1. Introduction

One of the largest energy consumers, resulting in substantial greenhouse gas (GHG) emissions, is the construction industry [

1,

2]. Statistics from the International Energy Agency (IEA) indicate that, in 2020, the construction sector accounts for 36% of the worldwide terminal energy consumption, which is also responsible for 37% of energy-related carbon emissions. China’s construction sector is the second largest in the world in terms of energy consumption, accounting for 46.7% of China’s total energy consumption [

3]. China’s construction industry has an energy conservation potential of up to 74%, which will generate over 50% of the energy conservation required to accomplish the projected peak carbon emission by 2030 [

4]. Therefore, China’s ability to meet its commitment under the Paris Agreement to reach its peak GHG emissions by 2030 directly depends on reducing the use of fossil fuels and improving energy efficiency in the construction industry. With increasing pressure to address critical energy and environmental issues, the development of low-carbon construction while maintaining steady economic growth is a substantial challenge for China’s construction industry. To reduce carbon emissions from the construction industry, it is crucial to find effective emission reduction strategies and optimize the energy structure through carbon policy.

Most people agree that carbon tax is an effective price-based policy mechanism for addressing the issues with carbon emissions [

5,

6,

7]. The fundamental justification is that the financial incentives provided by carbon tax can successfully motivate participants, which has a significant impact on emission reduction. Currently, more than 20 countries have implemented carbon tax policy, including the United Kingdom, France, the United States, etc. [

8,

9]. Their experience shows that carbon tax has decisive advantages in reducing carbon emissions.

Whether the carbon tax policy is a “booster” or “hindrance” to economic and social development, and whether it helps to alleviate the pressure to reduce emissions, has been the focus of intense political and academic debate in China [

10,

11]. However, a carbon tax on industries that consume different types and amounts of energy will have varying degrees of impact [

12]. Specific issues need to be addressed and analyzed on a case-by-case basis. Therefore, for the industry to promote sustainable growth, it is crucial to explore how the carbon tax affects economic and environmental variables, and to implement it as effectively as possible. The construction industry, as a national economic pillar industry in China, is facing serious pressure to mitigate emissions and economic pressure under the circumstance of peak carbon emissions [

13,

14]. This paper focuses on exploring emissions reduction policies for the construction industry, and studies the impact of carbon tax on the economy and environment at the industry level.

Nevertheless, carbon tax has, at least for the short-term, led to an increase in related energy prices, thus affecting enterprises’ investment and households’ consumption to the detriment of economic growth and social welfare [

15,

16]. To achieve a balance between economic growth and climate change mitigation via optimizing carbon tax policy, many scholars have suggested environmental tax reforms and analyzed double dividends by recycling tax revenues to taxpayers [

17,

18]. As a kind of price-based environmental regulation policy, carbon tax policy will enable enterprises to internalize their external costs and promote innovative technologies to improve energy efficiency [

19,

20,

21]. Energy efficiency improvement is considered an efficient way to mitigate potential negative consequences arising from the carbon tax [

22,

23,

24]. Some scholars have found that, when a new technology improves energy efficiency, it stimulates consumers and producers to use more energy, and the structure may even lead to more energy consumption [

25]. Focusing on carbon tax and improved energy efficiency simultaneously, whether the double dividend effect of the construction industry can be realized is an important point for the construction industry to propose green economy policies.

This study is focused on assessing the impact of carbon tax and improving energy efficiency in the construction industry and verifying whether it achieves a double dividend based on the environmental, economic, and welfare indicators derived from the analysis, and then to propose suggestions for improvement. At present, many studies have neglected to take into account the unique traits of different industries, resulting in a uniform carbon tax for multiple industries and failing to find an industry-specific carbon tax policy [

26].

Therefore, we apply the CGE model to compile the social accounting matrix (SAM) table based on the 2017 input–output table to evaluate the impact of carbon tax implementation in China’s construction industry. In addition, this paper investigates the “double dividend” hypothesis from an industry perspective by designing three carbon tax recycling schemes. Considering the characteristics of energy consumption in the construction industry, this study also simulates scenarios for improving energy efficiency and suggests reasonable energy-saving measures for industrial upgrading, thus contributing to specifically targeted low-carbon development plans and progress directions. This study contributes to the existing literature in three ways. Firstly, from an industry perspective, this paper integrates economic indicators to the CGE model such as gross domestic product (GDP), energy consumption, and government transfer payments to residents. In addition, a carbon tax block is included to investigate how it might affect other factors like output and emission. Secondly, we consider the idea of imposing carbon tax while recycling tax revenues to the government, households, and sectoral investment to achieve a “double dividend”. Finally, the combination of energy efficiency improvement and carbon tax policy is analyzed to simulate the variation of carbon emissions, economic growth, and social welfare in the context of various energy efficiency scenarios, investigating how well this relationship works.

