Connectedness between Pakistan’s Stock Markets with Global Factors: An Application of Quantile VAR Network Model

, , , , and

, , , , and

Abstract

:1. Introduction

- Studying the interconnectedness among global factors and main sector-level indices might offer developing countries like Pakistan valuable insights into the varying impacts of global factors on their stock market across different sectors. This study will provide valuable insights to policymakers and investors for their future actions.

- The prior literature has concentrated on related concerns at the aggregate and specific level or related to certain markets, particularly oil, energy, and non-energy commodities [13]. Limited studies, however, examine the nature of spillover effects at the sector level in Pakistan [14,15]. However, none of them have evaluated this association regarding connectedness among markets.

- There has been no research on quantile connectedness based on extreme events to determine how the global crude oil WTI index, MSCI index, European economic policy uncertainty, and significant sector-level specific indices of Pakistan are connected in a network and pairs. Evaluating tail risk behavior can help investors avoid the devastating impacts of left tail events’ shocks while achieving financial investment objectives [16]. As a result, this study will be unique in examining such interrelationships among these variables and various sector-level indices.

1.1. Statement of Problem

1.2. Objectives of Study

- (1)

- To determine the simultaneous influence and network connectedness among global crude oil price shocks, exchange rate fluctuations, and economic policy uncertainty and indices of different sectors in Pakistan.

- (2)

- To examine net pairwise directional connectedness among variables and sector level indices

1.3. Research Questions

- (1)

- Whether the global WTI crude oil price index, MSCI index, European economic policy uncertainty (EPEUI), and significant sector-level indices of Pakistan have total network connectedness.

- (2)

- How much pairwise connectedness does the WTI crude oil index, MSCI Index, and EPEUI have with individual significant sector-level indices of Pakistan?

2. Literature and Theoretical Underpinnings

2.1. Global WTI Crude Oil Index and Sector Level Indices

2.2. MSCI Index and Sector Level Indices

2.3. Economic Policy Uncertainty (EPU) and Sector-Level Indices

2.4. Global Factors and Commodity Prices

3. Research Methodology

3.1. Empirical Methodology

3.2. Quantile VAR (QVAR) Connectedness Approach

- (1)

- (2)

