Forecasting the Volatility of Cryptocurrencies in the Presence of COVID-19 with the State Space Model and Kalman Filter

Abstract

:1. Introduction

2. Materials and Methods

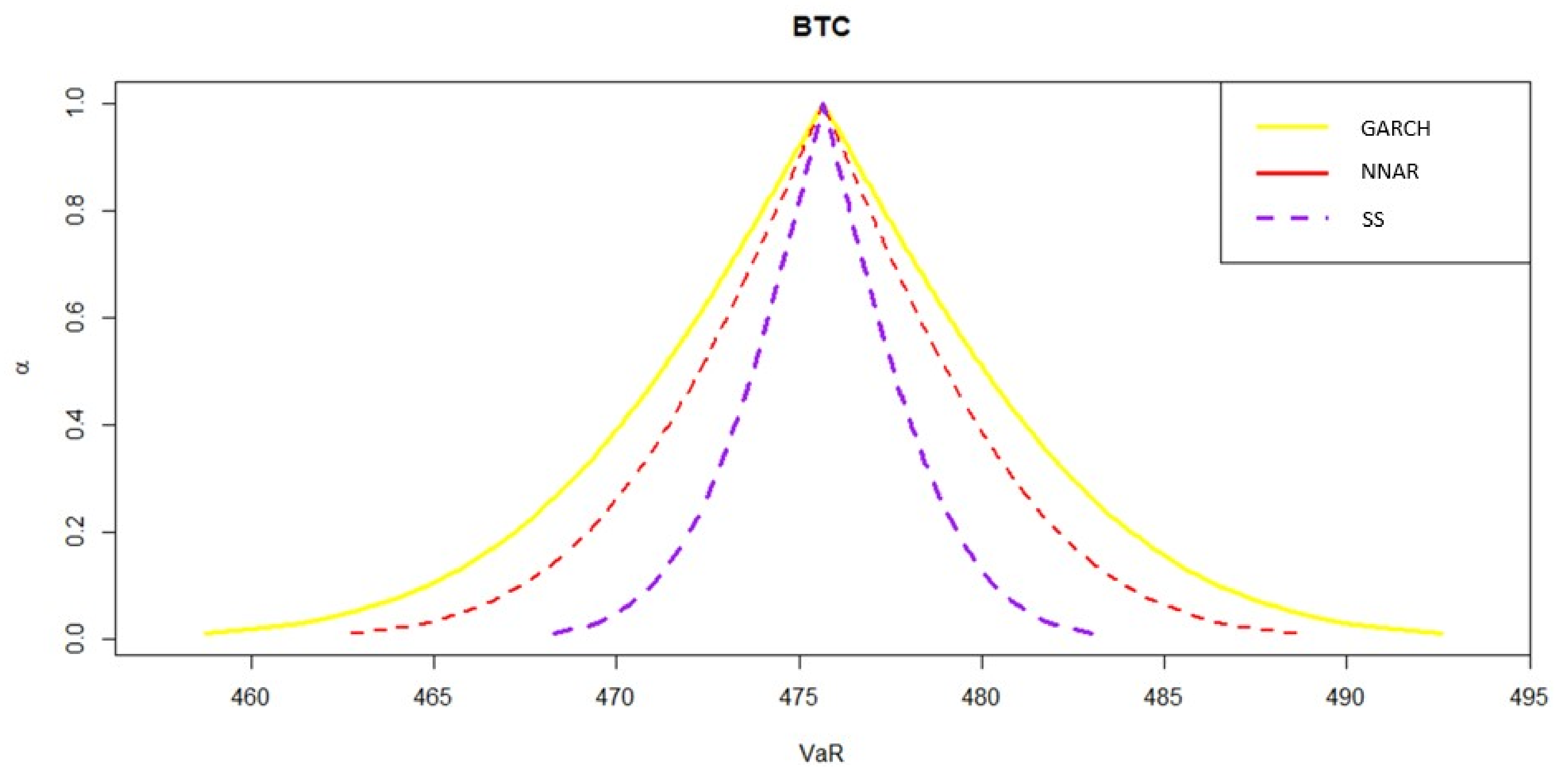

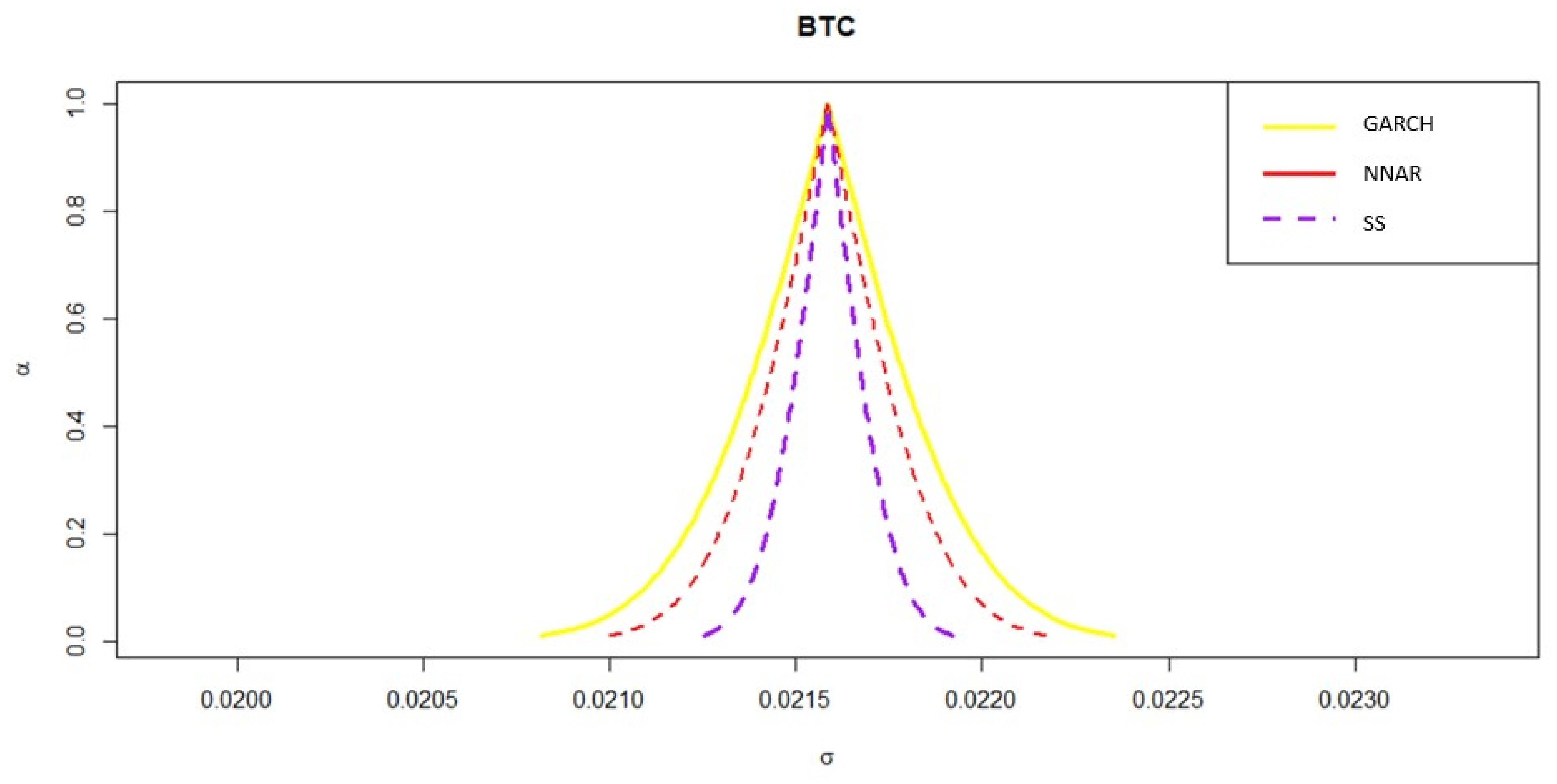

2.1. Forecasting VaR

2.2. The GARCH (1,1) Model

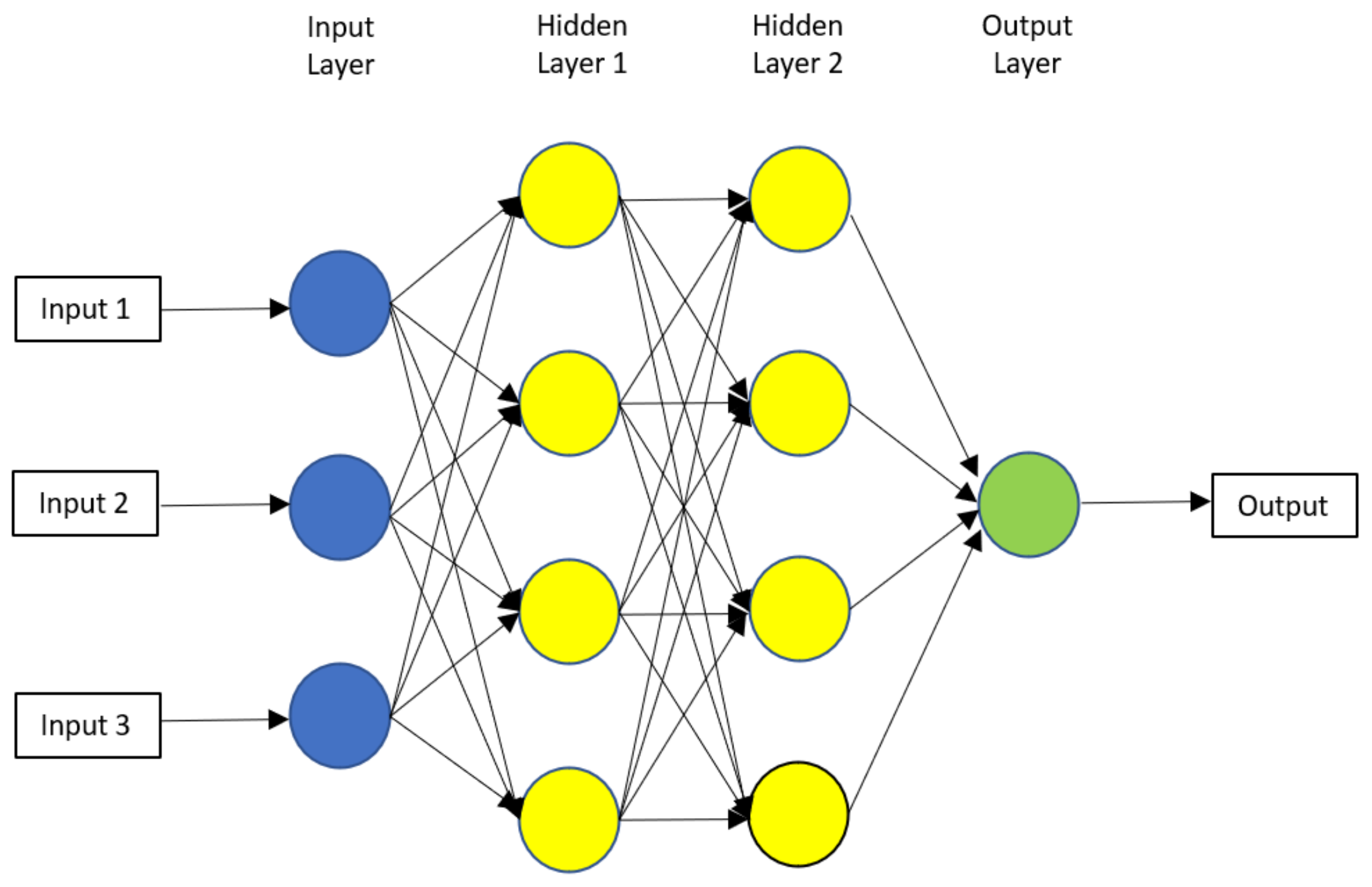

2.3. The NN Autoregressive (NNAR) Model

2.4. The State Space (SS) Model Based on the Kalman Filtering Algorithm for Volatility

2.4.1. Gaussian SS Model

2.4.2. The ARIMA SS Model

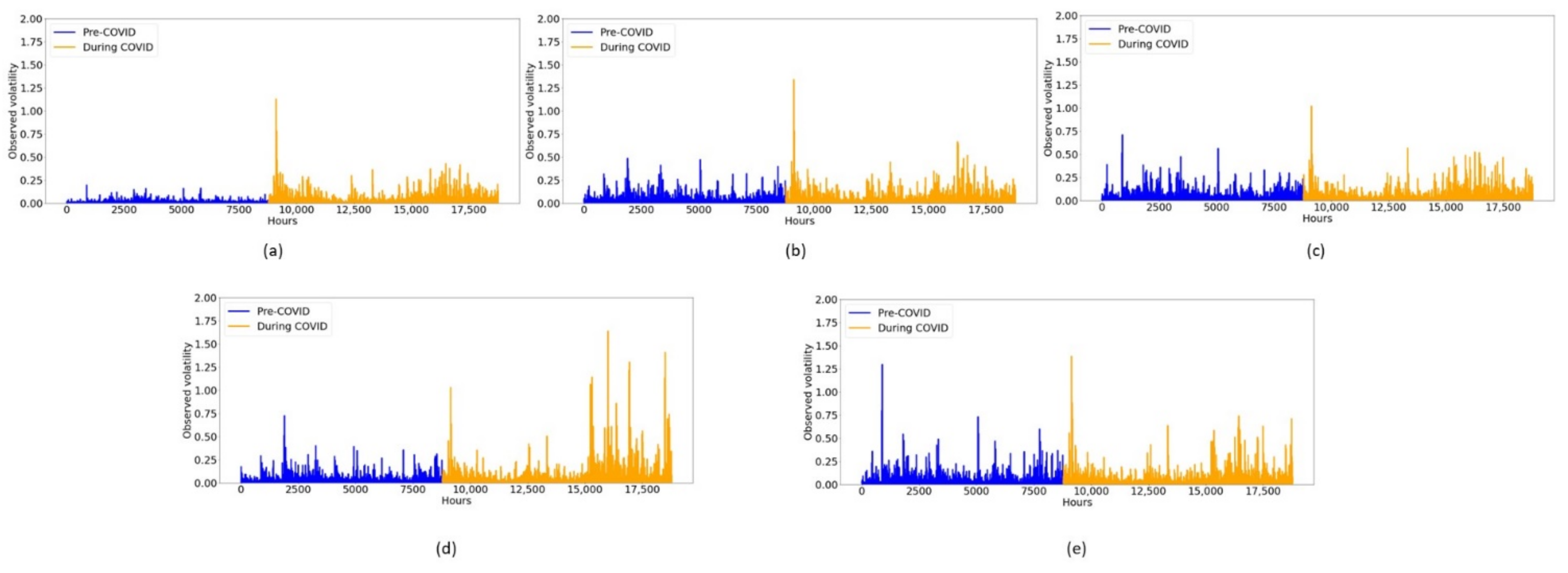

3. Data Description

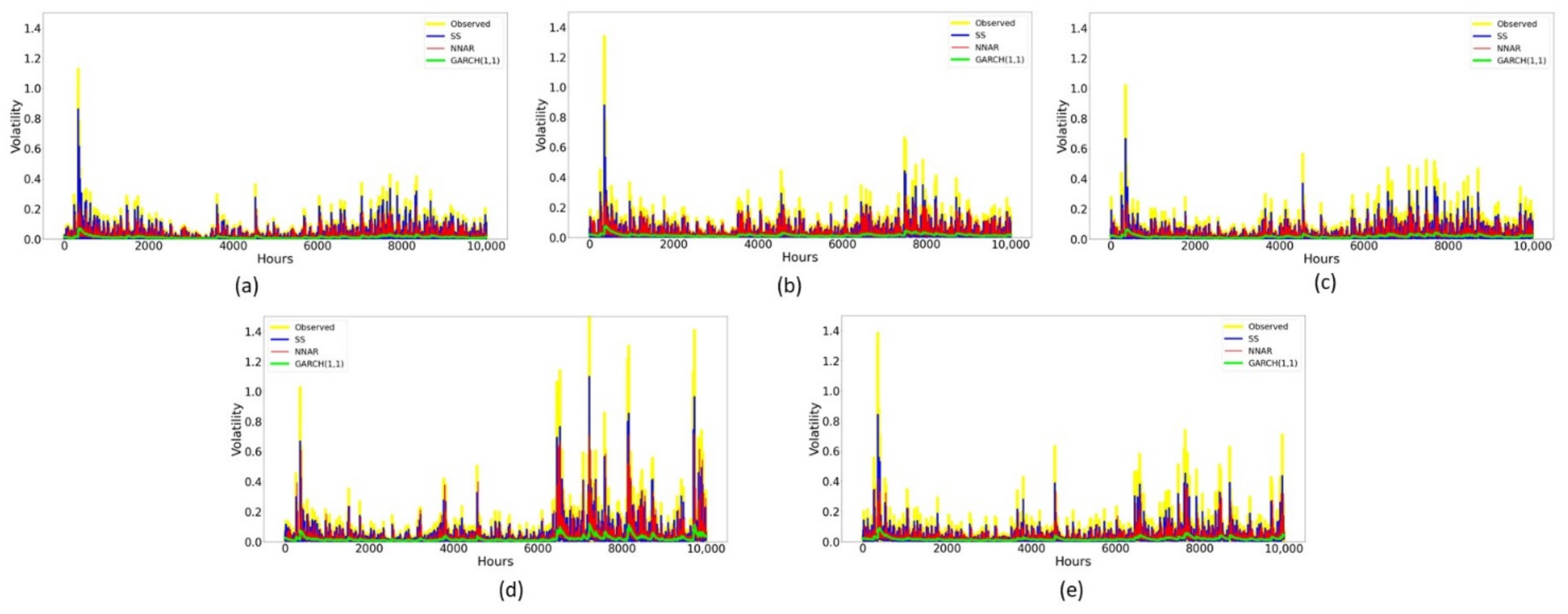

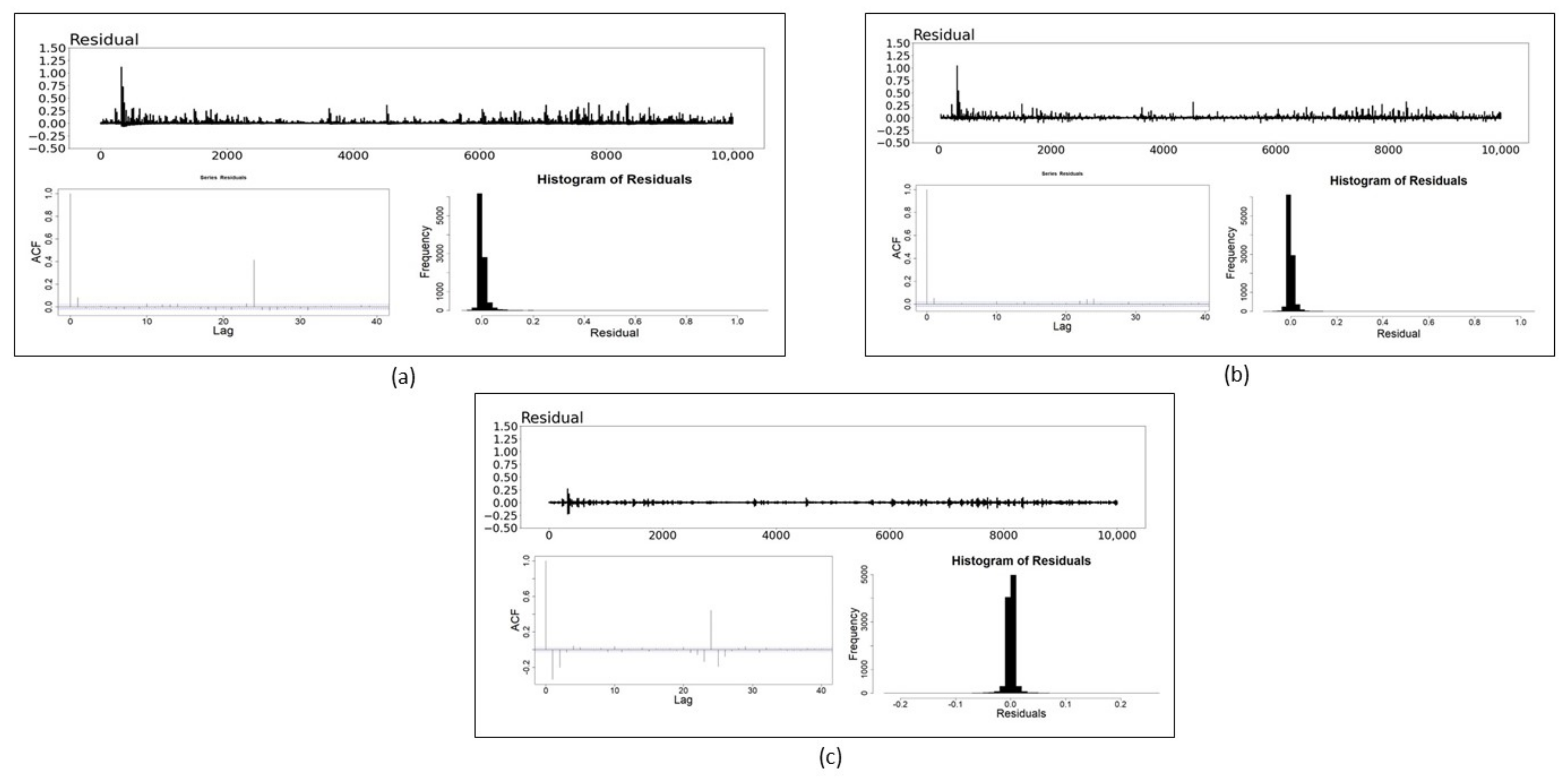

