1. Introduction

In Ethiopia, land is a key natural resource and development asset for most smallholder households whose primary livelihoods depend on agriculture. Agriculture is considered the backbone of the economy, which accounts for about 34 percent of the national GDP [

1]. About 74 percent of Ethiopian farmers are smallholders who contributed to more than 90 percent of both the total cultivated area and total agricultural production [

2]. Agriculture is dominated by rain-fed, labor-intensive, and scarcely mechanized production systems on extremely fragmented and small land parcels [

3,

4]. Official data on holding size in Ethiopia shows that 38 percent of households possess less than 0.5 hectares of land, 23.65 percent hold between 0.51 and 1 hectare, 24 percent between 1.1 and 2 hectares, and the remaining 14 percent hold above 2 hectares [

1]. Additionally, only two percent of smallholder landholding is irrigated, and only 3.7 of smallholders have access to agriculture machinery [

3]. However, the agriculture sector continues to provide an opportunity to address Ethiopia’s core development challenges, including poverty, persistent food insecurity, unemployment, climate vulnerability, and foreign exchange earnings, among others. However, the within-sector transformation in agriculture lags because of a weak policy and enabling environment [

1,

3].

Researchers argue that the flow of credit from formal financial institutions (FIs) toward the agriculture sector is relatively low. Only 13 percent of the total lending provided by the formal FIs is directed to the agriculture sector, with most of this credit being channeled towards large-scale agricultural enterprises [

5]. Another study found that two-thirds of smallholder farmers in Ethiopia are credit constrained, most of them (71.9 percent) due to risk factors and transaction costs (14.33 percent) [

2]. These include high interest rates, collateral requirements, and a high risk of losing collateral due to the inability to repay loans [

2,

6]. Others also found that credit constraint is often considered one of the key barriers to the adoption of modern agricultural technologies and low agricultural productivity [

5,

6]. Smallholder households facing capital constraints resort to unsustainable land use practices and production systems. However, it is believed that smallholders’ efficient and sustainable land use and management is essential for sustainable agricultural growth that positively contributes to the structural transformation of the country.

In this regard, documented land rights are a necessary condition for land markets and reduce the need for owners to spend resources on protecting claims [

7,

8]. Scholars often presumed that tenure security via land registration and titling increases access to credit by allowing landowners to use the land as collateral [

9,

10,

11]. However, evidence of credit effects of land registration and certification programs have been rare and, at times, with mixed results. The ability of land tenure security to make credit access easy is a necessary precursor for the rural world in general and the agricultural sector in that it is credit access that can lead to the modernization of the agricultural economy [

12]. In fact, evidence suggests that without several other factors put in place, such as an appropriate policy environment [

13], the hypothesized link to credit access fails to materialize [

14,

15,

16]. For instance, Deininger and Ali [

7], using land registry administrative data in Lesotho, found that land and credit market activation is exclusively due to policy reform rather than the systematic urban land titling program alone.

While there is a mixed result about the effect of land registration or titling on access to credit in different parts of the world, there is scanty rigorous evidence on the effects of digital land registers on access to credit in rural Ethiopia underpinned by technological and policy innovations. Nevertheless, in 2016, Cloudburst conducted an impact evaluation of the USAID-funded two successive programs run between 2005 and 2013 and found that the Second Level Landholding Certifications (SLLC) in the program areas led to a small increase in access to credit compared to control groups [

17]. Seven years later, a follow-on impact evaluation research of the same programs was undertaken by USAID, this time by commissioning another contractor called Landesa [

18]. The research team found a negligible impact of SLLC on the access to credit effect, although cautious to draw this conclusion due to the small sample size. However, the study is bold enough to conclude that SLLC may increase the likelihood of households obtaining credit until peaking 5 to 6 years after receiving the SLLC and then decreases [

18].

However, these studies did not account for the effect of the policy change and regulatory reforms of collateralization of land use rights enacted since 2017 and the technological innovations made since 2018 related to the National Rural Land Administration Information System (NRLAIS) and its effect on credit access to small landholders in rural Ethiopia. NRLAIS is a digital cadaster and land register that securely stores tens of millions of parcel records issued with an SLLC and holds information about the registration of sporadic subsequent land transactions, including mortgages. To fill this knowledge gap and generate new insights, this paper assessed the effect of access to information from the digital land registers, i.e., NRLAIS, on the credit-worthiness of smallholder households in rural Ethiopia. The study also assessed transaction risks of the SLLC-linked credit market anchored by new policy and regulatory reforms related to the collateralization of land use rights.

2. Background

Over the past half a century, Ethiopia has shown a faster demographic transition than the rest of Africa [

19] and a rapid urbanization with an annual rate of 5.4% [

20]. Although urbanization remained at 24% by 2021, agriculture will continue to dominate the economy, and competing access to land and transferability of rights remain to determine factors of the country’s economy. Hence, land is among the most controversial and politically sensitive, and complex issues in Ethiopia. As such, land tenure reforms have continuously been one of the top development agendas interwoven within nation-building among various governments that ruled the country over the past centuries. The pre-1974 land tenure has been characterized by empirical regimes with a landlord to tenant land tenure relationships [

21], while the socialist military regime (ruled between 1975 and 1991) is characterized by egalitarian land tenure reform [

22]. The period between 1991 and 2018, led by the Ethiopian People’s Revolutionary Democratic Front (EPRDF), reaffirms the state ownership of land inherited from the previous socialist military regime with limited reform regarding the transfer of usufruct rights among the hires, land lease, and rental arrangement. Since 2018, the Prosperity Party-led government has continued ruling the country without making any fundamental land policy reform, although many economic and structural reforms are being implemented. However, what remains common to all previous governments, including the current one, is that land tenure and its governance issues have been the maker and breaker of political power relations, determinants of resource allocation among societies, drivers of economic growth, and environmental sustainability.

