A Two-Phase Hybrid Trading of Green Certificate under Renewables Portfolio Standards in Community of Active Energy Agents

Abstract

:1. Introduction

- (1)

- The GC trading of AEA community under RPS is considered, and a two-phase hybrid mechanism combining P2P trading and centralized settlement is proposed.

- (2)

- The diversity of individual behaviors in GC trading is regarded, two types of AEAs are defined: naïve and sophisticated, and the impacts on updating quotation and concluding deals are quantitatively investigated.

- (3)

- The overall efficiency of GC trading is taken into account, a multi-option-based matching is designed to facilitate the P2P order-matching, and the parameters are numerically optimized.

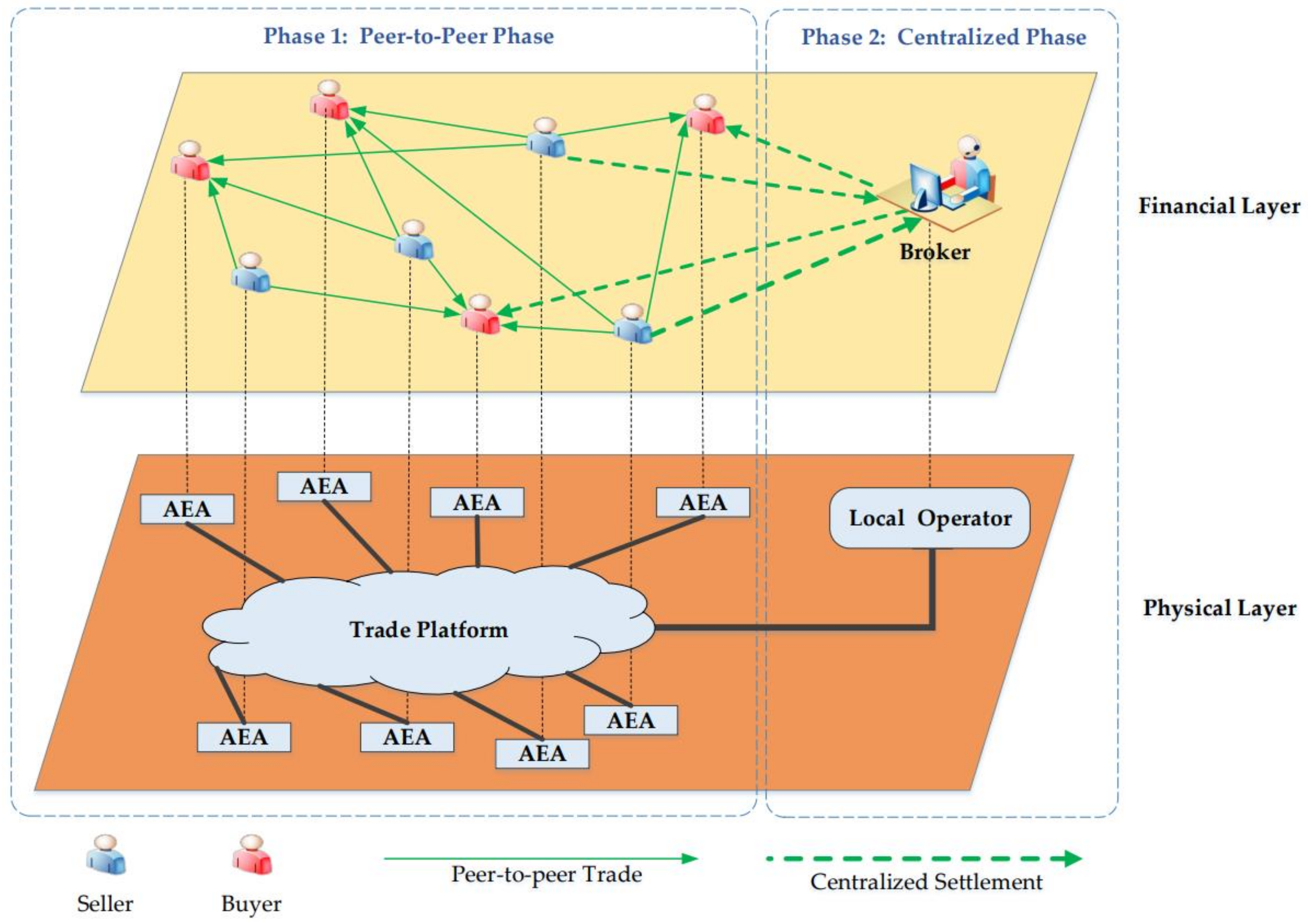

2. System Description

2.1. Structure of Market

2.2. Process of Trading

2.3. Types of AEA

- Naïve AEA: Naïve AEAs are work-sensitive and aim to conclude deals with minimum work. In Step 2, a naïve AEA attempts to find partners which provide abundant amount, and in Step 3, a naïve AEA adjusts quotation by compromising the market price and the latest quotation of its own.

- Sophisticated AEA: Sophisticated AEAs are profit-sensitive and aim to conclude deals for maximum profit. In Step 2, a sophisticated AEA attempts to find partners which provide favorable quotations, and in Step 3, a sophisticated AEA adjusts quotation by compromising not only the market price and its latest quotation, but also the time pressure.

