1. Introduction

Business profit and its stable development are key performance indicators (

Kliestik et al. 2022). According to the general theory of profitability, better indicators and higher satisfaction of the company employees lead to a higher return on the initial investment of property, capital, or other business components in the form of profit (

Visser et al. 2022). However, these measurements and assessments are only conducted at the corporate level, which can often make the real business environment look different. Even though the company achieves positive profitability values, there may be a problem if it compares itself to other companies in its industry or across the country that can achieve much better results. A high level of investment in innovation lays the foundation for economic stability during COVID-19 (

Didenko et al. 2022). After the COVID-19 era, the competition became even tougher, so it is important to keep an eye not only on your own company but also on the competition in general (

Aydogmus et al. 2022). It is also more challenging to obtain optimal outcomes, especially for business entities in different country classifications; for instance, there are different criteria for companies operating in developed versus developing countries (

Almashhadani 2021). This “gap” is even larger if we consider companies with varying numbers of board members (

Alabdullah et al. 2021), the company’s history (i.e., age and size) (

Mahmood et al. 2019), and the country’s GDP growth rate (

Kaya 2015). Other things, such as the government and its rules or the corporate culture itself, also affect how profitable a business is as a whole (

Akhmadi and Januarsi 2021).

Different study results—in particular, how popular the profitability solution is in different parts of the world—led to the creation of this scientific article on the conditions in Central Europe. Thus, the goal of this article was to ascertain whether particular profitability indicators also revealed the pandemic-related global crisis, particularly in the Visegrad Group countries. Visegrad Four was chosen because it is the largest grouping of Central European countries. A cultural and political alliance of Hungary, Poland, Czech Republic, and Slovakia is known collectively as the Visegrad Group, or V4 (

Ghani et al. 2022). This study was also influenced by the research findings of

Hassan (

2022), who solved the issue of profitability using a variety of mathematical and statistical techniques. The contribution of this study, compared with previous studies, is a comprehensive individual assessment of all categories of business according to the size of the V4 region. The investigation is based on robust samples, and it looks at the issue of enterprise size categories and how profitability indicators changed before, during, and after the pandemic. The novelty also comes from the applied methodology.

The article is divided into several sections as shown in

Figure 1. First, recent approaches and incentives on the issue of profitability are identified in the literature review. Then, materials and methods are discussed, with a focus on the group of businesses that serve as the foundation for the development of a scientific article. The requirements that the companies had to meet to take part in the study are described, as well as the total number of companies that participated, with a clear breakdown of the companies by size category and by the state where their size category is most common, and the total number of participating companies. Indicators of profitability, which are the primary pillars of scientific output, are analyzed. To make the research clearer, the highest and lowest measured values of each business’s profitability are also included, as well as the values of mean, standard deviation, and median for each business size category. Companies are classified based on whether profitability indicators experienced a significant change in a positive direction, a significant change in a negative direction, or no significant change over the monitored period of 2019–2021 based on the one-sample Wilcoxon signed-rank test. Next, the issue of contingency tables is solved, which are used to figure out how variables depend on each other. The last thing is the correspondence analysis, which is used to make graphs of the results for each indicator of profitability and size category of businesses over time. In addition, the article contains a description of the results, which is supplemented by tables and a description of each table in order to create a clear picture of the outputs that were measured throughout the monitored period. In

Section 5, the obtained results are compared with those obtained by other authors, and many observations and opinions are added. In

Section 6, the conclusions drawn from the findings of the study are evaluated, the limitations of the study are listed, and suggestions for future research are given.

2. Literature Review

Profitability is not just a group of indicators that have been studied in many investigations. For example, ROA (Return on Assets) was discussed by

Sohibien et al. (

2022). ROE (Return on Equity) was analyzed by

Habibniya et al. (

2022), and

Anton and Afloarei Nucu (

2020). ROS (Return on Sales) was evaluated by

Avi (

2022). ROR (Return on Revenue) was assessed by

Rupp et al. (

2022). Finally, ROI (Return on Investment) was highlighted by

Murphy et al. (

2022). To figure out how profitable something is, different variables that make up the denominator of the formula can be used. One of these variables is wages. When a social contribution for employees is built into a business model, wages become more profitable (

Cho et al. 2019). This contribution improves the performance of employees. A situation where employees have a high level of intellectual capital (

Ovechkin et al. 2021) and are motivated by social contribution leads to the creation of business efficiency, as intellectual character can be transformed through the advancement of science and technology for the profit of the business, thereby increasing the profitability of the economic unit (

Daneshgar and Zahedi 2022).

