Investigating the Effect of Perceived Security, Perceived Trust, and Information Quality on Mobile Payment Usage through Near-Field Communication (NFC) in Saudi Arabia

,

,

,

,  ,

,

Abstract

:1. Introduction

2. Literature Review

Near-Field Communication (NFC) Technology

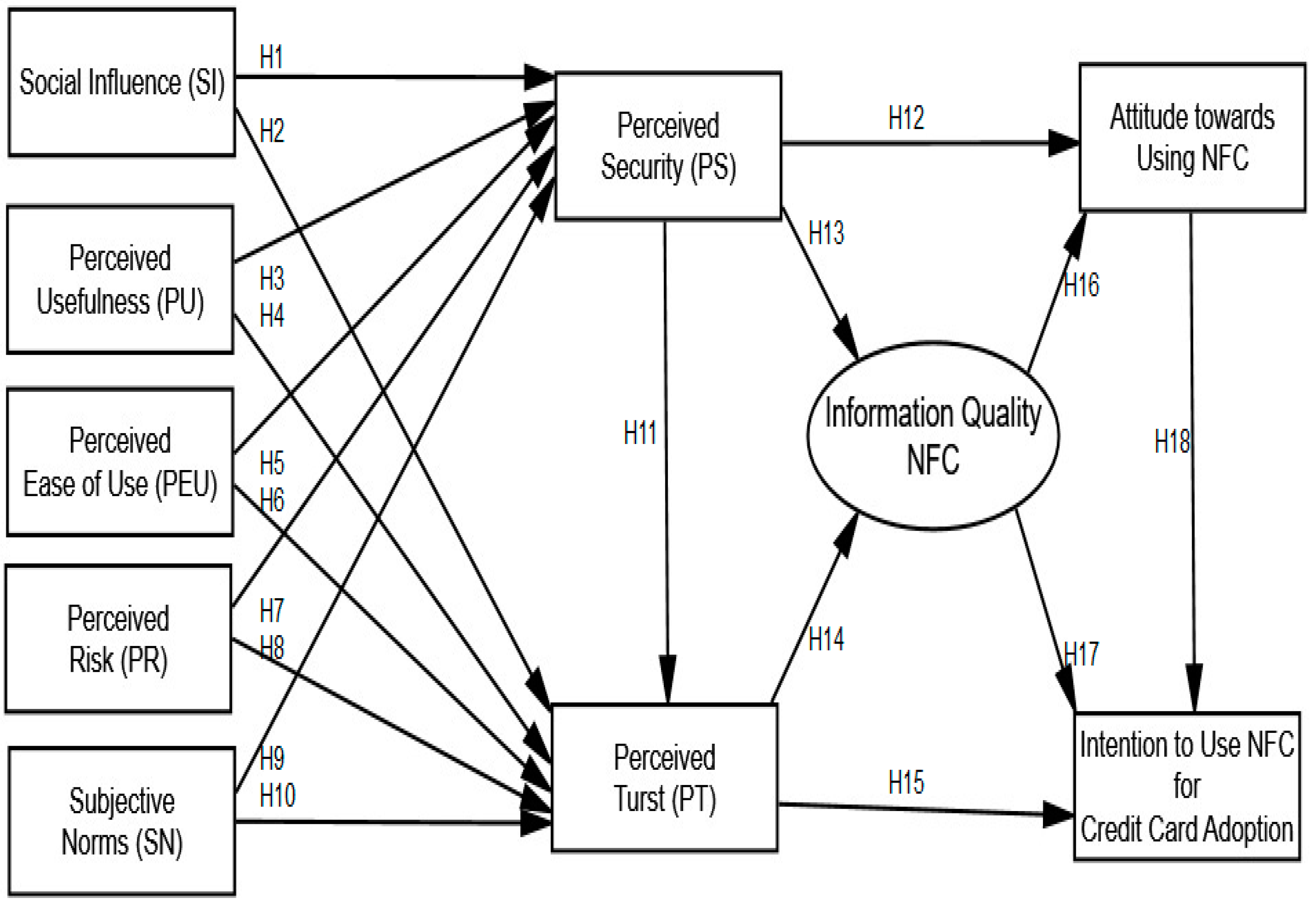

3. Research Model and Hypothesis Development

3.1. Social Influence

3.2. Perceived Usefulness

3.3. Perceived Ease of Use

3.4. Perceived Risk

3.5. Subjective Norms

3.6. Perceived Security

3.7. Perceived Trust

3.8. NFC Information Quality

3.9. Attitudes towards Using NFC

3.10. Consumer Intention to Use NFC for Credit Card

4. Methodology

4.1. Measurement Instrument

4.2. Data Collection and Sample Size

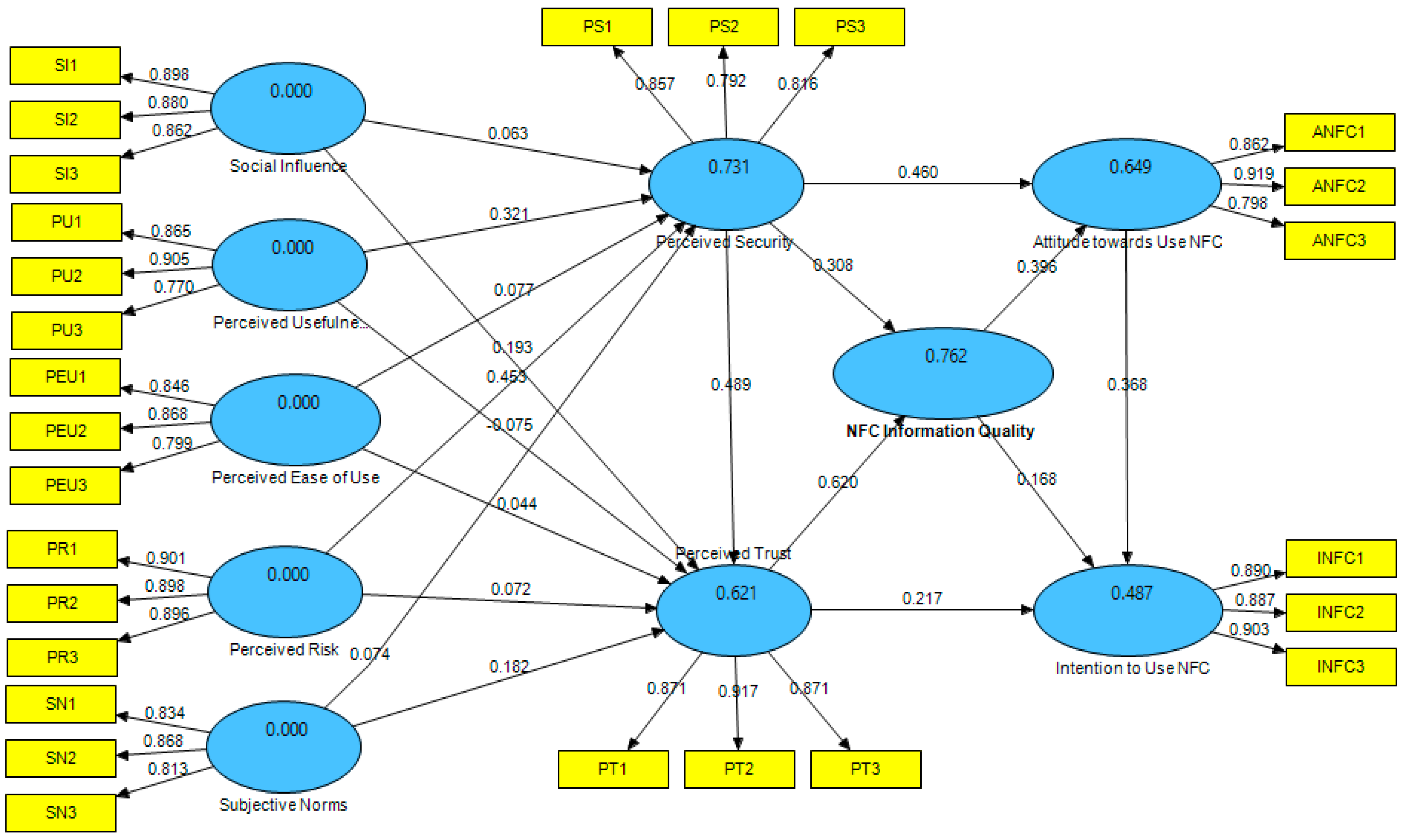

5. Results and Analysis

5.1. Reliability and Validity of Measures

5.2. Measurement Construct Validity

5.3. Measurement Validity of Construct

5.4. Model Measurement Fit

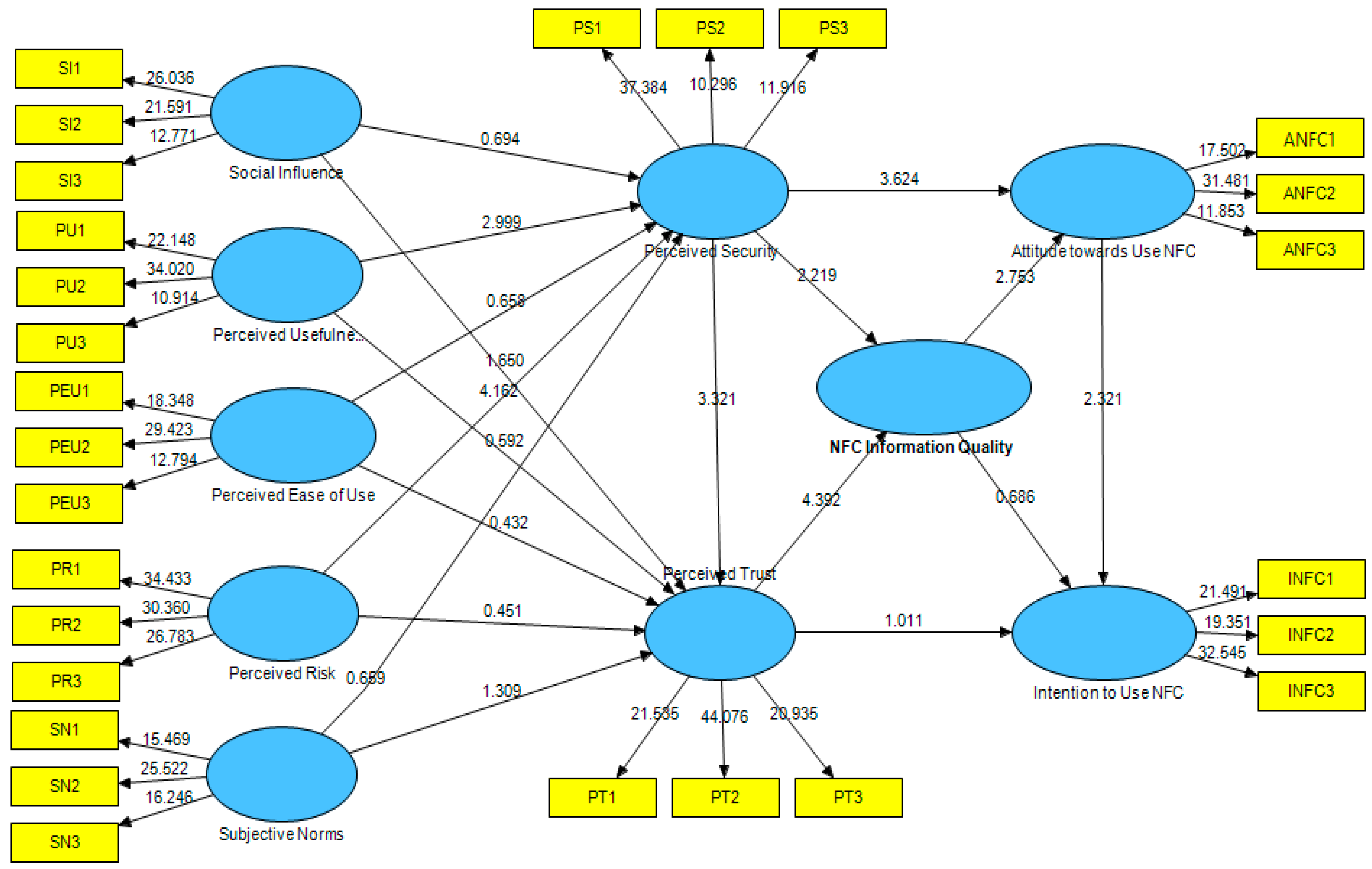

5.5. The Analysis of the Structural Model

6. Discussion and Academic Contribution

Research Contributions and Implications

7. Conclusions and Future Works

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Achsan, W.; Achsani, N.A.; Bandono, B. The Demographic and Behavior Determinant of Credit Card Default in Indonesia. Signifikan J. Ilmu Èkon. 2022, 11, 43–56. [Google Scholar] [CrossRef]

- Almaiah, M.A.; Al-Khasawneh, A.; Althunibat, A. Exploring the critical challenges and factors influencing the E-learning system usage during COVID-19 pandemic. Educ. Inf. Technol. 2020, 25, 5261–5280. [Google Scholar] [CrossRef]

- Afandi, A.; Fadhillah, A.; Sari, D.P. Pengaruh Persepsi Kegunaan, Persepsi Kemudahan dan Persepsi Kepercayaan Terhadap Niat Menggunakan E-Wallet Dengan Sikap Sebagai Variabel Int ervening. Innov. J. Soc. Sci. Res. 2021, 1, 568–577. [Google Scholar]

- Ahmed, W.; Rasool, A.; Javed, A.R.; Kumar, N.; Gadekallu, T.R.; Jalil, Z.; Kryvinska, N. Security in Next Generation Mobile Payment Systems: A Comprehensive Survey. IEEE Access 2021, 9, 115932–115950. [Google Scholar] [CrossRef]

- Bubukayr, M.A.S.; Almaiah, M.A. Cybersecurity concerns in smart-phones and applications: A survey. In Proceedings of the 2021 International Conference on Information Technology (ICIT), Amman, Jordan, 14–15 July 2021; pp. 725–731. [Google Scholar]

- Al Nafea, R.; Almaiah, M.A. Cyber security threats in cloud: Literature review. In Proceedings of the 2021 International Con-ference on Information Technology (ICIT), Amman, Jordan, 14–15 July 2021; pp. 779–786. [Google Scholar]

