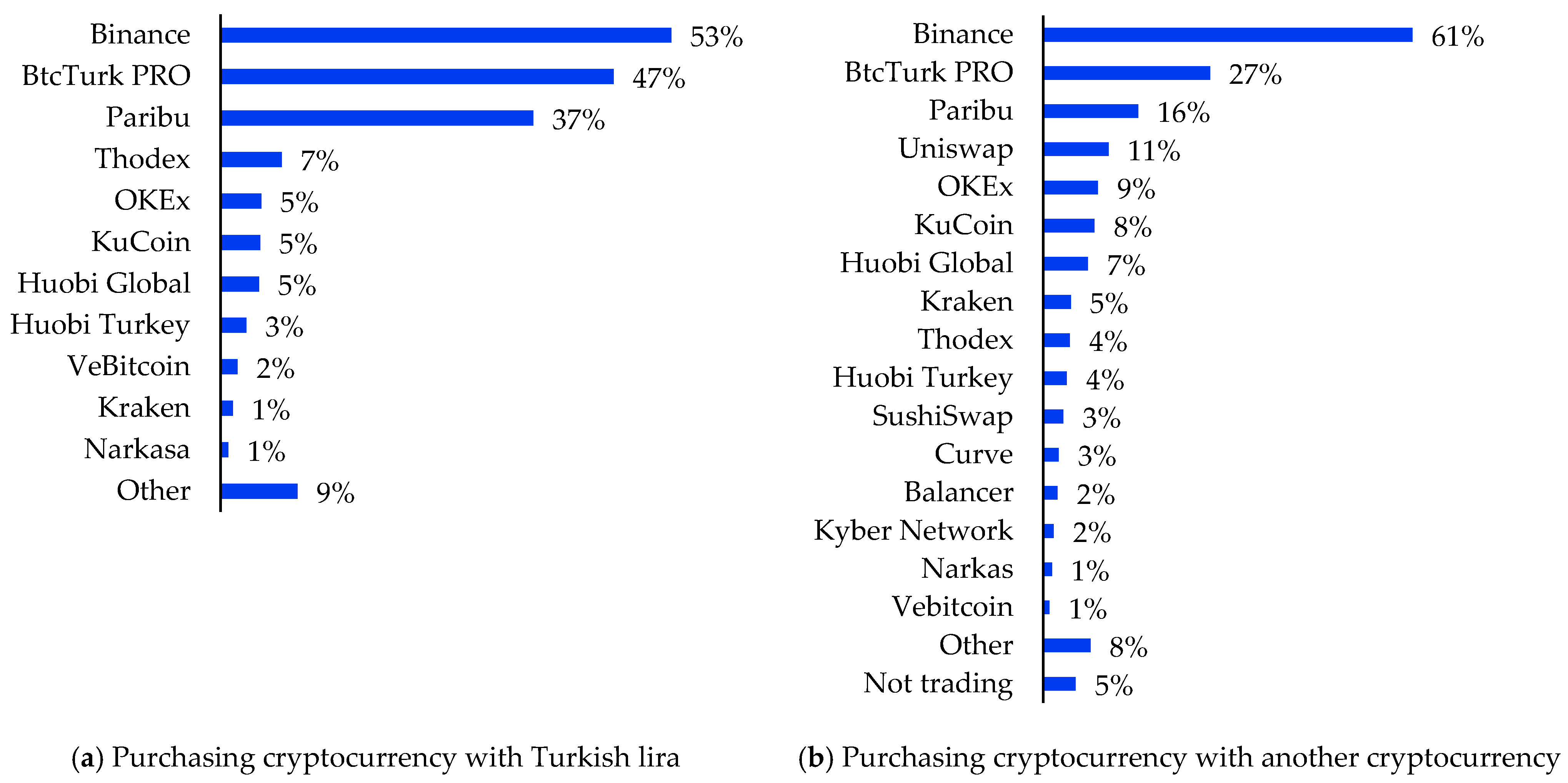

With 91%, the majority of people bought cryptocurrencies via exchanges, of which international cryptocurrency exchange Binance (61%) had the highest usage for purchasing cryptocurrencies with Turkish lira, followed by national cryptocurrency exchanges BtcTurk Pro (47%) and Paribu (37%), with the same ranking but different percentages (61%, 27% and 16%, respectively) for crypto-to-crypto exchanges (cf.

