1. Introduction

The worldwide spread of the COVID-19 pandemic has resulted in a significant economic impact that has intensified market risk aversion to a degree that has not been observed since the global financial crisis. During this period, financial markets worldwide have experienced a significant decline since January 2020. This disruption has resulted in highly high fluctuations and unpredictability. Despite the ongoing pandemic and its indeterminate long-term effects, the U.S. government has recently declared an end to the pandemic [

1], likely due to the transition to the endemic stage of the COVID-19 outbreak, characterized by the virus’s widespread presence but significantly reduced fatalities compared to 2020 [

2]. According to a study conducted by [

3], there is an adverse correlation between the number of confirmed COVID-19 cases and the U.S. stock market returns. The study further found that stock markets responded reasonably quickly to the increase in confirmed cases rather than deaths. Therefore, the impact of the crisis on financial markets and the broader economic environment, including consumer behavior and intentions, has been a topic of concern among many scholars [

3,

4,

5,

6,

7]. From this standpoint, asset management has become crucial for organizations seeking to optimize their asset utilization and maximize returns in challenging conditions and volatile markets.

The ongoing pandemic and its consequential impact on financial markets have already elicited significant scholarly attention. In the near future, this outbreak is expected to serve as a standard for comparison, exceeding the level of interest observed during previous crises of similar nature. Developing models that yield accurate stock market fluctuation predictions is fundamental to improving the informational base, meeting the investor’s goals and return expectations, and accommodating risk tolerance over a specified investment period. This is because asset allocation is a strategic approach that seeks to attain an equilibrium between risk and return by adjusting the proportion of each asset in a portfolio. Despite this exercise’s significance for risk management predictions, only a few prior studies (see [

8,

9,

10,

11]) have focused on the European stock market and attempted to estimate the key financial markets’ volatility. At the same time, the financial markets literature on forecasting cryptocurrencies, U.S. stock, and commodity market volatility is more mature; refer, for example, to recent academic research by [

5,

12,

13,

14,

15,

16,

17]), which has made predictions regarding significant incidents, such as COVID-19 and its economic consequences, while also examining the impact of past pandemics.

Therefore, this study aims to address the discrepancy in the literature on forecasting market fluctuations by examining the European stock market indices. The availability of financial market information has increased, strengthening the correlation between market distribution and other factors. Over the past decades, a significant body of research has grown on forecasting time series using various linear, nonlinear, and hybrid linear-nonlinear models. In this study, we employed the application of traditional statistical models, such as the autoregressive integrated moving average (ARIMA) [

18], as well as machine learning (ML), deep learning (DL), such as the long short-term memory (LSTM) and hybrid forecasting models, i.e., the ETS-ANN model [

19] to evaluate the volatility of the European stock markets. The European stock market encompasses a wide range of stock exchanges, including major ones, such as the London Stock Exchange (LTSE), Euronext (N100), Deutsche Börse (GDAXI), the French stock market (FCHI), and the Swiss Stock Exchange (SSMI).

