1. Introduction

Short-term lending markets have been the focus of concerns about financial stability for much of the last two decades. In particular, turbulence among prime money market mutual funds has repeatedly prompted emergency responses from the government and the Fed, as well as proposals to reform these markets. In both 2008, during the global financial crisis, and in 2020, at the outset of the COVID pandemic, lending facilities were created to ease concerns about money funds’ ability to redeem shares.

As a response to the events of the financial crisis, in 2014 the Securities and Exchange Commission (SEC) implemented a series of reforms intended to address vulnerabilities in prime funds. Those reforms were not fully effective at containing the challenges faced during the pandemic. As a result, many market observers and policymakers renewed their calls for further reforms. In fact, Eric Rosengren, then president of the Federal Reserve Bank of Boston, went as far as to say: “the money-market fund reform that occurred after the last crisis actually made things worse and so far there has not been a solution”. He went on to argue that prime money market funds needed to be “cleaned up” (

Marte 2021).

1On December 2021, the SEC again introduced a new set of proposed reforms to the rules governing money market funds. The proposal abandons the liquidity fees and redemption gates that were introduced in 2014. In their place, the proposal intends to implement an alternative valuation method for institutional prime and tax-exempt money market funds: swing pricing. The basic idea is to require funds to adjust floating net asset values (NAVs) by a swing factor reflecting transaction costs that would result from selling proportional amounts (a “vertical slice”) of the various assets in the fund. Finally, the proposal increases the minimum liquidity requirements serving as buffers for money market funds in times of large, unexpected redemptions.

In this article, we argue that this series of reforms does not directly address the fundamental problem created by prime institutional money funds. We describe this problem as arising from the propensity of the government and/or the central bank to provide emergency credit and liquidity to these funds in times of stress. The expectation of such support weakens funds’ incentives to prepare for such contingencies themselves.

Accordingly, we propose an approach to regulation that directly addresses the way funds provide for contingent liquidity in times of stress. Money funds should be required to enter contractual commitments for the provision of lines of credit that can be used in periods of high investor outflows. These credit lines are a close substitute for the support that otherwise the government feels compelled to provide at those times. The contractual approach allows for explicit recognition of the costs of backup support, which creates the right ex-ante incentives for investors when allocating funding across various alternatives.

An important aspect of the proposed approach is who in the private sector should provide contingent support to prime money market funds. We think that in the current U.S. regulatory environment, large stress-tested banks are the most appropriate entities to provide such support. Significant progress has been made in regulating large, systemically important banks in the U.S., including robust capital and liquidity requirements and regular sophisticated stress testing procedures. We propose to leverage that progress, which has resulted in a more accurate recognition of the risks and costs associated with liquidity provision in times of financial instability (

Acharya et al. 2016). Given that those banks recognize the relevant costs more accurately, they will price them in on their dealings with prime funds. Managers and investors of prime funds, then, will need to decide whether their investments are viable taking into account,

explicitly, the need for contingent liquidity support, which before was indirectly and implicitly provided by taxpayers.

We do not intend to argue here that the alternative proposed eliminates all trade-offs and costs present in the business model of prime funds. We aim, instead, at creating a more appropriate allocation of costs which moves the economy closer to an ideal, efficient state. Some of the costs, however, seem inescapable if prime funds are to stay a meaningful segment of the money market. We think, though, that by further removing the taxpayer as the ultimate provider of liquidity, the resulting allocation of risk and costs will be closer to optimal.

The paper is organized as follows. In the next section, we briefly describe the main features of money market funds, how they originated, and their link to the commercial paper market. In

Section 3, we discuss the reforms that were implemented after the 2008 financial crisis and the recent SEC proposals to amend those reforms. In

Section 4, we describe what we view as a fundamental problem behind the instability of prime institutional funds and propose an approach to address that problem. We also discuss its merits relative to other components of the reform under consideration.

Section 5 provides a brief conclusion.

2. Prime Money Market Funds in the U.S.

Money market mutual funds provide investors with a highly liquid form of savings that acts similarly to a bank account. Shareholders have ready access to their funds if needed for expenditures or other investments. The funds, in turn, hold exclusively short-term assets. Some funds (government MMFs) hold only assets issued by the US Treasury or government-sponsored entities. Others—the so-called prime funds—also hold short-term debt (commercial paper) of large corporations. A further distinction involves the investors in funds. “Retail” funds draw investments mainly from households and small businesses, while “institutional” funds are an important money management tool for financial institutions and other large corporations. Most of the regulatory attention in the U.S.—both in the 2014 reforms and in the current proposals—has been on prime institutional funds.

An important aspect of the development of money market funds is an accounting practice that under SEC rules is not available to other investment funds. Money market funds have historically been allowed to maintain a stable share price (typically one dollar), which enhances their usefulness to shareholders as a tool for money management. The most common method for maintaining a stable share price is the “amortized cost” method of valuation, under which individual securities are valued at acquisition cost.

2 Interest earned is accrued uniformly over the remaining maturity of the security and is paid to shareholders in the form of additional shares. In exchange for being able to offer a stable net asset value, money market funds must satisfy restrictions on their portfolio—essentially requiring them to hold only relatively safe, short-term securities. Funds can further protect against losses by securing backstop support from a bank or another party, although this practice varies among funds.