Since the early 2000s, with the aim to improve land tenure security and incentivize land-based investment, Ethiopia has implemented one of the largest progressive two-stage land certification programs in Africa. Despite the difference in the technology employed for the adjudication of parcel boundaries and data storage, there is no big and substantive legal difference in recognizing the de facto land tenure rights between the First Level Landholding Certification (FLLC) and Second Level Landholding Certification (SLLC) programs. However, the SLLC includes value-added information related to the land parcels with geo-referenced maps to the landholding certificates and relatively precise land area measurements. Historically, the FLLC started around the end of the 1990s and ran through 2010. In contrast, the SLLC pilots have been started since 2003 and run through 2013 [

23]. Since 2014, the SLLC rollout program has been launched nationwide and continued expanding in the highland parts of the country to date [

24]. An existing study shows that over 25 million rural land parcels were demarcated, mapped, and issued with an SLLC as of 2022 [

23]. Existing studies well documented the effects of this large-scale and cost-effective land certification program on tenure security [

25], agriculture productivity [

26], women empowerment [

18], land rental market participation [

27,

28], and land disputes [

29]. Although Xinyan Hu et al. [

30] find that land titling affects the political trust of farmers in China, there is scant evidence to what extent this large-scale land certification program influences political trust and power relations among the rural landholders in Ethiopia.

Since 2018, there have been changes in technology innovation of digitalizing the land registers and organizational constellations in the land administration institutions. Additionally, there is a change of policy and regulatory reforms related to the collateralization of rural land use rights in Ethiopia. Firstly, along with the SLLC program, Ethiopia developed and operationalized a digital cadaster and land registration system called the National Rural Land Administration Information System (NRLAIS). Since 2018, this system has been rolled out and made operational into over 300 woredas (districts) in which over 20 million rural land parcel information is securely digitized. Abab et al. [

24] found that this digital land administration information system makes updating the land records easy, transparent, less costly, and increases the availability and accessibility of land rights information to concerned bodies.

Secondly, in 2019, the Federal Government of Ethiopia enacted the Movable Property Security Rights Proclamation No. 1147/2019. Prior to this proclamation, the Amhara regional state enacted Proclamation No. 252/2017, which extended landholders’ rights to include the use of land as collateral for up to 30 years. As per this proclamation, Article 16 states that in the event of default, the landholder will not be evacuated from the land, but rather the financial institution will temporarily gain the use right to recover the loan amount. The revised draft rural land administration and use proclamation at the federal government level also included a provision that enables landholders to access loans from financial institutions after securing a collateral agreement that is attested and registered by local land administration offices in NRLAIS. This policy change and regulatory reforms and technological innovations coupled with the land certification programs stimulate the financial institutions and smallholder households to behave differently than ever before. This behavior includes the financial institutions incentivized to develop a new loan product that targets small landholders and the landholders also more interested in accessing those credit products using their documented land use rights as collateral.

3. Materials and Methods

3.1. Sample Size and Data

Table 1 presents the summary of sample size, tools, and methods employed by the 2021 USAID impact evaluation study and characteristics of the digital land register’s administrative data observations. The study was conducted in three regional states of Ethiopia (Amhara, Oromia, South Nation Nationalities and People (SNNP)), 19 districts, and 183 kebeles/villages. The study employed administrative data generated from the digital land registers of woredas that established the national rural land administration information system (NRLAIS). Those NRLAIS databases have been used to register all subsequent land transactions, including the registration of mortgages, and used as a matching approach with the household survey datasets. This digital register administrative data helps to implement an approach using administrative units that allows identifying the effects of the policy change and technological innovations separately from those of the two-stage systematic land registration programs.

To help compare the results, the study also used survey data collected for the 2021 follow-on impact evaluation (IE) studies of the USAID-funded land administration programs, namely the Ethiopia Land Tenure Administration Program (ELTAP, run between 2005 and 2008) and Ethiopia Land Administration Program (ELAP, run between 2008 and 2013). The evaluation examined land certification investments to better understand the impacts and limitations of the land certification programs on rural land users. Data were previously collected in three rounds, namely, 2008 as a baseline, 2015 as the end line, and 2021 as follow-on impact evaluation studies. Additionally, qualitative data is also collected through key informant interviews with land administration officials and financial institutions.

The administrative data were generated from 11 study woredas of Amhara, Oromia, and SNNP regional states,

Table 1. The digital registers administrative data after NRLAIS establishment and policy and regulatory reforms suggest that these changes triggered a distinct shift in (i) the number of registered, canceled, or amended mortgage transactions, including loan size and duration, (ii) the share of registered parcels after subsequent transactions reported by type of land transactions including the area in hectare and numbers, and (iii) share of parcels registered in the name of male-headed only, female-headed only and jointly male and female-headed households among others.

