Assessing the Intention to Adopt Cloud Accounting during COVID-19

,

,  ,

,

,

,  and

and

Abstract

:1. Introduction

2. Theoretical Background

2.1. Traditional Accounting and Cloud Accounting

2.2. Cloud Accounting Adoption

2.3. Technology-Organization-Environment (TOE) Framework

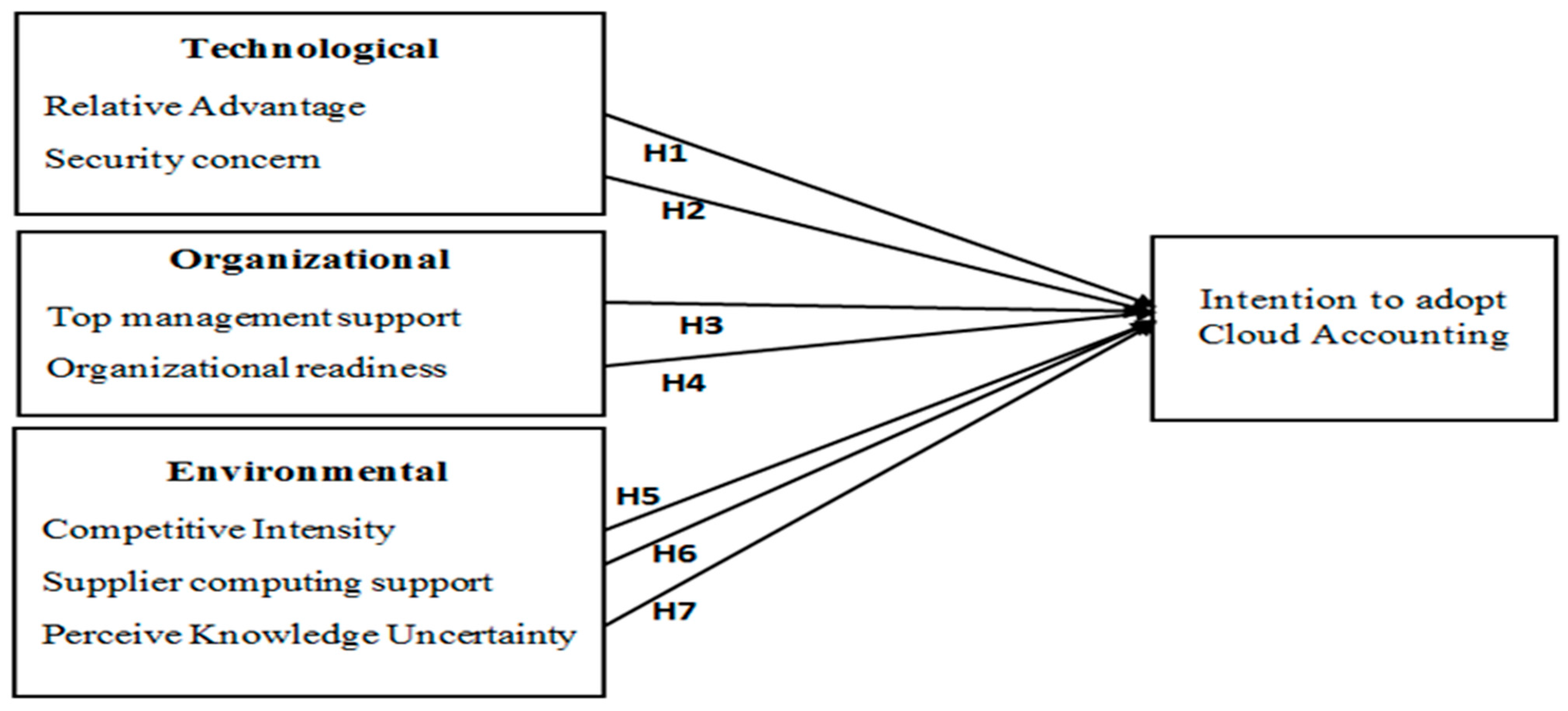

3. Research Model and Hypothesis

3.1. Technological Constructs

3.1.1. Relative Advantage (RA)

3.1.2. Security Concerns (SC)

3.2. Organisational Constructs

3.2.1. Top Management Support (TMS)

3.2.2. Organisational Readiness (OR)

3.3. Environmental Construct

3.3.1. Competition Intensity (CI)

3.3.2. Suppliers Computing Support (SCS)

3.3.3. Perceived Knowledge Uncertainty (PKU)

4. Materials and Methods

4.1. Measurement and Data Collection

4.2. Data Analysis

5. Results and Interpretation

5.1. Measurement Model

5.2. Structural Model

6. Discussion

6.1. Technology Context

6.2. Organisational Context

6.3. Environmental Context

7. Conclusions

7.1. Theoretical Implications

7.2. Practical Implications

7.3. Limitations and Recommendations for Future Studies

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

| Variable | Measurements | Source |

|---|---|---|

| C-ACC adoption | Our business intends to adopt C-ACC. Our business intends to start using C-ACC in regular bases in the future. Our business would highly recommend C-ACC for others to adopt. | [4] |