3Money market funds became a significant part of the US financial system in the 1970s. After the first public issuance of shares in 1972, these funds saw their greatest early growth in periods when short-term market interest rates rose above the regulatory limits that capped the rates paid on bank deposits at the time (Reg. Q). Toward the end of the decade and into the 1980s, growth in money funds accelerated—again, during a period of high and volatile interest rates. From the start, then, it was apparent that the main purpose of these funds was as a substitute for bank deposits that could provide similar services to investors with fewer regulatory constraints (

Cook and Duffield 1979). Money market funds continued to grow even after the repeal of Reg. Q interest rate caps because of cost differences that were—and to a large extent continue to be—attributable to differences in their regulatory treatment as compared to bank deposits.

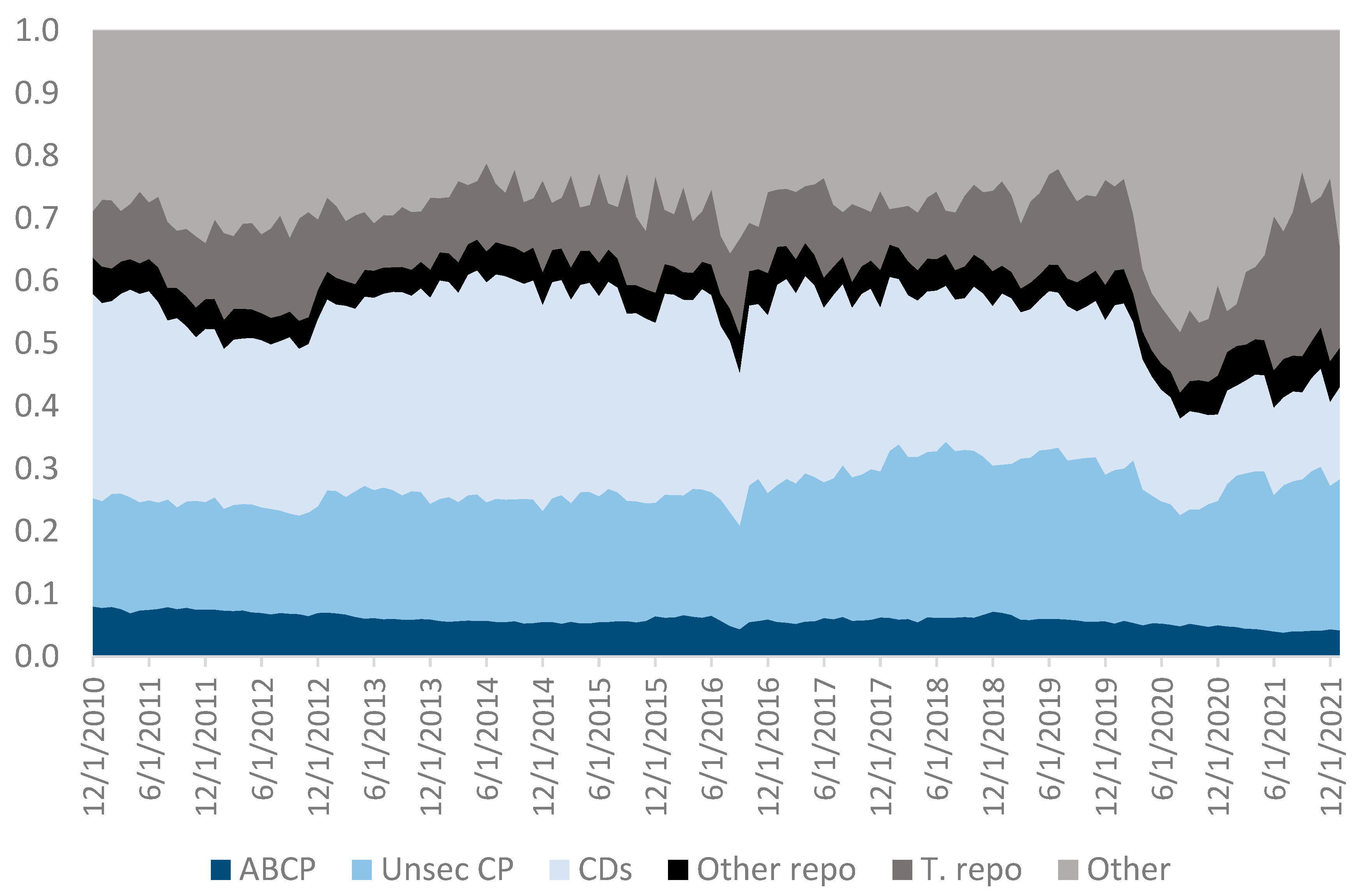

The evolution of prime money market funds in the U.S., especially beginning in the late 1970s, is closely linked to developments in the commercial paper (CP) market (See

Cook and Laroche 1994, chp. 9). Commercial paper is short-term debt issued by large firms—often, but not exclusively, bank holding companies and nonbank financial firms. As money funds attracted increasingly large sums of investors’ dollars away from bank accounts, they created a ready market for CP, and highly-rated issuers typically found borrowings in that market less costly than bank loans. Additionally, since CP is typically issued in large, indivisible offerings, money funds proved to be a convenient way for investors to make smaller, diversified investments in those instruments. At the beginning of 2020, commercial paper accounted for more than a quarter of the asset holdings of prime institutional funds (see

Figure 1).