- Almaiah, M.A.; Alamri, M.M.; Al-Rahmi, W. Applying the UTAUT Model to Explain the Students’ Acceptance of Mobile Learning System in Higher Education. IEEE Access 2019, 7, 174673–174686. [Google Scholar] [CrossRef]

- Ajzen, I. The theory of planned behavior. Organ. Behav. Hum. Decis. Process. 1991, 50, 179–211. [Google Scholar] [CrossRef]

- Alam, M.Z.; Alam MM, D.; Uddin, M.A.; Mohd Noor, N.A. Do mobile health (mHealth) services ensure the quality of health life? An integrated approach from a developing country context. J. Mark. Commun. 2022, 28, 152–182. [Google Scholar] [CrossRef]

- Alamoudi, H. Examining Retailing Sustainability in the QR Code-Enabled Mobile Payments Context During the COVID-19 Pandemic. Int. J. Cust. Relatsh. Mark. Manag. 2022, 13, 1–22. [Google Scholar] [CrossRef]

- Almaiah, M.A.; Alyoussef, I.Y. Analysis of the Effect of Course Design, Course Content Support, Course Assessment and Instructor Characteristics on the Actual Use of E-Learning System. IEEE Access 2019, 7, 171907–171922. [Google Scholar] [CrossRef]

- Ali, A.; Hameed, A.; Moin, M.F.; Khan, N.A. Exploring factors affecting mobile-banking app adoption: A perspective from adaptive structuration theory. Aslib J. Inf. Manag. 2022, 12, 25–37. [Google Scholar] [CrossRef]

- Ali, M.; Amir, H.; Ahmed, M. The role of university switching costs, perceived service quality, perceived university image and student satisfaction in shaping student loyalty. J. Mark. High. Educ. 2021, 27, 1–22. [Google Scholar] [CrossRef]

- Almaiah, M.A.; Jalil, M.A.; Man, M. Extending the TAM to examine the effects of quality features on mobile learning acceptance. J. Comput. Educ. 2016, 3, 453–485. [Google Scholar] [CrossRef]

- Alamri, M.M.; Almaiah, M.A.; Al-Rahmi, W.M. Social media applications affecting Students’ academic performance: A model developed for sustainability in higher education. Sustainability 2020, 12, 6471. [Google Scholar] [CrossRef]

- Almaiah, M.A.; Alismaiel, O.A. Examination of factors influencing the use of mobile learning system: An empirical study. Educ. Inf. Technol. 2019, 24, 885–909. [Google Scholar] [CrossRef]

- Alamer, M.; Almaiah, M.A. Cybersecurity in Smart City: A systematic mapping study. In Proceedings of the 2021 International Conference on Information Technology (ICIT), Amman, Jordan, 14–15 July 2021; pp. 719–724. [Google Scholar]

- Alshurideh, M.T.; Al Kurdi, B.; Masa’Deh, R.; Salloum, S.A. The moderation effect of gender on accepting electronic payment technology: A study on United Arab Emirates consumers. Rev. Int. Bus. Strat. 2021, 31, 375–396. [Google Scholar] [CrossRef]

- Ariansyah, K. Minat masyarakat terhadap layanan Near Field Communication (NFC) komersial di Indonesia. Bul. Pos dan Telekomun. 2015, 10, 125. [Google Scholar] [CrossRef]

