Modeling the Brand Equity and Usage Intention of QR-Code E-Wallets

,

,

Abstract

:1. Introduction

2. Literature Review

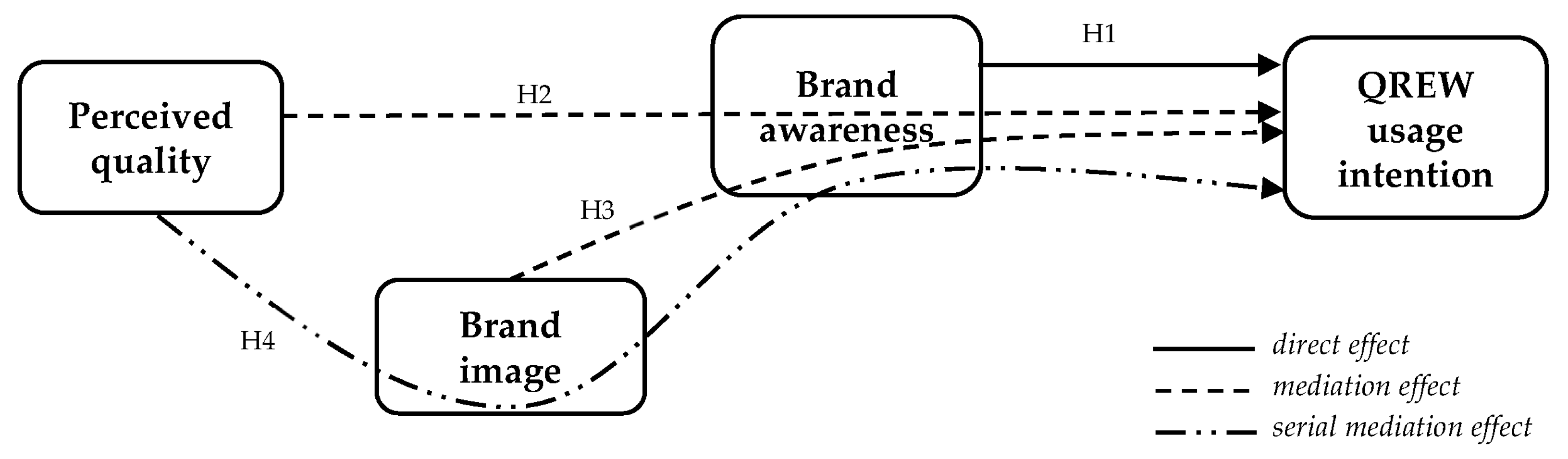

2.1. Brand Equity

2.2. Brand Awareness and QREW Usage Intention

2.3. Indirect Effect of Perceived Quality on QREW Usage Intention

2.4. Indirect Effect of Brand Image on QREW Usage Intention

2.5. Multiple Serial Mediation Effects of Brand Equity Elements

3. Methodology

3.1. Samples and Data Collection Procedures

3.2. Measures

3.3. Analysis Tool and Method Bias

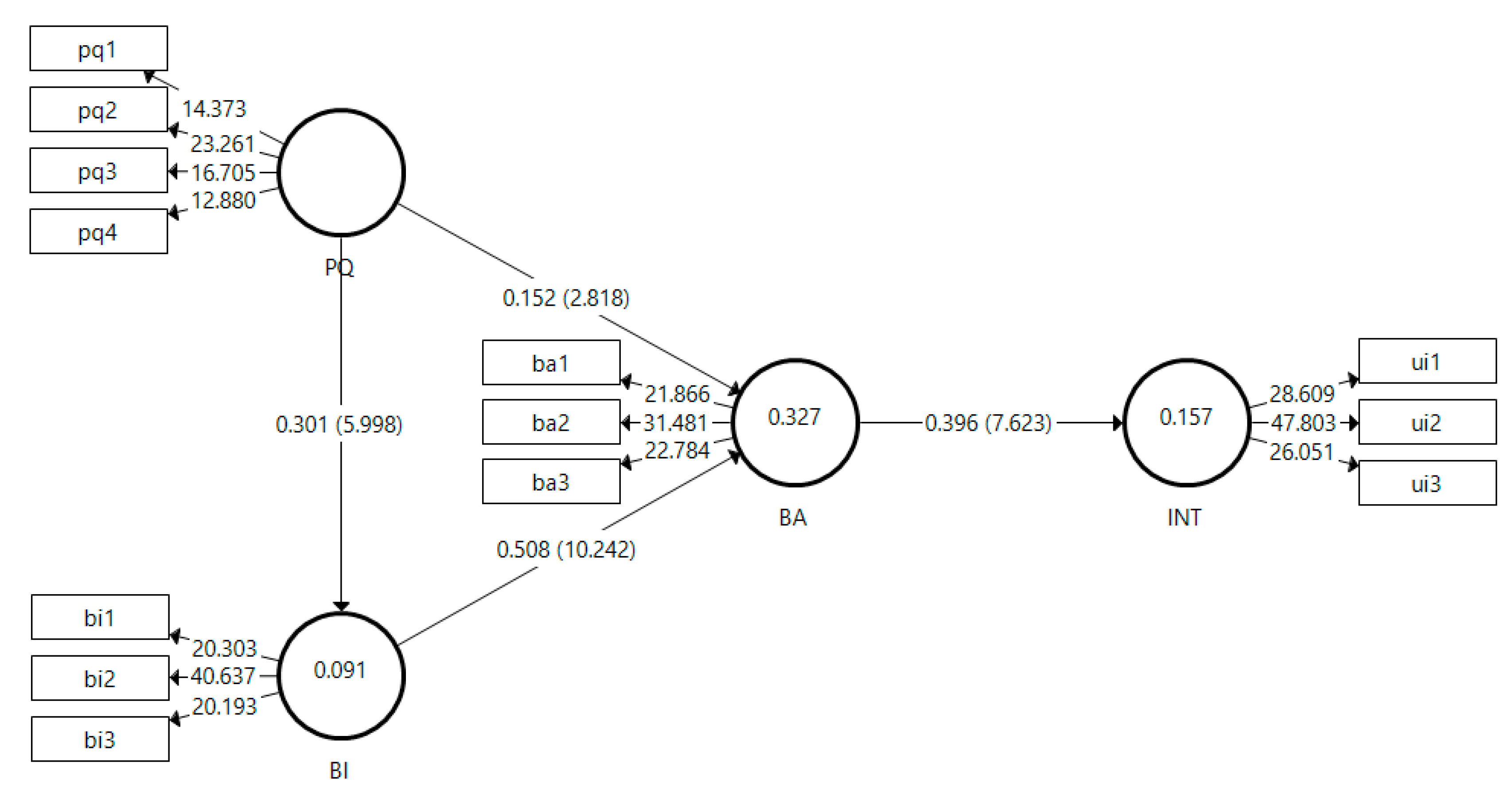

4. Findings

4.1. Sample Characteristics

4.2. Measurement Model

4.3. Structural Model

5. Discussion

5.1. Theoretical Implications

5.2. Practical Implications

5.3. Limitations and Future Research Directions

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

| PQ | BI | BA | INT | |

|---|---|---|---|---|