The paper is structured as follows: After the introduction in

Section 1,

Section 2 analyzed previous research about the effects of carbon tax. In

Section 3, the paper provides the methodological specifications, the data sources employed and scenario design. The simulation results and discussion under these scenarios are presented in

Section 4, while conclusions and recommendations for policymakers are summarized in

Section 5. All the equations of the CGE model are introduced in

Appendix A.

2. Literature Review

A carbon tax, imposed based on the carbon content or carbon emissions in fossil fuels [

27], aims to alleviate global warming by reducing GHG emissions. With a carbon tax, it is easier to implement a tax-based pricing mechanism than total volume control and trading. The carbon tax concept was first studied in the late 1980s [

28], and its taxation mechanism was frequently used in subsequent research [

29,

30,

31]. Later theoretical assessments aimed to further improve the carbon tax using economic tools and applied it to a variety of countries, e.g., Denmark and Finland [

32,

33]. The study of carbon tax effects has become a popular topic in the field of energy economics.

The most frequently accepted argument for the carbon tax effect is that an increase in enterprise cost following the implementation causes a drop in energy demand and reduction in carbon emissions. For another, a carbon tax would depress consumer demand and result in a loss of economic growth [

34,

35,

36]. Therefore, some scholars have attempted to test the double dividend hypothesis of the carbon tax, i.e., the potential for environmental and economic benefits by implementing a carbon tax policy and then reusing other existing taxes or tax allocations to mitigate negative effects [

37,

38]. However, there is still substantial disagreement among economists about the possibility of a double dividend, which deserves further study [

39,

40]. Furthermore, energy efficiency, a key factor in production, is an effective measure that can be utilized to mitigate the negative consequences of a carbon tax [

17,

41,

42]. The price factor of a carbon tax will encourage enterprises to advance technology and enhance energy efficiency in order to reduce final energy use [

43]. In recent years, scholars have primarily focused on the implementation of a carbon tax rather than on those combining tax with other policies [

44,

45]. Hence, this paper focuses on the combination of carbon tax collection, recycling, and energy efficiency improvement in China’s construction industry.

The impacts of carbon tax implementation have been studied in various other countries. According to a study by Wesseh and Lin [

46], if Liberia enacts a carbon tax policy that reduces carbon emissions in the range of 20–50%, it will reap economic benefits in terms of energy, employment, and welfare. Carroll and Stevens [

47] estimated the impact of a carbon tax on the U.S. power sector, which indicates that a USD 10 carbon tax would observably reduce carbon emissions and produce a net revenue of

$10.647 to

$118.33 billion. In China, extant studies on carbon tax rarely distinguish between different industries. Some researchers have applied carbon taxes only at the national level, ignoring the fact that different industries each have their own industrial characteristics [

38,

48]. Therefore, this paper, from the perspective of China’s construction industry, aims to enrich the studies measuring the impact of carbon tax.

The installation of a carbon tax in the construction industry will lead to a series of impacts. In general, the classical methods of measuring policy effects are to assume that carbon tax is implied and to compare actual and expected energy savings, ignoring the responses of residents and enterprises [

49,

50]. In contrast, the CGE models provide an efficient policy analysis tool for estimating the effects of a carbon tax via a system of joint cubic equations derived from the behavior of all participants in maximizing their own gains [

51,

52]. Furthermore, the model examines the variations in market supply, demand, prices, and amounts for commodities in the entire economic system, as well as their relationship to changes in exogenous variables. The model allows researchers to investigate the macroeconomic impact of the economic system’s transition from one equilibrium condition to another. Frequently, the CGE model is used in energy forecasts and policy assessment [

53,

54]. For instance, Sabine et al. [

55] estimated the environmental and economic changes of carbon tax on Reunion Island. Moreover, the CGE model is widely used for carbon tax assessment, not only to determine the overall economic cost, but also for more in-depth sectoral analyses.