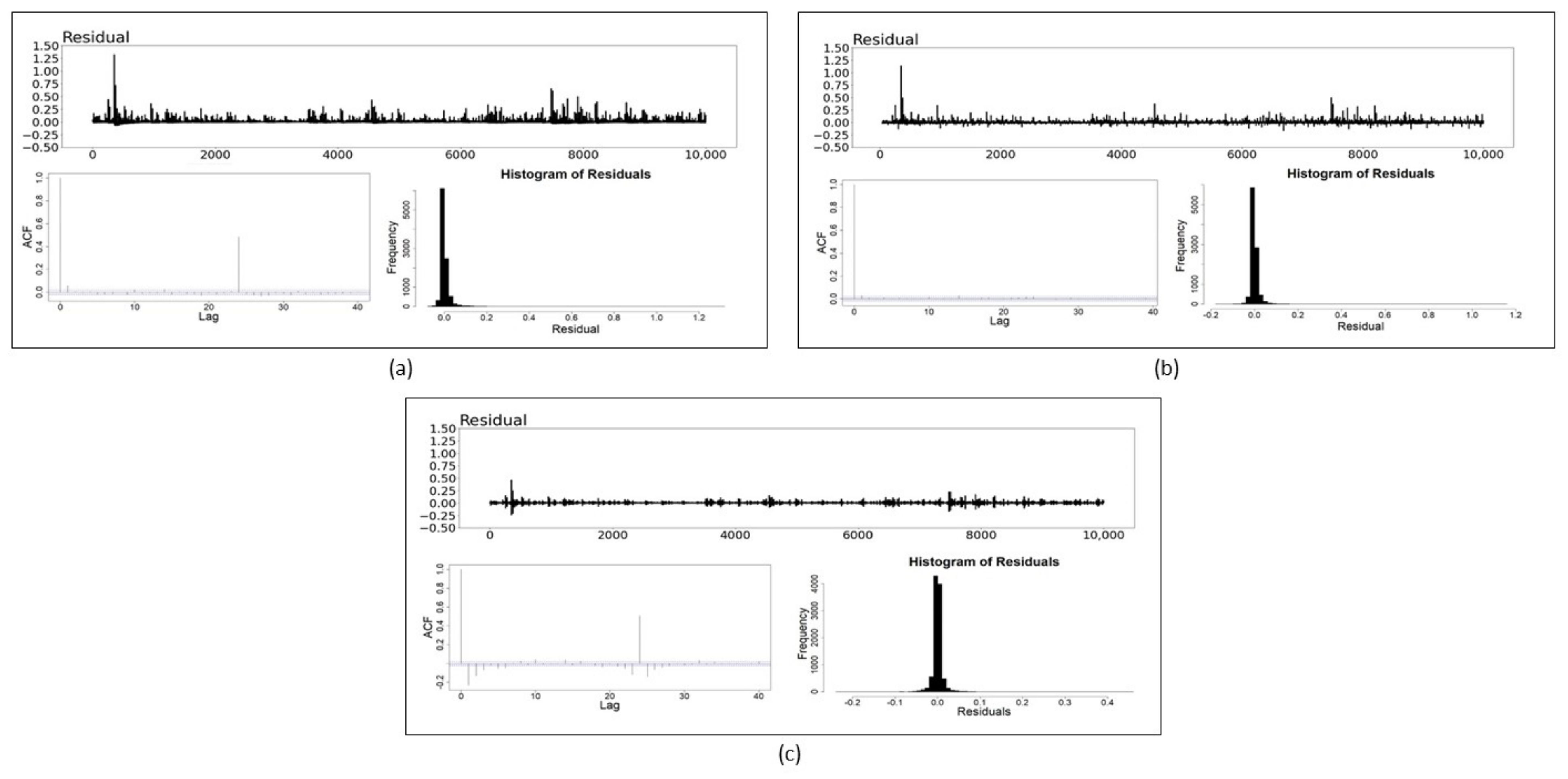

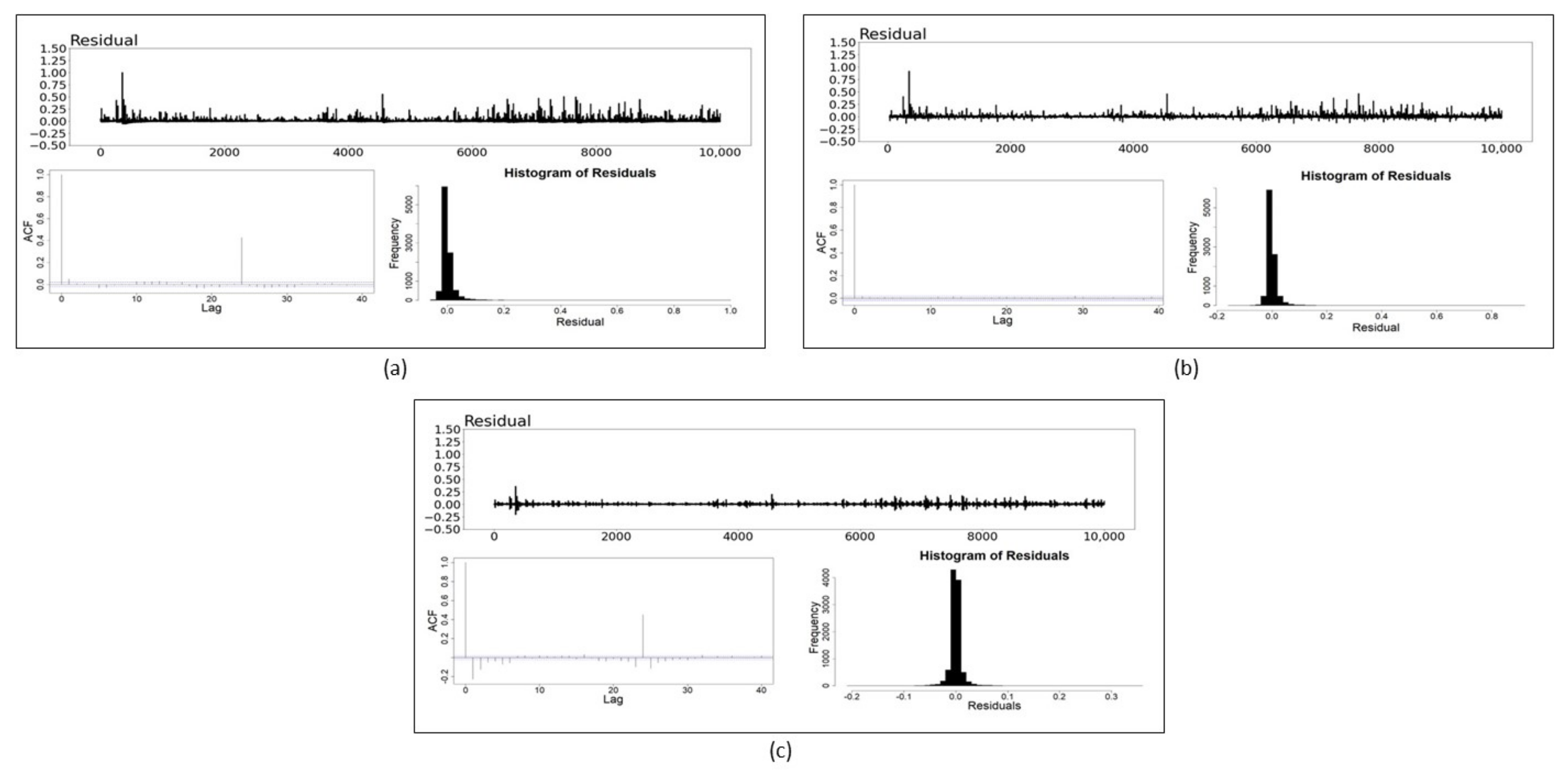

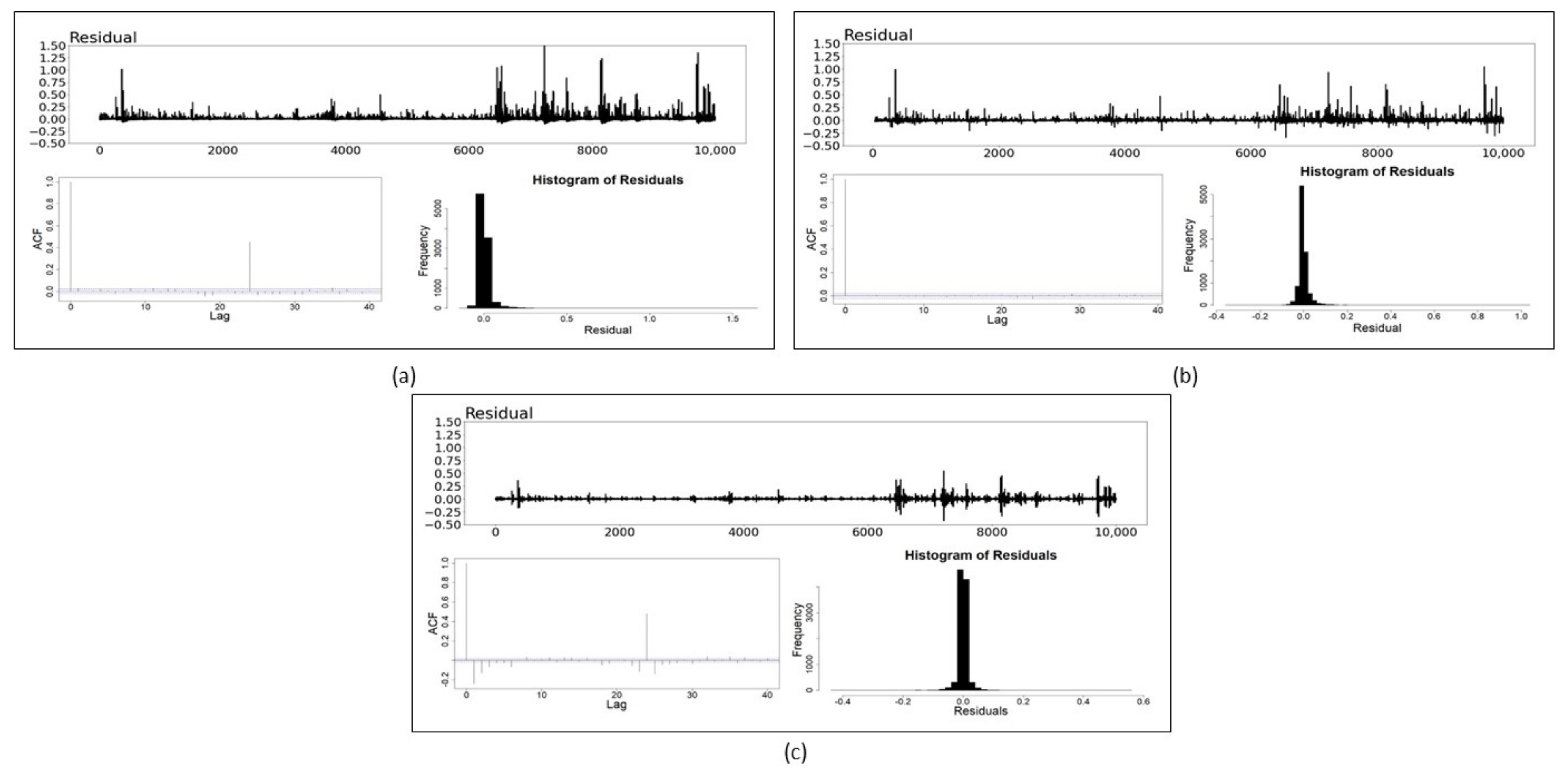

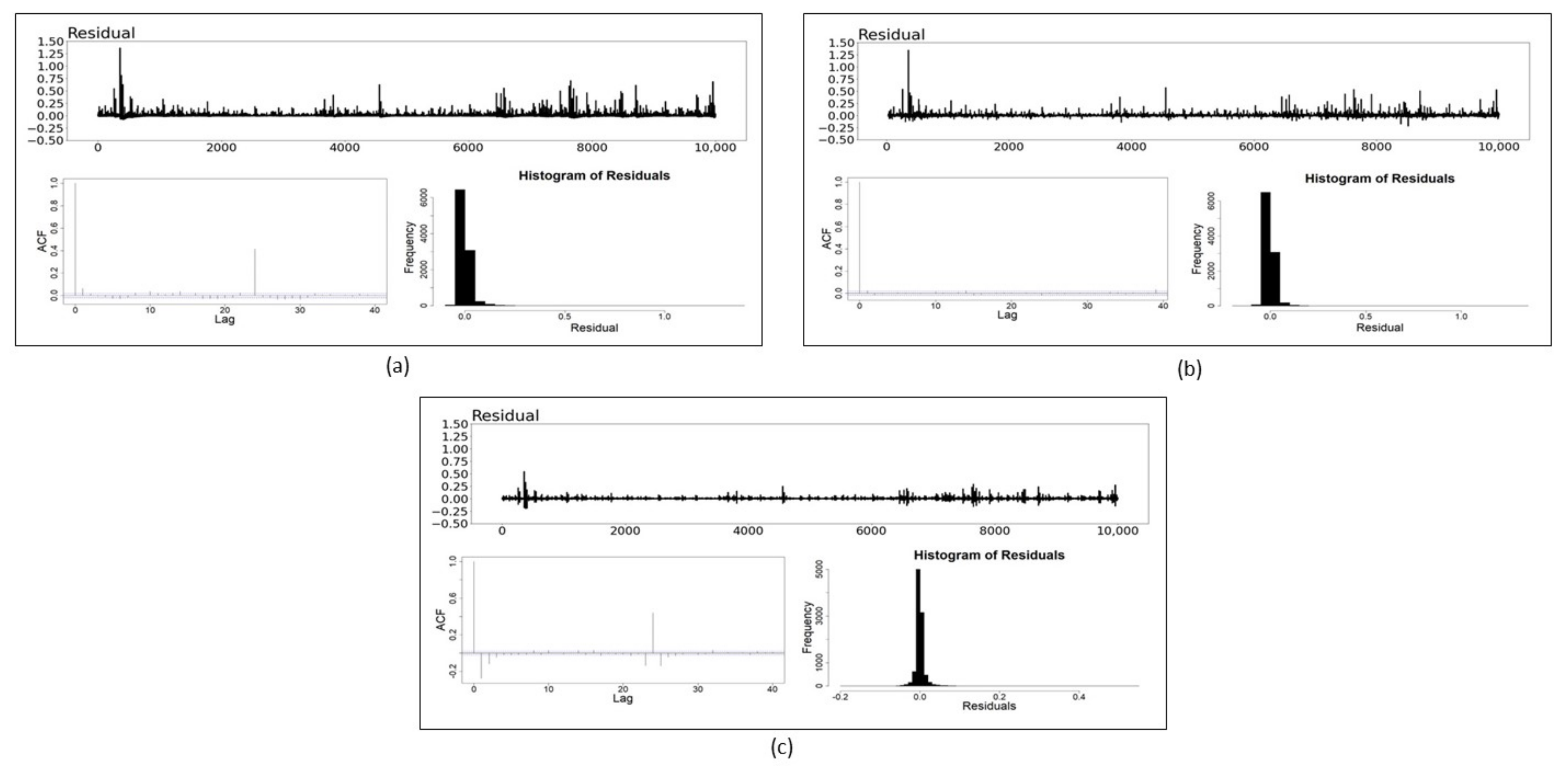

4. Results and Discussion

5. Conclusions

Supplementary Materials

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Milutinović, M. Cryptocurrency. Ekonomika 2018, 64, 105–122. [Google Scholar] [CrossRef]

- Pernice, I.G.A.; Scott, B. Cryptocurrency. Internet Policy Rev. 2021, 10, 1–5. [Google Scholar] [CrossRef]

- Nakamoto, S. Bitcoin: A peer-to-peer electronic cash system. Decentralized Bus. Rev. 2008, 21260, 1–9. [Google Scholar]

