Spanish Journal of Finance and Accounting (SJFA): Mapping of Knowledge over the Last 25 Years

, and

, and

Abstract

:1. Introduction

2. Methodology

3. Results

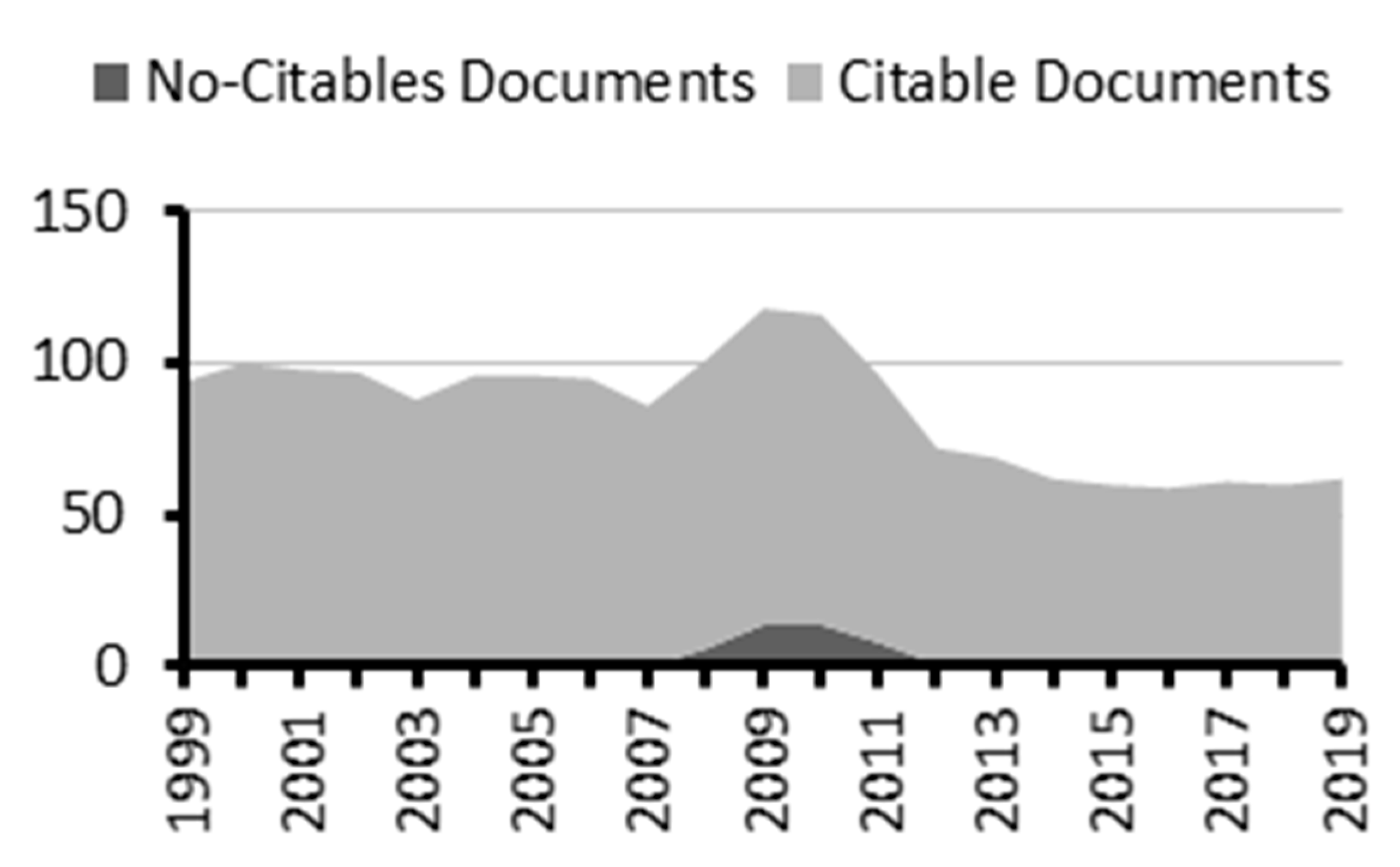

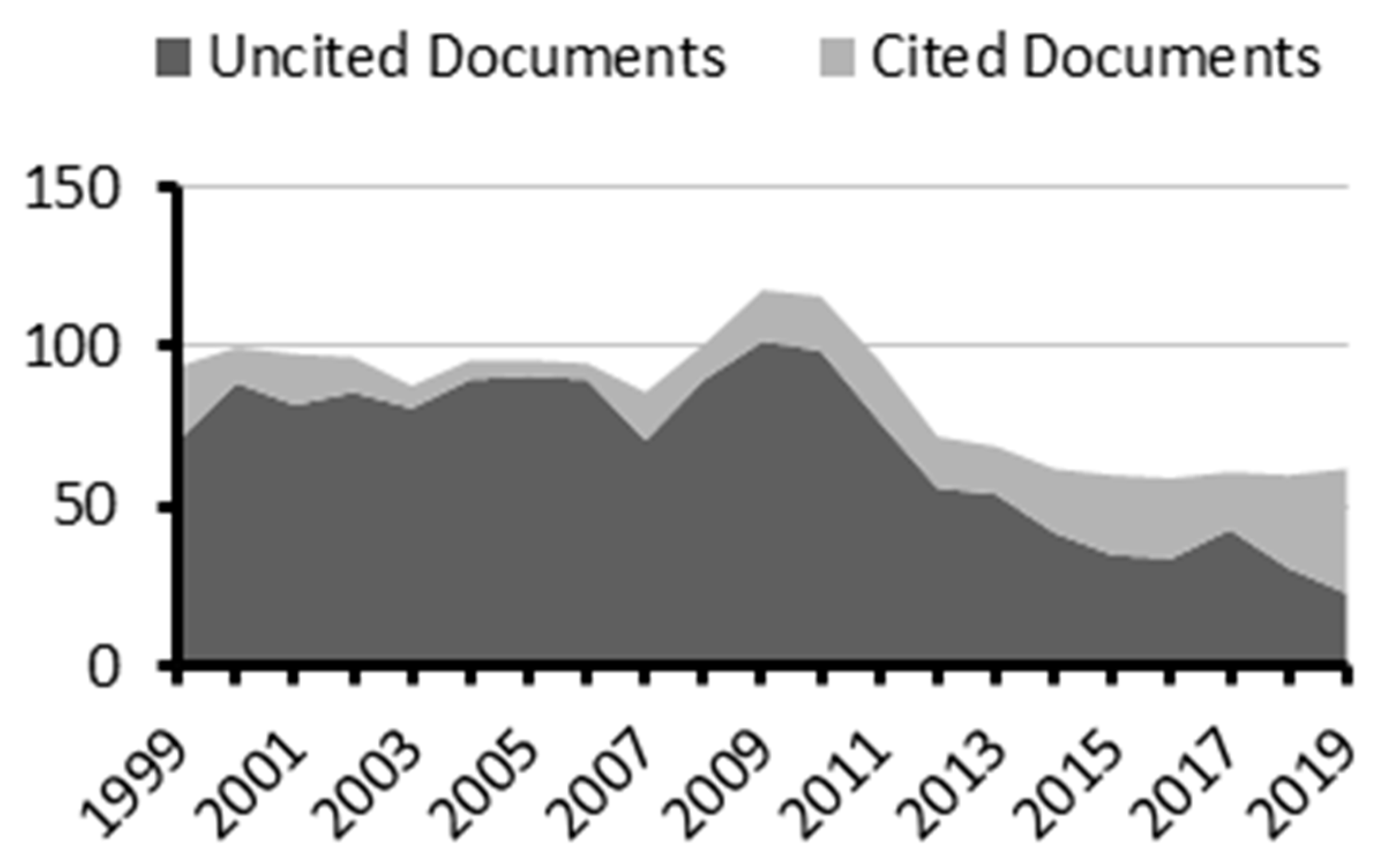

