Volatility Contagion from Bulk Shipping and Petrochemical Industries to Oil Futures Market during the Economic Uncertainty

Abstract

:1. Introduction

2. Literature Review

2.1. Review of Petrochemical and Shipping Industries’ Influence on Oil Markets

2.2. Review of Volatility Spillover

2.3. Review of the GARCH-MIDAS Model

- (1)

- Copula models: Gong et al. [22] used a three-variable Markov regime transition copula model to study the dynamic dependence between shipping and freight and the stock market. In most cases, the decrease in US-China trade increases the risk of contagion between the two markets;

- (2)

- The value-at-risk method: For example, Yang et al. [23] adopted the value-at-risk method to better understand the dry bulk shipping market, measuring the risk of the dry bulk shipping market in terms of the BDI. The risk of investment in the two reference markets of the stock market and crude oil market was used, and the risk spillover effect of the global stock market and crude oil market on the dry bulk market was discussed;

3. Materials and Methods

3.1. Volatility Transmission and Methodology

3.1.1. Volatility Transmission

3.1.2. Choice of Methodology: GARCH-MIDAS Model

3.2. Description of the GARCH-MIDAS Model

4. Data, Hypothesis, and Results

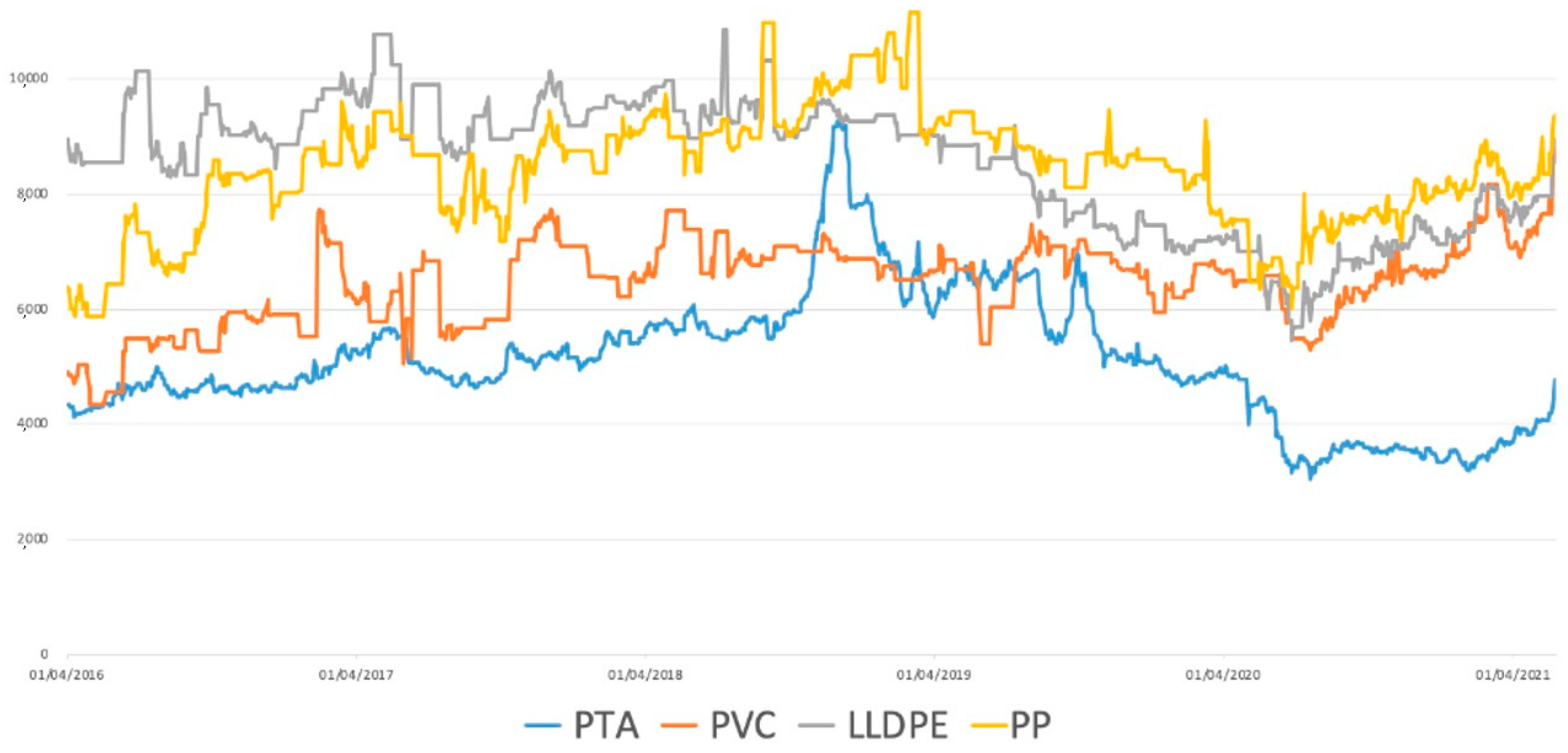

4.1. Data Description

4.1.1. Dependent Variables in High-Frequency Data

4.1.2. Independent Variables in Low-Frequency Data

4.2. Descriptive Statistics

4.3. Stationarity and Unit Root Test

4.4. Research Hypotheses

5. Empirical Results of GARCH-MIDAS

5.1. Results before the US-China Trade War

5.2. Results after Commencement of the US–China Trade War

5.3. Results after the US–China Trade War Extended to the Ukrainian–Russian War

6. Conclusions

6.1. Findings of Empirical Results

6.2. Practical Implications and Discussions

Funding

Conflicts of Interest