| PQ1 | 0.730 | 0.273 | 0.248 | 0.217 |

| PQ2 | 0.797 | 0.247 | 0.225 | 0.224 |

| PQ3 | 0.732 | 0.179 | 0.233 | 0.221 |

| PQ4 | 0.696 | 0.170 | 0.185 | 0.234 |

| BI1 | 0.231 | 0.760 | 0.439 | 0.196 |

| BI2 | 0.289 | 0.856 | 0.430 | 0.260 |

| BI3 | 0.200 | 0.780 | 0.459 | 0.239 |

| BA1 | 0.190 | 0.450 | 0.738 | 0.359 |

| BA2 | 0.227 | 0.421 | 0.825 | 0.284 |

| BA3 | 0.305 | 0.438 | 0.808 | 0.291 |

| UI1 | 0.294 | 0.249 | 0.341 | 0.837 |

| UI2 | 0.224 | 0.253 | 0.354 | 0.870 |

| UI3 | 0.242 | 0.229 | 0.301 | 0.815 |

References

- Ramli, F.A.A.; Hamzah, M.I. Mobile Payment and E-Wallet Adoption in Emerging Economies: A Systematic Literature Review. J. Emerg. Econ. Islam. Res. 2021, 9, 1–39. [Google Scholar] [CrossRef]

- Bank Negara Malaysia Payment System—List of Regulatees. Available online: https://www.bnm.gov.my/list-of-regulatees (accessed on 10 November 2022).