Existing studies have focused on respective studies on the impact of carbon tax and energy efficiency improvement on emissions reduction, while a few studies have combined carbon tax policy with energy efficiency improvement. Furthermore, it is challenging to identify how carbon tax affects different industries since many analyses ignore the construction industry’s heterogeneity and apply the same tax rate to all industries. To measure the carbon tax impact on China’s construction industry, the SAM table is used to obtain the database and the parameters designed in the model. Then, a set of equations for maximizing the benefits of all participants is established through the CGE model. Proposing the carbon tax for China’s construction industry through the tax implementation, rebate, and energy effects to improve living standards and energy efficiency while achieving energy conservation and emission reduction.

4. Results and Discussion

4.1. The Impact of Carbon Tax on the Construction Industry

As shown in

Figure 3, carbon emissions, output, and energy demand of the construction industry show a significant downward trend due to the implementation of the carbon tax. With the carbon tax rate gradually increasing from 20 to 100 RMB/t-CO

2, the reduction of carbon emissions, output, and energy demand in the construction industry increased from 1.75%, 0.396%, and 1.855% to 7.002%, 1.854%, and 8.254%. Carbon emissions and energy demand dropped the most, since coal and oil are both crucial to the inputs of construction industry, accounting for a high percentage of total energy consumption structure. A carbon tax is based on the carbon content of fossil fuels. The imposition of carbon tax on the construction industry would increase the energy’s cost and price, driving enterprises to use less high-carbon and expensive energy, leading to a significant reduction of fossil energy demand and carbon emissions.

It was discovered through a comparison of various tax rate conditions that the impact of output loss increased with the carbon tax rate. There is a minor difference in the decline of construction output, when the carbon tax rate is 20–40 RMB/t-CO2. The total output, however, drops sharply when the tax rate is between 60 RMB/t-CO2 and 100 RMB/t-CO2. This is because a tax on carbon emissions will lead to higher energy costs and prices, which will reduce energy demand and, to some extent, affect the manufacture of products by enterprises, leading to a significant reduction in industrial output. The fossil fuel industry, especially coal, is essential to the construction industry. The primary factor is that coal is cheaper than other forms of energy, and that the carbon monoxide it produces during burning can be used as a reducing agent. However, a carbon tax would lead to higher costs and prices for coal and oil, and lower output of the construction industry.

4.2. The Impact of Carbon Tax on Macroeconomy

4.2.1. Macroeconomic Indicators

This paper analyzes the macroeconomic impact after the carbon tax imposition on the construction industry, specifically in terms of carbon emissions, total investment, total output, GDP, and social welfare.

Figure 4 shows that carbon emissions and total output have significantly decreased, while GDP and social welfare also show a decreasing trend. This finding is consistent with Shi et al. [

58], who found that the implementation of carbon tax policy will inhibit economic and social welfare to some extent. While carbon tax will force enterprises to substitute essential components for energy inputs, the low elasticity of substitution of top-level production results in modest benefits in terms of labor and capital income, which are insufficient to offset the negative economic effects as a whole. In contrast to these indicators, total construction investment climbed marginally, owing to increasing demand for construction items because of urbanization. Furthermore, the rise in energy costs increased construction investment. As the increasing carbon tax rate from 80 to 100 RMB/t-CO

2, the emissions reduction increases from 13.970% to 16.491%, but the reduction of total output, GDP, and social welfare rise from 2.783%, 1.253%, and 0.998% to 3.139%, 1.574%, and 1.234%, respectively, indicating that high-priced carbon tax will have significant passive consequences on macroeconomic indicators and related industries. As shown in

Figure 4, while the total carbon emissions decline dramatically during the implementation of the carbon tax, GDP and social welfare decline less. Although the carbon tax does not realize a double dividend effect, the loss of GDP and social welfare is smaller than the amount of carbon emissions reduction. Therefore, compared to previous studies, the loss of GDP and social welfare caused by the implementation of carbon tax may be exaggerated.

To elucidate the impact of various carbon taxes on carbon emissions reduction and macroeconomy, this paper introduces the macroeconomic elasticity value of carbon emissions reduction as an evaluation index [

59]. This index can reflect the relationship between carbon emissions reduction and macroeconomic indicators brought on by various carbon taxes, so as to determine how to strike a balance between maximizing emissions reduction and decreasing unfavorable macroeconomic impact. The following are an expression of the macroeconomic elasticity of carbon emissions reduction:

Under different carbon tax rates, the greater the macroeconomic elasticity index of carbon emissions reduction, the smaller the relative macroeconomic loss and the greater the comprehensive benefit. As shown in