So, on both “end-user” sides of financial markets—ultimate savers and borrowers—CP and MMFs saw big increases in activity at a time when a combination of regulatory constraints and volatile market conditions hampered banks’ ability to provide a close substitute. During the 1980s and 1990s, the arbitrage of regulatory differences continued to drive the growth and evolution of these investment vehicles. The financing of financial and commercial firms through the issuance of commercial paper bought by money market funds exemplifies what has come to be known as “shadow banking” and can be thought of as a means of bypassing the banking system and its prudential regulation.

2.1. Fund Instability

Similar to many short-term financial arrangements, money funds can experience large demands for withdrawals if investors suddenly lose their appetite for this form of savings. In the case of prime funds, outflows may arise due to a broader loss of confidence in their holdings of commercial paper. The potential for sudden outflows is exacerbated if a money fund maintains a stable share value to make itself attractive to investors who are averse to taking losses on the balances they use, among other things, for cash management purposes (

Ennis 2012). This motivated the SEC’s 2014 rule requiring prime institutional money funds to adopt floating NAVs.

When investors request redemption of their money fund shares, funds may first meet those requests by selling the assets that can be sold most easily. In an environment of falling confidence, risk premia rise, even on short-term debt such as CP, in which case the easy-to-sell assets are unlikely to be CP. Yet if redemptions continue, funds may ultimately have to liquidate their CP holdings, as well. If they do so at a loss, they may be unable to live up to their commitment to redeem shares at a stable value. That is, late-coming redeemers may suffer a loss on their shares. Knowing this, when there is a loss of confidence in the underlying assets, fund investors may rush to withdraw as quickly as possible, further increasing the stress on the fund (and the CP market).

At times of economic and financial stress, it is also the case that funding can shift quickly away from prime funds and into other money-market instruments, including government funds. Government funds, for example, cannot invest in commercial paper and, hence, such shifts can exacerbate any sudden withdrawal of available funding for the CP market.

In principle, other intermediaries that invest in CP directly, such as large banks, could respond by selling government securities to government funds and using the proceeds to make loans to CP issuers or to buy their commercial paper, effectively re-channeling the funding in the system back to where it is needed. When this does not happen and funding problems persist, those initial withdrawals from prime institutional funds can be interpreted as a reflection of a more general desire of sophisticated investors to reduce their exposure to commercial paper in response to deterioration in the creditworthiness of issuers (not just a flight from prime funds).

