Assessment of Possible Production Leakage from Implementing the EU Biodiversity Strategy on Forest Product Markets

Abstract

:1. Introduction

2. Materials and Methods

2.1. Scenario Basics: Characteristics, Functions and Building Techniques

2.2. Scenario Generation

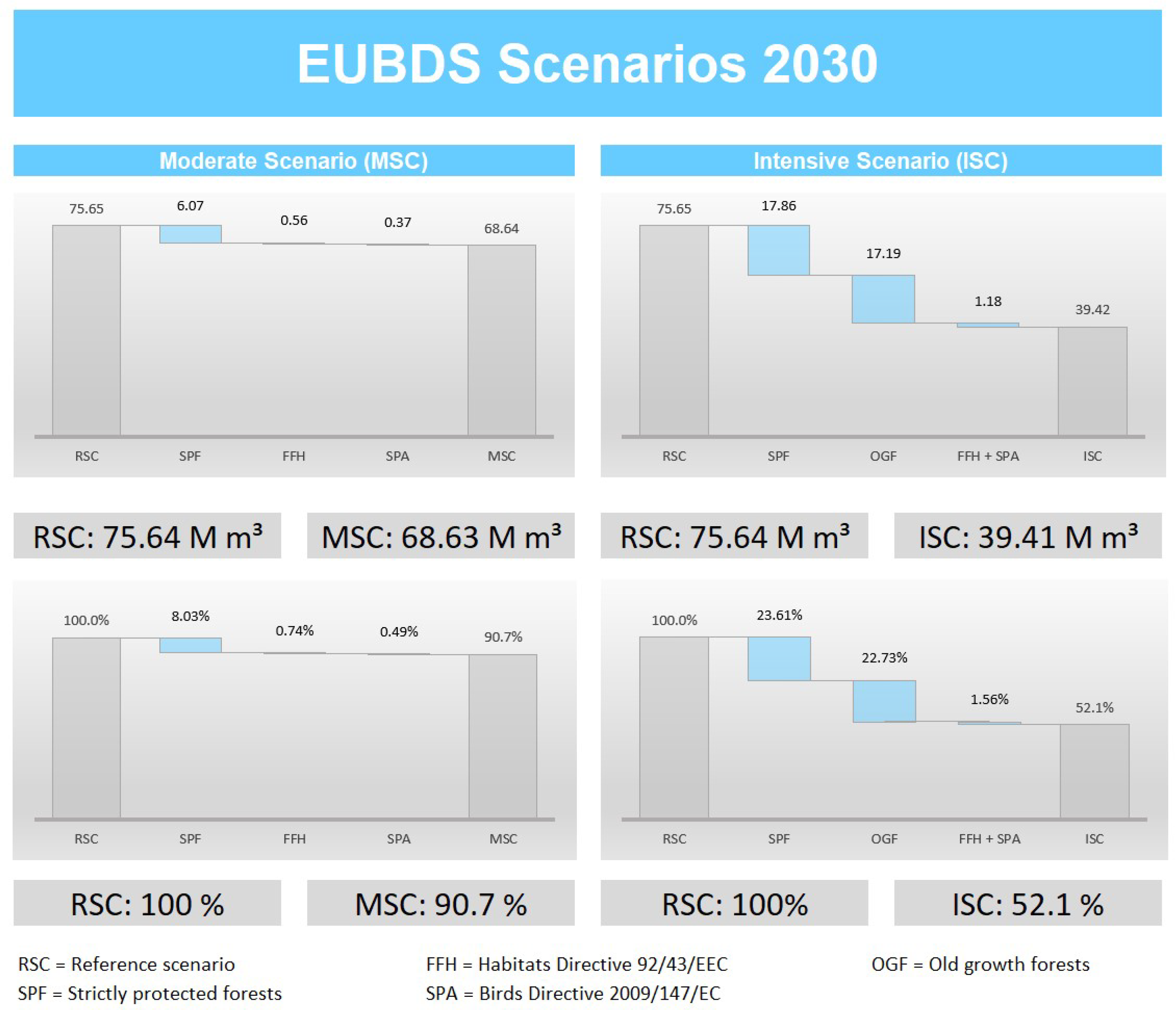

2.2.1. WEHAM Scenario and EUBDS Implementation Scenarios for Germany

2.2.2. Roundwood Production under Possible EUBDS Implementation in Germany

2.2.3. Scenario Generation on EU Level

