1. Introduction

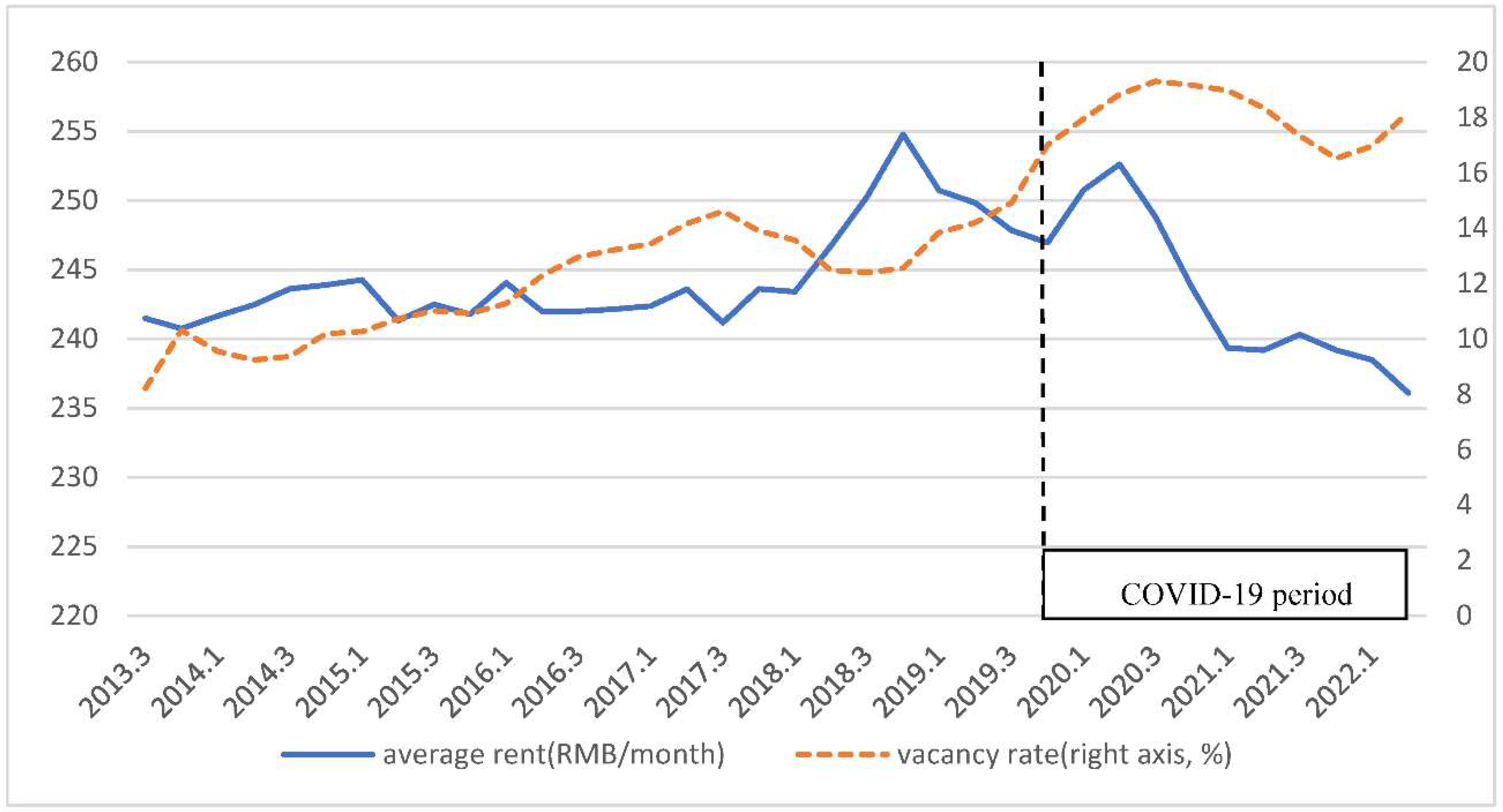

In 2021, China’s national office building net absorption rate exceeded 7.43 million square meters with an overall office vacancy of 23%; the supply of office building space is expected to peak in 2022, exceeding 9.5 million square meters of new supplies in the pipeline (CBRE [