Appendix A

{kind=link}

| WTI | BDI | BDTI | BCTI | PTA | PP | PVC | LLDPE | |

|---|---|---|---|---|---|---|---|---|

| WTI | Infinite | 1.000003 | 1.000017 | 1.016676 | 1.002712 | 1.004539 | 1.001010 | 1.000668 |

| BDI | 1.000003 | Infinite | 1.003605 | 1.012390 | 1.000342 | 1.022479 | 1.034121 | 1.005752 |

| BDTI | 1.000017 | 1.003605 | Infinite | 1.495456 | 1.023608 | 1.013466 | 1.089766 | 1.024890 |

| BCTI | 1.016676 | 1.012390 | 1.495456 | Infinite | 1.023130 | 1.004730 | 1.092122 | 1.010473 |

| PTA | 1.002712 | 1.000342 | 1.023608 | 1.023130 | Infinite | 1.223917 | 1.147003 | 1.293724 |

| PP | 1.004539 | 1.022479 | 1.013466 | 1.004730 | 1.223917 | Infinite | 1.777048 | 4.433990 |

| PVC | 1.001010 | 1.034121 | 1.089766 | 1.092122 | 1.147003 | 1.777048 | Infinite | 1.854945 |

| LLDPE | 1.000668 | 1.005752 | 1.024890 | 1.010473 | 1.293724 | 4.433990 | 1.854945 | Infinite |

References

- Masih, M.; Algahtani, I.; De Mello, L. Price dynamics of crude oil and the regional ethylene markets. Energy Econ. 2010, 32, 1435–1444. [Google Scholar] [CrossRef]

- Forbes. How Could the U.S.-China Trade War Impact Crude Oil Prices? Available online: https://www.forbes.com/sites/greatspeculations/2018/07/18/how-could-the-us-china-trade-war-impact-crude-oil-prices/#2df5beb47144 (accessed on 10 August 2020).

- International Energy Agency. Explore Energy Data by Category, Indicator, Country or Region. Available online: https://www.iea.org/data-and-statistics/data-tables?country=WORLD&energy=Balances&year=2017 (accessed on 10 August 2020).

- Lin, A.J.; Chang, H.-Y. Volatility Transmission from Equity, Bulk Shipping, and Commodity Markets to Oil ETF and Energy Fund—A GARCH-MIDAS Model. Mathematics 2020, 8, 1534. [Google Scholar] [CrossRef]

- IEA. World Energy Outlook. 2017. Available online: https://www.iea.org/reports/world-energy-outlook-2017 (accessed on 10 August 2020).