2.3. Quantitative Scenario Analysis: Forest Products Market Modelling

3. Results

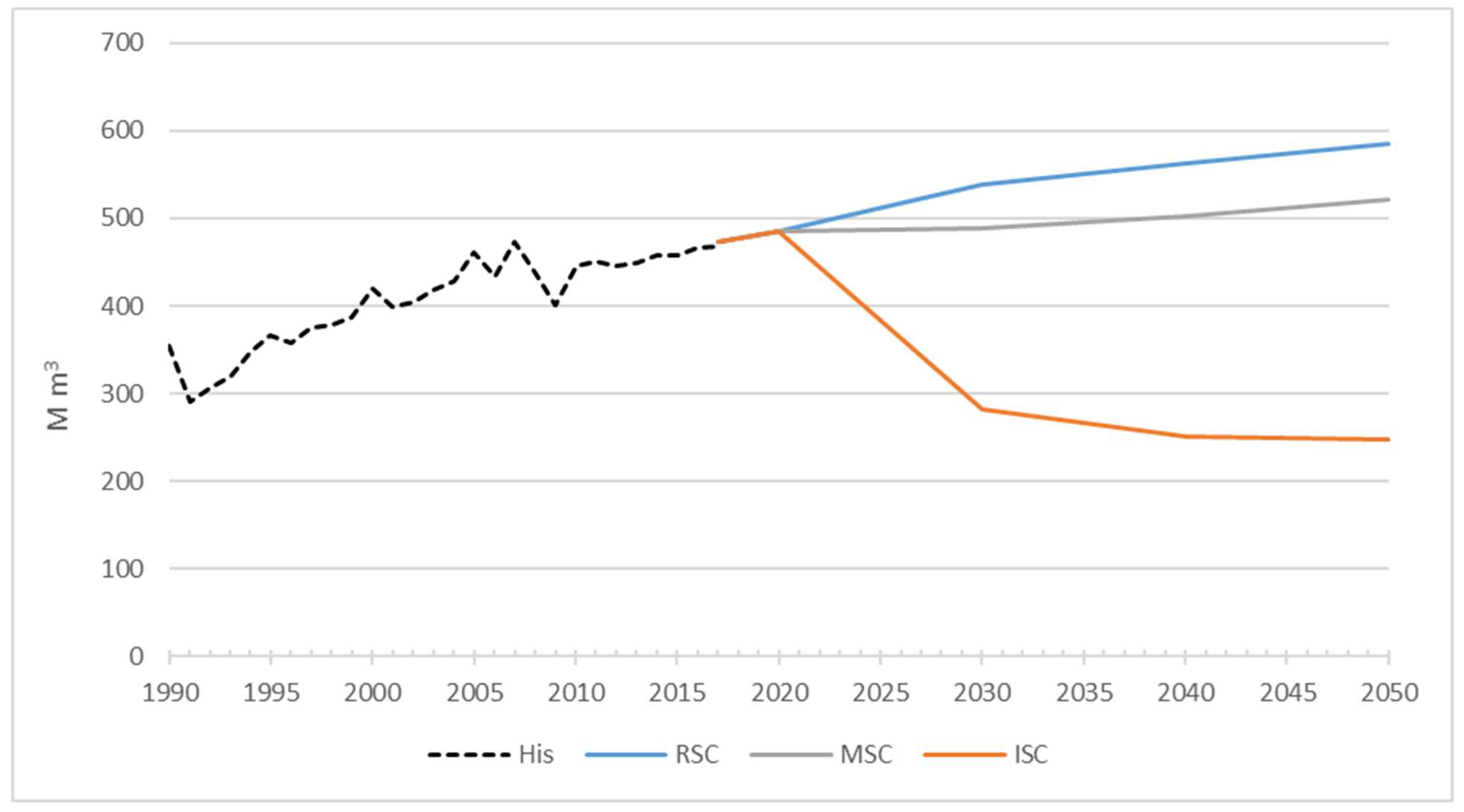

3.1. Impact on EU Roundwood Production

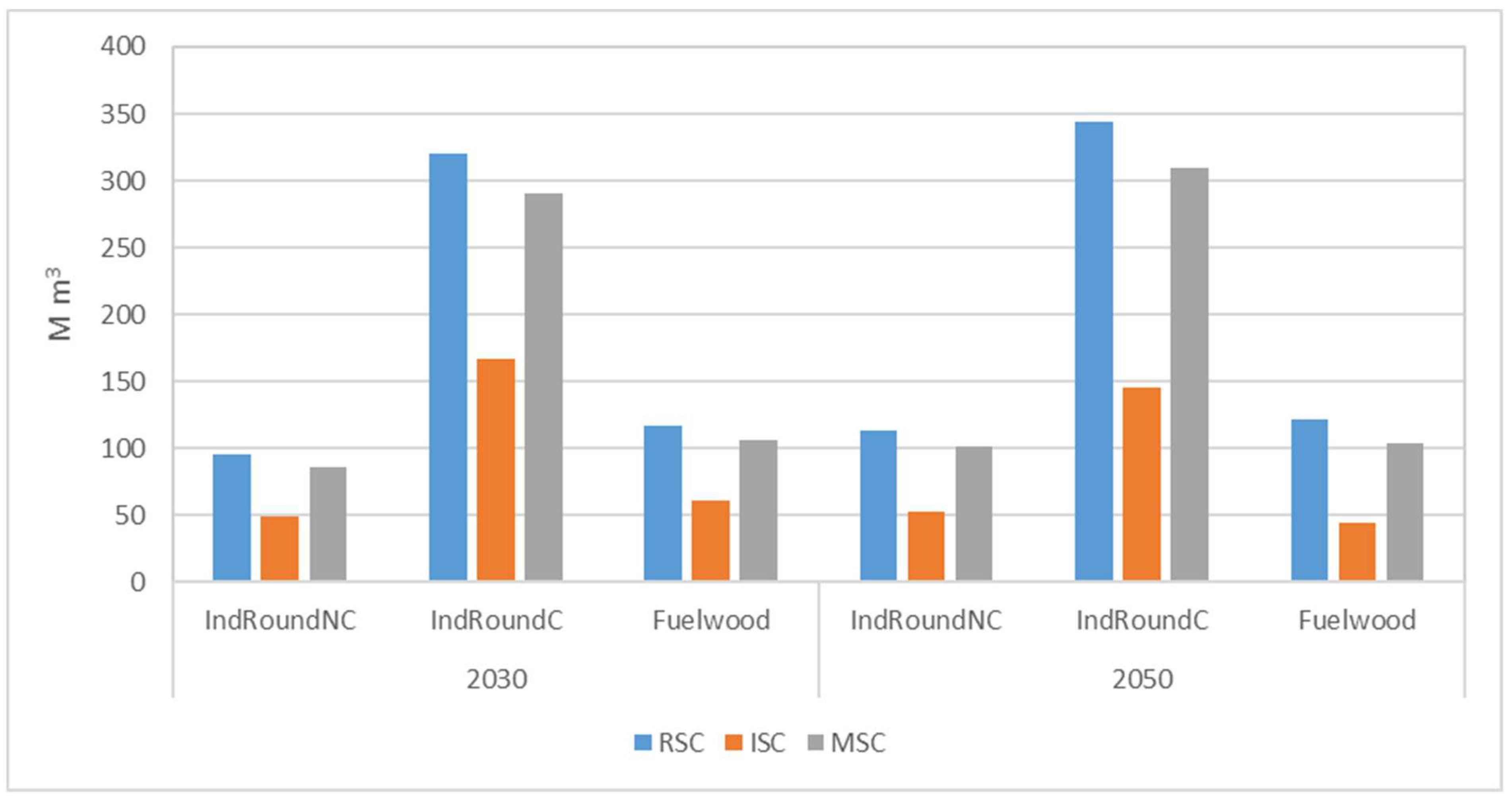

3.1.1. Impact on Industrial Round and Fuelwood Production

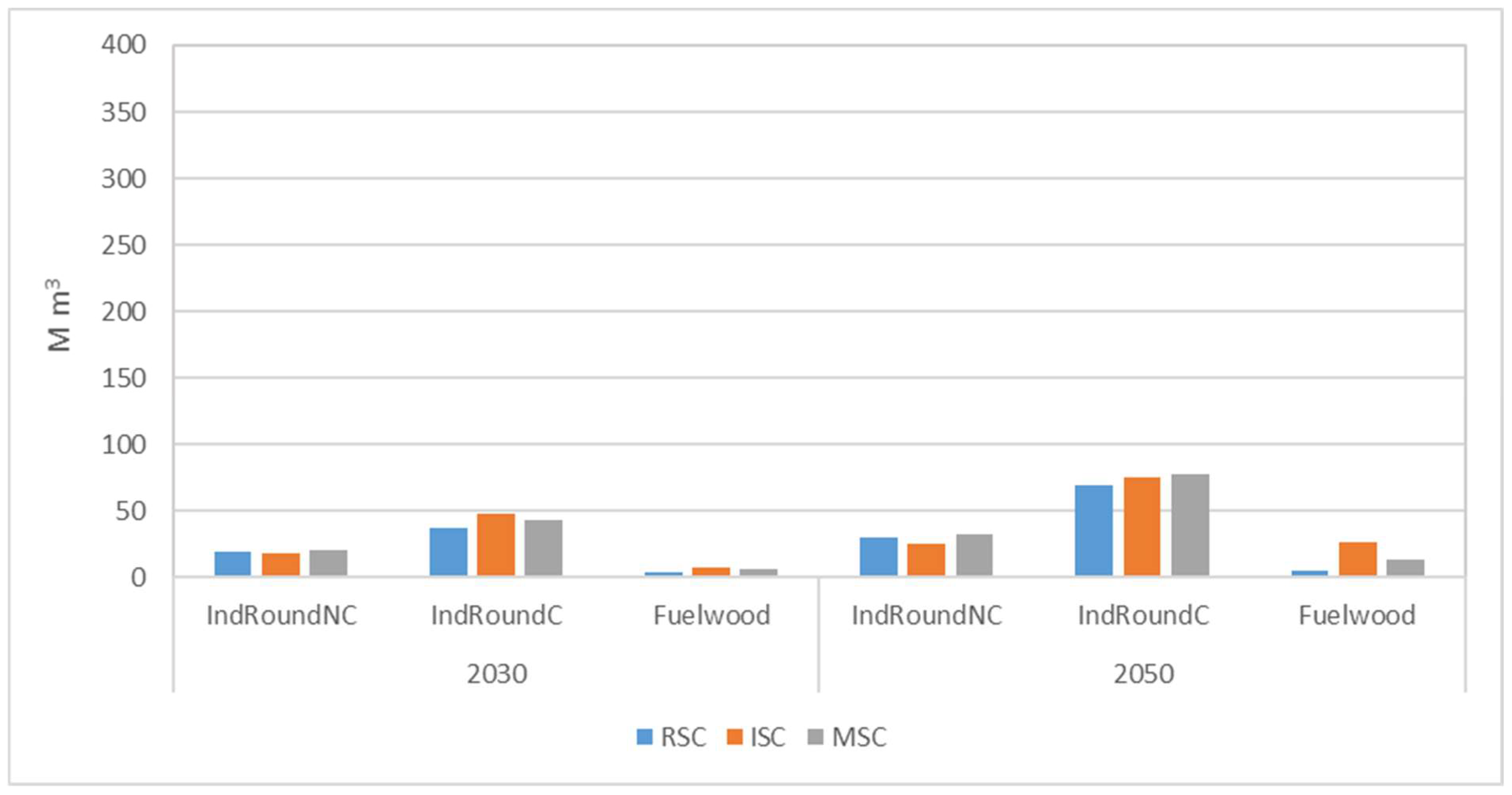

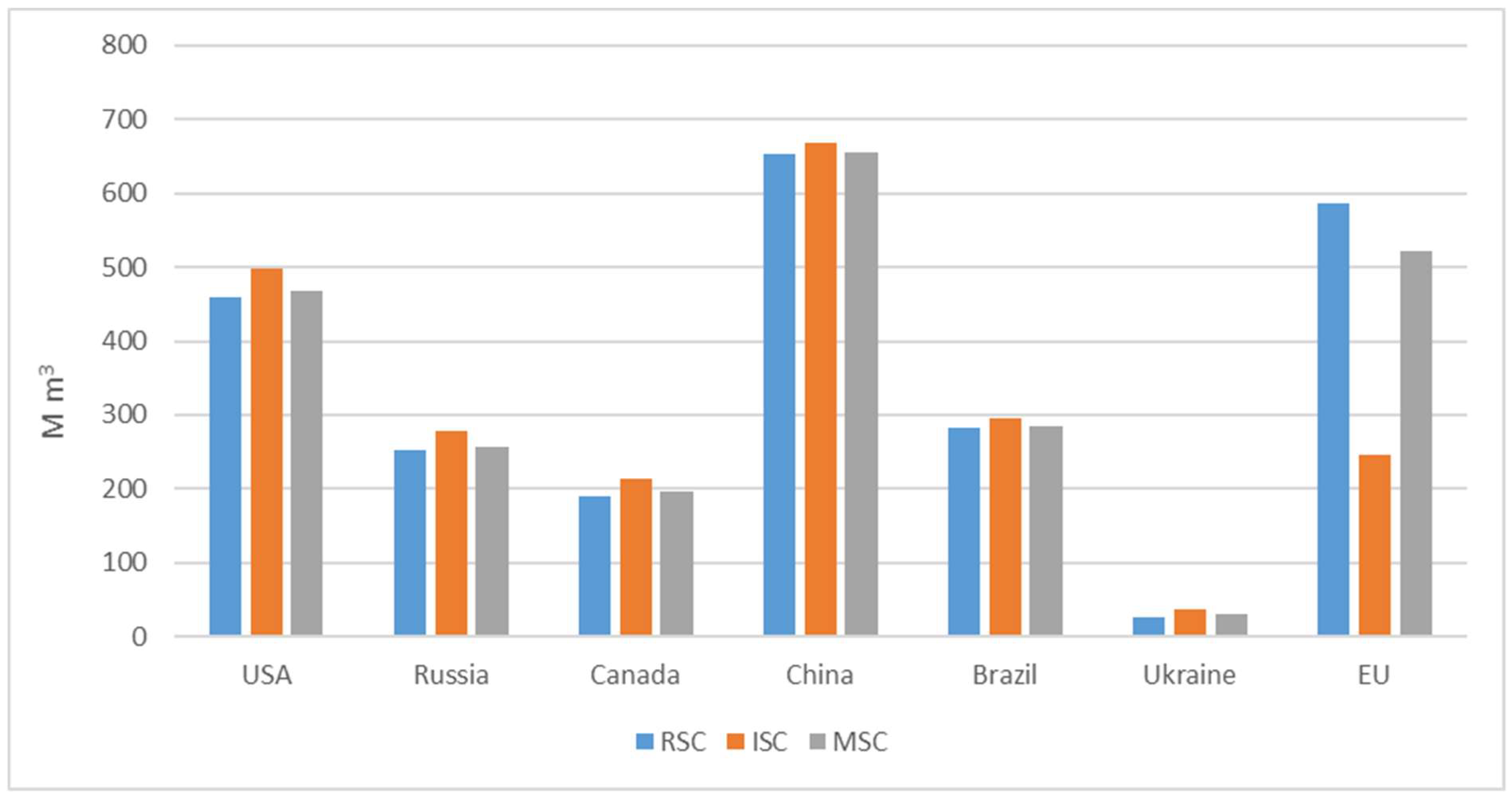

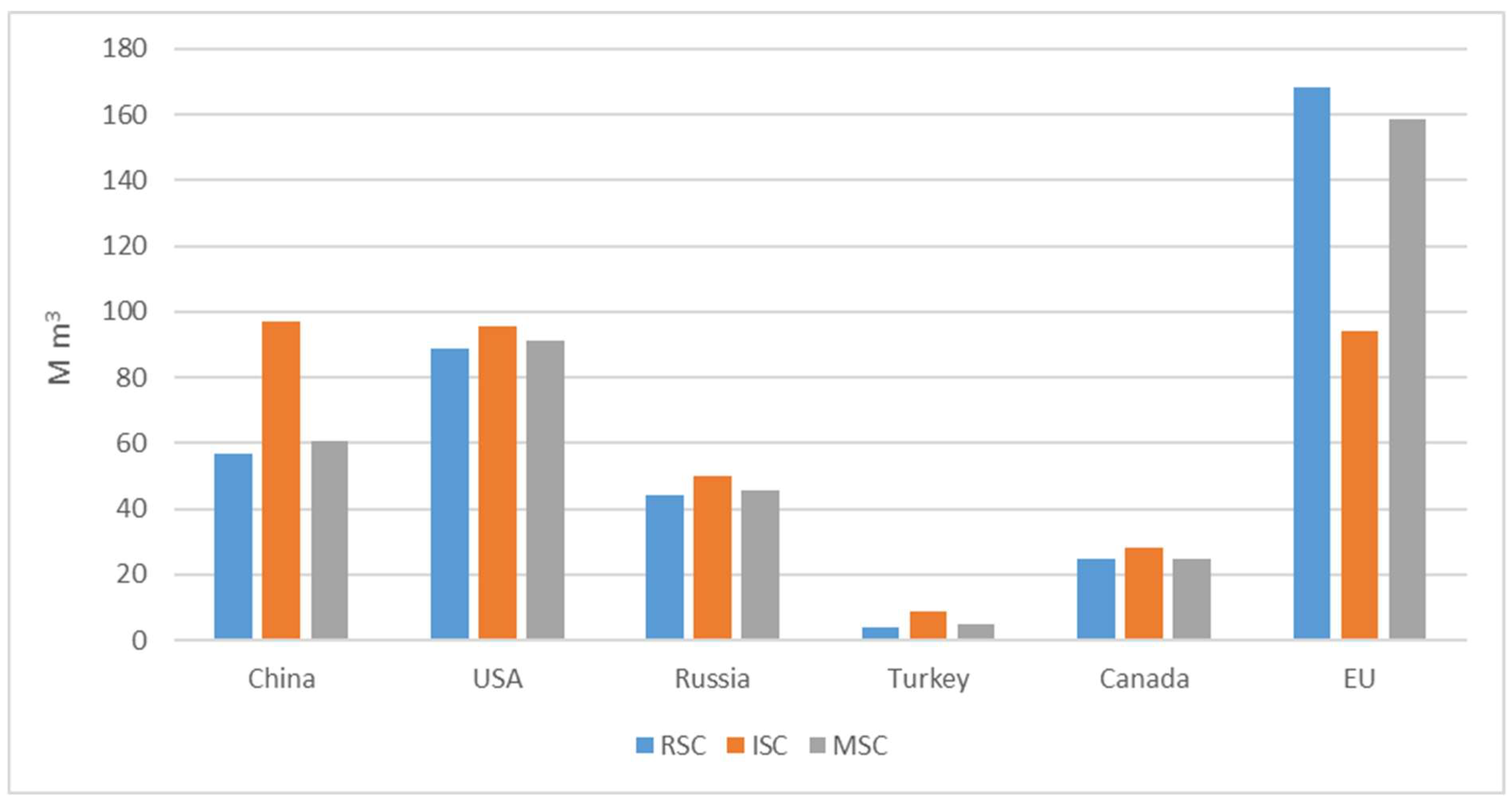

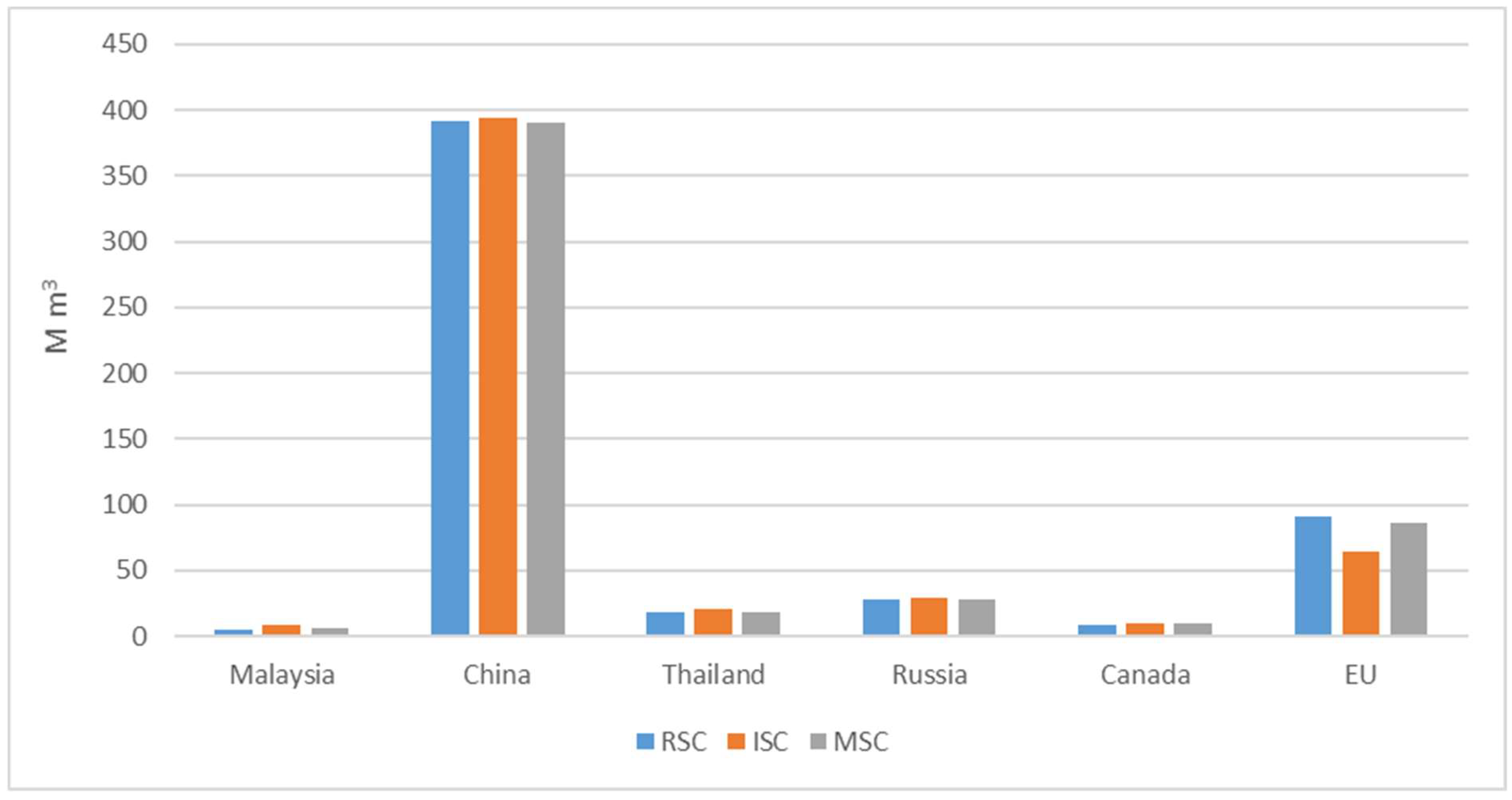

3.1.2. Trade Effects in European Roundwood Markets

