Forecasting Monthly Prices of Japanese Logs

Abstract

:1. Introduction

2. Materials and Methods

2.1. Study Objects and Their Data

2.2. Methods

2.2.1. Naïve Method and Snaïve Method

2.2.2. ETS

2.2.3. ARIMA

2.2.4. Forecasting Intervals

2.2.5. Measures of Forecasting Accuracy

3. Results

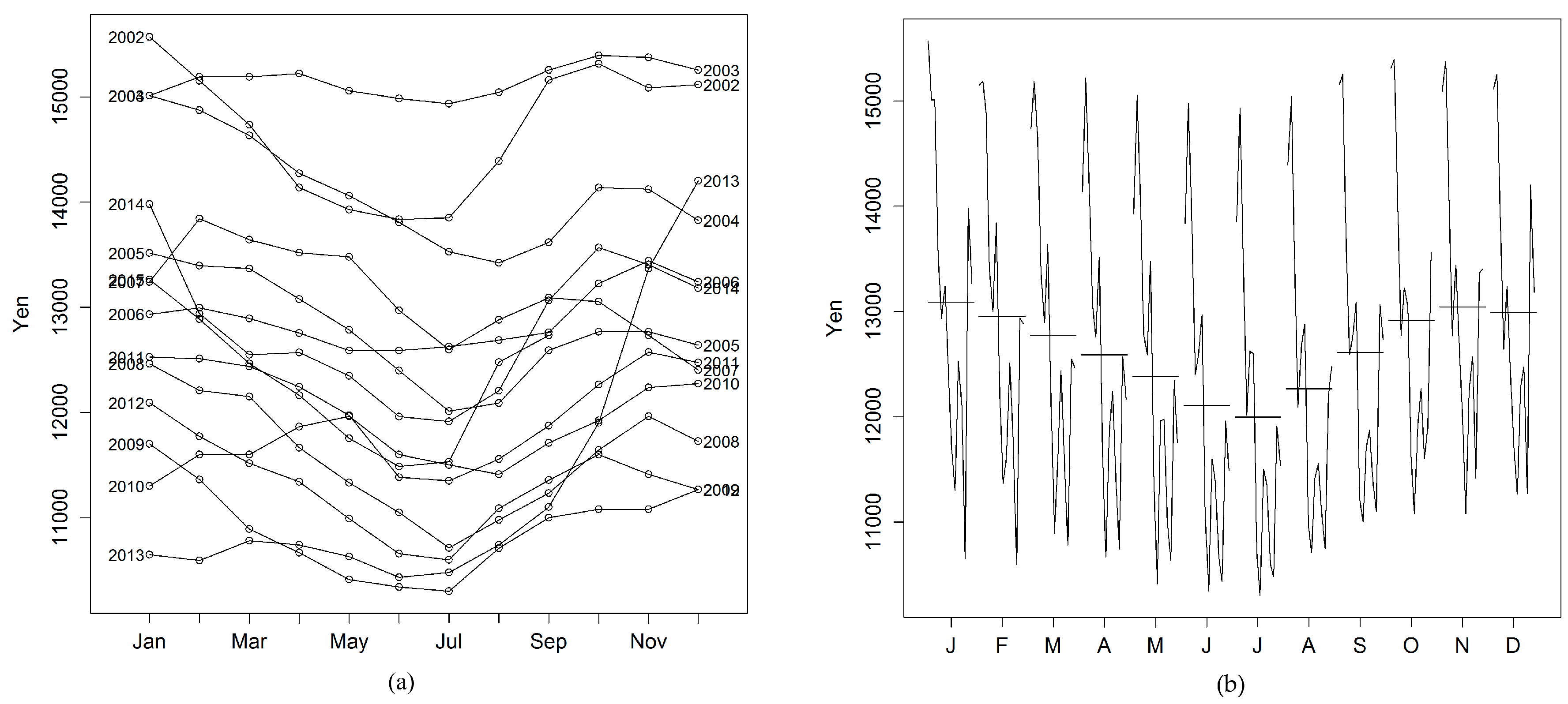

