5.1. Step I: Information Modeling

There are two risk variables (

RV) in soybean production projects, the variable operating cost (

VOC) and the soybean selling price (

SP). The risk variables for soybean oil production plant projects are the CBOT soybean price (

PC) (the internationally traded price on the Chicago Board of Trade is the basis for calculating the plants’ variable operating cost) and the soybean oil selling price (

OP). We consider that the risk variables (

RV) follow a GBM, whose characteristic parameters are specified in

Table 3.

Table 4 presents the correlation matrix for the risk variables, where

SP-

Fj (

j = 1, 2, 3) denotes the selling price of soybeans in field Fj, and

OP-Pj (

j = 1, 2, 3) denotes the selling price of soybean oil in plant

Pj.

VOC is the variable operating cost in the soybean fields, and

PC is the CBOT soybean price. The values shown are approximations that can usually be considered for the stipulated projects. Thus, one can notice a high correlation between the

PC prices and those negotiated in the fields,

SP (usually the CBOT price is a reference), but these correlations are lower when compared to the variable operational costs (

VOC) and the soybean oil selling prices (

OP), which are specific to each company. Strictly speaking, a more precise calculation would require historical series obtained from real companies, but the values defined keep coherence with the type of projects exemplified in the portfolio.

5.2. Step II: Portfolio Optimization without Real Options

For soybean field projects, the cost of capital,

µ, is assumed to be 8% p.a., and for soybean oil plant projects, 9% p.a. The risk-free rate (

rf) is 3% p.a. Using the information in

Table 1 and

Table 2, the expected cash flows are constructed for each project, and the risk variables are simulated using GBM (with their correlations).

Table 5 shows the cash flows for project F1 starting at

t’ = 0.

Row (a) in

Table 5 indicates the production level for each year. As shown in

Table 1, the initial production for F1 is 5 MM tons, but from year 2 to year 3, production increases at a rate of 4%, resulting in levels of 5.20- and 5.41-MM tons, with this last level remaining constant until the end of the project life. The risk variables (rows (b) and (c)) are simulated following a GBM. In order to illustrate how these simulations are performed, we present the formula used for SP, using the parameter values provided for F1 in

Table 3:

Equation (19) is the equation of a GBM in discrete form. Where ∆

t = 1 (year), the drift (

αsp) was transformed in continuous time by applying the function ln(1+

αsp) and

as an i.i.d. Normal correlated with the other risk variables (

RV) according to the correlation coefficients shown in the second column of

Table 4. Each simulation

will result in a different value but will be correlated with all risk variables in the portfolio. A practical way to simulate the correlated risk variables in an Excel spreadsheet is through @Risk’s RiskCorrmat function, which was used in this paper to run the simulations.

Table 5 presents the expected values for the risk variables. Still exemplifying with

SP, when performing a large number of simulations, the expected values converge to Equation (20):

Therefore, when considering expected values for the risk variables, the PVt’=0 of row (i), calculated according to Equation (4), would be the expected present value for the F1 project. E[PV]t’ = 1847.95. Similarly, the NPV0 of row (l) calculated with Equation (10) would also be the expected NPV at t = 0, E[NPV0] = 1097.95.

By setting up F1(0) simulated cash flows for the other projects at different starting dates, we obtain the expected values shown in

Table 6 (the largest E[

NPV0] for a given

t’ in each project are highlighted in bold).

The nomenclature Fj(t’) and Pj(t’) is used to indicate that the project Fj or Pj (j = 1, 2, 3) starts in period t’ (t’ = 0, 1, 2). So that the different expected values can be compared, they must be discounted at the risk-free rate rf. Therefore, E[NPV0] = E[NPV]t’ × (1 + rf.)−t’. If the choice of a project’s start time were based solely on the largest E[NPV0] for each t’ = 0,1, and 2, there would be no need to optimize the portfolio, thus ensuring the largest E[NPV0] in the portfolio. However, in doing so, the effect of risk is disregarded. The choice should be made by optimizing a performance measure that indicates the expected return per unit of risk taken.

The analysis by the Omega performance measure uses in its calculation the complete distribution of NPV of all projects in portfolio P, not being restricted to its mean and variance. The objective function of Equation (6) is then optimized subject to the constraint of Equation (8), and L = 0 is stipulated, i.e., the investor accepts at least to obtain a NPV = 0, which pays his cost of capital.

For comparison purposes, the portfolio has also been optimized using Markowitz’s mean-variance theory. In this case, the optimization program maximizes the expected NPVP divided by the standard deviation, E[NPVP]/σP (Equations (11) and (12)). In both Omega and mean-variance optimization, fifty thousand iterations were used to obtain the NPVP distribution (Equation (7)), necessary for the calculations of the optimized performance measures.

The results for both optimization models as well as the not optimized portfolio (from

Table 6) are summarized in

Table 7.

When

wj(t’) = 1, project

j must start in period

t’. For example, using the mean-variance methodology, project P2 would be started at period

t’ = 2 (

wP2(2) = 1), while with the Omega measure, it would be started at period

t’ = 1. Choosing this project by the highest E[

NPV0] (

Table 6), i.e., not optimized, P2 would be started at

t’ = 0.