Figure 2).

2.2. Empirical Approach

The identification of user groups is accomplished through the utilization of exploratory factor analysis, which employs the motives and characteristics of individuals as a basis. Factor analysis, a statistical method that is utilized to analyze data comprised of multiple interrelated variables, is a technique designed to uncover the underlying structure of a set of variables and to succinctly describe the relationships among them. Exploratory factor analysis, as one of the two main forms of factor analysis, serves to identify patterns in data and to reveal the underlying structure of variables. This technique, which reduces data and identifies the underlying factors that explain the variance in a set of variables (

Gorsuch 1988;

Park 2017;

Spearman 1904), is widely applied in various disciplines, including but not limited to psychology, sociology, economics and marketing.

The methodology employed in the analysis involves the construction of a matrix of correlations between the variables in question. Subsequently, principal component analysis (PCA) was conducted to uncover the underlying factors that account for the variance in the data. Factor extraction was then refined through the application of varimax rotation (

McCain 1990;

White and McCain 1998), in order to enhance the interpretability of the factors. Upon identification and rotation of the factors, the results were interpreted by scrutinizing the factor loadings, which represent the correlation coefficients between each variable and each factor. The magnitude of these coefficients serves as an indicator of the strength of the relationship between each variable and each factor.

Subsequently, we tested the fit of the factor analysis via the Kaiser–Meyer–Olkin (KMO) measure and Bartlett’s test of sphericity. The KMO measure is a statistic that is used to assess the suitability of a dataset for factor analysis. It is a measure of the sampling adequacy, which indicates the proportion of the variance in the variables that can be explained by the factors (

Dziuban and Shirkey 1974). The KMO measure ranges from 0 to 1, with values closer to 1 indicating a better suitability for factor analysis. A KMO value of 0.5 or higher is considered acceptable for factor analysis (

White and Griffith 1981). To calculate the KMO measure, we first compute the correlations between all pairs of variables in the dataset. Then, the KMO statistic is calculated as the mean of the partial correlations between the variables, adjusted for the sampling error.

Bartlett’s test of sphericity is a statistical test that is used to determine whether the correlations between a set of variables are sufficiently strong to warrant the use of factor analysis. It is a test of the null hypothesis that the correlation matrix of the variables is an identity matrix, which indicates that there are no correlations among the variables. To conduct Bartlett’s test of sphericity, we first calculate the correlations between all pairs of variables in the dataset and then calculate the test statistic, which is a function of the correlations and the sample size. The test statistic is compared to a critical value from a chi-squared distribution to determine the p-value of the test. If the p-value is less than the chosen level of significance (e.g., 0.05), it indicates that the correlations among the variables are not due to chance and that the null hypothesis can be rejected.

Subsequently, we fit a regression model to the data, with the factor loadings as the dependent variable and independent variables as the predictors, which allowed us to examine the relationships between the factor loadings and other variables and to make predictions about the factor loadings based on the values of the independent variables. This approach aims to decrease the number of variables in the analysis and avoid issues with multicollinearity that could arise from using all variables in principal component analysis. Additionally, we address a potential weakness caused by utilizing a rotated factor solution with Kaiser normalization. Without the subsequent step of regression analysis, potentially relevant and statistically significant results of socio-economic variables may be overlooked due to the factor analysis procedure. Thus, this combined approach of factor plus regression analysis increases the accuracy of the analysis and ensures that significant findings are not overlooked. Regression analysis is applied to examine the extent to which the identified groups differ on the basis of socio-demographics (male gender, age in years, income per 1000 Turkish lira, education as a score from 1 (no degree) to 5 (doctorate) and population density as the log-transformed population size of the district) and other factors. These are dummy variables for (1) agreeing on the question that cash should be abolished (ideological motivation to own cryptocurrency); (2) answering that more cryptocurrency is likely to be purchased in the next six months (purchase intention); and answering that respondents use domestic (3) or foreign (4) cryptocurrency exchanges to purchase cryptocurrency against Turkish lira. The issue of market access via the respective exchanges provides an opportunity to explore the extent to which cryptocurrency access and trading is a phenomenon that only affects Turkey locally, or whether users also rely on international offerings that may (in the future) be regulated differently, thus making it a highly relevant topic for regulatory questions.