- Jiang, J.; Marsh, T.L.; Tozer, P.R. Policy induced price volatility transmission: Linking the U.S. crude oil, corn and plastics markets. Energy Econ. 2015, 52, 217–227. [Google Scholar] [CrossRef]

- Teterin, P.; Brooks, R.; Enders, W. Smooth volatility shifts and spillovers in U.S. crude oil and corn futures markets. J. Empir. Financ. 2016, 38, 22–36. [Google Scholar] [CrossRef]

- Gu, F.; Wang, J.; Guo, J.; Fan, Y. Dynamic linkages between international oil price, plastic stock index and recycle plastic markets in China. Int. Rev. Econ. Financ. 2020, 68, 167–179. [Google Scholar] [CrossRef]

- Adland, R.; Cullinane, K. The non-linear dynamics of spot freight rates in tanker markets. Transp. Res. E Logist. Transp. Rev. 2006, 42, 211–224. [Google Scholar] [CrossRef]

- Alizadeh, A.H.; Huang, C.-Y.; van Dellen, S. A regime switching approach for hedging tanker shipping freight rates. Energy Econ. 2015, 49, 44–59. [Google Scholar] [CrossRef]

- Poulakidas, A.; Joutz, F. Exploring the link between oil prices and tanker rates. Marit. Policy Manag. 2009, 36, 215–233. [Google Scholar] [CrossRef]

- Chen, F.; Miao, Y.; Tian, K.; Ding, X.; Li, T. Multifractal cross-correlations between crude oil and tanker freight rate. Phys. Stat. Mech. Appl. 2017, 474, 344–354. [Google Scholar] [CrossRef]

- Wang, Y.; Liu, L.; Wu, C. Forecasting the real prices of crude oil using forecast combinations over time-varying parameter models. Energy Econ. 2017, 66, 337–348. [Google Scholar] [CrossRef]

- Kilian, L. Not All Oil Price Shocks Are Alike: Disentangling Demand and Supply Shocks in the Crude Oil Market. Am. Econ. Rev. 2009, 99, 1053–1069. [Google Scholar] [CrossRef]

- Ruan, Q.; Wang, Y.; Lu, X.; Qin, J. Cross-correlations between Baltic Dry Index and crude oil prices. Phys. Stat. Mech. Appl. 2016, 453, 278–289. [Google Scholar] [CrossRef]

- Lin, A.J.; Chang, H.Y.; Hsiao, J.L. Does the Baltic Dry Index drive volatility spillovers in the commodities, currency, or stock markets? Transp. Res. E Logist. Transp. Rev. 2019, 127, 265–283. [Google Scholar] [CrossRef]

- Forbes, K.J.; Rigobon, R. No Contagion, Only Interdependence: Measuring Stock Market Comovements. J. Financ. 2002, 57, 2223–2261. [Google Scholar] [CrossRef]

- Guesmi, K.; Abid, I.; Creti, A.; Chevallier, J. Oil Price Risk and Financial Contagion. Energy J. 2018, 39, 97. [Google Scholar] [CrossRef]

- Kavussanos, M.G.; Nomikos, N.K. The forward pricing function of the shipping freight futures market. J. Futures Mark. 1999, 19, 353–376. [Google Scholar] [CrossRef]

- Tsouknidis, D.A. Dynamic volatility spillovers across shipping freight markets. Transp. Res. Part E Logist. Transp. Rev. 2016, 91, 90–111. [Google Scholar] [CrossRef]

- Bouri, E.; Gkillas, K.; Gupta, R.; Pierdzioch, C. Forecasting Realized Volatility of Bitcoin: The Role of the Trade War. Comput. Econ. 2021, 57, 29–53. [Google Scholar] [CrossRef]

- Gong, Y.; Li, K.X.; Chen, S.-L.; Shi, W. Contagion risk between the shipping freight and stock markets: Evidence from the recent US-China trade war. Transp. Res. Part E Logist. Transp. Rev. 2020, 136, 101900. [Google Scholar] [CrossRef]

- Yang, J.; Zhang, X.; Ge, Y.-E. Measuring risk spillover effects on dry bulk shipping market: A value-at-risk approach. Marit. Policy Manag. 2022, 49, 558–576. [Google Scholar] [CrossRef]

- Conrad, C.; Custovic, A.; Ghysels, E. Long- and Short-Term Cryptocurrency Volatility Components: A GARCH-MIDAS Analysis. J. Risk Financ. Manag. 2018, 11, 23. [Google Scholar] [CrossRef]

- Wang, L.; Ma, F.; Liu, J.; Yang, L. Forecasting stock price volatility: New evidence from the GARCH-MIDAS model. Int. J. Forecast. 2020, 36, 684–694. [Google Scholar] [CrossRef]

- Salisu, A.A.; Gupta, R.; Bouri, E.; Ji, Q. Mixed-frequency forecasting of crude oil volatility based on the information content of global economic conditions. J. Forecast. 2022, 41, 134–157. [Google Scholar] [CrossRef]