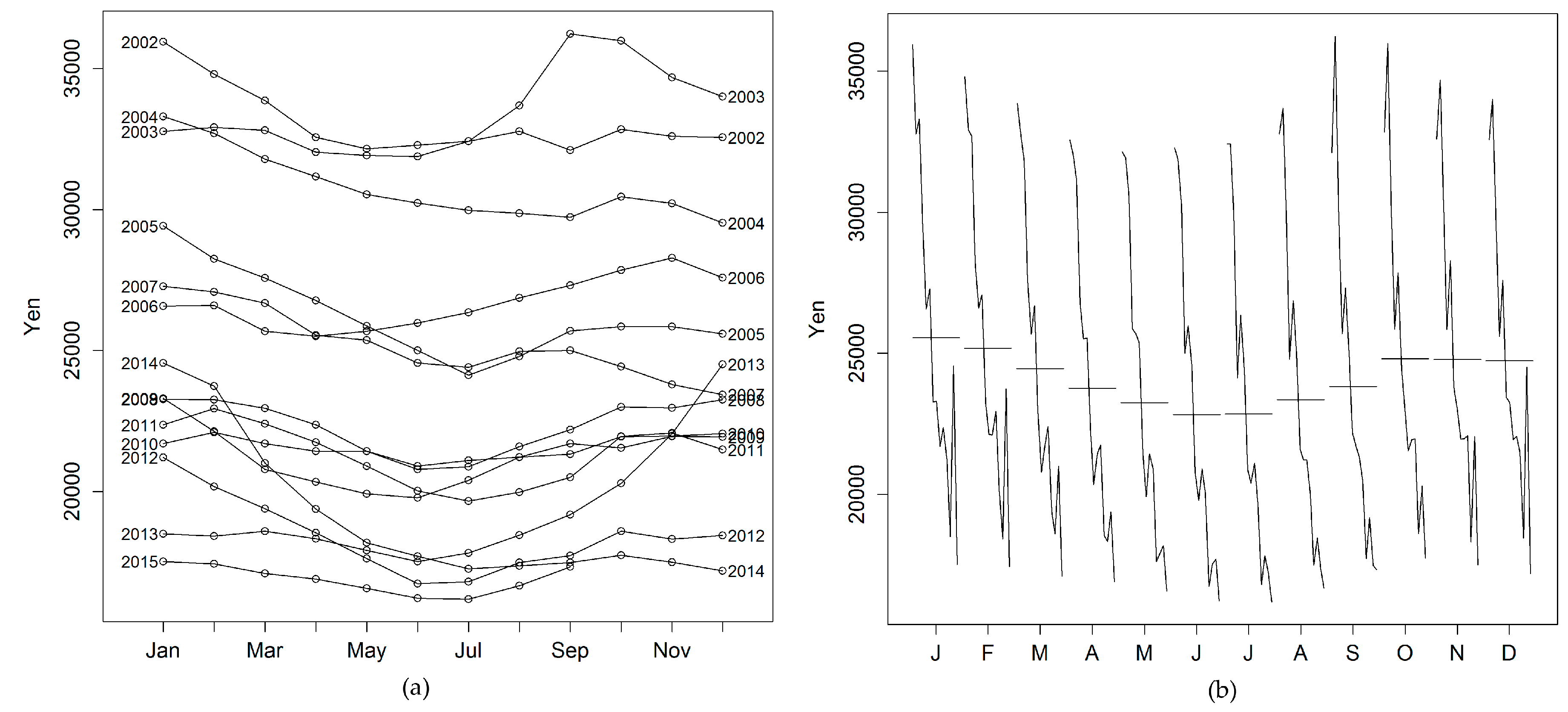

3.1. Seasonal Characteristics

3.2. Trend and Cycles

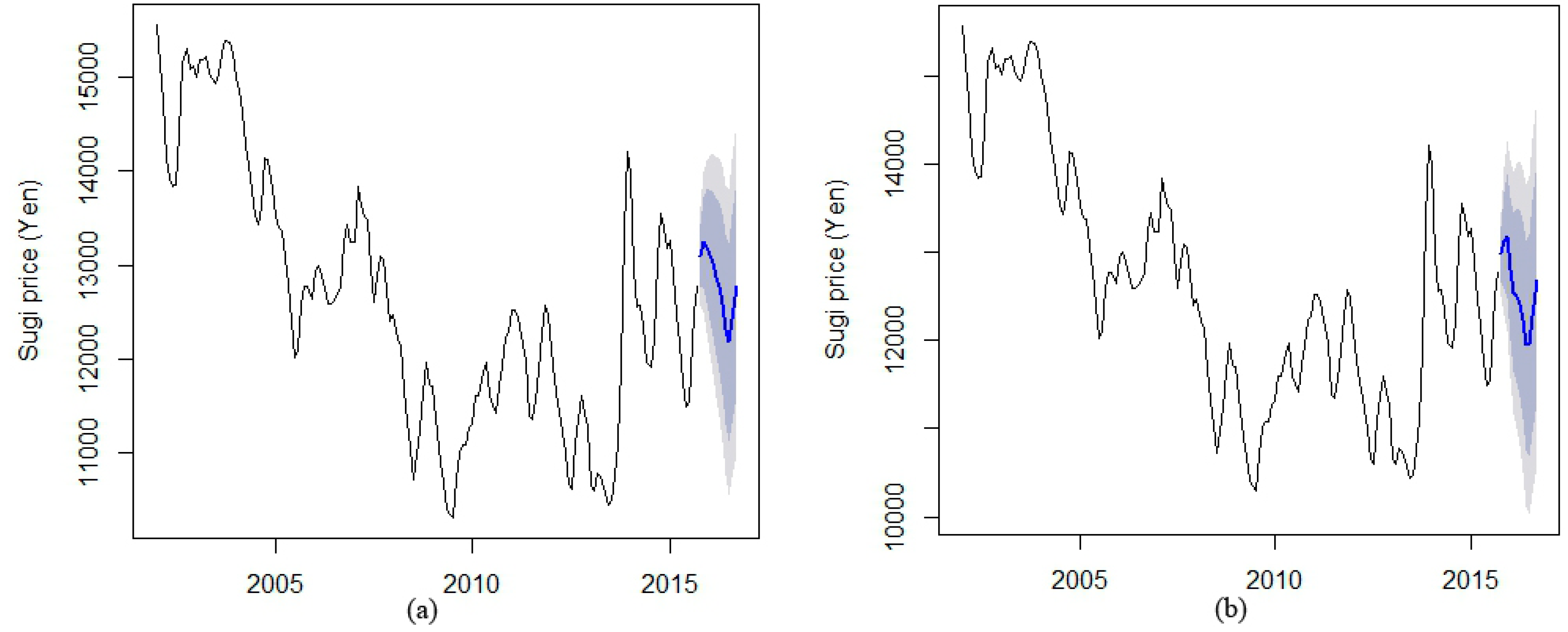

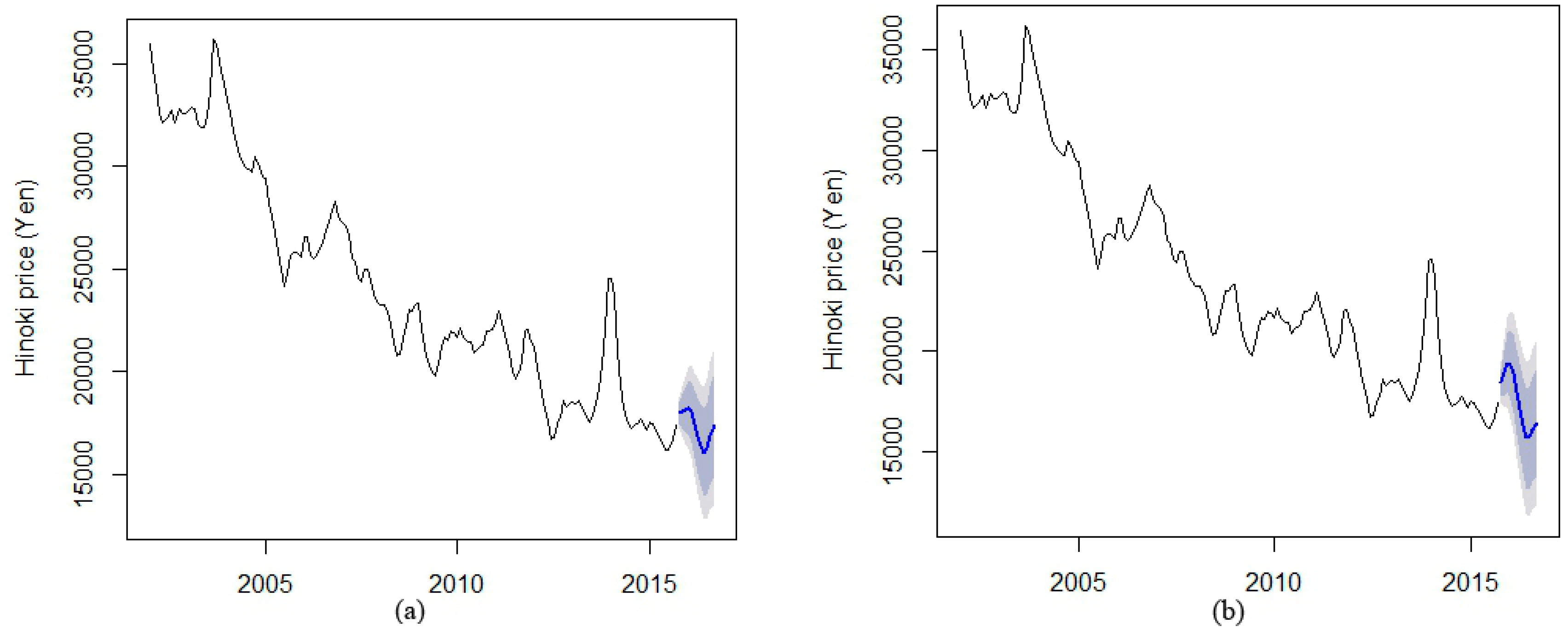

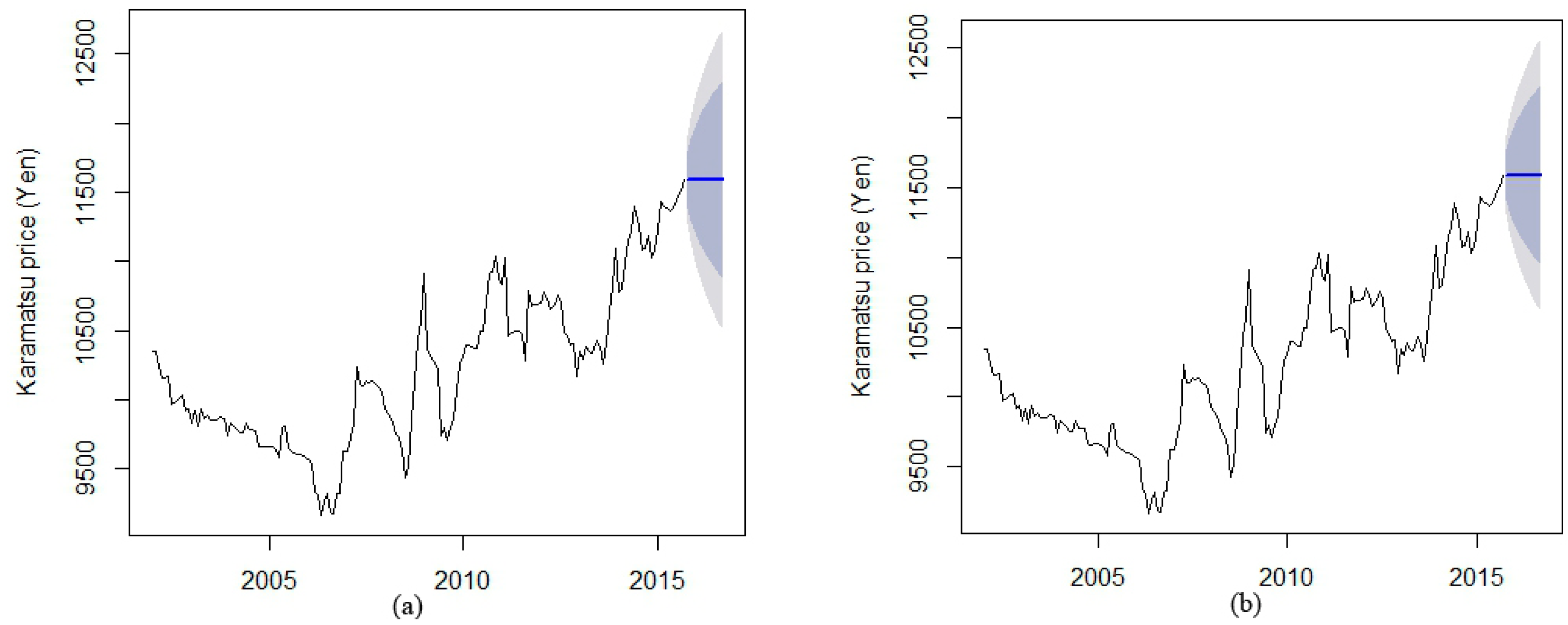

3.3. ETS Forecast Results

3.4. ARIMA Forecast Results

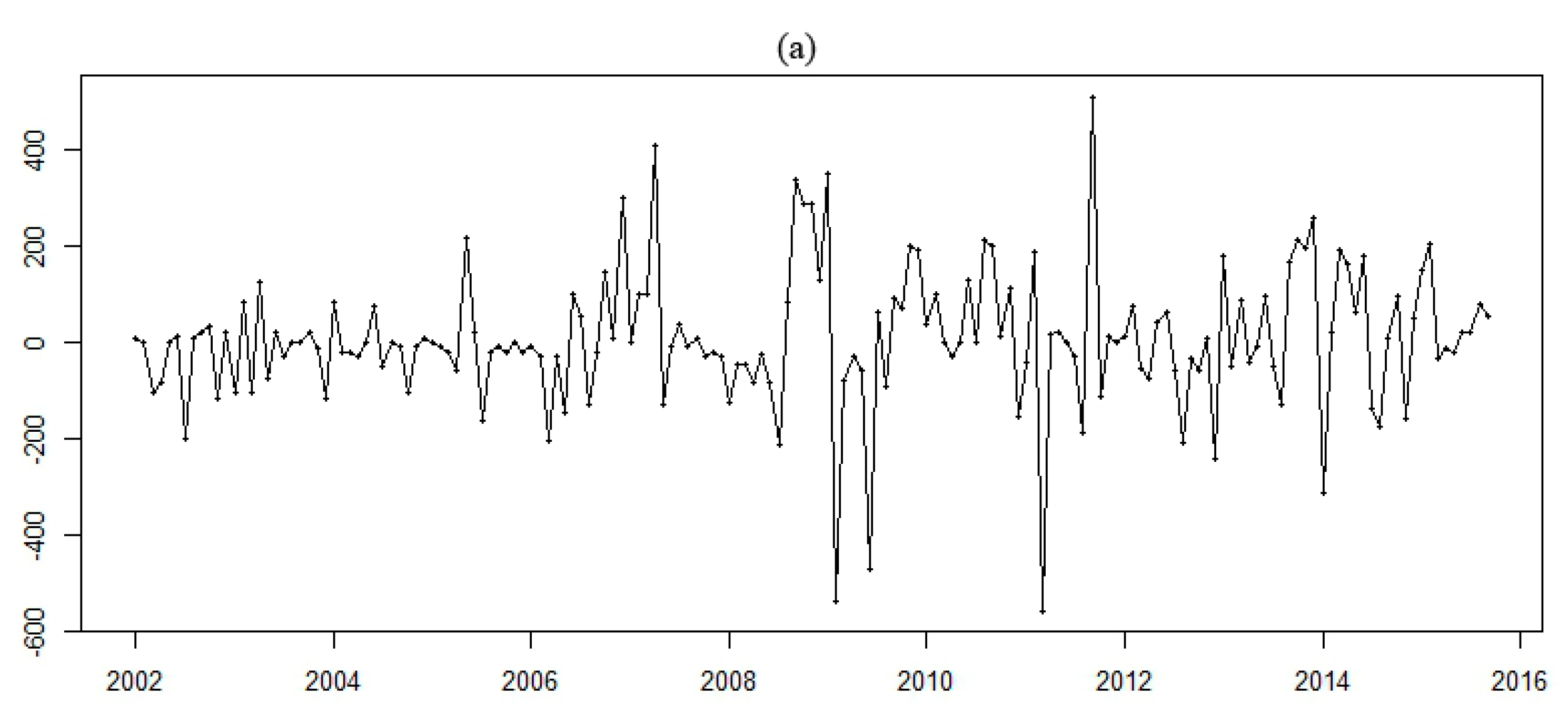

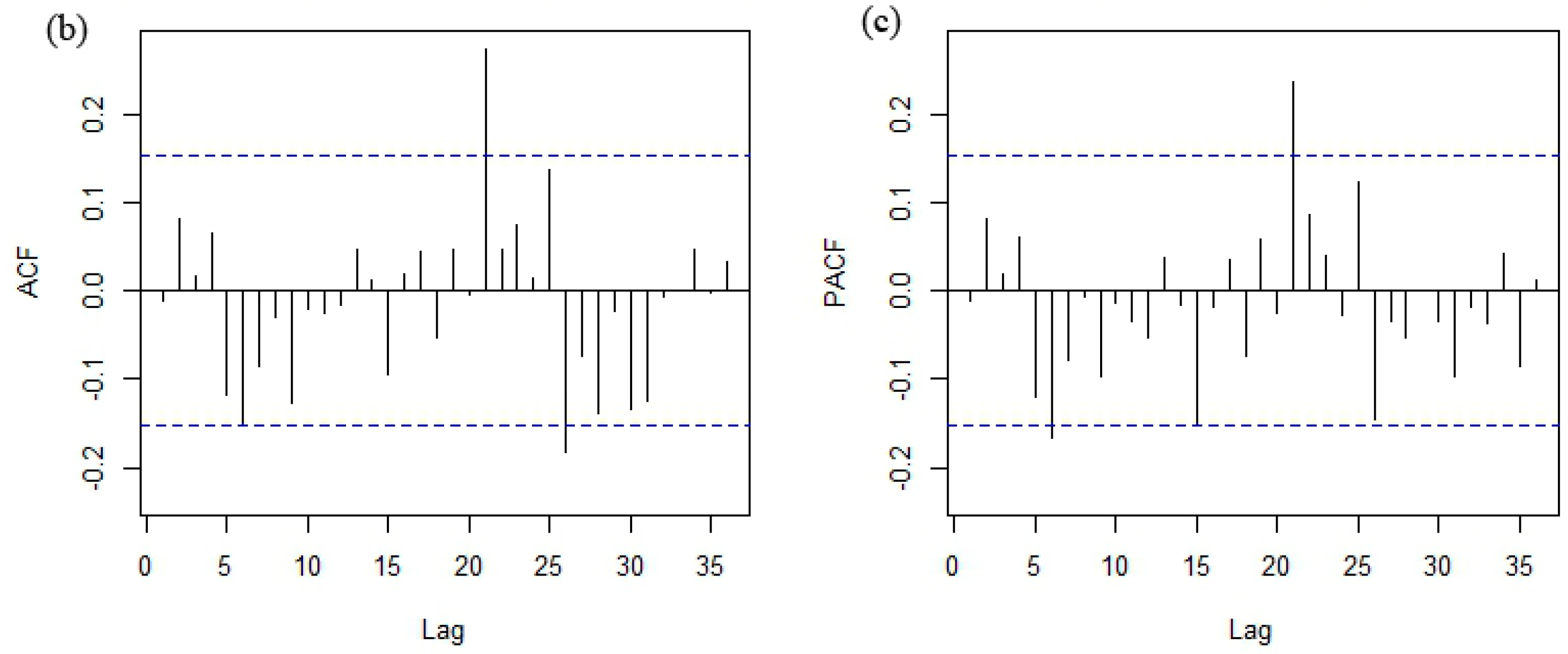

3.5. Diagnostic Check of Residuals in ARIMA Models

3.6. Measuring the Accuracy of Forecasts

4. Discussion

Supplementary Materials

Acknowledgments

Author Contributions

Conflicts of Interest

References

- Endo, K. Why Log Prices Collapsed: Reasons, Mechanism and Measures; National Forestry Extension Association: Tokyo, Japan, 2013; p. 144. [Google Scholar]

- Mochizuki, R. A statistical study on fluctuations in prices of main forest products. Bull. Tokyo Imp. Univ. For. 1929, 7, 1–121. [Google Scholar]

- Mitsui, T. On seasonal movements of timber prices. In Forestry Economic and Policy Materials; The Japan Forestry Association: Tokyo, Japan, 1938; Volume 3, pp. 43–56. [Google Scholar]