3. Problem Formulation

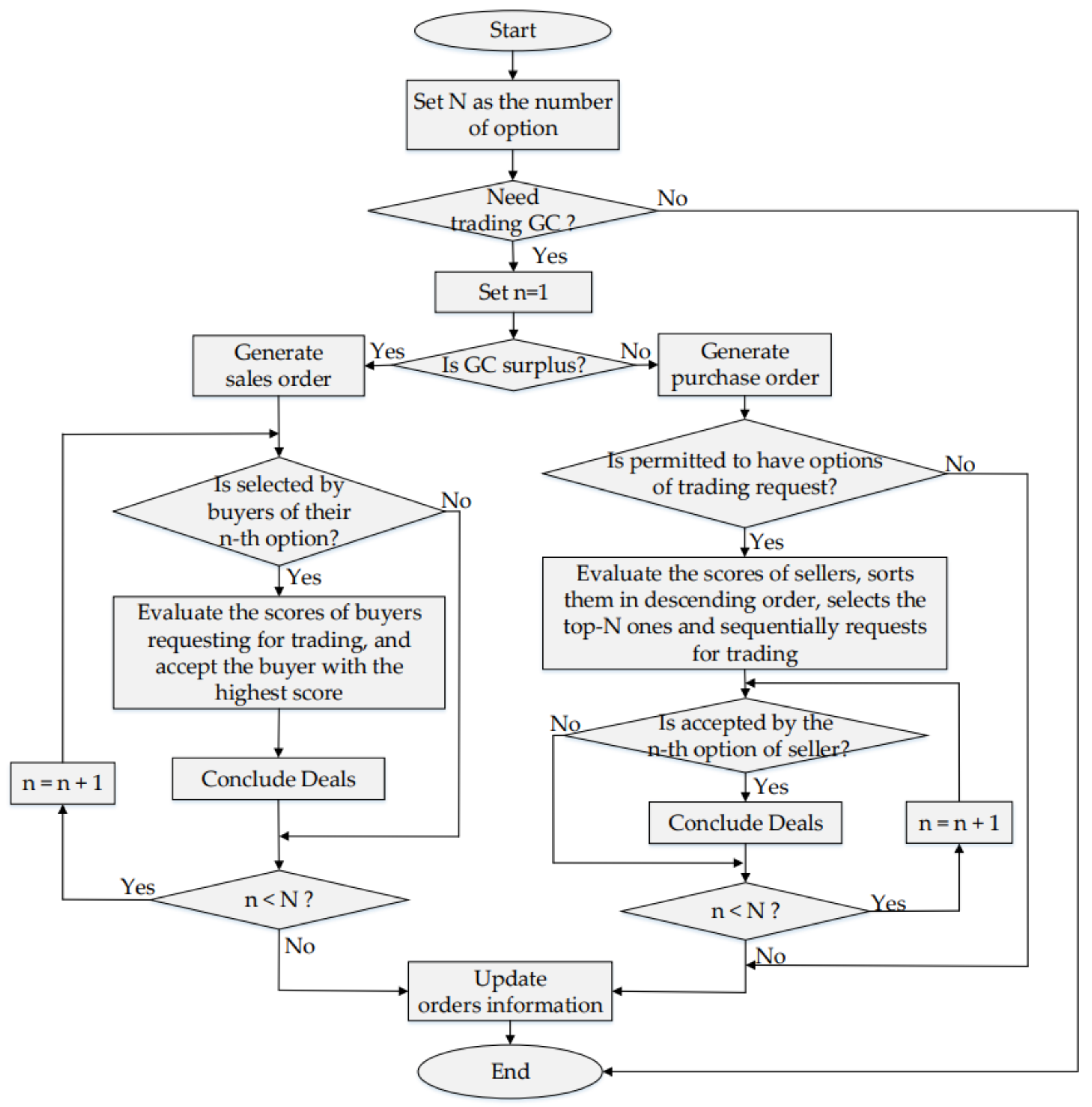

3.1. Initializing Order

3.2. Finding Partner

3.2.1. Scoring Partner

- Factor 1: GC quotation

- Factor 2: GC abundance

3.2.2. Multi-Option-Based Matching

3.3. Updating Order