- Salisu, A.A.; Gupta, R.; Bouri, E.; Ji, Q. The role of global economic conditions in forecasting gold market volatility: Evidence from a GARCH-MIDAS approach. Res. Int. Bus. Financ. 2020, 54, 101308. [Google Scholar] [CrossRef]

- Shi, Y.; Wang, L.; Ke, J. Does the US-China trade war affect co-movements between US and Chinese stock markets? Res. Int. Bus. Financ. 2021, 58, 101477. [Google Scholar] [CrossRef]

- An, S.; Gao, X.; An, H.; An, F.; Sun, Q.; Liu, S. Windowed volatility spillover effects among crude oil prices. Energy 2020, 200, 117521. [Google Scholar] [CrossRef]

- Hamilton, J.D. Causes and Consequences of the Oil Shock of 2007–08; Brookings Paper on Economic Activity; The Brookings Institution: Washington, DC, USA, 2009; pp. 215–261. [Google Scholar]

- Kilian, L.; Park, C. The Impact of Oil Price Shocks on the U.S. Stock Market. Int. Econ. Rev. 2009, 50, 1267–1287. [Google Scholar] [CrossRef]

- Boubaker, S.; Jouini, J.; Lahiani, A. Financial contagion between the US and selected developed and emerging countries: The case of the subprime crisis. Q. Rev. Econ. Financ. 2016, 61, 14–28. [Google Scholar] [CrossRef]

- Creti, A.; Joëts, M.; Mignon, V. On the links between stock and commodity markets’ volatility. Energy Econ. 2013, 37, 16–28. [Google Scholar] [CrossRef]

- Zhang, Y.-J.; Wang, J.-L. Do high-frequency stock market data help forecast crude oil prices? Evidence from the MIDAS models. Energy Econ. 2019, 78, 192–201. [Google Scholar] [CrossRef]

- Bonga-Bonga, L. Uncovering equity market contagion among BRICS countries: An application of the multivariate GARCH model. Q. Rev. Econ. Financ. 2018, 67, 36–44. [Google Scholar] [CrossRef]

- Arouri, M.E.H.; Lahiani, A.; Nguyen, D.K. Return and volatility transmission between world oil prices and stock markets of the GCC countries. Econ. Model. 2011, 28, 1815–1825. [Google Scholar] [CrossRef]

- Engle, R.F.; Ghysels, E.; Sohn, B. Stock Market Volatility and Macroeconomic Fundamentals. Rev. Econ. Stat. 2013, 95, 776–797. [Google Scholar] [CrossRef]

- Engle, R.F.; Rangel, J.G. The Spline-GARCH Model for Low-Frequency Volatility and Its Global Macroeconomic Causes. Rev. Financ. Stud. 2008, 21, 1187–1222. [Google Scholar] [CrossRef]

- Bełdycka-Bórawska, A.; Bórawski, P.; Borychowski, M.; Wyszomierski, R.; Bórawski, M.B.; Rokicki, T.; Ochnio, L.; Jankowski, K.; Mickiewicz, B.; Dunn, J.W. Development of Solid Biomass Production in Poland, Especially Pellet, in the Context of the World’s and the European Union’s Climate and Energy Policies. Energies 2021, 14, 3587. [Google Scholar] [CrossRef]

- Fałdziński, M.; Fiszeder, P.; Orzeszko, W. Forecasting Volatility of Energy Commodities: Comparison of GARCH Models with Support Vector Regression. Energies 2020, 14, 6. [Google Scholar] [CrossRef]

- Conrad, C.; Kleen, O. Two are better than one: Volatility forecasting using multiplicative component GARCH-MIDAS models. J. Appl. Econ. 2020, 35, 19–45. [Google Scholar] [CrossRef]

- Javed, F.; Asgharian, H.; Hou, A.J. Importance of macroeconomic variables for variance prediction: A GARCH-MIDAS approach. J. Forecast. 2013, 32, 600–612. [Google Scholar]

- Conrad, C.; Loch, K.; Rittler, D. On the macroeconomic determinants of long-term volatilities and correlations in U.S. stock and crude oil markets. J. Empir. Financ. 2014, 29, 26–40. [Google Scholar] [CrossRef]

- Koskinen, M.-M.; Hilmola, O.-P. Investment Cycles in the Newbuilding Market of Ice-Strengthened Oil Tankers. Marit. Econ. Logist. 2005, 7, 173–188. [Google Scholar] [CrossRef]