3.1. Publication Structure

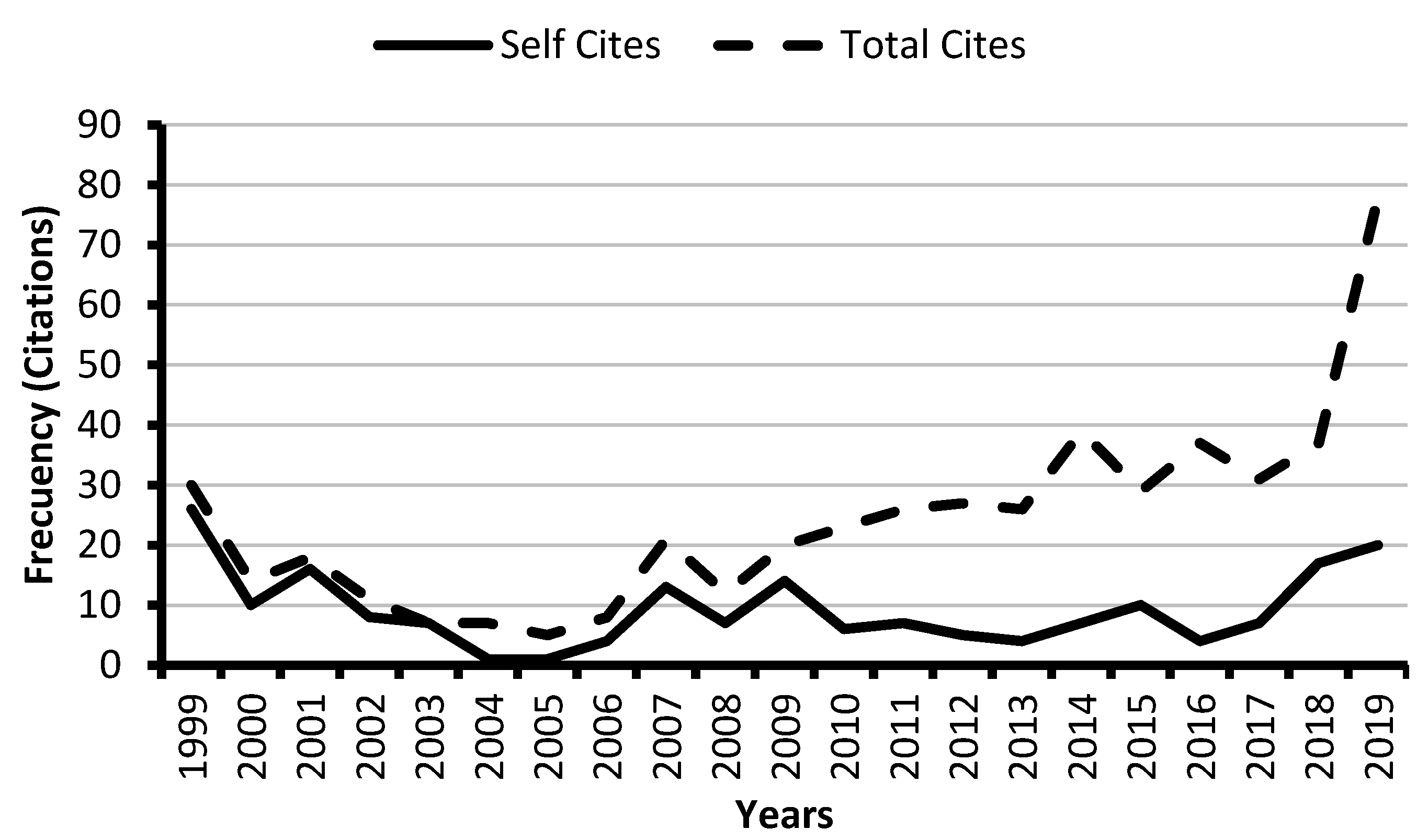

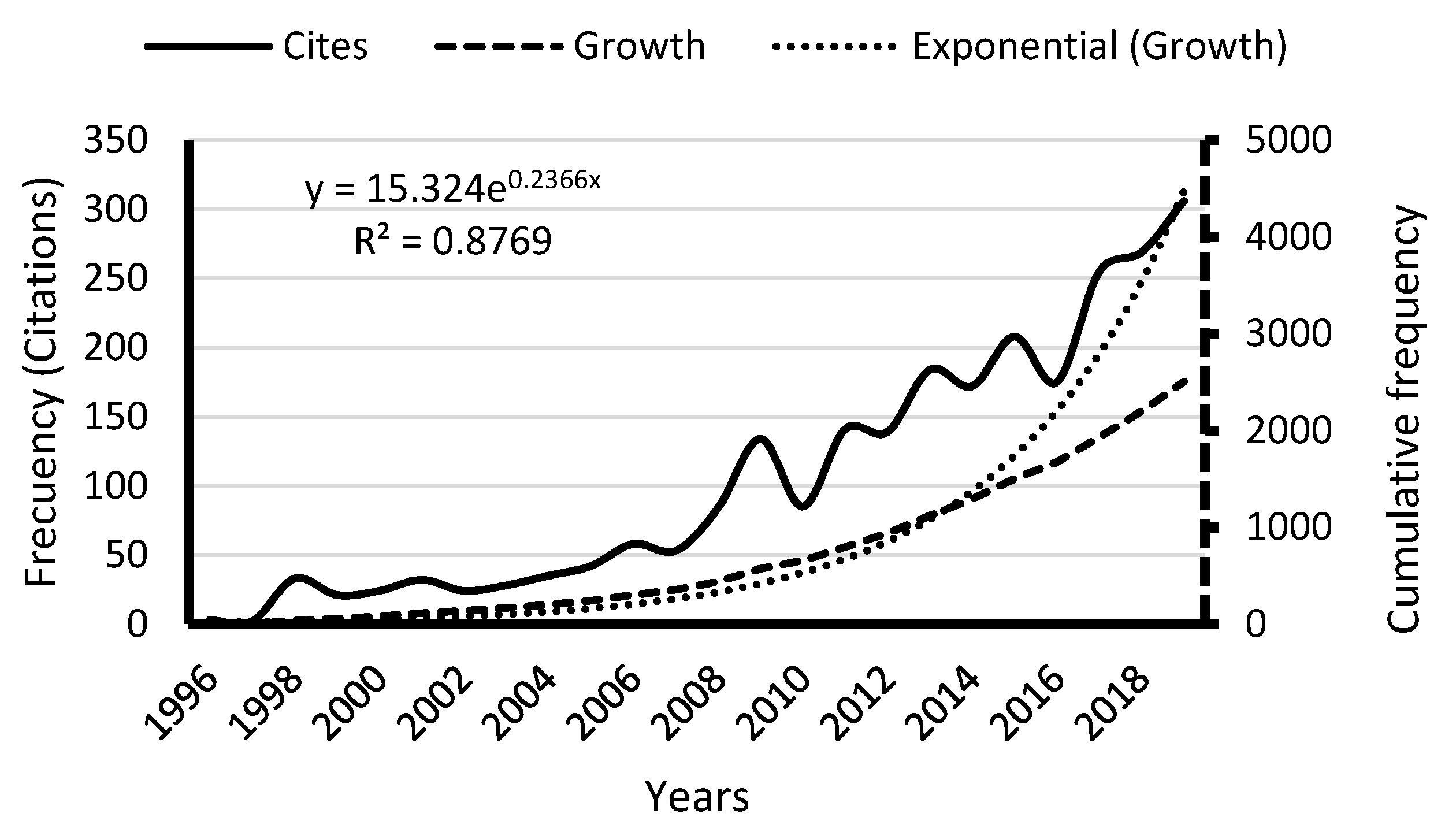

3.2. Citation Analysis

3.3. Influential Papers in SJFA

3.4. Main Authors, Institutions and Countries