4. Numeric Studies

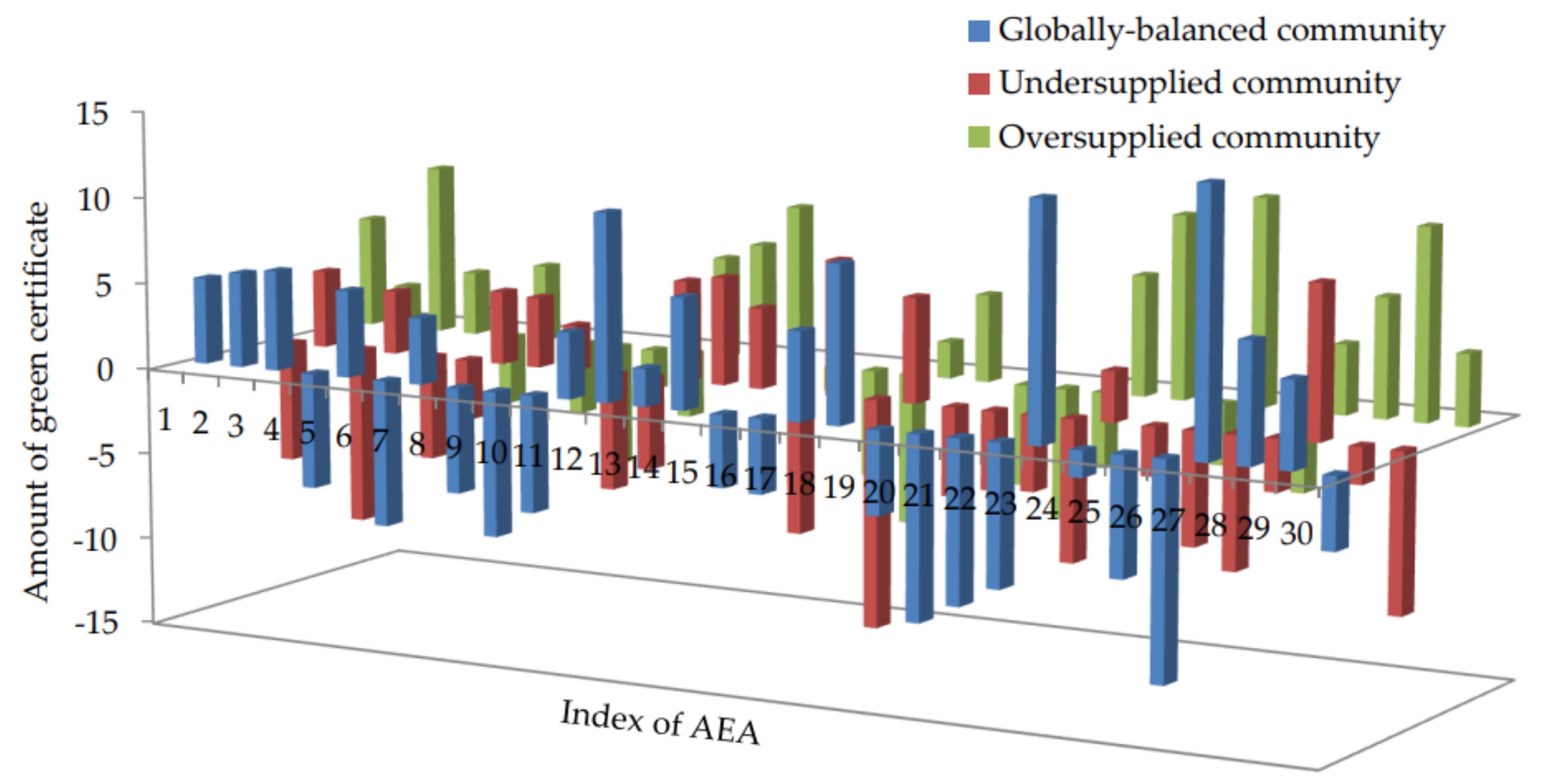

4.1. Simulation Setups

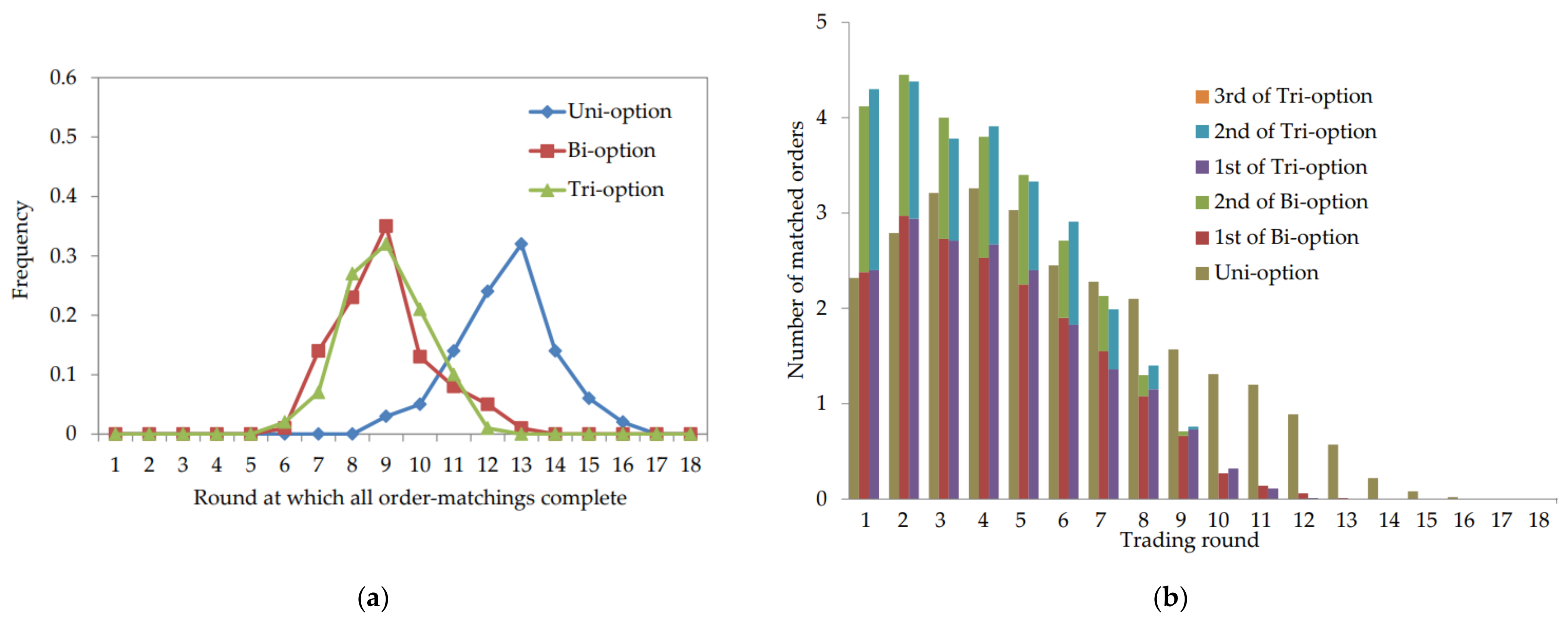

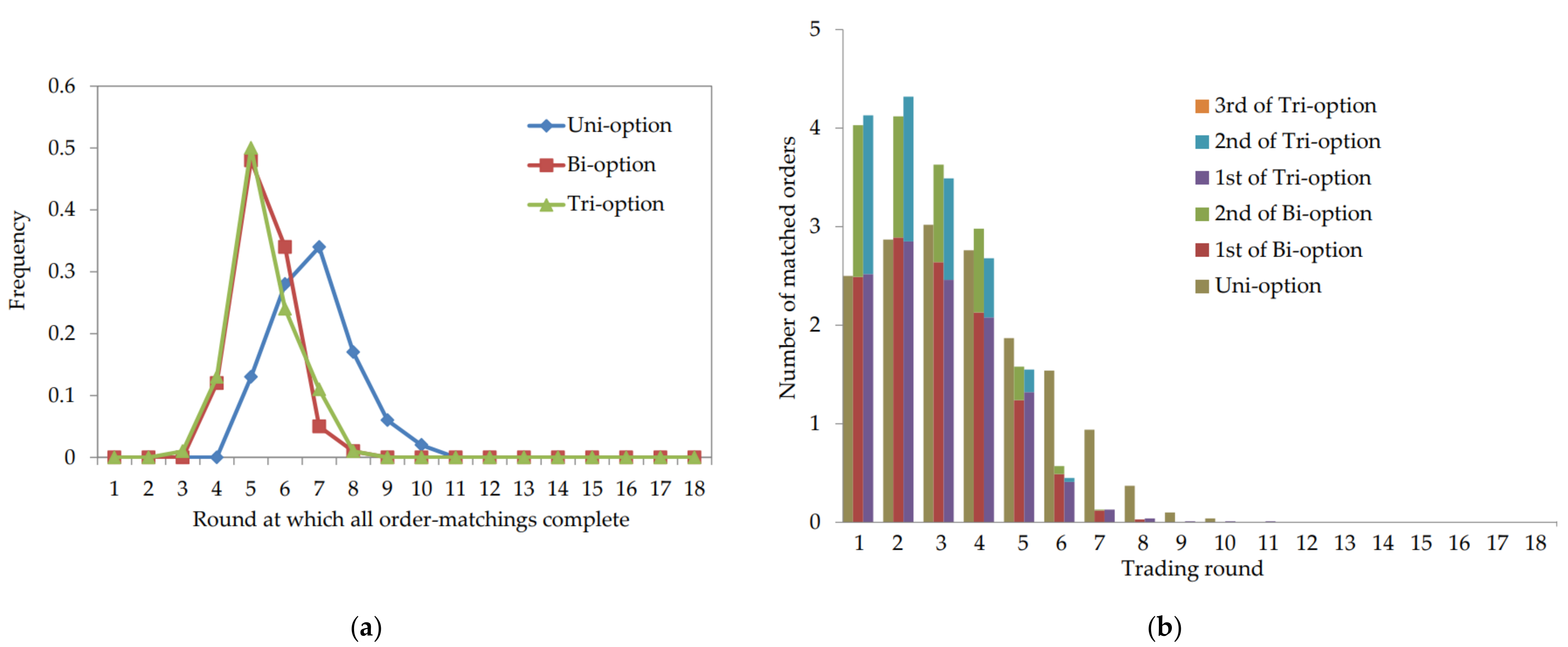

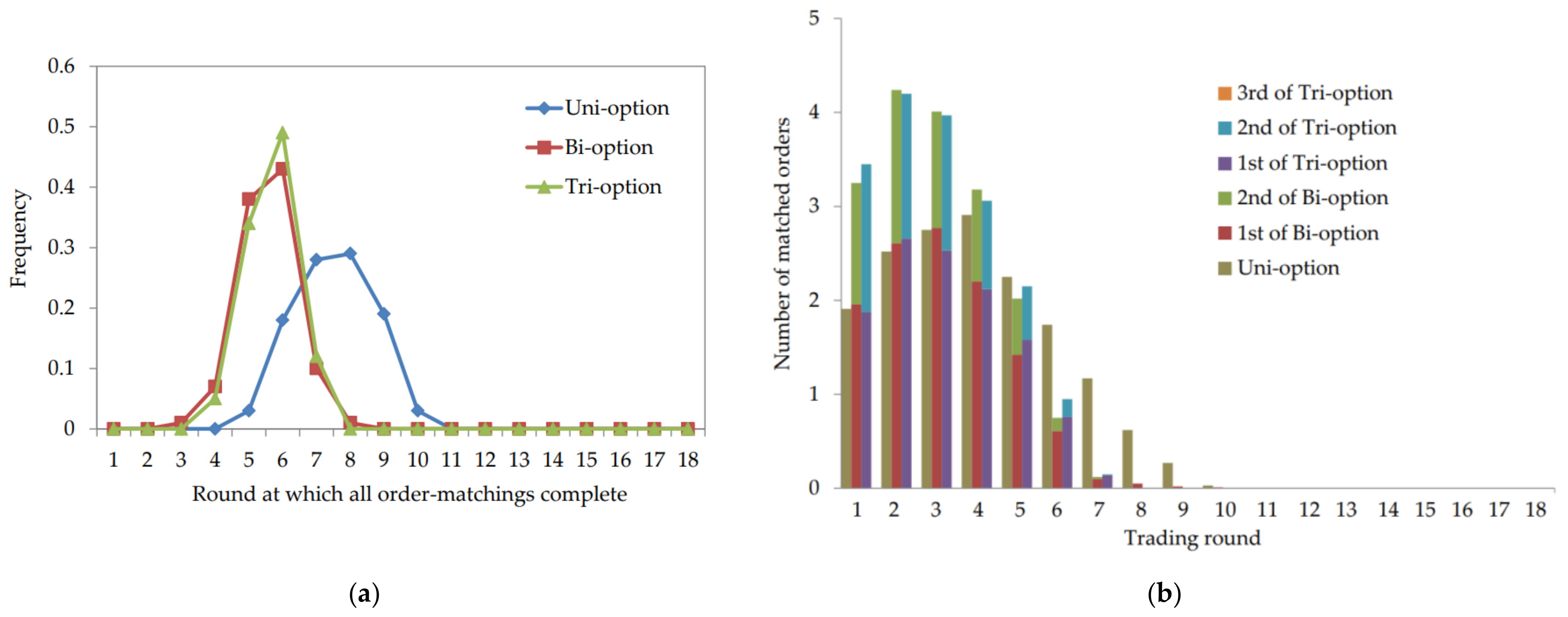

4.2. Determination of Key Parameters

- (a)

