Impact of Geopolitical Risk on G7 Financial Markets: A Comparative Wavelet Analysis between 2014 and 2022

Abstract

:1. Introduction

2. Literature

3. Data and Methodology

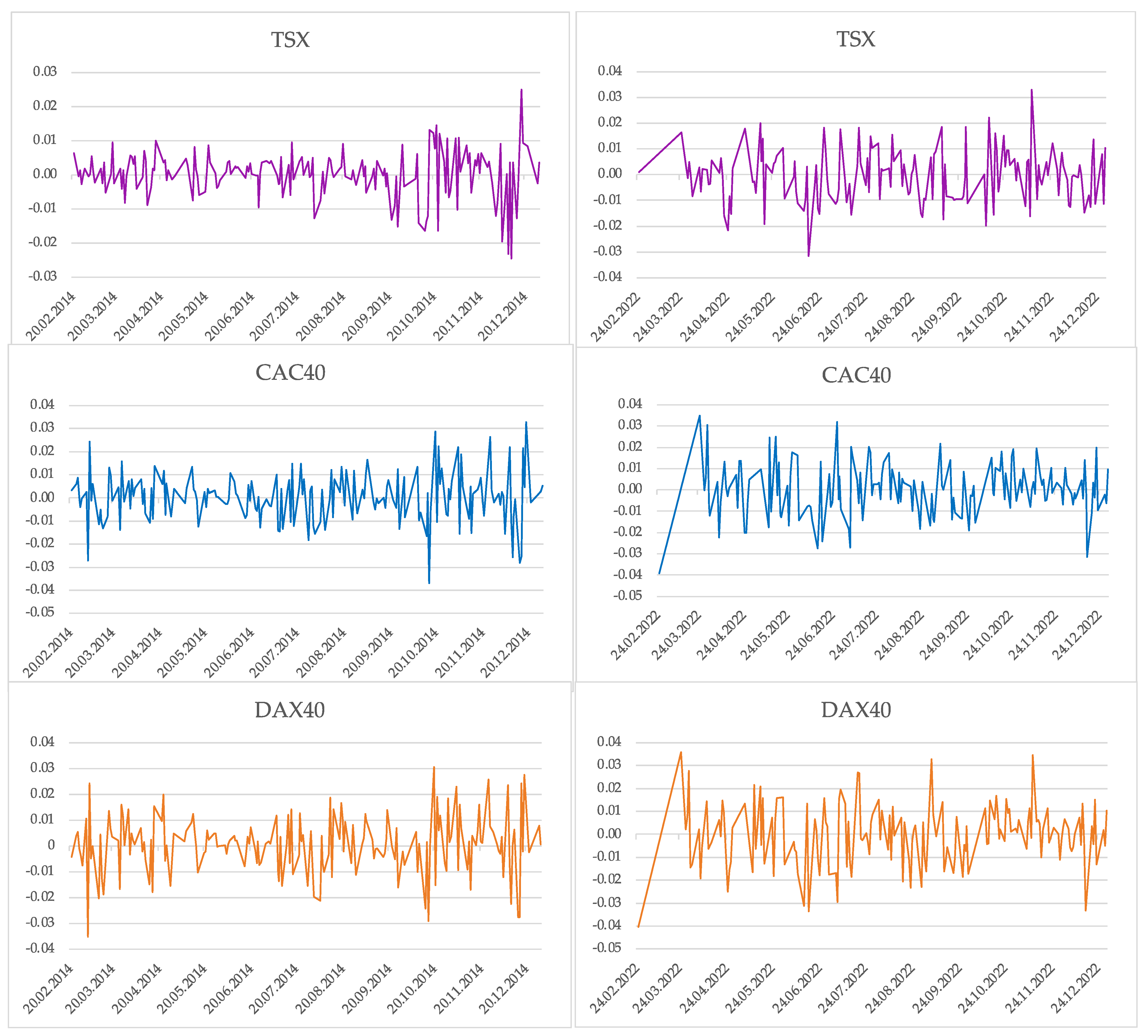

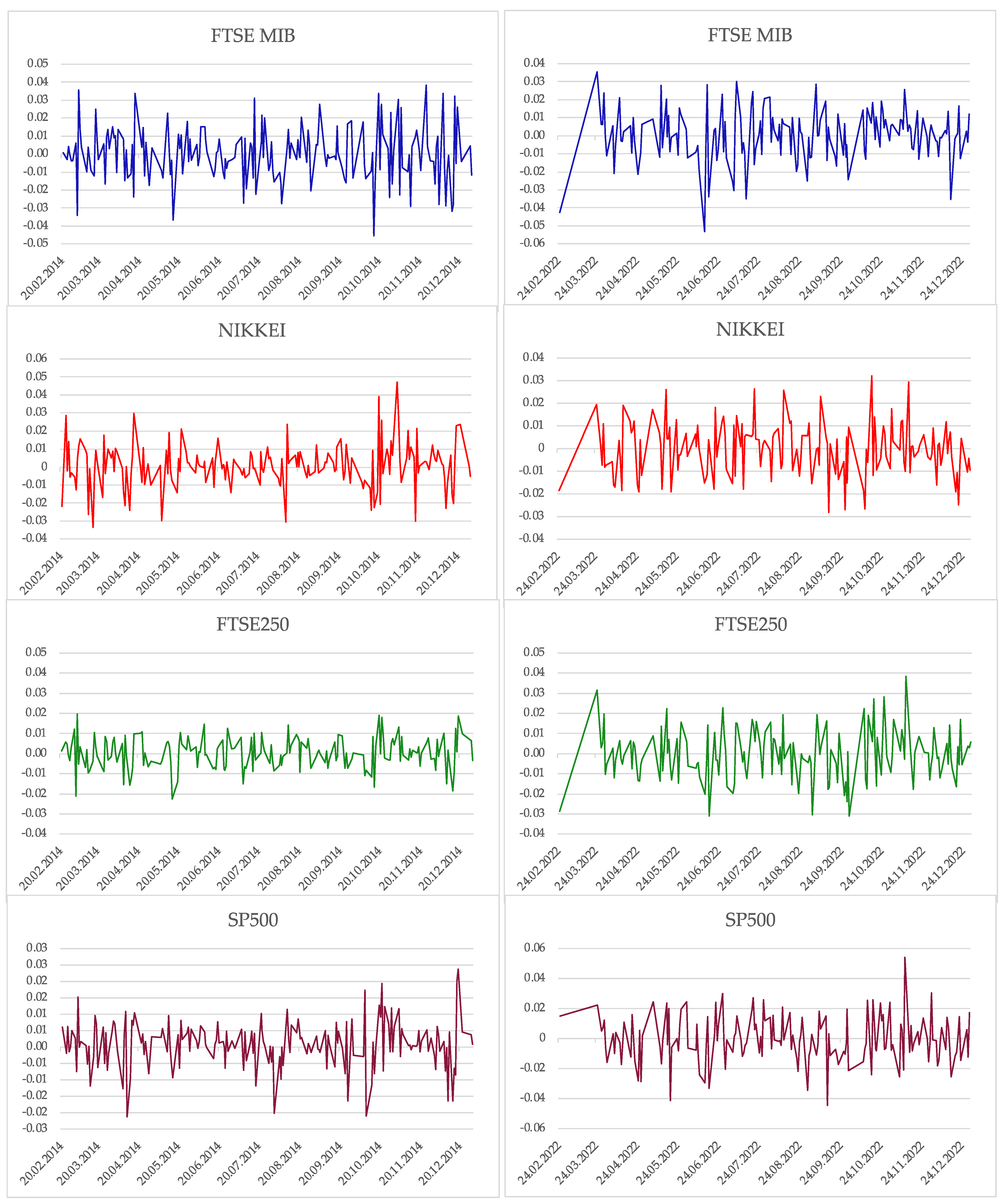

3.1. Data and Sources

3.2. Methodology

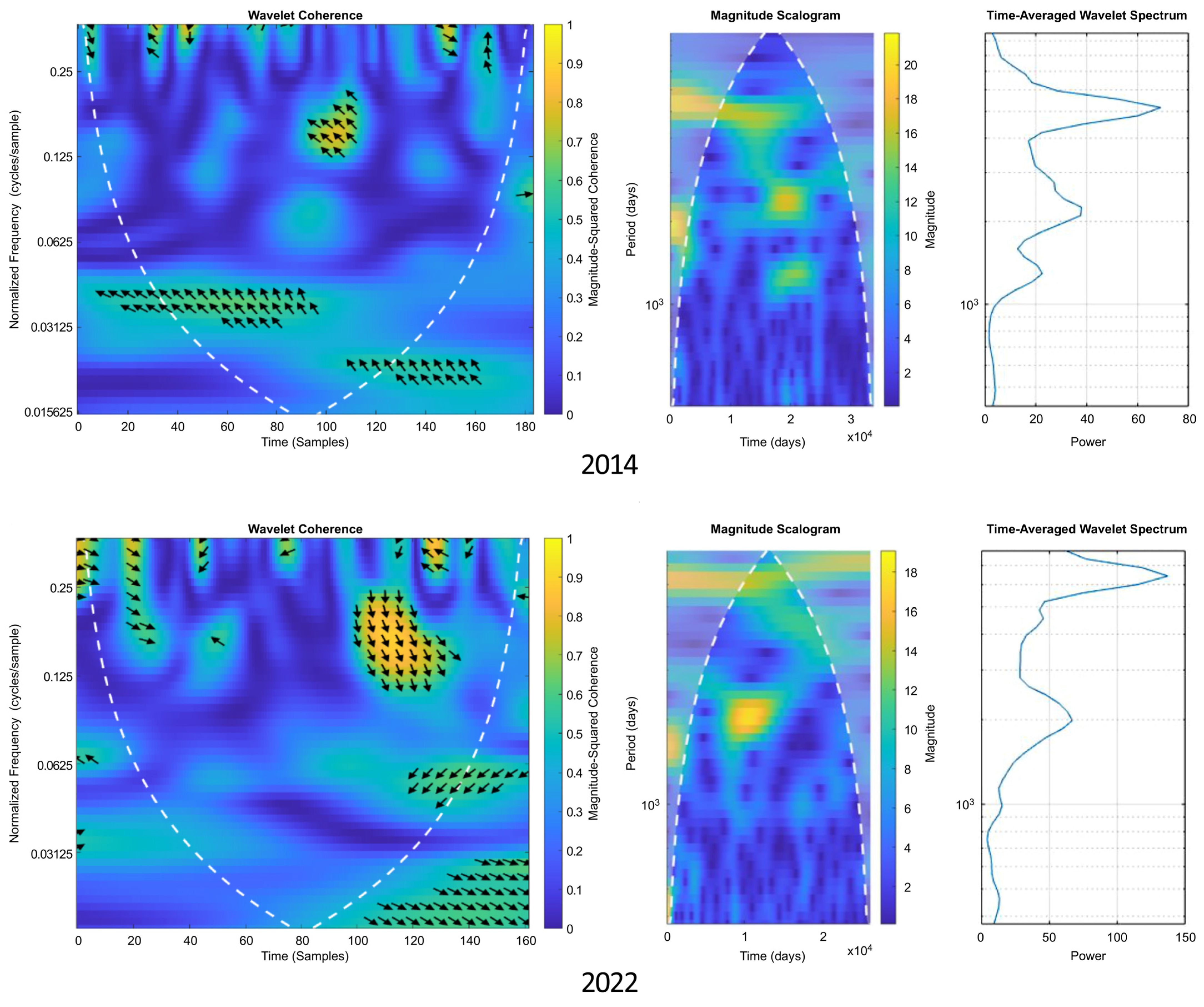

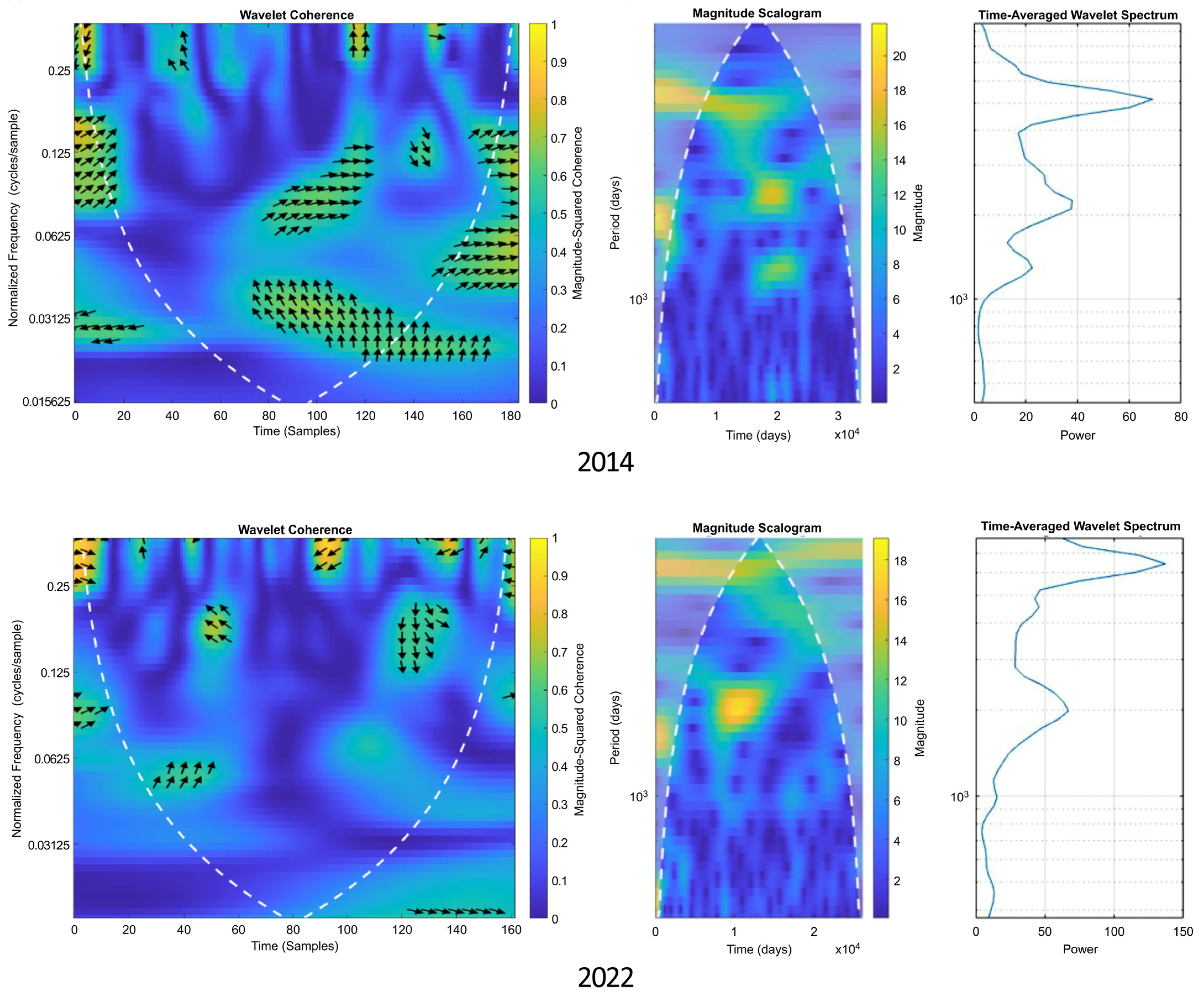

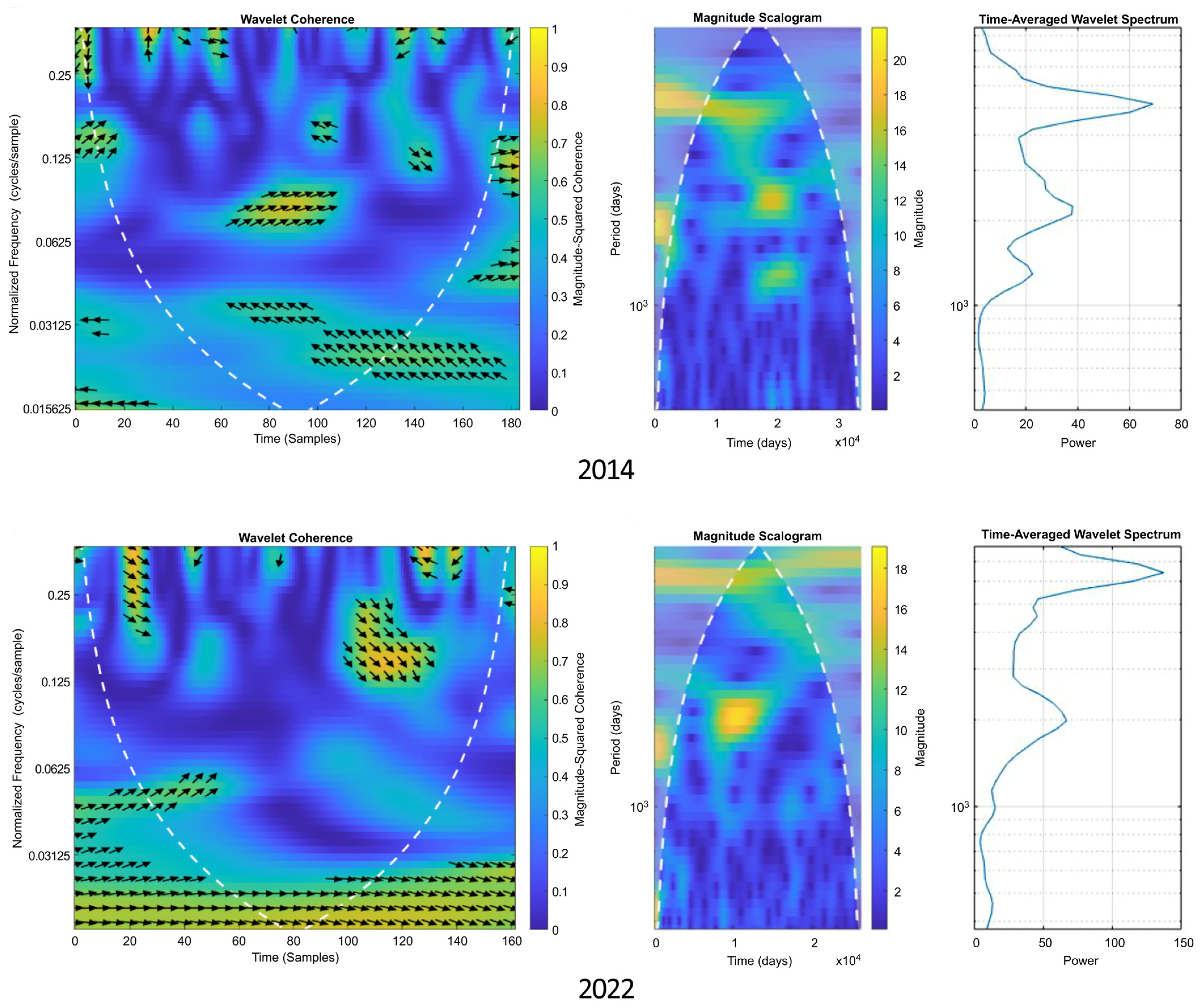

4. Results

4.1. Comparative Analysis between GPR and Canada Stocks in 2014 and 2022

4.2. Comparative Analysis between GPR and France Stocks in 2014 and 2022

4.3. Comparative Analysis between GPR and Germany Stocks in 2014 and 2022

4.4. Comparative Analysis between GPR and Italy Stocks in 2014 and 2022

4.5. Comparative Analysis between GPR and Japan Stocks in 2014 and 2022

4.6. Comparative Analysis between GPR and UK Stocks in 2014 and 2022