3.5. Article References

3.6. Trend in Topics

4. Network Visualisation

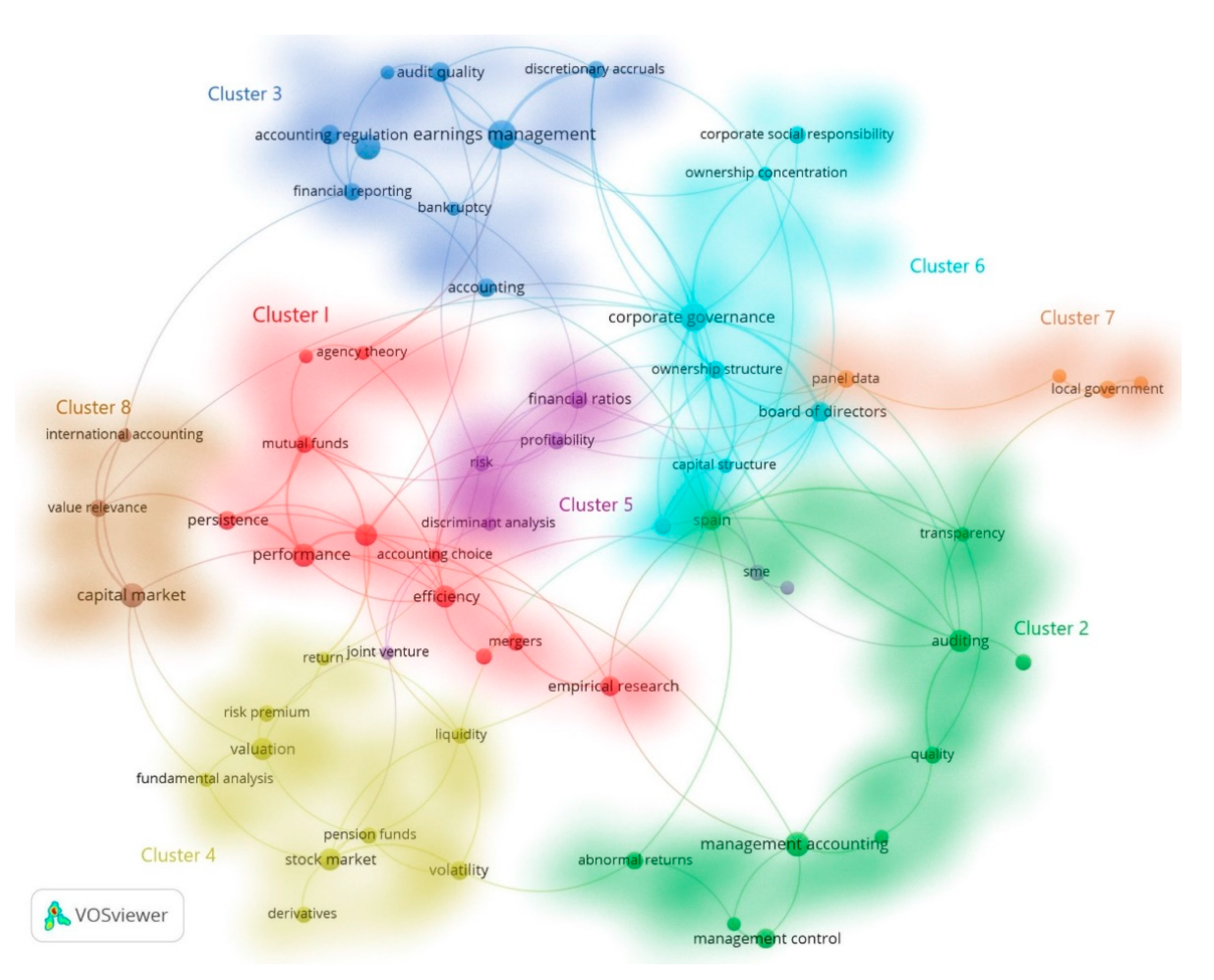

4.1. Co-Occurrence Author Keyword Network

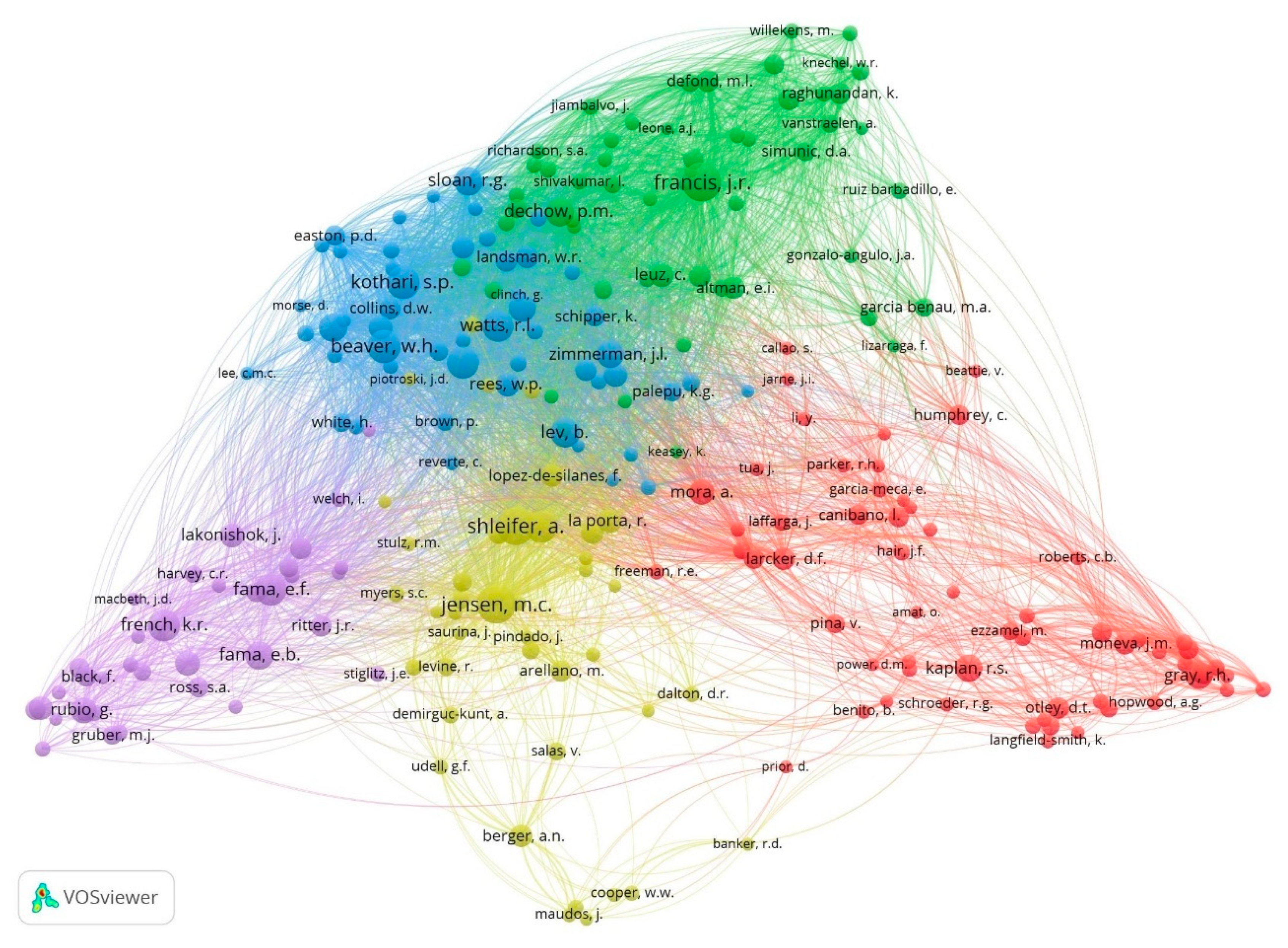

4.2. Author Co-Citation Analysis (ACA)