- Almaiah, M.A.; Al-Khasawneh, A. Investigating the main determinants of mobile cloud computing adoption in university campus. Educ. Inf. Technol. 2020, 25, 3087–3107. [Google Scholar] [CrossRef]

- Alghazi, S.S.; Kamsin, A.; Almaiah, M.A.; Wong, S.Y.; Shuib, L. For Sustainable Application of Mobile Learning: An Extended UTAUT Model to Examine the Effect of Technical Factors on the Usage of Mobile Devices as a Learning Tool. Sustainability 2021, 13, 1856. [Google Scholar] [CrossRef]

- Almaiah, M.A.; Al Mulhem, A. Analysis of the essential factors affecting of intention to use of mobile learning applications: A comparison between universities adopters and non-adopters. Educ. Inf. Technol. 2018, 24, 1433–1468. [Google Scholar] [CrossRef]

- Alamri, M.M.; Almaiah, M.A.; Al-Rahmi, W.M. The Role of Compatibility and Task-Technology Fit (TTF): On Social Networking Applications (SNAs) Usage as Sustainability in Higher Education. IEEE Access 2020, 8, 161668–161681. [Google Scholar] [CrossRef]

- Alsyouf, A.; Lutfi, A.; Al-Bsheish, M.; Jarrar, M.T.; Al-Mugheed, K.; Almaiah, M.A.; Ashour, A. Exposure Detection Applications Acceptance: The Case of COVID-19. Int. J. Environ. Res. Public Health 2022, 19, 7307. [Google Scholar] [CrossRef] [PubMed]

- Asravor, R.K.; Boakye, A.N.; Essuman, J. Adoption and intensity of use of mobile money among smallholder farmers in rural Ghana. Inf. Dev. 2021, 38, 204–217. [Google Scholar] [CrossRef]

- Baabdullah, A.M.; Alalwan, A.A.; Rana, N.P.; Kizgin, H.; Patil, P. Consumer use of mobile banking (M-Banking) in Saudi Arabia: Towards an integrated model. Int. J. Inf. Manag. 2018, 44, 38–52. [Google Scholar] [CrossRef] [Green Version]

- Almaiah, M.A.; Alfaisal, R.; Salloum, S.A.; Hajjej, F.; Thabit, S.; El-Qirem, F.A.; Lutfi, A.; Alrawad, M.; Al Mulhem, A.; Alkhdour, T.; et al. Examining the Impact of Artificial Intelligence and Social and Computer Anxiety in E-Learning Settings: Students’ Perceptions at the University Level. Electronics 2022, 11, 3662. [Google Scholar] [CrossRef]

- Bagozzi, R.P.; Yi, Y. On the evaluation of structural equation models. J. Acad. Mark. Sci. 1988, 16, 74–94. [Google Scholar] [CrossRef]

- Balakrishnan, V.; Shuib, N.L.M. Drivers and inhibitors for digital payment adoption using the Cashless Society Readiness-Adoption model in Malaysia. Technol. Soc. 2021, 65, 101554. [Google Scholar] [CrossRef]

- Beke, F.T.; Eggers, F.; Verhoef, P.C.; Wieringa, J.E. Consumers’ privacy calculus: The PRICAL index development and validation. Int. J. Res. Mark. 2022, 39, 20–41. [Google Scholar] [CrossRef]

- Belanche, D.; Casaló, L.V.; Flavián, M.; Ibáñez-Sánchez, S. Understanding influencer marketing: The role of con-gruence between influencers, products and consumers. J. Bus. Res. 2021, 132, 186–195. [Google Scholar] [CrossRef]

- Biswas, A.; Jaiswal, D.; Kant, R. Augmenting bank service quality dimensions: Moderation of perceived trust and perceived risk. Int. J. Prod. Perform. Manag. 2021. [Google Scholar] [CrossRef]

- Almaiah, M.A.; Jalil, M.M.A.; Man, M. Empirical investigation to explore factors that achieve high quality of mobile learning system based on students’ perspectives. Eng. Sci. Technol. Int. J. 2016, 19, 1314–1320. [Google Scholar] [CrossRef] [Green Version]

- Lutfi, A.; Saad, M.; Almaiah, M.A.; Alsaad, A.; Al-Khasawneh, A.; Alrawad, M.; Alsyouf, A.; Al-Khasawneh, A.L. Actual Use of Mobile Learning Technologies during Social Distancing Circumstances: Case Study of King Faisal University Students. Sustainability 2022, 14, 7323. [Google Scholar] [CrossRef]

- Almaiah, M.A. Acceptance and usage of a mobile information system services in University of Jordan. Educ. Inf. Technol. 2018, 23, 1873–1895. [Google Scholar] [CrossRef]

- Almaiah, M.A.; Alamri, M.M.; Al-Rahmi, W.M. Analysis the Effect of Different Factors on the Development of Mobile Learning Applications at Different Stages of Usage. IEEE Access 2019, 8, 16139–16154. [Google Scholar] [CrossRef]

- Althunibat, A.; Almaiah, M.A.; Altarawneh, F. Examining the Factors Influencing the Mobile Learning Applications Usage in Higher Education during the COVID-19 Pandemic. Electronics 2021, 10, 2676. [Google Scholar] [CrossRef]

- Mulhem, A.A.; Almaiah, M.A. A conceptual model to investigate the role of mobile game applications in education during the COVID-19 pandemic. Electronics 2021, 10, 2106. [Google Scholar] [CrossRef]

- Lutfi, A.; Alsyouf, A.; Almaiah, M.A.; Alrawad, M.; Abdo, A.A.K.; Al-Khasawneh, A.L.; Ibrahim, N.; Saad, M. Factors Influencing the Adoption of Big Data Analytics in the Digital Transformation Era: Case Study of Jordanian SMEs. Sustainability 2022, 14, 1802. [Google Scholar] [CrossRef]

- Almaiah, M.A.; Nasereddin, Y. Factors influencing the adoption of e-government services among Jordanian citi-zens. Electron. Gov. Int. J. 2020, 16, 236–259. [Google Scholar]

- Bojjagani, S.; Sastry, V.N.; Chen, C.M.; Kumari, S.; Khan, M.K. Systematic survey of mobile payments, protocols, and security infrastructure. J. Ambient. Intell. Humaniz. Comput. 2021, 1–46. [Google Scholar]

- Bulutoding, L.; Bidin CR, K.; Syariati, A.; Qarina, Q. Antecedents and Consequence of Murabaha Funding in Islamic Banks of Indonesia. J. Asian Financ. Econ. Bus. 2021, 8, 487–495. [Google Scholar]

- Caldeira, T.A.; Ferreira, J.B.; Freitas, A.; Falcão, R.P.D.Q. Adoption of Mobile Payments in Brazil: Technology Readiness, Trust and Perceived Quality. Braz. Bus. Rev. 2021, 18, 415–432. [Google Scholar]

- Cao, T. The Study of Factors on the Small and Medium Enterprises’ Adoption of Mobile Payment: Implications for the COVID-19 Era. Front. Public Health 2021, 9, 646592. [Google Scholar] [CrossRef] [PubMed]

- Cao, X.; Yu, L.; Liu, Z.; Gong, M.; Adeel, L. Understanding mobile payment users’ continuance intention: A trust transfer perspective. Internet Res. 2018, 28, 456–476. [Google Scholar] [CrossRef]

- Castro Merino, R.G. Diseño e Implementación de un Sistema de Inventario Usando la Tecnología NFC para la Unidad Educativa Particular Virgen del Cisne en la Ciudad de Machala Mediante una Aplicación con Sistema Operativo IOS. 2021. Available online: http://repositorio.ucsg.edu.ec/handle/3317/17679 (accessed on 25 September 2022).