Once the

wjt’ have been defined, the

NPVP distributions of the portfolios are built with the results obtained in each methodology, following Equation (7). From these distributions, the main statistics of the portfolios are calculated, as shown in

Table 8.

Table 8 shows that the non-optimized portfolio has the highest expected return, but its performance measures, both the E[

NPVP]/

σP and Omega, are inferior compared to portfolios optimized by mean-variance and Omega (

L = 0), respectively. Thus, the best risk-return ratio does not occur in the non-optimized portfolio. On the other hand, all portfolios show significant values at moments of skewness and kurtosis, which indicates that they are not normal distributions. This is reinforced through the Jarque-Bera normality test (

Jarque and Bera 1980), where values very far from zero are obtained. Optimization by mean-variance does not take into account higher-order moments of the distribution, limiting its analysis to the first two moments since we see that higher-order moments are relevant. Optimization by the Omega measure, on the other hand, takes into account the real shape of the

NPVP distribution. Therefore, the results obtained by this methodology are the ones we will consider.

5.3. Step III: Portfolio with Real Options

According to the optimization done in the previous step (Omega measure), the start times of each project were determined. Thus, we will consider the following projects in the portfolio, F1(0), F2(0), F3(0), P1(2), P2(1), and P3(1) (the number in parentheses indicates the start time

t’). The expected present values of these projects, E[

PV]

t’, and investments (

It’), were calculated in the second step of the methodology (

Table 6). The volatilities of the projects at their respective starting times should also be calculated. For this, we suggest applying the method described by

Brandão et al. (

2005) (BDH method), simulating the cash flows of all projects together to capture the effect of the correlation among the risk variables.

Table 9 summarizes the results of E[

PV]

t’,

It’ and volatilities (

σproject(t’)).

By applying Equation (14), the correlation coefficients among the projects’

PVs are calculated, and the matrix is shown in

Table 10.

Next, we will include some real options in the projects. Suppose that at

t = 5, the firm has the option to exercise one of three types of real options. These options and their parameters for each project are shown in

Table 11.

The real options in

Table 11 are mutually exclusive. In year 5, only the option that results in the highest value of the project in that year can be exercised (or not). Risk-neutral simulations of the average present value (E[

PV]

t’) are run simultaneously for the six chosen projects (Equation (15)), and the indicated real options are inserted in year 5.

Table 12 shows how the options in the projects were evaluated using the F1(0) project as an example in a given simulation (in total, 50,000 simulations were run using @Risk software), taking into account the parameters of

Table 9.

In

Table 12, row (a), rate (

CF/PV) comes from row (j) of

Table 5. This rate serves to calculate the expected value of

CF (row (d)) when multiplying, in a given year, the value of row (a) with the value of row (c). The path that was simulated is in row (b), using Equation (15). In such an equation, let us assume that the dividend rate (

δj) has a value equal to zero and that

N(0,1) is an i.i.d. Normal correlated with the other

PVs of the projects, according to the correlation matrix in

Table 10. In addition, for each passing year, before calculating a

PVt=i, we must subtract from

PVt=i−1 that year’s

CF, (

CF/PV)

t=i−1 ×

PVt=i−1 (annual cash flows are assumed not reinvested). The expected values of

PV and E[

PV]

t=i (row (c)), also follow this reasoning. For example, with

rf = 3%, E[

PV]

t=2 is equal to (E[

PV]

t=1 − E[

CF]

t=1) × exp(

rf).

The results PV5(E); PV5(C); PV5(A); PV5(N) are presented, which correspond to the project’s present values at t = 5 when exercising the options to expand, contract, abandon, or continue without exercising any option. The way to calculate the present values with options depends on the type of option. In the expand option, the expansion factor is multiplied to the simulated value (without options) of PVt=5, subtracting CFt=5 beforehand, decreasing the cost to expand, and adding the CFt=5. In the contraction option, the contraction factor is multiplied by the simulated value (without options) of PVt=5, subtracting CFt=5 beforehand, adding the recovered value, and adding the CFt=5. In the abandonment option, the salvage value plus CFt=5 is obtained at t = 5.

In the simulation presented, PV5(A) was the highest. Therefore, the option to abandon is exercised. Thus, PVt=5 (row b) will be equal to PV5(A). The real option value at t = 5, for the case presented would be PV5(A) − PV5(N) = 154.84 − 127.95 = 26.89. When running a large number of iterations of the simulation, in some cases, other options will be exercised, or none will be exercised (in this case, the real option is zero). At the end, a distribution of values of real options in t = 5 will be obtained , values that must be discounted at the risk-free rate in t = t’, to obtain the distribution in that year . Thus, to calculate the expected value of the option in t’ = 0 () for the F1(0) project, it would be equal to the expected value of the distribution , i.e., . After 50,000 simulations, that distribution was obtained and = 143.27. Another way to calculate is by subtracting the expected value of PV5 without options from the expected values of PV5 with options. In the example, at each simulation, E[Max(PV5(E); PV5(C); PV5(A); PV5(N))] offers the highest PV5, averaging at the end resulted in the value of 1137.16. In turn, E[PV]t=5 = 970.70 (row (c)). Therefore, = 1137.16 − 970.70 = 166.46, and discounted to t’ = 0, = 166.46 × exp(−5rf) = 143.27. On the other hand, and were calculated for each project using Equations (16) and (17), respectively.