- Sen, A. Malaysia’s Overpopulated e-Wallet Landscape: Deep Pockets Not Enough. Available online: https://thelowdown.momentum.asia/malaysias-overpopulated-e-wallet-landscape-deep-pockets-not-enough/ (accessed on 12 October 2022).

- Yan, L.Y.; Tan, G.W.H.; Loh, X.M.; Hew, J.J.; Ooi, K.B. QR Code and Mobile Payment: The Disruptive Forces in Retail. J. Retail. Consum. Serv. 2021, 58, 102300. [Google Scholar] [CrossRef]

- Zhang, S.; Peng, M.Y.P.; Peng, Y.; Zhang, Y.; Ren, G.; Chen, C.C. Expressive Brand Relationship, Brand Love, and Brand Loyalty for Tablet PCs: Building a Sustainable Brand. Front. Psychol. 2020, 11, 231. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Ramadan, R.; Aita, J. A Model of Mobile Payment Usage among Arab Consumers. Int. J. Bank Mark. 2018, 36, 1213–1234. [Google Scholar] [CrossRef]

- Sankaran, R.; Chakraborty, S. Measuring Consumer Perception of Overall Brand Equity Drivers for M-Payments. Int. J. Bank Mark. 2023, 41, 130–157. [Google Scholar] [CrossRef]

- Wang, W.T.; Li, H.M. Factors Influencing Mobile Services Adoption: A Brand-Equity Perspective. Internet Res. 2012, 22, 142–179. [Google Scholar] [CrossRef]

- Iman, N. Is Mobile Payment Still Relevant in the Fintech Era? Electron. Commer. Res. Appl. 2018, 30, 72–82. [Google Scholar] [CrossRef]

- Woodbury, B. QR Codes vs. NFC—The Battle That Is Shaping Mobile Payments Is Just Warming Up. Available online: https://www.fisglobal.com/en/insights/what-we-think/2019/february/qr-codes-nfc-shaping-mobile-payments (accessed on 25 September 2022).

- Meena, R.; Sarabhai, S. Extrinsic and Intrinsic Motivators for Usage Continuance of Hedonic Mobile Apps. J. Retail. Consum. Serv. 2023, 71, 103228. [Google Scholar] [CrossRef]

- Beristain, J.J.; Zorrilla, P. The Relationship between Store Image and Store Brand Equity: A Conceptual Framework and Evidence from Hypermarkets. J. Retail. Consum. Serv. 2011, 18, 562–574. [Google Scholar] [CrossRef]

- Suo, W.-J.; Goi, C.-L.; Goi, M.-T.; Sim, A.K.S. Factors Influencing Behavioural Intention to Adopt the QR-Code Payment. Int. J. Asian Bus. Inf. Manag. 2021, 13, 1–22. [Google Scholar] [CrossRef]

- de Luna, I.R.; Liébana-Cabanillas, F.; Sánchez-Fernández, J.; Muñoz-Leiva, F. Mobile Payment Is Not All the Same: The Adoption of Mobile Payment Systems Depending on the Technology Applied. Technol. Forecast. Soc. Chang. 2019, 146, 931–944. [Google Scholar] [CrossRef]

- Liu, Z.; Ben, S.; Zhang, R. Factors Affecting Consumers’ Mobile Payment Behavior: A Meta-Analysis. Electron. Commer. Res. 2019, 19, 575–601. [Google Scholar] [CrossRef]

- Leong, L.; Hew, J.; Lin, B. The Past and beyond of Mobile Payment Research: A Development of the Mobile Payment Framework. Internet Res. 2022. ahead-of-print. [Google Scholar] [CrossRef]

- Dahlberg, T.; Guo, J.; Ondrus, J. A Critical Review of Mobile Payment Research. Electron. Commer. Res. Appl. 2015, 14, 265–284. [Google Scholar] [CrossRef]

- Keller, K.L. Conceptualizing, Measuring, and Managing Customer-Based Brand Equity. J. Mark. 1993, 57, 1–22. [Google Scholar] [CrossRef]

- Christodoulides, G. Consumer Based Brand Equity Conceptualization & Measurement: A Literature Review. Int. J. Mark. Res. 2010, 52, 43–66. [Google Scholar]

- Aaker, D.A. Managing Brand Equity: Capitalizing on the Value of a Brand Name; The Free Press: New York, NY, USA, 1991; ISBN 0-02-900101-3. [Google Scholar]