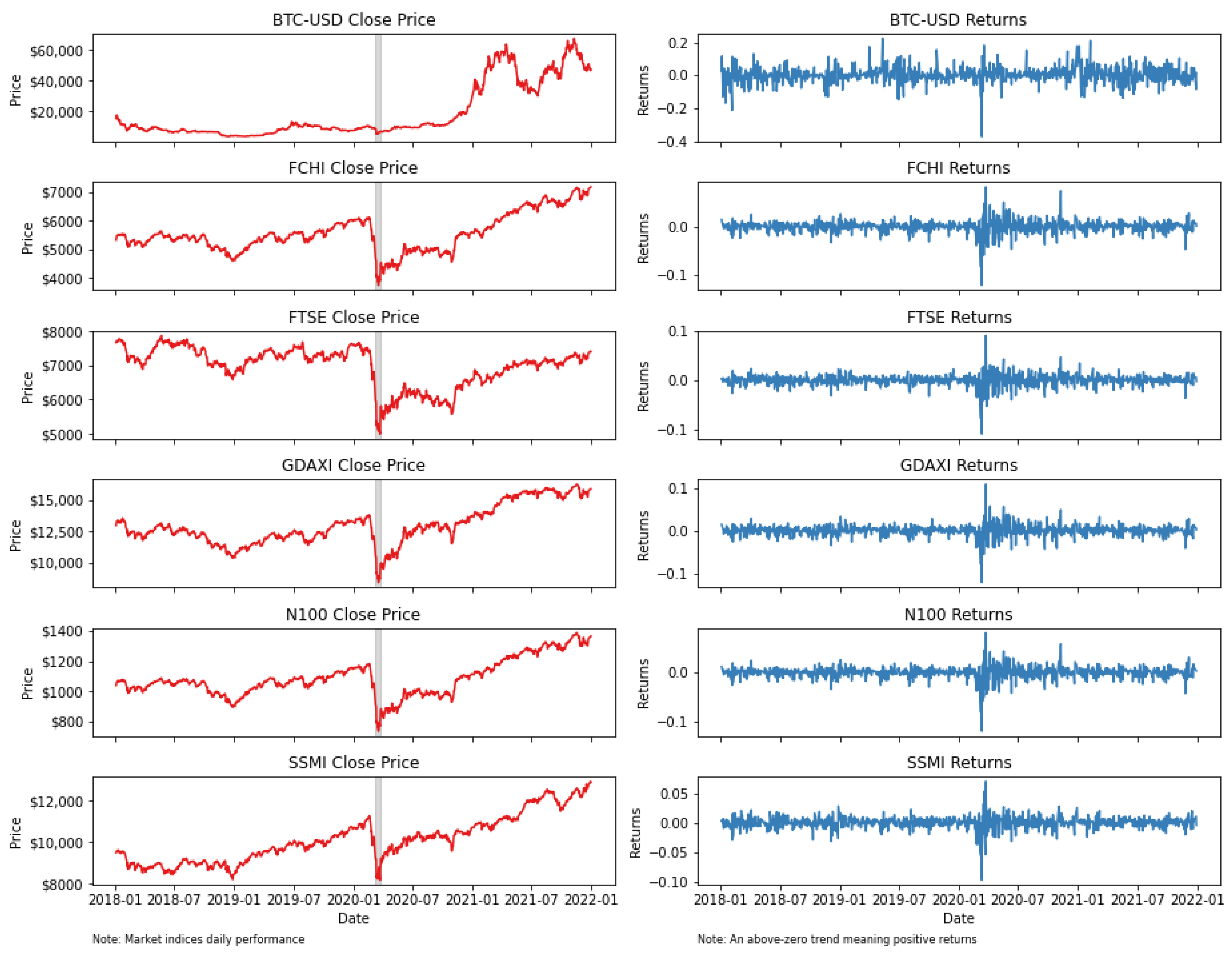

This study contributes twofold to the expanding body of literature in the field. First, it examines the distribution of fluctuations between the European stock market and cryptocurrency in three subperiods: before, during, and ongoing the COVID-19 outbreak. We chose to examine the European stock market because the COVID-19 pandemic has, from one side, severely impacted each European country. Still, on the other side, each government has imposed diverse restrictions within various time frames. For the financial markets, the COVID-19 pandemic constitutes a systematic risk factor. In this context, government-imposed restrictions on spreading the virus could not prevent the negative consequences of the financial stock markets’ trajectory [

3]. However, observing the cryptocurrency market, we picture a different likelihood (see,

Figure 1). Hence, examining the correlation between the European stock market and the cryptocurrency markets during this period is critical. This analysis of the cross-market relationships offers valuable information for financial market players concerning financial risk management. Bitcoin is the most well-known cryptocurrency with the highest capitalization and it serves as a benchmark for investors and academics. Hence, any disruptions in this market may also have ripple effects on the global financial market. Second, exploring various forecasting models, such as statistical, ML, DL, and hybrid models, we examine the dynamics of market distribution to provide an understanding of the market predictability among the European stock markets and Bitcoin during the COVID-19 pandemic through an analysis of daily data.