| Relative advantage | C-ACC enables our business to appropriately manage supply chain risks. C-ACC enables our business to minimize all types of waste throughout the warehousing operations. C-ACC would enable our business to respond faster than competitors would to changing environments. C-ACC would enable our business to minimize total product cost to final customers. C-ACC would enable our business to deliver product precisely on-time delivery to final customers. | [39] |

| Security Concern | The need to outsource BD creates concerns on data security and privacy. The need to outsource BD creates vulnerability in access control of the business’s information asset. The need to outsource BD creates risks through excessive dependency towards vendor. The need to outsource BD complicates the process of implementing corporate policy in protecting individual privacy and data security. | [55,60] |

| Top Management Support | Our top management determines the need for C-ACC solutions. Our top management involve in selection of appropriate hardware and software. Our top management promotes adoption of C-ACC. Our top management involve in planning for developments in C-ACC adoption. | [39] |

| Organizational Readiness | We are financially ready to use C-ACC. We have enough technological resources to use C-ACC. Our employees have adequate knowledge to use C-ACC. Our business values and norms would prevent us from using C-ACC in our operations. We have in-house expertise to use C-ACC. | [8] |

| Competitive Intensity | We feel pressure when competitors have adopted C-ACC. We feel the fear of losing a competitive advantage if they do not adopt C-ACC. We see competitors benefiting from adopting C-ACC. | [72] |

| Knowledge uncertainty | Cloud computing services might not perform well and create problems with our IT operations. Cloud computing services servers may not perform well and may not support our IT operations effectively. We think C-ACC has not reached its maturity. We think C-ACC still requires changes to become more efficient compared with existing technologies. | [72,98] |

| Supplier Computing support | Our cloud Supplier provides adequate technical support. Our cloud supplier is credible and trustworthy. Our cloud supplier has good relations with my organization. Our cloud supplier is experienced and provides quality training and services. Our cloud supplier communicates well with my organization. | [75] |

References

- Alsyouf, A. Self-Efficacy and Personal Innovativeness Influence on Nurses Beliefs about EHRs Usage in Saudi Arabia: Conceptual Model. Int. J. Manag. (IJM) 2021, 12, 1049–1058. [Google Scholar] [CrossRef]

- Khayer, A.; Talukder, M.S.; Bao, Y.; Hossain, M.N. Cloud computing adoption and its impact on SMEs’ performance for cloud supported operations: A dual-stage analytical approach. Technol. Soc. 2020, 60, 101225. [Google Scholar] [CrossRef]

- Lutfi, A.; Al-Khasawneh, A.L.; Almaiah, M.A.; Alsyouf, A.; Alrawad, M. Business Sustainability of Small and Medium Enterprises during the COVID-19 Pandemic: The Role of AIS Implementation. Sustainability 2022, 14, 5362. [Google Scholar] [CrossRef]

- Lutfi, A.; Alsyouf, A.; Almaiah, M.A.; Alrawad, M.; Abdo, A.A.K.; Al-Khasawneh, A.L.; Ibrahim, N.; Saad, M. Factors Influencing the Adoption of Big Data Analytics in the Digital Transformation Era: Case Study of Jordanian SMEs. Sustainability 2022, 14, 1802. [Google Scholar] [CrossRef]

- Usman, U.M.Z.; Ahmad, M.N.; Zakaria, N.H. The Determinants of Adoption of Cloud-Based ERP of Nigerian’s SMES Manufacturing Sector Using Toe Framework and Doi Theory. Int. J. Enterp.-Form. Syst. (IJEIS) 2019, 15, 27–43. [Google Scholar] [CrossRef]

- Asatiani, A.; Apte, U.; Penttinen, E.; Rönkkö, M.; Saarinen, T. Impact of accounting process characteristics on accounting outsourcing-Comparison of users and non-users of cloud-based accounting information systems. Inter-Natl. J. Account. Inf. Syst. 2019, 34, 100419. [Google Scholar] [CrossRef]

- Ma, D.; Fisher, R.; Nesbit, T. Cloud-based client accounting and small and medium accounting practices: Adoption and impact. Int. J. Account. Inf. Syst. 2021, 41, 100513. [Google Scholar] [CrossRef]

- Lutfi, A.; Idris, K.M.; Mohamad, R. The influence of technological, organizational and environmental factors on accounting information system usage among Jordanian small and medium-sized enterprises. Int. J. Econ. Financ. Issues 2016, 6, 240–248. [Google Scholar] [CrossRef]

- Buntin, M.B.; Burke, M.F.; Hoaglin, M.C.; Blumenthal, D. The benefits of health information technology: A review of the recent literature shows predominantly positive results. Health Aff. 2011, 30, 464–471. [Google Scholar] [CrossRef]

- Lutfi, A.; Alshira’h, A.F.; Alshirah, M.H.; Al-Okaily, M.; Alqudah, H.; Saad, M.; Ibrahim, N.; Abdelmaksoud, O. Antecedents and Impacts of Enterprise Resource Planning System Adoption among Jordanian SMEs. Sustainability 2022, 14, 3508. [Google Scholar] [CrossRef]