By performing path simulations of E[

PV] and real options, as done for F1(0) in the other five designs, we will obtain the results shown in

Table 13. It is appreciated that real options always add value to the projects, and as far as possible, they should be included when evaluating portfolios of investment projects.

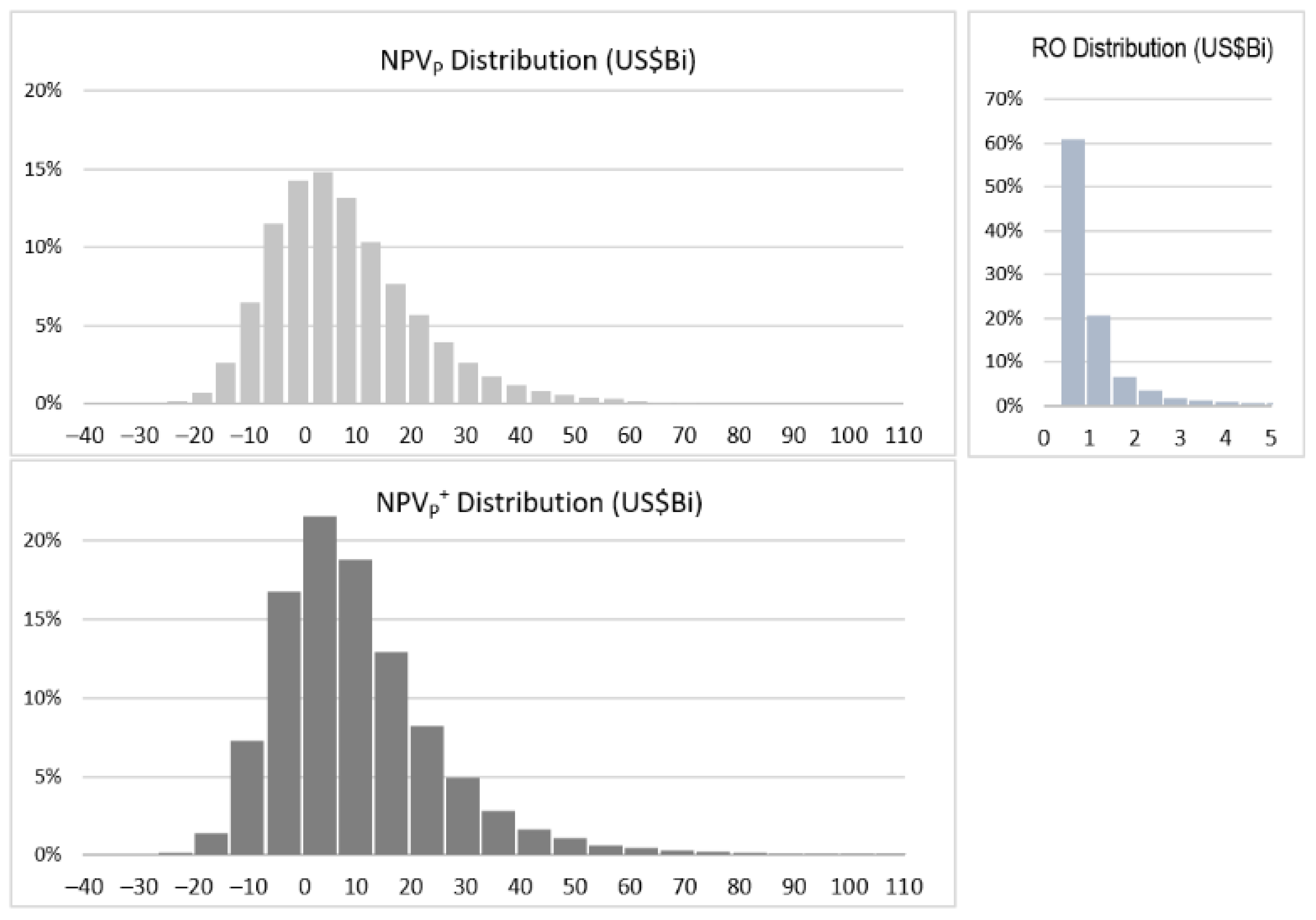

Figure 1 shows the distribution of the

NPV of the portfolio without real options (

NPVP), the distribution of real option values (

RO), and the distribution of the

NPV of the portfolio with real options

.

Note that in

Figure 1, the distribution of real options consists exclusively of positive values, highly concentrated in values below US

$1000 MM, which, when added to the

NPVP distribution, results in the portfolio distribution with real options,

NPVP+, clearly with a higher kurtosis, thus increasing the mean of the portfolio’s

NPV distribution from US

$5896.36 MM to US

$7251.21 MM.

{kind=link}