- Uni-option: N = 1;

- (b)

- Bi-option: N = 2;

- (c)

- Tri-option: N = 3.

4.3. Verification

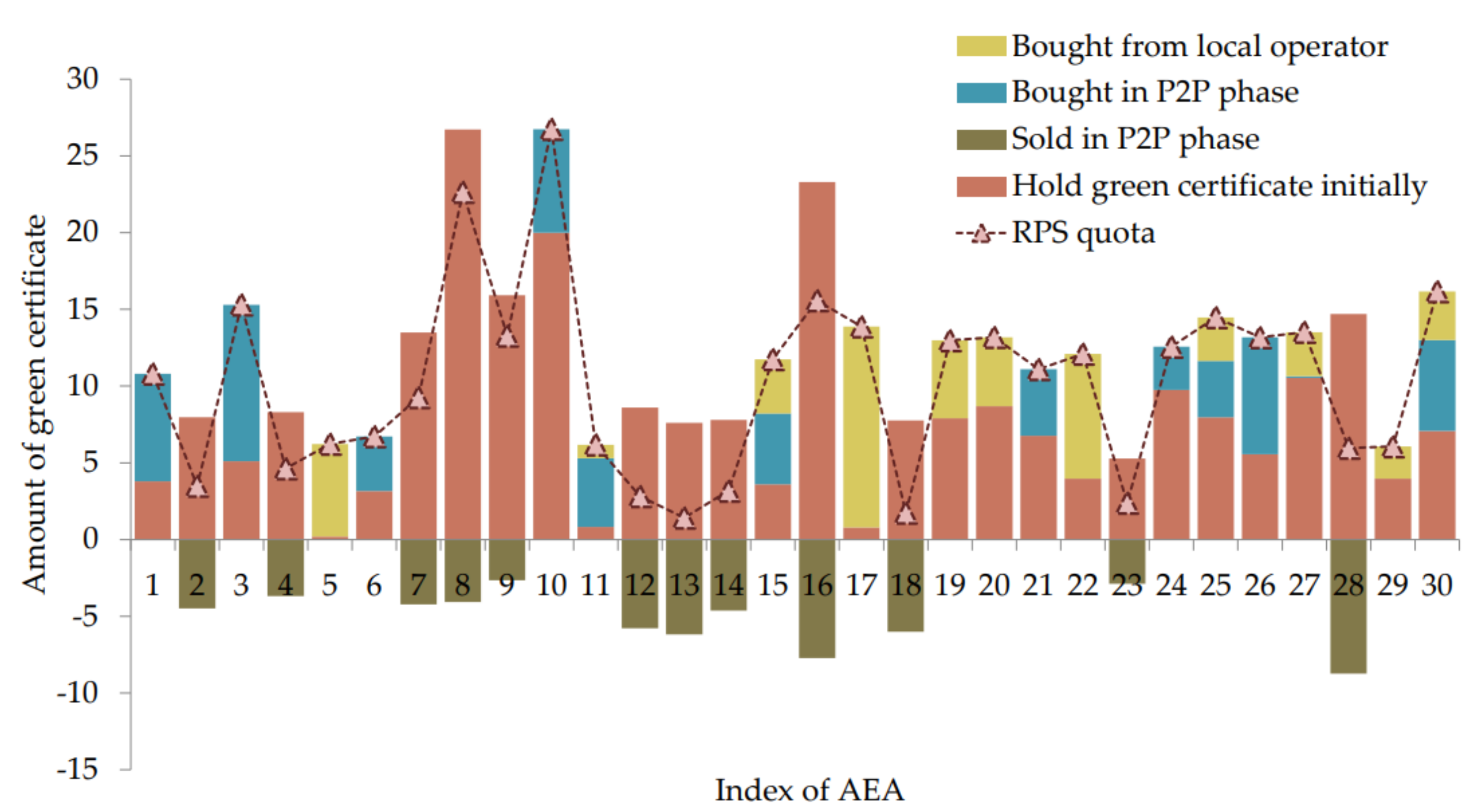

4.3.1. Overall Trading Results

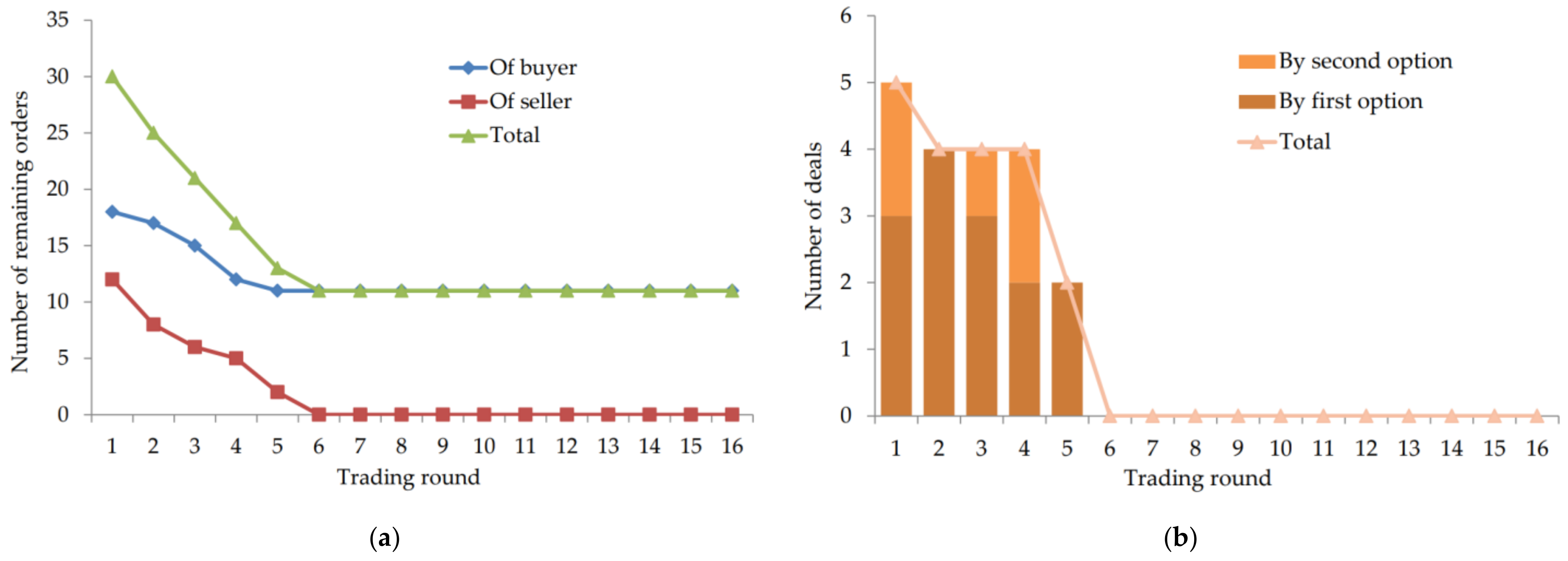

4.3.2. P2P Matching Orders

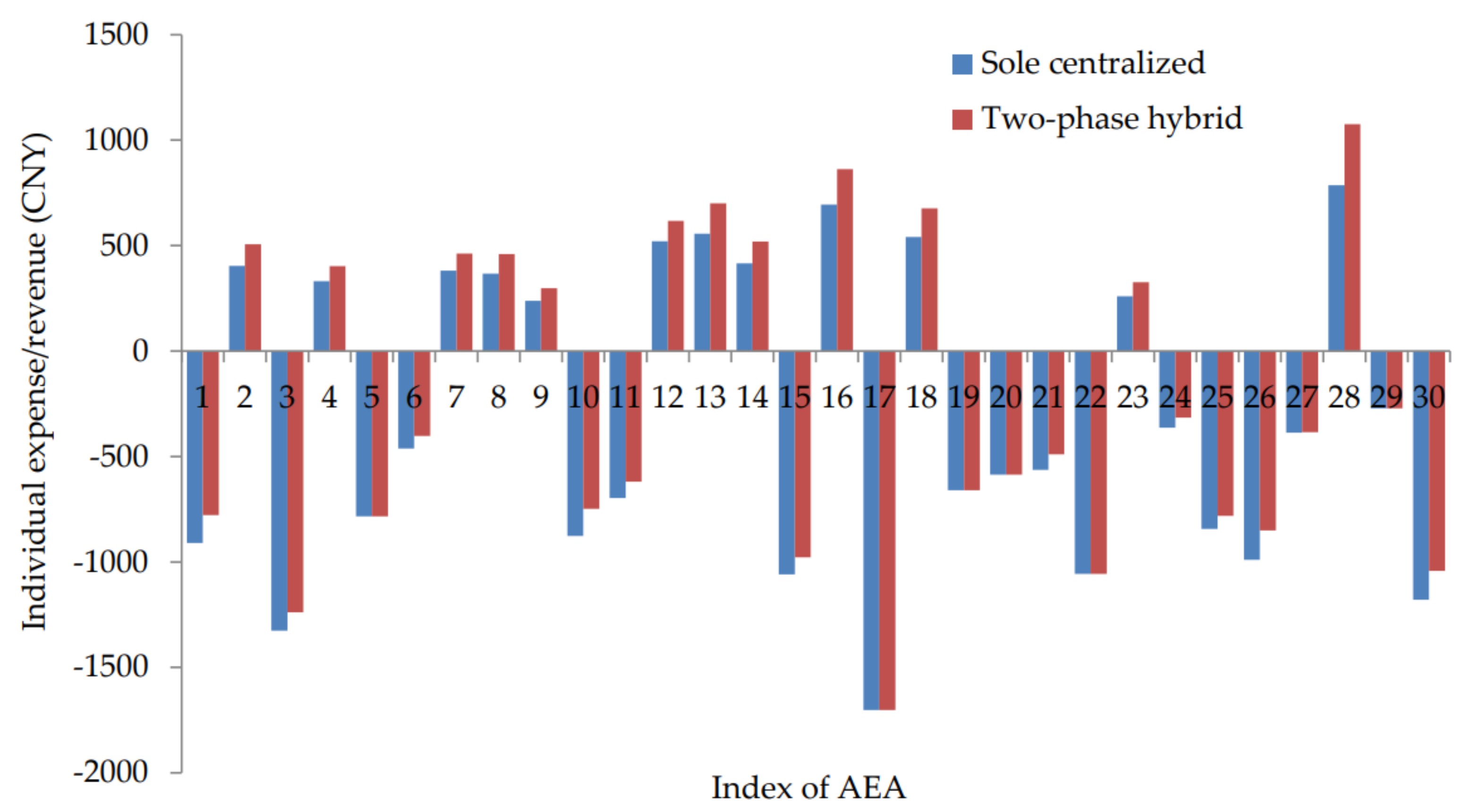

4.3.3. Economic Advantages

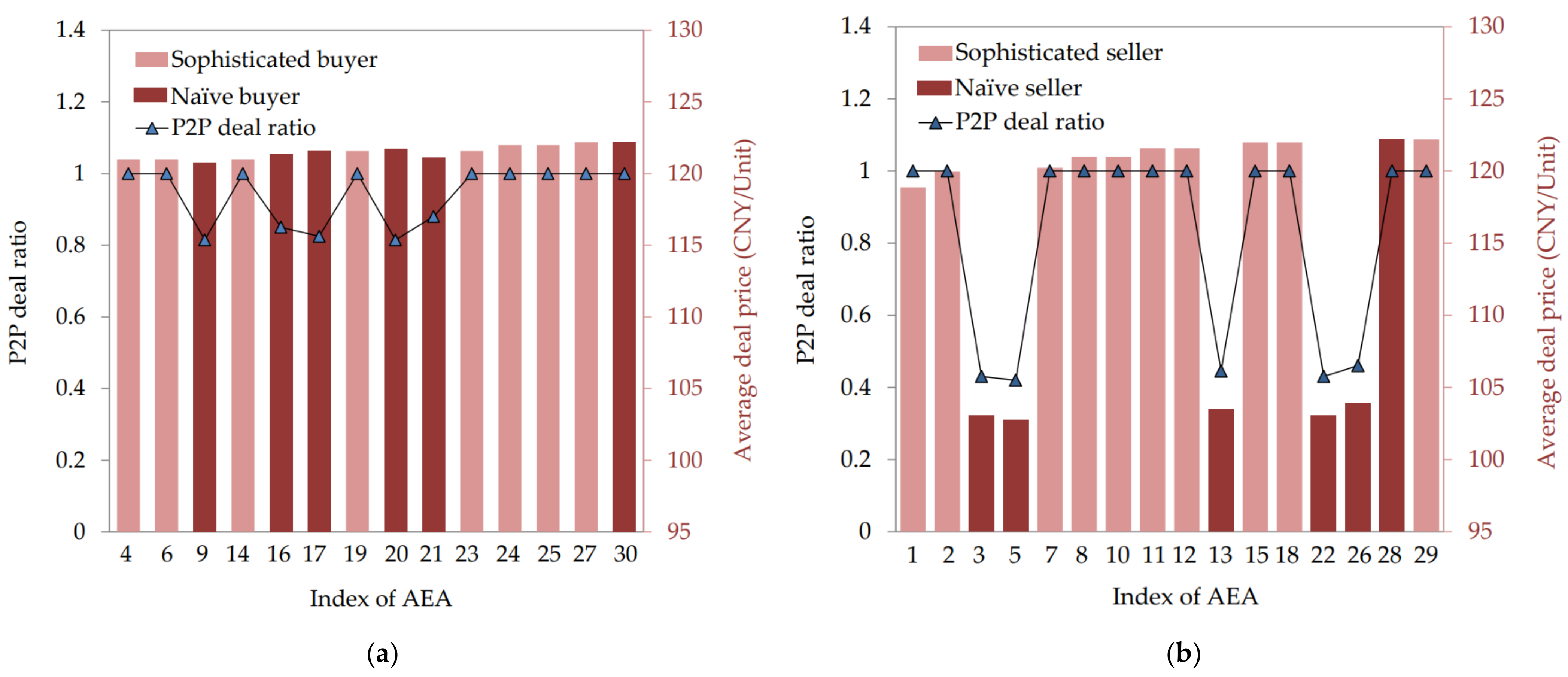

4.4. Discussion on Impact of AEA Type

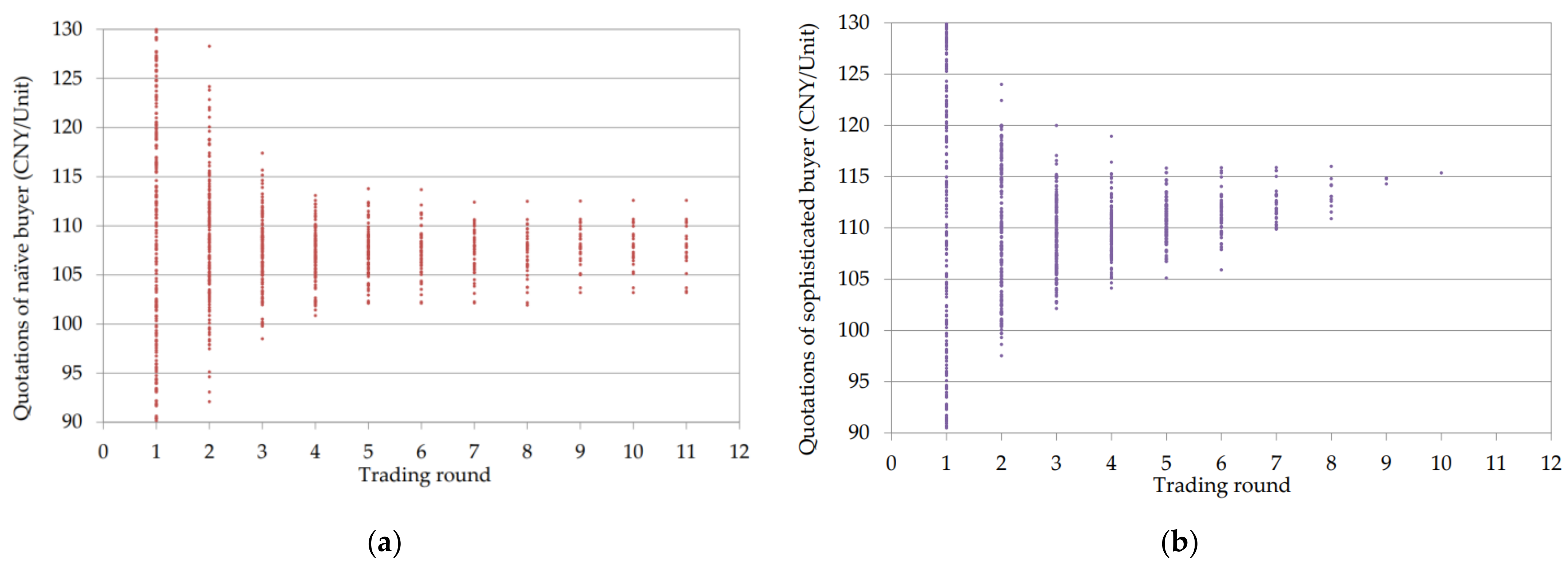

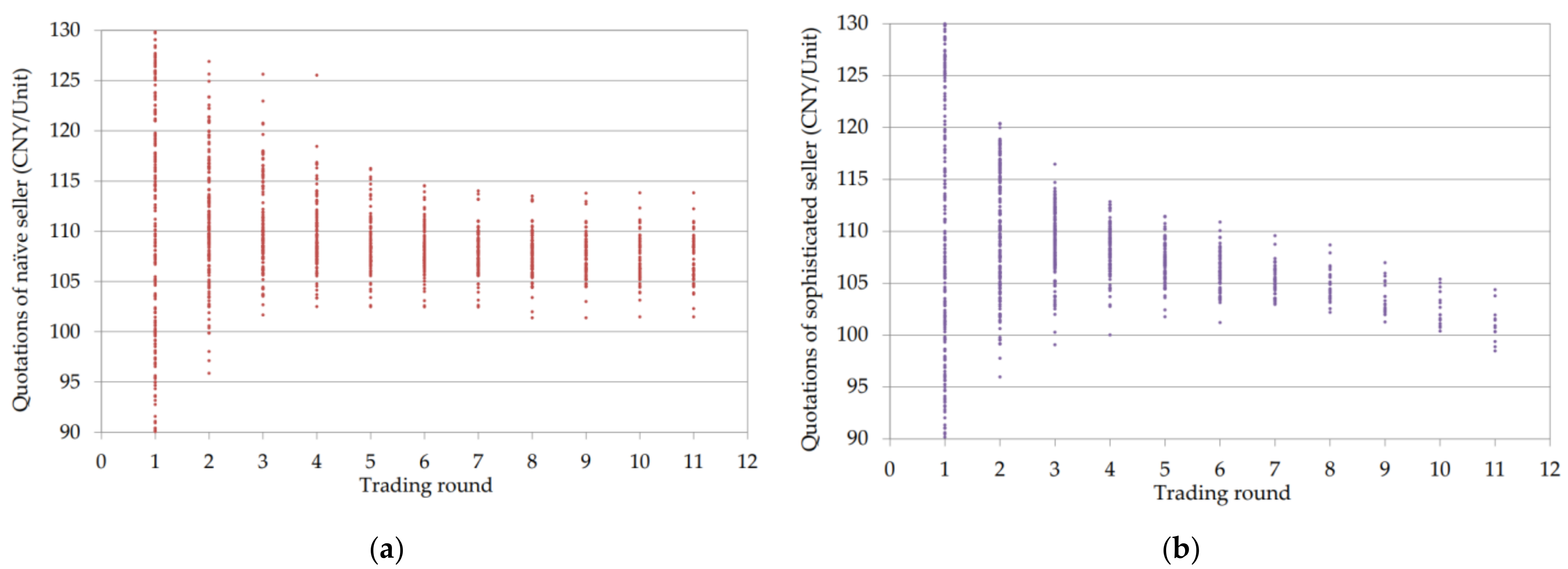

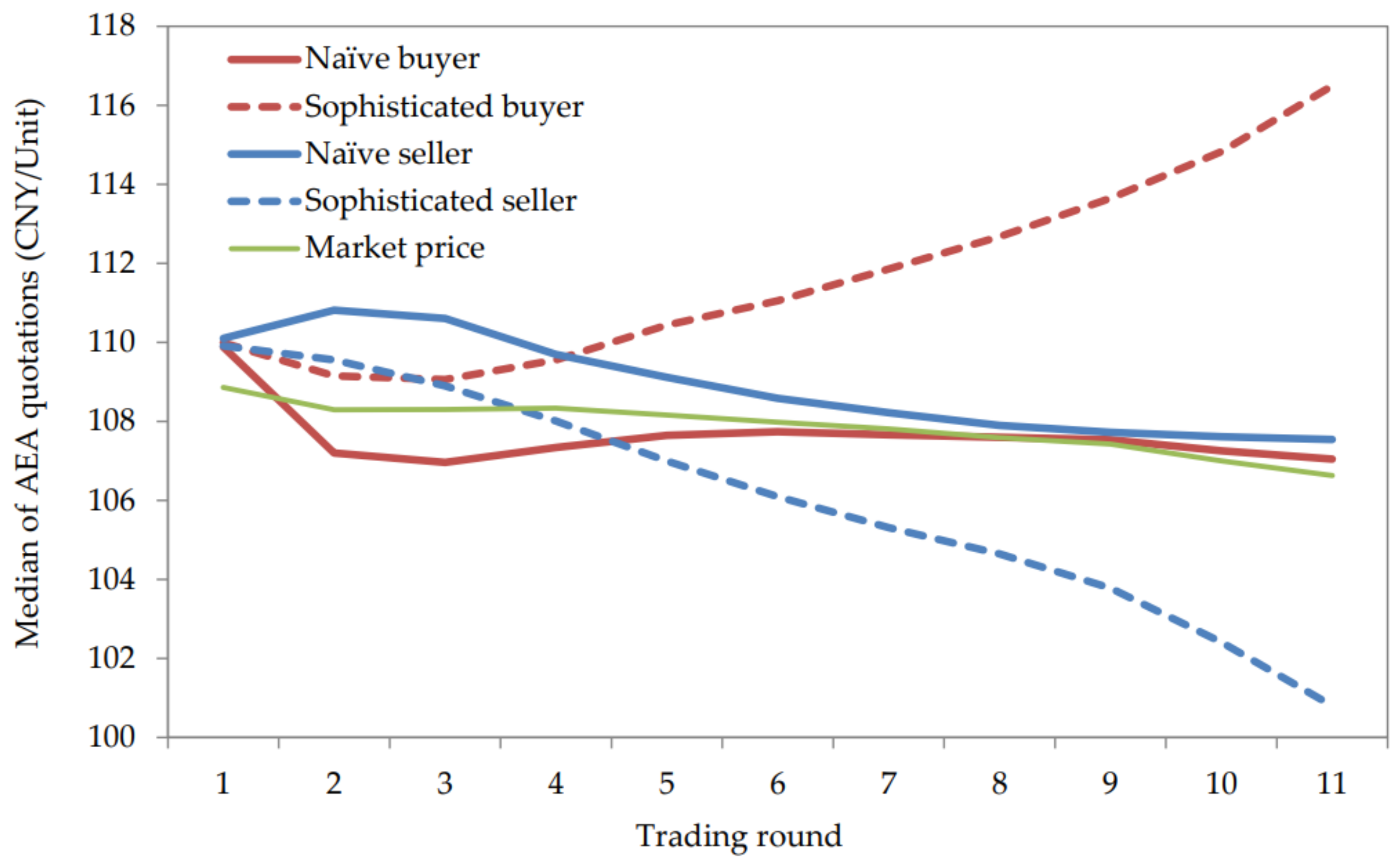

4.4.1. Impact on Updating Quotations

4.4.2. Impact on Concluding Deals

- average deal price: as for an AEA, the average price of all concluded deals in P2P phase.

- P2P deal ratio: as for an AEA, the average ratio of the amount traded in P2P phase and the total amount.

5. Conclusions and Future Work

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Index of AEA | Type of AEA | Weight of Quotation | Weight of Amount | RPS Quota |