1]). The accelerating vacancy rates in the Chinese office market, particularly in first-tier and second-tier cities, have caused extensive concerns among investors and policymakers (

Figure 1). To address the high vacancy rate in the Chinese office market, the Ministry of Housing and Urban-Rural Development of China implemented a new policy that encouraged local governments to convert vacant commercial real estate into rental housing in 2017 (MHURD, 2017) (

https://www.mohurd.gov.cn/gongkai/fdzdgknr/tzgg/201707/20170720_232676.html, accessed on 19 October 2022). While this policy aims to support the development of rental housing, it also indicates the high office buildings market vacancy rate in recent years in China. The onset of the COVID-19 pandemic further exacerbated this issue. The recent two years have seen the lasting effect of COVID-19 on China’s economy and office market; the office rent in major cities has declined sharply, and the vacancy rate remains high.

Importantly, various governments adopted COVID suppression or COVID-Zero policies. These policies would have an impact on investors’ sentiment. Naturally, this raises the question of whether the onset of COVID-19 directly affects real estate, particularly the direct office buildings sector. Although COVID-19 sentiment has a direct influence on China’s economic growth and urban development (Wang et al. [

2]), no study has been devoted to its impact on the office sector. Furthermore, COVID-19-induced work-from-home (WFH) may lead to a permanent change of structure (Davis et al. [

3]). Both these two factors may result in a decline in office buildings demand and further market change. However, two competing hypotheses have been proposed in the mainstream literature on the impact of COVID-19. Chen et al. [

4] asserted that COVID-19 should have a significant negative impact. This is in line with the fear sentiment hypothesis that was proposed by Da et al. [

5]. On the other hand, Nayaran et al. [

6] offered contradicting empirical evidence in which a positive effect is evident. They attributed this to the adoption of various governments’ stimulus policies to cushion the negative repercussions of unprecedented events such as COVID-19. Further, He et al. [

7] found that the impact of COVID-19 is not uniform. Specifically, they demonstrated that COVID-19 has a divergence effect in different sectors, highlighting the importance of sectorial studies.

Nevertheless, to the best of our knowledge, no study has been dedicated to assessing the impact of sentiment regarding COVID-19 on commercial properties. The impact of COVID-19 sentiment on real estate, therefore, is somewhat under-researched. This raises the following questions: (1) Does the onset of COVID-19 have an effect on the office markets? (2) Would the effect, if any, lead to a deterioration of office rents or an improvement of office rents? This research aims to fill the research gaps by examining the influence of COVID-19 sentiment on the office market rent in China. However, one could argue that these policies were short-lived, coming to an end with the availability of vaccines. As such, the short-lived COVID suppression policies might have a negligible effect on office buildings. This is particularly true for the office sector, as direct real estate is an illiquid asset with a prolonged transaction period (Lee and Lee [

8]). Unlike many countries, the Chinese property market offers a unique dataset as it has undergone a prolonged period of COVID-Zero policy. This unique dataset allows us to examine sentiment regarding COVID-19 more effectively.