For systematic comparison, the authors selected the same woredas covered by the 2021 follow-on USAID’s IE study except for woredas from the Tigray regional state. Woredas from Tigray regional states were not covered by the USAID 2021 follow-on IE study due to the war that took place in the country during the household survey data collection. In addition, 12 Kebeles in the Amhara region were excluded due to the security situation in this study area. Looking at the survey data closely, all study woredas in Amhara regional state established and made NRLAIS operational in 2019/2020. Contrarily, out of the six study woredas in the Oromia regional state, only one woreda, i.e., Bora woreda, established and made NRLAIS operational. In fact, Bora woreda is a new woreda split up from the parent Dugda woreda. According to the key informants, the other five woredas did not yet establish NRLAIS due to data quality issues with the cadastral index maps. Moreover, out of the six surveyed study woredas of SNNP, five woredas were established and made NRLAIS operational starting in 2020. However, Wendo Genet woreda has been moved to the newly established Sidama regional state and did not yet establish NRLAIS, so it was not considered in this study.

Manual data collection was also employed for those woredas without NRLAIS. While employing manual data collection in non-NRLAIS-established study woredas, it is important to note that those woredas have been registering subsequent land transactions sporadically and trying to update their semi-manual land registers. These records are considered objectively secured since they have been verified by legal and administrative procedures before the registration of those subsequent land transactions made on the legally protected land registers.

3.2. Conceptual Framework and Empirical Model

The conceptual framework presented in

Figure 1 shows the causal relationship between accessing the digital land registers (NRLAIS) as a service to secure formal credits, which is anchored by innovations in policy change of collateralization of land use rights, not necessarily pledging the conventional ownership rights of the land. This relationship reflects the ability of the land use rights to be used as collateral once a smallholder household receives a land certificate. What is equally important is the innovations in the institutional constellation of the NRLAIS in terms of people, organization, and technology.

From the available literature, one can draw the conclusion that stronger land tenure and property rights founded on the right policy and regulatory frameworks and the availability and accessibility of a digital land information system can contribute to at least two investment channels related to collaterals [

6,

13,

16] that are of interest for the current study. This includes an increase in the supply of credit and reduces the cost of contracting and monitoring enforcement of collateralization, i.e., transaction cost [

31]. These transaction costs are assumed to be related to credit transaction risks. To demonstrate this relationship, the land tenure literature suggests that land registration and certification programs enhance tenure security of land and resource rights which stimulates collateralization and increase the supply of credit [

32,

33,

34,

35].

The effect on the credit supply is an increase in the willingness of lenders to provide credit if borrowers can use secured land as collateral [

34,

36]. Additionally, the credit-worthiness of individual smallholders for collateral is dependent on the absence of uncertainty and asymmetric information [

34,

36,

37]. This may be due to the availability of dependable and secure information services delivery from the land administration institutions anchored by sustainable and functional digital land information systems [

16]. This incurs transaction costs but, managed properly, can reduce the inefficiencies arising from uncertainty [

34,

38,

39,

40]. Hence, credit impacts from land titling or registration would be expected only if such efforts are comprehensive, including enabling policy environment [

13], registries remain up to date over time [

41,

42], and third parties, such as mortgage lenders, can access reliable land registry information at low cost on a routine basis [

16].

Moreover, the existing literature suggests that transaction costs consist of the costs of measuring the valuable attributes of a right and the costs of protecting rights and enforcing contracts [

38,

39,

40]. This is mostly moderated by the availability and accessibility of reliable information from a functional land register. Enforcement of contracts depends on a constellation of supporting arrangements and implementation mechanisms, such as the coordination between financial, land administration, and law enforcement institutions [

34,

36,

40,

43]. With certified land that secures land rights as collateral for credit and contract enforcement, creditors can lawfully repossess land, if necessary, arise from a default [

36]. Additionally, the threat of repossession collateral acts as an incentive to the borrowers to repay the loan on time [

31].

Keeping this theoretical background in mind, recent policy changes and regulatory reforms at the federal and regional state levels in Ethiopia suggest a promising avenue for increasing the collateral capacity of small landholders. Up until recently, it was uncommon practice across the country to pledge land rights as collateral for individual loans from financial institutions. As the policy changes and legal framework improves at the regional level, and the digital land administration information system coverage expands, the SLLC-linked credit is significantly expanded to non-pilot areas of the country. Hence, as part of this research objective, the conceptual framework focuses on three investment channels of the policy change and the role played by the NRLAIS on (a) signaling the credit-worthiness of individual small landholders, (b) incentivizing the willingness of financial institutions to provide credit, and (c) reducing collateralization-related transaction costs and risks.

4. Results

4.1. Descriptive Statistics

Table 2 presents sex, marital status and educational level of the survey households. Totally, 2294 household heads participated in the third round of the household survey, which was conducted between 1 April and 16 May 2021, of which 78% of the respondents were male while 22% of the respondents were female. The average age of respondents was about 55 years, with the minimum and maximum of 19 and 99 years old, respectively, showing most household heads found their active and productive ages. Out of the total 2294 respondents, 76.26% (1749) were married, of which 74.14% (1700) were males and 2.12% (49) females. To understand the literacy level of the respondents, the survey also included the highest grade of schooling completed by the respondents. The data shows that about 51% of the respondents were illiterate while about 46% of the respondents were literate, including 11.75% of them who can read and write, 19.43% and 8.24% of them completed grade 4 and grade 8, respectively. This shows that most of the respondents need some level of support to read and understand their legal land use rights, obligations, and responsibilities.

About 989 households (26% women) obtained credit between May 2019 and April 2021, which linked to 3048 parcels from different lending institutions, including microfinance (60.7%), saving and credit cooperatives (25%), individuals (13.58%), and commercial banks (0.72%),

Table 3. This shows that the majority of small landholders have obtained credit from microfinance, followed by saving and credit cooperatives. The majority of heads of the survey households in the study areas practiced saving in their savings and credit cooperatives, increasing the liquidity of the cooperatives. Households with higher income, livestock, and landholding area per capita and closer to financial institutions are more likely to practice savings.

