The Linkage between Carbon Market and Green Bond Market: Evidence from Quantile Regression Based on Wavelet Analysis

Abstract

:1. Introduction

2. Data and Research Methods

2.1. Variable Selection and Data Source

2.1.1. Green Bond Market (GBM)

2.1.2. Carbon Market (CM)

2.1.3. Data Source

2.2. Research Methods

2.2.1. Maximum Overlapping Discrete Wavelet Transform

2.2.2. Quantile Autoregression (QAR) Unit Root Test

2.2.3. Quantile Granger Causality Test

2.2.4. Quantile-to-Quantile Regression

3. Results Analysis

3.1. Descriptive Statistics

3.2. Quantile Autoregression (QAR) Unit Root Test

4. Analysis of Maximum Overlapping Discrete Wavelet Transform

5. Quantile Granger Causality Inference

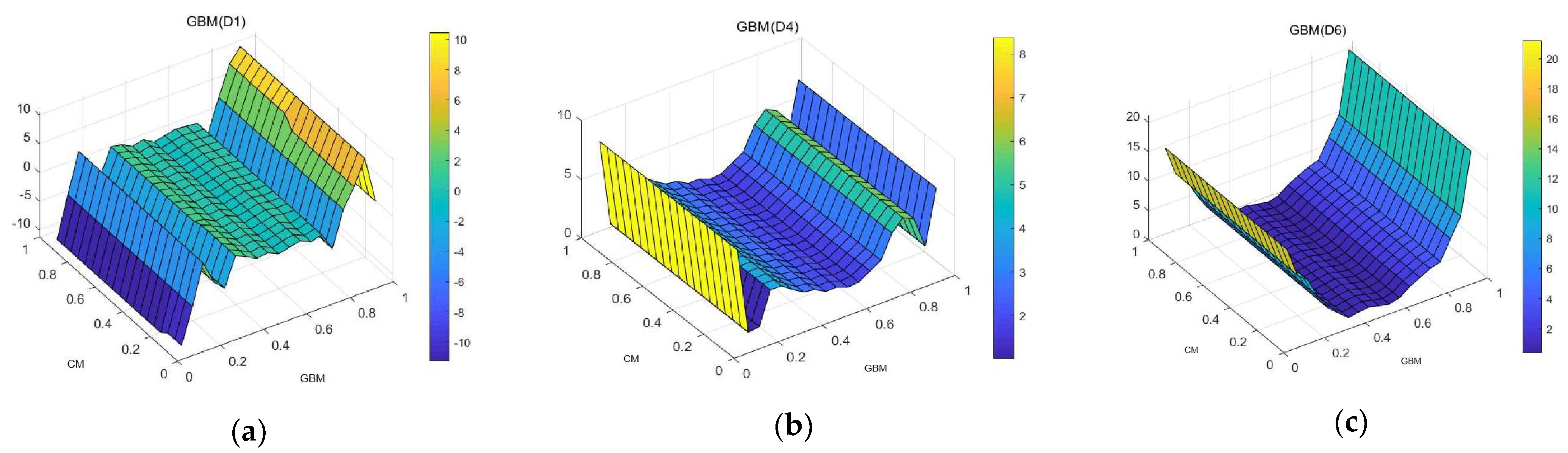

6. Quantile-to-Quantile Regression Results

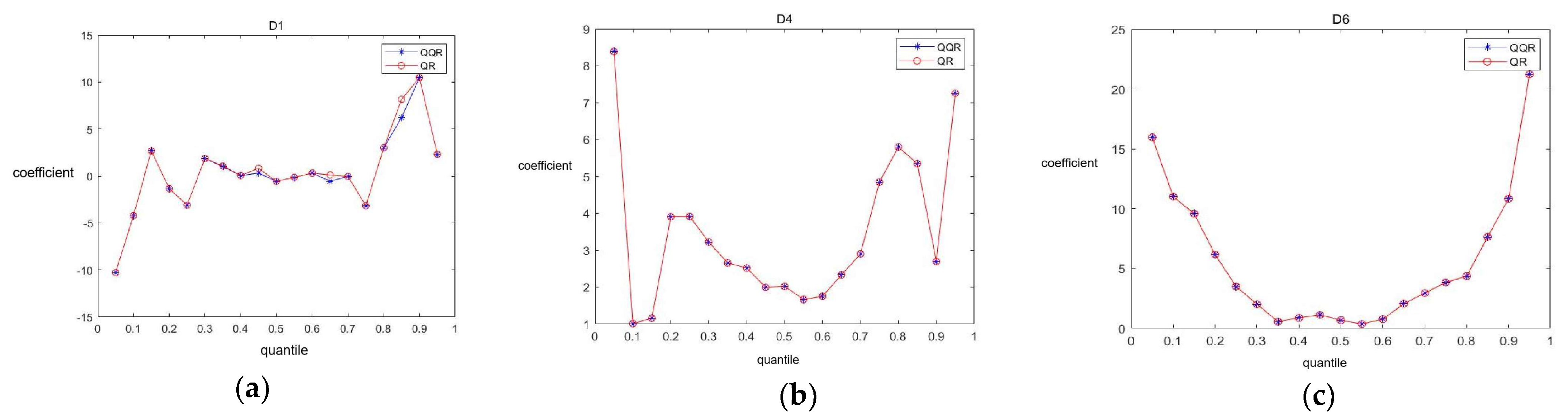

7. Robustness Test

7.1. OLS Regression

7.2. Comparison of Regression Coefficient between QQR and QR

8. Conclusions and Suggestions

9. Limitations and Future Research

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Palao, F.; Pardo, A. Assessing price clustering in European carbon markets. Appl. Energy 2012, 92, 51–56. [Google Scholar] [CrossRef]

- Liu, M. The driving forces of green bond market volatility and the response of the market to the COVID-19 pandemic. Econ. Anal. Policy 2022, 75, 288–309. [Google Scholar] [CrossRef]

- Lin, B.; Huang, C. Analysis of emission reduction effects of carbon trading: Market mechanism or government intervention? Sustain. Prod. Consum. 2022, 33, 28–37. [Google Scholar] [CrossRef]

