A Monte Carlo Approach to Bitcoin Price Prediction with Fractional Ornstein–Uhlenbeck Lévy Process

Abstract

:1. Introduction

2. Materials and Methods

- The process is likely to reverse the trend over the time frame considered.

- The process is random in which knowing one data point does not provide insight into predicting future data points.

- The process is persistent in the sense that a future data point is likely to be similar to a data point preceding it.

2.1. Fractional Brownian Motion

2.2. Lévy Process

2.2.1. Infinitely Divisible Distributions

2.2.2. Continuous-Time Stochastic Processes

- The random variables are independent for all and (independent increments);

- has the same distribution as for all (stationary increments);

- L is stochastically continuous; that is, for all and .

- The paths are right-continuous with left limits (cadlag-continue á droite et limite á gauche).

2.2.3. Normal Inverse Gaussian

- iv) (Poisson distribution).

2.3. Fractional Ornstein–Uhlenbeck Lévy Process

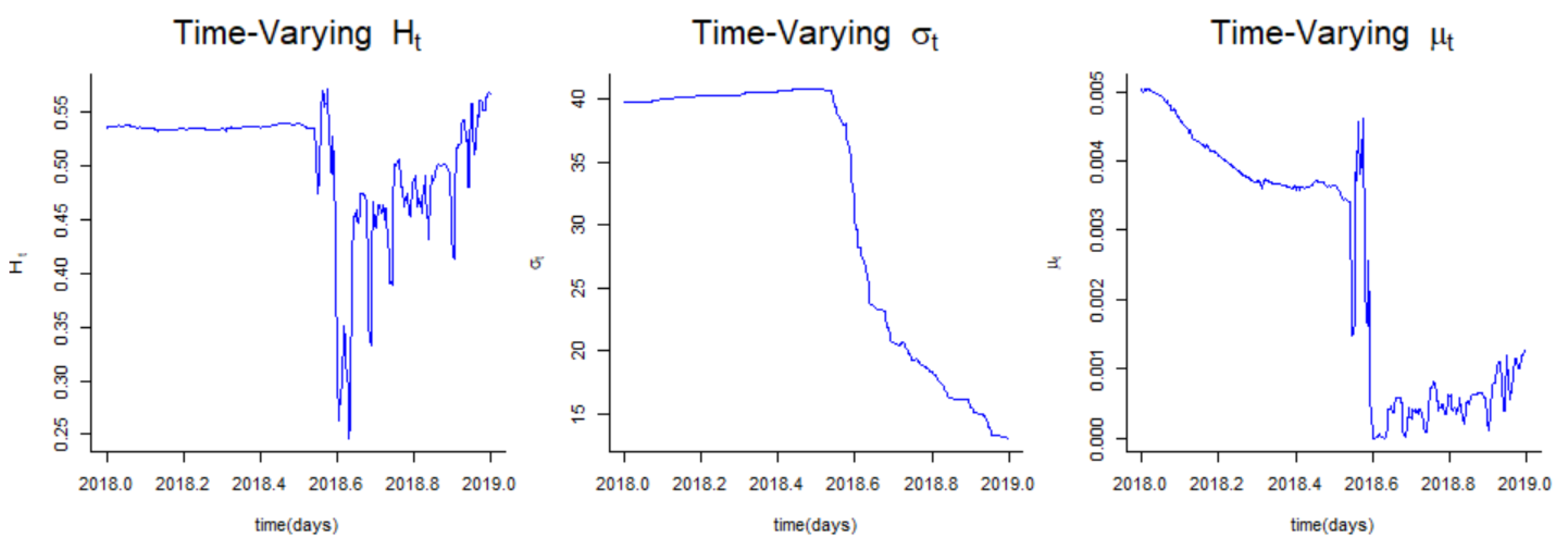

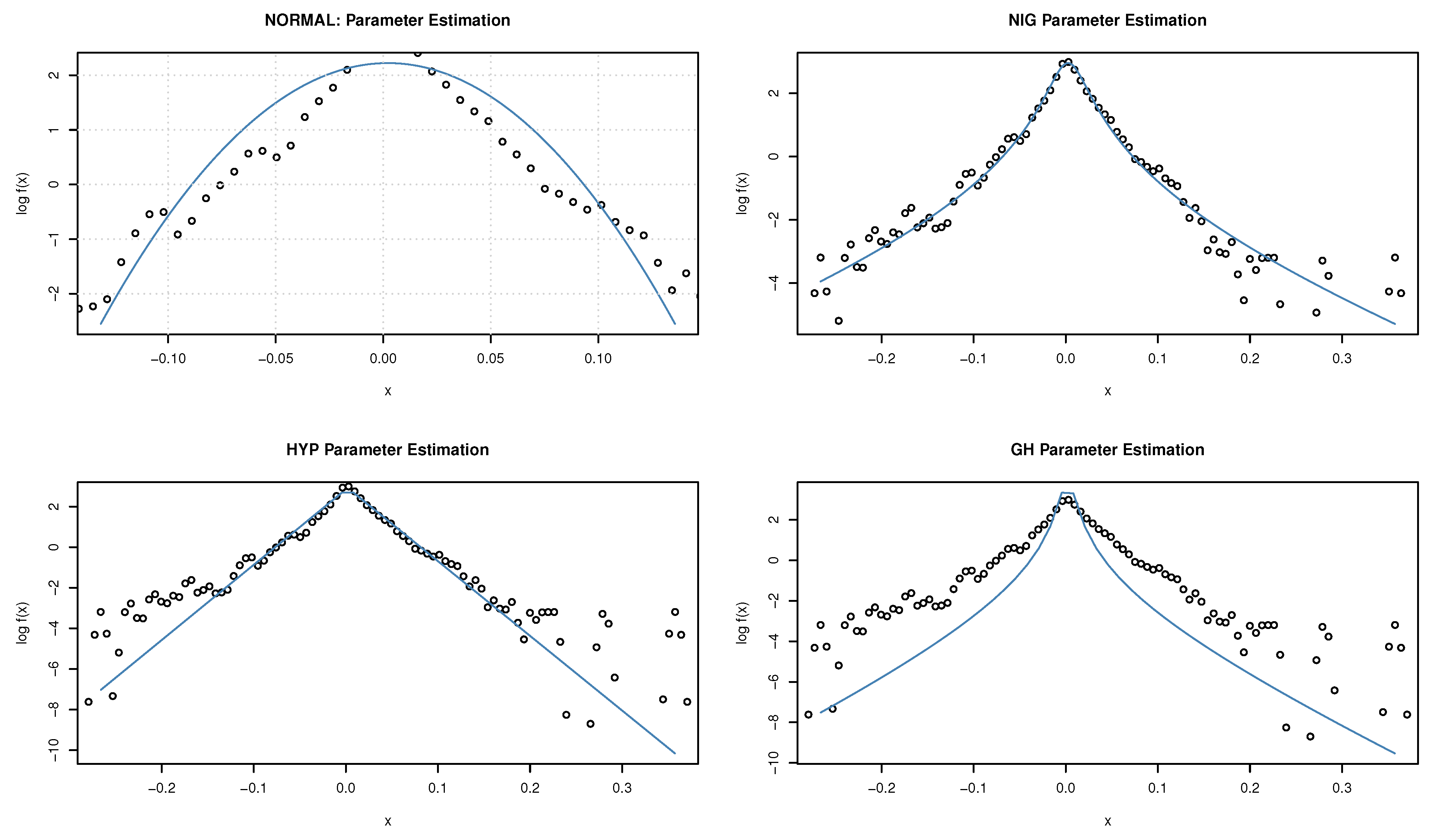

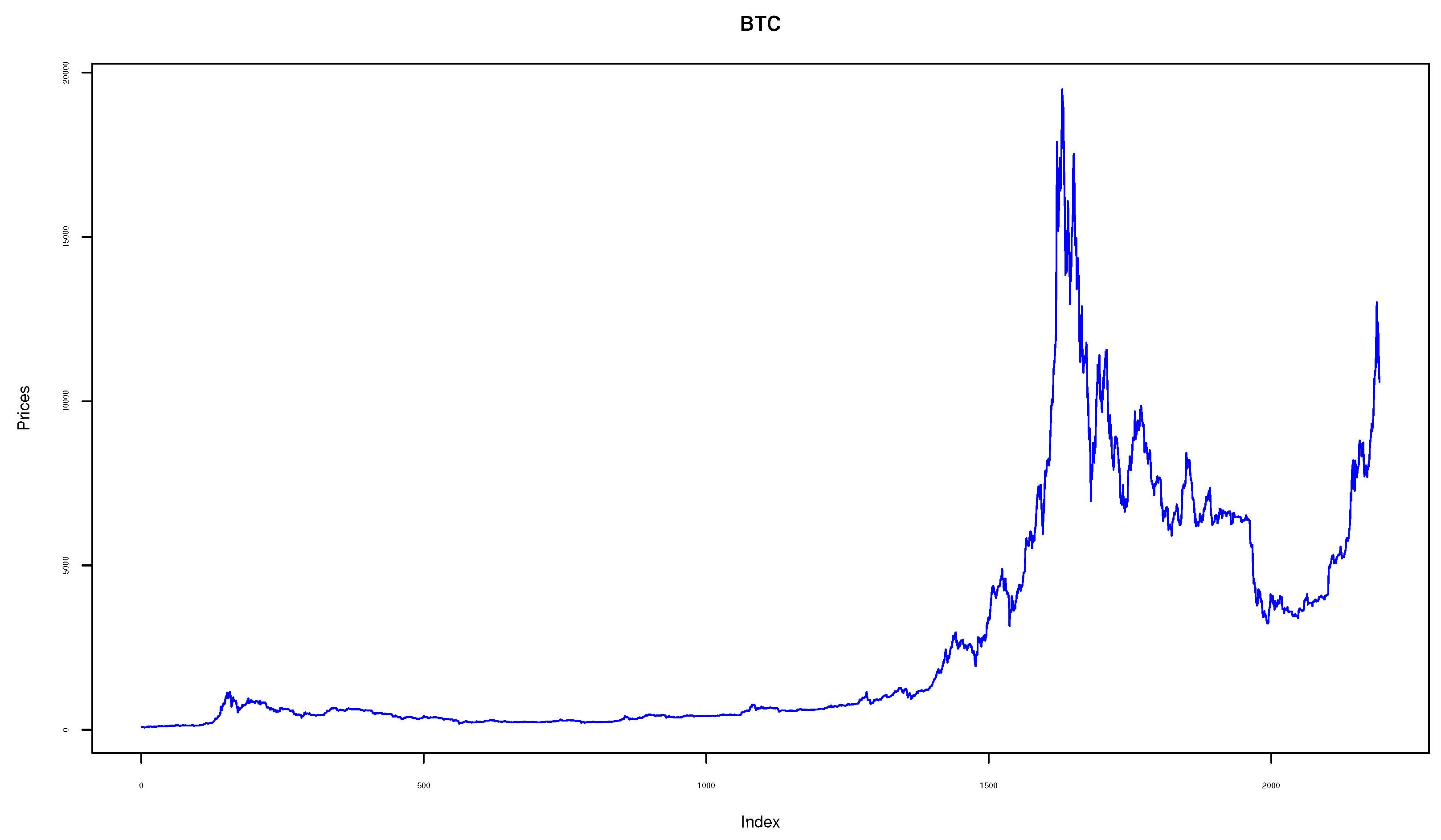

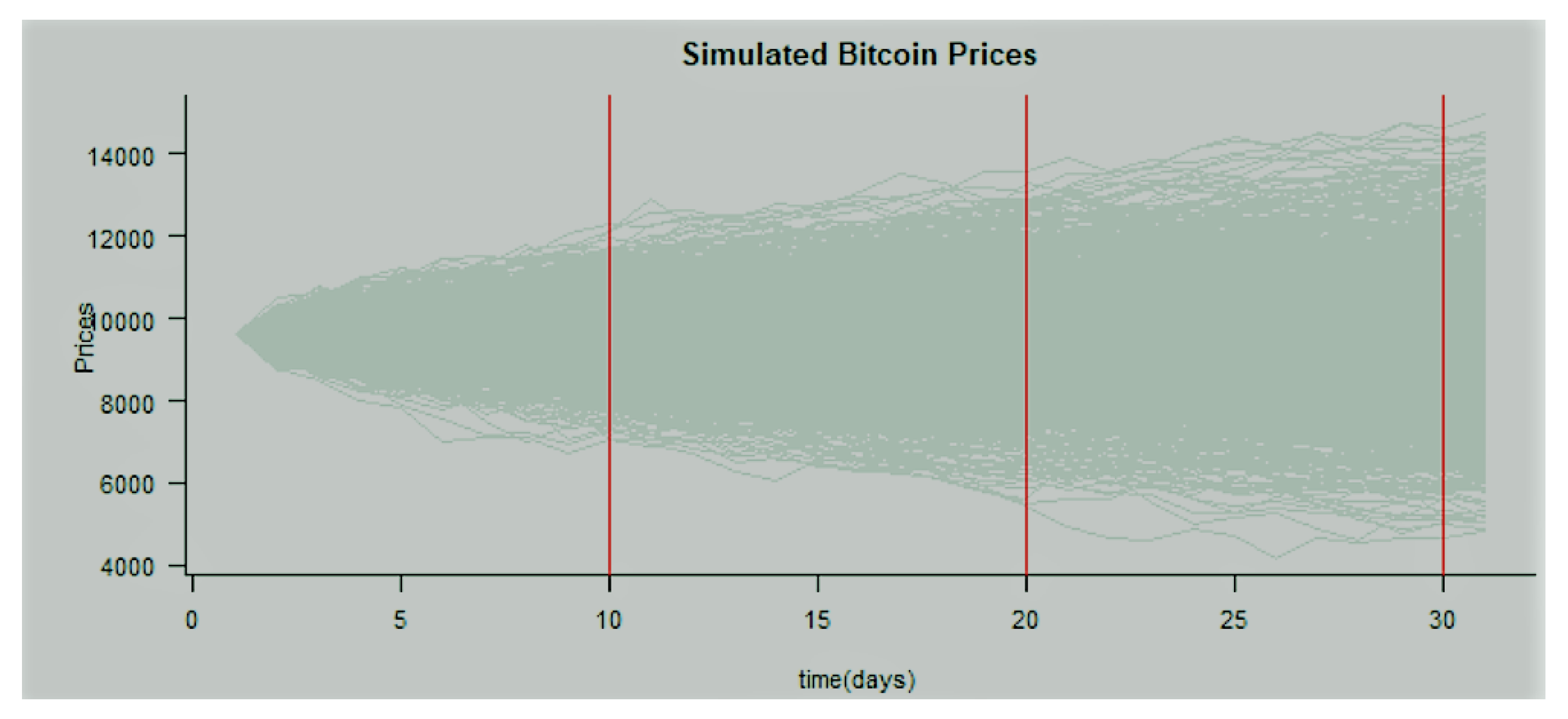

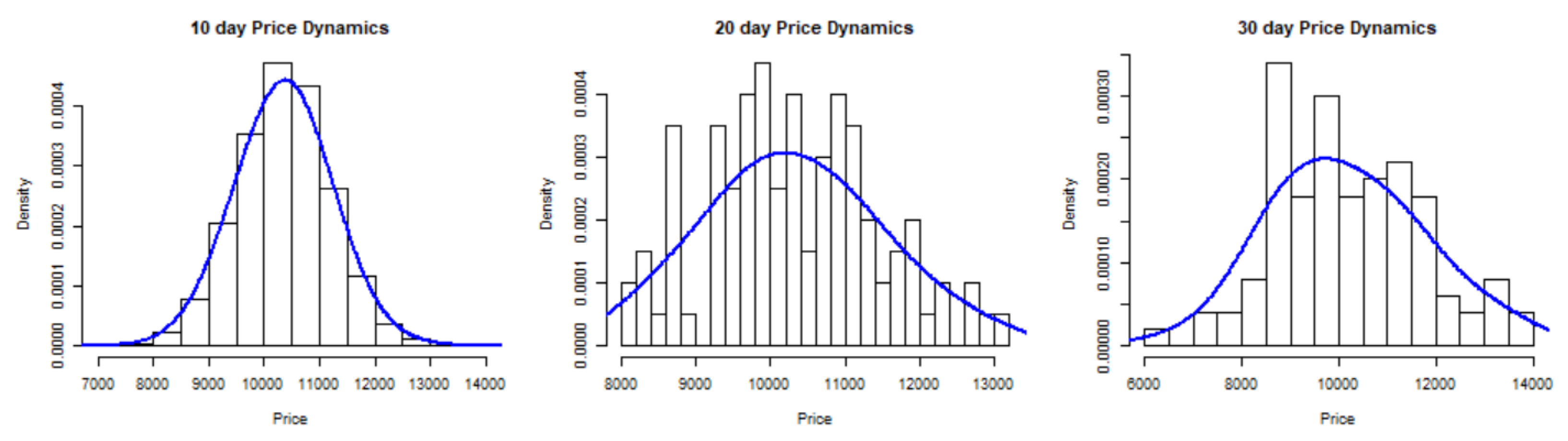