3.2. Impact on European Production of Wood-based Products

3.2.1. Sawnwood

3.2.2. Wood-Based Panels

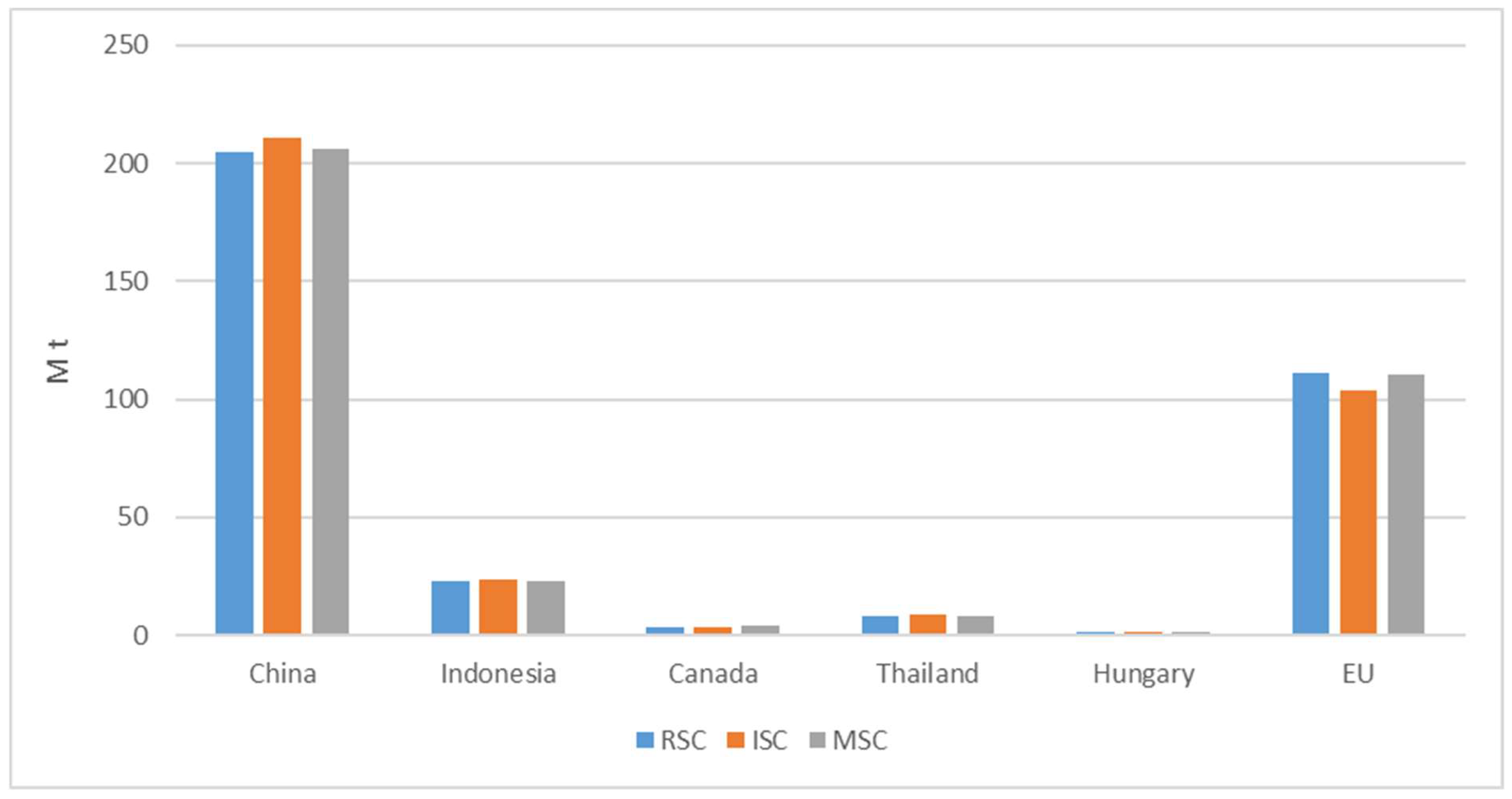

3.2.3. Wood Pulp and Paper and Paperboard

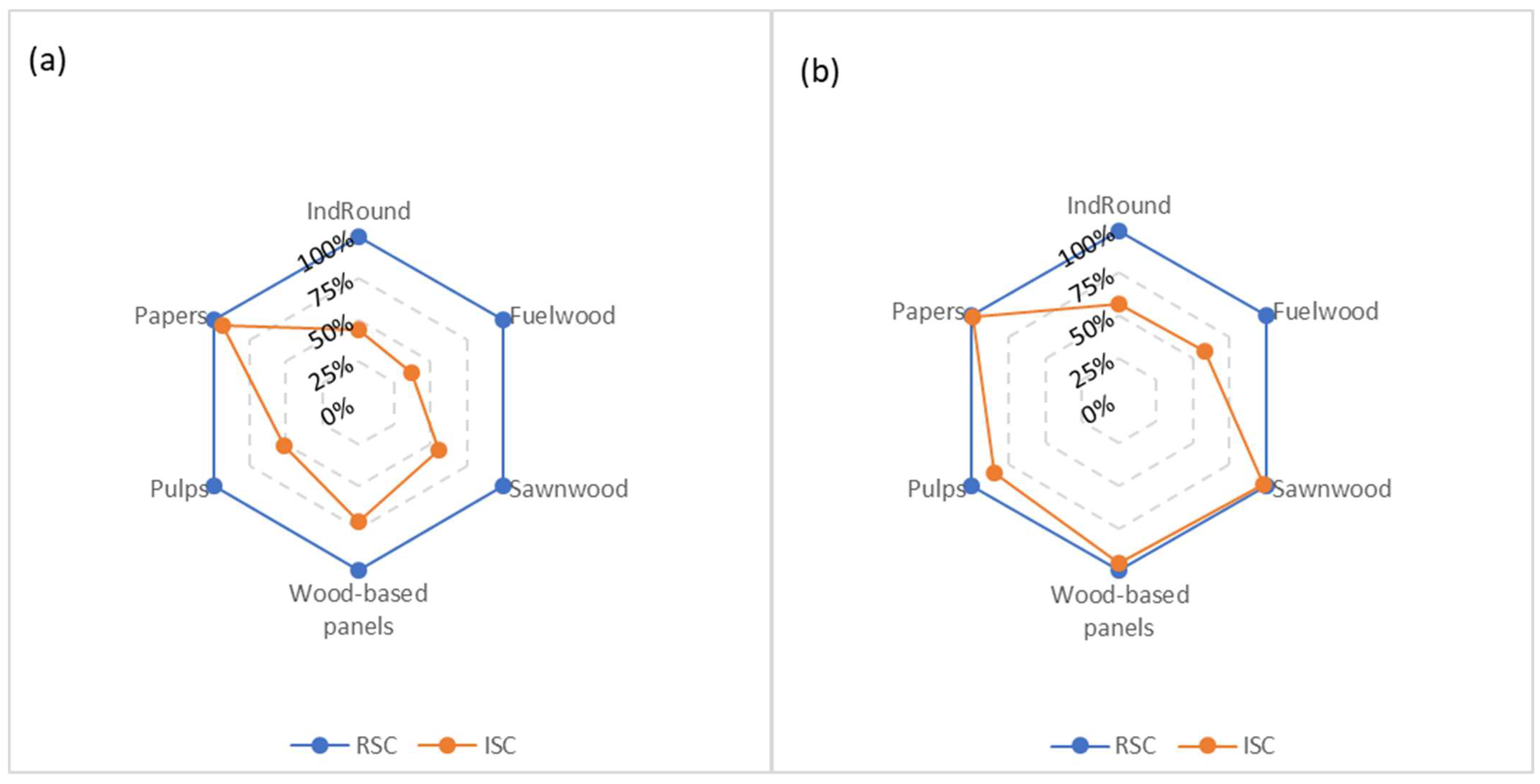

3.3. Production Leakage

3.3.1. Total Roundwood

Industrial Roundwood

Fuelwood

3.3.2. Sawnwood

3.3.3. Wood-Based Panels

3.3.4. Wood Pulp

3.3.5. Paper and Paperboard

4. Discussion

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Forest Area | Forest Growing Stock | Growing Stock Density | RW Production | RW Production | RW Production Intensity | Forest Area within Protected Areas, IUCN I–IV 4 | Forest Area 3 in Protected Areas, MCPFE 1.1 4 | Forest Area 3 in Protected Areas, MCPFE 1.2 4 | Forest Area 3 in Protected Areas, MCPFE 1.3 4 | Forest Area 3 in Protected Areas, MCPFE 2 4 | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Database 1 | FAO 2022 | FAOSTAT 2022 | FAO 2022 | Forest Europe 2020 | ||||||||||||

