1. Introduction

The banking and financial industries are undergoing a transformation as a result of technological advancements [

1,

2,

3]. Financial institutions now face increased competition, evolving client needs, and the requirement for stringent control and risk management in a very dynamic market. Simultaneously, technology has enabled the development of sophisticated business intelligence tools [

4]. There are technologies that the banking and financial industry can employ to exploit consumer data in order to gain insights that can result in more intelligent management practices and business decisions [

5,

6,

7]. To that end, there are several ways that banking and finance organisations are leveraging Business Intelligence (BI) technologies to increase profitability, mitigate risk, and gain a competitive edge. Business intelligence enables banks to react to changing economic conditions in both normal and tumultuous economic times [

8].

Globally, business intelligence (BI) methods and technologies help banks gain a better understanding of their operations, their clients, and their prospects. Additionally, BI can pave the way for efficiency by highlighting areas ripe for cost-cutting initiatives, new business opportunities, and more. Banking business intelligence helps users to integrate numerous and dissimilar system sets in order to present dynamic data visualisation dashboards that would not be capable of communicating across platforms in the absence of banking business intelligence [

9,

10]. Standardising that banking information is a mammoth undertaking that requires multiple workers to spend several weeks each month to finish. That is the present state of play for the majority of banks attempting to implement business intelligence in banking. Consider installing a software layer on top of all those disparate banking services data stores that connect them all and enable “live” reporting of all data at the same time. While that may sound like the simplest remedy possible, much work must be done to standardise the underlying data before they can be used effectively [

6,

11].

Banks cannot afford to simply add workers in order to increase income [

1,

12,

13,

14]. They must always look for ways to improve the efficiency of their present employees. Banks can utilise business intelligence tools to examine operational operations in order to help minimise ongoing expenses and/or maximise available resources and expertise. Banks can identify methods to improve and enhance the customer experience at the point-of-contact by assessing the performance of branch workers who engage with the customer base. Banks employ business intelligence technologies to monitor customer, product, and branch profitability [

4,

15,

16]. Banks are increasing profitability and tracking improvement through effective pricing strategies and efficient business operations. Additionally, business intelligence technologies are utilised for predictive analytics to determine which customers may be interested in acquiring which goods, when, and how (in-person, over the web, or direct mail) [

5]. Banks can use this additional data to develop new and enhanced goods and services that better fulfil client wants and increase their market competitiveness. Armed with profitability and demographic data on its customer households, banks will have a better idea of what a good prospect looks like and will be able to promote to them more effectively. Cross-selling and up-selling efforts can be more successful if banks know which customers to target [

3,

17]. Additionally, business intelligence systems can be used to analyse developments outside a bank in order to develop alternative investment plans. Investors can acquire particular insight into sentiment and build trade signals by analysing data from social media [

18]. Through the use of analytics and business intelligence technologies, entirely new categories of investing are developing. Financial institutions must be as lean and efficient as possible in today’s ultra-competitive industry. By analysing operational processes with business intelligence tools, banks can decrease ongoing costs and maximise available resources and knowledge [

19]. Organisations can identify methods to improve and enhance the customer experience at the point of contact by assessing the performance of customer-facing staff such as sales representatives, tellers, and account managers.

A limited amount of business intelligence (BI) studies has been found in Bangladesh [

12,

20,

21,

22,

23,

24]. Tumpa, Saifuzzaman [

20] studied the BI covering the mental healthcare sector of Bangladesh; Arefin, Hoque [

21] studied on organisational culture and BI; Al-Hasan, Aktar [

22] presented BI model for textile industries; Babu [

12] stated the challenges of artificial intelligence in Bangladesh; Nahar, Naheen [

23] studied artificial intelligence and fire surveying; and Biswas, Rahman [

24] stated the roles of emotional intelligence. However, there is a gap regarding the association of business intelligence with operational efficiency and perceptions of profitability of banks in Bangladesh.