- Coskun, E.; Ferman, M. Factors Encouraging and Hindering A Wider Acceptance And More Frequent Utilization Of Mobile Payment Systems: An Empirical Study Among Mobile Phone Subscribers In Turkey. J. Manag. Mar-Keting Logist. 2021, 8, 164–183. [Google Scholar] [CrossRef]

- Davis, F.D. Perceived usefulness, perceived ease of use, and user acceptance of information technology. MIS Q. 1989, 17, 319–340. [Google Scholar] [CrossRef] [Green Version]

- Dirsehan, T.; Cankat, E. Role of mobile food-ordering applications in developing restaurants’ brand satisfaction and loyalty in the pandemic period. J. Retail. Consum. Serv. 2021, 62, 102608. [Google Scholar] [CrossRef]

- Dogra, P.; Kaushal, A. The impact of Digital Marketing and Promotional Strategies on attitude and purchase in-tention towards financial products and service: A Case of emerging economy. J. Mark. Commun. 2022, 21, 1–28. [Google Scholar] [CrossRef]

- Dospinescu, O.; Anastasiei, B.; Dospinescu, N. Key Factors Determining the Expected Benefit of Customers When Using Bank Cards: An Analysis on Millennials and Generation Z in Romania. Symmetry 2019, 11, 1449. [Google Scholar] [CrossRef] [Green Version]

- Duggal, E.; Verma, H.V. Offline to online shopping: Shift in volition or escape from violation. J. Indian Bus. Res. 2022; ahead of print. [Google Scholar] [CrossRef]

- El-Chaarani, H.; El-Abiad, Z. The impact of technological innovation on bank performance. El-CHAARANI H. El-Abiad 2018, 25, 15–32. [Google Scholar]

- Fan, L.; Zhang, X.; Rai, L.; Du, Y. Mobile Payment: The Next Frontier of Payment Systems?—An Empirical Study Based on Push-Pull-Mooring Framework. J. Theor. Appl. Electron. Commer. Res. 2021, 16, 179–193. [Google Scholar] [CrossRef]

- Farhadi, M.; Fooladi, M. Performance of Islamic E-Banking: Case of Iran. Iran. J. Account. 2021, 5, 31–39. [Google Scholar] [CrossRef]

- Almaiah, M.A.; Al-Khasawneh, A.; Althunibat, A.; Almomani, O. Exploring the Main Determinants of Mobile Learning Application Usage During Covid-19 Pandemic in Jordanian Universities. In Emerging Technologies during the Era of COVID-19 Pandemic; Springer: Cham, Switzerland, 2021; pp. 275–290. [Google Scholar] [CrossRef]

- Almaiah, M.A.; Al-Zahrani, A.; Almomani, O.; Alhwaitat, A.K. Classification of cyber security threats on mobile devices and applications. In Artificial Intelligence and Blockchain for Future Cybersecurity Applications; Springer: Cham, Switzerland, 2021; pp. 107–123. [Google Scholar]

- Almaiah, M.A.; Hajjej, F.; Shishakly, R.; Lutfi, A.; Amin, A.; Awad, A.B. The Role of Quality Measurements in Enhancing the Usability of Mobile Learning Applications during COVID-19. Electronics 2022, 11, 1951. [Google Scholar] [CrossRef]

- Lutfi, A.; Alrawad, M.; Alsyouf, A.; Almaiah, M.A.; Al-Khasawneh, A.; Al-Khasawneh, A.L.; Alshira’H, A.F.; Alshirah, M.H.; Saad, M.; Ibrahim, N. Drivers and impact of big data analytic adoption in the retail industry: A quantitative investigation applying structural equation modeling. J. Retail. Consum. Serv. 2023, 70, 103129. [Google Scholar] [CrossRef]

- Almaiah, M.A.; Alfaisal, R.; Salloum, S.A.; Al-Otaibi, S.; Al Sawafi, O.S.; Al-Maroof, R.S.; Awad, A.B. Determinants influencing the continuous intention to use digital technologies in Higher Education. Electronics 2022, 11, 2827. [Google Scholar] [CrossRef]

- Althunibat, A.; Binsawad, M.; Almaiah, M.A.; Almomani, O.; Alsaaidah, A.; Al-Rahmi, W.; Seliaman, M.E. Sustainable applications of smart-government services: A model to understand smart-government adoption. Sustainability 2021, 13, 3028. [Google Scholar] [CrossRef]

- Alksasbeh, M.; Abuhelaleh, M.; Almaiah, M.A.; Al-Jaafreh, M.; Abu Karaka, A. Towards a Model of Quality Features for Mobile Social Networks Apps in Learning Environments: An Extended Information System Success Model. Int. J. Interact. Mob. Technol. 2019, 13, 75–93. [Google Scholar] [CrossRef] [Green Version]

- Gbongli, K.; Xu, Y.; Amedjonekou, K.M. Extended Technology Acceptance Model to Predict Mobile-Based Money Acceptance and Sustainability: A Multi-Analytical Structural Equation Modeling and Neural Network Approach. Sustainability 2019, 11, 3639. [Google Scholar] [CrossRef] [Green Version]

- Geebren, A.; Jabbar, A.; Luo, M. Examining the role of consumer satisfaction within mobile eco-systems: Evidence from mobile banking services. Comput. Hum. Behav. 2020, 114, 106584. [Google Scholar] [CrossRef]

- Gerbing, D.W.; Anderson, J.C. Monte Carlo Evaluations of Goodness of Fit Indices for Structural Equation Models. Sociol. Methods Res. 1992, 21, 132–160. [Google Scholar] [CrossRef]

- Gupta, B.B.; Narayan, S. A survey on contactless smart cards and payment system: Technologies, policies, attacks and countermeasures. J. Glob. Inf. Manag. 2020, 28, 135–159. [Google Scholar] [CrossRef]

- Gupta, S.; Dhingra, S. Modeling the key factors influencing the adoption of mobile financial services: An interpretive structural modeling approach. J. Financial Serv. Mark. 2021, 27, 96–110. [Google Scholar] [CrossRef]

- Hair, J.F., Jr.; Howard, M.C.; Nitzl, C. Assessing measurement model quality in PLS-SEM using confirmatory composite analysis. J. Bus. Res. 2020, 109, 101–110. [Google Scholar] [CrossRef]

- Hidayat-Ur-Rehman, I.; Alzahrani, S.; Rehman, M.Z.; Akhter, F. Determining the factors of m-wallets adoption. A twofold SEM-ANN approach. PLoS ONE 2022, 17, e0262954. [Google Scholar] [CrossRef] [PubMed]

- Ho, J.C.; Wu, C.-G.; Lee, C.-S.; Pham, T.-T.T. Factors affecting the behavioral intention to adopt mobile banking: An international comparison. Technol. Soc. 2020, 63, 101360. [Google Scholar] [CrossRef]

- Hoang, V.H.; Nguyen, P.M.; Luu, T.M.N.; Vu, T.M.H. Determinants of Intention to Borrow Consumer Credit in Vietnam: Application and Extension of Technology Acceptance Model. J. Asian Financ. Econ. Bus. 2021, 8, 885–895. [Google Scholar]

- Hossain, M.A. Security perception in the adoption of mobile payment and the moderating effect of gender. PSU Res. Rev. 2019, 31, 10–31. [Google Scholar] [CrossRef]

- Idrees, A.; Lodhi, R.N.; Rabbani, S.; Ahmad, S. Exploring Stimuli Affecting Behavioral Intention and Actual Credit Card Usage: Application of Updated Technology Acceptance Model. KASBIT Bus. J. 2021, 14, 155–175. [Google Scholar]

- Jadil, Y.; Rana, N.P.; Dwivedi, Y.K. A meta-analysis of the UTAUT model in the mobile banking literature: The moderating role of sample size and culture. J. Bus. Res. 2021, 132, 354–372. [Google Scholar] [CrossRef]

- Kamdjoug, J.R.K.; Wamba-Taguimdje, S.-L.; Wamba, S.F.; Kake, I.B. Determining factors and impacts of the intention to adopt mobile banking app in Cameroon: Case of SARA by afriland First Bank. J. Retail. Consum. Serv. 2021, 61, 102509. [Google Scholar] [CrossRef]

- Kar, A.K. What Affects Usage Satisfaction in Mobile Payments? Modelling User Generated Content to Develop the “Digital Service Usage Satisfaction Model”. Inf. Syst. Front. 2020, 23, 1341–1361. [Google Scholar] [CrossRef]

- Kasemsap, K. Investigating the Roles of Mobile Commerce and Mobile Payment in Global Business. In Securing Transactions and Payment Systems for m-Commerce; IGI Global: Hershey, PA, USA, 2016; pp. 1–23. [Google Scholar] [CrossRef]

- Khanra, S.; Dhir, A.; Kaur, P.; Joseph, R.P. Factors influencing the adoption postponement of mobile payment services in the hospitality sector during a pandemic. J. Hosp. Tour. Manag. 2020, 46, 26–39. [Google Scholar] [CrossRef]

- Khedmatgozar, H.R. The impact of perceived risks on internet banking adoption in Iran: A longitudinal survey. Electron. Commer. Res. 2021, 21, 147–167. [Google Scholar] [CrossRef]

- Kimiagari, S.; Baei, F. Promoting e-banking actual usage: Mix of technology acceptance model and technology-organization-environment framework. Enterp. Inf. Syst. 2022, 16, 1894356. [Google Scholar] [CrossRef]

- Kimiagari, S.; Malafe, N.S.A. The role of cognitive and affective responses in the relationship between internal and external stimuli on online impulse buying behavior. J. Retail. Consum. Serv. 2021, 61, 102567. [Google Scholar] [CrossRef]

- Kratschmann, M.; Dütschke, E. Selling the sun: A critical review of the sustainability of solar energy marketing and advertising in Germany. Energy Res. Soc. Sci. 2021, 73, 101919. [Google Scholar] [CrossRef]

- Lathiya, P.; Wang, J. Near-Field Communications (NFC) for Wireless Power Transfer (WPT): An Overview. Wirel. Power Transf. –Recent Dev. Appl. New Perspect. 2021, 23, 101–122. [Google Scholar] [CrossRef]