Anton (

2021) writes an interesting article about how to increase profits. He talks about how temperature affects profits and concludes that gas and heating companies make higher profits when the country’s temperature is higher. Interesting fact: The research was not conducted in places with high average annual temperatures. Instead, it was conducted in Belgium, Denmark, Finland, and 18 other places. On the other hand, the collective of authors,

da Silva et al. (

2022), focused on agricultural enterprises that demonstrated greater profitability when investing in irrigation systems in semi-arid regions, which increased production and were subsequently able to increase the total profits of agricultural enterprises through technological modernization. However, irrigation systems are not the only way to increase agricultural profitability.

Lozowicka et al. (

2022) state that incorporating chemistry into agriculture can also increase profitability, with the authors claiming that innovative solutions can produce previously unattainable profits within a few years. However, profitability is not solely dependent on the impact of introducing innovative business processes. China experienced a change in the profitability of businesses, specifically in the area of eliminating the carbon footprint of businesses (

Wang et al. 2022;

Zhu and Sun 2022). The COVID-19 pandemic revealed the biggest problems with businesses (

Dinu and Bunea 2022) that depended on the purchasing power of the population always going up (

Che-Ngoc et al. 2022). Banks also had to address this problem, which put pressure on the people (

Caby et al. 2022) who wanted to profit despite the bad economy. European banks were discussed by

Kozak and Wierzbowska (

2022). Asian banks were analyzed by

Nguyen and Le (

2022) and

Dsouza et al. (

2022). Vietnamese banks were evaluated by

Pham et al. (

2022), and sub-Saharan African banks were assessed by

Taylor et al. (

2022). Multiple studies show that it is important to look at profitability since the COVID-19 pandemic had a big effect on the indicators of this financial and economic tool (

Pervan et al. 2017). Some businesses were able to get back on their feet quickly after the pandemic and the ensuing financial crisis (

Lim and Morris 2023). Some businesses, like those in sub-Saharan Africa, increased the number of services to protect themselves from the bad effects of the pandemic. This helped them stay profitable (

Olarewaju and Msomi 2022). However, the crisis revealed the profitability indicators, such as ROA and ROE, that are most affected by the economic downturn (

Zhao et al. 2022). Numerous mathematical and statistical techniques were used to draw this conclusion. Not only the aforementioned authors performed profitability indicator analyses, but in their analysis of Indian banks,

Dsouza et al. (

2022) employed additional methods, including panel regression, one-dimensional analysis, and descriptive statistics. In the US, however,

Chue and Xu (

2022) used the model of Hou, Xue, and Zhang, which solved aggregate profitability and investment in assets and showed high predictive power.

Jihadi et al. (

2021) looked at the relationship between the financial performance of the given indicators and social performance by using indicators of liquidity, activity, leverage, and profitability.

3. Materials and Methods

This scientific contribution looks at whether the growth of profitability indicators (ROA, ROE, and ROS) for businesses of different sizes changed significantly in 2019, 2020, and 2021, which are the years before, during, and after the pandemic.