- Yli-Huumo, J.; Ko, D.; Choi, S.; Park, S.; Smolander, K. Where is current research on blockchain technology?—A systematic review. PLoS ONE 2016, 11, e0163477. [Google Scholar] [CrossRef] [PubMed]

- Pilkington, M. Blockchain technology: Principles and applications. In Research Handbook on Digital Transformations; Edward Elgar Publishing: London, UK, 2016. [Google Scholar]

- Zheng, Z.; Xie, S.; Dai, H.-N.; Chen, X.; Wang, H. Blockchain challenges and opportunities: A survey. Int. J. Web Grid Serv. 2018, 14, 352. [Google Scholar] [CrossRef]

- Noyes, C. Efficient Blockchain-Driven Multiparty Computation Markets at Scale; Technical Report; San Francisco State University: San Francisco, CA, USA, 2016. [Google Scholar]

- Jaag, C.; Bach, C. Blockchain technology and cryptocurrencies: Opportunities for postal financial services. In The Changing Postal and Delivery Sector; Springer: Cham, Switzerland, 2017; pp. 205–221. [Google Scholar]

- Zhang, Y.; Wen, J. An IoT electric business model based on the protocol of bitcoin. In Proceedings of the 2015 18th International Conference on Intelligence in Next Generation Networks, Paris, France, 17 February 2015; IEEE: Piscataway, NJ, USA, 2015; pp. 184–191. [Google Scholar] [CrossRef]

- Hardjono, T.; Smith, N. Cloud-based commissioning of constrained devices using permissioned blockchains. In