Figure 5, when the carbon tax is 40 RMB/t-CO

2, the elasticity index reaches its maximum value, representing the optimal socio-economic benefit and an obvious emissions reduction effect. Therefore, the most appropriate carbon tax rate for the construction industry is 40 RMB/t-CO

2. When the carbon tax rate is between 20–40 RMB/t-CO

2, the macroeconomic elasticity values γ2 and γ3 trend similarly, with an upward trend. This indicates that the passive impact on GDP and total output is less than the growth rate of carbon emissions reduction. When the carbon tax rate is between 40–80 RMB/t-CO

2, γ1 and γ2 fall rapidly, suggesting that macroeconomic growth is more pronounced than carbon reduction with an increased carbon tax. When the carbon tax is between 80–100 RMB/t-CO

2, the negative impact will be too large to be promoted as a current policy. γ4 trends suggest that social welfare will rise slightly with an increase in the carbon tax and then fall rapidly.

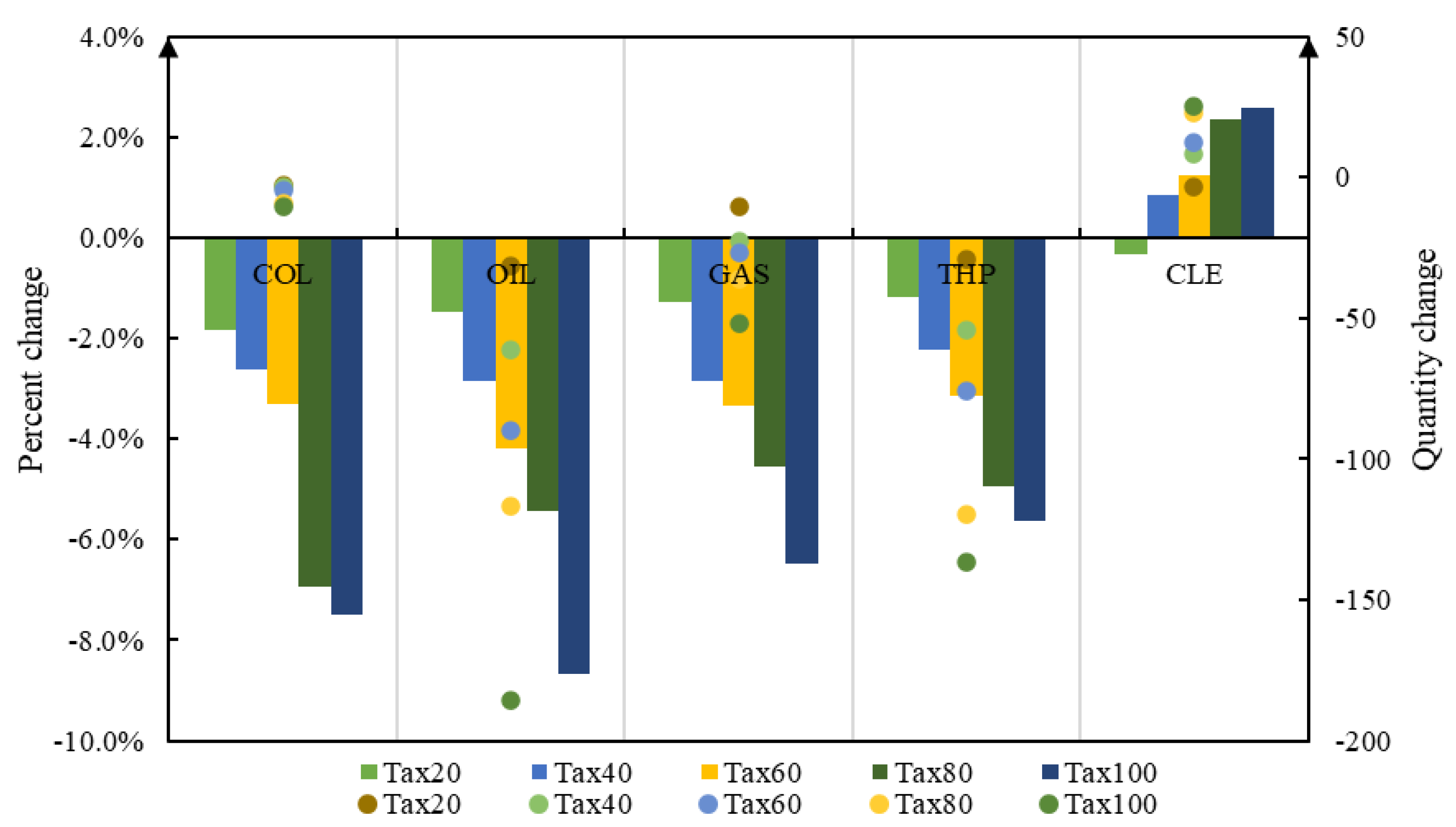

4.2.2. Energy Demand

Figure 6 shows the relative and absolute impact on energy demand after the carbon tax. When the carbon tax increases from 20 to 100 RMB/t-CO