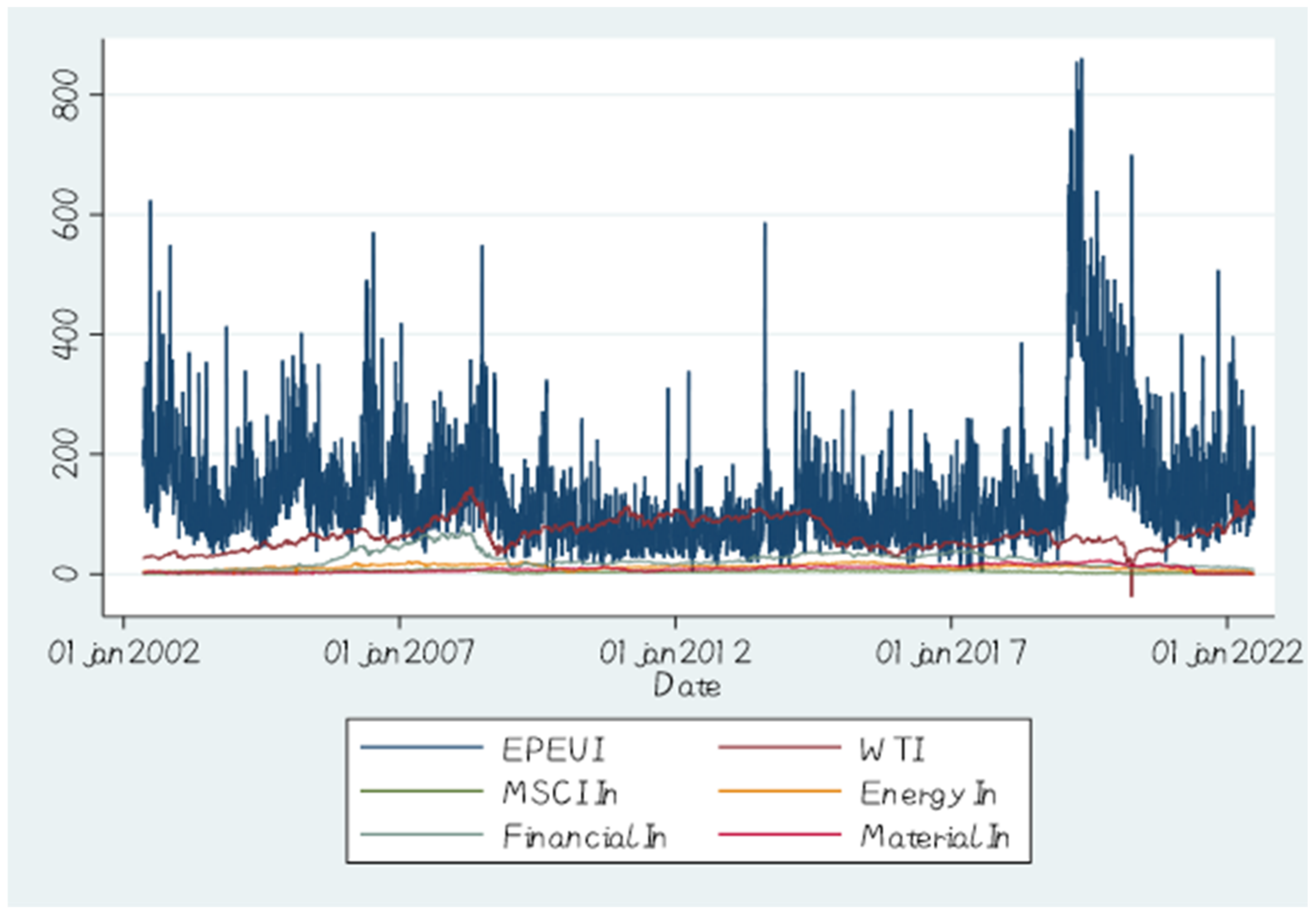

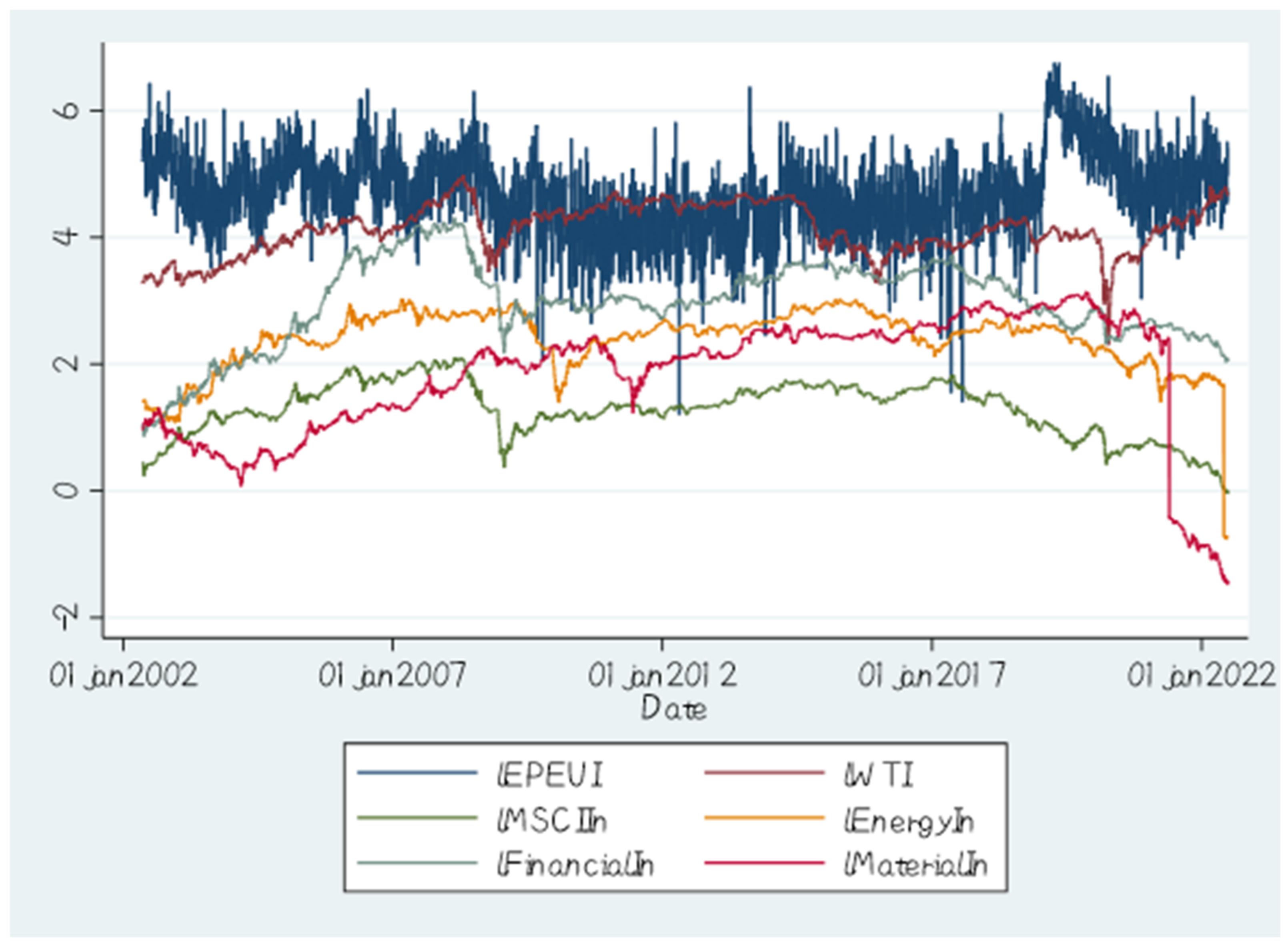

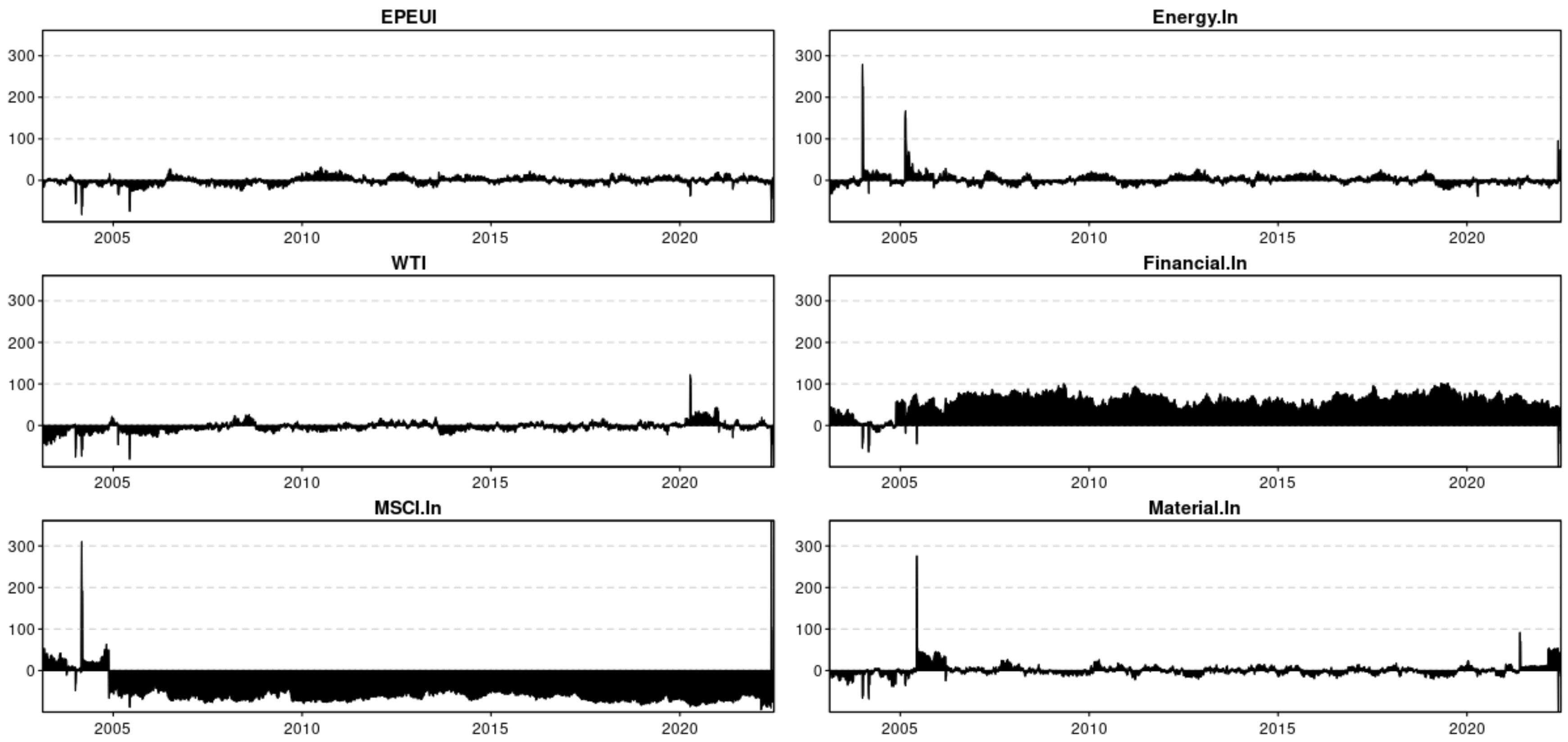

4. Data and Preliminary Statistics

5. Findings and Discussion

5.1. The Net Total Directional Connectedness

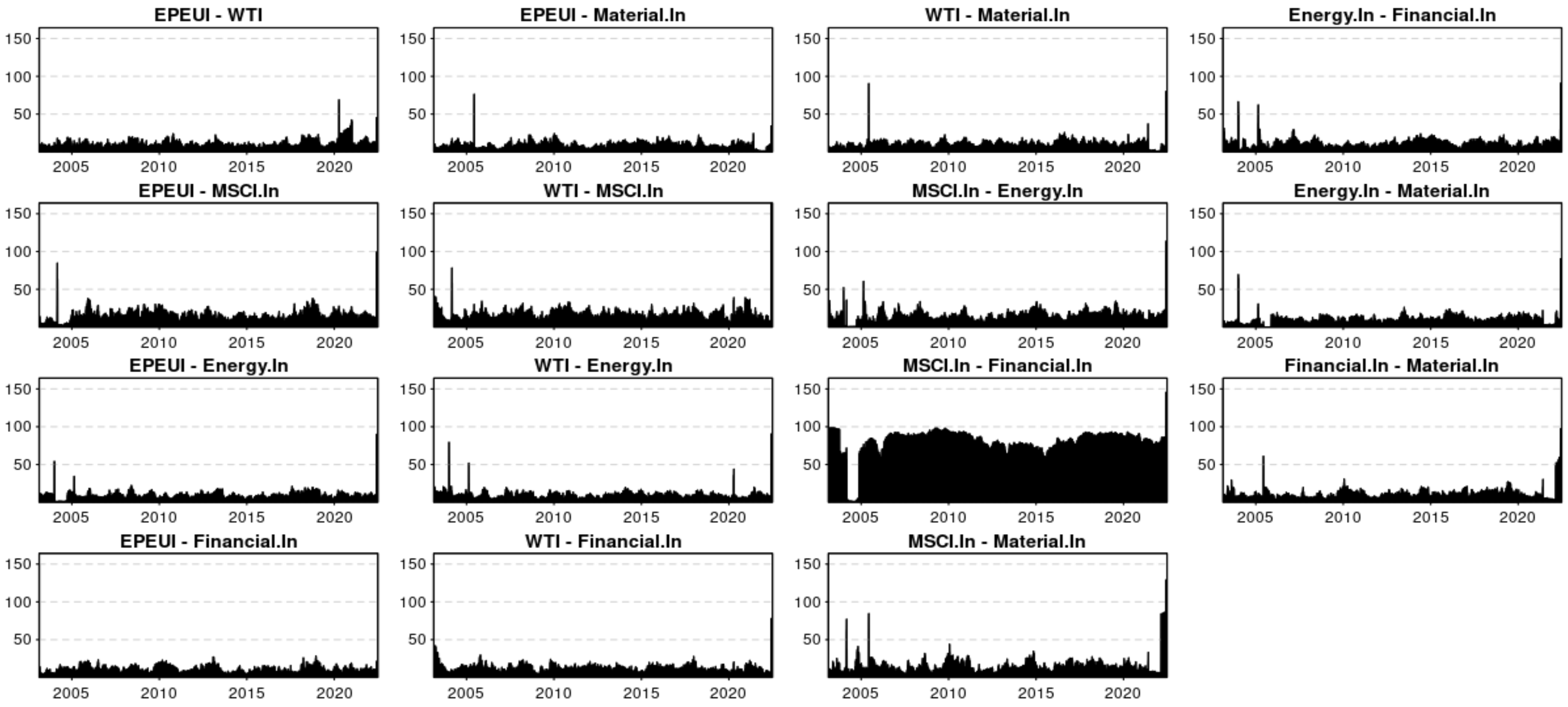

5.2. Dynamic Pairwise Directional Connectedness

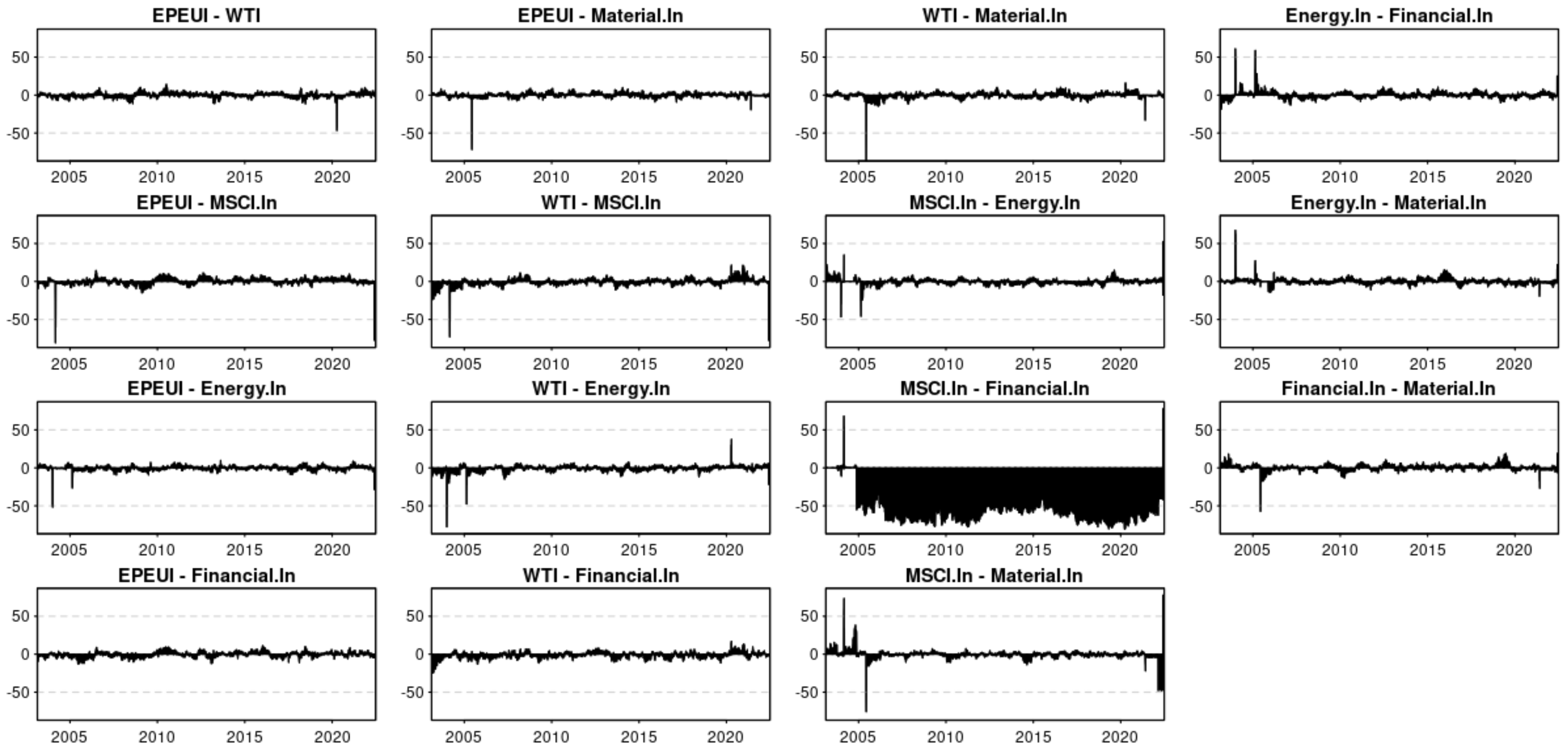

5.3. Net Pairwise Directional Connectedness

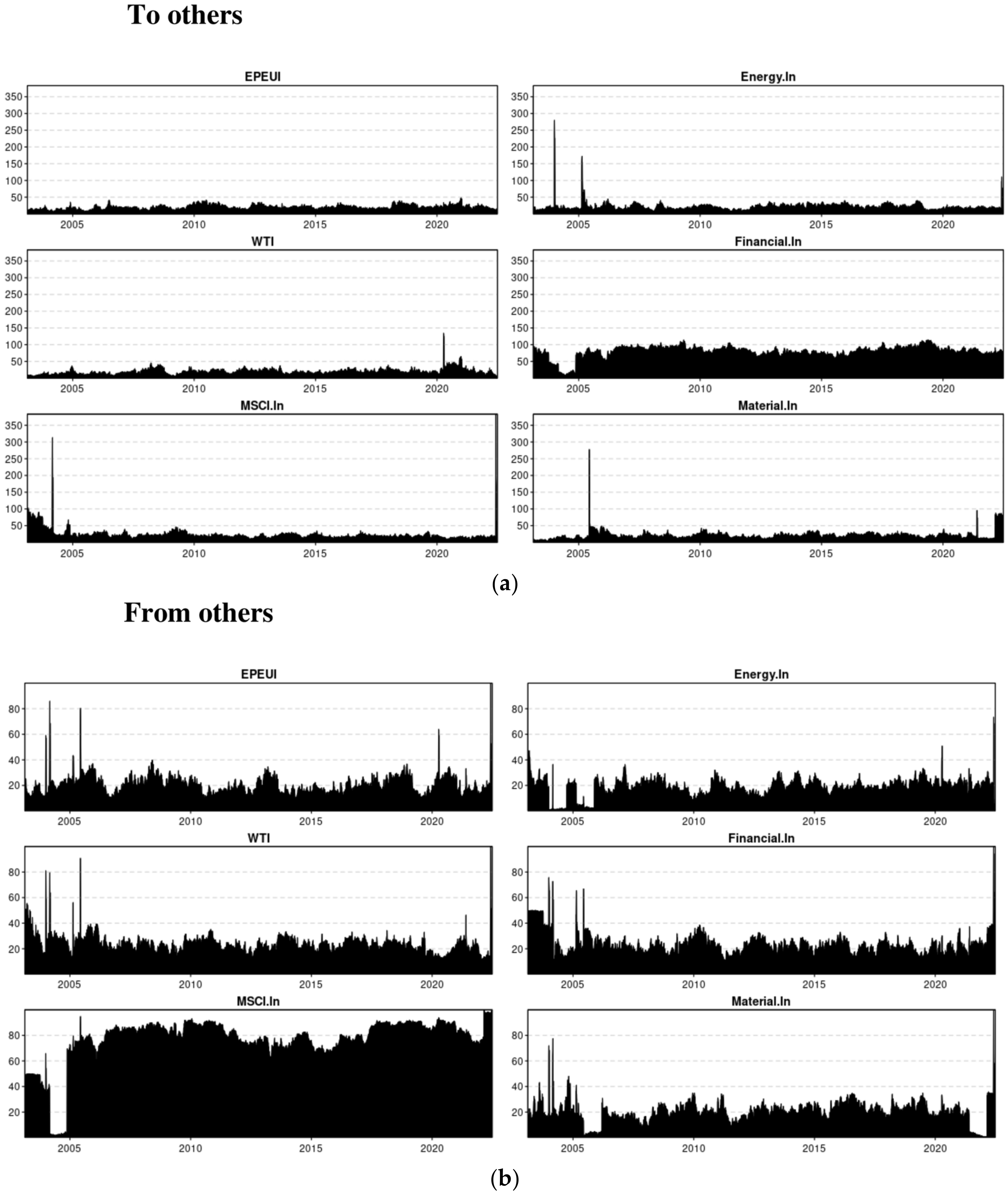

5.4. Dynamic Spillover “To Others” and “From Others”

5.5. Results of Static Quantile Connectedness

6. Conclusions

6.1. Practical Implications

6.2. Limitations and Future Research

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Masson, P. Contagion: Macroeconomic models with multiple equilibria. J. Int. Money Finance 1999, 18, 587–602. [Google Scholar] [CrossRef]

- Forbes, K.J.; Rigobon, R. No contagion, only interdependence: Measuring stock market co-movements. J. Finance 2002, 57, 2223–2261. [Google Scholar] [CrossRef]

- Keohane, R.O.; Nye, J.S. Power and Interdependence. Survival 1973, 15, 158–165. [Google Scholar] [CrossRef]