Proceedings of the 2nd ACM International Workshop on IoT Privacy, Trust, and Security, Xi’an, China, 30 May–3 June 2016; pp. 29–36. [Google Scholar] [CrossRef]

- Thakur, V.; Doja, M.N.; Dwivedi, Y.K.; Ahmad, T.; Khadanga, G. Land records on blockchain for implementation of land titling in India. Int. J. Inf. Manag. 2020, 52, 101940. [Google Scholar] [CrossRef]

- Gogerty, N.; Zitoli, J. DeKo: An Electricity-Backed Currency Proposal; Social Science Research Network: Rochester, NY, USA, 2011. [Google Scholar]

- Gräther, W.; Kolvenbach, S.; Ruland, R.; Schütte, J.; Torres, C.; Wendland, F. Blockchain for education: Lifelong learning passport. In Proceedings of the 1st ERCIM Blockchain Workshop 2018, European Society for Socially Embedded Technologies (EUSSET), Amsterdam, The Netherlands, 8–9 May 2018. [Google Scholar] [CrossRef]

- Han, M.; Li, Z.; He, J.; Wu, D.; Xie, Y.; Baba, A. A novel blockchain-based education records verification solution. In Proceedings of the 19th Annual SIG Conference on Information Technology Education 2018, Fort Lauderdale, FL, USA, 3–6 October 2018; pp. 178–183. [Google Scholar] [CrossRef]

- BYJUS. Cryptocurrency: Definition, Advantages Disadvantages; BYJUS: Bengaluru, India, 2022; Available online: https://byjus.com/current-affairs/cryptocurrency/ (accessed on 19 August 2022).