- Shindo, R. The Future of the Wood Market and Industry; Price Agency: Tokyo, Japan, 1949; p. 221. [Google Scholar]

- Akai, H. Research on Trend of Timber Prices; Bulletin of Forestry Management Institute: Tokyo, Japan, 1965; Volume 63, p. 302. [Google Scholar]

- Matsumoto, K. Research on Cyclic Fluctuations of Timber Prices; Bulletin of Forestry Management Institute: Tokyo, Japan, 1966; Volume 63, p. 92. [Google Scholar]

- Mori, Y. A Study on the Time-Series-Analysis of Lumber Price in Japan. J. Jpn. For. Soc. 1970, 52, 227–237. [Google Scholar]

- Matsushita, K. Applications of spectral analysis to the cyclical fluctuations of lumber prices. Trans. Jpn. For. Soc. 1984, 95, 17–18. [Google Scholar]

- Matsushita, K.; Handa, R. The cyclical fluctuation of lumber price. Bull. Kyoto Univ. For. 1981, 53, 76–86. [Google Scholar]

- Yukutake, K. Time series analysis of timber price fluctuation after World War II. The Current State of Japanese Forestry. In Proceedings of the IUFRO World Congress, Kyoto, Japan, 6–17 September 1981; Volume 1, pp. 41–54.

- Yukutake, K.; Yoshimoto, A.; Higuchi, Y. Time series analysis of timber prices at two private auction markets in Kyushu Japan. Jpn. J. For. Plan. 2004, 38, 61–74. [Google Scholar]

- Kuboyama, H.; Tachibana, S. Statistical analysis on price trend of softwood roundwood. Kanto J. For. Res. 2014, 65, 9–12. [Google Scholar]

- Elias, R.J.; Montgomery, D.C.; Kulahci, M. An overview of short-term statistical forecasting methods. Int. J. Manag. Sci. Eng. Manag. 2006, 1, 17–36. [Google Scholar]

- Makridakis, P.; Wheelwright, S.C.; Hyndman, R.J. Foresting: Methods and Applications, 3rd ed.; Wiley: New York, NY, USA, 1998; p. 656. [Google Scholar]

- Hyndman, R.J.; Koehler, A.B.; Ord, J.K.; Synder, R.D. Forecasting with Exponential Smoothing: The State Space Approach; Springer: Berlin, Germany, 2008; p. 359. [Google Scholar]

- R Core Team. R: A Language and Environment for Statistical Computing. R Foundation for Statistical Computing, Vienna, Austria. Available online: http://www.R-project.org/ (accessed on 2 February 2015).

- Hyndman, R.J. Forecasting Functions for Time Series and Linear Models. Available online: http://github.com/robjhyndman/forecast (accessed on 25 October 2015).

- Forestry Agency. Statistical Handbook of Forest and Forestry; Forestry Agency, Ministry of Agriculture, Forestry and Fisheries: Tokyo, Japan, 2013; p. 262. [Google Scholar]

- Forestry Agency. Balance Sheet of Wood. Available online: http://www.rinya.maff.go.jp/j/press/kikaku/pdf/150929-02.pdf (accessed on 5 December 2015).

- MAFF. Ministry of Agriculture, Forestry and Fisheries. Available online: http://www.maff.go.jp/j/tokei/kouhyou/kensaku/bunya5.html (accessed on 15 October 2015).

- Findley, D.F.; Monsell, B.C.; Bell, W.R.; Otto, M.C.; Chen, B.C. New Capabilities and methods of the X-12-ARIMA seasonal-adjustment Program. J. Bus. Econ. Stat. 1998, 16, 127–152. [Google Scholar] [CrossRef]

- Makridakis, S.; Hibon, M. The M3-Competition: Results, conclusions and implications. Int. J. Forecast. 2000, 16, 451–476. [Google Scholar] [CrossRef]

- Hyndman, R.J.; Koehler, A.B.; Snyder, R.D.; Grose, S. A state space framework for automatic forecasting using exponential smoothing methods. Int. J. Forecast. 2002, 18, 439–454. [Google Scholar] [CrossRef]

- Sanders, D.R.; Manfredo, M.R. USDA livestock price forecasts: A comprehensive evaluation. J. Agric. Resour. Econ. 2003, 28, 316–334. [Google Scholar]

- Sanders, D.R.; Manfredo, M.R. Rationality of U.S. Department of Agriculture Livestock price forecasts: A unified approach. J. Agric. Appl. Econ. 2007, 39, 75–85. [Google Scholar]

- Gelper, S.; Fried, R.; Croux, C. Robust forecasting with exponential and Holt-Winters smoothing. J. Forecast. 2010, 29, 285–300. [Google Scholar] [CrossRef]

- Hassani, H.; Silva, S.S.; Gupta, R.; Segnon, M.K. Forecasting the price of gold. Appl. Econ. 2015, 47, 4141–4152. [Google Scholar] [CrossRef]

- Guttormsen, A.G. Forecasting weekly salmon prices: Risk management in fish farming. Aquac. Econ. Manag. 1999, 3, 159–166. [Google Scholar] [CrossRef]

- Holt, C.C. Forecasting seasonals and trends by exponentially weighted moving averages (a reprinted version). Int. J. Forecast. 2004, 20, 5–10. [Google Scholar] [CrossRef]

- Brown, R.G. Statistical Forecasting for Inventory Control; McGraw/Hill: New York, NY, USA, 1959; p. 223. [Google Scholar]

- Winters, P.R. Forecasting Sales by Exponentially Weighted Moving Averages. Manag. Sci. 1960, 6, 324–342. [Google Scholar] [CrossRef]

- Hyndman, R.J.; Athanasopoulos, G. Forecasting: Principles and Practice. Available online: http://otexts.org/fpp/ (accessed on 10 September 2015).

- Burnham, K.P.; Anderson, D.R. Model Selection and Multimodel Inference: A Practical Information-Theoretic Approach, 2nd ed.; Springer-Verlag: Berlin, Germany, 2002; p. 488. [Google Scholar]

- Hamilton, J.D. Time Series Analysis; Princeton University Press: Princeton, NJ, USA, 1994; p. 799. [Google Scholar]

- Harvey, A.C. Forecasting, Structural Time Series and the Kalman Filter; Cambridge University Press: Cambridge, UK, 1989; p. 554. [Google Scholar]

- Said, S.E.; Dickey, D.A. Testing for unit roots in autoregressive-Moving Average Models of Unknown Order. Biometrika 1984, 71, 599–607. [Google Scholar] [CrossRef]

- Trapletti, A.; Hornik, K.; LeBaron, B. Time Series Analysis and Computational Finance. Package “tseries” in R. Available online: https://cran.r-project.org/web/packages/tseries/tseries.pdf (accessed on 10 December 2015).