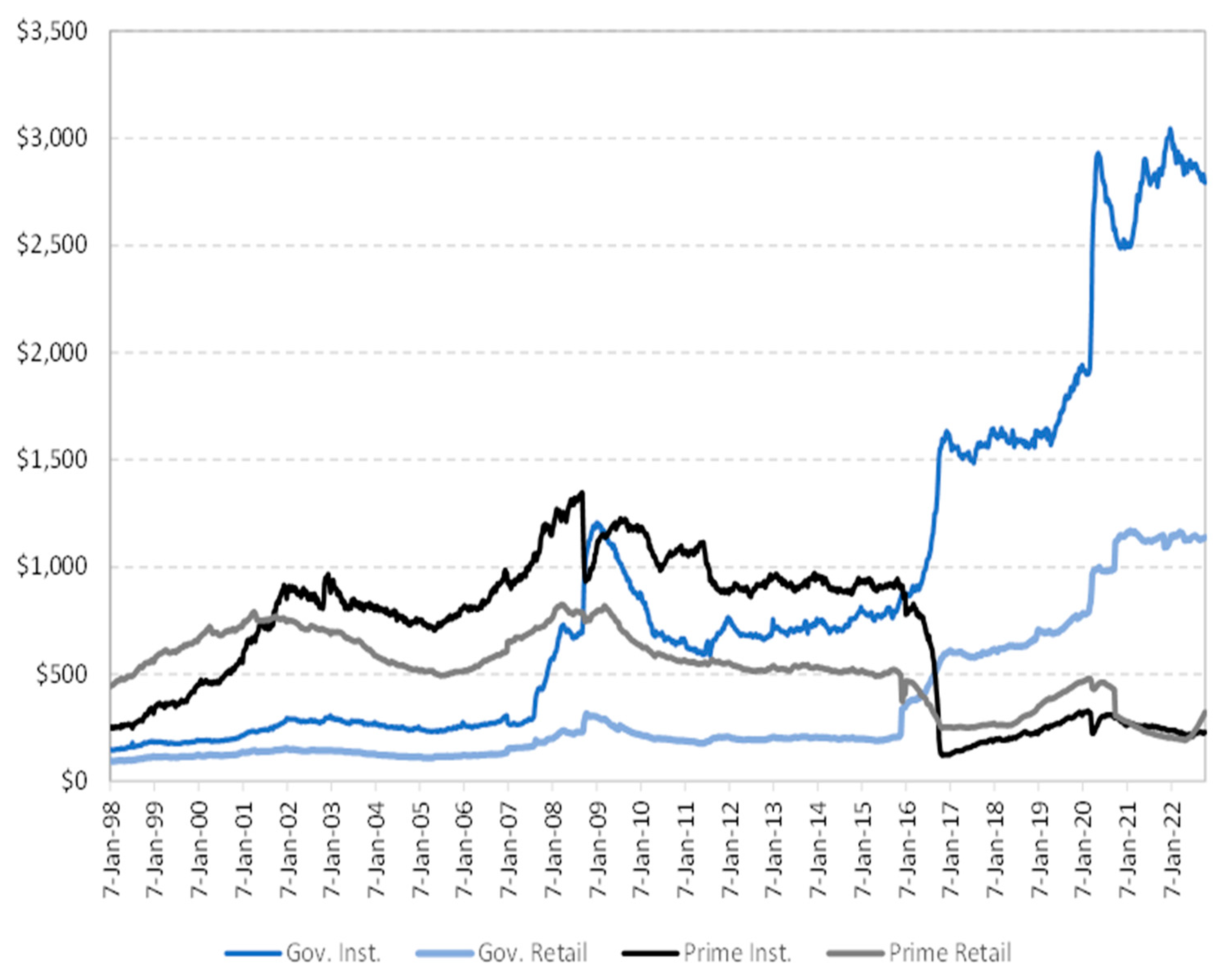

Indeed, investors’ desire to move out of prime money funds often reflects a broader move in the market to reduce exposure to the credit risk inherent in commercial paper. The contrasting behavior of balances in prime funds and government funds during periods of stress, as reflected in

Figure 2, supports this interpretation. While prime funds lose investors, government funds gain them.

The bankruptcy of Lehman Brothers in September 2008 provides an example of how a sharp movement of investors away from commercial paper can affect the prime money funds industry. Investors in prime funds, who in normal times may not pay much attention to the particular assets held by the funds they hold, became understandably concerned about exposure to commercial paper and other obligations of Lehman. One particular fund, Reserve Primary, had a large enough exposure to Lehman paper that marking those assets down made them unable to maintain a stable one-dollar share value. Instead, it placed its share value at 97 cents, thereby, “breaking the buck”. Reserve Primary was particularly vulnerable, because, unlike many other funds, it did not have a large sponsor that could provide financial support in the event of such stresses.

4 2.2. Emergency Liquidity Support

In principle, a fund can protect itself from liquidity-driven disruption by arranging a backup line of credit or other contingent support (see, for example,

Brady et al. 2012;

Parlatore 2016).

5 Similarly, an issuer of CP can take similar actions to enhance the credit quality of their paper. Securing such protection, however, is costly and eats into the cost advantage that this shadow banking segment typically enjoys over traditional banking.

Implicit sponsor support for money funds has been common over the years. For example, a

Moody’s Investor Service (

2010) report identified 145 instances prior to August 2007 where a U.S. MMF would have broken the buck absence sponsor support; of these, only just one fund was liquated at less than 100 cents on the dollar. From August 2007 through December 2009, the report estimates that all but two of the 62 MMFs that were at risk of breaking the buck received sponsor support—the two exceptions being funds issued by Reserve Fund (

Moody’s Investor Service 2010).

2.3. Lines of Credit from Banks

In principle, banks could also increase their provision of lines of credit to money market funds.