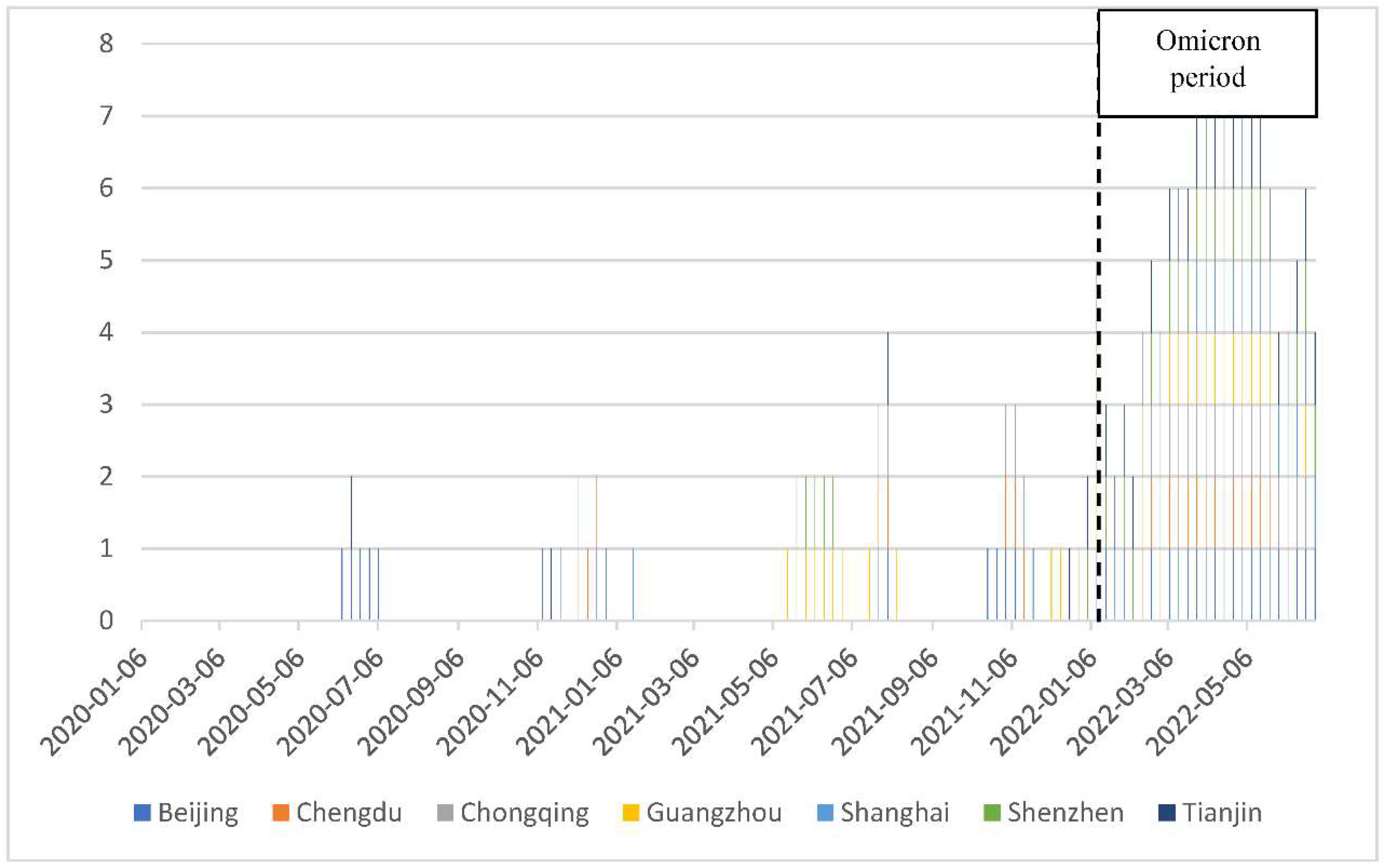

This study assesses the dynamics of office market rent and rental vacancy in seven cities in China: Beijing, Shanghai, Tianjin, Shenzhen, Guangzhou, Chongqing, and Chengdu. A two-stage Error Correction Model (ECM) is utilized to determine the short-run and long-run adjustments of rents and vacancy rates. We find that a heightened level of COVID-19 sentiment has an adverse and considerable effect on the Chinese office buildings market in the long run. The findings are consistent with Chen et al. [

4] for Bitcoins, for which COVID-19 fear sentiment has resulted in exacerbation of market volatility; thereby, a negative return should be documented. The finding is also in line with the notion of high investor sentiment in the behavioral finance literature (Da et al. [

5]; Tetlock [

9]). Further, COVID sentiment has a more substantial impact on office buildings rents where office vacancy is higher, reflecting an asymmetric effect. We also found that city-level gross domestic product (GDP) is a crucial variable determining office rent in China and an effective self-adjustment mechanism between rent and GDP growth. However, the supply market is mainly inefficient, and the high volume of office buildings in recent years and decreasing economic growth rate account for the high vacancy rates in China.