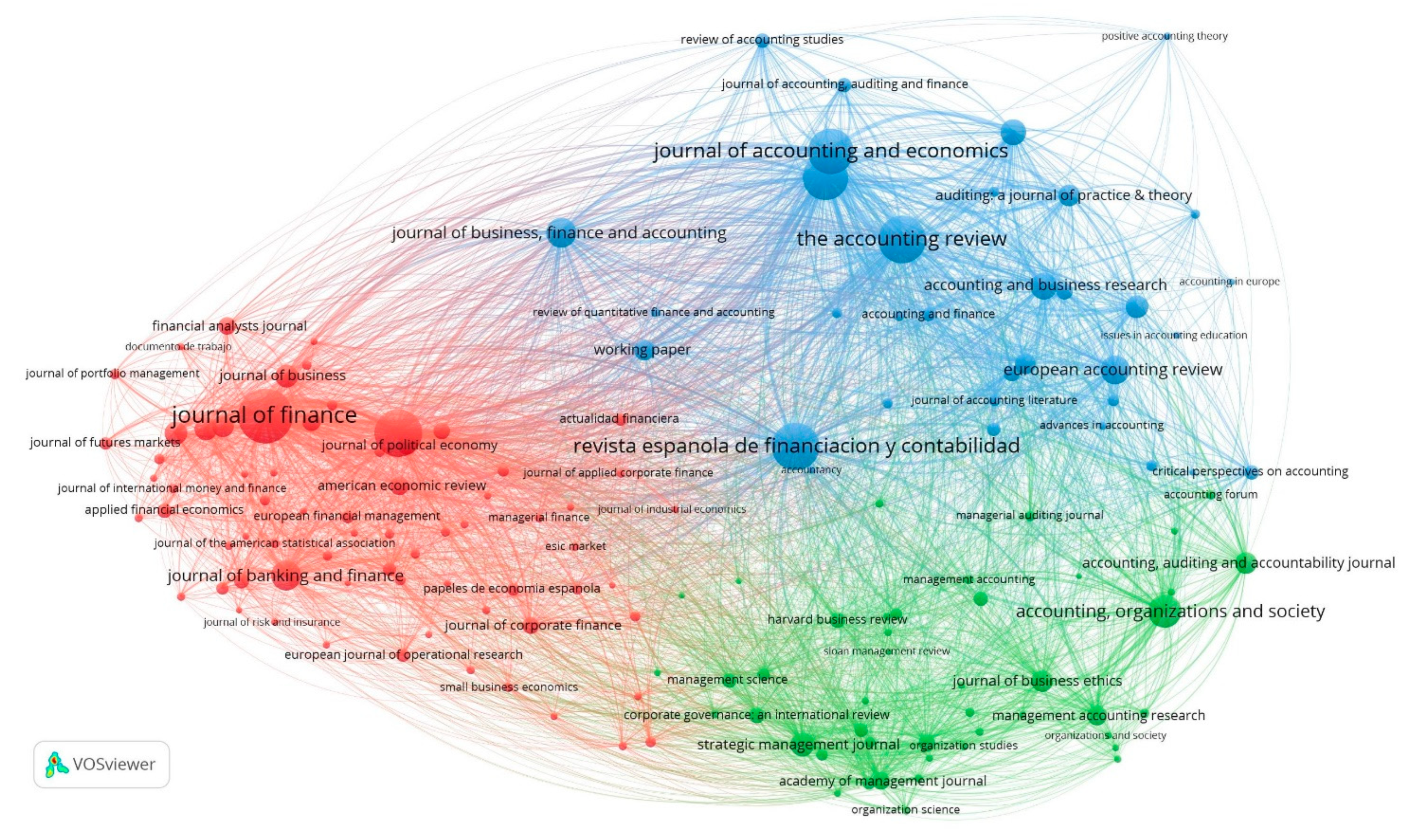

4.3. Journal Co-Citation Analysis (JCA)

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- SJFA. Available online: https://www.tandfonline.com/toc/refc20/current (accessed on 11 January 2022).