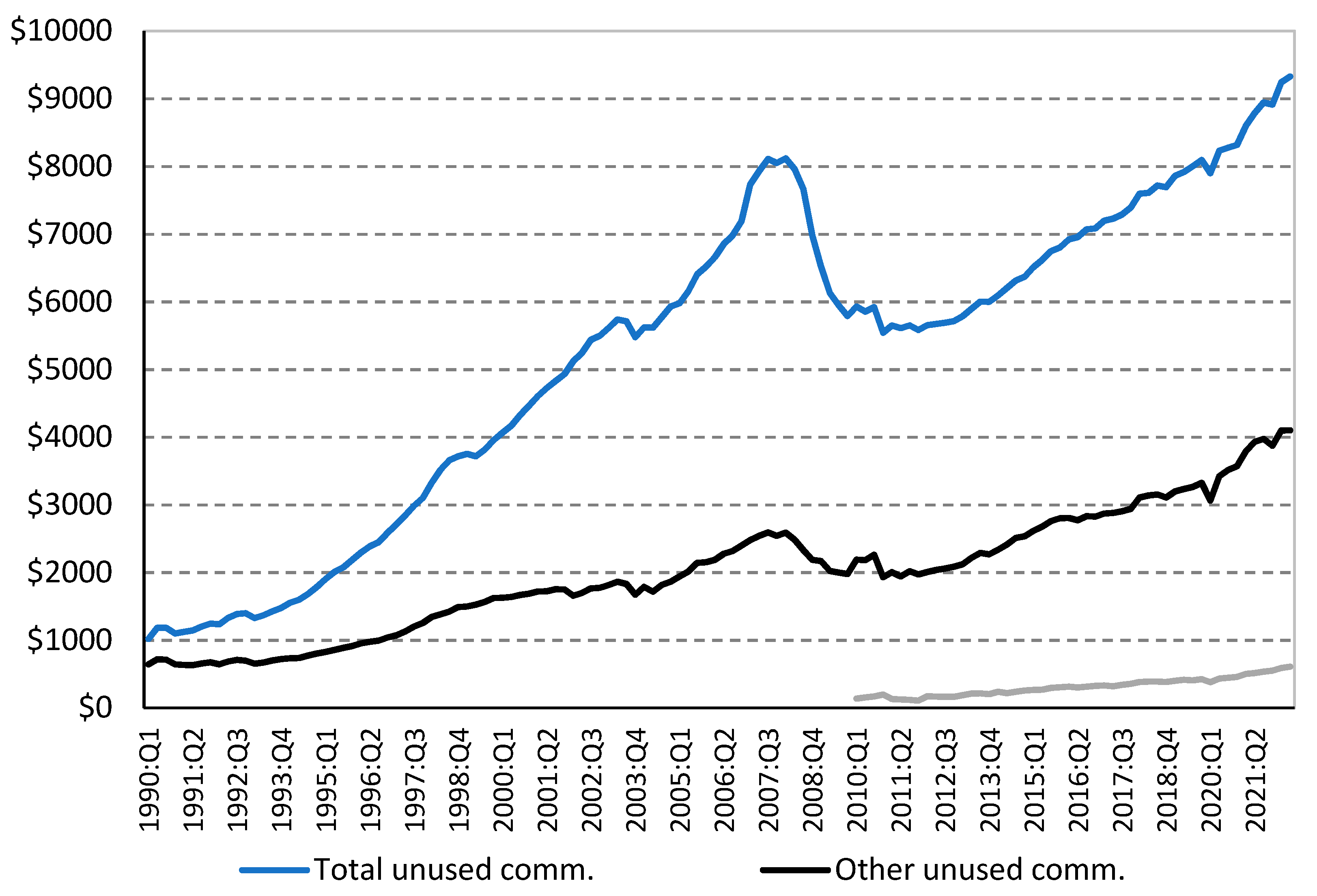

Figure 3 shows the total dollar amount of unused lines of credit provided by U.S. domestic banks. These are off-balance sheet commitments. However, to gain some perspective on their size, in the last ten years, they are roughly about 40 percent of the value of total assets in these institutions. A large portion of these commitments, though, is accounted for by credit card lines of credit or are associated with residential real estate. Other unused commitments include those related to C&I lending and a very small portion of those other unused commitments are, in fact, lines of credit to financial institutions.

Another pattern worth noticing from

Figure 3 is the significant drawdowns of unused commitments triggered by the 2008 financial turmoil. Clearly, lines of credit from banks played a role during that time, and to a lesser extent, while still noticeable, during the early months of the pandemic in 2020 (

Li et al. 2020). Interestingly, even in those extreme events, a significant proportion of the existing lines of credit from banks remain unused (as is clear from the figure).

2.4. Implicit Public Support

With limited liquidity commitments from the private sector, turmoil among money funds commonly induces a public sector reaction and often leads to support for money funds and the CP market from the Fed, the Treasury, or both. When the Reserve Primary fund broke the buck in September 2008 and fears arose of a broad retreat from money funds, the Treasury stepped in to provide a temporary guarantee for

all funds’ net assets values, and the Federal Reserve implemented lending programs to aid the CP market. When the onset of the pandemic in 2020 brought on a sharp increase in economic and financial uncertainty, the Fed again put in place credit facilities to support money market funds and commercial paper.

6 The prompt intervention in this instance may help explain the relatively modest decline in prime institutional funds, as seen in

Figure 2, while significant funding flowed into government funds as part of a broad flight to safety and liquidity.

This type of government reaction has a long history. The Federal Reserve was founded, in part, with the aim of providing backstop support to the CP market (

See Wicker 2015, p. 63;

Lacker 2013). More recently, after the Fed and the administration resisted entreaties to rescue the failing Penn Central railroad in 1970, their subsequent bankruptcy and commercial paper default roiled the CP market, making it difficult for other issuers to roll over maturing issues on accustomed terms. The Fed responded by encouraging banks to lend to enable their customers to pay off maturing commercial paper and signaling willingness to allow banks to borrow at the discount window to do so.

7 3. Money Market Fund Reform in the U.S.

Rule 2a-7 of the SEC is the basic regulatory framework for MMFs in the U.S. Different types of MMFs are subject to different requirements. In particular, the rule distinguishes between government, tax-exempt, and prime MMFs; and between institutional and retail funds.

Before the 2014 reform, all MMFs were allowed to use the stable NAV approach for portfolio valuation, a method that disregards small variations in the value of assets. MMFs were thereby able to offer a stable share price that made them attractive for short-run money management purposes. Stable NAVs are partly behind the pernicious dynamics inducing a rush from investors to withdraw from funds during stress episodes. This is particularly relevant for institutional prime funds, where investors tend to be more responsive to valuation differentials. For this reason, the 2014 reform mandated that institutional prime funds stop using stable NAV and, instead, adjust their NAV based on current market-based values of the securities in their portfolios (see

Ennis and Haltom 2014).