2, the trends in absolute energy demand impact are broadly consistent with the relative impact, demand for oil decreases by 1.468–8.659%, coal decreases by 1.847–7.496%, natural gas decreases by 1.281–6.486%, and thermal power decreases by 1.189–5.620%. Conversely, clean power demand grows from −0.347% to 2.573%. This finding is consistent with those reported in other papers [

57], who revealed that the clean power industry would enjoy the most obvious positive impacts following the imposition of carbon tax. In the construction industry, enterprises prefer low-cost oil to relatively expensive and inconvenient gas. When applying the same carbon tax rate on coal, oil, natural gas, clean power, and thermal power, this magnitude of emission reduction for various fossil energy may be influenced by the carbon tax rate and fossil fuel price; this magnitude of emission reduction for various fossil energy may be influenced by the carbon tax rate and fossil fuel price. Carbon tax is based on the carbon content of the fuel. Because of the high carbon content of oil, a carbon tax policy can have a drastic effect on the price of oil, causing enterprises to reduce oil demand in order to cut costs.

As a secondary energy source, thermal power does not produce direct carbon emissions, but it does produce significant indirect carbon emissions in the production process, resulting in carbon tax that indirectly affects thermal power demand. In addition, energy prices have risen, forcing enterprises to reduce their usage of fossil fuels to cut costs, resulting in an increased demand for clean power. Therefore, a separate carbon tax rate could be implemented for various energy species to encourage the use of clean and renewable energy across society and reduce carbon emissions.

