The Value of Craft Beer Styles: Evidence from the Italian Market

Abstract

:1. Introduction

2. The Italian Craft Beer Market

2.1. Market Data

2.2. A Review of Italian Economic Studies on Craft Beer

3. Materials and Methods

3.1. Data Collection and Description

3.2. Empirical Model and Statistical Analysis

4. Results and Discussion

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Cabras, I.; Higgins, D.M. Beer, brewing, and business history. Bus. Hist. 2016, 58, 609–624. [Google Scholar] [CrossRef] [Green Version]

- Betancur, M.I.; Motoki, K.; Spence, C.; Velasco, C. Factors influencing the choice of beer: A review. Int. Food Res. J. 2020, 137, 109367. [Google Scholar] [CrossRef] [PubMed]

- Garavaglia, C.; Swinnen, J. The craft beer revolution: An international perspective. Choices 2017, 32, 1–8. [Google Scholar] [CrossRef]

- Carroll, G.R.; Swaminathan, A. Why the microbrewery movement? Organizational dynamics of resource partitioning in the US brewing industry. Am. J. Sociol. 2000, 106, 715–762. [Google Scholar] [CrossRef] [Green Version]

- Wojtyra, B.; Kossowski, T.M.; Březinová, M.; Savov, R.; Lančarič, D. Geography of craft breweries in Central Europe: Location factors and the spatial dependence effect. Appl. Geogr. 2020, 124, 102325. [Google Scholar] [CrossRef]

- Wojciechowska-Solis, J. Consumer Ethnocentrism on the Market for Local Products: Determinants of Consumer Behaviors. CeON Repozytorium 2022, 373, 75–92. [Google Scholar] [CrossRef]

- Murray, D.W.; O’Neill, M.A. Craft beer: Penetrating a niche market. Br. Food J. 2012, 7, 899–909. [Google Scholar] [CrossRef] [Green Version]

- Jaeger, S.R.; Xia, Y.X.; Le Blond, M.; Beresford, M.K.; Hedderley, D.I.; Cardello, A.V. Supplementing hedonic and sensory consumer research on beer with cognitive and emotional measures, and additional insights via consumer segmentation. Food Qual. Prefer. 2019, 73, 117–134. [Google Scholar] [CrossRef]

- Baiano, A. Craft beer: An overview. Compr. Rev. Food Sci. Food Saf. 2021, 20, 1829–1856. [Google Scholar] [CrossRef]

- Durán-Sánchez, A.; de la Cruz del Río-Rama, M.; Álvarez-García, J.; Oliveira, C. Analysis of Worldwide Research on Craft Beer. SAGE Open 2022, 12, 21582440221108154. [Google Scholar] [CrossRef]

- Aquilani, B.; Laureti, T.; Poponi, S.; Secondi, L. Beer choice and consumption determinants when craft beers are tasted: An exploratory study of consumer preferences. Food Qual. Prefer. 2014, 41, 214–224. [Google Scholar] [CrossRef]

- Atallah, S.S.; Bazzani, C.; Ha, K.A.; Nayga, R.M. Does the Origin of Inputs and Processing Matter? Evidence from Consumers’ Valuation for Craft Beer. Food Qual. Prefer. 2021, 89, 104146. [Google Scholar] [CrossRef]

- Calvo-Porral, C.; Orosa-González, J.; Blazquez-Lozano, F. A Clustered-Based Segmentation of Beer Consumers: From “Beer Lovers” to “Beer to Fuddle”. Br. Food J. 2018, 120, 1280–1294. [Google Scholar] [CrossRef]

- Carbone, A.; Quici, L. Craft beer mon amour: An exploration of Italian craft consumers. Br. Food J. 2020, 122, 2671–2687. [Google Scholar] [CrossRef]

- Carvalho, N.B.; Minim, L.A.; Nascimento, M.; de Castro Ferreira, G.H.; Minim, V.P.R. Characterization of the consumer market and motivations for the consumption of craft beer. Br. Food J. 2018, 120, 378–391. [Google Scholar] [CrossRef] [Green Version]