This study contributes to the buildings and real estate literature in a number of ways. Firstly, this is probably the first attempt to examine how COVID-19 sentiment would have an impact on direct real estate, particularly the office sector. Specifically, property plays a critical role in the broader economy, and it has emerged as a key element of the capital market (Lee et al. [

10]). Despite extensive studies that have examined the impact of COVID-19 on the financial market, little study has been devoted to the direct real estate market. Allan et al. [

11] Hoesli and Malle [

12] are exceptions. Allan et al. [

10] provided some preliminary results to show that the Asia–Pacific region commercial property rent declined severely in regions exposed to the OVID-19 pandemic. Unlike Allan et al. [

10], we focus on COVID-19 sentiment for the first time. This provides a more complete view of investors’ sentiment as COVID-19 sentiment would be better captured by COVID-19-related keyword searches. As posited by the investors’ fear sentiment hypothesis of Chen et al. [

5], sentiment itself should be the major channel to create price adjustment, if any, instead of total deaths and confirmed cases of COVID-19. This is particularly true in China as China has low number of total COVID-19 deaths and confirmed cases as a result of its COVID-Zero policy. However, Hoesli and Malle [

12] provided a commentary on the shock of COVID-19 on the European market without any empirical evidence due to the short history datasets. Extending their study, the empirical evidence of COVID-19 sentiment is provided for the first time. As such, this study complements not only the property literature on COVID-19 in general but also the literature on the effect of COVID-19 on the economic and financial systems in particular. Second, using relatively recent data from the Chinese office market, we confirm that there is a relatively efficient rent adjustment process. Finally, this study contributes to the limited studies on office rent modelling during the COVID-19 era. Extensive studies have been placed on REITs modelling, but few studies have been devoted to office. This study offers an enhanced understanding of the office market performance during COVID-19.

The remainder of this paper is organized as follows. The second section contains a literature review. In the third section, we describe the data and the statistical description, and then, we introduce the method. The fourth section provides the detailed results of our analysis. In the end, a conclusion is presented.

5. Conclusions

This paper applies a two-stage ECM framework to assess the impact of COVID-19 sentiment on the long-run and short-run dynamics of office rents and vacancy rates in seven major cities in China. We also constructed a COVID-19 sentiment index using Baidu search queries on coronavirus-related words and further examined its influence on office rent and the vacancy rate.

Numerous key findings have been identified. COVID-19 sentiment emerges as a key determinant of the office market. Office rent decreased more than 8% by COVID-19 fear sentiment as a result of an increase in search interest in COVID-19 keywords for an entire quarter, and it has a more decisive influence on the office market in tier 2 cities than in tier 1 cities. The interaction terms model further confirms that COVID sentiment substantially impacts office rent where office vacancy is higher (tier 2 cities), suggesting an asymmetric effect exists. The findings support the assertion of Chen et al. [

4] that fear sentiment leads to hostile asset prices, thereby creating a softening office building market. Specifically, this study offers a fuller understanding of COVID-19 sentiment’s influence on the office sector, particularly in China. The study confirmed that COVID-19 sentiment does have a significant influence on property market performance. This also shows that COVID-19 may have a significant negative influence on the office market, especially after Omicron started to spread across the country in 2022.

These findings have some profound implications for investors’ investment strategies. The finding suggests that investors should monitor the COVID-19 sentiment in their decision-making. Notably, the constructed COVID-19 exposure index offers a piece of important information to investors that should be considered. Furthermore, investors should also acknowledge the presence of submarkets and asymmetric effects as second-tier cities with higher vacancy rates are more sensitive to the movements prompted by COVID-19 sentiment. Although our study highlights the importance of considering COVID-19 sentiment in determining the rent of office buildings, it is still unclear whether the potential change of new ways of work (such as work-from-home) would alter our findings. Further research should be conducted to ascertain this.

Our findings here also support the fear sentiment hypothesis of Da et al. [

5], and we proved that sentiment also plays an important role in explaining property performance, as it does in the finance market. Finally, we suggested that further research could examine the long-term effect of COVID-19-induced change (such as work-from-home) on the property market. Further, micro-level buildings’ attributes and performance data can be applied to identify the influence of COVID-19 on the property market at a disaggregated level. Specifically, the disaggregated studies offer further insights into property market dynamics (Bangura and Lee [

65] and Dunse and Jones [

66]). Our study focuses on COVID-19 sentiment, but the influence of sentiment on other topics, such as climate change, can be further examined in the post-COVID period.

{kind=link}

{kind=link}