- Flammer, C. Corporate green bonds. J. Financ. Econ. 2021, 142, 499–516. [Google Scholar] [CrossRef]

- Reboredo, J.C. Green bond and financial markets: Co-movement, diversification and price spillover effects. Energy Econ. 2018, 74, 38–50. [Google Scholar] [CrossRef]

- Pham, L. Frequency connectedness and cross-quantile dependence between green bond and green equity markets. Energy Econ. 2021, 98, 105257. [Google Scholar] [CrossRef]

- Fan, Y.; Jia, J.-J.; Wang, X.; Xu, J.-H. What policy adjustments in the EU ETS truly affected the carbon prices? Energy Policy 2017, 103, 145–164. [Google Scholar] [CrossRef]

- Ren, X.; Dou, Y.; Dong, K.; Li, Y. Information spillover and market connectedness: Multi-scale quantile-on-quantile analysis of the crude oil and carbon markets. Appl. Econ. 2022, 54, 4465–4485. [Google Scholar] [CrossRef]

- Mansanet-Bataller, M.; Soriano, P. Volatility transmission in the CO2 and energy markets. In Proceedings of the 6th International Conference on the European Energy Market, Leuven, Belgium, 27–29 May 2009; pp. 1–7. [Google Scholar]

- Chen, Y.; Qu, F.; Li, W.; Chen, M. Volatility spillover and dynamic correlation between the carbon market and energy markets. J. Bus. Econ. Manag. 2019, 20, 979–999. [Google Scholar] [CrossRef] [Green Version]

- Reboredo, J.C. Volatility spillovers between the oil market and the European Union carbon emission market. Econ. Model. 2014, 36, 229–234. [Google Scholar] [CrossRef]

- Mol, A.P.J. Carbon flows, financial markets and climate change mitigation. Environ. Dev. 2012, 1, 10–24. [Google Scholar] [CrossRef]