| Countries 2 | ts ha | M m3 o.b. | m3/ha | M m3 u. b. | m3/ha | m3/ha | ts ha | % | ts ha | % | ts ha | ] | ts ha | % | ts ha | % |

| Austria 5 | 3.881 | 1.146 | 295 | 18 | 5 | 0.02 | 852 | 22 | 0 | 0 | 30 | 1 | 472 | 12 | 333 | 9 |

| Belgium | 689 | 180 | 260 | 5 | 8 | 0.03 | 180 | 26 | 11 | 2 | 7 | 1 | 9 | 1 | 26 | 4 |

| Bulgaria | 3.833 | 680 | 178 | 6 | 2 | 0.01 | 704 | 18 | 58 | 2 | 77 | 2 | 22 | 1 | 546 | 14 |

| Croatia | 1.922 | 415 | 216 | 5 | 3 | 0.01 | 54 | 3 | 44 | 2 | 10 | 1 | 214 | 11 | 4 | 0 |

| Czechia | 2.668 | 768 | 288 | 16 | 6 | 0.02 | 147 | 5 | 28 | 1 | 99 | 4 | 34 | 1 | 599 | 22 |

| Denmark | 625 | 131 | 210 | 4 | 7 | 0.03 | 42 | 7 | 0 | 0 | 8 | 1 | 34 | 5 | 77 | 12 |

| Estonia | 2.421 | 492 | 203 | 10 | 4 | 0.02 | 498 | 21 | 165 | 7 | 146 | 6 | 224 | 9 | 4 | 0 |

| Finland | 22.409 | 2.449 | 109 | 59 | 3 | 0.02 | 2.831 | 13 | 1.913 | 9 | 629 | 3 | 276 | 1 | 922 | 4 |

| France | 16.836 | 2.856 | 170 | 50 | 3 | 0.02 | 3.826 | 23 | 0 | 0 | 129 | 1 | 3.274 | 19 | 3.010 | 18 |

| Greece | 3.902 | 192 | 49 | 1 | 0 | 0.01 | 164 | 4 | ||||||||

| Hungary | 2.061 | 379 | 184 | 6 | 3 | 0.02 | 458 | 22 | 4 | 0 | 9 | 0 | 647 | 31 | 216 | 10 |

| Ireland | 755 | 114 | 151 | 3 | 4 | 0.03 | 142 | 19 | 0 | 0 | 0 | 0 | 6 | 1 | 0 | 0 |

| Italy | 9.297 | 1.384 | 149 | 13 | 1 | 0.01 | 3.265 | 35 | 270 | 3 | 1.491 | 16 | 1.504 | 16 | 898 | 10 |

| Latvia | 3.391 | 656 | 193 | 12 | 4 | 0.02 | 544 | 16 | 9 | 0 | 198 | 6 | 186 | 5 | 163 | 5 |

| Lithuania | 2.187 | 537 | 246 | 6 | 3 | 0.01 | 460 | 21 | 26 | 1 | 87 | 4 | 90 | 4 | 151 | 7 |

| Luxembourg | 89 | 33 | 369 | 0 | 4 | 0.01 | 1 | 1 | ||||||||

| Netherlands | 365 | 79 | 217 | 2 | 6 | 0.03 | 217 | 59 | 3 | 1 | 33 | 181 | 50 | |||

| Poland | 9.420 | 2.550 | 271 | 41 | 4 | 0.02 | 3.079 | 33 | 63 | 1 | 0 | 0 | 3.016 | 32 | 451 | 5 |

| Portugal | 3.312 | 171 | 52 | 11 | 3 | 0.07 | 616 | 19 | 22 | 1 | 0 | 0 | 615 | 1 | 9 | 0 |

| Romania 6 | 6.901 | 2.222 | 322 | 15 | 2 | 0.01 | 2.606 | 38 | 136 | 2 | 84 | 1 | 178 | 3 | 141 | 2 |

| Slovakia | 1.922 | 535 | 279 | 9 | 5 | 0.02 | 554 | 29 | 68 | 4 | 0 | 0 | 486 | 25 | 286 | 15 |

| Slovenia | 1.248 | 415 | 332 | 5 | 4 | 0.01 | 257 | 21 | 10 | 1 | 78 | 6 | 78 | 6 | 92 | 7 |

| Spain | 18.551 | 1.059 | 57 | 17 | 1 | 0,02 | 7.400 | 40 | 36 | 0 | 494 | 3 | 2.302 | 12 | 1.285 | 7 |

| Sweden | 27.980 | 3.478 | 124 | 74 | 3 | 0,02 | 2.121 | 8 | 325 | 1 | 1.610 | 6 | 186 | 1 | 104 | 0 |

| Min | 89 | 33 | 49 | 0 | 0 | 0.01 | 42 | 3 | 0 | 0 | 0 | 0 | 6 | 1 | 0 | |

| Max | 27.980 | 3.478 | 369 | 74 | 8 | 0.07 | 7.400 | 59 | 1.913 | 9 | 1.610 | 16 | 3.274 | 32 | 3.010 | 5 |

| Average | 6.111 | 955 | 205 | 16 | 4 | 0.02 | 1.402 | 23 | 140 | 2 | 237 | 3 | 660 | 10 | 432 | 9 |

| Median | 2.990 | 536 | 207 | 9 | 4 | 0.02 | 549 | 21 | 27 | 1 | 77 | 2 | 214 | 6 | 172 | 7 |

| Germany | 11.419 | 3.663 | 321 | 69 | 6 | 0.02 | 3.306 | 29 | 0 | 0 | 220 | 2 | 3.086 | 27 | 5.958 | 52 |

| Category | Forest | Non-Forest |

|---|---|---|

| Natural forest development | 227 | 36 |

| FFH area | 1781 | 1377 |

| SPA | 792 | 1357 |

| sum | 2800 | 2770 |

| Protection Level | |||||||

|---|---|---|---|---|---|---|---|

| Land-Use Type | Very High | High | Medium | Low | Very Low | Not Protected | Total |

| waters | 12 | 88 | 240 | 65 | 45 | 159 | 608 |

| agriculture | 22 | 419 | 786 | 1358 | 3687 | 12,774 | 19,045 |

| other open habitats | 44 | 218 | 151 | 60 | 121 | 438 | 1031 |

| traffic and settlements | 1 | 20 | 48 | 81 | 772 | 3060 | 3983 |

| All non-forest | 79 | 744 | 1226 | 1563 | 4624 | 16,432 | 24,668 |

| forest | 161 | 743 | 1198 | 797 | 3572 | 4,654 | 11,125 |

| All land-use types | 240 | 1487 | 2425 | 2361 | 8198 | 21,092 | 35,803 |

| Moderate Scenario (MSC) | Intensive Scenario (ISC) | |||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Current: 2020 | Changes | Goal: 2030 | Current: 2020 | Changes | Goal: 2030 | |||||||||||||

| Germany | Forest | Non-Forest | Germany | Forest | Non-Forest | Germany | Forest | Non-Forest | Germany | Forest | Non-Forest | Germany | Forest | Non-Forest | Germany | Forest | Non-Forest | |

| Total area | 35,803 | 11,125 | 24,668 | 0 | 0 | 0 | 35,803 | 11,125 | 24,668 | 35,803 | 11,125 | 24,668 | 0 | 0 | 0 | 35,803 | 11,125 | 24,668 |

| 1. EUBDS-objective: legal protection of a minimum of 30% of the EU’s land area 3. EUBDS-objective: Effectively manage all protected areas, defining clear conservation objectives and measures and monitoring them appropriately. | ||||||||||||||||||

| Total protected area 1 | 5570 | 2800 | 2770 | 5171 | 2600 | 2572 | 10741 | 5400 | 5341 | 14711 | 6471 | 8236 | 0 | 0 | 0 | 14711 | 6471 | 8236 |

| of that Protected area with legal protection 2 | 5306 | 2573 | 2733 | 1854 | 1569 | 286 | 7162 | 4142 | 3020 | 14471 | 6311 | 8157 | −4664 * | −4164 * | −500 * | 9807 | 2147 | 7657 |

| 2. EUBDS-objective: Strictly protect at least a third of the EU’s protected areas, including all remaining EU primary and old-growth forests. | ||||||||||||||||||

| of that Protected area with strict legal protection 3 | 263 | 227 | 36 | 3317 | 1031 | 2285 | 3579 | 1258 | 2322 | 240 | 161 | 79 | 4664 * | 4164 * | 500 * | 4904 | 4325 | 579 |

| of that Primary forests and old- growth forests 4 | 1064 | 1064 | ||||||||||||||||

| Moderate Scenario (MSC) | |||||

|---|---|---|---|---|---|

| Wood Species Groups (WSG) | Total Forest Area | Additional Area Required or Areas with Additional Nature Conservation Measure | |||

| Accessible and Stocked Timberland | Strictly Protected Areas | Protected Areas | |||

| Developing Old-Growth Forests | Natural Forest Development | FFH-Areas | SPA-Areas | ||

| Oak | 1130 | 91 | 104 | 22 | |

| Beech | 3598 | 289 | 337 | 68 | |

| All deciduous trees | 4727 | 379 | 441 | 90 | |

| Spruce | 3164 | 254 | 27 | 81 | |

| Pine | 2737 | 220 | 23 | 70 | |

| All coniferous trees | 5900 | 474 | 51 | 152 | |

| Subtotal | 853 | 491 | 241 | ||

| of which without wood production according to NFI 2012: nature conservation and protection forest | 178 | ||||