- Ashraf, M.; Watto, W.A.; Alrawad, M. Do Uncertainty and Financial Development Influence the FDI In-flow of a Developing Nation? A Time Series ARDL Approach. Sustainability 2022, 14, 12609. [Google Scholar]

- Khairi, M.S.; Baridwan, Z. An empirical study on organizational acceptance accounting information systems in Sharia banking. Int. J. Account. Bus. Soc. 2015, 23, 97–122. [Google Scholar]

- Lutfi, A. Understanding Cloud Based Enterprise Resource Planning Adoption among SMEs in Jordan. J. Theor. Appl. Inf. Technol. 2021, 99, 5944–5953. [Google Scholar]

- Alshirah, M.; Alshirah, A.; Saad, M.; Ibrahim, N.; Mohammed, F. Influences of the environmental factors on the intention to adopt cloud based accounting information system among SMEs in Jordan. Accounting 2021, 7, 645–654. [Google Scholar] [CrossRef]

- Le, O.; Cao, Q. Examining the technology acceptance model using cloud-based accounting software of Vietnamese enterprises. Manag. Sci. Lett. 2020, 10, 2781–2788. [Google Scholar] [CrossRef]

- Khassawneh, A. The influence of organizational factors on accounting information systems (AIS) effectiveness: A study of Jordanian SMEs. Int. J. Mark. Technol. 2015, 4, 36–46. [Google Scholar]

- Lutfi, A.; Alkelani, S.N.; Al-Khasawneh, M.A.; Alshira’H, A.F.; Alshirah, M.H.; Almaiah, M.A.; Alrawad, M.; Alsyouf, A.; Saad, M.; Ibrahim, N. Influence of Digital Accounting System Usage on SMEs Performance: The Moderating Effect of COVID-19. Sustainability 2022, 14, 15048. [Google Scholar] [CrossRef]

- Almaiah, M.A.; Hajjej, F.; Al-Khasawneh, A.; Shehab, R.; Al-Otaibi, S.; Alrawad, M. Explaining the Factors Affecting Students’ Attitudes to Using Online Learning (Madrasati Platform) during COVID-19. Electronics 2022, 11, 973. [Google Scholar] [CrossRef]

- Alsyouf, A.; Al-Bsheish, M.; Jarrar, M.; Al-Mugheed, K.; Almaiah, M.A.; Alhazmi, F.N.; Masa’deh, R.; Anshasi, R.J.; Ashour, A. Exposure Detection Applications Acceptance: The Case of COVID-19. Int. J. Environ. Res. Public Health 2022, 19, 7307. [Google Scholar] [CrossRef]

- International Trade Centre. COVID-19: The Great Lockdown and Its Impact on Small Business; International Trade and Investment: Geneva, Switzerland, 2020; Available online: https://intracen.org/media/file/413 (accessed on 24 November 2022).

- Almaiah, M.A.; Alhumaid, K.; Aldhuhoori, A.; Alnazzawi, N.; Aburayya, A.; Alfaisal, R.; Salloum, S.A.; Lutfi, A.; Al Mulhem, A.; Alkhdour, T.; et al. Factors Affecting the Adoption of Digital Information Technologies in Higher Education: An Empirical Study. Electronics 2022, 11, 3572. [Google Scholar] [CrossRef]

- Almaiah, M.A.; Hajjej, F.; Al-Khasawneh, A.; Alkhdour, T.; Almomani, O.; Shehab, R. A Conceptual Framework for Determining Quality Requirements for Mobile Learning Applications Using Delphi Method. Electronics 2022, 11, 788. [Google Scholar] [CrossRef]

- Vardari, L.; Bytyqi, Q.; Lumi, A. The Impact of Information Technologies on Business During the COVID-19 Pandemic Outbreak. In Managing Risk and Decision Making in Times of Economic Distress, Part B (Contemporary Studies in Economic and Financial Analysis); Grima, S., Özen, E., Romānova, I., Eds.; Emerald Publishing Limited: Bingley, UK, 2022; Volume 108B, pp. 143–158. [Google Scholar] [CrossRef]

- Sastararuji, D.; Hoonsopon, D.; Pitchayadol, P.; Chiwamit, P. Cloud accounting adoption in Thai SMEs amid the COVID-19 pandemic: An explanatory case study. J. Innov. Entrep. 2022, 11, 1–25. [Google Scholar] [CrossRef] [PubMed]

- Alshirah, M.H.; Alshira’h, A.F.; Lutfi, A. Political connection, family ownership and corporate risk disclosure: Empirical evidence from Jordan. Meditari Account. Res. 2021; ahead-of-print. [Google Scholar]

- Sutthikun, W.; Thapo, R.; Sahayrak, K. Accounting in the Cloud. Int. J. Integr. Educ. Dev. 2018, 3, 19–27. [Google Scholar]

- Popivniak, Y. Cloud-Based Accounting Software: Choice Options in the Light of Modern International Tendencies. Balt. J. Econ. Stud. 2019, 5, 170–177. [Google Scholar] [CrossRef]