- Burton, B.; Kumar, S.; Pandey, N. Twenty-five years of The European Journal of Finance (EJF): A retrospective analysis. Eur. J. Financ. 2020, 26, 1817–1841. [Google Scholar] [CrossRef]

- Baker, H.K.; Kumar, S.; Pandey, N. Thirty years of the Global Finance Journal: A bibliometric analysis. Glob. Financ. J. 2021, 47, 100492. [Google Scholar] [CrossRef]

- Baker, H.K.; Kumar, S.; Pattnaik, D. Twenty-five years of the journal of corporate finance: A scientometric analysis. J. Corp. Financ. 2021, 66, 101572. [Google Scholar] [CrossRef]

- Kumar, S.; Sureka, R.; Pandey, N. A retrospective overview of the Asian Review of Accounting during 1992–2019. Asian Rev. Account. 2020, 28, 445–462. [Google Scholar] [CrossRef]

- Garfield, E. Citation analysis as a tool in journal evaluation. Science 1972, 178, 471–479. [Google Scholar] [CrossRef]

- Merigó, J.M.; Gil-Lafuente, A.M.; Yager, R.R. An overview of fuzzy research with bibliometric indicators. Appl. Soft Comput. 2015, 27, 420–433. [Google Scholar] [CrossRef]

- Frenken, K.; Hardeman, S.; Hoekman, J. Spatial scientometrics: Towards a cumulative research program. J. Informetr. 2009, 3, 222–232. [Google Scholar] [CrossRef] [Green Version]

- Hood, W.W.; Wilson, C.S. The literature of bibliometrics, scientometrics, and informetrics. Scientometrics 2001, 52, 291–314. [Google Scholar] [CrossRef]

- Nicholas, D.; Ritchie, M. Literature and Bibliometrics; Clive Bingley: London, UK, 1978. [Google Scholar]

- Broadus, R.N. Toward a definition of “Bibliometrics”. Scientometrics 1987, 12, 373–379. [Google Scholar] [CrossRef]

- Zhou, P.; Zhong, Y.; Yu, M. A bibliometric investigation on China–UK collaboration in food and agriculture. Scientometrics 2013, 97, 267–285. [Google Scholar] [CrossRef]

- Herbertz, H.; Müller-Hill, B. Quality and efficiency of basic research in molecular biology: A bibliometric analysis of thirteen excellent research institutes. Res. Policy 1995, 24, 959–979. [Google Scholar] [CrossRef]

- Franceschet, M. A comparison of bibliometric indicators for computer science scholars and journals on Web of Science and Google Scholar. Scientometrics 2009, 83, 243–258. [Google Scholar] [CrossRef] [Green Version]

- Belter, C.W.; Seidel, D.J. A bibliometric analysis of climate engineering research. Wiley Interdiscip. Rev. Clim. Change 2013, 4, 417–427. [Google Scholar] [CrossRef]

- Michalopoulos, A.; Falagas, M.E. A bibliometric analysis of global research production in respiratory medicine. Chest 2005, 128, 3993–3998. [Google Scholar] [CrossRef] [Green Version]

- Bonilla, C.A.; Merigó, J.M.; Torres-Abad, C. Economics in Latin America: A bibliometric analysis. Scientometrics 2015, 105, 1239–1252. [Google Scholar] [CrossRef]

- Fagerberg, J.; Fosaas, M.; Sapprasert, K. Innovation: Exploring the knowledge base. Res. Policy 2012, 41, 1132–1153. [Google Scholar] [CrossRef]

- Alexander, J.C., Jr.; Mabry, R.H. Relative significance of journals, authors, and articles cited in financial research. J. Financ. 1994, 49, 697–712. [Google Scholar] [CrossRef]

- Merigó, J.M.; Yang, J.B. Accounting research: A bibliometric analysis. Aust. Account. Rev. 2017, 27, 71–100. [Google Scholar] [CrossRef]

- Corral-Marfil, J.A.; Marín, C.E. Evolución y análisis bibliométrico de la revista Cuadernos de Turismo (1998–2019). Cuad. Tur. 2020, 46, 531–565. [Google Scholar] [CrossRef]

- Gaviria-Marin, M.; Merigo, J.M.; Popa, S. Twenty years of the Journal of Knowledge Management: A bibliometric analysis. J. Knowl. Manag. 2018, 22, 1655–1687. [Google Scholar] [CrossRef] [Green Version]

- Durisin, B.; Calabretta, G.; Parmeggiani, V. The intellectual structure of product innovation research: A bibliometric study of the journal of product innovation management, 1984–2004. J. Prod. Innov. Manag. 2010, 27, 437–451. [Google Scholar] [CrossRef]

- Verma, R.; Lobos-Ossandón, V.; Merigó, J.M.; Cancino, C.; Sienz, J. Forty years of applied mathematical modelling: A bibliometric study. Appl. Math. Model. 2021, 89, 1177–1197. [Google Scholar] [CrossRef]

- Mongeon, P.; Paul-Hus, A. The journal coverage of Web of Science and Scopus: A comparative analysis. Scientometrics 2016, 106, 213–228. [Google Scholar] [CrossRef]

- Cancino, C.A.; Merigo, J.M.; Torres, J.P.; Diaz, D. A bibliometric analysis of venture capital research. J. Econ. Financ. Adm. Sci. 2018, 23, 182–195. [Google Scholar] [CrossRef] [Green Version]

- Gaviria-Marin, M.; Merigó, J.M.; Baier-Fuentes, H. Knowledge management: A global examination based on bibliometric analysis. Technol. Forecast. Soc. Change 2019, 140, 194–220. [Google Scholar] [CrossRef]

- Hirsch, J.E. An index to quantify and individual’s scientific research output. Proc. Natl. Acad. Sci. USA 2005, 102, 16569–16572. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Costas, R.; Bordons, M. The h-index: Advantages, limitations and its relation with other bibliometric indicators at the micro level. J. Informetr. 2007, 1, 193–203. [Google Scholar] [CrossRef] [Green Version]

- Plomp, R. The significance of the number of highly cited papers as an indicator of scientific prolificacy. Scientometrics 1990, 19, 185–197. [Google Scholar] [CrossRef]

- Krampen, G.; Becker, R.; Wahner, U.; Montada, L. On the validity of citation counting in science evaluation: Content analyses of references and citations in psychological publications. Scientometrics 2007, 71, 191–202. [Google Scholar] [CrossRef]

- Archel, P. Social and environmental information reporting of big size Spanish firms in the period 1994–1998. Rev. Española Financ. Contab.-Span. J. Financ. Account. 2003, 32, 571–601. [Google Scholar]

- Prado Lorenzo, J.M.; Garcia Sanchez, I.M.; Gallego-Alvarez, I. Characteristics of the board of directors and information in matters of corporate social responsability. Rev. Española Financ. Contab.-Span. J. Financ. Account. 2009, 38, 107–135. [Google Scholar]

- García-Ayuso, M.; Larrinaga, C. Environmental disclosure in Spain: Corporate characteristics and media exposure. Rev. Española Financ. Contab.-Span. J. Financ. Account. 2003, 32, 184–214. [Google Scholar] [CrossRef] [Green Version]

- Guillamon, D.; Benito, B.; Bastida, F. Evaluation of local government debt in Spain. Rev. Española Financ. Contab.-Span. J. Financ. Account. 2011, 40, 251–285. [Google Scholar]