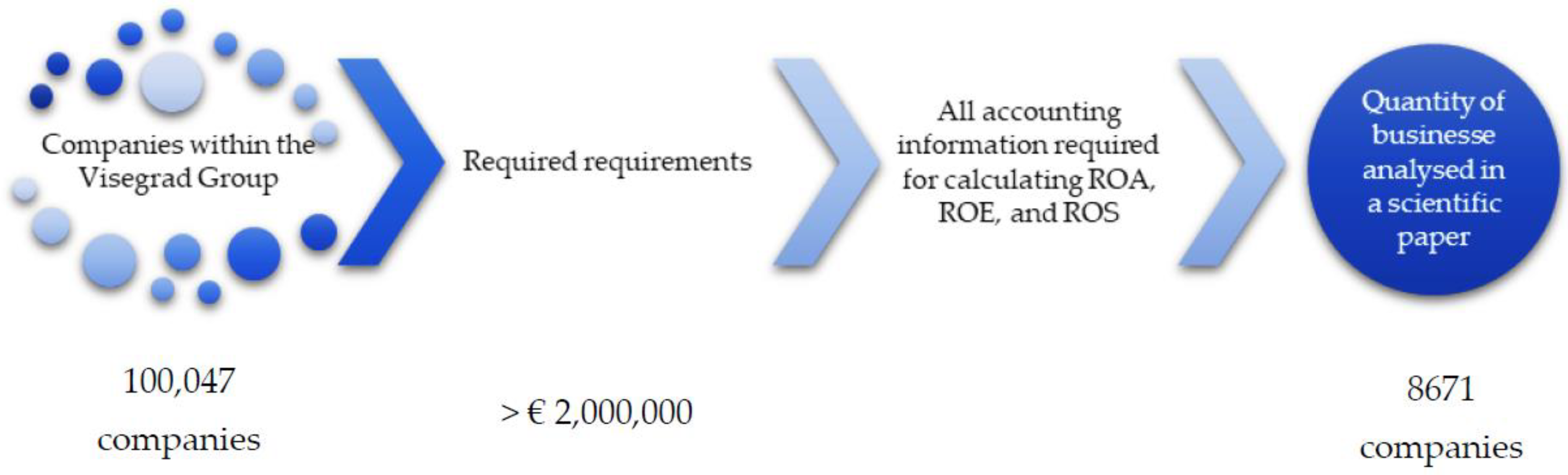

The article is mostly about how businesses work in the countries of the Visegrad Group. There are 100,477 businesses included in this group. The total number of businesses decreased to 8671 based on the criteria that a company must meet, i.e., a minimum amount of assets > €2,000,000 and all of the accounting data required to calculate ROA, ROE, and ROS, as shown in