- Lew, S.; Tan, G.W.-H.; Loh, X.-M.; Hew, J.-J.; Ooi, K.-B. The disruptive mobile wallet in the hospitality industry: An extended mobile technology acceptance model. Technol. Soc. 2020, 63, 101430. [Google Scholar] [CrossRef]

- Liébana-Cabanillas, F.; Molinillo, S.; Japutra, A. Exploring the Determinants of Intention to Use P2P Mobile Payment in Spain. Inf. Syst. Manag. 2020, 38, 165–180. [Google Scholar] [CrossRef]

- Liébana-Cabanillas, F.; Singh, N.; Kalinic, Z.; Carvajal-Trujillo, E. Examining the determinants of continuance intention to use and the moderating effect of the gender and age of users of NFC mobile payments: A multi-analytical approach. Inf. Technol. Manag. 2021, 22, 133–161. [Google Scholar] [CrossRef]

- Luna, I.R.D.; Montoro-Ríos, F.; Liébana-Cabanillas, F.; Luna, J.G.D. NFC technology acceptance for mobile payments: A Brazilian Perspective. Rev. Bras. Gestão Negócios 2017, 19, 82–103. [Google Scholar]

- Malaquias, R.F.; Hwang, Y. Mobile banking use: A comparative study with Brazilian and U.S. participants. Int. J. Inf. Manag. 2018, 44, 132–140. [Google Scholar] [CrossRef]

- Meghisan-Toma, G.M.; Puiu, S.; Florea, N.M.; Meghisan, F.; Doran, D. Generation Z’young adults and M-commerce use in Romania. J. Theor. Appl. Electron. Commer. Res. 2021, 16, 1458–1471. [Google Scholar] [CrossRef]

- Migliore, G.; Wagner, R.; Cechella, F.S.; Liébana-Cabanillas, F. Antecedents to the Adoption of Mobile Payment in China and Italy: An Integration of UTAUT2 and Innovation Resistance Theory. Inf. Syst. Front. 2022, 1–24. [Google Scholar] [CrossRef]

- Thaker, H.M.T.; Thaker, M.A.M.T.; Khaliq, A.; Pitchay, A.A.; Hussain, H.I. Behavioural intention and adoption of internet banking among clients’ of Islamic banks in Malaysia: An analysis using UTAUT2. J. Islam. Mark. 2021, 13, 1171–1197. [Google Scholar] [CrossRef]

- Mombeuil, C.; Uhde, H. Relative convenience, relative advantage, perceived security, perceived privacy, and continuous use intention of China’s WeChat Pay: A mixed-method two-phase design study. J. Retail. Consum. Serv. 2021, 59, 102384. [Google Scholar] [CrossRef]

- Almaiah, M.A.; Ayouni, S.; Hajjej, F.; Lutfi, A.; Almomani, O.; Awad, A.B. Smart Mobile Learning Success Model for Higher Educational Institutions in the Context of the COVID-19 Pandemic. Electronics 2022, 11, 1278. [Google Scholar] [CrossRef]

- Alrawad, M.; Lutfi, A.; Alyatama, S.; Elshaer, I.A.; Almaiah, M.A. Perception of Occupational and Environmental Risks and Hazards among Mineworkers: A Psychometric Paradigm Approach. Int. J. Environ. Res. Public Heal. 2022, 19, 3371. [Google Scholar] [CrossRef] [PubMed]

- Almaiah, M.A.; Alfaisal, R.; Salloum, S.A.; Al-Otaibi, S.; Shishakly, R.; Lutfi, A.; Al-Maroof, R.S. Integrating Teachers’ TPACK Levels and Students’ Learning Motivation, Technology Innovativeness, and Optimism in an IoT Acceptance Model. Electronics 2022, 11, 3197. [Google Scholar] [CrossRef]

- Almaiah, M.A.; Hajjej, F.; Lutfi, A.; Al-Khasawneh, A.; Alkhdour, T.; Almomani, O.; Shehab, R. A Conceptual Framework for Determining Quality Requirements for Mobile Learning Applications Using Delphi Method. Electronics 2022, 11, 788. [Google Scholar] [CrossRef]

- Shawai, Y.G.; Almaiah, M.A. Malay Language Mobile Learning System (MLMLS) using NFC Technology. Int. J. Educ. Manag. Eng. 2018, 8, 1. [Google Scholar] [CrossRef]

- Al Amri, M.; Almaiah, M.A. Sustainability Model for Predicting Smart Education Technology Adoption Based on Student Perspectives. Int. J. Adv. Soft Comput. Its Appl. 2021, 13, 60–77. [Google Scholar]

- Althunibat, A.; Altarawneh, F.; Dawood, R.; Almaiah, M.A. Propose a New Quality Model for M-Learning Ap-plication in Light of COVID-19. Mob. Inf. Syst. 2022, 2022, 3174692. [Google Scholar]

- Almudaires, F.; Almaiah, M. Data an Overview of Cybersecurity Threats on Credit Card Companies and Credit Card Risk Mitigation. In Proceedings of the 2021 International Conference on Information Technology (ICIT), Amman, Jordan, 14–15 July 2021; pp. 732–738. [Google Scholar] [CrossRef]

- Lutfi, A.; Al-Khasawneh, A.L.; Almaiah, M.A.; Alsyouf, A.; Alrawad, M. Business Sustainability of Small and Medium Enterprises during the COVID-19 Pandemic: The Role of AIS Implementation. Sustainability 2022, 14, 5362. [Google Scholar] [CrossRef]

- Khan, M.N.; Rahman, H.U.; Almaiah, M.A.; Khan, M.Z.; Khan, A.; Raza, M.; Al-Zahrani, M.; Almomani, O.; Khan, R. Improving energy efficiency with content-based adaptive and dynamic scheduling in wireless sensor networks. IEEE Access 2020, 8, 176495–176520. [Google Scholar] [CrossRef]

- Akour, I.; Alnazzawi, N.; Alshurideh, M.; Almaiah, M.A.; Al Kurdi, B.; Alfaisal, R.M.; Salloum, S. A Conceptual Model for Investigating the Effect of Privacy Concerns on E-Commerce Adoption: A Study on United Arab Emirates Consumers. Electronics 2022, 11, 3648. [Google Scholar] [CrossRef]

- Almaiah, M.A.; Alhumaid, K.; Aldhuhoori, A.; Alnazzawi, N.; Aburayya, A.; Alfaisal, R.; Salloum, S.A.; Lutfi, A.; Al Mulhem, A.; Alkhdour, T.; et al. Factors Affecting the Adoption of Digital Information Technologies in Higher Education: An Empirical Study. Electronics 2022, 11, 3572. [Google Scholar] [CrossRef]

- Althunibat, A.; Abdallah, M.; Almaiah, M.A.; Alabwaini, N.; Alrawashdeh, T.A. An Acceptance Model of Using Mobile-Government Services (AMGS). Comput. Model. Eng. Sci. 2022, 131, 865–880. [Google Scholar] [CrossRef]

- Almaiah, M.A.; Al-Rahmi, A.M.; Alturise, F.; Alrawad, M.; Alkhalaf, S.; Lutfi, A.; Awad, A.B. Factors influencing the adoption of internet banking: An integration of ISSM and UTAUT with price value and perceived risk. Front. Psychol. 2022. [Google Scholar] [CrossRef]

- Almaiah, M.A.; Alamri, M.M. Proposing a new technical quality requirements for mobile learning applications. J. Theor. Appl. Inf. Technol. 2018, 96, 6955–6968. [Google Scholar]

- Almaiah, M.A.; Al Mulhem, A. Thematic analysis for classifying the main challenges and factors influencing the successful implementation of e-learning system using NVivo. Int. J. Adv. Trends Comput. Sci. Eng. 2020, 9, 142–152. [Google Scholar] [CrossRef]

- Moore, G.C.; Benbasat, I. Development of an Instrument to Measure the Perceptions of Adopting an Information Technology Innovation. Inf. Syst. Res. 1991, 2, 192–222. [Google Scholar] [CrossRef] [Green Version]

- Museli, A.; Navimipour, N.J. A model for examining the factors impacting the near field communication technology adoption in the organizations. Kybernetes 2018, 12, 89–105. [Google Scholar] [CrossRef]

- Nam, T.H.; Quan, V.D.H. Multi-dimensional Analysis of Perceived Risk on Credit Card Adoption. In International Econometric Conference of Vietnam; Springer: Cham, Switzerland, 2018; pp. 606–620. [Google Scholar] [CrossRef]

- Omar, S.; Mohsen, K.; Tsimonis, G.; Oozeerally, A.; Hsu, J.-H. M-commerce: The nexus between mobile shopping service quality and loyalty. J. Retail. Consum. Serv. 2021, 60, 102468. [Google Scholar] [CrossRef]