Furthermore, only a few studies on business intelligence were found internationally [

17,

18,

25,

26,

27,

28,

29,

30]. Lim, Chen [

18] studied on business intelligence analytics and operations but did not link profitability; Ranjan [

25] showed the links between BI and strategic decision making; Elbashir, Collier [

17] found links between BI and bank performance; Sahay and Ranjan [

26] studied on BI and supply chain analytics; Nofal and Yusof [

27] researched BI and enterprise resource planning; Işık, Jones [

28] found links of BI with environmental decision and operational efficiency; Olszak [

29] studied the application of BI by collecting qualitative data; Yiu, Yeung [

31] links BI and profitability; and Lawrence [

30] found linked of BI with operational efficiency in hospitals. Thus, there is a gap in the association of BI with bank operational efficiency and profitability in the business intelligence literature internationally.

The study found a dearth of business intelligence studies in banking companies in both nationally (Bangladesh) and internationally. Furthermore, Tumpa, Saifuzzaman [

20], Al-Hasan, Aktar [

22], Biswas, Rahman [

24], Lim, Chen [

18], Elbashir, Collier [

17], Olszak [

29], and Lawrence [

30] suggested further study as BI has implications on businesses. In Bangladesh, banking companies are going to implement BI to attain a strong business frame. Thus, the study developed a research model (see