3. Results

4. Discussion

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Nakamoto, S. Re: Bitcoin P2P e-cash paper. Email Posted List. 2008, 9, 4. [Google Scholar]

- Yermack, D. Is Bitcoin a real currency? An economic appraisal. In Handbook of Digital Currency; Elsevier: Amsterdam, The Netherlands, 2015; pp. 31–43. [Google Scholar]

- Yermack, D. Corporate governance and blockchains. Rev. Financ. 2017, 21, 7–31. [Google Scholar] [CrossRef] [Green Version]

- Dwyer, G.P. The economics of Bitcoin and similar private digital currencies. J. Financ. Stab. 2015, 17, 81–91. [Google Scholar] [CrossRef] [Green Version]

- Ken-Iti, S. Lévy Processes and Infinitely Divisible Distributions; Cambridge University Press: Cambridge, UK, 1999. [Google Scholar]

- Cont, R.; Tankov, P. Nonparametric calibration of jump-diffusion option pricing models. J. Comput. Financ. 2004, 7, 1–49. [Google Scholar] [CrossRef] [Green Version]

- Katsiampa, P. Volatility estimation for Bitcoin: A comparison of GARCH models. Econ. Lett. 2017, 158, 3–6. [Google Scholar] [CrossRef] [Green Version]

- Cheah, E.T.; Fry, J. Speculative bubbles in Bitcoin markets? An empirical investigation into the fundamental value of Bitcoin. Econ. Lett. 2015, 130, 32–36. [Google Scholar] [CrossRef] [Green Version]

- Scaillet, O.; Treccani, A.; Trevisan, C. High-frequency jump analysis of the bitcoin market. J. Financ. Econom. 2020, 18, 209–232. [Google Scholar]

- Hencic, A.; Gouriéroux, C. Noncausal autoregressive model in application to bitcoin/USD exchange rates. In Econometrics of Risk; Springer: Cham, Switzerland, 2015; pp. 17–40. [Google Scholar]

- Tarnopolski, M. Modeling the price of Bitcoin with geometric fractional Brownian motion: A Monte Carlo approach. arXiv 2017, arXiv:1707.03746. [Google Scholar]