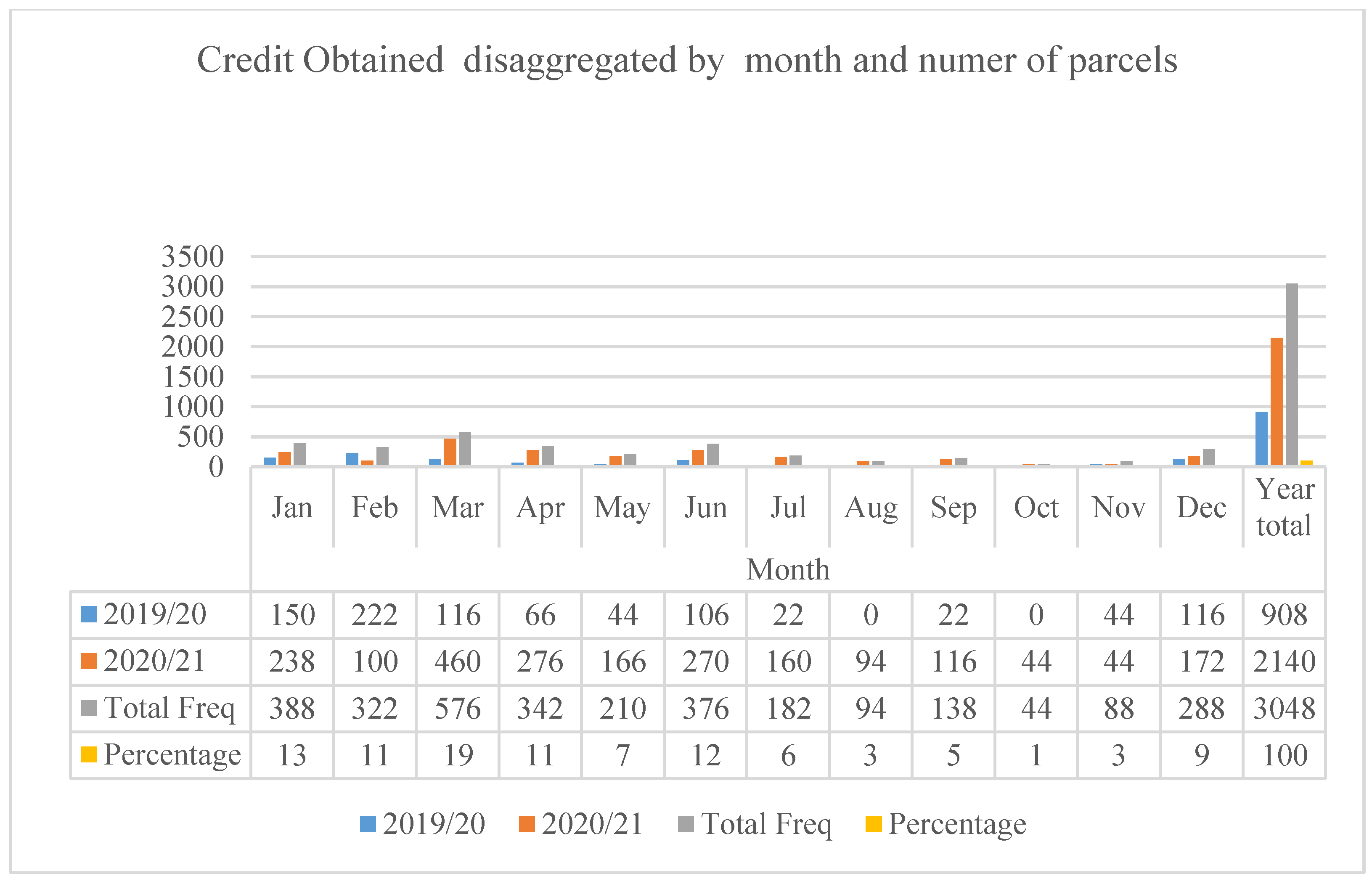

The survey results also revealed that the maximum (19 percent) and the minimum (1 percent) number of credits was obtained in March and October, respectively. Over the years (May 2019 to April 2021), 79 percent of the credit was obtained between the months of December and July, whereas the remaining 21 percent was obtained between the months of August and November,

Figure 2. This shows that household heads reported that most of the credits obtained were in line with agricultural land preparation calendars.

Respondents were also asked about the number and size of credits obtained, length of the repayment period, use of land certificate as collateral by type, and what will happen if they are unable to repay the loans. About 39 percent of household heads obtained a credit amount ranging between 500 ET Birr and 10,000 ET Birr, whereas only 5.45 percent of household heads obtained more than 50,000 ET Birr,

Table 4. The survey results also revealed that only 24 percent of household heads used their land certificate as collateral, and of those who used land certificate as collateral, 25 and 54 percent used FLLC and SLLC, respectively. This shows that creditors increasingly tended to hold SLLCs as collateral as SLLCs issuance coverage increased over time.

However, about 21 percent who reported that they have been using both FLLC and SLLC appear subject to the interpretation of contexts. This could happen when a landholder obtained one or more of the credits using FLLC in the first round before their possession of SLLC and another one after their possession of SLLC. Otherwise, this response could be generated due to the misunderstanding of the question itself since it is less likely that a landholder could have both the FLLC and SLLC to several parcels of landholdings under their possession within the same administrative registration Kebele. On the other hand, the results also revealed that 80 percent of household heads agreed to repay between 6 and 12 months, while only less than 1 percent agreed to a repayment schedule of 48 months, meaning most of the loans are short-term. Moreover, about 39 percent of the borrowers feel that they will lose their land certificate if they default on the repayment based on the terms and conditions of the credit agreement.