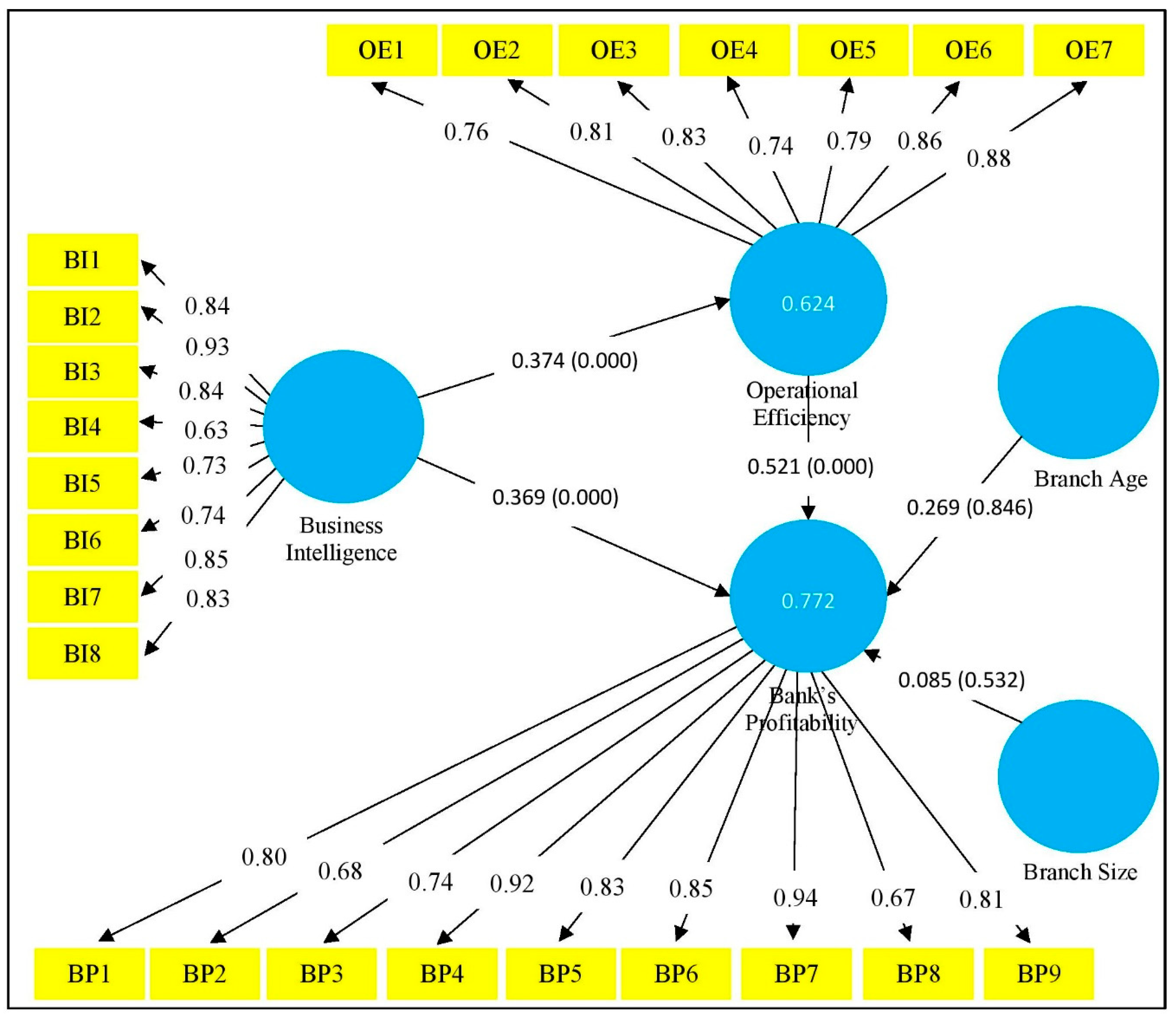

Figure 1) that links business intelligence with the operational efficiency and profitability of banks. More specifically, the study seeks answers to the following questions: “What is the impact of business intelligence on the operational efficiency of banks ?” and “What is the impact of business intelligence on the profitability of banks ?” Thus, the study aims to examine the effects of business intelligence on the operational efficiency and profitability of banks.

Figure 1 shows the conceptual model of the study.

The study uses 259 responses from general manager, senior officers, general officers, and employees of 27 branches of a commercial bank in Bangladesh, employing simple random sampling technique. This research uses the partial least square- structural equation modeling (PLS-SEM) method to test the hypotheses. The study verifies construct’s reliability by factor loadings, Cronbach’s alpha, rho-value and composite reliability while verifying construct validity by average variance extracted and the Fornell-Larcker criterion for the measurement model. Then, the study tests the structural model’s fitness through the f-square, R-square, standardized root means square residual, and normed fit index methods. The study finds that business intelligence is positively significant in improving operational efficiency and profitability of the branches. Furthermore, the study reveals that operational efficiency through business intelligence positively affects the profitability of the branches. Based on competitive theory, this research states that business intelligence allows a productive entity to generate superior margins compared to its market rivals. Thus, banks can offer better options more cheaply than their rivals and thereby ensure competitive advantage. Furthermore, based on resource-based view theory, the study argues that business intelligence as a strategic resource can provide a foundation to develop bank capabilities that can lead to superior performance over time.

This study contributes in at least four respects. First, the study shows a positive and significant relationship between business intelligence and operational efficiency in banks. This finding is unique in both national and international literature. Thus, management bodies and policymakers can implement this finding in banking companies to enhance operational efficiency. This finding somewhat complementary to Tumpa, Saifuzzaman [

20], Işık, Jones [

28], Olszak [

29], and Lawrence [

30] who conceptualises BI in the same direction. Furthermore, the study finds that business intelligence significantly increases the profitability of banks. Thus, this finding will create insights for banks and particularly for banking companies. This finding is also complementary to Arefin, Hoque [

21], Biswas, Rahman [

24], Ranjan [

25], Elbashir, Collier [

17], and Olszak [

29]. Second, the study employs resource-based view theory of business intelligence to explain the association between BI, operational efficiency, and bank’s profitability. Thus, this research has theoretical contribution in this respect. Third, structural equation modelling through the PLS technique, which offers an evaluation of the model fitness as to the reliability and validity of each tested construct and the overall model, was employed for the methodological contribution. Thus, the findings of this study are derived from the best-fitted model and make a methodological contribution to previous research [

8,

12,

20,

28,

32,

33,

34,

35,

36].