- Ou, C.X.; Zhang, X.; Angelopoulos, S.; Davison, R.M.; Janse, N. Security breaches and organization response strategy: Exploring consumers’ threat and coping appraisals. Int. J. Inf. Manag. 2022, 65, 102498. [Google Scholar] [CrossRef]

- Pal, A.; Herath, T.; De’, R.; Rao, H.R. Contextual facilitators and barriers influencing the continued use of mobile payment services in a developing country: Insights from adopters in India. Inf. Technol. Dev. 2020, 26, 394–420. [Google Scholar] [CrossRef]

- Palos-Sanchez, P.; Saura, J.R.; Velicia-Martin, F.; Cepeda-Carrion, G. A business model adoption based on tourism innovation: Applying a gratification theory to mobile applications. Eur. Res. Manag. Bus. Econ. 2021, 27, 100149. [Google Scholar] [CrossRef]

- Patil, P.; Tamilmani, K.; Rana, N.P.; Raghavan, V. Understanding consumer adoption of mobile payment in India: Extending Meta-UTAUT model with personal innovativeness, anxiety, trust, and grievance redressal. Int. J. Inf. Manag. 2020, 54, 102144. [Google Scholar] [CrossRef]

- Pelaez, A.; Chen, C.-W.; Chen, Y.X. Effects of Perceived Risk on Intention to Purchase: A Meta-Analysis. J. Comput. Inf. Syst. 2016, 59, 73–84. [Google Scholar] [CrossRef]

- Purwanto, A.; Juliana, J. The effect of supplier performance and transformational supply chain leadership style on supply chain performance in manufacturing companies. Uncertain Supply Chain Manag. 2022, 10, 511–516. [Google Scholar] [CrossRef]

- Purwanto, A.; Asbari, M.; Santoso, T.I.; Paramarta, V.; Sunarsi, D. Social and Management Research Quantitative Analysis for Medium Sample: Comparing of Lisrel, Tetrad, GSCA, Amos, SmartPLS, WarpPLS, and SPSS. J. Ilm. Ilmu Adm. Publik 2020, 10, 518–532. [Google Scholar]

- Qureshi, J.A.; Rehman, S.; Qureshi, M.A. Consumers’ attitude towards usage of debit and credit cards: Evidences from the digital economy of Pakistan. Int. J. Econ. Financ. Issues 2018, 8, 220–228. [Google Scholar]

- Rabaa’i, A.A.; AlMaati, S. Exploring the determinants of users’ continuance intention to use mobile banking ser-vices in Kuwait: Extending the expectation-confirmation model. Asia Pac. J. Inf. Syst. 2021, 31, 141–184. [Google Scholar]

- Ramos-De-Luna, I.; Montoro-Ríos, F.; Liébana-Cabanillas, F. Determinants of the intention to use NFC technology as a payment system: An acceptance model approach. Inf. Syst. e-Business Manag. 2015, 14, 293–314. [Google Scholar] [CrossRef]

- Rodrick, S.S.; Islam, H.; Sarker, S.A.; Tisha, F.F. Prospects and Challenges of using Credit Card Services: A Study on the users in Dhaka City. AIUB J. Bus. Econ. 2021, 18, 161–186. [Google Scholar]

- Sahi, A.M.; Khalid, H.; Abbas, A.F.; Khatib, S.F.A. The Evolving Research of Customer Adoption of Digital Payment: Learning from Content and Statistical Analysis of the Literature. J. Open Innov. Technol. Mark. Complex. 2021, 7, 230. [Google Scholar] [CrossRef]

- Saprikis, V.; Avlogiaris, G.; Katarachia, A. A Comparative Study of Users versus Non-Users’ Behavioral Intention towards M-Banking Apps’ Adoption. Information 2022, 13, 30. [Google Scholar] [CrossRef]

- Shahi, V.; Srivastava, Y.; Sangam, U.; Rai, A.; Saraswat, M. Web-Based Credit Card Allocation System Using Ma-chine Learning. In Process Mining Techniques for Pattern Recognition; CRC Press: Boca Raton, FL, USA, 2022; pp. 47–56. [Google Scholar]

- Shahid, S.; Islam, J.U.; Malik, S.; Hasan, U. Examining consumer experience in using m-banking apps: A study of its antecedents and outcomes. J. Retail. Consum. Serv. 2021, 65, 102870. [Google Scholar] [CrossRef]

- Shin, S.; Lee, W.-J. Factors affecting user acceptance for NFC mobile wallets in the U.S. and Korea. Innov. Manag. Rev. 2021, 18, 417–433. [Google Scholar] [CrossRef]

- Singh, N.; Sinha, N.; Liébana-Cabanillas, F.J. Determining factors in the adoption and recommendation of mobile wallet services in India: Analysis of the effect of innovativeness, stress to use and social influence. Int. J. Inf. Manag. 2020, 50, 191–205. [Google Scholar] [CrossRef]

- Sreelakshmi, C.C.; Prathap, S.K. Continuance adoption of mobile-based payments in Covid-19 context: An integrated framework of health belief model and expectation confirmation model. Int. J. Pervasive Comput. Commun. 2020, 12, 22–35. [Google Scholar]

- Sulaiman, S.N.A.; Almunawar, M.N. The adoption of biometric point-of-sale terminal for payments. J. Sci. Technol. Policy Manag. 2021, 35, 19–35. [Google Scholar] [CrossRef]

- Sun, S.; Law, R.; Schuckert, M.; Hyun, S.S. Impacts of mobile payment-related attributes on consumers’ repurchase intention. Int. J. Tour. Res. 2021, 24, 44–57. [Google Scholar] [CrossRef]

- Taylor, S.; Todd, P.A. Understanding Information Technology Usage: A Test of Competing Models. Inf. Syst. Res. 1995, 6, 144–176. [Google Scholar] [CrossRef]

- Teng, S.; Khong, K.W. Examining actual consumer usage of E-wallet: A case study of big data analytics. Comput. Hum. Behav. 2021, 121, 106778. [Google Scholar] [CrossRef]

- Tew, H.-T.; Tan, G.W.-H.; Loh, X.-M.; Lee, V.-H.; Lim, W.-L.; Ooi, K.-B. Tapping the Next Purchase: Embracing the Wave of Mobile Payment. J. Comput. Inf. Syst. 2021, 62, 527–535. [Google Scholar] [CrossRef]

- Trinh, H.N.; Tran, H.H.; Vuong, D.H.Q. Determinants of consumers’ intention to use credit card: A perspective of multifaceted perceived risk. Asian J. Econ. Bank. 2020, 4, 105–120. [Google Scholar] [CrossRef]

- Trinh, N.H.; Tran, H.H.; Vuong, Q.D.H. Perceived risk and intention to use credit cards: A case study in Vietnam. J. Asian Financ. Econ. Bus. 2021, 8, 949–958. [Google Scholar]

- Usman, H.; Projo, N.W.K.; Chairy, C.; Haque, M.G. The exploration role of Sharia compliance in technology acceptance model for e-banking (case: Islamic bank in Indonesia). J. Islam. Mark. 2021, 13, 1089–1110. [Google Scholar] [CrossRef]

- Venkatesh, V.; Bala, H. Technology Acceptance Model 3 and a Research Agenda on Interventions. Decis. Sci. 2008, 39, 273–315. [Google Scholar] [CrossRef] [Green Version]

- Venkatesh, V.; Morris, M.G.; Davis, G.B.; Davis, F.D. User acceptance of information technology: Toward a uni-fied view. MIS Q. 2003, 15, 425–478. [Google Scholar] [CrossRef] [Green Version]

- Vladimirovich Platov, A.; Kazbekovich Tarchokov, S.; Sobirovna Zikirova, S.; Igorevna Litvinova, O.; Eduardovich Udalov, D. NFC Technology Acceptance Factors in Tourism. In Proceedings of the IV International Scientific and Practical Conference, St. Petersburg, Russia, 18–19 March 2021; pp. 1–7. [Google Scholar]

- Wamba, S.F.; Queiroz, M.M.; Blome, C.; Sivarajah, U. Fostering financial inclusion in a developing country: Predicting user acceptance of mobile wallets in Cameroon. J. Glob. Inf. Manag. 2021, 29, 195–220. [Google Scholar] [CrossRef]

- Wang, E.S.T. Influences of Innovation Attributes on Value Perceptions and Usage Intentions of Mobile Payment. J. Electron. Commer. Res. 2022, 23, 45–58. [Google Scholar]

- Wei, M.F.; Luh, Y.H.; Huang, Y.H.; Chang, Y.C. Young generation’s mobile payment adoption behavior: Analysis based on an extended UTAUT model. J. Theor. Appl. Electron. Commer. Res. 2021, 16, 618–637. [Google Scholar] [CrossRef]