- NiBusinessInfo. Accepting Online Payments. Advantages and Disadvantages of Using Cryptocurrency. Available online: https://www.nibusinessinfo.co.uk/content/advantages-and-disadvantages-using-cryptocurrency (accessed on 19 August 2022).

- Mnif, E.; Jarboui, A.; Mouakhar, K. How the cryptocurrency market has performed during COVID 19? A multifractal analysis. Finance Res. Lett. 2020, 36, 101647. [Google Scholar] [CrossRef]

- Demir, E.; Bilgin, M.H.; Karabulut, G.; Doker, A.C. The relationship between cryptocurrencies and COVID-19 pandemic. Eurasian Econ. Rev. 2020, 10, 349–360. [Google Scholar] [CrossRef]

- Umar, Z.; Gubareva, M. A time–frequency analysis of the impact of the Covid-19 induced panic on the volatility of currency and cryptocurrency markets. J. Behav. Exp. Finance 2020, 28, 100404. [Google Scholar] [CrossRef]

- Danielsson, J. Financial Risk Forecasting: The Theory and Practice of Forecasting Market Risk with Implementation in R and Matlab; John Wiley Sons: Hoboken, NJ, USA, 2011; Volume 588. [Google Scholar]

- Engle, R.F. Autoregressive Conditional Heteroscedasticity with Estimates of the Variance of United Kingdom Inflation. Econometrica 1982, 50, 987–1007. [Google Scholar] [CrossRef]

- Bollerslev, T. Generalized autoregressive conditional heteroskedasticity. J. Econ. 1986, 31, 307–327. [Google Scholar] [CrossRef]

- Cheikh, N.B.; Zaied, Y.B.; Chevallier, J. Asymmetric volatility in cryptocurrency markets: New evidence from smooth transition GARCH models. Financ. Res. Lett. 2020, 35, 101293. [Google Scholar] [CrossRef]

- Hu, Y.; Ni, J.; Wen, L. A hybrid deep learning approach by integrating LSTM-ANN networks with GARCH model for copper price volatility prediction. Phys. A Stat. Mech. Its Appl. 2020, 557, 124907. [Google Scholar] [CrossRef]

- Kim, J.-M.; Jun, C.; Lee, J. Forecasting the Volatility of the Cryptocurrency Market by GARCH and Stochastic Volatility. Mathematics 2021, 9, 1614. [Google Scholar] [CrossRef]

- Nelson, D.B. Stationarity and Persistence in the GARCH(1,1) Model. Econ. Theory 1990, 6, 318–334. [Google Scholar] [CrossRef]

- Jafari, G.R.; Bahraminasab, A.; Norouzzadeh, P. Why Does the Standard Garch(1, 1) Model Work Well? Int. J. Mod. Phys. C 2007, 18, 1223–1230. [Google Scholar] [CrossRef]

- Ramos-Pérez, E.; Alonso-González, P.J.; Núñez-Velázquez, J.J. Forecasting volatility with a stacked model based on a hybridized Artificial Neural Network. Expert Syst. Appl. 2019, 129, 1–9. [Google Scholar] [CrossRef]

- Ewees, A.A.; Abd Elaziz, M.; Alameer, Z.; Ye, H.; Jianhua, Z. Improving multilayer perceptron neural network using chaotic grasshopper optimization algorithm to forecast iron ore price volatility. Resour. Policy 2020, 65, 101555. [Google Scholar] [CrossRef]

- Othman, A.; Kassim, S.; Bin Rosman, R.; Redzuan, N.H.B. Prediction accuracy improvement for Bitcoin market prices based on symmetric volatility information using artificial neural network approach. J. Revenue Pricing Manag. 2020, 19, 314–330. [Google Scholar] [CrossRef]

- Baffour, A.A.; Feng, J.; Taylor, E.K. A hybrid artificial neural network-GJR modeling approach to forecasting currency exchange rate volatility. Neurocomputing 2019, 365, 285–301. [Google Scholar] [CrossRef]

- Hyndman, R.; Athanasopoulos, G.; Bergmeir, C.; Caceres, G.; Chhay, L.; O’Hara-Wild, M.; Petropoulos, F.; Razbash, S.; Wang, E.; Yasmeen, F. Forecast: Forecasting Functions for Time Series and Linear Models, R Package: Version 8.15. 2021. Available online: https://pkg.robjhyndman.com/forecast/ (accessed on 15 July 2021).

- Thavaneswaran, A.; Thulasiram, R.K.; Zhu, Z.; Hoque, M.E.; Ravishanker, N. Fuzzy Value-at-Risk Forecasts Using a Novel Data-Driven Neuro Volatility Predictive Model. In Proceedings of the 2019 IEEE 43rd Annual Computer Software and Applications Conference (COMPSAC), Milwaukee, WI, USA, 15 June 2019; IEEE: Piscataway, NJ, USA, 2019; Volume 2, pp. 221–226. [Google Scholar] [CrossRef]

- Koller, D.; Friedman, N. Probabilistic Graphical Models; MIT Press: Cambridge, MA, USA, 2009. [Google Scholar]

- Kalman, R.E. A New Approach to Linear Filtering and Prediction Problems. J. Basic Eng. 1960, 82, 35–45. [Google Scholar] [CrossRef]

- Khashei, M.; Sharif, B.M. A Kalman filter-based hybridization model of statistical and intelligent approaches for exchange rate forecasting. J. Model. Manag. 2020, 16, 579–601. [Google Scholar] [CrossRef]

- Safari, A.; Davallou, M. Oil price forecasting using a hybrid model. Energy 2018, 148, 49–58. [Google Scholar] [CrossRef]

- Timmer, J.; Weigend, A.S. Modeling Volatility Using State Space Models. Int. J. Neural Syst. 1997, 8, 385–398. [Google Scholar] [CrossRef]

- Durbin, J.; Koopman, S.J. Time Series Analysis by State Space Methods; Oxford University Press: Oxford, UK, 2012. [Google Scholar]

- Ramos, P.; Santos, N.; Rebelo, R. Performance of state space and ARIMA models for consumer retail sales forecasting. Robot. Comput. Manuf. 2015, 34, 151–163. [Google Scholar] [CrossRef]

- Svetunkov, I.; Boylan, J.E. State-space ARIMA for supply-chain forecasting. Int. J. Prod. Res. 2020, 58, 818–827. [Google Scholar] [CrossRef]

- Hooda, E.; Verma, U.; Hooda, B.K. ARIMA and State-Space models for sugarcane (Saccharum officinarum) yield forecasting in Northern agro-climatic zone of Haryana. J. Appl. Nat. Sci. 2020, 12, 53–58. [Google Scholar] [CrossRef]

- Thavaneswaran, A.; Paseka, A.; Frank, J. Generalized value at risk forecasting. Commun. Stat.-Theory Methods 2020, 49, 4988–4995. [Google Scholar] [CrossRef]

- Ghalanos, A. Rugarch: Univariate Garch Models, R Package Version 1.4-1. 2020. Available online: https://cran.r-project.org/web/packages/rugarch/index.html (accessed on 15 July 2021).