The rest of the paper presents the literature review and hypothesis development in

Section 2, research methodology in

Section 3, analysis and results in

Section 4, Final two sections cover discussion and conclusions, respectively.

3. Research Methodology

The sample of the study consists of 27 branches out of 38 branches of a commercial bank in Bangladesh. Hair, Hult [

64] stated that a simple random sampling method ensures the unbiased selection of samples. Thus, the study applies simple random sampling in selecting all the branches. A random number generator (

https://www.random.org/ accessed on 2 January 2022) has been used to ensure the random selection of the branches. The researchers collected contact numbers from the website of the bank (

https://www.sonalibank.com.bd/ accessed on 25 November 2021) and communicated over the mobile phone. While 32 branches agreed to participate in the study ultimately only 27 branches provided us a proper timeline to proceed with them. As Alvarez, Núñez-Cortés [

65] argued that a 10% sample is appropriate for a PLS-SEM analysis, we reached the range of 71% (27/38). We spread 10 questionnaires aimed at manager (1), senior officers (3), general officers (3), and employees (3). Thus, the total respondents should be 270 (27 × 10) but we found 7 blank and 4 partly complete questionnaires. The study uses 259 (270 − 11) responses in the main analysis where the response rate is 96% (259/270).

The study followed a web-based survey to distribute the questionnaire to the bank branches as Dillman, Smyth [

41] stated that this method allows collecting data from a large sample over a dispersed area with a relatively lower cost but higher speed. The study applied the web and mobile survey guidelines of Dillman, Smyth [

41] to design and implement the survey. We used a seven-point Likert scale that ranges from seven for “strongly agree” to one for “strongly disagree”. For the administering purposes, the study adopted the pretesting method of Mokhtar, Jusoh [

66]. We pretested the questionnaires with two accounting lecturers and two cost-and-management accountants. Then, we revised the questionnaires as per the pretesting inputs. We further modified the questionnaires while piloting them with ten known practicing accountants. The study followed the research ethics and guidelines as per the institutional review board. The profiles of the respondents and banks are shown in

Table 1.

There are two sections of survey instruments. Profiles of the banks and participants are covered in section one and section two includes statements of business intelligence, operational efficiency, and bank profitability. The study adopted three items from Nithya and Kiruthika [

6], two items from Lim, Chen [

18], and three items from Ranjan [

25] to measure the business intelligence (BI) variable. Then, to measure bank’s operational Efficiency (OE) variable, the study adopted three items from Lim, Chen [

18], three items from Işık, Jones [

28], and one item from Olszak [

29]. Finally, adopting two items from Nithya and Kiruthika [

6], one item from Richards, Yeoh [

63], two items from Yiu, Yeung [

31], two items from Owusu [

51], and two items from Bordeleau, Mosconi [

16], we measured Bank’s Profitability (BP). This study considers two control variables branch size (number of employees) and branch age (years of operation) as past studies argued that bank size and bank age may affect the relationships of profitability, operational efficiency, and business intelligence.

The study used the partial least square structural equation model (PLS-SEM) to test the relationships of the study model. According to Hair, Matthews [

67], Sarstedt, Hair [

68], and Shmueli, Sarstedt [

69], using PLS-SEM is recommended due to the fact that it is best suited for testing hypotheses and is advanced enough to test theories as well as the goodness of fit criterion, and because it is also competent in examining the connections between multiple latent variables at the same time. PLS-SEM was an excellent choice for analysing the data from this study because we constructed a conceptual model (see

Figure 1) that consisted of several variables for testing multiple associations, making it a good fit for the data. Several aspects of model reliability and validity, including convergent validity and discriminant validity, non-response bias and common method bias, the goodness of fit, model performance and hypothesis testing, as well as a robustness check, have been discussed in greater depth in the analysis section.