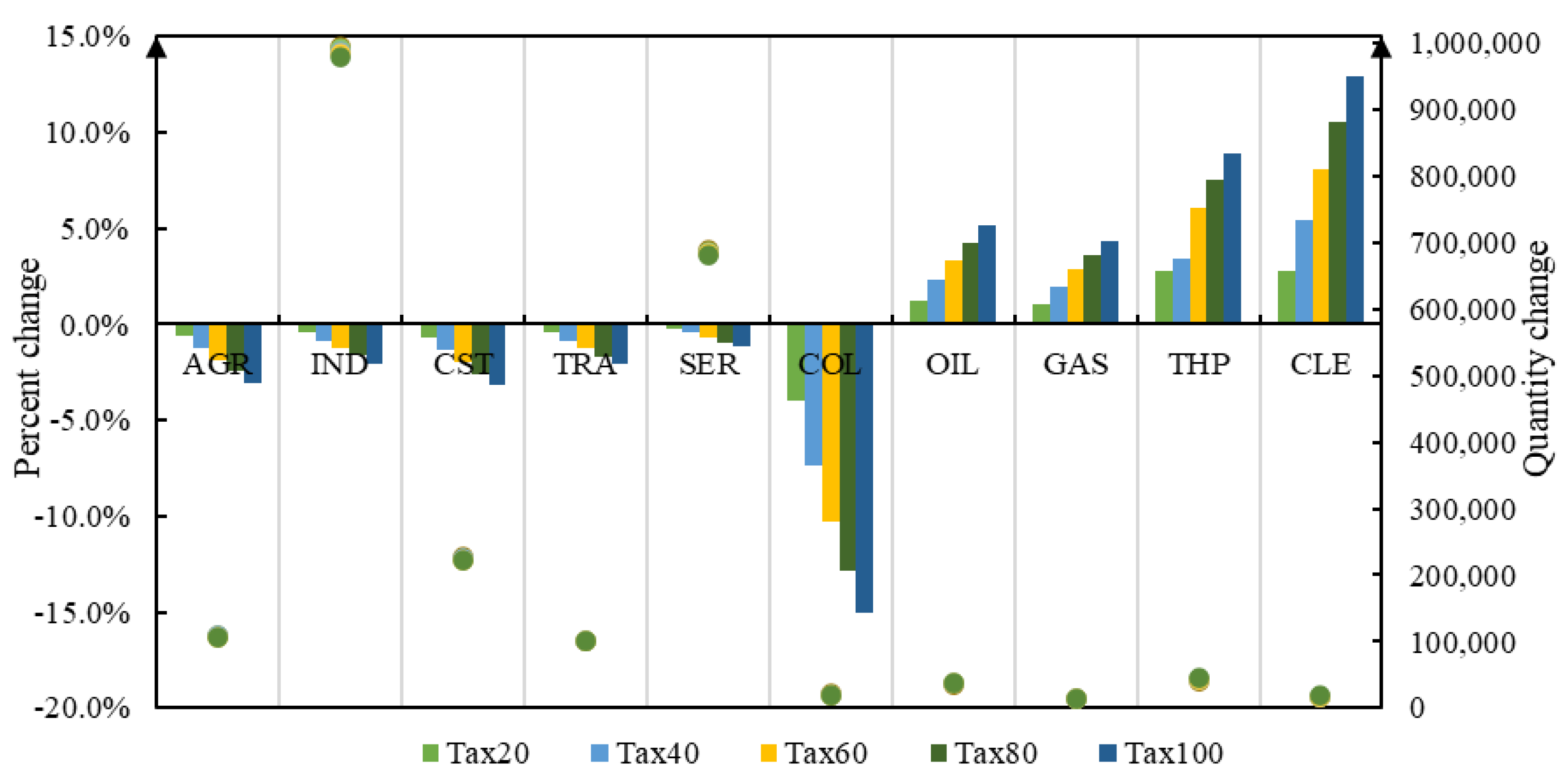

4.2.3. Sector Impacts

Figure 7 shows the changes in carbon emissions generated by each sector after the implementation of carbon tax on construction sector. In general, carbon emissions decreased significantly across sectors, especially in the energy sectors. With an increasing carbon tax, the coal sector decreases sharply from −6.749% to −25.560%. This may be due to the significantly different emission factors of various fossil fuel energy sources, with coal having the highest emission factor. This is followed by the reduction in carbon emissions from −4.784% to −18.395% in the industry sector, which is significantly greater than in agriculture, construction, transportation, and services. We found that the carbon tax on the construction industry not only follows the “law of increasing marginal emissions”, i.e., the higher the carbon tax rate, the higher the reduction capacity and marginal reduction capacity of the carbon tax. At the same time, carbon tax on construction industry also obviously affects the linkage industries with close connection, and the closer the connection with the construction industry, the more obvious the emission reduction effect. This finding is in agreement with Zhao et al. [

60], who revealed that a higher carbon price is helpful for enterprises taking some measures to reduce carbon emissions.

Figure 8 shows the impact of the construction industry’s carbon tax on the output of all sectors. As the carbon tax rises to 100 RMB/t-CO

2, the output of the agriculture, industry, construction, transportation, and services sector show different decreasing trends, from −0.647%, −0.431%, −0.678%, and −0.434%, and −0.231% to −3.043%, −2.030%, −3.166%, −2.056%, and −1.193%. The coal sector, on the other hand, shows a significant drop in output from −3.971% to −15.070%. As opposed to the coal sector, the oil, natural gas, thermal power, and clean power sectors show a significant increase in output. The reason for this situation may be that the imposition of carbon tax causes enterprises to abandon coal with high carbon emissions and choose other energy sources with relatively low carbon emissions for alternative production. Meanwhile, due to the increased cost of carbon tax in the construction industry, the industry will directly generate increased costs and reduced production. Coal, the upstream industry of the construction sector, will cause significant production cuts in terms of output. The finding gains support from Chan and Zhao [

61], who revealed that industry-level carbon tax will have asymmetric spillover effects on other related industries. Energy-intensive sectors will also suffer from the cost impact of energy price volatility, which will experience some degree of production reduction.

Combined with

Figure 7 and

Figure 8, it can be determined that the collection of a carbon tax on the construction industry can effectively reduce the carbon emissions of relevant departments. However, a carbon tax will also cause losses to their output value, especially in the coal sector, which is mainly dependent on energy for construction industry. The consumption of coal would be significantly impacted by a carbon tax. With an increased carbon tax, enterprises will be forced to reduce the use of coal and substitute it with other energy sources to reduce energy costs.