Figure 2.

Table 1 illustrates the categorization according to the ORBIS database. The enterprises must meet the criteria listed in the table in order to be classified as a medium, large, or very large enterprise. Otherwise, the enterprise was classified as a small enterprise.

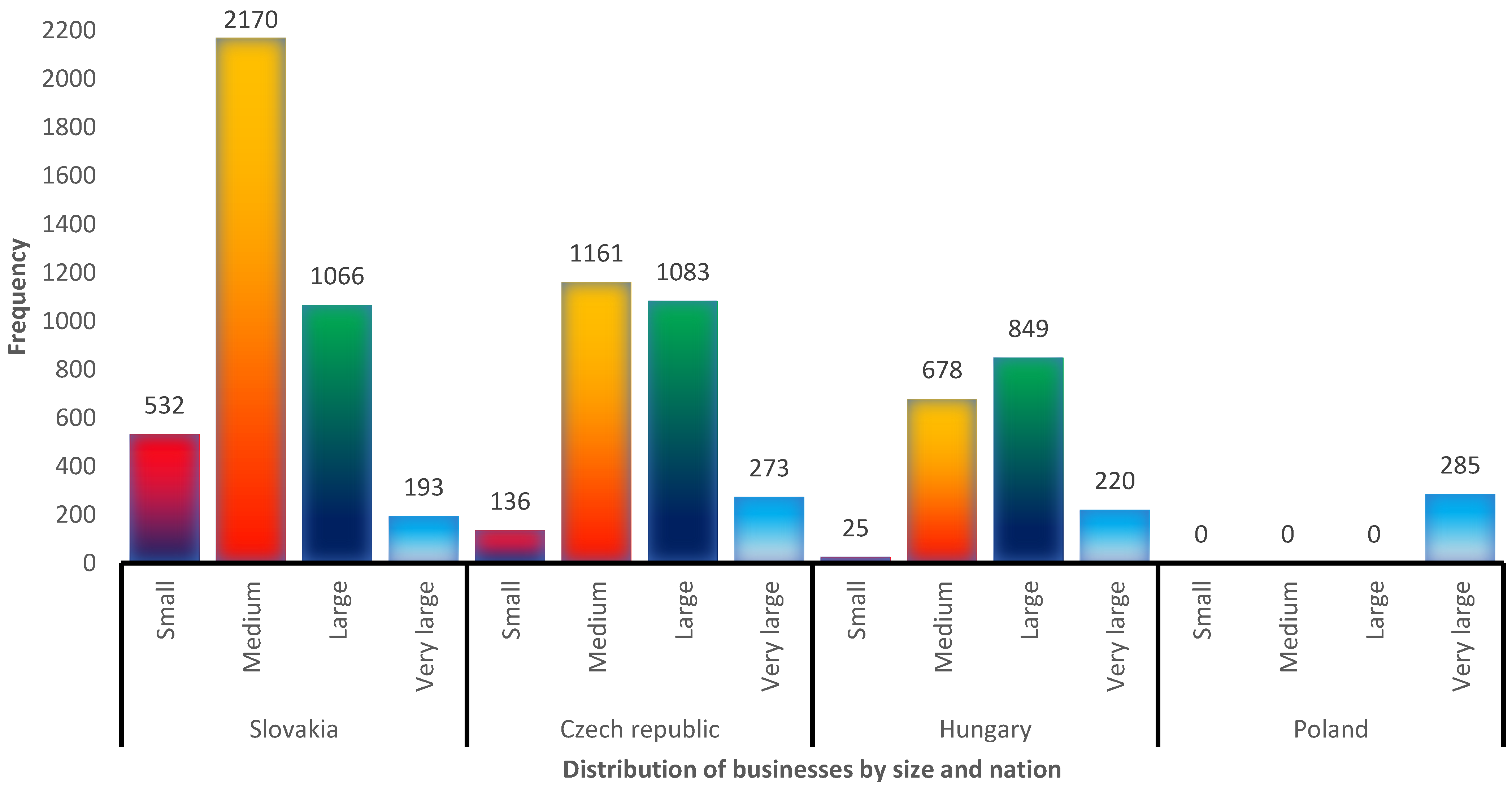

The representation of businesses in various nations is not uniform.