- Berl, A.; Gelenbe, E.; Di Girolamo, M.; Giuliani, G.; De Meer, H.; Dang, M.Q.; Pentikousis, K. Energy-efficient cloud computing. Comput. J. 2010, 53, 1045–1051. [Google Scholar] [CrossRef] [Green Version]

- Rohde, F.H. IS/IT outsourcing practices of small- and medium-sized manufacturers. Int. J. Account. Inf. Syst. 2004, 5, 429–451. [Google Scholar] [CrossRef]

- Sultan, N.A. Reaching for the “Cloud”: How SMEs can manage. Int. J. Inf. Manag. 2011, 31, 272–278. [Google Scholar] [CrossRef]

- Alshirah, M.; Alshirah, A.; Lutfi, A. Audit committee’s attributes, overlapping memberships on the audit committee and corporate risk disclosure: Evidence from Jordan. Accounting 2021, 7, 423–440. [Google Scholar] [CrossRef]

- Aini, Q.; Anoesyirwan, A.; Ana, Y. Effect of Cloud Accounting as income statement on Accountant Performance. Aptisi Trans. Manag. (ATM) 2020, 4, 13–21. [Google Scholar] [CrossRef]

- Effiong, S.A.; Udoayang, J.O.; Davies, S.D. Cloud Accounting Costs and Cost Structure Harmonization in Manufacturing Firms. Test Eng. Manag. J. 2020, 83, 24307–24321. [Google Scholar]

- Hsu, P.F.; Ray, S.; Li-Hsieh, Y.Y. Examining cloud computing adoption intention, pricing mechanism, and deployment model. Int. J. Inf. Manag. 2014, 34, 474–488. [Google Scholar] [CrossRef]

- Almaiah, M.A.; Alfaisal, R.; Salloum, S.A.; Al-Otaibi, S.; Shishakly, R.; Lutfi, A.; Alrawad, M.; Mulhem, A.A.; Awad, A.B.; Al-Maroof, R.S. Integrating Teachers’ TPACK Levels and Students’ Learning Motivation, Technology Innovativeness, and Optimism in an IoT Acceptance Model. Electronics 2022, 11, 3197. [Google Scholar] [CrossRef]

- Almaiah, M.A.; Alfaisal, R.; Salloum, S.A.; Hajjej, F.; Thabit, S.; El-Qirem, F.A.; Lutfi, A.; Alrawad, M.; Al Mulhem, A.; Alkhdour, T.; et al. Examining the Impact of Artificial Intelligence and Social and Computer Anxiety in E-Learning Settings: Students’ Perceptions at the University Level. Electronics 2022, 11, 3662. [Google Scholar] [CrossRef]

- Indriastuti, M.; Fuad, K. Impact of COVID-19 on digital transformation and sustainability in small and medium enterprises (smes): A conceptual framework. In Conference on Complex, Intelligent, and Software Intensive Systems; Springer: Cham, Switzerland, 2020; pp. 471–476. [Google Scholar]

- Papadopoulos, T.; Baltas, K.N.; Balta, M.E. The use of digital technologies by small and medium enterprises during COVID-19: Implications for theory and practice. Int. J. Inf. Manag. 2020, 55, 102192. [Google Scholar] [CrossRef]

- Lutfi, A.; Al-Okaily, M.; Alsyouf, A.; Alsaad, A.; Taamneh, A. The Impact of AIS Usage on AIS Effectiveness among Jordanian SMEs: A Multi Group Analysis of the Role of Firm Size. Glob. Bus. Rev. 2020, 2020, 1–19. [Google Scholar] [CrossRef]

- Lutfi, A.; Al-Khasawneh, A.L.; Almaiah, M.A.; Alshira’h, A.F.; Alshirah, M.H.; Alsyouf, A.; Alrawad, M.; Al-Khasawneh, A.; Saad, M.; Ali, R.A. Antecedents of Big Data Analytic Adoption and Impacts on Performance: Contingent Effect. Sustainability 2022, 14, 15516. [Google Scholar] [CrossRef]

- Low, C.; Chen, Y.; Wu, M. Understanding the determinants of cloud computing adoption. Ind. Manag. Data Syst. 2011, 111, 1006–1023. [Google Scholar] [CrossRef] [Green Version]

- Oliveira, T.; Thomas, M.; Espadanal, M. Assessing the determinants of cloud computing adoption: An analysis of the manufacturing and services sectors. Inf. Manag. 2014, 55, 497–510. [Google Scholar] [CrossRef]

- Ramdani, B.; Kawalek, P.; Lorenzo, O. Predicting SMEs’ adoption of enterprise systems. J. Enterp. Inf. Manag. 2009, 22, 10–24. [Google Scholar] [CrossRef]

- Lutfi, A.A.; Idris, K.M.; Mohamad, R. AIS usage factors and impact among Jordanian SMEs: The moderating effect of environmental uncertainty. J. Adv. Res. Bus. Manag. Stud. 2017, 6, 24–38. [Google Scholar]