4.2. Descriptive Statistics of Data from the Digital Land Registers

Table 5 presents descriptive statistics of the administrative data generated from the study woredas digital land registers in April 2023 for the period of two years (between January 2021 and December 2022). Although such data lack information on the socioeconomic characteristic of households, it includes information on the gender of registered landholders, numbers and types of transactions registered after first-time land certification, allows to compute the loan size, requested number of mortgage registration and cancellation, and estimates the SLLC-linked transaction risks.

In the current study, the total number of woredas covered by these administrative data was 11 (four woredas from Amhara and Oromia each and three woredas from SNNP regional states), covering 366 kebeles for the years 2021 and 2022. These woredas are the subset of the 19 woredas covered with the 2021 USAID impact evaluation study household surveys. According to these digital registers’ administrative data, the total number of households who received SLLC-linked credits was 10,789, of which 1621 (15.02%), 1152 (10.68%), and 8016 (74.3%) were headed by men, women, and dual/jointly headed households, respectively. The mean of households who received SLLC-linked credit per kebele was 4.43, 3.14, and 21.9, headed by men, women, and dual/jointly headed in the years 2021 and 2022, respectively. This indicates that only 3 percent of households in the study kebeles obtained SLLC-linked formal individual credits over the past two years.

Likewise, these administrative datasets indicate that about 11,679 parcels with a total area of 5636.31 hectares were collateralized for the total SLLC-linked credits obtained by the households in 366 kebeles. This shows that the total number of pledged parcels for the credits obtained is more than the total number of households, meaning households were pledging one or more parcels of their landholdings to access those credits. This is particularly common practice among households in the Amhara region compared to the other two regions (Oromia and SNNP). This variation may arise due to the average parcel size in the Amhara region being less than that of the average parcel size in the Oromia and the SNNP regional states.

According to the digital land registers administrative data, the total value of credit obtained within those two years (2021 and 2022) is 427 million Ethiopian Birr (ETB) which is equivalent to about 8 million US dollars for all study kebeles. One-fourth of this loan was obtained by dual/jointly headed households, while one-tenth of the loan was channeled to women-headed households. This shows that each household obtained about 40,000 ETB on average as individual credit over the past two years. This indicates a four times loan size increment compared to the household survey loan size that was conducted for the preceding couple of years. There is a clear increase in loan size obtained by the household heads during 2021 and 2022 compared with that of 2019 and 2021 (survey result) results. This may indicate the effect of the policy change of land use collateralization which was enacted in 2019 at the Federal government level and became effective in 2020. In addition, this may be due to the availability and opportunity to access digital land information, which is securely registering mortgage transactions and guaranteeing them from third-party interests. The key informants revealed that the establishment and operations of the digital land registers at the woreda level help to monitor volumes of transactions, including mortgages at risk, and take corrective measures.

According to the key informants, most households who obtained those credits have been used to procure agricultural productivity enhancement inputs such as fertilizers, improved seeds, and pesticides as well as for animal husbandry (bull and shoats fattening, dairy farms, and poultry) that diversify their livelihoods. The key informant interviews also revealed that the credit interest rate ranges from 8 percent to 15 percent, with an average loan repayment period ranging from 12 months to 60 months, meaning most of the credits are short term like the household survey data.

4.3. Estimates of the Parameters of the Probit Regression Model

The probit regression model result indicates that among the ten hypothesized explanatory variables, seven variables were found to influence the landholder’s credit-worthiness significantly. The model result and average marginal effect size estimates are presented in

Table 6. From the results, the regression model is outperformed by 7.17 percent of the baseline model. The likelihood ratio Chi-square of 162.84 with a

p-value of 0.000 indicates that the current study model is statistically significant.

Those independent variables with positive average marginal effects include sex, parcel distance, FLLC, and SLLC, whereas age, household type, and perceived credit transaction risk have negatively affected landholders’ credit-worthiness in the study areas. Education, parcel area, and time travel to the parcels were found to insignificantly affect the credit-worthiness of the landholders. The average marginal effects of each of the parameters are discussed based on their significance as follows.

Sex—the result revealed that the sex of the household head positively and significantly influenced credit-worthiness. The survey result revealed that a household headed by a male has a 7 percent increased probability of credit-worthiness compared with their counterpart household headed by a female. Meaning female-headed households were more credit constrained than their counterpart male-headed households. This may have a negative effect on the productivity and livelihood status of female-headed households in the study areas.

Age—the age of a household head is negatively and significantly affected credit-worthiness with an average marginal effect of 0.2 percent, meaning every one-year increase in the age of the household head leads to a 0.2 percent decrease in the probability of their credit-worthiness. This may indicate that households with older ages were less likely to obtain credit.

Household type—The result revealed that household type negatively and significantly affected credit-worthiness in the study areas with an average marginal effect of 1.5 percent, meaning a married household heads have a 1.5 percent decreased probability of credit-worthiness compared to their counterpart single household heads.

Land certificates—the tow-stage land certification program is one of the mechanisms sought for improving tenure security in Ethiopia. Under the current study, the survey result revealed that possessions of either FLLC or SLLC are found to positively influence credit-worthiness of household heads significantly in the study areas. The results indicated that certification increases the credit-worthiness of household heads with an average marginal effect of 7 and 5.4 percent for FLLC and SLLC, respectively. This result is consistent with the lessons of property rights theory, which predict a direct positive effect of land titling as a proxy measure of tenure security on credit-worthiness. Moreover, the result is in line with Cheng et al. [

39] found households living in counties where the local governments explicitly permitted the use of land as collateral, land titling reform had a positive effect on credit in China. Piza [

44] also found that land titling increases credit use, decreases reliance on credit borrowed from a relative, and increases credit borrowed from commercial banks in Brazil.