- Solomon, R.; Gault, A. The Interdependence of Nations: An Agenda for Research; National Science Foundation (U.S.), Directorate of Applied Science and Research Applications, Brookings Institution: Alexandria, VA, USA, 1977; Available online: https://books.google.com.pk/books?id=S6lAAAAAIAAJ (accessed on 13 July 2023).

- Ahmed, W. On the higher-order moment interdependence of stock and commodity markets: A wavelet coherence analysis. Q. Rev. Econ. Finance 2022, 83, 135–151. [Google Scholar] [CrossRef]

- Kaminsky, G.L.; Reinhart, C.M. On crises, contagion, and confusion. J. Int. Econ. 2000, 51, 145–168. [Google Scholar] [CrossRef]

- Pindyck, R.S.; Rotemberg, J.J. The Excess Co-Movement of Commodity Prices. Econ. J. 1990, 100, 1173–1189. [Google Scholar] [CrossRef]

- Alquist, R.; Bhattarai, S.; Coibion, O. Commodity-price co-movement and global economic activity. J. Monet. Econ. 2020, 112, 41–56. [Google Scholar] [CrossRef]

- Ji, Q.; Bouri, E.; Roubaud, D.; Shahzad, S.J.H. Risk spillover between energy and agricultural commodity markets: A dependence-switching CoVaR-copula model. Energy Econ. 2018, 75, 14–27. [Google Scholar] [CrossRef]

- Zhang, R.; Zhang, H.; Gao, W.; Li, T.; Yang, S. The Dynamic Effects of Oil Price Shocks on Exchange Rates—From a Time-Varying Perspective. Sustainability 2022, 14, 8452. [Google Scholar] [CrossRef]

- Zhu, X.; Liao, J.; Chen, Y. Time-varying effects of oil price shocks and economic policy uncertainty on the nonferrous metals industry: From the perspective of industrial security. Energy Econ. 2021, 97, 105192. [Google Scholar] [CrossRef]

- Hajar, A. Motivated by visions: A tale of a rural learner of English. Lang. Learn. J. 2018, 46, 415–429. [Google Scholar] [CrossRef]

- Saeed, T.; Bouri, E.; Alsulami, H. Extreme return connectedness and its determinants between clean/green and dirty energy investments. Energy Econ. 2021, 96, 105017. [Google Scholar] [CrossRef]