- Yoo, B.; Donthu, N. Developing and Validating a Multidimensional Consumer-Based Brand Equity Scale. J. Bus. Res. 2001, 52, 1–14. [Google Scholar] [CrossRef]

- Washburn, J.H.; Plank, R.E. Measuring Brand Equity: An Evaluation of a Consumer-Based Brand Equity Scale. J. Mark. Theory Pract. 2002, 10, 46–62. [Google Scholar] [CrossRef]

- Arai, A.; Ko, Y.J.; Ross, S. Branding Athletes: Exploration and Conceptualization of Athlete Brand Image. Sport Manag. Rev. 2014, 17, 97–106. [Google Scholar] [CrossRef]

- Gensler, S.; Völckner, F.; Egger, M.; Fischbach, K.; Schoder, D. Listen to Your Customers: Insights into Brand Image Using Online Consumer-Generated Product Reviews. Int. J. Electron. Commer. 2016, 20, 112–141. [Google Scholar] [CrossRef]

- Gong, X.; Cheung, C.M.K.; Zhang, K.Z.K.; Chen, C.; Lee, M.K.O. Cross-Side Network Effects, Brand Equity, and Consumer Loyalty: Evidence from Mobile Payment Market. Int. J. Electron. Commer. 2020, 24, 279–304. [Google Scholar] [CrossRef]

- Yeh, H. Factors in the Ecosystem of Mobile Payment Affecting Its Use: From the Customers’ Perspective in Taiwan. J. Theor. Appl. Electron. Commer. Res. 2020, 15, 13–29. [Google Scholar] [CrossRef] [Green Version]

- Aaker, D.A. Measuring Brand Equity Across Products and Markets. Calif. Manage. Rev. 1996, 38, 102–120. [Google Scholar] [CrossRef] [Green Version]

- Erdem, T.; Swait, J. Brand Equity as a Signaling Phenomenon. J. Consum. Psychol. 1998, 7, 131–157. [Google Scholar] [CrossRef]

- Guzmán, F.; Davis, D. The Impact of Corporate Social Responsibility on Brand Equity: Consumer Responses to Two Types of Fit. J. Prod. Brand Manag. 2017, 26, 435–446. [Google Scholar] [CrossRef]

- Hamzah, M.I.; Pontes, N. What Drives Car Buyers to Accept a Rejuvenated Brand? The Mediating Effects of Value and Pricing in a Consumer-Brand Relationship. J. Strateg. Mark. 2022, 1–23. [Google Scholar] [CrossRef]

- Stocchi, L.; Michaelidou, N.; Micevski, M. Drivers and Outcomes of Branded Mobile App Usage Intention. J. Prod. Brand Manag. 2019, 28, 28–49. [Google Scholar] [CrossRef] [Green Version]

- Kar, A.K. What Affects Usage Satisfaction in Mobile Payments? Modelling User Generated Content to Develop the “Digital Service Usage Satisfaction Model”. Inf. Syst. Front. 2021, 23, 1341–1361. [Google Scholar] [CrossRef]

- Tran, T.P.; Mai, E.S.; Taylor, E.C. Enhancing Brand Equity of Branded Mobile Apps via Motivations: A Service-Dominant Logic Perspective. J. Bus. Res. 2021, 125, 239–251. [Google Scholar] [CrossRef]

- Moghavvemi, S.; Mei, T.X.; Phoong, S.W.; Phoong, S.Y. Drivers and Barriers of Mobile Payment Adoption: Malaysian Merchants’ Perspective. J. Retail. Consum. Serv. 2021, 59, 102364. [Google Scholar] [CrossRef]

- Yoo, B.; Donthu, N.; Lee, S. An Examination of Selected Marketing Mix Elements and Brand Equity. J. Acad. Mark. Sci. 2000, 28, 195–211. [Google Scholar] [CrossRef]

- Chi, T. Understanding Chinese Consumer Adoption of Apparel Mobile Commerce: An Extended TAM Approach. J. Retail. Consum. Serv. 2018, 44, 274–284. [Google Scholar] [CrossRef]

- Karjaluoto, H.; Shaikh, A.A.; Saarijärvi, H.; Saraniemi, S. How Perceived Value Drives the Use of Mobile Financial Services Apps. Int. J. Inf. Manage. 2019, 47, 252–261. [Google Scholar] [CrossRef]