- Abadía, J.M.M.; Macarulla, F.L. Análisis de la información sobre responsabilidad social en las empresas industriales que cotizan en bolsa. Rev. Española Financ. Contab.-Span. J. Financ. Account. 1996, 26, 361–402. [Google Scholar]

- Cárcaba-García, A.I.; Garcia-Garcia, J. Determinants of Internet financial disclosure by local governments. Rev. Española Financ. Contab.-Span. J. Financ. Account. 2008, 37, 63–84. [Google Scholar]

- Bonsón, E.; Escobar, B. Voluntary disclose of financial reporting on Internet. A comparative world-wide analysis. Rev. Española Financ. Contab.-Span. J. Financ. Account. 2004, 33, 1063–1101. [Google Scholar]

- Cañibano, L.; Covarsi, M.G.A.; Sánchez, M.P. La relevancia de los intangibles para la valoración y la gestión de empresas: Revisión de la literatura. Rev. Española Financ. Contab.-Span. J. Financ. Account. 1999, 14, 17–88. [Google Scholar]

- García Osma, B.; Gill de Albornoz, B.; Gisbert, A. Research on Earnings Management. Rev. Española Financ. Contab.-Span. J. Financ. Account. 2005, 34, 1001–1033. [Google Scholar]

- Zafra-Gómez, J.L.; Pedauga, L.E.; Plata-Díaz, A.M.; López-Hernández, A.M. Do local authorities use NPM delivery forms to overcome problems of fiscal stress? Rev. Española Financ. Contab.-Span. J. Financ. Account. 2014, 43, 21–46. [Google Scholar] [CrossRef]

- Lotka, A.J. The frequency distribution of scientific productivity. J. Wash. Acad. Sci. 1926, 16, 317–323. [Google Scholar]

- Chandra, Y. Mapping the evolution of entrepreneurship as a field of research (1990–2013): A scientometric analysis. PLoS ONE 2018, 13, e0190228. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Sabando-Vera, D.; Yonfa-Medranda, M.; Montalván-Burbano, N.; Albors-Garrigos, J.; Parrales-Guerrero, K. Worldwide Research on Open Innovation in SMEs. J. Open Innov. Technol. Mark. Complex. 2022, 8, 20. [Google Scholar] [CrossRef]

- Montalván-Burbano, N.; Velastegui-Montoya, A.; Gurumendi-Noriega, M.; Morante-Carballo, F.; Adami, M. Worldwide research on land use and land cover in the amazon region. Sustainability 2021, 13, 6039. [Google Scholar] [CrossRef]

- García-Lillo, F.; Claver-Cortés, E.; Marco-Lajara, B.; Úbeda-García, M. Identifying the ‘knowledge base’or ‘intellectual structure’ of research on international business, 2000–2015: A citation/co-citation analysis of JIBS. Int. Bus. Revi. 2019, 28, 713–726. [Google Scholar] [CrossRef]

- Modak, N.M.; Lobos, V.; Merigó, J.M.; Gabrys, B.; Lee, J.H. Forty years of computers & chemical engineering: A bibliometric analysis. Comput. Chem. Eng. 2020, 141, 106978. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Year | Volume | Doc. Issue | ∑ Doc | fi | ∑ Issue | Fi | Year | Volume | Doc. Issue | ∑ Doc | fi | ∑ Issue | Fi | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (1) | (2) | (3) | (4) | (5) | ||||||||||||

| 1972 | Vol. 1 | 8 | 7 | 14 | - | - | 29 | 29 | 3 | 3 | 1997 | Vol. 27 | 9 | 7 | 7 | 7 | - | 30 | 765 | 4 | 93 |

| 1973 | Vol. 2 | 13 | 1 | 6 | - | - | 20 | 49 | 3 | 6 | 1998 | Vol. 27 | 9 | 7 | 7 | 7 | - | 30 | 795 | 4 | 97 |

| 1974 | Vol. 3 | 9 | 8 | 3 | 10 | - | 30 | 79 | 4 | 10 | 1999 | Vol. 28 | 8 | 8 | 12 | 8 | 14 | 50 | 845 | 5 | 102 |

| 1975 | Vol. 4 | 6 | 7 | 7 | 9 | - | 29 | 108 | 4 | 14 | 2000 | Vol. 29 | 7 | 7 | 7 | 7 | - | 28 | 873 | 4 | 106 |

| 1976 | Vol. 5 | 5 | 5 | 6 | 9 | - | 25 | 133 | 4 | 18 | 2001 | Vol. 30 | 8 | 8 | 13 | 8 | - | 37 | 910 | 4 | 110 |

| 1977 | Vol. 6 | 6 | 11 | 11 | 18 | - | 46 | 179 | 4 | 22 | 2002 | Vol. 31 | 8 | 8 | 8 | 7 | - | 31 | 941 | 4 | 114 |

| 1978 | Vol. 7 | 8 | 8 | 8 | 7 | - | 31 | 210 | 4 | 26 | 2003 | Vol. 32 | 9 | 7 | 7 | 7 | 12 | 42 | 983 | 5 | 119 |

| 1979 | Vol. 8 | 6 | 4 | 4 | 4 | - | 18 | 228 | 4 | 30 | 2004 | Vol. 33 | 12 | 7 | 7 | 8 | - | 34 | 1017 | 4 | 123 |

| 1980 | Vol. 9 | 13 | 7 | 7 | - | - | 27 | 255 | 3 | 33 | 2005 | Vol. 34 | 7 | 11 | 11 | 11 | - | 40 | 1057 | 4 | 127 |

| 1981 | Vol. 10 | 9 | 5 | 6 | - | - | 20 | 275 | 3 | 36 | 2006 | Vol. 35 | 13 | 8 | 8 | 9 | 8 | 46 | 1103 | 5 | 132 |

| 1982 | Vol. 11 | 8 | 13 | 13 | - | - | 34 | 309 | 3 | 39 | 2007 | Vol. 36 | 8 | 11 | 13 | 10 | - | 42 | 1145 | 4 | 136 |

| 1983 | Vol. 12 | 7 | 10 | 8 | - | - | 25 | 334 | 3 | 42 | 2008 | Vol. 37 | 12 | 11 | 10 | 10 | - | 43 | 1188 | 4 | 140 |

| 1984 | Vol. 13 | 6 | 8 | 5 | - | - | 19 | 353 | 3 | 45 | 2009 | Vol. 38 | 7 | 11 | 9 | 6 | - | 33 | 1221 | 4 | 144 |

| 1985 | Vol. 15 | 10 | 8 | 8 | - | - | 26 | 379 | 3 | 48 | 2010 | Vol. 39 | 8 | 7 | 6 | 5 | - | 26 | 1247 | 4 | 148 |

| 1986 | Vol. 16 | 12 | 7 | 9 | - | - | 28 | 407 | 3 | 51 | 2011 | Vol. 40 | 5 | 5 | 5 | 6 | - | 21 | 1268 | 4 | 152 |

| 1987 | Vol. 17 | 10 | 8 | 11 | - | - | 29 | 436 | 3 | 54 | 2012 | Vol. 41 | 5 | 5 | 5 | 6 | - | 21 | 1289 | 4 | 156 |