- Tabash, M.I.; Babar, Z.; Sheikh, U.A.; Khan, A.A.; Anagreh, S. The linkage between oil price, stock market indices, and exchange rate before, during, and after COVID-19: Empirical insights of Pakistan. Cogent Econ. Finance 2022, 10, 2129366. [Google Scholar] [CrossRef]

- Sheikh, U.A.; Asad, M.; Ahmed, Z.; Mukhtar, U. Asymmetrical relationship between oil prices, gold prices, exchange rate, and stock prices during global financial crisis 2008: Evidence from Pakistan. Cogent Econ. Finance 2020, 8, 1757802. [Google Scholar] [CrossRef]

- PIMCO. Understanding Investing: Tail Risk. 2017. Available online: https://www.pimco.com/en-us/resources/education/understanding-tail-risk/ (accessed on 11 July 2023).

- Hussain, H.; Faridi, M.Z.; Hussain, S. Changing Oil Prices, Exchange Rates and its Impact on Inflation in Pakistan. J. Account. Finance Emerg. Econ. 2022, 8, 113–122. [Google Scholar] [CrossRef]

- Kolaczkowski, M. Why Do Oil Prices Matter to the Global Economy? An Expert Explains. World Economic Forum. 2022. Available online: https://www.weforum.org/agenda/2022/02/why-oil-prices-matter-to-global-economy-expert-explains/ (accessed on 12 July 2023).