- Febriyantoro, M.T. Exploring YouTube Marketing Communication: Brand Awareness, Brand Image and Purchase Intention in the Millennial Generation. Cogent Bus. Manag. 2020, 7, 1787733. [Google Scholar] [CrossRef]

- Kaur, P.; Dhir, A.; Singh, N.; Sahu, G.; Almotairi, M. An Innovation Resistance Theory Perspective on Mobile Payment Solutions. J. Retail. Consum. Serv. 2020, 55, 102059. [Google Scholar] [CrossRef]

- Chen, C.C.; Chang, C.H.; Hsiao, K.L. Exploring the Factors of Using Mobile Ticketing Applications: Perspectives from Innovation Resistance Theory. J. Retail. Consum. Serv. 2022, 67, 102974. [Google Scholar] [CrossRef]

- Lian, J.W.; Li, J. The Dimensions of Trust:An Investigation of Mobile Payment Services in Taiwan. Technol. Soc. 2021, 67, 101753. [Google Scholar] [CrossRef]

- Shaw, N. The Mediating Influence of Trust in the Adoption of the Mobile Wallet. J. Retail. Consum. Serv. 2014, 21, 449–459. [Google Scholar] [CrossRef]

- Dubey, U.K.B.; Kothari, D.P. Research Methodology: Techniques and Trends; CRC Press: Boca Raton, FL, USA, 2022. [Google Scholar]

- Lee, G.; Leh, F. Dimensions of Customer-Based Brand Equity: A Study on Malaysian Brands. J. Mark. Res. Case Stud. 2011, 2011, 821981. [Google Scholar] [CrossRef] [Green Version]

- Venkatesh, V.; Morris, M.G.; Davis, G.B.; Davis, F.D. User Acceptance of Information Technology: Toward a Unified View. MIS Q. Manag. Inf. Syst. 2003, 27, 425–478. [Google Scholar] [CrossRef] [Green Version]

- Ringle, C.; Wende, S.; Becker, J. SmartPLS 3. Oststeinbek, Germany: SmartPLS. Available online: https://www.smartpls.com,2015 (accessed on 16 March 2023).

- Hair, J.; Hult, G.T.M.; Ringle, C.; Sarstedt, M. A Primer on Partial Least Squares Structural Equation Modeling (PLS-SEM), 2nd ed.; Sage Publications: Thousand Oaks, CA, USA, 2017; ISBN 9781452217444. [Google Scholar]

- Podsakoff, P.M.; MacKenzie, S.B.; Lee, J.-Y.; Podsakoff, N.P. Common Method Biases in Behavioral Research: A Critical Review of the Literature and Recommended Remedies. J. Appl. Psychol. 2003, 88, 879–903. [Google Scholar] [CrossRef] [PubMed]

- Kock, N. Common Method Bias: A Full Collinearity Assessment Method for PLS-SEM; Rigdon, E., Ed.; Springer: Cham, Switzerland, 2017; ISBN 9783319640693. [Google Scholar]

- Kline, R.B. Principles and Practice of Structural Equation Modeling: Third Edition, 3rd ed.; Guilford Press: New York, NY, USA, 2011; ISBN 978-1-60623-876-9. [Google Scholar]

- Gold, A.H.; Malhotra, A.; Segars, A.H. Knowledge Management: An Organizational Capabilities Perspective. J. Manag. Inf. Syst. 2001, 18, 185–214. [Google Scholar] [CrossRef]

- Ramayah, T.; Cheah, J.; Chuah, F.; Ting, H.; Memon, M.A. Partial Least Squares Structural Equation Modelling (PLS-SEM) Using SmartPLS 3.0, 2nd ed.; Pearson: Kuala Lumpur, Malaysia, 2018. [Google Scholar]

- Henseler, J.; Dijkstra, T.K.; Sarstedt, M.; Ringle, C.M.; Diamantopoulos, A.; Straub, D.W.; David, J.; Ketchen, J.; Hair, J.F.; Hult, G.T.M.; et al. Common Beliefs and Reality About PLS: Comments on Rönkkö and Evermann (2013). Organ. Res. Methods 2014, 17, 182–209. [Google Scholar] [CrossRef] [Green Version]

- Preacher, K.J.; Hayes, A.F. Asymptotic and Resampling Strategies for Assessing and Comparing Indirect Effects in Multiple Mediator Models. Behav. Res. Methods 2008, 40, 879–891. [Google Scholar] [CrossRef]