8While floating NAVs help avoid artificial incentives to withdraw from a fund in times of stress, timely market-based valuation of fund assets can be challenging. Many of the investments of money market funds trade in thin markets and can experience sharp fluctuations in price. In many cases, the prices are not readily available and fund managers have to impute an estimated price. These complications motivate the combination of floating NAVs with other preventive measures. In particular, the 2014 reform required funds to hold buffer stocks of liquid assets and allowed funds to impose redemption fees and gates when those liquidity buffers fell below certain thresholds.

That stable NAVs and weak liquidity provisioning was benefiting the riskier prime funds seems clear from the reaction to the 2014 reform reflected in

Figure 2. Around the time when the 2014 reform took effect in October 2016, prime institutional money market funds quickly lost ground while, simultaneously, assets under management in government funds increased substantially.

4. Government Lack-of-Commitment and a Path to Address It

At the heart of the challenge of crafting appropriate rules for prime money funds is the attractiveness, to both borrowers and lenders, of short-term debt. Investors who desire ready access to their funds will accept a lower yield in exchange for increased liquidity. The liquidity of longer-term debt instruments depends on how easy it is to sell before maturity. This can be difficult for bonds and other loans that do not trade in active secondary markets. The commercial paper provides liquidity in a more automatic fashion as well—simply let the note mature and receive the proceeds. From an investor’s point of view, liquidity is further enhanced by bundling commercial paper into mutual funds that are redeemable on demand. Borrowers, in turn, find the relatively low yields at which they can issue short-term debt attractive for obvious reasons. Short-term debt can also provide a sort of discipline for borrowers, if they need to repeatedly go to the market to roll their debt over (

Diamond 1993,

2004). So, under normal conditions, the reliance of firms on short-term borrowing through money market funds appears to be a win-win.

11But the very feature that makes investors willing to hold short-term debt at low yields—the ability to leave easily—can create strains in abnormal times. If a loss of appetite for credit risk makes it hard for borrowers to roll over their short-term borrowings, then defaults on commercial paper become a possibility.

4.1. Government Liquidity Support

The prospect of widespread defaults has often prompted government or Fed officials to intervene. Furthermore, that history is bound to affect market participants’ beliefs about the likelihood of similar interventions in the future. Such expectations can have pernicious effects. First, they can make short-term debt even less expensive for borrowers, encouraging excessive issuance (

Keister 2016). Additionally, expected implicit support dampens the extent to which the pricing of such debt differentiates between borrowers with different credit risk characteristics, offsetting (at least partially) the disciplinary benefits of short-term debt. More generally, it reduces the incentives of all participants to take costly actions to mitigate risk (

Dam and Koetter 2012;

Duchin and Sosyura 2014).

If investors believe that money funds benefit from support similar to that of large banking companies, the distortion of competition between these substitute forms of short-term investing is exacerbated—creating two alternatives with similar perceived government backing but very different regulatory frameworks. The result is likely to be the overuse of the less regulated alternative.

4.2. Lack of Commitment

Containing moral hazard effects is difficult. One approach is to simply refrain from intervening to protect investors and issuers (

Goodfriend and Lacker 1999). This requires commitment on the part of the institutions prone to intervene, such as the Treasury or the Federal Reserve, but their ability to commit in this realm appears to be limited. Ex post, when markets are in turmoil and some participants find themselves in difficult straits, intervention can be hard to resist; an example of the Samaritan’s Dilemma (

Buchanan 1975), where empathy at the moment conflicts with following through on a plan designed ex-ante to encourage self-reliance. Anticipation of a robust commitment to not intervene can provide the proper incentives for agents to modulate and reduce risk appropriately. When this is not possible, though, regulating arrangements

ex-ante to try to replicate self-reliance may be the next-best alternative.

From this perspective, liquidity regulations for MMFs serve to constrain the moral hazard effects of expectations of official intervention in the event of a surge in the demand for withdrawals. Such expectations naturally intensified after the precedents set by the Treasury and the Fed in 2008 (but have been present, arguably at least since 1970, as we explained earlier). In the absence of any attempt to disavow future interventions (perhaps due to the limited ability of any one administration to speak credibly for future administrations or recognition of the Samaritan’s Dilemma), beefing up ex-ante regulations made sense.

This limited commitment framework further suggests that efforts to limit the incidence of withdrawal-induced distress in money funds by constraining those withdrawals or penalizing them with swing pricing will not directly address the fundamental issue. Instead of suppressing the incentives to withdraw early, they accelerate the effects. Instead of preventing the Samaritan’s Dilemma, they alter its timing. Official support is likely to remain a factor.

12 4.3. A Role for Private Lines of Credit

A fundamental incentive distortion in the current environment comes, then, from the belief that backstop credit provision will be provided by the official sector. Yet line-of-credit facilities able to perform a similar function are readily available in the private sector, a point emphasized by

Goodfriend and Lacker (

1999). This suggests for regulators to focus on ensuring that MMFs have contractual commitments in place, in advance, for liquidity support from reliable private third parties, with the expectation that those are drawn on before any official support is forthcoming. The existence of such pre-arranged liquidity support is likely to enhance the ability of the official sector to resist intervening. It is important, of course, to include provisions that make those private commitments irrevocable, even if that increases their cost. More generally, the cost to a fund of obtaining contingent support should depend on the fund’s risk management practices. This, in turn, would provide appropriate independent incentives for funds to properly manage risk and possibly expand their liquidity buffers.