The variables included in the exploratory factor analysis were chosen in line with the cognitive balance theory. These variables serve as a foundation for our analysis and allow us to identify factors that are relevant to the cognitive balance of individuals. It is important to note that some other variables, such as education, cannot be operationalized via the cognitive balance theory and may still load on a single factor in the initial stage of analysis. This could potentially lead to misinterpretation of the results, as it may not accurately reflect the significant correlates across all factors. Therefore, we decided to employ a 2-step statistical approach, in which we include additional variables in the regression models. This allows us to better understand the relationships between the variables and the factors identified in the exploratory factor analysis. The added variables provide a more comprehensive picture of the data and help us to better understand the underlying relationships between the variables and the factors.

3. Results

Table 1 presents the Pearson correlation coefficient (r) for each pair of variables used for subsequent factor and regression analysis. Statistical significance based on a corresponding

p-value of 0.05 or higher is highlighted in bold. It is important to note that the Pearson correlation only measures linear relationships and may not accurately capture more complex relationships between variables.

We identified that correlation coefficients take a maximum value of 0.37 (male gender and income), which means that there is no multicollinearity between variables; thus, factor analysis and regression analysis are appropriate methods. We conducted principal component factor analysis with varimax rotation and Kaiser normalization, resulting in a three-factor solution that all have Eigenvalues >1.

Table 2 shows the factor loadings, for which, in line with

McCain (

1990), we defined a threshold of 0.4 to assign them to a factor. All variables but trading frequency loaded on a single factor. We assigned trading frequency to the largest loading, i.e., factor 3. The three identified factors explain 48% of the variance, and the KMO measure (0.52) and Bartlett’s test of sphericity (

p < 0.01) indicate that factor analysis is an appropriate methodology. The number of observations is 631 because not all respondents provided an answer on their income.

We coined the three factors (1) payment users, (2) crypto investors and (3) crypto traders, representing different cryptocurrency owner groups of Turkish individuals. The chosen nomenclature of each factor was based on the factor analysis results and on the variables included and excluded in the factor solutions. The factor names accurately reflect the underlying theme of each factor and were chosen to effectively communicate the findings to the reader. In this context, it is important to note that the naming of factors is a subjective procedure which requires careful interpretations and comparisons across studies. It is important to note that other researchers may use different names for these factors, which could potentially impact the interpretation and comparison of findings across studies. The first factor (payment users) comprises the usage of cryptocurrency for payments (+), investment (−) and technological literacy (+). Cryptocurrency owners in this section have a high degree of technical expertise and seem to be uninterested in the investment or speculative characteristics of cryptocurrencies, but care about its option as a means of payment. The fact that non-speculative (but still financial) motives represent the factor with the largest share of the variance is in line with

Steinmetz (

2021), who outlines that such motives may be less prevalent in the media or the academic literature but are still highly relevant. The second factor (crypto investors) comprises the variables financial literacy (+) and cryptocurrency experience (+), indicating that these individuals are investors with a long(er) time horizon, as also indicated by the high negative factor loading of trading frequency. Accordingly, it can be concluded that this is a group of people who presumably are not concerned by potential short-term volatility, and the low factor loading for payments suggests that this group of people is unlikely to see major benefit from cryptocurrencies for payments. With regard to the relevance of cryptocurrency payments, the same can be said for the third group. Factor 3 (crypto traders) comprises the degree of knowledge about different cryptocurrencies (+), trading frequency (+) and risk taking (+), thus indicating that these individuals are highly active traders that frequently buy and sell cryptocurrency. The negative factor loading of technological literacy (proxied via the ability to read code) suggests that this group is least likely to be involved in actual on-chain transactions or smart contract programming, as these individuals likely primarily trade on exchanges.