Credit transaction risk—the results of the survey indicated that perception of credit transaction risk negatively and significantly affected the credit-worthiness of household heads with an average marginal effect of 27.8 percent, meaning one-fourth of household heads were found risk averse, which hinders their credit-worthiness.

Contrarily, the survey results revealed that education, parcel area, and travel time to a parcel were found to influence on credit-worthiness of household heads negatively but insignificantly. This is a complete contradiction to the results found from the key informants’ interviews of microfinance and credit and saving cooperatives in that level of literacy, and land area are part of the key parameters while assessing the credit-worthiness of credit applicants.

5. Discussion

The key objective of the current study is to assess the effect of the policy and technological innovations on the credit-worthiness of small landholders in the three highland regions (Amhara, Oromia, and SNNP) of Ethiopia. While the quantitative analysis of the household survey helps us to understand the factors influencing access to credit, the descriptive statistics of data from the land registers and qualitative policy and legal framework analysis help us to indicate the differential effect of the policy and technological innovations. The current study also looked at the willingness of financial institutions to provide SLLC-linked individual loan products measured by the volume of credit transactions and related monitoring transaction costs or risks. Based on the descriptive statistics and regression model results, this section discusses the key elements of the conceptual framework shown in

Figure 1. The figure shows how the rural land administration information system as a service powered by technological innovations is brokering to access credit by individual smallholder households from formal financial institutions, moreover, how the institutional constellation helps to monitor and enforce collateral contracts, including valuation, registration, repayment, and defaults.

5.1. Policy Innovations Leads to Legislative Reforms

Access to credit for smallholder households has been much more limited in rural Ethiopia due to the absence of enabling policy and legal framework regarding financial institutions to lend money to smallholders using land as collateral, meaning smallholder households could not be able to use their usufruct rights, which is the main asset held by them, to use as collateral to access individual credit. The available option is group loans which did not always meet their needs in terms of loan size and repayment schedule. It is not surprising that even in the most advanced economies where reliable credit information and a wide range of financial products are available, borrowers have to offer collateral. Particularly, financial institutions operating in developing economies, including in Ethiopia, prefer to use immovable properties, such as land and real properties, as security interests. For instance, the land lease Proclamation 721/2011 Article 35.1 proclaimed that a leaseholder may transfer his lease-holding rights or use them as collateral or capital contribution. However, according to the Ministry of Urban and Infrastructure, only 12 percent of 6 million estimated urban land parcels and properties will be registered in the legal cadaster by the end of 2022, which is one of the collateral requirements to access credit and asked by the financial institution in the processing credit application. This increases the financial market friction with that of rural and urban land market imperfection and negatively impacts the productivity of the smallholder households as an entrepreneur in the agricultural sector.

One of the ways to increase access to credit lies in improving or reforming secured transaction laws and registries. A sound legal framework and institutional arrangement, as well as a well-functioning and secured transaction system, enables business firms and individual proprietors to use the best available assets as security to guarantee capital. In this regard, secure land tenure and property rights founded on sound policy and regulatory frameworks are vital. The sound land policy clearly contains the forms (private, communal, public and/or state, and customary) and bundle (access, withdrawal, management, exclusion, and alienation) of land tenure and property rights [

45]. This, in turn, requires a clear and detailed legislative framework, including laws, regulations, and directives that specify the rights, restrictions, responsibilities, and institutional arrangements with definitive powers and accountabilities. In addition, the availability and accessibility of functional land registers with streamlined information service standards are the key enablers if the rural credit market should work for most smallholder households.

Recent policy and regulatory reforms at the regional state level in Ethiopia suggest a promising avenue for increasing the collateral capacity of smallholder households. Until 2017 in the Amhara region and 2019 at the federal government level by implication to other regions, there was no enabling policy and legal framework that promoted the collateralization of land rights to access credit. Hence, it was not a common practice across the country to pledge land rights as collateral for individual loans from financial institutions. However, the Amhara regional state amended the existing law and proclaimed new rural land administration, and used Proclamation number 252/2017. Article 16 of the same proclamation clarified and expanded landholders’ rights to include the use of land use rights as collateral for up to 30 years. Under this article, in the event of default, the landholder will not be evacuated from the land, but rather the financial institution will temporarily gain the right to use the land until it recovers the loan. This can be done either by leasing/renting the subject parcel of landholding to a third party or by another means, such as agricultural profits; the landholders shall regain their landholding rights.

The current study results revealed that 60 percent and 25 percent of households obtained credit from microfinance institutions and credit and saving cooperatives, respectively, between May 2019 and April 2021. This shows that microfinance and cooperatives of credit and saving have been the main source of finance for rural smallholder households. This may indicate that those institutions will continue dominating the rural credit market over the coming years. This result is consistent with the Ethiopian Economics Association findings in that the supply of credit by formal and semi-formal financial institutions accounts for 80 percent of the total amount channeled to the agricultural sector in Ethiopia [

46]. However, this may make sense where rural financial institutions can and do respond effectively to increased demand on the part of newly collateralized households [

47]. Alibhal et al. [

5] found in Ethiopia that only 13 percent of the total lending provided by formal financial institutions is directed to the agriculture sector, with most of this credit being channeled toward large-scale agricultural enterprises, meaning smallholder households are still credit constrained. This finding is consistent with Mukasa et al. [

2], who found that two-thirds of smallholder farmers in Ethiopia are credit constrained.