|---|---|---|---|---|

| 1 | Sophisticated | 0.9 | 0.1 | 0.3 |

| 2 | Sophisticated | 0.8 | 0.2 | 0.11 |

| 3 | Naïve | 0.2 | 0.8 | 0.51 |

| 4 | Sophisticated | 0.55 | 0.45 | 0.11 |

| 5 | Naïve | 0.3 | 0.7 | 0.095 |

| 6 | Sophisticated | 0.6 | 0.4 | 0.23 |

| 7 | Sophisticated | 0.65 | 0.35 | 0.3 |

| 8 | Sophisticated | 0.7 | 0.3 | 0.8 |

| 9 | Naïve | 0.2 | 0.8 | 0.45 |

| 10 | Sophisticated | 0.9 | 0.1 | 0.7 |

| 11 | Sophisticated | 0.6 | 0.4 | 0.3 |

| 12 | Sophisticated | 0.55 | 0.45 | 0.22 |

| 13 | Naïve | 0.2 | 0.8 | 0.18 |

| 14 | Sophisticated | 0.7 | 0.3 | 0.3 |

| 15 | Sophisticated | 0.65 | 0.35 | 0.57 |

| 16 | Naïve | 0.35 | 0.65 | 0.76 |

| 17 | Naïve | 0.2 | 0.8 | 0.26 |

| 18 | Sophisticated | 0.8 | 0.2 | 0.17 |

| 19 | Sophisticated | 0.75 | 0.25 | 0.63 |

| 20 | Naïve | 0.25 | 0.75 | 0.66 |

| 21 | Naïve | 0.25 | 0.75 | 0.54 |

| 22 | Naïve | 0.35 | 0.65 | 0.68 |