As we have argued here, the problem of MMF liquidity is closely related to the behavior of the CP market. Indeed, interventions to support MMF liquidity typically have been accompanied by interventions in the CP market. Some interventions aimed at supporting MMFs amount to taking the commercial paper off their hands on advantageous terms. The limited commitment perspective suggests that it might be most useful if the regulation of prime MMFs portfolios were to encourage holding commercial paper for which the issuer had contractual commitments of third-party liquidity support, such as a backup line of credit at a bank. Regulations that push MMF holdings toward such paper would incentivize issuers to obtain lines of credit and reduce the likelihood of falling CP prices inducing crises and intervention.

In short, reform should partly aim at replacing the public backup support of MMFs and commercial paper with pre-arranged backup support from other private investors, with all costs duly recognized in the ex-ante market transactions and pricing.

4.4. Private Providers of Contingent Liquidity

It is crucial for the arguments being advanced here that the private providers of liquidity are, in turn, not subject to the same problems faced by money funds. Under current conditions the U.S., large, systemically important banks are a natural candidate for this task. The regulatory framework for these banks has evolved in promising ways in the recent past—with the passing of the Dodd-Frank Act as a reaction to the 2008 global financial crisis. Capital and liquidity regulations are now quite robust. Importantly, capital regulations have been adapted to account explicitly for the on and off-balance sheet risks created by contingent obligations.

13 Furthermore, these large banks are subject to periodic stress-tests that assess their ability to go through with all their commitments to creditors, with no expectation of any meaningful government support.

These enhanced regulations, of course, create additional costs for banks. Those extra costs are the counterpart of removing the need for taxpayers’ support in certain crucial contingencies. In turn, the extra cost should be properly reflected in the price of any contractual commitments between the banks and money funds. This resulting impact on the prices of contracts is, in fact, the way that appropriate incentives regarding liquidity allocation are transmitted to fund managers, and investors more generally.

14Leveraging the regulatory framework of large stress-tested domestic banks is also particularly important to minimize potential feedback loops between money funds and the banking system during a liquidity event. Between 70 and 80 percent of the CP held by MMFs (mainly, prime) is debt issued by financial firms (including banks). Similarly, close to 70 percent of U.S. commercial paper is issued by foreign borrowers, many of them branches of foreign banks. As a result, MMFs are significant providers of dollar funding to large foreign global banks. Furthermore, regulatory frameworks across jurisdictions differ on important details and can create anomalies in the way that foreign banks interact with the rest of the U.S. financial system (see, for example,

Aldasoro et al. 2022). For these reasons, money funds should be required to secure lines of credit from banks that are not exposed to the commercial paper market. To increase robustness, the regulatory framework of large, stress-tested banks should recognize, and appropriately limit, the reliance on short-term funding from money market funds. While we realize that these are complex problems, the stress testing approach to large-bank regulation currently provides the best chance of successfully addressing them.

4.5. Parallels with Traditional Banking

The fact that as financial intermediaries MMFs serve a function that closely parallels the banking system suggests broader perspectives on the regulatory issues. First, a similar limited commitment problem has beset the banking system—the Fed, the Federal Deposit Insurance Corporation (FDIC), and other regulators have traditionally struggled with the temptation to rescue bank creditors. The deposit insurance system provides a legislative mandate for insured depositors, of course, but uninsured depositors and other creditors have often been rescued as well. This has led to the problem known as “too big to fail” (TBTF)—creditors believe support will be forthcoming, reliance on which leads to fragile funding arrangements, such as very short-term debt, that make nonintervention more damaging and thus increase the likelihood of intervention (

Stern and Feldman 2004).

Counteracting the resulting incentive distortion through constraints on risk-taking is a costly endeavor. The Dodd-Frank Act meaningfully stiffened such constraints, but also included a provision that addresses the fundamental limited commitment problem in a fashion similar to our proposal for dealing with MMFs and commercial paper. Large, systemically important financial institutions are required to submit to regulators’ resolution plans—so-called “living wills”—that detail how they will be resolved in various failure scenarios. The Fed and the FDIC can reject plans they do not view as credible and can “impose more stringent capital, leverage, or liquidity requirements, or restrictions on the growth, activities, or operations of the company”.

15 Plans include specification of sources of liquidity in the event of financial distress. Mandating ex-ante third-party liquidity support for MMFs would parallel the fruitful approach of living wills.

4.6. Capital Regulations and Other Considerations

An alternative approach to enhancing the stability of prime institutional funds, which has been proposed by some experts (

Squam Lake Group 2010), is to create a capital requirement for them similar to bank capital regulation.