- Taylor, J.S.; Spriggs, J. Effects of the Monetary Macro-Economy on Canadian Agricultural Prices. Can. J. Econ. 1989, 22, 278. [Google Scholar] [CrossRef]

- French, J.J.; Li, W.X. Economic policy uncertainty and fund flow to the United States. Finance Res. Lett. 2022, 45, 102126. [Google Scholar] [CrossRef]

- Cepni, O.; Colak, M.S.; Hacıhasanoglu, Y.S.; Yılmaz, M.H. Capital flows under global uncertainties: Evidence from Turkey. Borsa Istanb. Rev. 2021, 21, 175–185. [Google Scholar] [CrossRef]

- Chiang, T.C. Economic policy uncertainty, risk and stock returns: Evidence from G7 stock markets. Finance Res. Lett. 2019, 29, 41–49. [Google Scholar] [CrossRef]

- Luo, Y.; Zhang, C. Economic policy uncertainty and stock price crash risk. Res. Int. Bus. Finance 2020, 51, 101112. [Google Scholar] [CrossRef]

- Demir, E.; Gozgor, G.; Lau, C.K.M.; Vigne, S.A. Does economic policy uncertainty predict the Bitcoin returns? An empirical investigation. Finance Res. Lett. 2018, 26, 145–149. [Google Scholar] [CrossRef]

- Nilavongse, R.; Salah, G. Economic policy uncertainty shocks, economic activity, and exchange rate adjustments. Econ. Lett. 2020, 186, 108765. [Google Scholar] [CrossRef]

- Canh, N.P.; Binh, N.T.; Thanh, S.D. Determinants of foreign direct investment in flows: The role of economic policy uncertainty. Int. Econ. 2020, 161, 159–172. [Google Scholar] [CrossRef]

- Zhu, H.; Meng, L.; Ge, Y.; Hau, L. Dependent relationships between Chinese commodity markets and the international financial market: Evidence from quantile time-frequency analysis. N. Am. J. Econ. Finance 2020, 54, 101256. [Google Scholar] [CrossRef]

- Aslam, F.; Hunjra, A.I.; Bouri, E.; Mughal, K.S.; Khan, M. Dependence structure across equity sectors: Evidence from vine copulas. Borsa Istanb. Rev. 2023, 23, 184–202. [Google Scholar] [CrossRef]

- Borges, A.M. Applied general equilibrium models: An assessment of their usefulness for policy analysis. OECD Econ. Stud. 1988, 7, 15. [Google Scholar]

- Khan, N.; Saleem, A.; Ozkan, O. Do geopolitical oil price risk influence stock market returns and volatility of Pakistan: Evidence from novel non-parametric quantile causality approach. Resour. Policy 2023, 81, 103355. [Google Scholar] [CrossRef]

- Atil, A.; Nawaz, K.; Lahiani, A.; Roubaud, D. Are natural resources a blessing or a curse for financial development in Pakistan? The importance of oil prices, economic growth and economic globalization. Resour. Policy 2020, 67, 101683. [Google Scholar] [CrossRef]

- Ai, C.; Chatrath, A.; Song, F. On the Co-Movement of Commodity Prices. Am. J. Agric. Econ. 2006, 88, 574–588. [Google Scholar] [CrossRef]

- Byrne, J.P.; Sakemoto, R.; Xu, B. Commodity price co-movement: Heterogeneity and the time-varying impact of fundamentals. Eur. Rev. Agric. Econ. 2019, 47, 499–528. [Google Scholar] [CrossRef]

- Adhikari, R.; Putnam, K.J. Co-movement in the commodity futures markets: An analysis of the energy, grains, and livestock sectors. J. Commod. Mark. 2020, 18, 100090. [Google Scholar] [CrossRef]

- Chen, H.; Xu, C.; Peng, Y. Time-frequency connectedness between energy and nonenergy commodity markets during COVID-19: Evidence from China. Resour. Policy 2022, 78, 102874. [Google Scholar] [CrossRef] [PubMed]

- Stuermer, M. Industrialization and the demand for mineral commodities. J. Int. Money Finance 2017, 76, 16–27. [Google Scholar] [CrossRef]

- Hameed, Z.; Shafi, K.; Nadeem, A. Volatility spillover effect between oil prices and foreign exchange markets. Energy Strategy Rev. 2021, 38, 100712. [Google Scholar] [CrossRef]

- Yang, L.; Zhu, Y.; Wang, Y.; Wang, Y. Multifractal detrended cross-correlations between crude oil market and Chinese ten sector stock markets. Phys. Stat. Mech. Its Appl. 2016, 462, 255–265. [Google Scholar] [CrossRef]

- Ji, Q.; Liu, B.-Y.; Nehler, H.; Uddin, G.S. Uncertainties and extreme risk spillover in the energy markets: A time-varying copula-based CoVaR approach. Energy Econ. 2018, 76, 115–126. [Google Scholar] [CrossRef]

- Caporale, G.M.; Ali, F.M.; Spagnolo, N. Oil price uncertainty and sectoral stock returns in China: A time-varying approach. China Econ. Rev. 2015, 34, 311–321. [Google Scholar] [CrossRef]

- Marfatia, H.; Zhao, W.L.; Ji, Q. Uncovering the global network of economic policy uncertainty. Res. Int. Bus. Finance 2020, 53, 101223. [Google Scholar] [CrossRef]

- Istrefi, K.; Piloiu, A. Economic Policy Uncertainty and Inflation Expectations; Working papers 511; Banque de France: Paris, France, 2014; p. 43. [Google Scholar]

- Baker, S.R.; Bloom, N.; Davis, S.J. Measuring Economic Policy Uncertainty. Q. J. Econ. 2016, 131, 1593–1636. [Google Scholar] [CrossRef]

- Brogaard, J.; Detzel, A. The asset-pricing implications of government economic policy uncertainty. Manag. Sci. 2015, 61, 3–18. [Google Scholar] [CrossRef]

- Pástor, Ľ.; Veronesi, P. Political uncertainty and risk premia. J. Financ. Econ. 2013, 110, 520–545. [Google Scholar] [CrossRef]

- Joëts, M.; Mignon, V.; Razafindrabe, T. Does the volatility of commodity prices reflect macroeconomic uncertainty? Energy Econ. 2017, 68, 313–326. [Google Scholar] [CrossRef]

- Bakas, D.; Triantafyllou, A. Volatility forecasting in commodity markets using macro uncertainty. Energy Econ. 2019, 81, 79–94. [Google Scholar] [CrossRef]

- Van Robays, I. Macroeconomic Uncertainty and Oil Price Volatility. Oxf. Bull. Econ. Stat. 2016, 78, 671–693. [Google Scholar] [CrossRef]