However, according to the key informants, some banks which have been operating as microfinance institutions are upgrading to commercial banks and being embraced the SLLC-linked loan product for smallholder households. This includes Sinqii Bank, Tseday Bank, and Omo Bank, which were upgraded from microfinance institutions to commercial banks in the past couple of years. According to the same key informant, the UK-financed Land Investment for Transformation (LIFT) program (run between 2014 and 2021) provided technical assistance to the federal and regional governments as well as microfinance institutions to develop and pilot an agricultural credit product tailored to small landholders that catalyzes the reform. This shows that the recently enforced policy change and regulatory reform facilitated the financial institutions feeling confident and willing to provide the SLLC-linked loan product for smallholder households at scale. According to the same key informants, this policy innovation removes unnecessary restrictions on creating collateral, leaving lenders uncertain about whether a credit agreement will be enforced by law. This emerging perception is consistent with findings in other countries by Mehnaz et al. [

48] in that businesses are not rationed out of the credit market because they lack assets to meet the (unnecessarily high) collateral requirements of banks and other lenders; instead, because the legal framework prevents them from using their assets to secure loans. Using registers data, Ali and Deininger [

7] also found similar results in Lesotho, where land and credit market activation is exclusively due to policy reforms. Similarly, Mehnaz et al. [

49] found that reforming the collateralization laws in Albania and Romania unlocked dead capital and increased access to finance, especially for small firms.

5.2. Whether Possession of Land Certificate Signals Credit-Worthiness

The land tenure literature suggests that land registration and certification programs enhance tenure security of land and resource rights which stimulates collateralization and increase the supply of credit [

30,

48]. Land registration becomes socially more valuable as more parcels are registered in the system because it leads to more investment and more transactions [

50,

51]. However, recent reviews of the evidence do not show a clear link between land certification and access to formal credit in developing economies [

14,

26]. Sanjak et al. [

52] suggest that the expectation that land formalization will increase farmers’ access to credit fails to consider other significant factors, including the farmer’s income levels, the availability of credit in the market, and borrowers’ business plans.

Up until the early 2000s, a large share of land in Ethiopia was undocumented and often insecure and hence could not be used as collateral. However, Ignacio [

35] found that the second-level landholding certificate (SLLC)-linked individual loan product increased over time compared to the predominantly group-lending arrangements. However, the findings of the current study results indicated that only 24 percent of households who obtained any credit used their land certificate as collateral, and most of them were from the informal credit market. Despite the critical mass of smallholder households receiving land certificates in highland Ethiopia, this finding is unsurprising given that there was no supporting legal framework that allowed the use of land as collateral before 2017. This is consistent with the findings of Cloudburst in 2016 [

17] in that SLLC may facilitate credit access by indicating that the loan will be used for agricultural purposes, validating livelihood and credit-worthiness, especially through alternative financing such as community-based lending and microfinancing in Ethiopia. It implies the need to have a clear legal framework and institutional infrastructures, including secured transaction systems such as collateral registries for movable and immovable assists and functional land registers. This leads us to the discussion on the role played by digital land registers in increasing the credit-worthiness of small landholders in the study areas and the willingness of financial institutions to supply more credit.

5.3. Whether Access to Digital Land Registers Signals Credit-Worthiness

Available evidence shows that based on well-defined land rights in a legal framework, low-cost access to reliable information on individual land rights reduces transaction costs and uncertainty that hinders the exchange, such as the use of land as collateral to secure credit [

16]. Likewise, making information accessible in the digital land registers may facilitate the credit market. The results of the current study revealed that perception of credit transaction risk is found to influence negatively and significantly the credit-worthiness of households with an average marginal effect of 27.8 percent due to the asymmetry of information, meaning one-fourth of household heads were found risk averse. This indicates that households perceive that lack of access to information from the land registers, which is the legal information bearer of their land right, may hinder their credit-worthiness. The current rural cadastral and land registers contain spatial information about parcels (location, area, and shape) and textual information related to the landholders’ particulars and the nature of rights, restrictions, and responsibilities. However, there is no information on landed properties such as houses and buildings which undermines the value and role of the land registers for land value assessment and appraisal of loan applications by lending institutions. Ethiopia’s rural cadastral system may get more traction use, such as by banks and insurance companies if it is further developed in line with what Bennett et al. [

53] envisioned as future cadaster and their roles in the ever-changing world.

Notwithstanding this, since 2020, access to information by the rightsholders about their legal rights from woreda digital land registers has improved when the need arises to process credit applications. Abab et al. [

23] found that all mortgages or credit transactions had been registered in the digital land registers in Basona worena woreda of Ethiopia, where the system has been up and running since 2019. Results from the digital land registers of the current study show that the total number of households who received SLLC-linked credits was 10,789 with a credit value of 8 million US dollars equivalent, although only 3% of smallholder households obtained this volume of credit in the study kebeles. Figure from key informant interviews also shows that the volume of SLLC-linked loans increased and reached over 80 million US dollars were disbursed to over 50,000 rural small landholders over the past couple of years. This should not be underestimated by any measure, given that the digital registers have been fully operational only starting in 2020. This clearly indicates that the role played by access to the digital land register signaling the credit-worthiness of small landholders was found encouraging. Deininger and Goyal [

16] found similar results in India in that computerization of the land registers reduces the cost associated with keeping the land register up to date, eliminates informal side payments that have traditionally been associated with property rights registration, and improves third-party access to information in the registers as well as increases credit volume.