- Donadini, G.; Porretta, S. Uncovering patterns of consumers’ interest for beer: A case study with craft beers. Food Res. Int. 2017, 91, 183–198. [Google Scholar] [CrossRef]

- Gómez-Corona, C.; Escalona-Buendía, H.B.; García, M.; Chollet, S.; Valentin, D. Craft vs. industrial: Habits, attitudes and motivations towards beer consumption in Mexico. Appetite 2016, 96, 358–367. [Google Scholar] [CrossRef]

- Gómez-Corona, C.; Valentin, D.; Escalona-Buendía, H.B.; Chollet, S. The role of gender and product consumption in the mental representation of industrial and craft beers: An exploratory study with Mexican consumers. Food Qual. Prefer. 2017, 60, 31–39. [Google Scholar] [CrossRef]

- Jaeger, S.R.; Worch, T.; Phelps, T.; Jin, D.; Cardello, A.V. Effects of “craft” vs.“traditional” labels to beer consumers with different flavor preferences: A comprehensive multi-response approach. Food Qual. Prefer. 2020, 87, 104043. [Google Scholar] [CrossRef]

- Lerro, M.; Marotta, G.; Nazzaro, C. Measuring consumers’ preferences for craft beer attributes through Best-Worst Scaling. Agric. Food Econ. 2020, 8, 1. [Google Scholar] [CrossRef] [Green Version]

- Rivaroli, S.; Calvo-Porral, C.; Spadoni, R. Using food choice questionnaire to explain Millennials’ attitudes towards craft beer. Food Qual. Prefer. 2022, 96, 104408. [Google Scholar] [CrossRef]

- Villacreces, S.; Blanco, C.A.; Caballero, I. Developments and characteristics of craft beer production processes. Food Biosci. 2022, 45, 101495. [Google Scholar] [CrossRef]

- Clemons, E.K.; Gao, G.G.; Hitt, L.M. When online reviews meet hyperdifferentiation: A study of the craft beer industry. J. Manag. Inf. Syst. 2006, 23, 149–171. [Google Scholar] [CrossRef] [Green Version]

- Fastigi, M.; Viganò, E.; Esposti, R. The Italian microbrewing experience: Features and perspectives. Bio-Based Appl. Econ. 2018, 7, 59–86. [Google Scholar] [CrossRef]

- Garavaglia, C.; Mussini, M. What is craft?—An empirical analysis of consumer preferences for craft beer in Italy. Mod. Econ. 2020, 11, 1195–1208. [Google Scholar] [CrossRef]

- Donadini, G.; Spigno, G.; Fumi, M.D.; Pastori, R. Evaluation of ideal everyday Italian food and beer pairings with regular consumers and food and beverage experts. J. Inst. Brew. 2008, 114, 329–342. [Google Scholar] [CrossRef]

- Cipollaro, M.; Fabbrizzi, S.; Sottini, V.A.; Fabbri, B.; Menghini, S. Linking sustainability, embeddedness and marketing strategies: A study on the craft beer sector in Italy. Sustainability 2021, 13, 10903. [Google Scholar] [CrossRef]

- AssoBirra. Annual Report. 2021. Available online: https://www.assobirra.it/wp-content/uploads/2022/12/AnnualReport_2021.pdf (accessed on 17 February 2023).

- Microbirrifici the Italian Beer Database. Available online: https://www.microbirrifici.org/ (accessed on 17 February 2023).

- Rosen, S. Hedonic prices and implicit markets: Product differentiation in pure competition. J. Political Econ. 1974, 82, 34–55. [Google Scholar] [CrossRef]

- Ladd, G.W.; Suvannunt, V. A model of consumer goods characteristics. Am. J. Agr. Econ. 1976, 58, 504–510. [Google Scholar] [CrossRef]

- Carlucci, D.; Stasi, A.; Nardone, G.; Seccia, A. Explaining price variability in the Italian yogurt market: A hedonic analysis. Agribusiness 2013, 29, 194–206. [Google Scholar] [CrossRef]

- Szathvary, S.; Trestini, S. A Hedonic Analysis of Nutrition and Health Claims on Fruit Beverage Products. J. Agric. Econ. 2013, 65, 505–517. [Google Scholar] [CrossRef]