- McNally, S. Predicting the Price of Bitcoin Using Machine Learning. Ph.D. Thesis, National College of Ireland, Dublin, Ireland, 2016. [Google Scholar]

- McNally, S.; Roche, J.; Caton, S. Predicting the price of Bitcoin using Machine Learning. In Proceedings of the 2018 26th Euromicro International Conference on Parallel, Distributed and Network-based Processing (PDP), Cambridge, UK, 21–23 March 2018; pp. 339–343. [Google Scholar]

- Jalali, M.F.M.; Heidari, H. Predicting changes in Bitcoin price using grey system theory. Financ. Innov. 2020, 6, 13. [Google Scholar]

- Gatabazi, P.; Mba, J.C.; Pindza, E.; Labuschagne, C. Grey Lotka- Volterra models with application to cryptocurrencies adoption. Chaos Solitons Fractals 2019, 122, 47–57. [Google Scholar] [CrossRef]

- Gatabazi, P.; Mba, J.C.; Pindza, E. Modeling cryptocurrencies transaction counts using variable-order Fractional Grey Lotka-Volterra dynamical system. Chaos Solitons Fractals 2019, 127, 283–290. [Google Scholar] [CrossRef]

- Gatabazi, P.; Mba, J.C.; Pindza, E. Fractional gray Lotka- Volterra models with application to cryptocurrencies adoption. Chaos Interdiscip. J. Nonlinear Sci. 2019, 29, 073116. [Google Scholar] [CrossRef] [PubMed]

- Wu, L.; Liu, S.; Yao, L.; Yan, S. The effect of sample size on the grey system model. Appl. Math. Model. 2013, 37, 6577–6583. [Google Scholar] [CrossRef]

- Chen, H.; De, P.; Hu, Y.J.; Hwang, B.H. Wisdom of crowds: The value of stock opinions transmitted through social media. Rev. Financ. Stud. 2014, 27, 1367–1403. [Google Scholar] [CrossRef]

- Kristoufek, L. What are the main drivers of the Bitcoin price? Evidence from wavelet coherence analysis. PLoS ONE 2015, 10, e0123923. [Google Scholar] [CrossRef] [PubMed]

- Lahmiri, S.; Bekiros, S.; Salvi, A. Long-range memory, distributional variation and randomness of bitcoin volatility. Chaos Solitons Fractals 2018, 107, 43–48. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| 29 July | 8 August | 18 August | |

|---|---|---|---|

| Quantiles | 10 Day | 20 Day | 30 Day |

| 25% | 9812 | 9590 | 8915 |

| 50% | 10,360 | 10,283 | 9956 |

| 75% | 10,841 | 11,029 | 11,161 |

| 90% | 11,342 | 11,818 | 12,049 |

| 95% | 11,881 | 12,245 | 13,157 |

| 99% | 11,963 | 12,885 | 13,600 |

| mean | 10,085.65 | 10,085.66 | 10,085.68 |

| skweness | −0.0899 | −0.0891 | −0.0626 |

| kurtosis | 1.1390 | 0.5511 | 0.3755 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Mba, J.C.; Mwambi, S.M.; Pindza, E. A Monte Carlo Approach to Bitcoin Price Prediction with Fractional Ornstein–Uhlenbeck Lévy Process. Forecasting 2022, 4, 409-419. https://doi.org/10.3390/forecast4020023

Mba JC, Mwambi SM, Pindza E. A Monte Carlo Approach to Bitcoin Price Prediction with Fractional Ornstein–Uhlenbeck Lévy Process. Forecasting. 2022; 4(2):409-419. https://doi.org/10.3390/forecast4020023

Chicago/Turabian StyleMba, Jules Clément, Sutene Mwambetania Mwambi, and Edson Pindza. 2022. "A Monte Carlo Approach to Bitcoin Price Prediction with Fractional Ornstein–Uhlenbeck Lévy Process" Forecasting 4, no. 2: 409-419. https://doi.org/10.3390/forecast4020023