4.7. Comparative Analysis between GPR and US Stocks in 2014 and 2022

5. Discussion

6. Robustness

7. Conclusions

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Caldara, D.; Iacoviello, M. Measuring Geopolitical Risk; International Finance Discussion Papers (IFDP) 1222r1; Board of Governors of the Federal Reserve System: Washington, DC, USA, 2022. Available online: https://www.federalreserve.gov/econres/ifdp/measuring-geopolitical-risk.htm (accessed on 25 July 2023).

- Liu, Y.; Wei, Y.; Wang, Q.; Liu, Y. International stock market risk contagion during the COVID-19 pandemic. Financ. Res. Lett. 2022, 45, 102145. [Google Scholar] [CrossRef] [PubMed]

- Alqahtani, A.; Bouri, E.; Vo, X.V. Predictability of GCC stock returns: The role of geopolitical risk and crude oil returns. Econ. Anal. Policy 2020, 68, 239–249. [Google Scholar] [CrossRef]

- Raheem, I.D.; Roux, S.L. Geopolitical risks and tourism stocks: New evidence from causality-in-quantile approach. Q. Rev. Econ. Financ. 2023, 88, 1–7. [Google Scholar] [CrossRef]

- Apergis, N.; Bonato, M.; Gupta, R.; Kyei, C. Does geopolitical risks predict stock returns and volatility of leading defense companies? Evidence from a nonparametric approach. Def. Peace Econ. 2018, 29, 684–696. [Google Scholar] [CrossRef]

- Zhang, Z.; Bouri, E.; Klein, T.; Jalkh, N. Geopolitical risk and the returns and volatility of global defense companies: A new race to arms? Int. Rev. Financ. Anal. 2022, 83, 102327. [Google Scholar] [CrossRef]

- Crozet, M.; Hinz, J. Friendly fire: The trade impact of the Russia sanctions and counter-sanctions. Econ. Policy 2020, 35, 97–146. [Google Scholar] [CrossRef]

- Davydov, D.; Sihvonen, J.; Solanko, L. Who cares about sanctions? Observations from annual reports of European firms. Post-Sov. Aff. 2022, 38, 222–249. [Google Scholar] [CrossRef]

- Elder, J.; Miao, H.; Ramchander, S. Jumps in Oil Prices: The Role of Economic News. Energy J. 2012, 34, 2013. [Google Scholar] [CrossRef]

- Irawan, D.; Okimoto, T. Conditional capital surplus and shortfall across renewable and non-renewable resource firms. Energy Econ. 2022, 112, 106092. [Google Scholar] [CrossRef]

- Feng, L.; Fu, T.; Shi, Y. How does news sentiment affect the states of Japanese stock return volatility? Int. Rev. Financ. Anal. 2022, 84, 102267. [Google Scholar] [CrossRef]

- Manela, A.; Moreira, A. News implied volatility and disaster concerns. J. Financ. Econ. 2017, 123, 137–162. [Google Scholar] [CrossRef]

- Smales, L.A. Geopolitical risk and volatility spillovers in oil and stock markets. Q. Rev. Econ. Financ. 2021, 80, 358–366. [Google Scholar] [CrossRef]