Figure 3 depicts the number of businesses in each state as well as their classification by size category. As can be seen, the largest representation of companies comes from the Slovak Republic, which has 3961 companies, the majority of which are medium-sized businesses. In second place is the Czech Republic, with 2653 businesses, the majority of which are medium-sized enterprises, just as in the Slovak Republic. Another country represented is Hungary, with 1772 businesses. Compared with all other size categories, Hungary has the highest proportion of large companies. Poland, which has 285 companies represented in this scientific article, is the concluding member of the V4 group. All these companies qualify as extremely large businesses.

With the help of MS Excel and IBM Statistics 25, the information in tables and conclusions was presented in a clear way. MS Excel was also used to choose secondary data from the ORBIS database, which is owned by Bureau van Dijk, a 1991-founded subsidiary of Moody’s Investors Service, Yellow Maple Holding B.V., and has business information on all European countries.

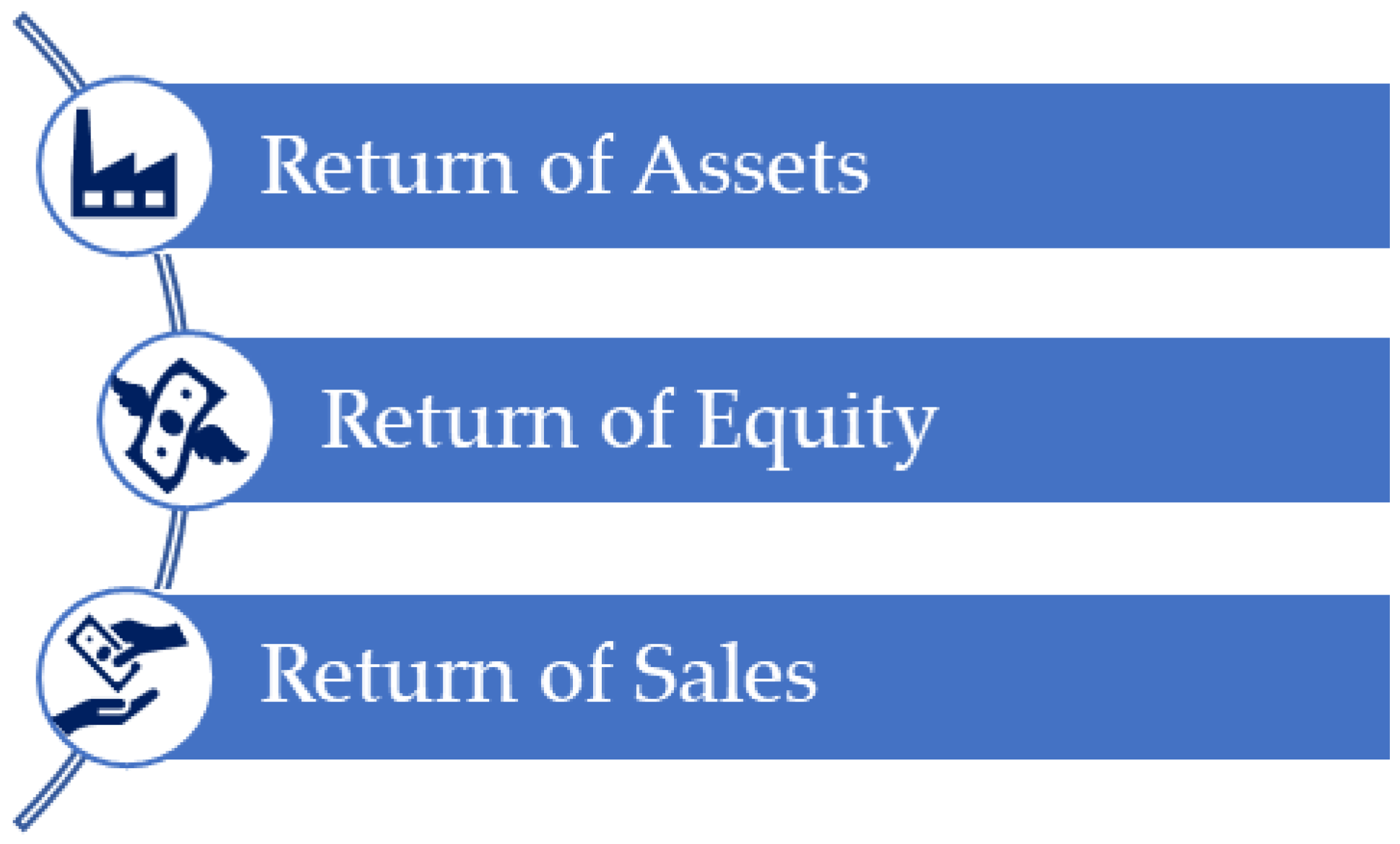

Figure 4 indicates the profitability indicators that were calculated.

In mathematical terms, ROA (Equation (1)), ROE (Equation (2)), and ROS (Equation (3)) are calculated as follows:

Earnings after tax, or EAT, is used in the calculations, as well as maximum, minimum, and the values of the median, mean, and standard deviation for 2019, 2020, and 2021 for the ROA, ROE, and ROS indicators for the different size categories of enterprises. The values of the entire Visegrad Group are in addition to these values (

Table 2). The values of small businesses are presented in

Table 2, the values of medium-sized businesses in

Table 3, the values of large businesses in

Table 4, and the values of extremely large businesses in

Table 5.

The normality test was run to determine whether the enterprises are classified by average (if the population follows a normal distribution) or median values (if the population does not follow a normal distribution). The Kolmogorov–Smirnov test is recommended if each sample contains at least 50 observations. The following hypotheses were tested using 0.05 as the significance level.

H0. The population from which a sample of ROA, ROE, and ROS is taken in the observed years 2019, 2020, and 2021 follows a normal distribution.

H1. The population from which a sample of ROA, ROE, and ROS is taken in the observed years 2019, 2020, and 2021 does not follow a normal distribution.

The test was run for each subsample. If the computed

-value (significance) was lower than the significance level alpha, the null hypothesis should be rejected, and the alternative hypothesis should be accepted based on