- Kennedy, P.E. Estimation with correctly interpreted dummy variables in semilogarithmic equations. Am. Econ. Rev. 1981, 71, 801. [Google Scholar]

- Ramsey, J.B. Tests for specification errors in classical linear least squares regression analysis. J. R. Stat. Soc. 1969, 31, 50–371. [Google Scholar] [CrossRef]

- Silayoi, P.; Speece, M. Packaging and purchase decisions: A focus group study on the impact of involvement level and time pressure. Br. Food J. 2004, 106, 607–628. [Google Scholar] [CrossRef]

- Waldrop, M.E.; McCluskey, J.J. Does information about organic status affect consumer sensory liking and willingness to pay for beer? Agribusiness 2019, 35, 149–167. [Google Scholar] [CrossRef]

- Barska, A.; Wojciechowska-Solis, J. E-consumers and local food products: A perspective for developing online shopping for local goods in Poland. Sustainability 2020, 12, 4958. [Google Scholar] [CrossRef]

- Samadi, R.; Marjanen, H.; Razavian, M.T. Consumers in Limbo: How the COVID-19 Pandemic Has Changed Local Food Consumption in Tehran. Food Stud. 2022, 13, 1. [Google Scholar] [CrossRef]

- Śmiglak-Krajewska, M.; Wojciechowska-Solis, J. Consumer versus organic products in the COVID-19 pandemic: Opportunities and barriers to market development. Energies 2021, 14, 5566. [Google Scholar] [CrossRef]

- Prentice, C.; Chen, J.; Wang, X. The influence of product and personal attributes on organic food marketing. J. Retail. Consum. Serv. 2019, 46, 70–78. [Google Scholar] [CrossRef]

- Barska, A.; Wojciechowska-Solis, J.; Wyrwa, J.; Jędrzejczak-Gas, J. Practical Implications of the Millennial Generation’s Consumer Behaviour in the Food Market. Int. J. Environ. Res. Public Health. 2023, 20, 2341. [Google Scholar] [CrossRef]

- Donadini, G.; Bertuzzi, T.; Rossi, F.; Spigno, G.; Porretta, S. Uncovering Patterns of Italian Consumers’ Interest for Gluten-Free Beers. J. Am. Soc. Brew. Chem. 2021, 79, 356–369. [Google Scholar] [CrossRef]

- Capitello, R.; Maehle, N. Case Studies in the Beer Sector; Woodhead Publishing: Cambridge, UK, 2020. [Google Scholar] [CrossRef]

- Dabić, M.; Vlačić, B.; Kovač, I. Guest editorial: The future of family business: Marketing challenges in times of crisis. J. Fam. Bus. Manag. 2023, 13, 1–6. [Google Scholar] [CrossRef]

- Jędrzejczak-Gas, J.; Barska, A.; Siničáková, M. Level of development of e-commerce in EU countries. Management 2019, 23, 209–224. [Google Scholar] [CrossRef] [Green Version]

- Allen, F.; Cantwell, D. Barley Wine: History, Brewing Techniques, Recipes (Classic Beer Style Series, 11); Brewers Publications: Boulder, CO, USA, 1998; ISBN 978-0937381595. [Google Scholar]

- Alfeo, V.; Todaro, A.; Migliore, G.; Borsellino, V.; Schimmenti, E. Microbreweries, brewpubs and beerfirms in the Sicilian craft beer industry. J. Wine Bus. Res. 2019, 32, 122–138. [Google Scholar] [CrossRef]

- Kumar, S. Price elasticity of alcohol demand in India. Alcohol Alcohol. 2017, 52, 390–395. [Google Scholar] [CrossRef] [PubMed]

- Strong, G.; England, K. 7 Beer Judge Certification Program “BJCP Style Guidelines”. 2015. Available online: www.bjcp.org/docs/2015_Guidelines_Beer.pdf (accessed on 26 January 2023).

- Ruttanajarounsub, R. Hedonic Prices and Country of Origin Bias in the U.S. Brewing Industry. Master’s Thesis, Oregon State University, Corvallis, OR, USA, 2007. Available online: https://ir.library.oregonstate.edu/concern/graduate_thesis_or_dissertations/3b591c328 (accessed on 26 January 2023).