Our results show that predicting BTC-USD distributions is challenging, and the accuracy levels are generally low, especially in 2018 and 2019. GDAXI is more predictive than BTC-USD, and the ETS-ANN and kNN models perform both in different subperiods. The ARIMA and ETS-ANN models perform better than the kNN model for predicting the FTSE index’s performance, but their performances were generally weak in 2018–2021 and 2020. ARIMA and ETS-ANN models perform better over extended periods than the kNN model, with ARIMA being the best-performing model in 2018–2021 and the hybrid ETS-ANN model in 2020. The hybrid ETS-ANN model shows significant potential for forecasting financial time series in this context.

The subsequent sections of the document are organized as follows:

Section 2 provides a short review of the literature on financial market forecasts through machine learning techniques.

Section 3 discusses the data collection and modeling methodologies.

Section 4 compares the different models’ accuracy measures and outcomes. The article concludes with the fifth section, including future research suggestions.

4. Discussion

Table 3 reports the accuracy metrics for three different time series forecasting models, namely, ARIMA, ETS-ANN, and

kNN, for different SSMI financial market assets, i.e., BTC-USD, GDAXI, FTSE, N100, FCHI, and SSMI, from 2018 to 2021. The accuracy of the models is evaluated based on the following metrics: mean absolute error (MAE), root mean square error (RMSE), and the mean absolute percentage error (MAPE).

The findings indicate that the ranking of the models’ performance remains consistent across each examined subperiod. Based on all accuracy metrics, it can be observed that the hybrid ETS-ANN model is the prevailing model for studying the specific dataset of financial market assets. According to the MAPE metric, the ETS-ANN model had the lowest value for almost all indices and subperiods except for the entire period results. The kNN model displayed some lower results during the pro-COVID-19 period of 2018 and 2019 for the BTC, FTSE, and SSMI indices. In contrast, ARIMA had a lower MAPE for almost all financial market assets for the entire period, except the BTC market and the pro-COVID-19 period for the BTC, GDAXI, N100, and FCHI indices. Therefore, the choice of the most suitable model for a particular financial market asset and period depends on the specific characteristics of the data and the modeling assumptions. Overall, the results suggest that the hybrid ETS-ANN model is a promising financial time series forecasting approach and can offer valuable perspectives to support investment decision-making.

More specifically, starting with BTC-USD, which represents the Bitcoin–USD exchange rate, we notice that all models show high error rates in predicting the exchange rate for all three years. Specifically, in the 2018–2021 forecast period, the MAPE values for the three models ranged from 15.48% to 28.45%, indicating that the model’s predictions were off by more than 15% to 28% of the actual value. The best-performing model in this period is ETS-ANN, which achieves a MAPE of 15.48%, indicating a moderate accuracy level. In the year 2018, the ETS-NN model had the highest MAE, RMSE, and MAPE values, indicating less accurate forecasts compared to ARIMA and kNN models. ARIMA performs better than both ETS-NN and kNN in terms of every accuracy measure. In 2019, the models’ performance worsened, with the MAPE values ranging from 8.58% to 44.08%. Similar to the previous period, the best-performing model in 2019 was the ETS-ANN, which achieved a MAPE of 8.58% and a low MAE comparable to other models, indicating a higher level of accuracy. In 2020, the models’ performance weakened, with high MAPE values ranging from 22.51% to 37.23%, with the kNN showing the best performance. It is also worth noticing that during the first wave of the COVID outbreak in 2020, the kNN model achieved the lowest MAE, indicating a moderate level of accuracy. Similarly, in 2021, during the ongoing pandemic, the ETS-ANN model generated the best MAPE with a value of 8.39%. Overall, the results suggest that predicting BTC-USD is challenging for the selected models, and the accuracy levels are generally low, especially in 2020.

Moving to GDAXI, we observe that the models’ performance is relatively better than BTC-USD. For the whole period, the MAPE values for the three models ranged from 2.45% to 9.52%, indicating that the predictions were off by less than 10% of the actual value. The best-performing model is the ARIMA model, which achieves the lowest MAPE 2.45% and the lowest MAE, indicating a good level of accuracy. Starting with the year 2018, the kNN and ARIMA models show similar forecast accuracies with lower MAE, RMSE, and MAPE values compared to ETS-NN. In 2019, the models’ performance declined, with the MAPE values ranging from 3.91% to 5.89%. The best-performing model in 2019 was ARIMA, which achieved a MAPE of 3.91%. In 2020, the models’ performance worsened even further, with the MAPE values ranging from 1.35% to 16.64%. The best model, ETS-ANN, achieved the lowest MAPE, which was also similar in the post-COVID year 2021. Overall, the results suggest that predicting GDAXI is more predictable than estimating the BTC-USD, and the ETS-ANN and the ARIMA models perform in different subperiods to a great extent.