5. Discussion

This study found that the application of business intelligence improves the operational efficiency of banks, indicating that a 1% increase in business intelligence implementation improves the operational efficiency of a bank by 0.374%. Data analysis at the local level is substantially facilitated by business intelligence, which assures a high level of accuracy [

22]. Each branch’s cash flow, personnel composition, and urgent needs can be assessed swiftly and separately. As a result, it is an effective tool for assuring, for example, that every bank branch has a healthy financial situation. Predictive analytics added to BI makes it a powerful tool for increasing branch efficiency by automating formerly manual processes [

5]. Improved data management also makes teams more available, allowing them to concentrate on their primary business tasks on a daily basis. The promise of BI is that technology would help organisations become more responsive and flexible, allowing them to take advantage of new opportunities and innovate in a highly competitive market [

6]. Among other things, it promises to enable enterprises to analyse and exploit massive volumes of heterogeneous data in a more efficient and precise manner. Connecting separate systems in banking eliminates the need to manually prepare reports for each one. The use of business intelligence in banking enables institutions to collect unprecedented amounts of data on their consumers, allowing them to better serve their clients [

23]. With banking BI, banks may gain a better understanding of their consumers, allowing them to handle issues before they arise. Business intelligence in banking eliminates the need to manually wrangle data by connecting directly to core system databases [

23,

63]. Decision-makers will be able to acquire a competitive advantage by implementing a BI solution that is company-wide. Making decisions based on data increases the likelihood that those decisions will be correct, as the element of guesswork is eliminated [

63]. Everyone will be happier, wealthier, and wiser as a result of business intelligence. The findings, thus, create insights into how the banking industry can improve its operational efficiency.

Furthermore, the study found that business intelligence increases the profitability of banks, indicating that a bank’s profitability increases by 0.369% if there is a 1% increase in business intelligence implementation. When companies are able to swiftly identify and act on critical operational data, they are more likely to increase their selling efficiency and profit margins. The good news is that most banks can afford the business intelligence (BI) solutions required to facilitate this data analysis [

63]. When the underlying analysis is supported by the correct data, the forecasting load can be greatly reduced and the forecast’s reliability greatly increased. With the help of business intelligence (BI) software, managers have quick and easy access to historical sales data [

68]. The ability to quickly and easily access sales data from the past helps improve forecast accuracy as well as procurement and inventory decision-making.

Finally, the study found that operational efficiency increases the profitability of banks, indicating that a 1% increase in operational efficiency of banks increases the profitability by 0.521%. The key to avoiding unpleasant month-end surprises is to recognize and act on reliable information as soon as possible through BI. To stay on top of the latest company news, sales teams in the modern-day rely on business intelligence (BI) solutions. In these companies, managers and sales representatives are able to quickly comprehend the large picture and then drill down to find specific areas of concern, such as individual goods, accounts, and/or sales regions or representatives [

26,

61,

66]. Organisations that put forth the effort to achieve these sales and marketing objectives stand to gain much from having the appropriate information structured in an efficient manner. The appropriate BI tools may help organisations use their data in new and more efficient ways, regardless of whether or not they already have the data they need. Current BI technologies are easy to adopt and pay for themselves in a matter of months for many banks [

7]. The findings, thus, create insights into the banking industries to improve profitability.

This research is interesting and original because it provides empirical evidence on the positive impact of business intelligence on the operational efficiency and profitability of banks. The study uses a comprehensive approach to measure the reliability and validity of the constructs and test the fitness of the structural model, which enhances the credibility of the findings. Additionally, the study takes a unique perspective by applying two theories, competitive theory and resource-based view theory, to support the argument that business intelligence is a strategic resource that can provide a competitive advantage and lead to superior performance over time.

Furthermore, this study is original in the sense that it was conducted on a sample of 27 branches of a commercial bank, which provides insights into the effects of business intelligence at the local level. This approach is different from previous studies that mostly focus on the effects of business intelligence at the organisational level. The study’s findings have practical implications for the banking industry, as it recommends the use of business intelligence as a tool to enhance decision-making effectiveness and ensure competitive advantage. Overall, this research contributes to the growing body of literature on the impact of business intelligence on organisational performance, particularly in the banking sector. It provides a unique perspective and empirical evidence on the benefits of using business intelligence and offers practical implications for the banking industry’s decision-makers.