5.4. Monitoring and Enforcement Costs and Risks of Credit Agreement

The existing literature suggests that credit transaction costs consist of the costs of measuring the valuable attributes of a right, the costs of protecting rights and enforcing contracts [

32,

34,

38]. During the credit evaluation process, the primary focus of the lending financial institutions of smallholder households is whether an applicant has secured land rights that are registered in the land registers.

According to the key informants, procedurally, the Woreda Land Offices are the legal custodian of the digital land registers and provide each credit applicant of small landholder with a “blocking letter”. The blocking letter attests that the landholder who possesses an SLLC applies for individual credit and is free from third-party interest, including those not already being used as collateral for previous credit. The small landholder applies to lend to financial institutions with supporting documents, including a copy of the SLLC and business plan demonstrating their capacity. The lending financial institution reviews their application and requests the Woreda Land Office to ensure that the SLLC is registered in the land register, only pledged once, and registers the mortgage deed on the subject parcel of landholding as collateral once the credit is approved to the applicant. The applicants should also pledge their original SLLC upon approval of the credit application to the lender’s financial institution.

Based on the agreed payment schedule, the borrower is expected to repay the credit. In case of a default, the lending financial institution has the right to reclaim the land use rights of the subject parcels as a lien according to the agreed terms in the mortgage contract or until it recovers its credit amount, including the principal and interest. Recovering the defaulted credit can be collected by renting out the subject parcels to the same landholder as agricultural profits or any other potential tenant. Once the lending financial institution fully recovered the loan amount and interest, the lender writes a letter of mortgage cancellation to the pertinent Woreda Land Office. The lending financial institution also hands back the SLLC to the borrower. The Woreda Land Office updates the record in the digital land register by canceling the mortgage information registered on the subject parcel. According to the key informants, both the lending financial institutions and landholders have access to information about the legal status of the subject parcels without any service fee. This free-of-charge land information service is provided since this transaction type was recently introduced as one of the Woreda Land Office services. This may help increase the volume of registered credit transactions in the digital land register. However, if the land administration service needs to be sustainable, the Woreda Land Offices should consider reasonable service changes to the registration of mortgages in the digital land registers.

On the other hand, the establishment and operationalization of a movable collateral registry system were enacted by law. Part four of Proclamation No. 1147/2019 stipulates a collateral registry, including the establishment of the collateral registry office (Article 20) and the collateral registry (Article 21), grantor’s authorization for registration of security rights (Article 22), and public access of the collateral registry (Article 24), among others. Additionally, in 2020, the National Bank of Ethiopia (NBE) adopted two directives that helped to materialize the implementation of this proclamation. The first one is directive number 186/2020 which stipulates the codification, valuation, and registration of movable properties, including land use rights. Directive number 186/2020 Article 7 sub-Articles 1 to 5 stipulate the land use rights codification, valuation, and registration. The second directive number MCR/01/2020, focuses on the operationalization of a movable collateral registry, which is an electronic registry system established for receiving, storing, and making information available and accessible to the public about the security of rights and non-consensual rights in movable properties (Article 2.2). However, there is no clear plan for the establishment and operationalization of a secured electronic movable collateral registry system and how this new system interface with the existing systems such as NRLAIS.

6. Conclusions

This study assessed the policy and technological innovation of land tenure on the credit-worthiness of the smallholder households in three highland regional states (Amhara, Oromia, and SNNP) in Ethiopia, who have often been credit constrained. The study explored the differential effects of access to information from the digital land registry on improving the credit-worthiness of the smallholder households in the study areas from that of the two-stage land certification program in the country. Additionally, the study contributed to an important assumption yet controversial argument in much literature in the field regarding land titling alone would lead to more credit access. The study tests the extent to which this is valid and identifies the needed requirements which make this argument valid or not. This was possible by employing quantitative data analysis generated from the digital land register or NRLAIS and the 2021 USAID impact evaluation household survey data complemented with key informant interviews and policy and legal document reviews. This approach also allows for identifying the effect of policy and regulatory reforms on the credit-worthiness of small landholders. The approach yielded to fill the knowledge gap on how reforming secure transaction laws and registers increases the credit-worthiness of smallholder households, reduces credit transaction costs and risks, and increases the willingness of financial institutions to provide credits to smallholder households.

These reforms represent a paradigm shift from the previous approach and allow rural smallholder households to access the capital required to move from subsistence farming to more productive, sustainable land use practices, commercial farming, and the development of the non-farm economy. The study concludes that while the two-stage land certification programs allow smallholders to possess documented land rights and increase the value of land, their credit-worthiness may likely remain negligible without such further technological and policy innovations. This implies two policy implications, including land tenure improvement interventions such as land registration and certification, need to be supported with reforming secure transaction law and digitalization of land registers for higher level land rights trade ability such as functional credit and land market. Based on the findings, the study recommends that policymakers and practitioners in the land sector should strengthen their efforts to raise the awareness and financial literacy of smallholder households as well as streamline procedures and service fee structures of mortgage registration.

While the enactment of Proclamation No. 1147/2019 and its implementing directives are welcoming policy actions, the current study did not assess the implementation effectiveness of this policy from the credit supply side, i.e., financial institution and enforcement mechanism. Future research should look at this dimension, particularly the establishment and operationalization of the movable collateral registry system and its interoperability with the digital land registers and their effect on the national economy.

{kind=link}

{kind=link}