- Priyadarshinee, P.; Raut, R.D.; Jha, M.K.; Gardas, B.B. Understanding and predicting the determinants of cloud computing adoption: A two staged hybrid SEM-Neural networks approach. Comput. Hum. Behav. 2017, 76, 341–362. [Google Scholar] [CrossRef]

- Almaiah, M.A.; Ayouni, S.; Hajjej, F.; Almomani, O.; Awad, A.B. Smart Mobile Learning Success Model for Higher Educational Institutions in the Context of the COVID-19 Pandemic. Electronics 2022, 11, 1278. [Google Scholar] [CrossRef]

- Almaiah, M.A.; Al-Rahmi, A.M.; Alturise, F.; Alrawad, M.; Alkhalaf, S.; Lutfi, A.; Al-Rahmi, W.M.; Awad, A.B. Factors influencing the adoption of internet banking: An integration of ISSM and UTAUT with price value and perceived risk. Front. Psychol. 2022, 13, 919198. [Google Scholar] [CrossRef]

- Almaiah, M.A.; Al-Otaibi, S.; Lutfi, A.; Almomani, O.; Awajan, A.; Alsaaidah, A.; Alrawad, M.; Awad, A.B. Employing the TAM Model to Investigate the Readiness of M-Learning System Usage Using SEM Technique. Electronics 2022, 11, 1259. [Google Scholar] [CrossRef]

- Alsyouf, A.; Masa’deh, R.E.; Albugami, M.; Al-Bsheish, M.; Alsubahi, N. Risk of Fear and Anxiety in Utilising Health App Surveillance Due to COVID-19: Gender Differences Analysis. Risks 2021, 9, 179. [Google Scholar] [CrossRef]

- Elkaseh, A.M.; Wong, K.W.; Fung, C.C. Perceived ease of use and perceived usefulness of social media for e-learning in Libyan higher education: A structural equation modeling analysis. Int. J. Inf. Educ. Technol. 2016, 6, 192. [Google Scholar] [CrossRef]

- Siamagka, N.T.; Christodoulides, G.; Michaelidou, N.; Valvi, A. Determinants of social media adoption by B2B organizations. Ind. Mark. Manag. 2015, 51, 89–99. [Google Scholar] [CrossRef] [Green Version]

- Abbas, H.A.; Hamdy, H.I. Determinants of continuance intention factor in Kuwait communication market: Case study of Zain-Kuwait. Comput. Hum. Behav. 2015, 49, 648–657. [Google Scholar] [CrossRef]

- Lutfi, A.; Alrawad, M.; Alsyouf, A.; Almaiah, M.A.; Al-Khasawneh, A.; Al-Khasawneh, A.L.; Alshira’h, A.F.; Alshirah, M.H.; Saad, M.; Ibrahim, N. Drivers and impact of big data analytic adoption in the retail industry: A quantitative investigation applying structural equation modeling. J. Retail. Consum. Serv. 2023, 70, 103129. [Google Scholar] [CrossRef]

- Alrawad, M.; Alyatama, S.; Elshaer, I.A.; Almaiah, M.A. Perception of Occupational and Environmental Risks and Hazards among Mineworkers: A Psychometric Paradigm Approach. Int. J. Environ. Res. Public Health 2022, 19, 3371. [Google Scholar] [CrossRef]

- Maroufkhani, P.; Tseng, M.L.; Iranmanesh, M.; Ismail, W.K.W.; Khalid, H. Big data analytics adoption: Determinants and performances among small to medium-sized enterprises. Int. J. Inf. Manag. 2020, 54, 102190. [Google Scholar] [CrossRef]

- Sahandi, R.; Alkhalil, A.; Opara-Martins, J. SMEs’ perception of cloud computing: Potential and security. In Working Conference on Virtual Enterprises; Springer: Berlin/Heidelberg, Germany, 2012; pp. 186–195. [Google Scholar] [CrossRef]

- Almaiah, M.A.; Al-Rahmi, A.; Alturise, F.; Hassan, L.; Lutfi, A.; Alrawad, M.; Alkhalaf, S.; Al-Rahmi, W.M.; Al-sharaieh, S.; Aldhyani, T.H.H. Investigating the Effect of Perceived Security, Perceived Trust, and Information Quality on Mobile Payment Usage through Near-Field Communication (NFC) in Saudi Arabia. Electronics 2022, 11, 3926. [Google Scholar] [CrossRef]

- Salum, K.H.; Rozan, M.Z.A. Exploring the challenge impacted SMEs to adopt cloud ERP. Indian J. Sci. Technol. 2016, 9, 1–8. [Google Scholar] [CrossRef]

- Almaiah, M.A.; Hajjej, F.; Shishakly, R.; Amin, A.; Awad, A.B. The Role of Quality Measurements in Enhancing the Usability of Mobile Learning Applications during COVID-19. Electronics 2022, 11, 1951. [Google Scholar] [CrossRef]

- Salleh, K.A.; Janczewski, L. Adoption of Big Data Solutions: A study on its security determinants using Sec-TOE Framework. In Proceedings of the CONF-IRM 2016 Conference, Cape Town, South Africa, 18–20 May 2016. [Google Scholar]