- Chen, S.; Li, G. Why does option-implied volatility forecast realized volatility? Evidence from news events. J. Bank. Financ. 2023, 156, 107019. [Google Scholar] [CrossRef]

- Kamal, M.R.; Wahlstrøm, R.R. Cryptocurrencies and the threat versus the act event of geopolitical risk. Financ. Res. Lett. 2023, 57, 104224. [Google Scholar] [CrossRef]

- Adekoya, B.O.; Oliyide, A.J.; Noman, A. The volatility connectedness of the EU carbon market with commodity and financial markets in time- and frequency-domain: The role of the U.S. economic policy uncertainty. Resour. Policy 2021, 74, 102252. [Google Scholar] [CrossRef]

- D’Ecclesia, R.L.; Magrini, E.; Montalbano, P.; Triulzi, U. Understanding recent oil price dynamics: A novel empirical approach. Energy Econ. 2014, 46, S11–S17. [Google Scholar] [CrossRef]

- Ullrich, K.K.; Transchel, S. Demand–supply mismatches and stock market performance: A retailing perspective. Prod. Oper. Manag. 2017, 26, 1444–1462. [Google Scholar] [CrossRef]

- Baker, S.R.; Bloom, N.; Davis, S.J. Measuring economic policy uncertainty. Q. J. Econ. 2016, 131, 1593–1636. [Google Scholar] [CrossRef]

- Mansour-Ichrakieh, L.; Zeaiter, H. The role of geopolitical risks on the Turkish economy opportunity or threat. N. Am. J. Econ. Financ. 2019, 50, 101000. [Google Scholar] [CrossRef]

- Dutta, A.; Bouri, E.; Saeed, T. News-based equity market uncertainty and crude oil volatility. Energy 2021, 222, 119930. [Google Scholar] [CrossRef]

- Chen, X. Are the shocks of EPU, VIX, and GPR indexes on the oil-stock nexus alike? A time-frequency analysis. Appl. Econ. 2022, 55, 5637–5652. [Google Scholar] [CrossRef]

- Ahmed, S.; Hasan, M.M.; Kamal, M.R. Russia–Ukraine crisis: The effects on the European stock market. Eur. Financ. Manag. 2022, 29, 1–41. [Google Scholar] [CrossRef]

- Neely, C.J. Financial market reactions to the Russian invasion of Ukraine. Fed. Reserve Bank St. Louis Rev. 2022, 104, 266–296. [Google Scholar] [CrossRef]

- Lo, G.D.; Marcelin, I.; Bassène, T.; Sène, B. The Russo-Ukrainian war and financial markets: The role of dependence on Russian commodities. Financ. Res. Lett. 2022, 50, 103194. [Google Scholar] [CrossRef]

- Sun, M.; Zhang, C. Comprehensive analysis of global stock market reactions to the Russia-Ukraine war. Appl. Econ. Lett. 2022, 30, 2673–2680. [Google Scholar] [CrossRef]

- Bougias, A.; Episcopos, A.; Leledakis, G.N. Valuation of European firms during the Russia–Ukraine war. Econ. Lett. 2022, 218, 110750. [Google Scholar] [CrossRef]

- Fang, Y.; Shao, Z. The Russia-Ukraine conflict and volatility risk of commodity markets. Financ. Res. Lett. 2022, 50, 103264. [Google Scholar] [CrossRef]

- Singh, A.; Patel, R.; Singh, H. Recalibration of priorities: Investor preference and Russia-Ukraine conflict. Financ. Res. Lett. 2022, 50, 103294. [Google Scholar] [CrossRef]

- Umar, M.; Riaz, Y.; Yousaf, I. Impact of Russian-Ukraine war on clean energy, conventional energy, and metal markets: Evidence from event study approach. Resour. Policy 2022, 79, 102966. [Google Scholar] [CrossRef]

- Adekoya, O.B.; Asl, M.G.; Oliyide, J.A.; Izadi, P. Multifractality and cross-correlation between the crude oil and the European and non-European stock markets during the Russia-Ukraine war. Resour. Policy 2023, 80, 103134. [Google Scholar] [CrossRef]

- Yousaf, I.; Patel, R.; Yaroyaya, L. The reaction of G20+ stock markets to the Russia–Ukraine conflict “black-swan” event: Evidence from event study approach. J. Behav. Exp. Financ. 2022, 35, 100723. [Google Scholar] [CrossRef]

- Ha, L.T. Dynamic interlinkages between the crude oil and gold and stock during Russia-Ukraine War: Evidence from an extended TVP-VAR analysis. Environ. Sci. Pollut. Res. 2023, 30, 23110–23123. [Google Scholar] [CrossRef] [PubMed]

- Bossman, A.; Gubareva, M. Asymmetric impacts of geopolitical risk on stock markets: A comparative analysis of the E7 and G7 equities during the Russian-Ukrainian conflict. Heliyon 2023, 9, e13626. [Google Scholar] [CrossRef] [PubMed]

- He, Z. Geopolitical risks and investor sentiment: Causality and TVP-VAR analysis. N. Am. J. Econ. Financ. 2023, 67, 101947. [Google Scholar] [CrossRef]

- Abbassi, W.; Kumari, V.; Pandey, D.K. What makes firms vulnerable to the Russia–Ukraine crisis? J. Risk Financ. 2022, 24, 24–39. [Google Scholar] [CrossRef]

- Shaik, M.; Jamil, S.A.; Hawaldar, I.T.; Sahabuddin, M.; Rabbani, M.R.; Atif, M. Impact of geo-political risk on stocks, oil, and gold returns during GFC, COVID-19, and Russian–Ukraine War. Cogent Econ. Financ. 2023, 11, 2190213. [Google Scholar] [CrossRef]