- Albulescu, C.T.; Demirer, R.; Raheem, I.D.; Tiwari, A.K. Does the U.S. economic policy uncertainty connect financial markets? Evidence from oil and commodity currencies. Energy Econ. 2019, 83, 375–388. [Google Scholar] [CrossRef]

- Yin, L.; Han, L. Macroeconomic uncertainty: Does it matter for commodity prices? Appl. Econ. Lett. 2014, 21, 711–716. [Google Scholar] [CrossRef]

- Malik, F.; Umar, Z. Dynamic connectedness of oil price shocks and exchange rates. Energy Econ. 2019, 84, 104501. [Google Scholar] [CrossRef]

- Xu, Y.; Han, L.; Wan, L.; Yin, L. Dynamic link between oil prices and exchange rates: A non-linear approach. Energy Econ. 2019, 84, 104488. [Google Scholar] [CrossRef]

- Beckmann, J.; Czudaj, R.L.; Arora, V. The relationship between oil prices and exchange rates: Revisiting theory and evidence. Energy Econ. 2020, 88, 104772. [Google Scholar] [CrossRef]

- Mumtaz, H.; Theodoridis, K. Common and country specific economic uncertainty. J. Int. Econ. 2017, 105, 205–216. [Google Scholar] [CrossRef]

- Gu, X.; Cheng, X.; Zhu, Z.; Deng, X. Economic policy uncertainty and China’s growth-at-risk. Econ. Anal. Policy 2021, 70, 452–467. [Google Scholar] [CrossRef]

- Hernandez, J.A.; Kang, S.H.; Jiang, Z.; Yoon, S.M. Spillover Network among Economic Sentiment and Economic Policy Uncertainty in Europe. Systems 2022, 10, 93. [Google Scholar] [CrossRef]

- Jiang, Y.; Wu, L.; Tian, G.; Nie, H. Do cryptocurrencies hedge against EPU and the equity market volatility during COVID-19?–New evidence from quantile coherency analysis. J. Int. Financ. Mark. Inst. Money 2021, 72, 101324. [Google Scholar] [CrossRef]

- Choi, S.Y. Industry volatility and economic uncertainty due to the COVID-19 pandemic: Evidence from wavelet coherence analysis. Finance Res. Lett. 2020, 37, 101783. [Google Scholar] [CrossRef] [PubMed]

- Jiang, Y.; He, L.; Meng, J.; Nie, H. Non-linear impact of economic policy uncertainty shocks on credit scale: Evidence from China. Phys. Stat. Mech. Its Appl. 2019, 521, 626–634. [Google Scholar] [CrossRef]

- Bahloul, W.; Balcilar, M.; Cunado, J.; Gupta, R. The role of economic and financial uncertainties in predicting commodity futures returns and volatility: Evidence from a nonparametric causality-in-quantiles test. J. Multinatl. Financ. Manag. 2018, 45, 52–71. [Google Scholar] [CrossRef]

- Bakas, D.; Triantafyllou, A. The impact of uncertainty shocks on the volatility of commodity prices. J. Int. Money Finance 2018, 87, 96–111. [Google Scholar] [CrossRef]

- Ma, R.; Zhou, C.; Cai, H.; Deng, C. The forecasting power of EPU for crude oil return volatility. Energy Rep. 2019, 5, 866–873. [Google Scholar] [CrossRef]

- Ando, T.; Greenwood-Nimmo, M.; Shin, Y. Quantile Connectedness: Modelling Tail Behaviour in the Topology of Financial Networks. 2018. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3164772 (accessed on 10 July 2023).

- Koop, G.; Pesaran, M.H.; Potter, S.M. Impulse response analysis in non-linear multivariate models. J. Econom. 1996, 74, 119–147. [Google Scholar] [CrossRef]

- Pesaran, H.H.; Shin, Y. Generalized impulse response analysis in linear multivariate models. Econ. Lett. 1998, 58, 17–29. [Google Scholar] [CrossRef]

- Chatziantoniou, I.; Gabauer, D. EMU risk-synchronisation and financial fragility through the prism of dynamic connectedness. Q. Rev. Econ. Finance 2021, 79, 1–14. [Google Scholar] [CrossRef]

- Ripple, W.J.; Wolf, C.; Newsome, T.M.; Gregg, J.W.; Lenton, T.M.; Palomo, I.; Eikelboom, J.A.J.; Law, B.E.; Huq, S.; Duffy, P.B.; et al. World scientists’ warning of a climate emergency 2021. BioScience 2021, 71, 894–898. [Google Scholar] [CrossRef]

- World Economic Forum. Tackling the Climate Crisis with Innovative Green Technologies. United Nations Climate Change Conference COP27. 2022. Available online: https://www.weforum.org/impact/first-movers-coalition-is-tackling-the-climate-crisis/ (accessed on 4 May 2023).

- Rehman, M.Z.; Khan, S.; Khan, U.A.; Alonazi, W.B.; Noman, A.A. How Do Global Uncertainties Spillovers Affect Leading Renewable Energy Indices? Evidence from the Network Connectedness Approach. Sustainability 2023, 15, 13630. [Google Scholar] [CrossRef]

- Elliott, G.; Rothenberg, T.J.; Stock, J.H. Efficient Tests for an Autoregressive Unit Root; National Bureau of Economic Research: Cambridge, MA, USA, 1996. [Google Scholar]

- Jarque, C.M.; Bera, A.K. Efficient tests for normality, homoscedasticity and serial independence of regression residuals. Econ. Lett. 1980, 6, 255–259. [Google Scholar] [CrossRef]

- Zhu, H.; Chen, Y.; Ren, Y.; Xing, Z.; Hau, L. Time-frequency causality and dependence structure between crude oil, EPU and Chinese industry stock: Evidence from multiscale quantile perspectives. N. Am. J. Econ. Finance 2022, 61, 101698. [Google Scholar] [CrossRef]

- Das, D.; Kannadhasan, M. The asymmetric oil price and policy uncertainty shock exposure of emerging market sectoral equity returns: A quantile regression approach. Int. Rev. Econ. Finance 2020, 69, 563–581. [Google Scholar] [CrossRef]