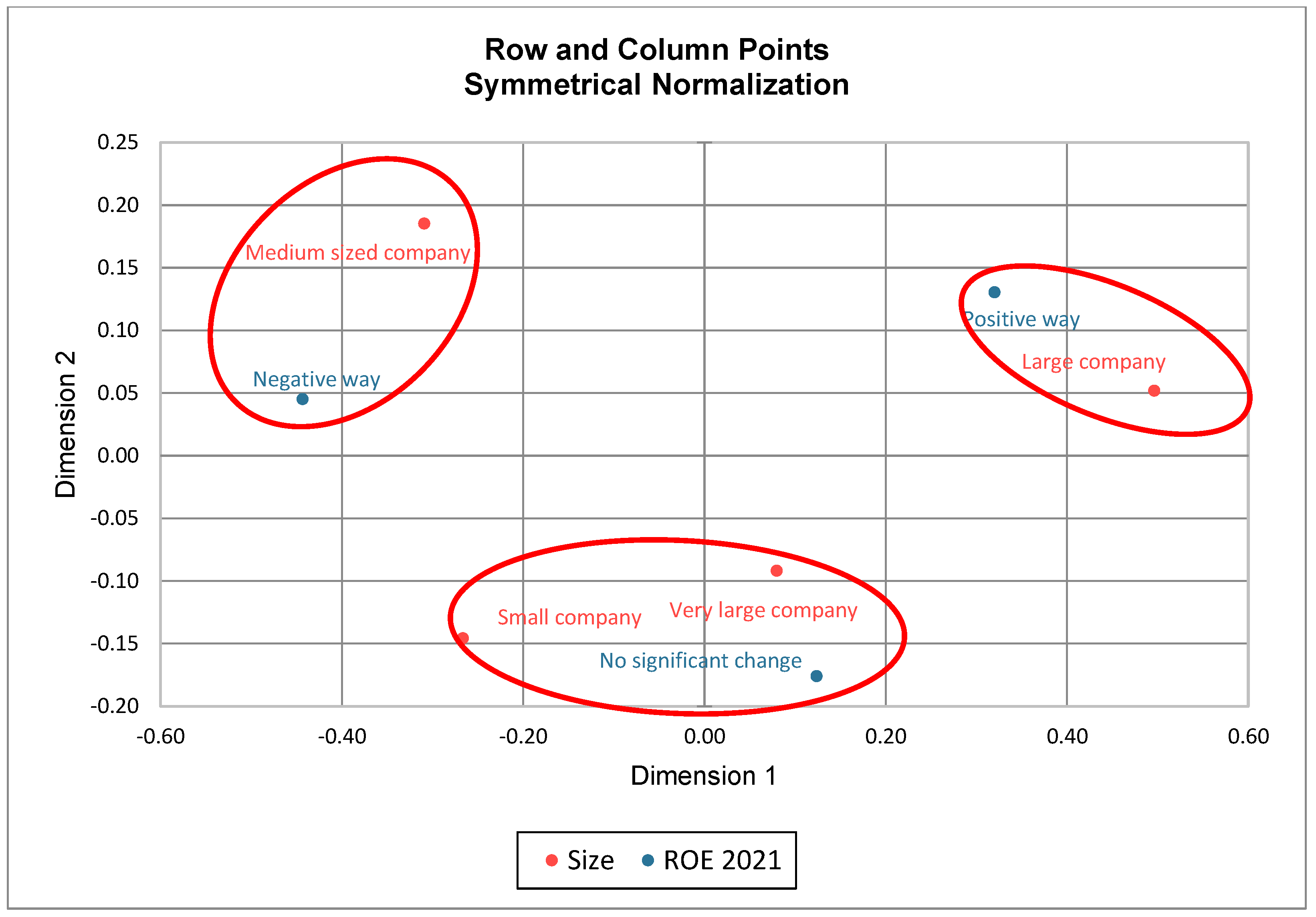

Table 6. The populations from which a sample of ROA, ROE, and ROS was taken in the observed years of 2019, 2020, and 2021 do not follow a normal distribution in all cases. Thus, the given size categories were able to reach the profitability indicator values with a positive change, a negative change, or no significant change based on the median values.

The one-sample Wilcoxon signed-rank test was run for each enterprise, each indicator, and each year according to the size of the business to see if the median values

of ROA, ROE, and ROS were different from zero. The tested median value was chosen based on specific values from

Table 2,

Table 3,

Table 4 and

Table 5. If the median value of ROA, ROE, and ROS was not different from zero, there was no significant change. On the contrary, if the median value was different from zero, its positive value showed a positive change in profitability, and the negative value showed a positive one in ROA, ROE, and ROS (

Figure 5). This approach was derived based on

Valaskova and Gajdosikova (

2022). They used the parametric

-test, but we preferred the nonparametric version of t

-test because there was no following normal distribution of analyzed populations of ROA, ROE, and ROS.

Thus, the following hypotheses were tested using 0.05 as the significance level.

H0. In the observed years 2019, 2020, and 2021, the median values of the indicators ROA, ROE, and ROS was not different from zero.

H1. In the monitored years of 2019, 2020, and 2021, the values of the indicators ROA, ROE, and ROS was different from zero.

The enterprises were divided into three groups based on a comparison of the specific p-value and significance level alpha:

Businesses that changed significantly for the worse;

Businesses that did not significantly change;

Businesses that changed significantly for the better.

The fundamental idea underlying the Pearson chi-square test is to compare the observed data values with the expected values if the prerequisites are met. The assumption of 80% of expected observations must be equal to/higher than value 5, and the second assumption of all cells of expected counts must be higher than value 1 (

Valaskova et al. 2018).

The following hypotheses were tested using 0.05 as the significance level.

H0. In the observed years 2019, 2020, and 2021, the values of the indicators ROA, ROE, and ROS did not change.

H1. In the monitored years of 2019, 2020, and 2021, the values of the indicators ROA, ROE, and ROS changed.

After testing hypotheses for 2019, 2020, and 2021, the strength between two nominal variables was measured. Cramer’s V and contingency coefficient C were used if the dependence was confirmed.

where

is test statistic from Pearson

test,

is the number of total observations,

is the number of rows,

is the number of columns.

Olah et al. (

2021), and

Musova et al. (

2021) determine indicative limits for the strength of the dependence determined by Cramer’s V and contingency coefficient according to these limits:

0.0 < the rate of the coefficients ≤ 0.3 weak dependence;

0.3 < the rate of the coefficients ≤ 0.8 medium dependence;

0.8 < the rate of the coefficients ≤ 1.0 strong dependence.

It is also necessary to test the significance of the identified coefficients of contingency (

Olah et al. 2021). The hypotheses for this test are as follows:

H0. Cramer’s V (Contingency coefficient) is not statistically significant.

H1. Cramer’s V (Contingency coefficient) is statistically significant.