| of which without FFH management requirements | 595 | 241 | |||

| all tree species | 10,628 | 1031 | 1569 | ||

| Intensive Scenario (ISC) | |||||

| Wood Species Groups (WSG) | Total Forest Area | Additional Area Required or Areas with Additional Nature Conservation Measure | |||

| Accessible and Stocked Timberland | Strictly Protected Areas | Protected Areas | |||

| Developing Old-Growth Forests | Natural Forest Development | FFH-Areas | SPA-Areas | ||

| Oak | 1130 | 119 | 309 | 268 | |

| Beech | 3598 | 583 | 921 | 867 | |

| All deciduous trees | 4727 | 702 | 1230 | 1134 | |

| Spruce | 3164 | 246 | 892 | 70 | |

| Pine | 2737 | 116 | 801 | 60 | |

| All coniferous trees | 5900 | 362 | 1692 | 130 | |

| Subtotal | 1064 | 2922 | 1265 | ||

| of which without wood production according to NFI 2012: nature conservation and protection forest | 178 | ||||

| of which without FFH management requirements | 882 | ||||

| All tree species | 10,628 | 4164 | 2147 | ||

| WEHAM Scenario | Moderate Scenario (MSC) | Reduction | |||||

|---|---|---|---|---|---|---|---|

| WEHAM-Projection Period | Total Forest Area | Additional EUBDS Protected Areas | Total Forest Area | % | |||

| without EUBDS Implementation | Strictly Protected Areas | Protected Areas | with EUBDS Implementation | ||||

| Development- Old-Growth Forests | Natural Forest Development | FFH Areas | SPA Areas | ||||

| 2018–2022 | 82,806 | −6647 | −634 | −409 | 75,116 | 90.7% | |

| 2023–2027 | 73,048 | −5863 | −537 | −361 | 66,286 | 90.7% | |

| 2028–2032 | 75,647 | −6072 | −563 | −374 | 68,638 | 90.7% | |

| 2033–2037 | 75,028 | −6022 | −547 | −371 | 68,087 | 90.7% | |

| 2038–2042 | 75,522 | −6062 | −549 | −373 | 68,538 | 90.8% | |

| 2043–2047 | 75,636 | −6071 | −551 | −374 | 68,640 | 90.7% | |

| 2048–2052 | 78,434 | −6296 | −554 | −388 | 71,196 | 90.8% | |

| 2018–2052 | 76,589 | −6148 | −562 | −379 | 69,500 | 90.7% | |

| WEHAM scenario | Intensive scenario (ISC) | Reduction | |||||

| WEHAM-Projection Period | Total Forest Area | Additional EUBDS Protected Areas | Total Forest Area | % | |||

| without EUBDS Implementation | Strictly Protected Areas | Protected Areas | with EUBDS Implementation | ||||

| Development- Old-Growth Forests | Natural Forest Development | FFH Areas | SPA Areas | ||||

| 2018–2022 | 82,806 | −15,280 | −20,632 | −1430 | 45,464 | 54.9% | |

| 2023–2027 | 73,048 | −15,270 | −17,654 | −1163 | 38,961 | 53.3% | |

| 2028–2032 | 75,647 | −17,192 | −17,860 | −1178 | 39,416 | 52.1% | |

| 2033–2037 | 75,028 | −16,286 | −17,948 | −1134 | 39,660 | 52.9% | |

| 2038–2042 | 75,522 | −16,079 | −18,162 | −1157 | 40,124 | 53.1% | |

| 2043–2047 | 75,636 | −15,802 | −18,282 | −1138 | 40,414 | 53.4% | |

| 2048–2052 | 78,434 | −16,488 | −18,927 | −1131 | 41,887 | 53.4% | |

| 2018–2052 | 76,589 | −16,057 | −18,495 | −1190 | 40,847 | 53.3% | |

| RSC | ISC | MSC | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| 2017 | 2030 | 2050 | 2017 | 2030 | 2050 | 2017 | 2030 | 2050 | ||

| production | ||||||||||

| total roundwood * | M m3 | 473 | 539 | 586 | 473 | 281 | 247 | 473 | 490 | 521 |

| fuelwood | 112 | 117 | 122 | 112 | 61 | 45 | 112 | 106 | 104 | |

| coniferous industrial roundwood | 278 | 321 | 343 | 278 | 167 | 146 | 278 | 291 | 309 | |

| non-coniferous industrial roundwood | 76 | 95 | 113 | 76 | 50 | 53 | 76 | 87 | 102 | |

| sawnwood | 107 | 134 | 168 | 107 | 83 | 94 | 107 | 125 | 158 | |

| plywood and panels | 61 | 79 | 91 | 61 | 56 | 65 | 61 | 76 | 86 | |

| wood pulps | M t | 37 | 37 | 45 | 37 | 21 | 23 | 37 | 35 | 42 |

| paper and paperboards | 88 | 96 | 111 | 88 | 87 | 104 | 88 | 95 | 110 | |

| import | ||||||||||

| total roundwood | M m3 | 57 | 60 | 106 | 57 | 73 | 128 | 57 | 70 | 123 |

| fuelwood | 4 | 4 | 6 | 4 | 7 | 26 | 4 | 6 | 13 | |

| coniferous industrial roundwood | 35 | 37 | 70 | 35 | 48 | 76 | 35 | 43 | 78 | |

| non-coniferous industrial roundwood | 17 | 19 | 30 | 17 | 18 | 26 | 17 | 20 | 32 | |

| sawnwood | 33 | 26 | 25 | 33 | 36 | 34 | 33 | 27 | 26 | |

| plywood and panels | 30 | 11 | 9 | 30 | 18 | 16 | 30 | 11 | 10 | |

| wood pulps | M t | 17 | 18 | 24 | 17 | 21 | 25 | 17 | 19 | 24 |

| paper and paperboards | 46 | 26 | 24 | 46 | 29 | 25 | 46 | 26 | 23 | |

| export | ||||||||||

| total roundwood | M m3 | 44 | 47 | 59 | 44 | 25 | 16 | 44 | 40 | 49 |

| fuelwood | 4 | 4 | 6 | 4 | 2 | 0 | 4 | 2 | 1 | |

| coniferous industrial roundwood | 28 | 25 | 26 | 28 | 15 | 8 | 28 | 22 | 23 | |

| non-coniferous industrial roundwood | 12 | 18 | 28 | 12 | 8 | 8 | 12 | 16 | 25 | |

| sawnwood | 56 | 75 | 110 | 56 | 39 | 47 | 56 | 67 | 101 | |

| plywood and panels | 33 | 26 | 30 | 33 | 17 | 14 | 33 | 23 | 27 | |

| wood pulps | M t | 13 | 17 | 30 | 13 | 9 | 14 | 13 | 16 | 28 |

| paper and paperboard | 62 | 41 | 38 | 62 | 36 | 33 | 62 | 41 | 36 | |

| apparent domestic consumption | ||||||||||

| total roundwood * | M m3 | 485 | 553 | 632 | 485 | 329 | 358 | 485 | 519 | 595 |

| fuelwood | 112 | 116 | 122 | 112 | 66 | 71 | 112 | 110 | 116 | |

| coniferous industrial roundwood | 285 | 333 | 388 | 285 | 200 | 213 | 285 | 312 | 364 | |

| non-coniferous industrial roundwood | 82 | 97 | 116 | 82 | 60 | 71 | 82 | 91 | 109 | |

| sawnwood | 85 | 85 | 83 | 85 | 80 | 81 | 85 | 84 | 83 | |

| plywood and panels | 58 | 64 | 70 | 58 | 57 | 67 | 58 | 63 | 69 | |

| wood pulps | M t | 41 | 39 | 39 | 41 | 33 | 33 | 41 | 38 | 38 |

| paper and paperboards | 72 | 81 | 97 | 72 | 80 | 96 | 72 | 81 | 97 | |

References

- COM. EU Biodiversity Strategy for 2030-Bringing Nature Back into our Lives; Communication from the Commission to the European Parliament, the Council, the European Economic and Social Committee and the Committee of the Regions COM (2020) 380 Final: Brussels, Belgium, 2020. [Google Scholar]

- Jonsson, R.; Mbongo, W.; Felton, A.; Boman, M. Leakage Implications for European Timber Markets from Reducing Deforestation in Developing Countries. Forests 2012, 3, 736–744. [Google Scholar] [CrossRef] [Green Version]

- Meyfroidt, P.; Roy Chowdhury, R.; Bremond, A.d.; Ellis, E.C.; Erb, K.-H.; Filatova, T.; Garrett, R.D.; Grove, J.M.; Heinimann, A.; Kuemmerle, T.; et al. Middle-range theories of land system change. Glob. Environ. Chang. 2018, 53, 52–67. [Google Scholar] [CrossRef]