The analysis shows that the ARIMA and ETS-ANN models perform better than the kNN model for predicting the FTSE index’s performance. As such, the models’ performance is generally considered moderate, particularly during the periods of 2018–2021 and 2020. In the entire period, the MAPE values for the three models ranged from 2.38% to 6.88%, with ARIMA being the best-performing model, followed by the ETS-ANN model (6.35%). In 2018, the ETS-NN method demonstrated the best forecast accuracy with significantly low MAPE (1.70%) compared to ARIMA and kNN (3.59%), respectively. In 2019, the models’ performance improved, with the MAPE values ranging from 1.56% to 2.00%. In 2020, the models’ performance drastically dropped, with the MAPE values ranging from 6.05% to 8.18%, indicating a considerable increase in prediction errors. The best-performing model in 2020 was the ETS-ANN model, followed by kNN, which achieved MAPE values of 6.05% and 6.34%, respectively. Similarly, in 2021, the ETS-ANN outperformed the other models.

As for the N100 index, the models’ performance is generally better than other indices. During the 2018–2021 period, MAPE values ranged from 4.40% to 12.37%, with ARIMA outperforming the other models. In 2019, the models’ performance was better, with the MAPE values ranging from 2.91% to 4.00%. In 2018, both ARIMA and ETS-NN methods showed quite similar forecast accuracies with lower MAPE values than kNN, with ETS-NN (MAPE: 3.76%) outperforming the other models. Similarly, the best-performing model in 2019 was ARIMA, which achieved a MAPE of 2.91%. In 2020, the models’ performance dropped due to the pandemic, with the MAPE values ranging from 7.71% to 10.54%, with kNN outperforming the other models, followed closely by the ETS-ANN model. In the year 2021, ETS-ANN showed more robust accuracy results, surpassing the other two models with a MAPE of 2.94%, and demonstrating better performance across all other measures compared to the other models. The FCHI index indicates that the models’ performance is generally weak, especially during the pandemic year 2020. The analysis shows that the ARIMA and ETS-ANN models performed better over more periods than the kNN model. For the 2018–2021 period, ARIMA generated the most robust predictive results, outperforming the other models, with a MAPE value of 5.24%, while ETS-ANN provided the worst accuracy (11.27%). In 2018, both ARIMA and ETS-NN models exhibited similar forecast accuracies, with slightly lower MAE and RMSE values compared to kNN, with ETS-NN outperforming ARIMA. In 2019, the models’ performance slightly improved, with the MAPE values ranging from 3.56% to 4.72%, with a similar performance ranking ARIMA as the best model, followed by the hybrid ETS-ANN model. In 2020, the models’ performance drastically dropped, with the MAPE values ranging from 8.18% to 9.66%, indicating a considerable increase in prediction errors. The best-performing model in 2020 was the hybrid ETS-ANN model, followed by kNN, which achieved a MAPE value of 9.01%. In the end, the ETS-ANN outperformed the other models in the year 2021.

Finally, the SSMI index performed worse than the comparable indices, except the BTC, for almost every period. The models’ performance was generally weak, especially in 2018–2021 and post-pandemic 2021. In the 2018–2021 period, the MAPE values for the three models ranged from 7.03% to 8.54%, with ARIMA being the best-performing model. However, the kNN model generated almost similar MAE accuracy to ARIMA for the same period. Starting in the year 2018, all three models showed comparable forecast accuracies for the SSMI index, with slightly lower MAE and RMSE values for kNN, and ARIMA showing equal MAPE with the ETS-NN (1.81%). In 2019, the models’ performance slightly improved, with the kNN model generating a more robust MAPE value of 3.73% and similarly better MAE performance. During the pandemic, the models’ performance surprisingly improved, with MAPE values ranging from 0.97% to 6.22%, indicating a considerable and robust increase in prediction errors. The best-performing model in 2020 was the ETS-ANN model, followed by the kNN model, which achieved a MAPE of 2.98%. Finally, the ETS-ANN outperformed the other models in 2021 with more robust MAPE and MAE accuracies. The analysis shows that the ARIMA and kNN models performed with high precision, similar to the ETS-ANN model, except for one period.