- Salisu, A.A.; Omoke, P.C.; Sikiru, A.A. Geopolitical risk and global financial cycle: Some forecasting experiments. J. Forecast. 2023, 42, 3–16. [Google Scholar] [CrossRef]

- Li, S.; Zhang, W.; Zhang, W. Dynamic time-frequency connectedness and risk spillover between geopolitical risks and natural resources. Resour. Policy 2023, 82, 103554. [Google Scholar] [CrossRef]

- Agyei, S.K. Emerging markets equities’ response to geopolitical risk: Time-frequency evidence from the Russian-Ukrainian conflict era. Heliyon 2023, 9, e13319. [Google Scholar] [CrossRef]

- Elsayed, A.H.; Helmi, M.H. Volatility transmission and spillover dynamics across financial markets: The role of geopolitical risk. Ann. Oper. Res. 2021, 305, 1–22. [Google Scholar] [CrossRef]

- Mei, D.; Ma, F.; Liao, Y.; Wang, L. Geopolitical risk uncertainty and oil future volatility: Evidence from MIDAS models. Energy Econ. 2020, 86, 104624. [Google Scholar] [CrossRef]

- Wang, L.; Ma, F.; Hao, J.; Gao, X. Forecasting crude oil volatility with geopolitical risk: Do time-varying switching probabilities play a role? Int. Rev. Financ. Anal. 2021, 76, 101756. [Google Scholar] [CrossRef]

- Bouri, E.; Hammoud, R.; Kassm, C.A. The effect of oil implied volatility and geopolitical risk on GCC stock sectors under various market conditions. Energy Econ. 2023, 120, 106617. [Google Scholar] [CrossRef]

- Huang, J.; Ding, Q.; Zhang, H.; Guo, Y.; Suleman, M.T. Nonlinear dynamic correlation between geopolitical risk and oil prices: A study based on high-frequency data. Res. Int. Bus. Financ. 2021, 56, 101370. [Google Scholar] [CrossRef]

- Wu, F.L.; Zhan, X.D.; Zhou, J.Q.; Wang, M.H. Stock market volatility and Russia–Ukraine conflict. Financ. Res. Lett. 2023, 55, 103919. [Google Scholar] [CrossRef]

- Balcilar, M.; Bonato, M.; Demirer, R.; Gupta, R. Geopolitical risks and stock market dynamics of the BRICS. Econ. Syst. 2018, 42, 295–306. [Google Scholar] [CrossRef]

- Boubaker, S.; Jouini, J.; Lahiani, A. Financial contagion between the US and selected developed and emerging countries: The case of the subprime crisis. Q. Rev. Econ. Financ. 2016, 61, 14–28. [Google Scholar] [CrossRef]

- Zhou, Z.; Lin, L.; Li, S. International stock market contagion: A CEEMDAN wavelet analysis. Econ. Model. 2018, 72, 333–352. [Google Scholar] [CrossRef]

- Corbet, S.; Hou, Y.G.; Hu, Y.; Oxley, L. The growth of oil futures in China: Evidence of market maturity through global crises. Energy Econ. 2022, 114, 106243. [Google Scholar] [CrossRef]

- Davidovic, M. From Pandemic to Financial Contagion: High-Frequency Risk Metrics and Bayesian Volatility Analysis. Financ. Res. Lett. 2021, 42, 101913. [Google Scholar] [CrossRef]

- Gunay, S. Comparing COVID-19 with the GFC: A shockwave analysis of currency markets. Res. Intl. Bus. Financ. 2021, 56, 101377. [Google Scholar] [CrossRef]

- Batten, A.J.; Boubaker, S.; Kinateder, H.; Choudhury, T.; Wagner, F.N. Volatility impacts on global banks: Insights from the GFC, COVID-19, and the Russia-Ukraine war. J. Econ. Behav. Organ. 2023, 215, 325–350. [Google Scholar] [CrossRef]

- O’Loughlin, J.; Toal, G. The Crimea conundrum: Legitimacy and public opinion after annexation. Eurasian Geogr. Econ. 2019, 60, 6–27. [Google Scholar] [CrossRef]

- Ivanov, S.; Yudina, S.; Lysa, O.; Drahun, A. Classification and assessment of losses from the armed conflict in Donbas and annexation of Crimea. Econ. Ann.-XXI 2020, 184, 107–123. [Google Scholar] [CrossRef]

- Haukkala, H. From cooperative to contested Europe? The conflict in Ukraine as a culmination of a Long-Term crisis in EU–Russia relations. J. Contemp. Eur. Stud. 2015, 23, 25–40. [Google Scholar] [CrossRef]

- Giumelli, F. The Redistributive Impact of Restrictive Measures on EU Members: Winners and Losers from Imposing Sanctions on Russia. J. Common Mark. Stud. 2017, 55, 1062–1080. [Google Scholar] [CrossRef]

- Raik, K. The Ukraine Crisis as a Conflict over Europe’s Political, Economic and Security Order. Geopolitics 2019, 24, 51–70. [Google Scholar] [CrossRef]

- Doornich, J.B.; Raspotnik, A. Economic sanctions disruption on international trade patterns and global trade dynamics: Analyzing the effects of the European Union’s sanctions on Russia. J. East-West Bus. 2020, 26, 344–364. [Google Scholar] [CrossRef]

- Mykhnenko, V. Causes and consequences of the war in Eastern Ukraine: An Economic Geography perspective. Eur.-Asia Stud. 2020, 72, 528–560. [Google Scholar] [CrossRef]

- Antonakakis, N.; Chatziantoniou, I.; Gabauer, D. Refined Measures of Dynamic Connectedness based on Time-Varying Parameter Vector Autoregressions. J. Risk Financ. Manag. 2020, 13, 84. [Google Scholar] [CrossRef]

- Haar, A. Zur Theorie der orthogonalen Funktionensysteme. Math. Ann. 1910, 69, 331–371. Available online: https://link.springer.com/article/10.1007/BF01456326 (accessed on 27 July 2023). [CrossRef]

- Grossmann, A.; Morlet, J. Decomposition of Hardy Functions into Square Integrable Wavelets of Constant Shape. SIAM J. Math. Anal. 1984, 15, 723–736. [Google Scholar] [CrossRef]

- Meyer, Y. Principe d’incertitude, bases hilbertiennes et al.gebres d’operateur. Seminaire Bourbaki 1985, 38, 31–39. Available online: http://www.numdam.org/item/SB_1985-1986__28__209_0 (accessed on 31 July 2023).