| 23 | Sophisticated | 0.65 | 0.35 | 0.15 |

| 24 | Sophisticated | 0.85 | 0.15 | 0.49 |

| 25 | Sophisticated | 0.6 | 0.4 | 0.7 |

| 26 | Naïve | 0.2 | 0.8 | 0.78 |

| 27 | Sophisticated | 0.65 | 0.35 | 0.59 |

| 28 | Naïve | 0.2 | 0.8 | 0.56 |

| 29 | Sophisticated | 0.55 | 0.45 | 0.26 |

| 30 | Naïve | 0.25 | 0.75 | 0.67 |

References

- Jiang, Y.; Cao, H.; Yang, L.; Fei, F.; Li, J.; Lin, Z. Mechanism design and impact analysis of renewable portfolio standard. Autom. Electr. Power Syst. 2020, 44, 187–199. [Google Scholar]

- Zahedi, A. A review on feed-in tariff in Australia, what it is now and what it should be. Renew. Sustain. Energy Rev. 2010, 14, 3252–3255. [Google Scholar] [CrossRef]

- Cao, W. Local government’s consumption obligation in the construction of renewable energy quota system. Local Legis. J. 2019, 4, 91–102. [Google Scholar]

- Zhao, X.; Liang, J.; Ren, L.; Zhang, Y.; Xu, J. Top-level institutional design for energy low-carbon transition: Renewable portfolio standards. Power Syst. Technol. 2018, 42, 1164–1169. [Google Scholar]

- Lipp, J. Lessons for effective renewable electricity policy from Denmark, Germany and the United Kingdom. Energy Policy 2007, 35, 5481–5495. [Google Scholar] [CrossRef]

- Matsumoto, K.; Morita, K.; Mavrakis, D.; Konidari, P. Evaluating Japanese policy instruments for the promotion of renewable energy sources. Int. J. Green Energy 2017, 14, 724–736. [Google Scholar] [CrossRef]

- Sun, Y. The optimal percentage requirement and welfare comparisons in a two-country electricity market with a common tradable green certificate system. Econ. Model. 2016, 55, 322–327. [Google Scholar] [CrossRef]

- Joshi, J. Do renewable portfolio standards increase renewable energy capacity? Evidence from the United States. J. Environ. Manag. 2021, 287, 112261. [Google Scholar] [CrossRef]