- Widagdo, B.; Roz, K. Hedonic shopping motivation and impulse buying: The effect of website quality on customer satisfaction. J. Asian Financ. Econ. Bus. 2021, 8, 395–405. [Google Scholar]

- Widyanto, H.A.; Kusumawardani, K.A.; Yohanes, H. Safety first: Extending UTAUT to better predict mobile payment adoption by incorporating perceived security, perceived risk and trust. J. Sci. Technol. Policy Manag. 2021, 20, 22–35. [Google Scholar] [CrossRef]

- Wu, R.-Z.; Lee, J.-H.; Tian, X.-F. Determinants of the Intention to Use Cross-Border Mobile Payments in Korea among Chinese Tourists: An Integrated Perspective of UTAUT2 with TTF and ITM. J. Theor. Appl. Electron. Commer. Res. 2021, 16, 1537–1556. [Google Scholar] [CrossRef]

- Yuan, T.; Honglei, Z.; Xiao, X.; Ge, W.; Xianting, C. Measuring perceived risk in sharing economy: A classical test theory and item response theory approach. Int. J. Hosp. Manag. 2021, 96, 102980. [Google Scholar] [CrossRef]

- Yuen, T.W. Factors influencing foreign consumers to adopt mobile payment extensions offered by multinational mobile messaging applications. Int. J. Multinatl. Corp. Strategy 2020, 3, 130–152. [Google Scholar] [CrossRef]

- Zhang, B.; Peng, G.; Xing, F.; Chen, S. Mobile Applications in China’s Smart Cities: State-of-the-Art and Lessons Learned. J. Glob. Inf. Manag. 2021, 29, 1–18. [Google Scholar] [CrossRef]

- Zhang, R.; Zhang, Y.; Xia, J. Impact of mobile payment on physical health: Evidence from the 2017 China household finance survey. Front. Public Health 2022, 10, 15–35. [Google Scholar] [CrossRef]

- Zhao, H.; Anong, S.T.; Zhang, L. Understanding the impact of financial incentives on NFC mobile payment adoption. Int. J. Bank Mark. 2019, 37, 1296–1312. [Google Scholar] [CrossRef]

- Zhao, Y.; Bacao, F. How Does the Pandemic Facilitate Mobile Payment? An Investigation on Users’ Perspective under the COVID-19 Pandemic. Int. J. Environ. Res. Public Health 2021, 18, 1016. [Google Scholar] [CrossRef] [PubMed]

- Zhong, Y.; Oh, S.; Moon, H.C. Service transformation under industry 4.0: Investigating acceptance of facial recognition payment through an extended technology acceptance model. Technol. Soc. 2021, 64, 101515. [Google Scholar] [CrossRef]

- Zhou, Q.; Lim, F.J.; Yu, H.; Xu, G.; Ren, X.; Liu, D.; Wang, X.; Mai, X.; Xu, H. A study on factors affecting service quality and loyalty intention in mobile banking. J. Retail. Consum. Serv. 2020, 60, 102424. [Google Scholar] [CrossRef]

- Zhu, Q.; Lyu, Z.; Long, Y.; Wachenheim, C.J. Adoption of mobile banking in rural China: Impact of information dissemination channel. Socio-Economic Plan. Sci. 2021, 83, 101011. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| No | Factors | Code | Pilot Test | Final Test |

|---|---|---|---|---|

| 1 | Social Influence | SI | 0.704 | 0.856 |

| 2 | Perceived Usefulness | PU | 0.732 | 0.804 |

| 3 | Perceived Ease of Use | PEU | 0.801 | 0.890 |

| 4 | Perceived Risk | PR | 0.711 | 0.881 |

| 5 | Subjective Norms | SN | 0.782 | 0.889 |

| 6 | Perceived Security | PS | 0.716 | 0.865 |

| 7 | Perceived Trust | PT | 0.786 | 0.864 |

| 8 | NFC Information Quality | NFCQ | 0.792 | 0.927 |

| 9 | Attitude towards Using NFC | ANFC | 0.809 | 0.824 |

| 10 | Intention to Use NFC | INFC | 0.708 | 0.874 |

| Characteristics | Number | |

|---|---|---|

| Gender | Male | 588 |

| Female | 629 | |

| Age | 22–25 years old | 216 |

| 26–30 years old | 268 | |

| 31–35 years old | 227 | |

| 36–40 years old | 276 | |

| More than 40 years old | 230 | |

| Monthly Average Income | 3000–5000 Saudi Riyal | 305 |

| 6000–8000 Saudi Riyal | 251 | |

| 9000–12,000 Saudi Riyal | 227 | |

| 13,000–15,000 Saudi Riyal | 220 | |

| More than 16,000 Saudi Riyal | 214 | |

| Factors | Items | Factor Loadings | Composite Reliability | Cronbach’s Alpha | AVE | R-Squared |

|---|---|---|---|---|---|---|

| Attitude towards Using NFC | ANFC1 | 0.862 | 0.895 | 0.824 | 0.741 | 0.649 |

| ANFC2 | 0.919 | |||||

| ANFC3 | 0.798 | |||||

| Social Influence | SI1 | 0.898 | 0.912 | 0.856 | 0.775 | 0.000 |

| SI2 | 0.880 | |||||

| SI3 | 0.862 | |||||

| Intention to Use NFC | INFC1 | 0.890 | 0.922 | 0.874 | 0.798 | 0.487 |

| INFC2 | 0.887 | |||||

| INFC3 | 0.903 | |||||

| Perceived Risk | PR1 | 0.901 | 0.926 | 0.881 | 0.808 | 0.000 |

| PR2 | 0.898 | |||||

| PR3 | 0.896 | |||||

| Perceived Ease of Use | PEU1 | 0.846 | 0.876 | 0.890 | 0.702 | 0.000 |

| PEU2 | 0.868 | |||||

| PEU3 | 0.799 | |||||

| Subjective Norms | SN1 | 0.834 | 0.876 | 0.889 | 0.703 | 0.000 |

| SN2 | 0.868 | |||||

| SN3 | 0.813 | |||||

| Perceived Usefulness | PU1 | 0.865 | 0.885 | 0.804 | 0.720 | 0.000 |

| PU2 | 0.905 | |||||

| PU3 | 0.770 | |||||

| Perceived Security | PS1 | 0.857 | 0.862 | 0.865 | 0.675 | 0.731 |

| PS2 | 0.792 | |||||

| PS3 | 0.816 | |||||

| NFC Information Quality | NFCQ1 | 0.939 | 0.953 | 0.927 | 0.872 | 0.762 |

| NFCQ2 | 0.938 | |||||

| NFCQ3 | 0.924 | |||||

| Perceived Trust | PT1 | 0.871 | 0.917 | 0.864 | 0.786 | 0.621 |

| PT2 | 0.917 | |||||

| PT3 | 0.871 |

| Factors | Items | ANFC | SI | INFC | PR | PEU | SN | PU | PS | NFCQ | PT |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Attitude towards Using NFC | ANFC1 | 0.862 | 0.539 | 0.599 | 0.617 | 0.522 | 0.543 | 0.630 | 0.716 | 0.657 | 0.670 |

| ANFC2 | 0.919 | 0.565 | 0.614 | 0.603 | 0.538 | 0.611 | 0.599 | 0.694 | 0.687 | 0.707 | |

| ANFC3 | 0.798 | 0.544 | 0.477 | 0.507 | 0.372 | 0.437 | 0.366 | 0.549 | 0.586 | 0.572 | |

| Social Influence | SI1 | 0.584 | 0.898 | 0.579 | 0.496 | 0.476 | 0.508 | 0.465 | 0.502 | 0.504 | 0.556 |

| SI2 | 0.613 | 0.880 | 0.557 | 0.516 | 0.426 | 0.509 | 0.429 | 0.535 | 0.570 | 0.539 | |

| SI3 | 0.461 | 0.862 | 0.518 | 0.439 | 0.341 | 0.418 | 0.328 | 0.371 | 0.462 | 0.425 | |

| Intention to Use NFC | INFC1 | 0.592 | 0.537 | 0.890 | 0.657 | 0.566 | 0.602 | 0.624 | 0.584 | 0.528 | 0.576 |

| INFC2 | 0.541 | 0.517 | 0.887 | 0.558 | 0.509 | 0.532 | 0.533 | 0.528 | 0.554 | 0.527 | |

| INFC3 | 0.628 | 0.625 | 0.903 | 0.680 | 0.530 | 0.623 | 0.548 | 0.607 | 0.599 | 0.605 | |

| Perceived Risk | PR1 | 0.631 | 0.532 | 0.668 | 0.901 | 0.532 | 0.604 | 0.625 | 0.764 | 0.650 | 0.609 |