| 1988 | Vol. 18 | 5 | 7 | 7 | - | - | 19 | 455 | 3 | 57 | 2013 | Vol. 42 | 5 | 5 | 5 | 5 | - | 20 | 1309 | 4 | 160 |

| 1989 | Vol. 19 | 9 | 8 | 9 | 7 | - | 33 | 488 | 4 | 61 | 2014 | Vol. 43 | 6 | 5 | 5 | 5 | - | 21 | 1330 | 4 | 164 |

| 1990 | Vol. 20 | 6 | 8 | 10 | 6 | - | 30 | 518 | 4 | 65 | 2015 | Vol. 44 | 5 | 6 | 5 | 5 | - | 21 | 1351 | 4 | 168 |

| 1991 | Vol. 21 | 9 | 10 | 12 | 6 | - | 37 | 555 | 4 | 69 | 2016 | Vol. 45 | 4 | 5 | 5 | 6 | - | 20 | 1371 | 4 | 172 |

| 1992 | Vol. 22 | 10 | 8 | 8 | 9 | - | 35 | 590 | 4 | 73 | 2017 | Vol. 46 | 5 | 5 | 5 | 6 | - | 21 | 1392 | 4 | 176 |

| 1993 | Vol. 23 | 8 | 9 | 6 | 11 | - | 34 | 624 | 4 | 77 | 2018 | Vol. 47 | 5 | 5 | 7 | 6 | - | 23 | 1415 | 4 | 180 |

| 1994 | Vol. 24 | 10 | 8 | 8 | 8 | - | 34 | 658 | 4 | 81 | 2019 | Vol. 48 | 5 | 5 | 5 | 7 | - | 22 | 1437 | 4 | 184 |

| 1995 | Vol. 25 | 11 | 10 | 13 | 9 | - | 43 | 701 | 4 | 85 | 2020 | Vol. 49 | 6 | 5 | 5 | 5 | - | 21 | 1458 | 4 | 188 |

| 1996 | Vol. 26 | 9 | 8 | 8 | 9 | - | 34 | 735 | 4 | 89 | |||||||||||

| Year | Cite Score | Best Categorie | Rank | Percentile | Citations Last 3 Years | Documents Last 3 Years | %Cited | SNIP | SJR |

|---|---|---|---|---|---|---|---|---|---|

| 2013 | 0.5 | Economics & Econometrics | 405/510 | 20% | 41 | 82 | 26 | 0.461 | 0.226 |

| 2014 | 0.8 | Economics & Econometrics | 361/520 | 30% | 60 | 79 | 29 | 0.598 | 0.197 |

| 2015 | 0.6 | Economics & Econometrics | 399/530 | 24% | 50 | 79 | 42 | 0.337 | 0.186 |

| 2016 | 0.8 | Finance | 150/225 | 33% | 62 | 77 | 43 | 0.344 | 0.283 |

| 2017 | 0.9 | Finance | 142/244 | 41% | 75 | 80 | 43 | 0.388 | 0.263 |

| 2018 | 0.9 | Finance | 170/260 | 34% | 68 | 79 | 49 | 0.383 | 0.213 |

| 2019 | 1.4 | Finance | 132/270 | 51% | 115 | 80 | 65 | 0.664 | 0.283 |

| Year | ∑ D | ∑ C | C > 100 | 100 ≥ C > 50 | 50 ≥ C > 10 | 10 ≥ C ≥1 | C = 0 | ∑ C/∑ D | H-Index |

|---|---|---|---|---|---|---|---|---|---|

| 1996 | 34 | 143 | 0 | 0 | 1 | 23 | 10 | 4.21 | 6 |

| 1997 | 30 | 71 | 0 | 0 | 2 | 19 | 9 | 2.37 | 5 |

| 1998 | 28 | 145 | 0 | 0 | 5 | 18 | 5 | 5.18 | 7 |

| 1999 | 40 | 126 | 0 | 0 | 4 | 19 | 17 | 3.15 | 5 |

| 2000 | 26 | 78 | 0 | 0 | 2 | 15 | 9 | 3.00 | 6 |

| 2001 | 29 | 65 | 0 | 0 | 1 | 19 | 9 | 2.24 | 5 |

| 2002 | 31 | 91 | 0 | 0 | 0 | 22 | 9 | 2.94 | 7 |

| 2003 | 36 | 223 | 0 | 2 | 1 | 30 | 3 | 6.19 | 7 |

| 2004 | 29 | 115 | 0 | 0 | 4 | 14 | 11 | 3.97 | 5 |

| 2005 | 29 | 145 | 0 | 0 | 4 | 20 | 5 | 5.00 | 7 |

| 2006 | 27 | 83 | 0 | 0 | 2 | 14 | 11 | 3.07 | 6 |

| 2007 | 38 | 94 | 0 | 0 | 2 | 22 | 14 | 2.47 | 6 |

| 2008 | 39 | 161 | 0 | 0 | 4 | 20 | 15 | 4.13 | 7 |

| 2009 | 25 | 147 | 0 | 1 | 2 | 16 | 6 | 5.88 | 6 |

| 2010 | 24 | 84 | 0 | 0 | 2 | 14 | 8 | 3.50 | 6 |

| 2011 | 22 | 167 | 0 | 0 | 6 | 11 | 5 | 7.59 | 7 |

| 2012 | 21 | 85 | 0 | 0 | 3 | 14 | 4 | 4.05 | 5 |

| 2013 | 17 | 65 | 0 | 0 | 3 | 10 | 4 | 3.82 | 5 |

| 2014 | 20 | 136 | 0 | 0 | 6 | 11 | 3 | 6.80 | 8 |

| 2015 | 20 | 69 | 0 | 0 | 1 | 19 | 0 | 3.45 | 5 |

| 2016 | 19 | 61 | 0 | 0 | 0 | 16 | 3 | 3.21 | 6 |

| 2017 | 20 | 53 | 0 | 0 | 2 | 14 | 4 | 2.65 | 5 |

| 2018 | 19 | 47 | 0 | 0 | 1 | 17 | 1 | 2.47 | 5 |

| 2019 | 21 | 44 | 0 | 0 | 1 | 17 | 3 | 2.10 | 5 |

| 2020 | 29 | 9 | 0 | 0 | 0 | 10 | 19 | 0.31 | 2 |

| 673 | 2507 | 0 | 3 | 59 | 424 | 187 | 3.73 | 17 |

| R. | Journal | Documents | Subject Area | Documents |

|---|---|---|---|---|

| 1 | Revista Espanola De Financiacion Y Contabilidad | 273 | Business, Management and Accounting | 1157 |

| 2 | Revista De Contabilidad Spanish Accounting Review | 84 | Economics, Econometrics and Finance | 863 |