- Zhu, H.; Yang, D.; Yu, G.; Zhang, H.; Yao, K. A simple hydrothermal route for synthesizing SnO2 quantum dots. Nanotechnology 2006, 17, 2386. [Google Scholar] [CrossRef]

- Fillis, I.; Johannson, U.; Wagner, B. Factors impacting on e-business adoption and development in the smaller firm. Int. J. Entrep. Behav. Res. 2004, 10, 178–191. [Google Scholar] [CrossRef]

- Alsyouf, A.; Ishak, A.K. Understanding EHRs continuance intention to use from the perspectives of UTAUT: Practice environment moderating effect and top management support as predictor variables. Int. J. Electron. Healthc. 2018, 10, 24–59. [Google Scholar] [CrossRef]

- Alsyouf, A.; Ishak, A.K.; Lutfi, A.; Alhazmi, F.N.; Al-Okaily, M. The Role of Personality and Top Management Support in Continuance Intention to Use Electronic Health Record Systems among Nurses. Int. J. Environ. Res. Public Health 2022, 19, 11125. [Google Scholar] [CrossRef]

- Jeyaraj, A.; Rottman, J.W.; Lacity, M.C. A review of the predictors, linkages, and biases in IT innovation adoption research. J. Inf. Technol. 2006, 21, 1–23. [Google Scholar] [CrossRef]

- Almaiah, M.A.; Alfaisal, R.; Salloum, S.A.; Al-Otaibi, S.; Al Sawafi, O.S.; Al-Maroof, R.S.; Lutfi, A.; Alrawad, M.; Mulhem, A.A.; Awad, A.B. Determinants influencing the continuous intention to use digital technologies in Higher Education. Electronics 2022, 11, 2827. [Google Scholar] [CrossRef]

- Fathian, M.; Akhavan, P.; Hoorali, M. E-readiness assessment of non-profit ICT SMEs in a developing country: The case of Iran. Technovation 2008, 28, 578–590. [Google Scholar] [CrossRef]

- Awa, H.O.; Ukoha, O.; Emecheta, B.C. Using TOE theoretical framework to study the adoption of ERP solution. Cogent Bus. Manag. 2016, 3, 1196571. [Google Scholar] [CrossRef]

- Scupola, A. The adoption of Internet commerce by SMEs in the south of Italy: An environmental, techno-logical and organizational perspective. J. Glob. Inf. Technol. Manag. 2003, 6, 52–71. [Google Scholar] [CrossRef]

- Gutierrez, A.; Boukrami, E.; Lumsden, R. Technological, organisational and environmental factors influencing managers’ decision to adopt cloud computing in the UK. J. Enterp. Inf. Manag. 2015, 28, 788–807. [Google Scholar] [CrossRef]

- Lutfi, A.; Saad, M.; Almaiah, M.A.; Alsaad, A.; Al-Khasawneh, A.; Alrawad, M.; Alsyouf, A.; Al-Khasawneh, A.L. Actual Use of Mobile Learning Technologies during Social Distancing Circumstances: Case Study of King Faisal University Students. Sustainability 2022, 14, 7323. [Google Scholar] [CrossRef]

- Malik, S.; Chadhar, M.; Vatanasakdakul, S.; Chetty, M. Factors affecting the organizational adoption of blockchain technology: Extending the technology–organization–environment (TOE) framework in the Australian con-text. Sustainability 2021, 13, 9404. [Google Scholar] [CrossRef]

- Misra, S.C.; Mondal, A. Identification of a company’s suitability for the adoption of cloud computing and modelling its corresponding Return on Investment. Math. Comput. Model. 2011, 53, 504–521. [Google Scholar] [CrossRef]

- Alshira’h, A.; Alsqour, M.A.; Alsyouf, A.; Alshirah, M. A Socio-Economic Model of Sales Tax Compliance. Economies 2020, 8, 88. [Google Scholar] [CrossRef]

- Gangwar, H. Cloud computing usage and its effect on organizational performance. Hum. Syst. Manag. 2017, 36, 13–26. [Google Scholar] [CrossRef]

- Iacovou, C.L.; Benbasat, I.; Dexter, A.S. Electronic data interchange and small organizations: Adoption and impact of technology. MIS Q. 1995, 19, 465–485. [Google Scholar] [CrossRef] [Green Version]

- Maqueira-Marín, J.M.; Bruque-Cámara, S.; Minguela-Rata, B. Environment determinants in business adoption of Cloud Computing. Ind. Manag. Data Syst. 2017, 117, 228–246. [Google Scholar] [CrossRef]

- Simatupang, T.M.; Sridharan, R. The collaboration index: A measure for supply chain collaboration. Int. J. Phys. Distrib. Logist. Manag. 2005, 35, 44–62. [Google Scholar] [CrossRef]

- Frambach, R.T.; Barkema, H.G.; Nooteboom, B.; Wedel, M. Adoption of a service innovation in the business market: An empirical test of supply-side variables. J. Bus. Res. 1998, 41, 161–174. [Google Scholar] [CrossRef]