Following the previous analysis of the financial market assets, we evaluated the performances of three different time series forecasting models, namely, the ARIMA, ETS-ANN, and kNN, from 2018 to 2021. The findings indicate that the hybrid ETS-ANN model is the prevailing choice for examining the specific dataset of financial market assets, with the lowest MAPE for almost all indices and subperiods except for the 2018–2021 period results. On the other side, MAPE received criticism due to some drawbacks; thus, considering MAE, we observe that the ARIMA and kNN models demonstrated similar performance in several subperiods. Therefore, the choice of the most suitable model depends on the specific characteristics of the data and the modeling assumptions. In conclusion, the hybrid ETS-ANN model is a promising financial time series forecasting approach that can provide valuable investment decision insights.

Table 4 shows the average relative MAE results per year. The results reveal that the ETS-NN and

kNN models outperformed ARIMA in most cases. Therefore, ETS-NN had the lowest AvgRelMAE for all asset indices in 2020 during the outbreak and in 2021, while

kNN exceeded ARIMA and had a low MAE in 2020. However, ARIMA outperformed both models during 2018–2021, except the ETS-NN model for BTC, and generated the lowest AvgRelMAE for almost every asset index, except BTC and FTSE in 2019. In 2018, we observed that ARIMA outperformed, in many cases, the other methods, except the ETS-NN model for the FTSE, N100, and FCHI indices. Similarly,

kNN generated better forecasting accuracy than ARIMA in the GDAXI and FTSE indices. Finally, ARIMA outperformed the

kNN model for every asset index except the BTC and SSMI in 2021. Once again, the performances of the models varied across financial market indices and years, highlighting the importance of selecting the appropriate model for a particular market and period.

5. Conclusions

According to the literature, studies evaluating the European financial markets’ performance are scant because of the extensive number of publications focusing on the U.S. market. This study aims to compare parametric and non-parametric forecasting models, such as the ARIMA, Hybrid ETS-ANN, and kNN predictive models, in predicting the key European stock market indices and comparing them to the cryptocurrency market for an extended period, including the pandemic in 2020. The study period was divided into three subperiods: the pre-pandemic period, the pandemic period, and the continuous period.

It is worth noting that the performances of the models varied across different indices and years, indicating that the choice of the best model should depend on the specific context and data. Overall, the ARIMA and ETS-ANN models performed better than the kNN model while evaluating the model’s accuracy. For instance, the ARIMA model ranks better and unexpectedly outperforms the hybrid ETS-ANN and kNN machine learning models. The ARIMA model performed better for the BTC and GDAXI indices before COVID-19, as it is a commonly used model in finance and has been shown to perform well in time series forecasting. The cryptocurrency market is known for its fluctuation and unpredictability, making it challenging to forecast accurately.

Unsurprisingly, ARIMA performed well in the years 2018 and 2019. On the other hand, the kNN model showed better results for the FTSE and SSMI indices during the pro-COVID-19 period. It is also interesting to see that kNN outperformed the other models in 2020 because it is not a traditional time series forecasting model but rather a machine learning algorithm for classification and regression.

In conclusion, the results suggest that the ETS-ANN model is the best-performing model despite its moderate level of accuracy. The low MAPE values across almost all subperiods indicate that the model predictions perform well in different subperiods. Therefore, it is essential to carefully evaluate the performances of other models and choose the one that provides the most reliable and accurate forecast for the specific application.

As with any study, there are limitations. For example, although we used different hyperparameters for the ARIMA and kNN models based on the year and financial index in this study, we used the same hyperparameters across years for the hybrid ETS-ANN model. Further research could investigate the performances of other forecasting models or consider additional variables and parameters to improve the accuracies of financial market predictions. In addition, researchers could analyze how past events such as COVID-19 have impacted the financial sector and compare financial indices to a broader range of cryptocurrencies. Comparing COVID-19 to past events could create a portfolio suitable for today’s highly interconnected and unpredictable economic landscape.

{kind=link}