- Robe, M.A.; Wallen, J. Fundamentals, Derivatives Market Information and Oil Price Volatility. J. Futures Mark. 2016, 36, 317–344. [Google Scholar] [CrossRef]

- Ji, Q.; Fan, Y. How does oil price volatility affect non-energy commodity markets? Appl. Energy 2012, 89, 273–280. [Google Scholar] [CrossRef]

| Mean | Median | Sd | Skew | Kurt | ADF | PP | JB | |

|---|---|---|---|---|---|---|---|---|

| WTI | −0.004 | 0.003 | 0.129 | −19.452 | 442.537 | −41.441 *** | −41.565 *** | 5,889,872 *** |

| BDI | −0.018 | 0.019 | 0.361 | 0.828 | 6.341 | −17.902 *** | −17.897 *** | 420.56 *** |

| BDTI | 0.003 | 0.010 | 0.245 | 0.016 | 4.760 | −22.461 *** | −23.189 *** | 93.736 *** |

| BCTI | 0.005 | 0.088 | 0.321 | −1.210 | 7.129 | −21.795 *** | −22.517 *** | 692.84 *** |

| PTA | 0.008 | 0.027 | 0.086 | −0.750 | 3.929 | −32.652 *** | −32.988 *** | 94.207 *** |

| PVC | 0.000 | −0.004 | 0.093 | 0.564 | 4.357 | −36.543 *** | −36.534 *** | 55.738 *** |

| PP | −0.001 | −0.006 | 0.069 | 0.009 | 3.264 | −37.135 *** | −37.170 *** | 40.587 *** |

| LLDPE | 0.003 | −0.009 | 0.067 | 0.318 | 3.151 | −36.829 *** | −36.851 *** | 12.915 *** |

| Variables/Test | ADF | PP | KPSS |

|---|---|---|---|

| ΔWTI | −41.441 *** | −41.565 *** | 0.182 |

| ΔBDI | −17.902 *** | −17.897 *** | −36.851 *** |

| ΔBDTI | −22.461 *** | 0.533 ** | 0.136 |

| ΔBCTI | −21.795 *** | −23.189 *** | 0.644 ** |

| ΔPTA | −32.652 *** | −22.517 *** | 0.447 * |

| ΔPVC | −36.543 *** | −32.988 *** | 0.379 ** |

| ΔLLDPE | −37.135 *** | −36.534 *** | 0.24 |

| ΔPP | −36.829 *** | −37.170 *** | 0.296 |

| Variable | Μ | α | β | m | θ | BIC | |

|---|---|---|---|---|---|---|---|

| BDI | 0.166 (0.189) | 0.000 (0.120) | 0.360 (0.243) | −1.269 (1.416) | 0.083 (0.064) | 5.334 *** (1.046) | 260.488 |

| BDTI | 0.180 (0.180) | 0.000 (0.144) | 0.350 (0.287) | −0.388 (0.709) | 0.064 (0.048) | 5.290 *** (1.148) | 264.304 |

| BCTI | 0.133 (0.206) | 0.000 (0.152) | 0.964 *** (0.077) | 0.262 (15.113) | −0.051 (0.472) | 3.161 (12.077) | 265.751 |

| PTA | 0.170 (0.189) | 0.000 (0.169) | 0.351 (0.283) | 3.274 (2.743) | −0.589 (0.579) | 11.461 ** (5.163) | 264.210 |

| PVC | 0.134 (0.175) | 0.000 (0.118) | 0.980 *** (0.070) | 0.303 (6.203) | −0.054 (0.200) | 3.644 *** (0.165) | 264.351 |

| LLDPE | 0.202 (0.138) | 0.000 (0.101) | 0.799 *** (0.112) | 7.797 *** (2.693) | −0.805 *** (0.292) | 1.697 *** (0.471) | 260.453 |

| PP | 0.175 (0.185) | 0.000 (0.100) | 0.330 (0.267) | 0.713 (0.839) | −0.008 (0.044) | 1.000 (2.616) | 266.811 |

| Μ | α | β | m | θ | BIC | ||

|---|---|---|---|---|---|---|---|

| BDI | 0.279 ** (0.113) | 0.080 (0.067) | 0.878 *** (0.029) | 8.568 *** (2.474) | −0.117 *** (0.037) | 1.784 *** (0.281) | 1419.643 |