| PR2 | 0.568 | 0.503 | 0.620 | 0.898 | 0.538 | 0.583 | 0.577 | 0.706 | 0.667 | 0.588 | |

| PR3 | 0.612 | 0.452 | 0.623 | 0.896 | 0.518 | 0.556 | 0.573 | 0.665 | 0.587 | 0.582 | |

| Perceived Ease of Use | PEU1 | 0.401 | 0.362 | 0.510 | 0.436 | 0.846 | 0.508 | 0.467 | 0.436 | 0.408 | 0.414 |

| PEU2 | 0.511 | 0.446 | 0.539 | 0.530 | 0.868 | 0.608 | 0.632 | 0.617 | 0.517 | 0.512 | |

| PEU3 | 0.484 | 0.381 | 0.453 | 0.503 | 0.799 | 0.647 | 0.434 | 0.495 | 0.423 | 0.484 | |

| Subjective Norms | SN1 | 0.526 | 0.434 | 0.540 | 0.504 | 0.635 | 0.834 | 0.592 | 0.555 | 0.448 | 0.484 |

| SN2 | 0.560 | 0.518 | 0.622 | 0.569 | 0.599 | 0.868 | 0.571 | 0.570 | 0.548 | 0.594 | |

| SN3 | 0.473 | 0.423 | 0.487 | 0.554 | 0.543 | 0.813 | 0.424 | 0.536 | 0.561 | 0.527 | |

| Perceived Usefulness | PU1 | 0.517 | 0.319 | 0.510 | 0.544 | 0.521 | 0.546 | 0.865 | 0.658 | 0.478 | 0.528 |

| PU2 | 0.595 | 0.485 | 0.611 | 0.580 | 0.577 | 0.617 | 0.905 | 0.669 | 0.505 | 0.506 | |

| PU3 | 0.483 | 0.397 | 0.495 | 0.559 | 0.474 | 0.432 | 0.770 | 0.563 | 0.390 | 0.405 | |

| Perceived Security | PS1 | 0.815 | 0.574 | 0.628 | 0.704 | 0.511 | 0.576 | 0.555 | 0.857 | 0.824 | 0.808 |

| PS2 | 0.508 | 0.417 | 0.482 | 0.609 | 0.492 | 0.565 | 0.668 | 0.792 | 0.464 | 0.449 | |

| PS3 | 0.489 | 0.300 | 0.440 | 0.632 | 0.550 | 0.483 | 0.650 | 0.816 | 0.529 | 0.494 | |

| NFC Information Quality | NFCQ1 | 0.695 | 0.588 | 0.605 | 0.633 | 0.484 | 0.548 | 0.494 | 0.703 | 0.939 | 0.787 |

| NFCQ2 | 0.729 | 0.557 | 0.580 | 0.702 | 0.566 | 0.608 | 0.523 | 0.768 | 0.938 | 0.793 | |

| NFCQ3 | 0.675 | 0.497 | 0.576 | 0.645 | 0.467 | 0.581 | 0.503 | 0.679 | 0.924 | 0.798 | |

| Perceived Trust | PT1 | 0.643 | 0.550 | 0.545 | 0.555 | 0.374 | 0.472 | 0.426 | 0.594 | 0.735 | 0.871 |

| PT2 | 0.695 | 0.470 | 0.611 | 0.564 | 0.527 | 0.569 | 0.503 | 0.643 | 0.792 | 0.917 | |

| PT3 | 0.679 | 0.535 | 0.543 | 0.638 | 0.596 | 0.658 | 0.580 | 0.734 | 0.729 | 0.871 |

| No | Factors | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | Attitude towards Using NFC | 1.000 | |||||||||

| 2 | Intention to Use NFC | 0.659 | 1.000 | ||||||||

| 3 | NFC Information Quality | 0.750 | 0.628 | 1.000 | |||||||

| 4 | Perceived Ease of Use | 0.561 | 0.599 | 0.542 | 1.000 | ||||||

| 5 | Perceived Risk | 0.672 | 0.710 | 0.707 | 0.589 | 1.000 | |||||

| 6 | Perceived Security | 0.764 | 0.643 | 0.768 | 0.626 | 0.794 | 1.000 | ||||

| 7 | Perceived Trust | 0.758 | 0.639 | 0.848 | 0.566 | 0.661 | 0.742 | 1.000 | |||

| 8 | Perceived Usefulness | 0.628 | 0.636 | 0.543 | 0.619 | 0.659 | 0.745 | 0.569 | 1.000 | ||

| 9 | Social Influence | 0.636 | 0.629 | 0.586 | 0.477 | 0.553 | 0.543 | 0.583 | 0.470 | 1.000 | |

| 10 | Subjective Norms | 0.621 | 0.658 | 0.620 | 0.706 | 0.648 | 0.660 | 0.640 | 0.632 | 0.549 | 1.000 |

| No | Hypotheses Links | Path Coefficient | Mean | S.D. | S.E. | T-Value | Results |

|---|---|---|---|---|---|---|---|

| 1 | Social Influence → Perceived Security | 0.063 | 0.071 | 0.091 | 0.091 | 0.694 | Accepted |

| 2 | Social Influence → Perceived Trust | 0.193 | 0.171 | 0.117 | 0.117 | 1.650 | Accepted |

| 3 | Perceived Usefulness → Perceived Security | 0.321 | 0.330 | 0.107 | 0.107 | 2.999 | Accepted |

| 4 | Perceived Usefulness → Perceived Trust | 0.075 | 0.080 | 0.127 | 0.127 | 0.592 | Accepted |

| 5 | Perceived Ease of Use → Perceived Security | 0.077 | 0.098 | 0.117 | 0.117 | 0.658 | Accepted |

| 6 | Perceived Ease of Use → Perceived Trust | 0.044 | 0.051 | 0.101 | 0.101 | 0.432 | Rejected |

| 7 | Perceived Risk → Perceived Security | 0.453 | 0.443 | 0.109 | 0.109 | 4.162 | Accepted |

| 8 | Perceived Risk → Perceived Trust | 0.072 | 0.097 | 0.160 | 0.160 | 0.451 | Accepted |

| 9 | Subjective Norms → Perceived Security | 0.074 | 0.060 | 0.113 | 0.113 | 0.659 | Accepted |

| 10 | Subjective Norms → Perceived Trust | 0.182 | 0.176 | 0.139 | 0.139 | 1.309 | Accepted |

| 11 | Perceived Security → Perceived Trust | 0.489 | 0.489 | 0.147 | 0.147 | 3.321 | Accepted |

| 12 | Perceived Security → NFC Information Quality | 0.308 | 0.295 | 0.139 | 0.139 | 2.219 | Accepted |

| 13 | Perceived Security → Attitude towards Using NFC | 0.460 | 0.478 | 0.127 | 0.127 | 3.624 | Accepted |

| 14 | Perceived Trust → Intention to Use NFC | 0.217 | 0.186 | 0.215 | 0.215 | 1.011 | Accepted |

| 15 | Perceived Trust → NFC Information Quality | 0.620 | 0.634 | 0.141 | 0.141 | 4.392 | Accepted |

| 16 | NFC Information Quality → Attitude towards Using NFC | 0.396 | 0.383 | 0.144 | 0.144 | 2.753 | Accepted |

| 17 | NFC Information Quality → Intention to Use NFC | 0.168 | 0.213 | 0.245 | 0.245 | 0.686 | Accepted |

| 18 | Attitude towards Using NFC → Intention to Use NFC | 0.368 | 0.357 | 0.159 | 0.159 | 2.321 | Accepted |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Almaiah, M.A.; Al-Rahmi, A.; Alturise, F.; Hassan, L.; Lutfi, A.; Alrawad, M.; Alkhalaf, S.; Al-Rahmi, W.M.; Al-sharaieh, S.; Aldhyani, T.H.H. Investigating the Effect of Perceived Security, Perceived Trust, and Information Quality on Mobile Payment Usage through Near-Field Communication (NFC) in Saudi Arabia. Electronics 2022, 11, 3926. https://doi.org/10.3390/electronics11233926

Almaiah MA, Al-Rahmi A, Alturise F, Hassan L, Lutfi A, Alrawad M, Alkhalaf S, Al-Rahmi WM, Al-sharaieh S, Aldhyani THH. Investigating the Effect of Perceived Security, Perceived Trust, and Information Quality on Mobile Payment Usage through Near-Field Communication (NFC) in Saudi Arabia. Electronics. 2022; 11(23):3926. https://doi.org/10.3390/electronics11233926

Chicago/Turabian StyleAlmaiah, Mohammed Amin, Ali Al-Rahmi, Fahad Alturise, Lamia Hassan, Abdalwali Lutfi, Mahmaod Alrawad, Salem Alkhalaf, Waleed Mugahed Al-Rahmi, Saleh Al-sharaieh, and Theyazn H. H. Aldhyani. 2022. "Investigating the Effect of Perceived Security, Perceived Trust, and Information Quality on Mobile Payment Usage through Near-Field Communication (NFC) in Saudi Arabia" Electronics 11, no. 23: 3926. https://doi.org/10.3390/electronics11233926