- Gabrielyan, G.; McCluskey, J.; Marsh, T.; Ross, C. Willingness to Pay for Sensory Attributes in Beer. Agric. Econ. Res. Rev. 2014, 43, 125–139. [Google Scholar] [CrossRef]

- Cardello, A.V.; Pineau, B.; Paisley, A.G.; Roigard, C.M.; Chheang, S.L.; Guo, L.F.; Hedderley, D.I.; Jaeger, S.R. Cognitive and emotional differentiators for beer: An exploratory study focusing on ‘‘uniqueness”. Food Qual. Prefer. 2016, 54, 23–38. [Google Scholar] [CrossRef]

- Donadini, G.; Fumi, M.D.; Kordialik-Bogacka, E.; Maggi, L.; Lambri, M.; Sckokai, P. Consumer interest in specialty beers in three European markets. Food Res. Int. 2016, 85, 301–314. [Google Scholar] [CrossRef]

{kind=link}

| Year | % Var. 2011–2021 | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | ||

| Breweries (n.) | 350 | 421 | 509 | 599 | 688 | 757 | 868 | 874 | 853 | 769 | 814 | 132 |

| Artisanal or microbrewers | 336 | 407 | 491 | 505 | 540 | 718 | 693 | 692 | 684 | 624 | 657 | 95 |

| Production (million hL) | 13.4 | 13.3 | 13.3 | 13.5 | 14.3 | 14.5 | 15.6 | 16.4 | 17.3 | 15.8 | 17.6 | 31 |

| Direct employment (n.) | 4500 | 4700 | 4800 | 5000 | 5350 | 5350 | 5470 | 5500 | 5700 | 5200 | 5300 | 17 |

| Import (million hL) | - | 6.2 | 6.2 | 6.2 | 7.1 | 7.1 | 6.4 | 7.0 | 7.4 | 6.3 | 7.0 | |

| Export (million hL) | - | 2.0 | 2.0 | 2.1 | 2.5 | 2.6 | 2.8 | 3.0 | 3.5 | 3.3 | 3.8 | |

| Domestic consumption (million hL) | 17.7 | 17.5 | 17.5 | 17.7 | 18.9 | 19.0 | 19.8 | 20.4 | 21.2 | 18.7 | 20.8 | 18 |

| Per-capita consumption (L) | 28.5 | 28 | 28.5 | 29 | 31 | 31 | 33 | 34 | 35 | 31 | 35.2 | 24 |

| Variables | Variables Description | Mean a |

|---|---|---|

| Price | Beer price EUR/L | 12.502 (min: 3.2–max: 23.93; s.d. 3.30) |

| Glass_Package | 1 = beer in glass bottle | 0.6190 |

| Content_size_33cl | 1 = beer in package size equal or less of 0.33 L | 0.6489 |