- Liu, Z.; Zhang, Y.-X. Assessing the maturity of China’s seven carbon trading pilots. Adv. Clim. Chang. Res. 2019, 10, 150–157. [Google Scholar] [CrossRef]

- Lin, B.; Chen, Y. Carbon price in China: A CO2 abatement cost of wind power perspective. Emerg. Mark. Financ. Trade 2018, 54, 1653–1671. [Google Scholar] [CrossRef]

- Fan, X.; Li, X.; Yin, J.; Tian, L.; Liang, J. Similarity and heterogeneity of price dynamics across China’s regional carbon markets: A visibility graph network approach. Appl. Energy 2019, 235, 739–746. [Google Scholar] [CrossRef]

- Das, D.; Kannadhasan, M. Do global factors impact bitcoin prices? Evidence from wavelet approach. J. Econ. Res. 2018, 23, 227–264. [Google Scholar]

- Mishra, S.; Sharif, A.; Khuntia, S.; Meo, M.S.; Khan, S.A.R. Does oil prices impede Islamic stock indices? Fresh insights from wavelet-based quantile-on-quantile approach. Resour. Policy 2019, 62, 292–304. [Google Scholar] [CrossRef]

- Koenker, R.; Xiao, Z. Unit root quantile autoregression inference. J. Am. Stat. Assoc. 2004, 99, 775–787. [Google Scholar] [CrossRef] [Green Version]

- Galvao, A.F., Jr. Unit root quantile autoregression testing using covariates. J. Econom. 2009, 152, 165–178. [Google Scholar] [CrossRef]

- Jeong, K.; Härdle, W.K.; Song, S. A consistent nonparametric test for causality in quantile. Econom. Theory 2012, 28, 861–887. [Google Scholar] [CrossRef] [Green Version]

- Troster, V. Testing for Granger-causality in quantiles. Econom. Rev. 2018, 37, 850–866. [Google Scholar] [CrossRef]

- Sim, N.; Zhou, H. Oil prices, US stock return, and the dependence between their quantiles. J. Bank. Financ. 2015, 55, 1–8. [Google Scholar] [CrossRef]

- Ren, X.; Lu, Z.; Cheng, C.; Shi, Y.; Shen, J. On dynamic linkages of the state natural gas markets in the USA: Evidence from an empirical spatio-temporal network quantile analysis. Energy Econ. 2019, 80, 234–252. [Google Scholar] [CrossRef]

- Wen, F.; Shui, A.; Cheng, Y.; Gong, X. Monetary policy uncertainty and stock returns in G7 and BRICS countries: A quantile-on-quantile approach. Int. Rev. Econ. Financ. 2022, 78, 457–482. [Google Scholar] [CrossRef]

- Mensi, W.; Hammoudeh, S.; Tiwari, A.K. New evidence on hedges and safe havens for Gulf stock markets using the wavelet-based quantile. Emerg. Mark. Rev. 2016, 28, 155–183. [Google Scholar] [CrossRef]

- Selmi, R.; Mensi, W.; Hammoudeh, S.; Bouoiyour, J. Is Bitcoin a hedge, a safe haven or a diversifier for oil price movements? A comparison with gold. Energy Econ. 2018, 74, 787–801. [Google Scholar] [CrossRef]

- Rannou, Y.; Boutabba, M.A.; Barneto, P. Are Green Bond and Carbon Markets in Europe complements or substitutes? Insights from the activity of power firms. Energy Econ. 2021, 104, 105651. [Google Scholar] [CrossRef]

- Ahmad, M.; Ahmed, Z.; Khan, S.A.; Alvarado, R. Towards environmental sustainability in E−7 countries: Assessing the roles of natural resources, economic growth, country risk, and energy transition. Resour. Policy 2023, 82, 103486. [Google Scholar] [CrossRef]