- Ljung, G.; Box, G. On a measure of lack of fit in Time Series Models. Biometrika 1978, 65, 297–303. [Google Scholar] [CrossRef]

- Zamani, M. An econometrics forecasting model of short term oil spot price. In Proceedings of the 6th IAEE European Conference, Zurich, Switzerland, 2–3 September 2004.

- Nogales, F.J.; Contreras, J.; Conejo, A.J.; Espinola, R. Forecasting next-day electricity prices by time series models. IEEE Trans. Power Syst. 2002, 17, 342–348. [Google Scholar] [CrossRef]

- Weron, R. Electricity price forecasting: A review of the state-of-the-art with a look into the future. Int. J. Forecast. 2014, 30, 1030–1081. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Log | Month | ETS | ARIMA | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Point Forecasts | Low 80% | High 80% | Low 95% | High 95% | Point Forecasts | Low 80% | High 80% | Low 95% | High 95% | ||

| Sugi | 15 October | 13,045 | 12,704 | 13,386 | 12,523 | 13,567 | 12,913 | 12,604 | 13,223 | 12,440 | 13,387 |

| 15 November | 13,189 | 12,704 | 13,674 | 12,447 | 13,931 | 13,072 | 12,525 | 13,620 | 12,235 | 13,910 | |

| 15 December | 13,151 | 12,556 | 13,746 | 12,241 | 14,061 | 13,129 | 12,427 | 13,832 | 12,055 | 14,204 | |

| 16 January | 13,058 | 12,372 | 13,744 | 12,009 | 14,107 | 12,753 | 11,944 | 13,562 | 11,516 | 13,990 | |

| 16 February | 12,972 | 12,207 | 13,738 | 11,802 | 14,143 | 12,489 | 11,593 | 13,384 | 11,119 | 13,858 | |

| 16 March | 12,827 | 11,991 | 13,663 | 11,549 | 14,106 | 12,442 | 11,466 | 13,418 | 10,949 | 13,935 | |

| 16 April | 12,716 | 11,816 | 13,615 | 11,340 | 14,092 | 12,367 | 11,315 | 13,419 | 10,759 | 13,976 | |

| 16 May | 12,534 | 11,576 | 13,492 | 11,069 | 13,999 | 12,175 | 11,051 | 13,298 | 10,456 | 13,893 | |

| 16 June | 12,260 | 11,249 | 13,270 | 10,715 | 13,804 | 11,888 | 10,697 | 13,079 | 10,067 | 13,709 | |

| 16 July | 12,122 | 11,063 | 13,181 | 10,502 | 13,741 | 11,888 | 10,634 | 13,142 | 9970 | 13,806 | |

| 16 August | 12,368 | 11,261 | 13,476 | 10,675 | 14,062 | 12,213 | 10,899 | 13,527 | 10,203 | 14,222 | |

| 16 September | 12,720 | 11,563 | 13,877 | 10,951 | 14,489 | 12,628 | 11,256 | 13,999 | 10,530 | 14,725 | |

| Hinoki | 15 October | 17,909 | 17,409 | 18,408 | 17,145 | 18,672 | 18,366 | 17,711 | 19,022 | 17,364 | 19,368 |

| 15 November | 17,989 | 17,207 | 18,772 | 16,792 | 19,187 | 18,804 | 17,691 | 19,917 | 17,102 | 20,507 | |

| 15 December | 18,039 | 17,027 | 19,051 | 16,492 | 19,587 | 19,322 | 17,853 | 20,791 | 17,076 | 21,568 | |

| 16 January | 18,113 | 16,897 | 19,328 | 16,254 | 19,971 | 19,256 | 17,514 | 20,998 | 16,591 | 21,920 | |

| 16 February | 17,952 | 16,553 | 19,351 | 15,812 | 20,092 | 18,848 | 16,894 | 20,803 | 15,859 | 21,838 | |

| 16 March | 17,346 | 15,781 | 18,910 | 14,953 | 19,739 | 17,886 | 15,763 | 20,009 | 14,639 | 21,132 | |

| 16 April | 16,801 | 15,088 | 18,515 | 14,180 | 19,423 | 17,046 | 14,787 | 19,305 | 13,591 | 20,501 | |

| 16 May | 16,336 | 14,486 | 18,186 | 13,507 | 19,166 | 16,261 | 13,889 | 18,633 | 12,633 | 19,889 | |

| 16 June | 15,966 | 13,990 | 17,942 | 12,944 | 18,988 | 15,614 | 13,146 | 18,081 | 11,839 | 19,388 | |

| 16 July | 16,131 | 14,036 | 18,226 | 12,927 | 19,335 | 15,606 | 13,055 | 18,157 | 11,705 | 19,508 | |

| 16 August | 16,758 | 14,545 | 18,971 | 13,374 | 20,142 | 16,041 | 13,416 | 18,665 | 12,027 | 20,054 | |

| 16 September | 17,320 | 14,991 | 19,650 | 13,757 | 20,883 | 16,389 | 13,699 | 19,079 | 12,275 | 20,503 | |

| Karamatsu | 15 October | 11,546 | 11,342 | 11,750 | 11,234 | 11,858 | 11,546 | 11,363 | 11,729 | 11,266 | 11,826 |

| 15 November | 11,546 | 11,257 | 11,835 | 11,105 | 11,987 | 11,546 | 11,287 | 11,805 | 11,150 | 11,942 | |

| 15 December | 11,546 | 11,193 | 11,899 | 11,005 | 12,087 | 11,546 | 11,229 | 11,863 | 11,061 | 12,031 | |

| 16 January | 11,546 | 11,138 | 11,954 | 10,922 | 12,170 | 11,546 | 11,180 | 11,912 | 10,986 | 12,106 | |

| 16 February | 11,546 | 11,090 | 12,002 | 10,848 | 12,244 | 11,546 | 11,136 | 11,956 | 10,920 | 12,172 | |