- Woodside, A.G.; Biemans, W. Managing relationships, networks, and complexity in innovation, diffusion, and adoption processes. J. Bus. Ind. Mark. 2005, 20, 335–338. [Google Scholar] [CrossRef]

- Alshamaila, Y.; Papagiannidis, S.; Li, F. Cloud computing adoption by SMEs in the northeast of England: A multi-perspective framework. J. Enterp. Inf. Manag. 2013, 26, 250–275. [Google Scholar] [CrossRef]

- Lutfi, A. Investigating the moderating effect of Environment Uncertainty on the relationship between institutional factors and ERP adoption among Jordanian SMEs. J. Open Innov. Technol. Mark. Complex. 2020, 6, 91. [Google Scholar] [CrossRef]

- Brislin, R.W. Back-translation for cross-cultural research. J. Cross-Cult. Psychol. 1970, 1, 185–216. [Google Scholar] [CrossRef]

- Alshira’h, A.F.; Al-Shatnawi, H.M.; Al-Okaily, M.; Alshirah, M.H. Do public governance and patriotism matter? Sales tax compliance among small and medium enterprises in developing countries: Jordanian evidence. EuroMed J. Bus. 2020, 16, 431–455. [Google Scholar] [CrossRef]

- Alyatama, S.; Al Khattab, A.; Sliman, S.; Almaiah, M.R.; Arfa, H.; Ahmed, N.; Alsyouf, A.; Al-Khasawneh, A.L. Assessing customers perception of online shopping risks: A structural equation modeling-based multi-group analysis. J. Retail. Consum. Serv. 2023, 71, 103188. [Google Scholar] [CrossRef]

- Alshira’h, A.F. The Effect of Peer Influence on Sales Tax Compliance among Jordanian SMEs. Int. J. Acad. Res. Bus. Soc. Sci. 2019, 9, 710–721. [Google Scholar] [CrossRef] [Green Version]

- Hair, J.F., Jr.; Hult, G.T.M.; Ringle, C.M.; Sarstedt, M. A Primer on Partial Least Squares Structural Equation Modeling (PLS-SEM); Sage Publications: New York, NY, USA, 2021. [Google Scholar]

- Reinartz, W.; Haenlein, M.; Henseler, J. An empirical comparison of the efficacy of covariance-based and variance-based SEM. Int. J. Res. Mark. 2009, 26, 332–344. [Google Scholar] [CrossRef] [Green Version]

- Fornell, C.; Larcker, D.F. Evaluating structural equation models with unobservable variables and measurement error. J. Mark. Res. 1981, 18, 39–50. [Google Scholar] [CrossRef]

- Henseler, J.; Ringle, C.M.; Sarstedt, M. A new criterion for assessing discriminant validity in variance-based structural equation modeling. J. Acad. Mark. Sci. 2015, 43, 115–135. [Google Scholar] [CrossRef] [Green Version]

- Alkhater, N.; Walters, R.; Wills, G. An empirical study of factors influencing cloud adoption among private sector organisations. Telemat. Inform. 2018, 35, 38–54. [Google Scholar] [CrossRef]

- Makena, J.N. Factors that affect cloud computing adoption by small and medium enterprises in Kenya. Int. J. Comput. Appl. Technol. Res. 2013, 2, 517–521. [Google Scholar] [CrossRef]

- Lutfi, A. Factors Influencing the Intention to Adopt Cloud Based Accounting Information System in Jordanian SMEs. Int. J. Digit. Account. Res. 2022, 22, 47–70. [Google Scholar] [CrossRef]

- Ahani, A.; Rahim, N.Z.A.; Nilashi, M. Forecasting social CRM adoption in SMEs: A combined SEM-neural network method. Comput. Hum. Behav. 2017, 75, 560–578. [Google Scholar] [CrossRef]

- Lutfi, A. Factors Influencing the Continuance Intention to Use Accounting Information System in Jordanian SMEs from the Perspectives of UTAUT: Top Management Support and Self-Efficacy as Predictor Factors. Economies 2022, 10, 75. [Google Scholar] [CrossRef]

- Lutfi, A.; Al-Okaily, M.; Alsyouf, A.; Alrawad, M. Evaluating the D&M IS Success Model in the Context of Ac-counting Information System and Sustainable Decision Making. Sustainability 2022, 14, 7323. [Google Scholar] [CrossRef]

- Almaiah, M.A.; Alfaisal, R.; Salloum, S.A.; Hajjej, F.; Shishakly, R.; Lutfi, A.; Alrawad, M.; Al Mulhem, A.; Alkhdour, T.; Al-Maroof, R.S. Measuring Institutions’ Adoption of Artificial Intelligence Applications in Online Learning Environments: Integrating the Innovation Diffusion Theory with Technology Adoption Rate. Electronics 2022, 11, 3291. [Google Scholar] [CrossRef]