- Ahmad, M.; Ahmed, Z.; Yang, X.; Can, M. Natural Resources Depletion, Financial Risk, and Human Well-Being: What is the Role of Green Innovation and Economic Globalization? Soc. Indic. Res. 2023, 167, 269–288. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| CM | GBM | |

|---|---|---|

| Obs | 1808 | 1808 |

| Mean | 0.0004 | 0.0003 |

| Minimum | −1.891 | −0.008 |

| 25% quantile | −0.066 | −0.0001 |

| 75% quantile | 0.068 | 0.0006 |

| Maximum | 1.964 | 0.193 |

| Std.Dev | 0.204 | 0.001 |

| Skewness | 0.339 | 2.411 |

| Kurtosis | 27.954 | 52.174 |

| Jarque–Bera test | 46,943.147 *** | 183,916.170 *** |

| GBM | CM | |||||

|---|---|---|---|---|---|---|

| Quantile | T-Value | CV | T-Value | CV | ||

| 0.05 | 0.297 | −7.093 | −3.279 | −0.367 | −14.301 | −2.310 |

| 0.1 | 0.371 | −15.273 | −3.317 | −0.351 | −31.837 | −2.553 |

| 0.15 | 0.368 | −22.250 | −3.355 | −0.307 | −49.3862 | −2.468 |

| 0.20 | 0.380 | −30.440 | −3.401 | −0.275 | −60.670 | −2.638 |

| 0.25 | 0.375 | −34.513 | −3.337 | −0.265 | −66.040 | −2.732 |

| 0.30 | 0.370 | −39.352 | −3.327 | −0.258 | −72.014 | −2.832 |

| 0.35 | 0.374 | −42.826 | −3.269 | −0.250 | −75.923 | −2.847 |

| 0.40 | 0.382 | −43.830 | −3.272 | −0.262 | −80.462 | −2.927 |

| 0.45 | 0.382 | −46.104 | −3.237 | −0.267 | −85.669 | −2.896 |

| 0.50 | 0.386 | −46.3145 | −3.287 | −0.252 | −86.437 | −2.852 |

| 0.55 | 0.402 | −45.566 | −3.238 | −0.255 | −88.133 | −2.801 |

| 0.60 | 0.408 | −42.313 | −3.193 | −0.271 | −93.759 | −2.760 |

| 0.65 | 0.420 | −38.819 | −3.116 | −0.265 | −84.966 | −2.757 |

| 0.70 | 0.435 | −32.769 | −3.074 | −0.262 | −80.750 | −2.582 |

| 0.75 | 0.434 | −29.072 | −3.046 | −0.250 | −71.484 | −2.510 |

| 0.80 | 0.409 | −26.190 | −2.971 | −0.279 | −60.926 | −2.310 |

| 0.85 | 0.406 | −21.589 | −2.922 | −0.309 | −44.966 | −2.310 |

| 0.90 | 0.431 | −15.227 | −2.755 | −0.333 | −29.725 | −2.310 |

| 0.95 | 0.382 | −7.128 | −2.486 | −0.424 | −16.049 | −2.510 |

| Short-Term | Medium-Term | Long-Term | |

|---|---|---|---|

| CM | CM | CM | |

| GBM | −3.193 | 3.112 ** | 6.665 *** |

| (−0.50) | (2.16) | (7.75) | |

| _cons | −0.000 | 0.000 | 0.000 |

| (−0.00) | (0.00) | (0.00) | |

| N | 1808 | 1808 | 1808 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Wu, D.; Luo, Z.; Zhang, T.; Tang, L.; Ahmad, M.; Fang, X. The Linkage between Carbon Market and Green Bond Market: Evidence from Quantile Regression Based on Wavelet Analysis. Sustainability 2023, 15, 10634. https://doi.org/10.3390/su151310634

Wu D, Luo Z, Zhang T, Tang L, Ahmad M, Fang X. The Linkage between Carbon Market and Green Bond Market: Evidence from Quantile Regression Based on Wavelet Analysis. Sustainability. 2023; 15(13):10634. https://doi.org/10.3390/su151310634

Chicago/Turabian StyleWu, Ding, Zhenqing Luo, Tidong Zhang, Lu Tang, Mahmood Ahmad, and Xiaoyun Fang. 2023. "The Linkage between Carbon Market and Green Bond Market: Evidence from Quantile Regression Based on Wavelet Analysis" Sustainability 15, no. 13: 10634. https://doi.org/10.3390/su151310634