- BuHamra, S.; Smaoui, N.; Gabr, M. The Box–Jenkins analysis and neural networks: Prediction and time series modelling. Appl. Math. Model. 2003, 27, 805–815. [Google Scholar] [CrossRef]

- Hyndman, R.J.; Khandakar, Y. Automatic Time Series Forecasting: The forecast Package for R. J. Stat. Softw. 2008, 27, 1–22. [Google Scholar] [CrossRef]

- Helske, J. KFAS: Exponential Family State Space Models in R. J. Stat. Softw. 2017, 78, 1–39. [Google Scholar] [CrossRef]

- Kwiatkowski, D.; Phillips, P.C.B.; Schmidt, P.; Shin, Y. Testing the null hypothesis of stationarity against the alternative of a unit root: How sure are we that economic time series have a unit root? J. Econom. 1992, 54, 159–178. [Google Scholar] [CrossRef]

- Top 5 Potentially Profitable Cryptocurrencies in 2020: Investment Advice. Yahoo! Finances. 3 February 2020. Available online: https://finance.yahoo.com/news/top-5-potentially-profitable-cryptocurrencies-100627541.html (accessed on 19 August 2022).

- El Montasser, G.; Charfeddine, L.; Benhamed, A. COVID-19, cryptocurrencies bubbles and digital market efficiency: Sensitivity and similarity analysis. Finance Res. Lett. 2022, 46, 102362. [Google Scholar] [CrossRef]

- Ethereum Ethereum Launches. Ethereum Foundation Blog. Available online: https://blog.ethereum.org/2015/07/30/ethereum-launches/ (accessed on 19 August 2022).

- Dannen, C. Introducing Ethereum and Solidity; Apress: Berkeley, CA, USA, 2017; Volume 1, pp. 159–160. [Google Scholar]

- Lee, C. [ANN] Litecoin—A Lite Version of Bitcoin. Launched! Bitcoin Forum. Available online: https://bitcointalk.org/index.php?topic=47417.0 (accessed on 19 August 2022).

- Litecoin Whitepaper. Available online: https://whitepaper.io/document/683/litecoin-whitepaper (accessed on 19 August 2022).

- Schwartz, D.; Youngs, N.; Britto, A. The ripple protocol consensus algorithm. Ripple Labs Inc. White Paper 2014, 5, 151. [Google Scholar]

- Catania, L.; Grassi, S.; Ravazzolo, F. Predicting the volatility of cryptocurrency time-series. In Mathematical and Statistical Methods for Actuarial Sciences and Finance; Springer: Cham, Switzerland, 2018; pp. 203–207. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Cryptocurrency | Initial Release Date | Original Author | Usage |

|---|---|---|---|

| Bitcoin (BTC) | 9 January 2009 | Satoshi Nakamoto [3] | Largest cryptocurrency in the world. Alternative to currencies. |

| Ethereum (ETH) | 30 July 2015 | Vitalik Buterin & Gavin Wood [51] | Coin value is referred to as Ether which is the native token to Ethereum that can be used as an alternative to currencies. Ethereum makes it possible for creating and running applications, smart contracts etc. on the network [52]. |

| Litecoin (LTC) | 9 October 2011 | Charlie Lee [53] | Peer-to-peer internet currency with instant transactions and near-zero cost payments to anyone in the world [54]. |

| Ripple (XRP) | June 2012 | David Schwartz, Jed McCaleb, & Arthur Britto | Digital payment network and protocol [55]. |

| Bitcoin Cash (BCH) | August 2017 | Bitcoin Cash is a fork of Bitcoin | Electronic cash payment system. |

| Dataset | Maximum | Minimum | Mean | Median | Standard Deviation | Skewness | Kurtosis | NNAR | ARIMA |

|---|---|---|---|---|---|---|---|---|---|

| BTC | 1 | −0.49492 | 0.000189 | −0.00014 | 0.015105 | −3.47787 | 174.4704 | (39,0,20) | (5,1,1) |

| ETH | 1 | −0.61396 | 0.000233 | −0.00021 | 0.018783 | −2.75487 | 163.5906 | (39,0,20) | (5,2,0) |

| LTC | 1 | −0.49576 | 0.000155 | −0.00011 | 0.019459 | −1.26584 | 81.98503 | (32,0,16) | (5,2,0) |

| XRP | 1 | −0.66014 | 0.000201 | 0 | 0.025944 | 2.698127 | 152.0154 | (35,0,18) | (5,2,0) |

| BCH | 1 | −0.61638 | 0.000132 | −0.0000866 | 0.020892 | −2.55303 | 140.3643 | (28,0,14) | (1,1,2) |

| MODEL | BTC | ETH | LTC | XRP | BCH | |||||

|---|---|---|---|---|---|---|---|---|---|---|

| RMSE | MAE | RMSE | MAE | RMSE | MAE | RMSE | MAE | RMSE | MAE | |

| GARCH (1,1) | 0.0299 | 0.0116 | 0.0354 | 0.0144 | 0.0340 | 0.0147 | 0.0562 | 0.0192 | 0.0409 | 0.0162 |

| NNAR | 0.0227 | 0.0099 | 0.0257 | 0.0121 | 0.0265 | 0.0130 | 0.0393 | 0.0169 | 0.0334 | 0.0149 |

| SS | 0.0109 | 0.0046 | 0.0155 | 0.0070 | 0.0150 | 0.0072 | 0.0248 | 0.0096 | 0.0182 | 0.0077 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Azman, S.; Pathmanathan, D.; Thavaneswaran, A. Forecasting the Volatility of Cryptocurrencies in the Presence of COVID-19 with the State Space Model and Kalman Filter. Mathematics 2022, 10, 3190. https://doi.org/10.3390/math10173190

Azman S, Pathmanathan D, Thavaneswaran A. Forecasting the Volatility of Cryptocurrencies in the Presence of COVID-19 with the State Space Model and Kalman Filter. Mathematics. 2022; 10(17):3190. https://doi.org/10.3390/math10173190

Chicago/Turabian StyleAzman, Shafiqah, Dharini Pathmanathan, and Aerambamoorthy Thavaneswaran. 2022. "Forecasting the Volatility of Cryptocurrencies in the Presence of COVID-19 with the State Space Model and Kalman Filter" Mathematics 10, no. 17: 3190. https://doi.org/10.3390/math10173190