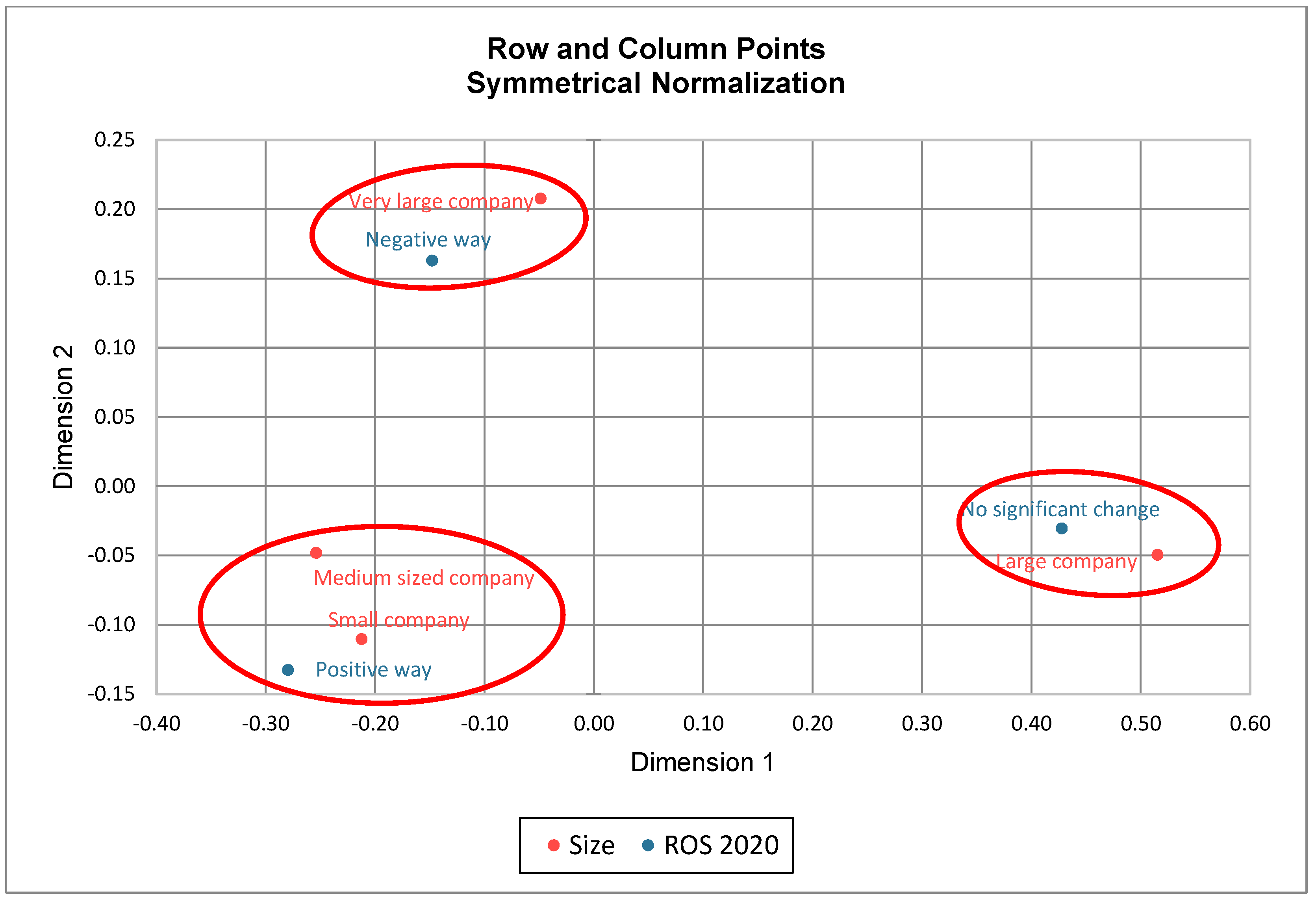

Based on the outcomes of the chi-square test (

Shen et al. 2022), the size criteria of enterprises and changes in profitability indicators were further analyzed by means of correspondence analysis. The correspondence analysis is a common data visualization technique; see

Liu et al. (

2022),

Ragazou et al. (

2022), and

Gajdosikova et al. (

2022). We distinguish between simple and multiple correspondence analyses. In both instances, the results are displayed using points on a map. The relative frequencies in the contingency table are denoted by dots (

Verma 2012). The position of the points indicates the similarity between the row and column categories, as well as their interdependence. Using this method, we have attempted to display the points by reducing the space dimensions so that hidden relationships and associations between the analyzed variables stand out; see

Kral et al. (

2009). The following is the procedure for calculating the correspondence method and marking with symbols:

The matrix of row profiles is denoted by the symbol R (Equation (4)), while the matrix of column profiles is denoted by the symbol C (Equation (5)).

r-term vector of row loads as r and s-term vector of column loads as c.