- Baron, R.M.; Kenny, D.A. The Moderator—Mediator Variable Distinction in Social Psychological Research: Conceptual, Strategic, and Statistical Considerations. J. Pers. Soc. Psychol. 1986, 51, 1173. [Google Scholar] [CrossRef] [PubMed]

- Zhao, X.; Lynch, J.G.; Chen, Q. Reconsidering Baron and Kenny: Myths and Truths about Mediation Analysis. J. Consum. Res. 2010, 37, 197–206. [Google Scholar] [CrossRef]

- Kaur, P.; Dhir, A.; Bodhi, R.; Singh, T.; Almotairi, M. Why Do People Use and Recommend M-Wallets? J. Retail. Consum. Serv. 2020, 56, 102091. [Google Scholar] [CrossRef]

- Sarkar, S.; Chauhan, S.; Khare, A. A Meta-Analysis of Antecedents and Consequences of Trust in Mobile Commerce. Int. J. Inf. Manage. 2020, 50, 286–301. [Google Scholar] [CrossRef]

- Hasim, M.A.; Manaf, S.A.; Ali, A.M. Customer Expectations in E-Wallet Services. Eur. J. Mol. Clin. Med. 2020, 7, 4160–4178. [Google Scholar]

- Lu, M.P.; Kosim, Z. An Empirical Study to Explore the Influence of the COVID-19 Crisis on Consumers’ Behaviour towards Cashless Payment in Malaysia. J. Financ. Serv. Mark. 2022, 1–12. [Google Scholar] [CrossRef]

- Zariman, N.F.M.; Humaidi, N.; Abd Rashid, M.H. Mobile Commerce Applications Service Quality in Enhancing Customer Loyalty Intention: Mediating Role of Customer Satisfaction. J. Financ. Serv. Mark. 2022, 1–15. [Google Scholar] [CrossRef]

- Mouakket, S. Investigating the Role of Mobile Payment Quality Characteristics in the United Arab Emirates: Implications for Emerging Economies. Int. J. Bank Mark. 2020, 38, 1465–1490. [Google Scholar] [CrossRef]

- Hamzah, M.I.; Othman, A.K.; Hassan, F. Mediating Effects of Individual Market Orientation on the Link between Learning Orientation and Job Performance. J. Bus. Ind. Mark. 2020, 35, 655–668. [Google Scholar] [CrossRef]

- Grover, P.; Kar, A.K. User Engagement for Mobile Payment Service Providers—Introducing the Social Media Engagement Model. J. Retail. Consum. Serv. 2020, 53, 101718. [Google Scholar] [CrossRef]

- Zhao, Z.; Balagué, C. Designing Branded Mobile Apps: Fundamentals and Recommendations. Bus. Horiz. 2015, 58, 305–315. [Google Scholar] [CrossRef]

- Lau, U.H.; Lee, L.E.; Kang Lew, D.; Loo, L.S.; Ooi, S.X.; Lee, V.H.; Loh, X.M.; Tan, G.H.W. Mobile Payment Adoption: Barriers for Baby Boomers in Malaysia. In Proceedings of the International Conference on Emerging Technologies and Intelligent Systems; Springer: Cham, Switzerland, 2022; pp. 568–579. [Google Scholar]

- Hopalı, E.; Vayvay, Ö.; Kalender, Z.T.; Turhan, D.; Aysuna, C. How Do Mobile Wallets Improve Sustainability in Payment Services? A Comprehensive Literature Review. Sustainability 2022, 14, 16541. [Google Scholar] [CrossRef]

- Parameswar, N.; Dhir, S.; Dhir, S. Banking on Innovation, Innovation in Banking at ICICI Bank. Glob. Bus. Organ. Excell. 2017, 36, 6–16. [Google Scholar] [CrossRef]