- Choi, S. Evidence from a multiple and partial wavelet analysis on the impact of geopolitical concerns on stock markets in North-East Asian countries. Financ. Res. Lett. 2022, 46, 102465. [Google Scholar] [CrossRef]

- Karamti, C.; Belhassine, O. COVID-19 pandemic waves and global financial markets: Evidence from wavelet coherence analysis. Financ. Res. Lett. 2022, 45, 102136. [Google Scholar] [CrossRef] [PubMed]

- Özdemir, O. Cue the volatility spillover in the cryptocurrency markets during the COVID-19 pandemic: Evidence from DCC-GARCH and wavelet analysis. Financ. Innov. 2022, 8, 12. [Google Scholar] [CrossRef]

- Daubechies, I. Orthonormal bases of compactly supported wavelets. Commun. Pure Appl. Math. 1988, 41, 909–996. [Google Scholar] [CrossRef]

- Mallat, S.G. A theory for multiresolution signal decomposition: The wavelet representation. IEEE Trans. Pattern Anal. Mach. Intell. 1989, 11, 674–693. [Google Scholar] [CrossRef]

- Sharif, A.; Aloui, C.; Yarovaya, L. COVID-19 pandemic, oil prices, stock market, geopolitical risk and policy uncertainty nexus in the US economy: Fresh evidence from the wavelet-based approach. Int. Rev. Financ. Anal. 2020, 70, 101496. [Google Scholar] [CrossRef]

- Matar, A.; Al-Rdaydeh, M.; Ghazalat, A.; Eneizan, B. Co-movement between GCC stock markets and the US stock markets: A wavelet coherence analysis. Cogent Bus. Manag. 2021, 8, 1948658. [Google Scholar] [CrossRef]

- Mensi, W.; Naeem, M.A.; Vo, X.V.; Kang, S.H. Dynamic and frequency spillovers between green bonds, oil and G7 stock markets: Implications for risk management. Econ. Anal. Policy 2022, 73, 331–344. [Google Scholar] [CrossRef]

- Torrence, C.; Webster, P.J. Interdecadal changes in the ENSO-Monsoon system. J. Clim. 1999, 12, 2679–2690. [Google Scholar] [CrossRef]

- Rubbaniy, G.; Khalid, A.A.; Samitas, A. Are cryptos safe-haven assets during COVID-19? Evidence from wavelet coherence analysis. Emerg. Mark. Financ. Trade 2021, 57, 1741–1756. [Google Scholar] [CrossRef]

- Fama, E.F. Efficient Capital Markets: A review of theory and Empirical work. J. Financ. 1970, 25, 383. [Google Scholar] [CrossRef]

- Narayan, S.; Sriananthakumar, S.; Islam, Z.S. Stock market integration of emerging Asian economies: Patterns and causes. Econ. Model. 2014, 39, 19–31. [Google Scholar] [CrossRef]

- Babaei, H.; Hübner, G.; Muller, A. The effects of uncertainty on the dynamics of stock market interdependence: Evidence from the time-varying cointegration of the G7 stock markets. J. Int. Money Financ. 2023, 139, 102961. [Google Scholar] [CrossRef]

- Nguyen, A.T.K.; Truong, L.D.; Friday, H.S. Expiration-Day Effects of Index Futures in a Frontier Market: The Case of Ho Chi Minh Stock Exchange. Int. J. Financ. Stud. 2022, 10, 3. [Google Scholar] [CrossRef]

- Nusair, A.S.; Al-Khasawneh, A.J. Impact of economic policy uncertainty on the stock markets of the G7 Countries: A nonlinear ARDL approach. J. Econ. Asymmetries 2022, 26, e00251. [Google Scholar] [CrossRef]

- Koop, G.; Korobilis, D. A new index of financial conditions. Eur. Econ. Rev. 2014, 71, 101–116. [Google Scholar] [CrossRef]

- El Khoury, R.; Nasrallah, N.; Hussainey, K.; Assaf, R. Spillover analysis across FinTech, ESG, and renewable energy indices before and during the Russia–Ukraine war: International evidence. J. Int. Financ. Manag. Account. 2023, 34, 279–317. [Google Scholar] [CrossRef]

- Gabauer, D.; Gupta, R. On the transmission mechanism of country-specific and international economic uncertainty spillovers: Evidence from a TVP-VAR connectedness decomposition approach. Econ. Lett. 2018, 171, 63–71. [Google Scholar] [CrossRef]