- Liu, J.; Dou, Y.; Batistella, M.; Challies, E.; Connor, T.; Friis, C.; Millington, J.D.A.; Parish, E.; Romulo, C.L.; Silva, R.F.B.; et al. Spillover systems in a telecoupled Anthropocene: Typology, methods, and governance for global sustainability. Curr. Opin. Environ. Sustain. 2018, 33, 58–69. [Google Scholar] [CrossRef] [Green Version]

- Bastos Lima, M.G.; Persson, U.M.; Meyfroidt, P. Leakage and boosting effects in environmental governance: A framework for analysis. Environ. Res. Lett. 2019, 14, 105006. [Google Scholar] [CrossRef] [Green Version]

- Gan, J.; McCarl, B.A. Measuring transnational leakage of forest conservation. Ecol. Econ. 2007, 64, 423–432. [Google Scholar] [CrossRef]

- Dieter, M.; Englert, H. Competitiveness in the global forest industry sector: An empirical study with special emphasis on Germany. Eur. J. For. Res. 2007, 126, 401–412. [Google Scholar] [CrossRef]

- Murray, B.C.; McCarl, B.A.; Lee, H.-C. Estimating Leakage from Forest Carbon Sequestration Programs. Land Econ. 2004, 80, 109–124. [Google Scholar] [CrossRef]

- Kallio, A.M.I.; Maarit, I.; Solberg, B.; Käär, L.; Päivinen, R. Economic impacts of setting reference levels for the forest carbon sinks in the EU on the European forest sector. For. Policy Econ. 2018, 92, 193–201. [Google Scholar] [CrossRef]

- Li, R.; Buongiorno, J.; Turner, J.A.; Zhu, S.; Prestemon, J. Long-term effects of eliminating illegal logging on the world forest industries, trade, and inventory. For. Policy Econ. 2008, 10, 480–490. [Google Scholar] [CrossRef]

- Sohngen, B.; Mendelsohn, R.; Sedjo, R. Forest Management, Conservation, and Global Timber Markets. Am. J. Agric. Econ. 1999, 81, 1–13. [Google Scholar] [CrossRef]

- Kallio, A.M.I.; Solberg, B. Leakage of forest harvest changes in a small open economy: Case Norway. Scand. J. For. Res. 2018, 33, 502–510. [Google Scholar] [CrossRef]

- Hu, X.; Shi, G.; Hodges, D. International Market Leakage from China’s Forestry Policies. Forests 2014, 5, 2613–2625. [Google Scholar] [CrossRef]

- Hope, E.; Gagnon, B.; Avdić, V. Assessment of the Impact of Climate Change Policies on the Market for Forest Industrial Residues. Sustainability 2020, 12, 1787. [Google Scholar] [CrossRef] [Green Version]

- Ford, S.A.; Jepsen, M.R.; Kingston, N.; Lewis, E.; Brooks, T.M.; MacSharry, B.; Mertz, O. Deforestation leakage undermines conservation value of tropical and subtropical forest protected areas. Glob. Ecol. Biogeogr. 2020, 29, 2014–2024. [Google Scholar] [CrossRef]

- Dieter, M.; Weimar, H.; Iost, S.; Englert, H.; Fischer, R.; Günter, S.; Morland, C.; Roering, H.-W.; Schier, F.; Seintsch, B.; et al. Assessment of Possible Leakage Effects of Implementing EU COM Proposals for the EU Biodiversity Strategy on Forestry and Forests in Non-EU Countries; Thünen Working Paper No. 159; Johann Heinrich von Thünen-Institut: Braunschweig, Germany, 2020; Available online: https://www.thuenen.de/media/publikationen/thuenen-workingpaper/ThuenenWorkingPaper_159.pdf (accessed on 10 June 2022).

- FAOSTAT. Forestry Production and Trade: Datenbank. Available online: https://www.fao.org/faostat/en/#data/FO (accessed on 12 October 2021).

- Nakicenovic, N.; Alcamo, J.; Davis, G.; de Vries, B.; Fenhann, J.; Gaffin, S.; Gregory, K.; Grübler, A.; Jung, T.Y.; Kram, T.; et al. Special Report on Emissions Scenarios: A Special Report of Working Group III of the Intergovernmental Panel on Climate Change; Cambridge University Press: Cambridge, MA, USA, 2000; Available online: https://www.ipcc.ch/site/assets/uploads/2018/03/emissions_scenarios-1.pdf (accessed on 8 September 2020).

- FAO. Global Forest Resources Assessment 2010. Available online: http://www.fao.org/forest-resources-assessment/past-assessments/fra-2010/en/ (accessed on 30 September 2020).

- O’Neill, B.C.; Kriegler, E.; Riahi, K.; Ebi, K.L.; Hallegatte, S.; Carter, T.R.; Mathur, R.; van Vuuren, D.P. A new scenario framework for climate change research: The concept of shared socioeconomic pathways. Clim. Chang. 2014, 122, 387–400. [Google Scholar] [CrossRef] [Green Version]

- FAO. Global Forest Resources Assessment. 2022. Available online: https://fra-data.fao.org/ (accessed on 10 June 2022).

- Moiseyev, A.; Solberg, B.; Michie, B.; Kallio, A.M.I. Modeling the impacts of policy measures to prevent import of illegal wood and wood products. For. Policy Econ. 2010, 12, 24–30. [Google Scholar] [CrossRef]

- Kosow, H.; Gaßner, R. Methods of Future and Scenario Analysis: Overview, Assessment, and Selection Criteria; DIE Studies No. 39; German Development Institute: Bonn, Germany, 2008; Available online: https://nbn-resolving.org/urn:nbn:de:0168-ssoar-193660 (accessed on 10 June 2022).

- Buongiorno, J.; Zhu, S.; Zhang, D.; Turner, J.; Tomberlin, D. The Global Forest Products Model; Academic Press: Cambridge, MA, USA, 2003; ISBN 978-0-12-141362-0. [Google Scholar]

- Hermoso, V.; Carvalho, S.B.; Giakoumi, S.; Goldsborough, D.; Katsanevakis, S.; Leontiou, S.; Markantonatou, V.; Rumes, B.; Vogiatzakis, I.N.; Yates, K.L. The EU Biodiversity Strategy for 2030: Opportunities and challenges on the path towards biodiversity recovery. Environ. Sci. Policy 2022, 127, 263–271. [Google Scholar] [CrossRef]

- Timm, S.; Dieter, M.; Fischer, R.; Günter, S.; Heinrich, B.; Iost, S.; Matthes, U.; Rock, J.; Rüter, S.; Schabel, A.; et al. Konsequenzen der „EU-Biodiversitätsstrategie 2030“ für Wald und Forstwirtschaft in Deutschland: Abschlussbericht. 2022. Available online: https://www.lwf.bayern.de/mam/cms04/service/dateien/ma17_biodiversit%C3%A4tsstrategie-bericht.pdf (accessed on 13 June 2022).

- Rock, J.; Dunger, K.; Marks, A.; Schmidt, U. Wald und Rohholzpotenzial der nächsten 40 Jahre: Ausgewählte Ergebnisse der Waldentwicklungs- und Holzaufkommensmodellierung 2013 bis 2052. 2016. Available online: https://www.bmel.de/SharedDocs/Downloads/DE/Broschueren/Wald-Rohholzpotential-40Jahre.pdf;jsessionid=ED7D78C8F7B6DFD567C2D6475DD49EAA.internet2841?__blob=publicationFile&v=3 (accessed on 19 August 2020).

- BWI. Dritte Bundeswaldinventur-Ergebnisdatenbank. Available online: https://bwi.info/start.aspx (accessed on 7 August 2020).

- Dudley, N. Guidelines for Applying Protected Area Management Categories; Best Practice Protected Area Guidelines Series, No. 21; IUCN: Gland, Switzerland, 2008; Available online: https://portals.iucn.org/library/sites/library/files/documents/PAG-021.pdf (accessed on 10 June 2022).

- FAO. Global Forest Resources Assessment: Terms and Definitions; Forest Resources Assessment Working Paper 188; FAO: Rome, Italia, 2020; Available online: http://www.fao.org/3/I8661EN/i8661en.pdf (accessed on 7 September 2020).

- Forest Europe. State of Europe’s Forests. 2020. Available online: https://foresteurope.org/wp-content/uploads/2016/08/SoEF_2020.pdf (accessed on 10 June 2022).

- Röder, N.; Laggner, B. Landnutzung in Deutschland Nach Rechtlichem Schutzstatus der Flächen; Johann Heinrich von Thünen-Institut: Braunschweig, Germany, 2020; (Unpublished). [Google Scholar]

- Steinacker, C.; Engel, F.; Meyer, P. Natürliche Waldentwicklung: Wird das 5%-Ziel erreicht? Dtsch. Wald. 2020, 15–16. [Google Scholar]

- BMUB. Nationale Strategie Zur Biologischen Vielfalt: Kabinettsbeschluss Vom 7. November 2007, Berlin. 2007. Available online: https://www.bmuv.de/fileadmin/Daten_BMU/Pools/Broschueren/nationale_strategie_biologische_vielfalt_2015_bf.pdf (accessed on 12 July 2022).