- Loucanova, E.; Olsiakova, M. Comparison of Innovation in the Electronic Banking Services of the Largest Slovak Banks. Mark. Manag. Innov. 2022, 4, 1–9. [Google Scholar] [CrossRef]

| Demographic Variable | n | % | Demographic Variable | n | % | ||

|---|---|---|---|---|---|---|---|

| Age | Occupation | ||||||

| 18–23 years old | 93 | 30.5 | Employed | 201 | 65.9 | ||

| 24–29 years old | 79 | 25.9 | Student | 100 | 32.8 | ||

| 30–39 years old | 82 | 26.9 | Retired | 4 | 1.3 | ||

| 40–49 years old | 37 | 12.1 | Income | ||||

| 50 years & above | 14 | 4.6 | <RM2500 | 196 | 64.3 | ||

| Gender | RM2501–RM4500 | 59 | 19.3 | ||||

| Male | 117 | 38.4 | RM4501–RM6500 | 28 | 9.2 | ||

| Female | 188 | 61.6 | RM6501–RM8500 | 12 | 3.9 | ||

| Education level | >RM8501 | 10 | 3.3 | ||||

| Diploma & lower | 75 | 24.6 | Brand | ||||

| Bachelor’s degree | 112 | 36.7 | Touch n Go | 123 | 40.3 | ||

| Postgraduate’s degree | 44 | 14.4 | Boost | 80 | 26.2 | ||

| Other qualifications | 74 | 24.3 | GrabPay | 71 | 23.3 | ||

| Others | 31 | 10.2 | |||||

| Item | Scale | Loadings | CR | AVE |

|---|---|---|---|---|

| Perceived quality | ||||

| PQ1 | This E-wallet brand offers good service quality. | 0.73 | 0.83 | 0.55 |

| PQ2 | This E-wallet brand is very reliable. | 0.80 | ||

| PQ3 | This E-wallet brand is of better quality compared to other brands. | 0.73 | ||

| PQ4 | This E-wallet brand is trustworthy. | 0.70 | ||

| Brand image | ||||

| BI1 | Some characteristics of this E-wallet come to my mind quickly. | 0.76 | 0.84 | 0.64 |

| BI2 | I can quickly recall the logo of this E-wallet. | 0.86 | ||

| BI3 | I have no difficulty imagining this E-wallet in my mind. | 0.78 | ||

| Brand awareness | ||||

| BA1 | I can recognize this E-wallet brand among competing brands. | 0.74 | 0.83 | 0.63 |

| BA2 | This E-wallet brand is the only brand recalled when I need to make a QR code based cashless transaction. | 0.82 | ||

| BA3 | This E-wallet brand comes up first in my mind when I need to make a QR code-based cashless transaction. | 0.81 | ||

| Usage intention | ||||

| UI1 | I intend to use this E-wallet in the next 2 months. | 0.84 | 0.88 | 0.71 |

| UI2 | I predict I will use this E-wallet in the next 2 months. | 0.87 | ||

| UI3 | I plan to use this E-wallet in the next 2 months. | 0.81 |

| PQ | BI | BA | INT | |

|---|---|---|---|---|

| PQ | ||||

| BI | 0.406 | |||

| BA | 0.422 | 0.780 | ||

| INT | 0.399 | 0.384 | 0.527 |

| Bias Corrected | |||||||

|---|---|---|---|---|---|---|---|

| Hypothesized Paths | β | S.E. | t-Value | LLCI | ULCI | Remarks | |

| H1 | BA → INT | 0.396 | 0.052 | 7.623 | 0.290 | 0.493 | Supported |

| H2 | PQ → BA → NT | 0.060 | 0.024 | 2.465 | 0.017 | 0.112 | Supported |

| H3 | BI → BA → INT | 0.201 | 0.035 | 5.718 | 0.134 | 0.271 | Supported |

| H4 | PQ → BI → BA → INT | 0.061 | 0.018 | 3.440 | 0.031 | 0.098 | Supported |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ramli, F.A.A.; Hamzah, M.I.; Wahab, S.N.; Shekhar, R. Modeling the Brand Equity and Usage Intention of QR-Code E-Wallets. FinTech 2023, 2, 205-220. https://doi.org/10.3390/fintech2020013

Ramli FAA, Hamzah MI, Wahab SN, Shekhar R. Modeling the Brand Equity and Usage Intention of QR-Code E-Wallets. FinTech. 2023; 2(2):205-220. https://doi.org/10.3390/fintech2020013

Chicago/Turabian StyleRamli, Faten Aisyah Ahmad, Muhammad Iskandar Hamzah, Siti Norida Wahab, and Rishabh Shekhar. 2023. "Modeling the Brand Equity and Usage Intention of QR-Code E-Wallets" FinTech 2, no. 2: 205-220. https://doi.org/10.3390/fintech2020013