| 16 March | 11,546 | 11,046 | 12,046 | 10,781 | 12,311 | 11,546 | 11,097 | 11,995 | 10,860 | 12,232 | |

| 16 April | 11,546 | 11,006 | 12,086 | 10,720 | 12,372 | 11,546 | 11,061 | 12,031 | 10,805 | 12,287 | |

| 16 May | 11,546 | 10,969 | 12,123 | 10,663 | 12,429 | 11,546 | 11,028 | 12,064 | 10,754 | 12,338 | |

| 16 June | 11,546 | 10,934 | 12,158 | 10,609 | 12,483 | 11,546 | 10,996 | 12,096 | 10,706 | 12,386 | |

| 16 July | 11,546 | 10,900 | 12,192 | 10,559 | 12,533 | 11,546 | 10,967 | 12,125 | 10,660 | 12,432 | |

| 16 August | 11,546 | 10,869 | 12,223 | 10,511 | 12,581 | 11,546 | 10,938 | 12,154 | 10,617 | 12,475 | |

| 16 September | 11,546 | 10,839 | 12,253 | 10,464 | 12,628 | 11,546 | 10,911 | 12,181 | 10,576 | 12,516 | |

| Valuations | MAPE (%) | MAE (Yen) | RMSE (Yen) | |||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Snaïve/Naïve | ETS | ARIMA | Snaïve/Naïve | ETS | ARIMA | Snaïve/Naïve | ETS | ARIMA | ||

| 1 | Sugi | 3.96 | 4.77 | 5.57 | 504 | 578 | 685 | 670 | 697 | 748 |

| Hinoki | 19.01 | 3.25 | 1.64 | 3273 | 545 | 282 | 4065 | 626 | 332 | |

| Kara. | 2.20 | 2.20 | 2.20 | 252 | 252 | 252 | 285 | 285 | 285 | |

| 2 | Sugi | 4.99 | 3.33 | 2.37 | 639 | 416 | 300 | 872 | 457 | 347 |

| Hinoki | 19.74 | 2.44 | 1.74 | 3401 | 418 | 301 | 4094 | 479 | 378 | |

| Kara. | 1.93 | 1.93 | 1.93 | 220 | 220 | 220 | 261 | 261 | 261 | |

| 3 | Sugi | 5.82 | 3.24 | 2.26 | 740 | 407 | 289 | 967 | 455 | 360 |

| Hinoki | 19.90 | 3.29 | 2.52 | 3432 | 571 | 436 | 4101 | 708 | 516 | |

| Kara. | 1.26 | 1.26 | 1.26 | 142 | 142 | 142 | 151 | 151 | 151 | |

| 4 | Sugi | 6.53 | 3.33 | 2.05 | 825 | 426 | 263 | 1045 | 498 | 342 |

| Hinoki | 19.60 | 5.45 | 8.84 | 3386 | 940 | 1523 | 4091 | 1035 | 1577 | |

| Kara. | 1.42 | 1.42 | 1.42 | 158 | 158 | 158 | 208 | 208 | 208 | |

| 5 | Sugi | 7.25 | 2.75 | 2.38 | 913 | 354 | 309 | 1126 | 429 | 395 |

| Hinoki | 18.92 | 14.06 | 6.07 | 3278 | 2429 | 1051 | 4069 | 2607 | 1139 | |

| Kara. | 1.17 | 1.17 | 1.17 | 132 | 132 | 132 | 147 | 147 | 147 | |

| 6 | Sugi | 7.98 | 2.32 | 1.74 | 1007 | 301 | 225 | 1218 | 373 | 284 |

| Hinoki | 18.23 | 15.43 | 7.50 | 3166 | 2678 | 1304 | 4043 | 2977 | 1442 | |

| Kara. | 1.19 | 1.19 | 1.19 | 135 | 135 | 135 | 160 | 160 | 160 | |

| 7 | Sugi | 8.92 | 2.64 | 1.60 | 1125 | 346 | 211 | 1323 | 445 | 319 |

| Hinoki | 17.46 | 15.54 | 8.20 | 3046 | 2720 | 1432 | 3990 | 2854 | 1592 | |

| Kara. | 1.95 | 1.96 | 1.95 | 220 | 221 | 220 | 257 | 258 | 257 | |

| 8 | Sugi | 10.04 | 3.17 | 3.43 | 1266 | 400 | 444 | 1418 | 456 | 512 |

| Hinoki | 16.51 | 34.81 | 22.13 | 2922 | 6161 | 3926 | 3890 | 6397 | 4029 | |

| Kara. | 3.39 | 3.39 | 3.39 | 380 | 380 | 380 | 402 | 402 | 402 | |

| 9 | Sugi | 11.51 | 12.42 | 5.86 | 1457 | 1571 | 738 | 1571 | 1588 | 782 |

| Hinoki | 15.37 | 40.29 | 24.09 | 2841 | 7177 | 4305 | 3767 | 7642 | 4520 | |

| Kara. | 3.11 | 3.10 | 3.11 | 348 | 346 | 348 | 377 | 375 | 377 | |

| 10 | Sugi | 13.05 | 16.79 | 12.67 | 1675 | 2125 | 1602 | 1830 | 2204 | 1653 |

| Hinoki | 14.08 | 65.79 | 30.81 | 2759 | 11,862 | 5573 | 3622 | 12,709 | 5931 | |

| Kara. | 1.16 | 1.16 | 1.16 | 129 | 129 | 129 | 170 | 170 | 170 | |

| Valuations | MAPE (%) | MAE (Yen) | RMSE (Yen) | |||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Snaïve/Naïve | ETS | ARIMA | Snaïve/Naïve | ETS | ARIMA | Snaïve/Naïve | ETS | ARIMA | ||