- Koop, G.; Pesaran, M.H.; Potter, S.M. Impulse response analysis in nonlinear multivariate models. J. Econom. 1996, 74, 119–147. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Index | TSX | CAC40 | DAX40 | FTSE MIB | NIKKEI | FTSE250 | SP500 |

|---|---|---|---|---|---|---|---|

| Mean | 0.0004 | 0.0002 | 0.0004 | −0.7471 | 0.0008 | −0.0004 | 0.0009 |

| Median | 0.0008 | 0.0006 | 0.0010 | 0.4600 | 0.0009 | −0.0003 | 0.0009 |

| Maximum | 0.0251 | 0.0329 | 0.0307 | 27.1400 | 0.0471 | 0.0356 | 0.0237 |

| Minimum | −0.0244 | −0.0370 | −0.0350 | −33.6900 | −0.0335 | −0.0454 | −0.0211 |

| Std. dev. | 0.0067 | 0.0106 | 0.0110 | 9.6257 | 0.0122 | 0.0150 | 0.0070 |

| Skewness | −0.6226 | −0.0893 | −0.1880 | −0.2699 | 0.1272 | 0.0353 | −0.2726 |

| Kurtosis | 5.1890 | 4.0446 | 3.7125 | 3.3475 | 4.5860 | 3.1579 | 4.5179 |

| Index | TSX | CAC40 | DAX40 | FTSE MIB | NIKKEI | FTSE250 | SP500 |

|---|---|---|---|---|---|---|---|

| Mean | −0.0006 | −0.0002 | −0.0005 | −0.0002 | −0.0005 | −0.0004 | −0.0003 |

| Median | −0.0002 | −0.0010 | 0.0002 | 0.0003 | 0.0003 | −0.0011 | −0.0016 |

| Maximum | 0.0329 | 0.0349 | 0.0360 | 0.0353 | 0.0320 | 0.0383 | 0.0540 |

| Minimum | −0.0315 | −0.0390 | −0.0404 | −0.0531 | −0.0282 | −0.0311 | −0.0442 |

| Std. dev. | 0.0101 | 0.0124 | 0.0134 | 0.0142 | 0.0115 | 0.0125 | 0.0153 |

| Skewness | 0.1556 | 0.0296 | −0.0802 | −0.4236 | 0.1148 | 0.1556 | 0.0928 |

| Kurtosis | 3.1845 | 3.3959 | 3.3583 | 4.0241 | 3.0455 | 3.1452 | 3.5733 |

| State | Canada | France | Germany | Italy | Japan | UK | US | GPR | FROM |

|---|---|---|---|---|---|---|---|---|---|

| Canada | 50.42 | 7.23 | 6.92 | 6.74 | 0.32 | 5.54 | 22.42 | 0.41 | 49.58 |

| France | 4.43 | 28.32 | 23.52 | 20.23 | 0.40 | 13.84 | 9.00 | 0.26 | 71.68 |

| Germany | 4.51 | 24.40 | 29.91 | 17.00 | 0.23 | 15.26 | 8.57 | 0.12 | 70.09 |

| Italy | 4.22 | 22.43 | 18.47 | 32.20 | 0.69 | 13.35 | 7.76 | 0.90 | 67.80 |

| Japan | 6.36 | 11.73 | 8.93 | 7.12 | 39.43 | 7.32 | 18.46 | 0.64 | 60.57 |

| UK | 5.62 | 16.58 | 17.25 | 14.13 | 0.88 | 33.50 | 11.77 | 0.28 | 66.50 |

| US | 17.08 | 12.33 | 10.59 | 9.72 | 0.76 | 9.90 | 39.03 | 0.58 | 60.97 |

| GPR | 2.46 | 0.68 | 0.33 | 2.99 | 0.28 | 0.80 | 1.46 | 91.00 | 9.00 |

| TO | 44.68 | 95.38 | 86.01 | 77.93 | 3.56 | 66.01 | 79.42 | 3.20 | 456.19 |

| NET | −4.90 | 23.70 | 15.92 | 10.12 | −57.01 | −0.49 | 18.46 | −5.80 | 57.02 |

| State | Canada | France | Germany | Italy | Japan | UK | US | GPR | FROM |

|---|---|---|---|---|---|---|---|---|---|

| Canada | 28.71 | 11.35 | 12.93 | 13.26 | 1.73 | 11.29 | 20.53 | 0.20 | 71.29 |

| France | 9.47 | 23.61 | 20.54 | 18.58 | 1.48 | 16.44 | 8.95 | 0,92 | 76.39 |

| Germany | 10.46 | 20.04 | 22.98 | 18.05 | 1.22 | 17.09 | 9.44 | 0.71 | 77.02 |

| Italy | 11.40 | 19.54 | 19.41 | 24.62 | 0.63 | 15.13 | 8.61 | 0.65 | 75.38 |

| Japan | 16.00 | 6.83 | 9.07 | 5.98 | 33.24 | 8.79 | 19.95 | 0.13 | 66.76 |

| UK | 10.27 | 17.81 | 19.07 | 15.68 | 2.31 | 25.67 | 8.92 | 0.26 | 74.33 |

| US | 23.00 | 10.99 | 12.42 | 10.84 | 1.21 | 9.72 | 31.73 | 0.10 | 68.26 |

| GPR | 1.04 | 1.58 | 0.98 | 1.11 | 0.65 | 0.65 | 1.02 | 92.97 | 7.03 |

| TO | 81.64 | 88.14 | 94.42 | 83.52 | 9.24 | 79.13 | 77.43 | 2.97 | 516.47 |

| NET | 10.35 | 11.75 | 17.40 | 8.14 | −57.53 | 4.80 | 9.15 | −4.06 | 64.56 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Panazan, O.; Gheorghe, C. Impact of Geopolitical Risk on G7 Financial Markets: A Comparative Wavelet Analysis between 2014 and 2022. Mathematics 2024, 12, 370. https://doi.org/10.3390/math12030370

Panazan O, Gheorghe C. Impact of Geopolitical Risk on G7 Financial Markets: A Comparative Wavelet Analysis between 2014 and 2022. Mathematics. 2024; 12(3):370. https://doi.org/10.3390/math12030370

Chicago/Turabian StylePanazan, Oana, and Catalin Gheorghe. 2024. "Impact of Geopolitical Risk on G7 Financial Markets: A Comparative Wavelet Analysis between 2014 and 2022" Mathematics 12, no. 3: 370. https://doi.org/10.3390/math12030370