| BDTI | 0.251 ** (0.107) | 0.091 *** (0.003) | 0.894 *** (0.003) | 1.803 *** (0.236) | 0.008 *** (0.002) | 3.140 ** (3.705) | 1415.199 |

| BCTI | 0.268 ** (0.114) | 0.052 * (0.027) | 0.913 *** (0.025) | 5.864 *** (1.390) | −0.069 *** (0.025) | 1.078 *** (0.370) | 1403.580 |

| PTA | 0.272 ** (0.124) | 0.041 (0.026) | 0.929 *** (0.031) | 0.395 (0.468) | 0.108 *** (0.028) | 21.491 *** (4.494) | 1409.485 |

| PVC | 0.285 ** (0.111) | 0.138 *** (0.000) | 0.861 *** (0.0006) | −5.206 (1.925) | 0.852 ** (0.338) | 2.810 *** (0.968) | 1410.148 |

| LLDPE | 0.254 ** (0.115) | 0.147 *** (0.0006) | 0.850 *** (0.000) | −4.393 (3.416) | 0.783 *** (0.290) | 1.000 *** (0.168) | 1416.732 |

| PP | 0.261 ** (0.120) | 0.144 *** (0.0001) | 0.856 *** (0.0008) | 9.940 *** (2.898) | −0.286 * (0.167) | 2.730 * (1.463) | 1415.243 |

| Variable | Μ | α | Β | m | θ | BIC | |

|---|---|---|---|---|---|---|---|

| BDI | −0.001 (0.003) | 0.000 (0.099) | 0.483 (0.656) | −6.906 *** (0.128) | 2.310 *** (0.422) | 217.363 *** (28.467) | 274.477 |

| BDTI | 0.005 ** (0.002) | 0.000 (0.035) | 0.968 *** (0.042) | −7.047 *** (0.229) | 2.655 ** (1.147) | 45.263 (38.276) | 1118.216 |

| BCTI | 0.002 (0.002) | 0.338 *** (0.011) | 0.661 *** (0.012) | −2.727 (1.811) | 16,216 (13.375) | 1.319 ** (0.530) | 642.168 |

| PTA | 0.002 (0.002) | 0.347 *** (0.072) | 0.652 *** (0.073) | −3.031 (2.341) | 28.049 (26.240) | 1.000 *** (0.286) | 2167.535 |

| PVC | 0.003 (0.002) | 0.137 ** (0.063) | 0.844 *** (0.053) | −6.529 *** (0.812) | −5.928 ** (3.003) | 274.160 *** (20.564) | 2187.396 |

| LLDPE | 0.004 (0.002) | 0.149 * (0.090) | 0.826 *** (0.062) | −6.413 *** (1.361) | −11.652 ** (5.244) | 223.870 *** (76.000) | 2579.454 |

| PP | 0.003 (0.002) | 0.175 *** (0.067) | 0.810 *** (0.061) | −5.910 *** (0.962) | −112.156 (95.244) | 2.644 *** (0.661) | 2606.940 |

| WTI | |||

|---|---|---|---|

| Before the U.S.-China Trade War (K = 24) | After the U.S.-China Trade War Extended to COVID-19 (K = 24) | Extended to Ukraine-Russia War (K = 24) | |

| BDI | Insignificant | Significant *** | Significant *** |

| BDTI | Insignificant | Significant ** | Significant ** |

| BCTI | Insignificant | Significant *** | Insignificant |

| PTA | Insignificant | Significant *** | Insignificant |

| PVC | Insignificant | Significant *** | Significant ** |

| LLDPE | Significant *** | Significant *** | Significant ** |

| PP | Insignificant | Significant * | Insignificant |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Lin, A.J. Volatility Contagion from Bulk Shipping and Petrochemical Industries to Oil Futures Market during the Economic Uncertainty. Mathematics 2023, 11, 3737. https://doi.org/10.3390/math11173737

Lin AJ. Volatility Contagion from Bulk Shipping and Petrochemical Industries to Oil Futures Market during the Economic Uncertainty. Mathematics. 2023; 11(17):3737. https://doi.org/10.3390/math11173737

Chicago/Turabian StyleLin, Arthur Jin. 2023. "Volatility Contagion from Bulk Shipping and Petrochemical Industries to Oil Futures Market during the Economic Uncertainty" Mathematics 11, no. 17: 3737. https://doi.org/10.3390/math11173737