- NW-FVA. Schutzgebiete NWE, FFH, SPA in Deutschland: Auswertung von Daten des Bundesamtes für Naturschutz (2020); Nordwestdeutsche Forstliche Versuchsanstalt: Göttingen, Germany, 2021. [Google Scholar]

- Rosenkranz, L.; Seintsch, B.; Wippel, B.; Dieter, M. Income losses due to the implementation of the Habitats Directive in forests—Conclusions from a case study in Germany. For. Policy Econ. 2014, 38, 207–218. [Google Scholar] [CrossRef]

- Rosenkranz, L.; Seintsch, B. Opportunitätskostenanalyse zur Implementierung des naturschutzorientierten Waldbehandlungskonzepts “Neue Multifunktionalität“. Landbauforsch. Appl. Agric. For. Res. 2015, 65, 145–160. [Google Scholar] [CrossRef]

- Sjølie, H.K.; Latta, G.S.; Solberg, B. Combining backcasting with forest sector projection models to provide paths into the future bio-economy. Scand. J. For. Res. 2016, 31, 708–718. [Google Scholar] [CrossRef]

- Hurmekoski, E.; Sjølie, H.K. Comparing forest sector modelling and qualitative foresight analysis: Cases on wood products industry. JFE 2018, 31, 11–16. [Google Scholar] [CrossRef]

- ten Brink, P.; Badura, T.; Bassi, S.; Daly, E.; Dickie, I.; Ding, H.; Gantioler, S.; Gerdes, H.; Kettunen, M.; Lago, M.; et al. Estimating the Overall Economic Value of the Benefits Provided by the Natura 2000 Network: Final Report to the European Commission; DG Environment on Contract ENV.B.2/SER/2008/0038; Institute for European Environmental Policy (IEEP), GHK., Ecologic Institute: Brussels, Belgium, 2011. [Google Scholar]

- Kallio, A.M.I.; Maarit, I.; Moiseyev, A.; Solberg, B. Economic impacts of increased forest conservation in Europe: A forest sector model analysis. Environ. Sci. Policy 2006, 9, 457–465. [Google Scholar] [CrossRef]

- Schier, F.; Weimar, H. Holzmarktmodellierung-Szenarienbasierte Folgenabschätzung verschiedener Rohholzangebotssituationen für den Sektor Forst und Holz; Thünen Working Paper 2018; Johann Heinrich von Thünen-Institut: Braunschweig, Germany, 2018. [Google Scholar] [CrossRef]

- van Kooten, G.C.; Johnston, C. Global impacts of Russian log export restrictions and the Canada–U.S. lumber dispute: Modeling trade in logs and lumber. For. Policy Econ. 2014, 39, 54–66. [Google Scholar] [CrossRef]

- Nepal, P.; Ince, P.J.; Skog, K.E.; Chang, S.J. Projection of U.S. forest sector carbon sequestration under U.S. and global timber market and wood energy consumption scenarios, 2010–2060. Biomass Bioenergy 2012, 45, 251–264. [Google Scholar] [CrossRef]

- Buongiorno, J. Global modelling to predict timber production and prices: The GFPM approach. Forestry 2015, 88, 291–303. [Google Scholar] [CrossRef]

- Turner, J.A.; Buongiorno, J.; Katz, A.; Zhu, S. Implications of the Russian roundwood export tax for the Russian and global wood products sectors. Scand. J. For. Res. 2008, 23, 154–166. [Google Scholar] [CrossRef]

- Johnston, C.M.T.; Buongiorno, J. Impact of Brexit on the forest products industry of the United Kingdom and the rest of the world. Forestry 2017, 90, 47–57. [Google Scholar] [CrossRef]

- Buongiorno, J.; Zhu, S. Consequences of carbon offset payments for the global forest sector. JFE 2013, 19, 384–401. [Google Scholar] [CrossRef]

- Buongiorno, J.; Johnston, C.; Zhu, S. An assessment of gains and losses from international trade in the forest sector. For. Policy Econ. 2017, 80, 209–217. [Google Scholar] [CrossRef] [Green Version]

- Morland, C.; Schier, F.; Weimar, H. The Structural Gravity Model and Its Implications on Global Forest Product Trade. Forests 2020, 11, 178. [Google Scholar] [CrossRef] [Green Version]

- Schier, F.; Morland, C.; Janzen, N.; Weimar, H. Impacts of changing coniferous and non-coniferous wood supply on forest product markets: A German scenario case study. Eur. J. For. Res. 2018, 137, 279–300. [Google Scholar] [CrossRef]

- World Bank. World Development Indicators|DataBank. Available online: https://databank.worldbank.org/source/world-development-indicators (accessed on 4 September 2020).

- Panayotou, T. Empirical Tests and Policy Analysis of Environmental Degradation at Different Stages of Economic Development; Working Paper No. 238; International Labour Organization: Geneva, Switzerland, 1993; Available online: http://www.ilo.org/public/libdoc/ilo/1993/93B09_31_engl.pdf (accessed on 4 April 2022).

- Riahi, K.; van Vuuren, D.P.; Kriegler, E.; Edmonds, J.; O’Neill, B.C.; Fujimori, S.; Bauer, N.; Calvin, K.; Dellink, R.; Fricko, O.; et al. The Shared Socioeconomic Pathways and their energy, land use, and greenhouse gas emissions implications: An overview. Glob. Environ. Chang. 2017, 42, 153–168. [Google Scholar] [CrossRef] [Green Version]

- Morland, C.; Schier, F.; Janzen, N.; Weimar, H. Supply and demand functions for global wood markets: Specification and plausibility testing of econometric models within the global forest sector. For. Policy Econ. 2018, 92, 92–105. [Google Scholar] [CrossRef]

- UNEP. Global Environment Outlook 3: Past, Present and Future perspectives. 2002. Available online: https://wedocs.unep.org/bitstream/handle/20.500.11822/8609/GEO-3%20REPORT_English.pdf?sequence=7&isAllowed=y (accessed on 10 June 2022).

- Grunwald, A. Technikfolgenabschätzung: Eine Einführung; Sigma: Berlin, Germany, 2002; ISBN 3894049316. [Google Scholar]

- Solberg, B.; Moiseyev, A.; Kallio, A.M.I.; Toppinen, A. Forest sector market impacts of changed roundwood export tariffs and investment climate in Russia. For. Policy Econ. 2010, 12, 17–23. [Google Scholar] [CrossRef]

- EC. Criteria and Guidance for Protected Areas Designations. Available online: https://circabc.europa.eu/ui/group/6f30d1d2-d6f2-4c6e-a4dc-1feb66201929/library/89652963-8cc4-459a-b24f-19373ea73fbf/details (accessed on 11 March 2022).

- Im, E.H.; Adana, D.M.; Latta, G.S. Potential impacts of carbon taxes on carbon flux in western Oregon private forests. For. Policy Econ. 2007, 9, 1006–1017. [Google Scholar] [CrossRef]

- Buongiorno, J.; Johnston, C. Effects of parameter and data uncertainty on long-term projections in a model of the global forest sector. For. Policy Econ. 2018, 93, 10–17. [Google Scholar] [CrossRef]

- Kallio, A.M.I. Accounting for uncertainty in a forest sector model using Monte Carlo simulation. For. Policy Econ. 2010, 12, 9–16. [Google Scholar] [CrossRef]

| Class | Attribution | Specification | |

|---|---|---|---|

| Scope | time | long-term horizon | 2017–2050 |

| geopraphic | global | EU and worldwide | |

| thematic | policy evaluation | forest protection measures and leakage | |

| Character | explorative | explorative-descriptive scenarios | test “what if” the EUBDS would be implemented |

| normative | - | normative character given by EUBDS1 | |

| Type | quantitative | formalized scenarios | mathematical and model-based approach |

| qualitative | - | qualitative elements given by EUBDS1 | |

| Purpose | alternative | alternative scenarios | explore options for actions “if we change the road” |

| reference | - | reference adapted from other sources1 |

| EUBDS Objectives | Moderate Scenario | Intensive Scenario |

|---|---|---|

| “1. Legally protect a minimum of 30% of the EU’s land area and 30% of the EU’s sea area and integrate ecological corridors, as part of a true Trans-European Nature Network.” |

|

|

| “2. Strictly protect at least a third of the EU’s protected areas, including all remaining EU primary and old-growth forests.” |

|

|

| “3. Effectively manage all protected areas, defining clear conservation objectives and measures, and monitoring them appropriately.” |

|

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Schier, F.; Iost, S.; Seintsch, B.; Weimar, H.; Dieter, M. Assessment of Possible Production Leakage from Implementing the EU Biodiversity Strategy on Forest Product Markets. Forests 2022, 13, 1225. https://doi.org/10.3390/f13081225

Schier F, Iost S, Seintsch B, Weimar H, Dieter M. Assessment of Possible Production Leakage from Implementing the EU Biodiversity Strategy on Forest Product Markets. Forests. 2022; 13(8):1225. https://doi.org/10.3390/f13081225

Chicago/Turabian StyleSchier, Franziska, Susanne Iost, Björn Seintsch, Holger Weimar, and Matthias Dieter. 2022. "Assessment of Possible Production Leakage from Implementing the EU Biodiversity Strategy on Forest Product Markets" Forests 13, no. 8: 1225. https://doi.org/10.3390/f13081225