| 1 | Sugi | 3.47 | 2.87 | 2.25 | 414 | 345 | 273 | 427 | 362 | 299 |

| Hinoki | 7.63 | 2.34 | 2.99 | 1264 | 388 | 496 | 1460 | 409 | 521 | |

| Kara. | 0.44 | 0.44 | 0.44 | 50 | 50 | 50 | 71 | 71 | 71 | |

| 2 | Sugi | 3.13 | 4.09 | 2.63 | 370 | 483 | 312 | 404 | 519 | 330 |

| Hinoki | 11.29 | 4.54 | 1.46 | 1889 | 751 | 240 | 2162 | 776 | 284 | |

| Kara. | 0.39 | 0.39 | 0.39 | 44 | 44 | 44 | 44 | 46 | 46 | |

| 3 | Sugi | 2.85 | 6.33 | 6.70 | 336 | 752 | 798 | 391 | 791 | 821 |

| Hinoki | 16.58 | 5.92 | 1.12 | 2817 | 980 | 187 | 3345 | 1057 | 221 | |

| Kara. | 1.49 | 1.49 | 1.49 | 170 | 170 | 170 | 171 | 171 | 171 | |

| 4 | Sugi | 3.17 | 4.12 | 2.83 | 388 | 493 | 344 | 460 | 567 | 372 |

| Hinoki | 22.13 | 7.12 | 2.09 | 3806 | 1194 | 350 | 4387 | 1294 | 404 | |

| Kara. | 2.54 | 2.54 | 2.54 | 290 | 290 | 290 | 297 | 297 | 297 | |

| 5 | Sugi | 3.78 | 3.99 | 2.16 | 480 | 487 | 268 | 590 | 599 | 311 |

| Hinoki | 27.70 | 4.72 | 1.91 | 4779 | 798 | 325 | 5274 | 958 | 356 | |

| Kara. | 2.55 | 2.55 | 2.55 | 290 | 290 | 290 | 315 | 315 | 315 | |

| 6 | Sugi | 2.98 | 5.06 | 3.70 | 387 | 641 | 472 | 538 | 705 | 513 |

| Hinoki | 30.42 | 2.54 | 2.08 | 5268 | 434 | 359 | 5553 | 563 | 395 | |

| Kara. | 1.44 | 1.44 | 1.44 | 163 | 163 | 163 | 177 | 177 | 177 | |

| 7 | Sugi | 4.45 | 2.59 | 4.08 | 594 | 333 | 531 | 847 | 398 | 579 |

| Hinoki | 30.38 | 1.59 | 2.25 | 5282 | 275 | 392 | 5560 | 332 | 422 | |

| Kara. | 1.42 | 1.42 | 1.42 | 161 | 161 | 161 | 203 | 203 | 203 | |

| 8 | Sugi | 6.84 | 2.86 | 2.58 | 907 | 381 | 342 | 1166 | 434 | 402 |

| Hinoki | 28.19 | 3.27 | 2.41 | 4914 | 570 | 421 | 5371 | 610 | 478 | |

| Kara. | 0.99 | 0.99 | 0.99 | 112 | 112 | 112 | 164 | 164 | 164 | |

| 9 | Sugi | 8.78 | 3.28 | 2.82 | 1143 | 436 | 374 | 1310 | 491 | 455 |

| Hinoki | 23.22 | 4.97 | 3.23 | 4046 | 867 | 564 | 4737 | 928 | 634 | |

| Kara. | 1.28 | 1.28 | 1.28 | 142 | 142 | 142 | 158 | 158 | 158 | |

| 10 | Sugi | 9.88 | 3.81 | 2.06 | 1262 | 502 | 274 | 1405 | 577 | 393 |

| Hinoki | 17.07 | 4.54 | 9.18 | 2967 | 793 | 1602 | 3772 | 909 | 1680 | |

| Kara. | 2.47 | 2.47 | 2.47 | 274 | 274 | 274 | 285 | 285 | 285 | |

| Valuations | 12-Months-Ahead | 6-Months-Ahead | ||||||

|---|---|---|---|---|---|---|---|---|

| MAPE | MAE | RMSE | MAPE | MAE | RMSE | |||

| 1 | Sugi | 5.09 | 620 | 714 | 2.56 | 309 | 329 | |

| Hinoki | 2.18 | 369 | 414 | 2.66 | 442 | 456 | ||

| 2 | Sugi | 2.85 | 357 | 394 | 3.36 | 398 | 421 | |

| Hinoki | 1.96 | 337 | 409 | 2.85 | 469 | 509 | ||

| 3 | Sugi | 2.72 | 344 | 398 | 6.52 | 775 | 805 | |

| Hinoki | 2.91 | 503 | 604 | 2.88 | 475 | 552 | ||

| 4 | Sugi | 2.66 | 342 | 415 | 3.32 | 399 | 461 | |

| Hinoki | 1.70 | 293 | 323 | 4.61 | 772 | 836 | ||

| 5 | Sugi | 2.42 | 314 | 400 | 2.76 | 337 | 422 | |

| Hinoki | 4.16 | 718 | 768 | 3.23 | 548 | 640 | ||

| 6 | Sugi | 1.99 | 258 | 320 | 4.38 | 556 | 605 | |

| Hinoki | 4.02 | 698 | 797 | 2.02 | 346 | 431 | ||

| 7 | Sugi | 2.07 | 273 | 374 | 3.17 | 410 | 471 | |

| Hinoki | 11.87 | 2076 | 2216 | 1.57 | 274 | 337 | ||

| 8 | Sugi | 1.26 | 163 | 213 | 2.71 | 360 | 413 | |

| Hinoki | 28.47 | 5043 | 5211 | 2.84 | 496 | 537 | ||

| 9 | Sugi | 9.14 | 1155 | 1176 | 3.05 | 405 | 471 | |

| Hinoki | 32.19 | 5741 | 6077 | 4.10 | 715 | 775 | ||

| 10 | Sugi | 14.73 | 1863 | 1922 | 2.91 | 385 | 477 | |

| Hinoki | 48.30 | 8717 | 9317 | 2.34 | 408 | 410 | ||

© 2016 by the authors; licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC-BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Michinaka, T.; Kuboyama, H.; Tamura, K.; Oka, H.; Yamamoto, N. Forecasting Monthly Prices of Japanese Logs. Forests 2016, 7, 94. https://doi.org/10.3390/f7050094

Michinaka T, Kuboyama H, Tamura K, Oka H, Yamamoto N. Forecasting Monthly Prices of Japanese Logs. Forests. 2016; 7(5):94. https://doi.org/10.3390/f7050094

Chicago/Turabian StyleMichinaka, Tetsuya, Hirofumi Kuboyama, Kazuya Tamura, Hiroyasu Oka, and Nobuyuki Yamamoto. 2016. "Forecasting Monthly Prices of Japanese Logs" Forests 7, no. 5: 94. https://doi.org/10.3390/f7050094