- Wiser, R.; Porter, K.; Grace, R. Evaluating experience with renewables portfolio standards in the United States. Mitig. Adapt. Strateg. Glob. Chang. 2005, 10, 237–263. [Google Scholar] [CrossRef]

- Unger, T.; Ahlgren, E.O. Impacts of a common green certificate market on electricity and CO-emission markets in the Nordic countries. Energy Policy 2005, 33, 2152–2163. [Google Scholar] [CrossRef]

- Marchenko, O.V. Modeling of a green certificate market. Renew. Energy 2008, 33, 1953–1958. [Google Scholar] [CrossRef]

- Barbose, G.; Bird, L.; Heeter, J.; Flores-Espino, F.; Wiser, R. Cost and benefits of renewables portfolio standards in the United States. Renew. Sustain. Energy Rev. 2016, 52, 523–533. [Google Scholar] [CrossRef]

- Yu, S.; Bi, P.; Yang, W.; Wang, Y.; Huang, Y.; Yu, H. Dynamic development system dynamics of renewable energy considering renewable energy quota system. Proc. Chin. Soc. Electr. Eng. 2018, 38, 2599–2608. [Google Scholar]

- Zhang, Y.; Luo, Z.; Zhou, D. Research on power absorption simulation analysis of renewable energy based on agent. J. Syst. Simul. 2020, 34, 170–178. [Google Scholar]

- An, X.; Zhang, S.; Li, X.; Du, D. Two-stage joint equilibrium model of electricity market with tradable green certificates. Trans. Inst. Meas. Control 2019, 41, 1615–1626. [Google Scholar] [CrossRef]

- Wu, Y.; Sun, M. Multi-oligarch dynamic game model for regional power market with renewable portfolio standard policies. Appl. Math. Model. 2022, 107, 591–620. [Google Scholar] [CrossRef]

- Fu, M.; Xu, Z.; Wang, N.; Lyu, X.; Xu, W. “Peer-to-Peer Plus” electricity transaction within community of active energy agents regarding distribution network constraints. Energies 2020, 13, 2408. [Google Scholar] [CrossRef]

- Morstyn, T.; Farrell, N.; Darby, S.J.; McCulloch, M.D. Using peer-to-peer energy-trading platforms to incentivize prosumers to form federated power plants. Nat. Energy 2018, 3, 94–101. [Google Scholar] [CrossRef]

- Guo, L.; Chen, X.; Deng, H.; He, Y.; Chen, Q. A framework of operating mechanism based on peer-to-peer transaction among distributed energy resources in community microgrid. Electr. Power Constr. 2018, 39, 2–9. [Google Scholar]

- Zhang, C.; Wu, J.; Zhou, Y.; Cheng, M.; Long, C. Peer-to-peer energy trading in a microgrid. Appl. Energy 2018, 220, 1–12. [Google Scholar] [CrossRef]

- Fu, M.; Xu, Z.; Lyu, X.; Xu, W.; Wang, N. Two-stage load-source coordination for multi-microgrid system: A joint approach of demand response and peer-to-peer transaction. In Proceedings of the 38th Chinese Control Conference (CCC2019), Guangzhou, China, 28–30 July 2019. [Google Scholar]

- Wang, N.; Xu, W.; Xu, Z.; Shao, W. Peer-to-peer energy trading among microgrids with multidimensional willingness. Energies 2018, 11, 3312. [Google Scholar] [CrossRef] [Green Version]

- Shen, Z.; Chen, S.; Yan, Z.; Ping, J.; Luo, B.; Shu, G. Distributed energy trading technology based on blockchain. Proc. CSEE 2021, 41, 3841–3851. [Google Scholar]

- Sun, Y.; Ling, J.; Qin, Y.; Chen, N.; Zhang, L.; Gao, B. A bidding optimization method for renewable energy cross-regional transaction under green certificate trading mechanism. Renew. Energy Resour. 2018, 36, 942–948. [Google Scholar]

- Cai, Y.; Guo, Y.; Luo, G.; Zhang, X.; Chen, Q. Blockchain based trading platform of green power certificate: Concept and practice. Autom. Electr. Power Syst. 2020, 44, 1–9. [Google Scholar]

| Scenario | Total Deficit GCs (Unit) | Total Surplus GCs (Unit) | Normalized Ratio of Surplus and Deficit |

|---|---|---|---|

| Globally-balanced community | 102.1886 | 102.5842 | 1.004/1 |

| Undersupplied community | 113.2179 | 61.036 | 0.549/1 |

| Oversupplied community | 63.2392 | 110.6169 | 1.749/1 |

| Multi-Option Setting | Globally Balanced Community | Undersupplied Community | Oversupplied Community |

|---|---|---|---|

| Uni-option | 12.53 | 6.81 | 7.52 |

| Bi-option | 8.94 | 5.35 | 5.57 |

| Tri-option | 8.97 | 5.34 | 5.68 |

| Deal No. | Buyer No. | Seller No. | GC Amount (Unit) | GC Price (CNY/Unit) |

|---|---|---|---|---|

| 1 | 10 | 7 | 4.230 | 109.099 |

| 2 | 26 | 16 | 7.614 | 111.681 |

| 3 | 3 | 28 | 8.736 | 123.123 |

| 4 | 1 | 4 | 3.679 | 109.280 |

| 5 | 30 | 12 | 5.784 | 106.715 |

| 6 | 6 | 8 | 3.556 | 113.153 |

| 7 | 27 | 16 | 0.106 | 107.505 |

| 8 | 21 | 18 | 4.337 | 112.965 |

| 9 | 1 | 23 | 2.883 | 113.081 |

| 10 | 1 | 8 | 0.438 | 112.692 |

| 11 | 24 | 9 | 2.645 | 112.611 |

| 12 | 3 | 18 | 1.464 | 111.592 |

| 13 | 10 | 13 | 2.510 | 113.975 |

| 14 | 15 | 14 | 4.620 | 112.485 |

| 15 | 24 | 18 | 0.154 | 112.513 |

| 16 | 11 | 2 | 4.482 | 112.837 |

| 17 | 30 | 8 | 0.076 | 111.463 |

| 18 | 25 | 13 | 3.668 | 113.031 |

| 19 | 30 | 18 | 0.054 | 111.214 |

| Market | Total Expense of Buyers (CNY) | Total Revenue of Sellers (CNY) |

|---|---|---|

| Sole Centralized | 14,718.33 | 5493.24 |

| Two-Phase Hybrid | 13,688.55 | 6904.91 |

| Advantage of Hybrid | −1029.78 | +1411.67 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Tan, Y.; Xu, Z.; Xu, W. A Two-Phase Hybrid Trading of Green Certificate under Renewables Portfolio Standards in Community of Active Energy Agents. Energies 2022, 15, 6915. https://doi.org/10.3390/en15196915

Tan Y, Xu Z, Xu W. A Two-Phase Hybrid Trading of Green Certificate under Renewables Portfolio Standards in Community of Active Energy Agents. Energies. 2022; 15(19):6915. https://doi.org/10.3390/en15196915

Chicago/Turabian StyleTan, Yaxin, Zhiyu Xu, and Weisheng Xu. 2022. "A Two-Phase Hybrid Trading of Green Certificate under Renewables Portfolio Standards in Community of Active Energy Agents" Energies 15, no. 19: 6915. https://doi.org/10.3390/en15196915