As shown in

Table 3, the relationships between various variables and the factor loadings of the individual groups were analyzed using ordinary least-squares (OLS) regression, with one factor per model. The models were able to explain between 3–13% of the variance in the data, indicating that there are additional, unobserved variables that contribute to the characteristics of the groups.

Standard errors were adjusted to account for heteroskedasticity. For the group of payment users, we found that ideology had a positive, significant influence on group membership, while short-term purchase intention had a negative effect. For the group of investors, we also observed a negative relationship with short-term purchase intention, but this was more pronounced than in the payment users’ group. Additionally, we found that membership in the investor group was influenced by the use of domestic exchanges, as well as by gender (being male), higher income and higher education level. Similar effects were found for the trader group (factor 3) with regards to gender and education; however, in contrast to the other two groups, we observed a positive relationship between group membership and short-term purchase intention. Furthermore, we found significant influences of both domestic and foreign exchanges on trader group membership, with the effect of foreign exchanges being significantly stronger.

4. Discussion

To the best of our knowledge, this study is the first to profile and characterize Turkish cryptocurrency owners. The results provide evidence of the diversity of users of cryptocurrency: there is not “the crypto owner”, but user groups are clearly distinguishable with regards to the investigated usage characteristics. We identified three distinct groups of owners: (1) payment users, (2) crypto investors and (3) crypto traders.

The differentiation of user groups of cryptocurrency owners in Turkey adds to the literature regarding cryptocurrency user characteristics and usage (e.g., as summarized by

Steinmetz et al. (

2021)) that has so far focused on different economies in two regards. First, it complements existing studies by providing insights into cryptocurrency users and use in a geographical region, which has so far received insufficient attention in relation to its above-average ownership rates. As an emerging market, insights into Turkish usage characteristics may foreshadow similar developments in comparable economies. Second, our results complement existing findings regarding the usage patterns of cryptocurrency users, e.g., by

Steinmetz et al. (

2021) on the primary use cases of German cryptocurrency users and by

Steinmetz (

2021) on the user groups clustered by the frequency with which respondents applied cryptocurrency in certain application domains. In comparison to these studies, our analysis introduces new variables (e.g., technological and financial literacy, self-estimated risk affinity) and reduces the primary use cases for cryptocurrency. The three groups identified in the previous section resemble those three identified by

Steinmetz (

2021), where ‘moderate conservatives’, ‘all-out activists’ and ‘passive investors’ are clustered by the primary use case but also by frequency of use. In contrast, however, the grouping of Turkish users reveals higher distinction of the groups, particularly with regards to users focused on payments. The group of payment users can be identified as a particular characteristic of the Turkish market and potentially of emerging markets in general.

Payment users may thus be the most interesting user group and they also form the most relevant group statistically: they can be described as utility-oriented and ideologically driven cryptocurrency users. This is in contrast to past studies about cryptocurrency use that found less pronounced ambitions to use cryptocurrency for payments in developed countries (e.g.,

Auer and Tercero-Lucas (

2022) for the USA and

Steinmetz (

2021) for Germany), where it is counterintuitive to use cryptocurrency as an alternative means of payment due to their volatility (

Walther et al. 2019). This contrasting finding reveals the demand for cryptocurrency’s utility as a payment vehicle under specific Turkish circumstances, which seem to outweigh the disadvantage of volatility. It is conceivable that the demand for cryptocurrency is associated with the fiscal and economic situation in Turkey, particularly with the Turkish lira’s inflation rates and inflation uncertainty (

Sivrikaya 2020). Another explanation could be the increased availability and circulation of stablecoins. The most popular stablecoins are pegged to the USD and backed USD cash and cash equivalents giving holders USD exposure (

Ante et al. 2021;

Fiedler and Ante 2023). Hence, stablecoins overcome the volatility of other cryptocurrencies and are more useful for payment purposes. It is thus conceivable that part of the discrepancy of finding payment users in Turkey but not in former research can be explained by stablecoins’ increase in popularity in the time between the sample collection of the research. This hypothesis requires further research as also called for by

Ante et al. (

2023) in their systematic literature review on stablecoins.