- Alshamaila, Y.Y. An Empirical Investigation of Factors Affecting Cloud Computing Adoption among SMEs in the North East of England. Ph.D. Thesis, Newcastle University, Newcastle upon Tyne, UK, 2013. [Google Scholar]

| Traditional Accounting | Cloud Accounting | |

|---|---|---|

| Number of users | limited License | Unlimited |

| Technical support | Provided by a third party | Provided by a third party |

| System location | Chosen by the company | In the cloud |

| Information Technology resources | Provided by the business itself or outsourced | No necessary |

| Maintenance costs | Separated | Included |

| Hardware | Provided by the business itself | Included |

| Accounting software license | Business own it | Business is the renter (tenant) |

| System operating | Manage by business | Manage by vendors |

| Characteristic | Frequency | Percent | |

|---|---|---|---|

| Position | CEOs | 78 | 50.0% |

| Senior managers | 41 | 26.3% | |

| Managers | 37 | 24.7% | |

| Experience | 3 years or less | 41 | 26.3% |

| 4–7 years | 32 | 20.5% | |

| 8–11 years | 44 | 28.2% | |

| More than 11 | 39 | 25.0% | |

| Gender | Male | 94 | 60.3% |

| Female | 62 | 39.7% | |

| Age | 20–29 years | 33 | 21.2% |

| 30–39 years | 39 | 25.0% | |

| 40–49 years | 59 | 37.8% | |

| 50 years and above | 25 | 16.0% | |

| Education | Diploma or below | 18 | 11.5% |

| Bachelor degree | 75 | 48.1% | |

| Master’s degree | 51 | 32.7% | |

| PhD | 12 | 7.7% |

| Latent Construct | Cronbach Alpha | CR | AVE |

|---|---|---|---|

| >0.700 | >0.700 | >0.500 | |

| IA C-ACC | 0.864 | 0.917 | 0.787 |

| RA | 0.842 | 0.893 | 0.678 |

| SC | 0.827 | 0.885 | 0.657 |

| TMS | 0.817 | 0.891 | 0.731 |

| OR | 0.859 | 0.904 | 0.703 |

| CI | 0.849 | 0.899 | 0.688 |

| SCS | 0.758 | 0.860 | 0.673 |

| PKU | 0.792 | 0.878 | 0.709 |

| IA C-ACC | OR | TMS | SC | PU | CP | SCS | PKU | |

|---|---|---|---|---|---|---|---|---|

| IA C-ACC | 0.888 | |||||||

| OR | 0.751 | 0.839 | ||||||

| TMS | 0.623 | 0.651 | 0.773 | |||||

| SC | 0.535 | 0.710 | 0.523 | 0.810 | ||||

| PU | 0.692 | 0.677 | 0.549 | 0.649 | 0.824 | |||

| CP | 0.441 | 0.528 | 0.481 | 0.545 | 0.445 | 0.824 | ||

| SCS | 0.661 | 0.577 | 0.492 | 0.476 | 0.601 | 0.350 | 0.888 | |

| PKU | 0.286 | 0.377 | 0.265 | 0.413 | 0.479 | 0.162 | 0.272 | 0.632 |

| Hypothesis No. | Paths | β | S. E | T-Values | p-Values | Decision |

|---|---|---|---|---|---|---|

| H1 | RA–IA C-ACC | 0.164 | 0.042 | 3.839 ** | 0.000 | Accepted |

| H2 | SC–IA C-ACC | −0.163 | 0.043 | 3.748 ** | 0.000 | Accepted |

| H3 | TMS–IA C-ACC | 0.155 | 0.040 | 3.878 ** | 0.000 | Accepted |

| H4 | OR–IA C-ACC | 0.262 | 0.051 | 5.077 ** | 0.000 | Accepted |

| H5 | CI–IA C-ACC | 0.279 | 0.054 | 5.110 ** | 0.000 | Accepted |

| H6 | SCS–IA C-ACC | 0.091 | 0.040 | 2.282 * | 0.025 | Accepted |

| H7 | PKU–IA C-ACC | 0.170 | 0.052 | 3.286 ** | 0.000 | Rejected |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Saad, M.; Lutfi, A.; Almaiah, M.A.; Alshira’h, A.F.; Alshirah, M.H.; Alqudah, H.; Alkhassawneh, A.L.; Alsyouf, A.; Alrawad, M.; Abdelmaksoud, O. Assessing the Intention to Adopt Cloud Accounting during COVID-19. Electronics 2022, 11, 4092. https://doi.org/10.3390/electronics11244092

Saad M, Lutfi A, Almaiah MA, Alshira’h AF, Alshirah MH, Alqudah H, Alkhassawneh AL, Alsyouf A, Alrawad M, Abdelmaksoud O. Assessing the Intention to Adopt Cloud Accounting during COVID-19. Electronics. 2022; 11(24):4092. https://doi.org/10.3390/electronics11244092

Chicago/Turabian StyleSaad, Mohamed, Abdalwali Lutfi, Mohammed Amin Almaiah, Ahmad Farhan Alshira’h, Malek Hamed Alshirah, Hamza Alqudah, Akif Lutfi Alkhassawneh, Adi Alsyouf, Mahmaod Alrawad, and Osama Abdelmaksoud. 2022. "Assessing the Intention to Adopt Cloud Accounting during COVID-19" Electronics 11, no. 24: 4092. https://doi.org/10.3390/electronics11244092