| Special_Cap | 1 = beer with special cap (e.g., cork, tear-off cap) | 0.0666 |

| Organic | 1 = beer with organic certification | 0.0191 |

| Gluten_Free | 1 = beer with gluten-free certification | 0.0275 |

| Italian Producers | 1 = beer produced in Italy | 0.4459 |

| American Pale Ale | 1 = American Pale Ale beer style | 0.0607 |

| Abbey | 1 = Abbey beer style | 0.0532 |

| Amber/Brown Ale | 1 = Amber/Brown Ale beer style | 0.0100 |

| Barleywine | 1 = Barleywine beer style | 0.0075 |

| Belgian Ale | 1 = Belgian Ale beer style | 0.0216 |

| Biere de Garde | 1 = Biere de Garde beer style | 0.0017 |

| Sour | 1 = Sour beer style | 0.1032 |

| Fruit | 1 = Fruit beer style | 0.0108 |

| Herbal | 1 = Herbal beer style | 0.0067 |

| Blanche | 1 = Blanche beer style | 0.0333 |

| Bock | 1 = Bock beer style | 0.0166 |

| British Bitter | 1 = British bitter beer style | 0.0158 |

| California Common | 1 = California Common beer style | 0.0008 |

| Dark Lager | 1 = Dark Lager beer style | 0.0083 |

| German Amber Lager | 1 = German Amber Lager beer style | 0.0050 |

| India Pale Ale | 1 = India Pale Ale beer style | 0.2845 |

| Irish Red Ale | 1 = Irish Red Ale beer style | 0.0025 |

| Italian Grape Ale | 1 = Italian Grape Ale beer style | 0.0083 |

| Lager | 1 = Lager beer style | 0.0358 |

| Light Ale | 1 = Light Ale beer style | 0.0399 |

| Pils/Pilsner | 1 = Pils/Pilsner beer style | 0.0266 |

| Porter | 1 = Porter beer style | 0.0250 |

| Saison | 1 = Saison beer style | 0.0333 |

| Smoked | 1 = Smoked beer style | 0.0033 |

| Specialties | 1 = Specialties beer style | 0.0083 |

| Stout | 1 = Stout beer style | 0.0732 |

| Strong Ale | 1 = Strong Ale beer style | 0.0699 |

| Weiss/Wheatbeer | 1 = Weiss/Wheatbeer beer style | 0.0341 |

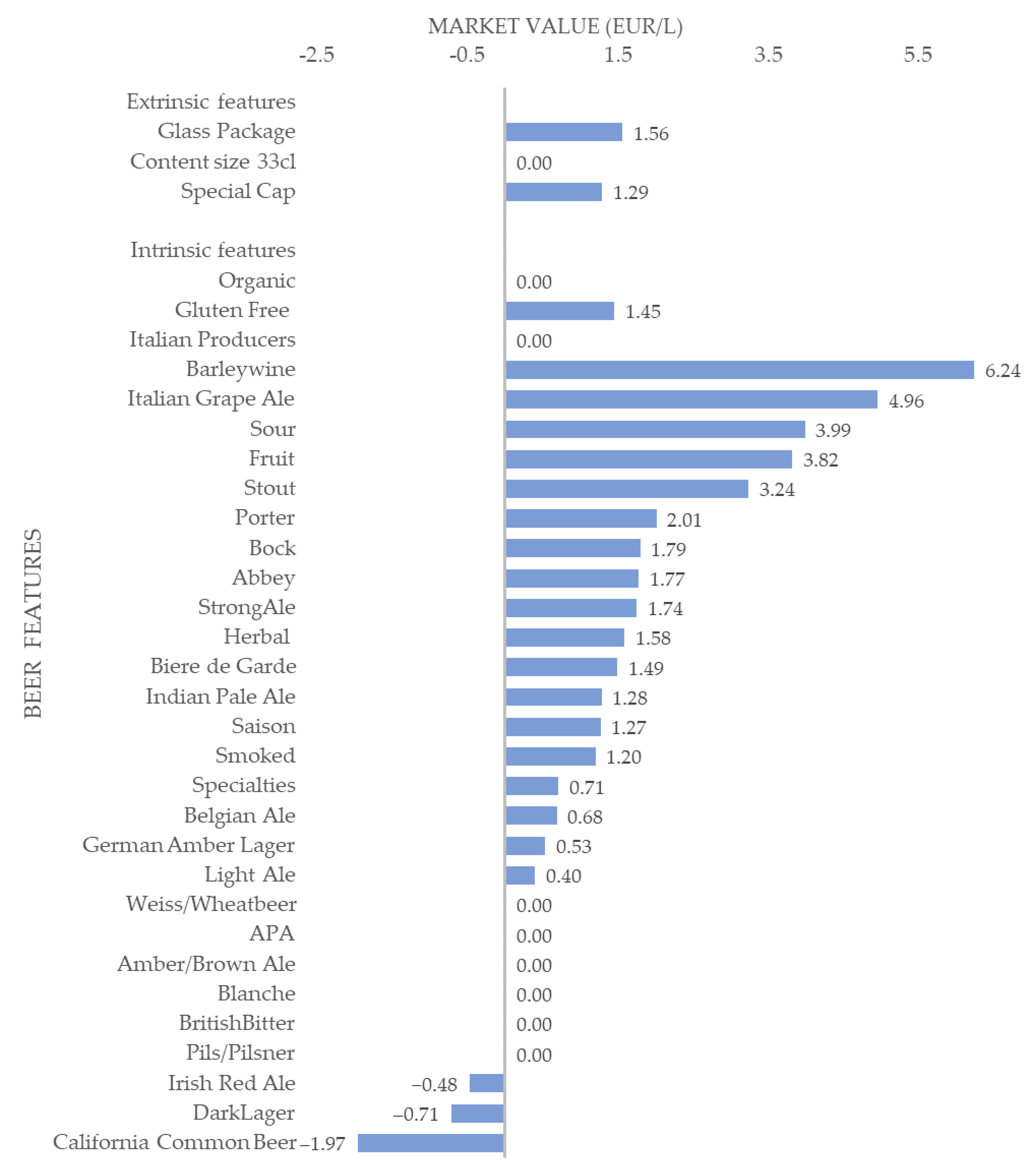

| Variable | β | Percentage Premium Price a |

|---|---|---|

| Glass Package | 0.118 *** (0.0153) | +12.48 |

| Content Size less than 0.33 L | 0.010 (0.0283) | |