In any case, the identification of the group of payment users complements findings by

Bhimani et al. (

2022) that cryptocurrency usage differs across countries with differently developed economies. Certainly, more research is needed to assess the perceptions, ideologies and motives of the identified group of payment users, e.g., whether payment users make use of stablecoins rather than speculative crypto assets, whose characteristics of cryptocurrency drive their decision, and whether payments are made in domestic or international settings, i.e., whether cryptocurrency payments replace payments with the Turkish lira.

The identified group of payment users likely (1) has payment-related needs and (2) receives high net benefits from payment-related innovations of cryptocurrencies. Taking also into consideration the very high cryptocurrency ownership rates in Turkey (

de Best 2022;

Exton and Doidge 2018;

Paribu 2021), in comparison to other countries, we identify the described group of Turkish (cryptocurrency) payment users as potential lead users according to

von Hippel (

1986), whose current needs represent common needs for users in other markets in the future. More precisely, other economies, which are referred to as emerging markets and face similar problems to Turkey, may exhibit similar adoption patterns of cryptocurrency in the future, e.g., for the purposes of payments or capital preservation. The benefits for citizens would contrast a decline in governmental and fiscal power and control.

According to the lead market theory (

Beise and Cleff 2004;

Tiwari and Herstatt 2012), lead users induce demand advantages, which, among four other factors, could facilitate Turkey to become a “lead market” for cryptocurrency in the future. On that basis, future studies of technology acceptance and innovation diffusion should also investigate the question whether Turkey can even play a role as a “lead market” (

Beise and Cleff 2004) for cryptocurrencies. This would allow a contribution to the broader understanding of (international) innovation diffusion (

Rogers 2003) with regard to cryptocurrency adoption.

With reference to the possible future regulation of (foreign) cryptocurrency exchanges in Turkey, the results also offer the insight that foreign exchanges do not seem to be a significant metric for the user group, while the investor group seems to prefer domestic exchanges. Only the relatively (statistically) smallest group of traders shows higher statistical correlations to foreign exchanges. This can be interpreted as an indication that a majority of the people who might be targeted by the discussed regulation, users and investors, may hardly be affected. Rather, such regulation would mainly affect the third group of traders, who increasingly use foreign exchanges in addition to local ones.

The survey data used in this research paper are not representative based on, e.g., age and gender of the Turkish population and may also not be a representative sample of Turkish cryptocurrency owners. As a consequence, certain demographic characteristics, such as gender and age, may be over or underrepresented in the sample, potentially limiting the ability to derive generalized implications based on the results. Therefore, it is important to acknowledge the limitations of this study, and we recommend that future research should validate the results through more robust and diverse sampling methods. This would enable an even more comprehensive and accurate understanding of the cryptocurrency landscape in Turkey and facilitate the development of effective policies and strategies in this field.

5. Conclusions

In conclusion, our study of Turkish cryptocurrency owners reveals the existence of three distinct groups with different motivations for owning cryptocurrency. They can best be described as follows: (1) The first group, payment users, see cryptocurrency as a means of making payments and are not concerned with its speculative value; (2) The second group, crypto investors, are experienced investors who hold cryptocurrency as part of their investment strategy; (3) The third group, crypto traders, are risk-tolerant individuals who engage in trading activity.

The results of our investigation reveal marked variations in demographics, income, educational attainment, ideological inclination, purchase intent and domestic or foreign exchanges utilized among the identified groups. These distinctions are more pronounced than those observed in previous research on the topic and serve to underscore the diversity of usage patterns and user characteristics across various geographical regions and economies of varying levels of development. Of particular significance is the identification of payment users in Turkey, which suggests that the primary utility of cryptocurrency is subject to variation across nations and may be related to the recent proliferation of stablecoins, which offer the benefits of cryptocurrency without subjecting the holder to the volatility of market prices. These findings not only provide valuable insights into the motivations and characteristics of Turkish cryptocurrency owners, which can inform regulatory processes in the country, but also contribute to a more nuanced understanding of cryptocurrency usage in other countries and markets.

{kind=link}

{kind=link}