4.3. The Impact of Carbon Tax Revenue Recycling

The aforementioned findings imply that a carbon tax can successfully cut carbon emissions while also reducing the consumption of fossil fuels. However, the national economy, particularly social welfare, will dramatically decline. The carbon tax revenue recycling impact signifies how carbon tax gains are recycled in various ways to assist reduce economic expenses [

56]. In order to realize revenue neutrality and reduce the passive socioeconomic impact, three scenarios are designed to model the impact of recycling tax revenue at an acceptable tax rate of 60 RMB/t-CO

2 (

Table 2).

The findings demonstrate that recycling carbon tax revenues not only mitigate the negative macroeconomic impacts but also improve energy efficiency and emissions control. Compared to the scenario without revenue recycling (Recy1), Recy2 scenario can mitigate the GDP loss and social welfare loss from 0.948% and 0.757% to 0.890% and 0.497%, respectively. Meanwhile, the energy demand and carbon emissions reduction respectively increase from 5.233% and 11.141% to 4.990% and 10.950%. In the Recy3 scenario, total output and GDP decrease to 0.842% and 0.833%, respectively, and the change in social welfare decreases from subtractive to 0.235% (

Table 3).

The decrease in the price of most commodities in the recycling scenario is the primary reason for the increase in social welfare compared to the Recy1 scenario. Costs associated with carbon emissions and energy use rise as a result of carbon tax, resulting in increased manufacturing costs and commodity prices. Tax relief for households and sectoral investment, on the other hand, will lower manufacturing costs to some extent, which is a fundamental driver of dropping prices and a rebound in households’ consumption willingness [

38]. In the sector investment, there are some stakeholders that adopt sustainability, such as low-carbon enterprises. Although the imposition of carbon tax increases energy prices, low enterprises’ economic loss would be minimal. Conversely, the recycling of carbon tax revenues into sector investments is an additional subsidy for low-carbon enterprises, which enhances the incentive for stakeholders to continue to adopt sustainability and directly stimulates a virtuous cycle of low-carbon production in the construction industry [

62]. The recycling carbon tax scenario, as opposed to the Recy1 scenario, better realizes the double dividend mechanism of economic and social welfare, and can be a useful low-carbon policy tool.

4.4. The Impact of Improving Energy Efficiency

Carbon tax, as the previous results illustrate, can boost the cost of energy, applying to it a more expensive element of production. This will push up the cost of production for businesses, resulting in the reduction of enterprises’ production. To improve energy efficiency and reduce energy consumption, enterprises will also implement energy-saving technologies, especially in China where the price elasticity of demand for energy sources such as coal and oil is still relatively high. Therefore, in this paper, three scenarios are designed to simulate the impact of improving energy efficiency based on a tax rate of 60 RMB/t-CO2.

Table 4 shows the changes in the social subjects as a result of the increase in energy efficiency. By advancing technology, enterprises increase their energy utilization efficiency to 15% and significantly lower their carbon emissions from 7.790% to 20.510%. Compared to the Tax60 scenario, GDP, household income (HY), household savings (HS), and total investment (TINV) show a large upward trend, from 1.922%, 2.097%, and 1.318%, and 2.281% to 5.010%, 5.473%, 5.152%, and 5.960%, respectively. Meanwhile, household demand (HD), government revenue (GY), and government savings (GS) slightly increase. In contrast, government consumption (GC) declined from −1.259% to −3.252%.

From an environmental perspective, when energy efficiency is gradually improved, carbon emissions shift significantly, going from −7.790% to −20.510%. The reason is that improving energy efficiency efficaciously reduces the amount of fossil energy used, which results in a decrease in carbon emissions. However, at the same time, there is a potential risk that the improved energy efficiency will encourage the consumption of fossil energy, lower the cost of products, and to a certain extent restrain the use of cleaner energy. Carbon tax policies, which are levied on fossil energy, can avoid this risk and promote the industry’s demand for clean energy. Therefore, the combination of improved energy efficiency instrument and carbon tax policy should be used to make up for each other’s shortcomings, and achieve the promotion of cleaner energy use on the basis of reducing carbon emissions.

From a macro perspective, most economic participators derive some benefit from improving energy efficiency, as do households. To some extent, GS, as the carbon tax collector, will increase more tax revenue, leading to the associated TINV rising as well. Additionally, as government transfers to local welfare, households’ lives are also improved. This phenomenon arises because the carbon tax pushes companies to invest more in technology and increase the efficiency of energy use by improving the level of energy-related technologies, which increases output in all sectors and thus increases aggregate social demand.