6. Conclusions

The purpose of the study is to examine the effects of business intelligence on bank operational efficiency and perceptions of profitability. The study uses 259 responses from general managers, senior officers, general officers, and employees of 27 branches of a commercial bank in Bangladesh, employing a simple random sampling technique. The study finds that business intelligence is positively significant to improve operational efficiency. This finding is somewhat consistent with Tumpa, Saifuzzaman [

20], Işık, Jones [

28], Olszak [

29], and Lawrence [

30] who conceptualizes BI in the same direction. The study finds that business intelligence significantly increases the profitability of banks. This finding also adds value to the studies of Arefin, Hoque [

21], Biswas, Rahman [

24], Ranjan [

25], Elbashir, Collier [

17], and Olszak [

29]. Furthermore, the study reveals that operational efficiency through business intelligence positively affects the profitability of banks. The findings indicate that business intelligence systems can ensure competitive advantage through improved operational efficiency and increased profitability.

Anecdotal evidence on the benefits of BI systems has been lacking until now, but this study fills that gap with empirical evidence gleaned using a PLS-SEM technique. This empirical evidence, which comes from a developing country, is critical because there is a lack of research on the subject in the business intelligence literature. According to this research, BI systems can improve both operational efficiency and profitability for banks by implementing BI solutions. This has given managers and policymakers an understanding of the importance of using a holistic approach when analysing the impact of IT, such as BI systems, because of the intangibility of some of the benefits. The usage of business intelligence (BI) technologies should also be encouraged by bank managers in order to reap financial rewards in the long run. Vendors and other decision-makers in developing nations could make use of the study’s empirical evidence to help raise awareness about BI systems in these countries.

The findings of this study have significant theoretical implications, especially from the perspective of the resource-based view (RBV) theory. According to the RBV, a firm’s resources and capabilities play a vital role in achieving and sustaining competitive advantage and superior performance. This theory posits that firms with unique and valuable resources can gain a competitive advantage over their rivals. This study shows that business intelligence can be viewed as a strategic resource for banks. The study indicates that when banks use business intelligence, they can improve their operational efficiency, which positively affects their profitability. Moreover, the study suggests that the application of business intelligence can lead to the development of bank capabilities, which can ultimately lead to superior performance over time. In other words, the findings of this study suggest that business intelligence can be considered as a strategic resource that provides a foundation for the development of bank capabilities, which can lead to a sustainable competitive advantage and superior performance in the long run. This is an important contribution to the literature on RBV theory, as it demonstrates the importance of business intelligence as a strategic resource for banks, which can contribute to their long-term success and competitive advantage.

This study has some limitations. First, the study targets the branches of a bank (single bank but multiple branches); thus, the results may not be applicable to other banks as the branches are regulated under the same regulatory framework. Second, this study is cross-sectional, and thus, a future study may choose a panel data approach such as the study of Salehi and Arianpoor [

75]. Third, this research uses banks from Bangladesh, and thus, the findings are not generalizable to other economies. Fourth, the study is based on only quantitative data. Future studies may consider mixed-method approach to make the findings more interesting and practical [

76,

77,

78]. Fifth, this research could provide more nuanced insights into the mechanisms through which different types of business intelligence affect bank performance. Thus, future research should explore the effects of specific types of business intelligence, such as data mining, predictive analytics, and data visualisation, on operational efficiency and profitability in the banking sector [

79]. Finally, this research could shed light on the contextual factors that influence the effectiveness of business intelligence in the banking sector, and could inform the development of more tailored business intelligence strategies for different types of banks. Thus, future research could investigate how organisational factors, such as organisational culture, leadership style, and IT infrastructure, moderate the relationship between business intelligence and bank performance.

{kind=link}

{kind=link}