16 This seems a natural route to consider, given the similarities between the financial intermediation done by the two types of entities. Yet creating a capital regime for money funds would be a nontrivial exercise. Similarly to all mutual funds, money funds have a simple capital structure—they issue ownership shares. The intent of a capital requirement is to have claims that are junior to the claims at risk of a run—shares, in the case of MMFs—in order to absorb losses before senior claimants. This would be especially complicated in the case of MMFs. Creating a junior class of loss-absorbing claimants would fundamentally alter the nature of shareholders’ claims; they would no longer be pro rata portfolio interests but would become debt-like instruments that are invariant across a range of asset values. Such a financial structure would reinforce the expectation of shareholders that they will be protected from losses and arguably only strengthen the pressure for ex-post support when shareholders losses loom.

It is worth emphasizing that concerns about instability in money funds—both in 2008 and 2020—have been almost exclusively focused on prime institutional funds. That is, the propensity of the largest and most sophisticated money managers to quickly move out of these funds and the commercial paper they hold has created the anxiety that has led to government support for these funds in the past. In the episodes that have prompted discussions of money fund reform, retail funds and government-only funds have generally remained quite stable (see

Figure 2). So, while reform discussions have rightly focused on the prime institutional side of the market, one might be tempted to ask a broader question. If these funds repeatedly threaten instability that induces government intervention, have we misjudged the net social value of prime money funds? Perhaps money funds should be restricted to holding only government securities, as proposed by

Anadu and Sanders (

2021).

4.7. Regulatory Bypass and Stablecoins

The many parallels between MMFs and the banking system suggest a cautionary note. The evolution of banking regulation—particularly its increasing scope and rigor—has arguably contributed to the growth of intermediation arrangements such as MMFs that bypass the banking system. As banking regulations have become more elaborate and costly to implement, intermediation through the banking system has become more costly as well. Alternative financial arrangements with similar properties—such as flexible short-term investment and funding—thereby become more attractive. Those arrangements will be additionally attractive to the extent that they also benefit from an implicit commitment of official support, the same type of support which, ironically, motivated the stiffening of the regulation of the formal banking sector after various past crises.

While strengthening MMF regulations seems well advised, if stronger pre-commitment not to intervene is unavailable, policymakers should be aware that doing so is likely to enhance the incentive for further bypass, using arrangements beyond the banking system and MMFs. Just such an attempt seems to be underway, in the form of stablecoin cryptocurrencies: intermediation arrangements promising investors fixed nominal dollar payoffs, similar to the fixed NAV offered by MMFs. The backing of these arrangements is in some cases opaque (

Yellen 2022), and some arrangements have broken the buck in dramatic fashion (

Wong 2022).

Thus far, official intervention to rescue stablecoin investors has been absent. The regulatory world is at something of a crossroads, however. Officials have suggested that consumer protection and prudential regulation may be warranted, under the presumption that consumers are entitled to expect fixed payoff commitments to be satisfied with higher probability.

17 Regulation aimed at ensuring those fixed payoffs might broadly resemble historic MMF and banking regulations, possibly restricting portfolio holdings or constraining redemption opportunities. A challenge with implementing such regulations lies in that they may create expectations of government financial support to ensure payouts of the established commitments. That path is fraught with difficulties, of course, as the banking and money funds history in the U.S. reflects. Alternatively, officials might want to advocate in favor of the principle of caveat emptor, warning consumers to be aware that these arrangements are outside of the familiar world of regulated financial intermediaries and that heightened prudence is warranted.

5. Conclusions

Ideally, we want financial dealings to be determined by the true economic costs and benefits of alternative instruments and contractual agreements. Yet when a set of financial arrangements benefit from an expectation that government resources will be deployed to rescue participants in the event of distress, that assessment is distorted. We can no longer trust private market participants to choose based solely on the true economic benefits and costs. Financial sectors benefitting from a perceived promise of support will overexpand. Moreover, they will underweight risks that may induce that support and overweight arrangements that make them vulnerable in the event of distress.

While we might be better off in a world in which the relevant authorities can credibly commit ex-ante to not providing support ex-post, that world may not be available to us at present. If so, then, MMFs should be required to have contractual commitments in place, in advance, for liquidity support from reliable private third parties in the event of financial distress. Such requirements would enhance the ability of the official sector to resist intervening and provide market-based incentives for MMFs to mitigate funding risks.

To be clear, we are not suggesting here to go back to the situation pre-2014 reforms. On the contrary, our suggestion is to complement those regulatory enhancements by introducing explicit private liquidity support, the pricing of which effectively acknowledges the cost that such support entails. Taxpayers should not be residual bearers of oversized liquidity risk taken by financial institutions partially responding to distorted incentives.

The approach we are advocating to address this limited commitment problem is, we believe, applicable more broadly, beyond just prime MMFs. The idea is to put in place mechanisms that reduce the perceived need for official intervention in the event of financial distress. We are guided by the nature of the typical official intervention, and we propose to ask MMFs to contract ex-ante with other private parties for the type of contingent liquidity support that would be provided by the government in the case of lost funding. In a different context, living wills work in a similar fashion; they specify private sector funding to take the place of government funding that would otherwise be provided if a bank finds itself in trouble, and in this way, should reduce the need for official support. We believe this general principle could be used productively to address many of the issues that arise from the government’s inability to commit to not intervening in stressed financial markets.

{kind=link}

{kind=link}

{kind=link}