- Cedic, S.; Mahmoud, A.; Manera, M.; Salah, G. Uncertainty and Stock Returns in Energy Markets: A Quantile Regression Approach. Fond. Eni Enrico Mattei FEEM 1999. [Google Scholar] [CrossRef]

- Si, D.K.; Zhao, B.; Li, X.L.; Ding, H. Policy uncertainty and sectoral stock market volatility in China. Econ. Anal. Policy 2021, 69, 557–573. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variable | Obs | Mean | Std. dev. | Min | Max |

|---|---|---|---|---|---|

| EPEUI | 5000 | 130.5569 | 91.53704 | 3.32 | 861.1 |

| WTI | 5000 | 66.47627 | 24.35423 | −37.63 | 145.29 |

| MSCI.ln | 5000 | 3.927233 | 1.547751 | 0 | 8.21742 |

| Energy.ln | 5000 | 11.8362 | 4.275205 | 0 | 20.88646 |

| Financial.ln | 5000 | 23.49974 | 14.23758 | 0 | 74.5574 |

| Material.ln | 5000 | 8.656145 | 5.658858 | 0 | 23.20922 |

| EPEUI | WTI | MSCI.In | Energy.In | Financial.In | Material.In | FROM | |

|---|---|---|---|---|---|---|---|

| EPEUI | 31.13 | 14.21 | 13.45 | 13.36 | 14.1 | 13.74 | 68.87 |

| WTI | 13.86 | 32.46 | 13.16 | 13.16 | 14.01 | 13.34 | 67.54 |

| MSCI.In | 13.82 | 12.78 | 20.6 | 12.52 | 27.17 | 13.1 | 79.4 |

| Energy.In | 13.37 | 13.11 | 13.43 | 33.32 | 13.57 | 13.21 | 66.68 |

| Financial.In | 14.22 | 13.37 | 14.48 | 13.01 | 31.3 | 13.62 | 68.7 |

| Material.In | 13.56 | 12.73 | 12.51 | 13.31 | 13.44 | 34.43 | 65.57 |

| TO | 68.83 | 66.2 | 67.04 | 65.37 | 82.31 | 67.01 | 416.76 |

| Inc.Own | 99.96 | 98.66 | 87.64 | 98.69 | 113.61 | 101.44 | cTCI/TCI |

| NET | −0.04 | −1.34 | −12.36 | −1.31 | 13.61 | 1.44 | 83.35/69.46 |

| NPT | 3 | 1 | 2 | 2 | 3 | 4 |

| EPEUI | WTI | MSCI.In | Energy.In | Financial.In | Material.In | FROM | |

|---|---|---|---|---|---|---|---|

| EPEUI | 4.27 | 3.64 | 3.65 | 4.29 | 3.41 | 19.24 | |

| WTI | 77.75 | 4.59 | 4.11 | 5.17 | 4.25 | 22.25 | |

| MSCI.In | 3.82 | 3.73 | 24.32 | 3.76 | 60.01 | 4.37 | 75.68 |

| Energy.In | 3.29 | 2.95 | 3.52 | 82.3 | 4.19 | 3.75 | 17.7 |

| Financial.In | 80.76 | 3.8 | 6.55 | 4.34 | 77.52 | 3.99 | 22.48 |

| Material.In | 4.14 | 3.72 | 3.35 | 3.91 | 4.42 | 81.09 | 18.91 |

| TO | 18.57 | 18.46 | 21.64 | 19.76 | 78.06 | 19.77 | 176.26 |

| Inc.Own | 99.32 | 96.21 | 45.96 | 102.06 | 155.58 | 100.87 | cTCI/TCI |

| NET | −0.68 | −3.79 | −54.04 | 2.06 | 55.58 | 0.87 | 35.25/29.38 |

| NPT | 2 | 1 | 1 | 5 | 4 | 2 |

| EPEUI | WTI | MSCI.In | Energy.In | Financial.In | Material.In | FROM | |

|---|---|---|---|---|---|---|---|

| EPEUI | 35.44 | 13.09 | 12.59 | 13.01 | 12.81 | 13.05 | 64.56 |

| WTI | 12.71 | 33.2 | 13.11 | 13.83 | 14.12 | 13.04 | 66.8 |

| MSCI.In | 11.8 | 13.8 | 21.55 | 12.54 | 27.2 | 13.12 | 78.45 |

| Energy.In | 12.11 | 13.12 | 12.88 | 35.7 | 13.65 | 12.54 | 64.3 |

| Financial.In | 12.03 | 14.24 | 15.25 | 13.56 | 31.4 | 13.52 | 68.6 |

| Material.In | 12.31 | 13.07 | 12.95 | 12.84 | 13.63 | 35.2 | 64.8 |

| TO | 60.95 | 67.31 | 66.79 | 65.79 | 81.4 | 65.27 | 407.52 |

| Inc.Own | 96.4 | 100.5 | 88.34 | 101.48 | 112.8 | 100.47 | cTCI/TCI |

| NET | −3.6 | 0.51 | −11.66 | 1.48 | 12.8 | 0.47 | 81.50/67.92 |

| NPT | 0 | 4 | 2 | 3 | 4 | 2 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zaidi, S.B.; Khan, A.; Khan, S.; Rehman, M.Z.; Alonazi, W.B.; Noman, A.A. Connectedness between Pakistan’s Stock Markets with Global Factors: An Application of Quantile VAR Network Model. Mathematics 2023, 11, 4177. https://doi.org/10.3390/math11194177

Zaidi SB, Khan A, Khan S, Rehman MZ, Alonazi WB, Noman AA. Connectedness between Pakistan’s Stock Markets with Global Factors: An Application of Quantile VAR Network Model. Mathematics. 2023; 11(19):4177. https://doi.org/10.3390/math11194177

Chicago/Turabian StyleZaidi, Syeda Beena, Abidullah Khan, Shabeer Khan, Mohd Ziaur Rehman, Wadi B. Alonazi, and Abul Ala Noman. 2023. "Connectedness between Pakistan’s Stock Markets with Global Factors: An Application of Quantile VAR Network Model" Mathematics 11, no. 19: 4177. https://doi.org/10.3390/math11194177