Their relationship is then expressed as follows:

where

is a diagonal matrix containing vector r elements and

is a diagonal matrix containing vector

c elements. Then, the correspondence matrix can be expressed as follows (Equation (6)):

While the following relations hold true for the vector of row loads

r (Equation (7)) and the vector of column loads

c (Equation (8)):

Before beginning the actual procedure of the correspondence analysis, it is necessary to assess the suitability of the input variables. Thus, for the variables under consideration, we will evaluate their mutual relationship or association. The chi-square test for testing independence is utilized (

Durana et al. 2019). If a statistically significant association is confirmed, the data are appropriate for the method’s application.

The degree of dissimilarity between the variable categories in the rows and columns is then assessed. The definition of the chi-squared distance calculation is as follows (Equation (9)):

where

rij and

ri’j are elements of the matrix of row profiles

R, and

cj is the vector of column loads. Simultaneously, the vector of column loads equals the average column profile, also known as the centroid (center of gravity) of column profiles (

Khomytska et al. 2020). Similarly, the degree of dissimilarity, or the distance between column categories

j and

j′, can be calculated.

which represents the elements of the row load vector

r, is used as a weight.

According to

Gimferrer et al. (

2020), the Euclidean distance between plane points is comparable to X

2, the distance between points in three-dimensional space. It is required to find a projection that preserves, as much as possible, the relationship between the original points of the multidimensional space. We use the matrix of standardized residuals

Z to look for the projection. Each element in the

i-th row and

j-th column is defined by the members of the correspondence matrix and their respective marginal sums (Equation (10)):

To compute the eigenvalues, we use singular value decomposition. We begin by calculating the Z matrix of standard residuals. When showing the graph, we do not search for coordinates in the original row and column profiles. Based on the standard residuals, which show the divergence of the row and column categories from independence, we take the following action. This matrix’s entries gain values in accordance with the relationship Equation (10). The correspondence matrix is denoted by the letter p.

The marginal row frequencies

(Equation (11)) are referred to as row loadings. Column marginal frequencies

(Equation (12)) are called column loads. The relationships are applicable to both row and column loads:

Linear marginal absolute frequencies

(Equation (13)) of character occurrence

X and column marginal absolute abundances of character Y

(Equation (14)), which are in Equations (11) and (12), are computed based on the following relationships:

6. Conclusions

In this paper, the authors address the global COVID-19 pandemic and how it affected the size of companies based on how the values of certain profitability indicators, such as ROA, ROE, and ROS, changed.

Figure 15 below provides an overview of this chapter.

Using the MS Excel calculation software, secondary data from the ORBIS business-economic information database, which is managed by Bureau van Dijk and has more than 400 million financial statements from businesses in the European ecosystem, were used to figure out profitability indicators. From the obtained values, median values were calculated for individual indicators as well as for the entire V4 group, which served as the study’s central pillar. After dividing the values into significant positive and negative changes, putting the companies into size categories, and making hypotheses, the given hypotheses were tested, and the relationships between the given variables were found. After obtaining partial results, which determined the future direction of the research, a correspondence analysis was conducted, followed by a comparison of the results of this correspondence analysis, i.e., the drawing of groups on correspondence maps. Thus, the overall work showed the classification of size categories of enterprises in the evaluation of the number of selected profitability indicators for the monitored period of 2019 to 2021, where 2019 was the base year that showed the basic distribution of enterprises, 2020 was expected to be the year with the biggest change from the initial distribution, and 2021 was expected to be reclassified according to the basic grouping from 2019. The research results, however, revealed a different classification. Fiscal authorities may monitor the level and risk across a region of countries and keep an eye on the practical ramifications of these results. Before doing a thorough examination of the particular company and the due diligence phase, auditors may use the approach as the initial step of their research for the specific size of the company.

Out of the original 100,041 companies, only 8671 met the required criteria (assets greater than €2 million and complete accounting data). Searching through public databases of business financial statements could produce accounting data. This would lead to more businesses. Another constraint was the uneven distribution of businesses across nations. One of the problems is that only one method of analysis and a small number of time periods were looked at. These problems could be fixed by using more than one method of comparison and looking at a longer time period, or by looking at the time before the economic crisis in 2009 up until 2022 and seeing how different factors might have affected businesses in the V4 group.

In future research, we would focus on other measures of profitability, like ROC, ROI, ROR, and wage profitability, which we would look at using new methods and a longer time frame, as was explained in the last paragraph.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}