| Special Cap | 0.098 ** (0.0488) | +10.32 |

| Organic | 0.044 (0.0430) | |

| Gluten-Free | 0.110 *** (0.0321) | +11.58 |

| Italy | −0.028 (0.0584) | |

| American Pale Ale | 0.026 (0.0166) | |

| Abbey | 0.132 *** (0.0107) | +14.19 |

| Amber/Brown Ale | 0.015 (0.0121) | |

| Barleywine | 0.405 *** (0.0487) | +49.95 |

| Belgian Ale | 0.053 ** (0.0199) | +5.47 |

| Biere de Garde | 0.112 * (0.0623) | +11.88 |

| Sour | 0.277 *** (0.0468) | +31.89 |

| Fruit | 0.266 *** (0.0304) | +30.55 |

| Herbal | 0.119 *** (0.0248) | +12.64 |

| Blanche | 0.009 (0.0160) | |

| Bock | 0.134 *** (0.0405) | +14.35 |

| British Bitter | 0.007 (0.0150) | |

| California Common Beer | −0.171 *** (0.0135) | −15.74 |

| Dark Lager | −0.058 *** (0.0081) | −5.72 |

| German Amber Lager | 0.041 *** (0.0119) | +4.21 |

| India Pale Ale | 0.097 *** (0.0136) | +10.24 |

| Irish Red Ale | −0.038 ** (0.0168) | −3.81 |

| Italian Grape Ale | 0.334 *** (0.0228) | +39.65 |

| Light Ale | 0.031 ** (0.0135) | +3.17 |

| Pils/Pilsner | −0.032 (0.0200) | −3.23 |

| Porter | 0.149 *** (0.0167) | +16.09 |

| Saison | 0.096 *** (0.0266) | +10.15 |

| Smoked | 0.091 * (0.0475) | +9.58 |

| Specialties | 0.055 * (0.0309) | +5.67 |

| Stout | 0.230 *** (0.0375) | +25.93 |

| Strong Ale | 0.130 *** (0.0145) | +13.94 |

| Weiss/Wheatbeer | 0.035 (0.0547) | 3.60 |

| Constant | 2.0568 *** |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Bimbo, F.; De Meo, E.; Baiano, A.; Carlucci, D. The Value of Craft Beer Styles: Evidence from the Italian Market. Foods 2023, 12, 1328. https://doi.org/10.3390/foods12061328

Bimbo F, De Meo E, Baiano A, Carlucci D. The Value of Craft Beer Styles: Evidence from the Italian Market. Foods. 2023; 12(6):1328. https://doi.org/10.3390/foods12061328

Chicago/Turabian StyleBimbo, Francesco, Emilio De Meo, Antonietta Baiano, and Domenico Carlucci. 2023. "The Value of Craft Beer Styles: Evidence from the Italian Market" Foods 12, no. 6: 1328. https://doi.org/10.3390/foods12061328