All macroeconomic and welfare indicators increase in varying degrees. The results of the model show that the overall economy grows, although GC is declining. The macroeconomic impact of energy technology progress is positive, as shown in

Table 4. Therefore, improving energy efficiency is of great practical significance for decreasing energy consumption and carbon emissions, while maintaining macroeconomic growth.

5. Conclusions and Policy Recommendations

5.1. Conclusions

The construction industry is a representative energy-intensive industry, leading to excessive resource consumption, rising environmental pollution, and carbon emissions. Under the dual pressure of energy and environment, how to maintain stable economic growth while developing a low-carbon construction industry is an urgent issue to be solved. Carbon tax is a promising tool to address the carbon emissions issue in China. However, most literature focuses on how the carbon tax affects the macroeconomic environment as a whole. The construction industry has unique characteristics with different impact mechanisms and outcomes. To estimate the impact of the carbon tax on the construction sector, macroeconomy, and social welfare, a CGE model is established in this paper. Meanwhile, three carbon tax revenue recycling schemes and energy efficiency improvement schemes are designed, respectively, to reduce the passive impact of a carbon tax on the macroeconomy and social welfare. The main conclusions of the implementation of carbon tax on the construction industry in China include:

(1) Carbon tax on the construction industry has a key role to play in reducing energy demand and carbon emissions in China. In addition, the higher the carbon tax rate, the lower the energy demand and carbon emissions. From the perspective of economic cost and emissions reduction, the carbon tax suitable for the construction industry is 40 RMB/t-CO2.

(2) Carbon tax has significant negative effects on the macroeconomy, households’ welfare, and output in numerous sectors, and the economic and welfare costs of carbon emissions reduction cannot be ignored. Moreover, the proper carbon tax rates vary depending on the category of energy. Coal and oil should be subject to higher carbon tax rates due to their higher carbon emissions, whereas clean energy sources should be subject to lower carbon tax rates.

(3) The “weak double dividend” effect of carbon tax is achieved by tax revenue recycling for households and sectoral investment. When carbon tax revenues are recycled to households and sectoral investment, the negative macroeconomy and social welfare consequences of carbon tax are greatly minimized. At the same time, additional energy savings and carbon reduction effects can be achieved.

(4) The carbon tax, along with the improvement of energy efficiency, can effectively reduce the economic and welfare costs of carbon emissions reduction and maintain moderate economic growth, increasing the welfare of the population, and the negative impact on the output of various production sectors is small, potentially producing a “double dividend” effect. The policy combination can suppress the output of high-emission sectors and have a positive effect on the optimization of the industrial structure, while promoting the development of clean power and strengthening the substitution of clean power for other energy sources.

5.2. Policy Recommendations

(1) The government should take industrial heterogeneity into account when drafting policies, and formulate carbon tax policies suitable for different industries. Given that the demand impact is a significant factor for a carbon tax to inhibit the development of the construction industry, it is crucial to pay attention to this effect and combine macro-political advice from the government with self-regulatory market mechanisms to reduce the loss.

(2) To lessen opposition to a carbon tax on construction industry, tax neutrality should be followed. In other words, carbon tax should be combined with tax revenue recycling strategy. When concentrating on social effects, the policy of combining a carbon tax with revenue recycling, returning to households and sectors’ investment through transfer payments, is more effective.

(3) Improving energy efficiency is critical to achieving a carbon-neutral country. Adoption of the latest energy technologies in the construction industry must be actively encouraged. Revenues from a carbon tax can be an effective means to promote the development of energy technology. This requires increased investment in energy-related science and technology research and development, especially to improve coal processing and conversion efficiency and clean utilization, accelerate clean energy development and utilization, and enhance the proportion of non-fossil energy in energy consumption.

The approach adopted in this paper has the advantage of applying the CGE model to accurately depict the impact of a carbon tax on the construction industry, which is highly dependent on fossil energy. In particular, the tax revenues’ recycling scenarios are utilized to achieve revenue neutrality for the government and boost energy efficiency. However, there are still certain limitations in which the model simplifies the market environment, which can be somewhat different from the actual situation, and it does not take dynamic influences into account, such as time. Therefore, we will continue the following points in our future research work. Firstly, subsequent studies should further accurate calibration of the parameters and introduce a dynamic CGE model to further combine the long and short-term impacts of carbon tax policy with energy efficiency improvement in the construction industry. Secondly, China’s economic system is relatively complex. To better match the characteristics of China’s economy, more policy tools should be considered to explore a successful combination of carbon emissions reduction and economic growth policies, promoting the sustainable development of China’s green economy.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}