| 3 | Sustainability Switzerland | 41 | Decision Sciences | 93 |

| 4 | Innovar | 30 | Computer Science | 73 |

| 5 | Academia Revista Latinoamericana de Administración | 20 | Energy | 73 |

| 6 | Contaduria Y Administracion | 19 | Arts and Humanities | 69 |

| 7 | Capital Intangible | 18 | Agricultural and Biological Sciences | 35 |

| 8 | Corporate Social Responsibility & Environmental Manag. | 17 | Biochemistry, Genetics and Molecular Biology | 5 |

| 9 | Journal Of Business Ethics | 17 | Earth and Planetary Sciences | 4 |

| 10 | European Accounting Review | 15 | Chemistry | 2 |

| R | Title | Author/s | Year | Age | 1996–2000 | 2001–2005 | 2006–2010 | 2011–2015 | 2016–2020 | ∑C | ∆ |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | Social and enviromental information reporting of big size Spanish pirms in the period 1994–1998 | Archel Domenech, P. | 2003 [32] | 17 | 0 | 0 | 20 | 25 | 22 | 67 | 3.94 |

| 2 | Characteristics of the board of directors and information in matters of corporate social responsability | Prado-Lorenzo, J.M. García Sánchez, I.M. Gallego-Álvarez, I. | 2009 [33] | 11 | 0 | 0 | 3 | 20 | 35 | 58 | 5.27 |

| 3 | Environmental disclosure in Spain: Corporate characteristics and media | García-Ayuso, M. Larrinaga, C. | 2003 [34] | 17 | 0 | 1 | 15 | 16 | 24 | 56 | 3.29 |

| 4 | Evaluation of local government debt in Spain | Guillamón, D. Benito, B. Bastida, F. | 2011 [35] | 9 | 0 | 0 | 0 | 15 | 28 | 43 | 4.78 |

| 5 | Análisis de la información sobre responsabilidad social en las empresas industriales que cotizan en Bolsa | Abadía, J.M.M., Macarulla, F.L | 1996 [36] | 24 | 3 | 5 | 12 | 11 | 15 | 46 | 1.92 |

| 6 | Determinants of Internet financial disclosure by local governments | Cárcaba-García, A. García-García, J. | 2008 [37] | 12 | 0 | 0 | 2 | 12 | 21 | 35 | 2.92 |

| 7 | Voluntary, disclose of financial reporting on internet. A comparative world-wide analysis | Bonsón, E. Escobar-Rodríguez, T. | 2004 [38] | 16 | 0 | 0 | 4 | 13 | 16 | 33 | 2.06 |

| 8 | La relevancia de los intangibles para la valoración y la gestión de empresas: Revisión de la literatura (1) | Cañibano, L. Corvasi, M.G.A. Sánchez, M.P. | 1999 [39] | 21 | 0 | 7 | 7 | 11 | 8 | 33 | 1.57 |

| 9 | Research on earnings management | García-Osma, B. Gill-de-Albornoz, B. Gisbert, A. | 2005 [40] | 15 | 0 | 0 | 5 | 9 | 16 | 30 | 2.00 |

| 10 | Do local authorities use NPM delivery forms to overcome problems of fiscal stress? | Zafra Gómez, J.L. Pedauga, L.E. Plata-Díaz, A.M. López Hernández, A.M. | 2014 [41] | 6 | 0 | 0 | 0 | 2 | 21 | 23 | 3.83 |

| R. | Author Name | Country | Affiliation | SJFA | |||||

|---|---|---|---|---|---|---|---|---|---|

| fi | LA | SA | C | C/fi | h-Index | ||||

| 1 | García-Ayuso, M. (Covarsi) | Universidad de Sevilla | Spain | 12 | 10 | 2 | 82 | 6.83 | 3 |

| 2 | Ruiz-Barbadillo, E. | Universidad de Cádiz | Spain | 11 | 3 | 1 | 46 | 4.18 | 5 |

| 3 | Inchausti, B.G. | Universidad de Valencia | Spain | 9 | 6 | 1 | 36 | 4 | 4 |

| 4 | Iñiguez Sánchez, R. | Universidad de Alicante | Spain | 9 | 5 | 0 | 27 | 3 | 3 |

| 5 | Monterrey Mayoral, J. | Universidad de Extremadura | Spain | 9 | 5 | 1 | 29 | 3.22 | 3 |

| 6 | Ruiz-Cabestre, F.J. | Universidad de Zaragoza | Spain | 9 | 1 | 0 | 12 | 1.33 | 3 |

| 7 | Escobar-Pérez, B. | Universidad de Sevilla | Spain | 8 | 4 | 0 | 49 | 6.13 | 5 |

| 8 | Gandía, J.L. | Universidad de Valencia | Spain | 8 | 1 | 3 | 52 | 6.5 | 5 |

| 9 | Laffarga, J. | Universidad de Sevilla | Spain | 7 | 0 | 0 | 8 | 1.14 | 1 |

| 10 | Larrinaga, C. | Universidad de Burgos | Spain | 7 | 1 | 3 | 94 | 13.4 | 5 |

| Year | Authors Number | ƩDocuments | ƩAuthorship | ƩDoc.Co | IC | DC | |||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | 5 | +5 | ||||||

| 1996 | 15 | 11 | 5 | 2 | 0 | 1 | 34 | 66 | 19 | 1.94 | 0.56 |

| 1997 | 13 | 8 | 8 | 2 | 0 | 0 | 31 | 61 | 18 | 1.97 | 0.58 |

| 1998 | 13 | 10 | 1 | 3 | 0 | 0 | 27 | 48 | 14 | 1.78 | 0.52 |

| 1999 | 13 | 13 | 11 | 2 | 1 | 0 | 40 | 85 | 27 | 2.13 | 0.68 |

| 2000 | 9 | 12 | 5 | 0 | 1 | 0 | 27 | 53 | 18 | 1.96 | 0.67 |

| 2001 | 8 | 16 | 4 | 1 | 0 | 0 | 29 | 56 | 21 | 1.93 | 0.72 |

| 2002 | 11 | 16 | 5 | 0 | 0 | 0 | 32 | 58 | 21 | 1.81 | 0.66 |

| 2003 | 12 | 12 | 10 | 2 | 0 | 0 | 36 | 74 | 24 | 2.06 | 0.67 |

| 2004 | 8 | 11 | 7 | 0 | 2 | 0 | 28 | 61 | 20 | 2.18 | 0.71 |

| 2005 | 4 | 14 | 10 | 1 | 1 | 0 | 30 | 71 | 26 | 2.37 | 0.87 |

| 2006 | 5 | 17 | 5 | 1 | 0 | 0 | 28 | 58 | 23 | 2.07 | 0.82 |

| 2007 | 17 | 13 | 7 | 1 | 0 | 0 | 38 | 68 | 22 | 1.79 | 0.58 |

| 2008 | 20 | 9 | 10 | 1 | 0 | 0 | 40 | 72 | 20 | 1.80 | 0.50 |

| 2009 | 3 | 4 | 14 | 3 | 0 | 0 | 24 | 65 | 21 | 2.71 | 0.88 |

| 2010 | 2 | 8 | 9 | 1 | 2 | 0 | 22 | 59 | 20 | 2.68 | 0.91 |

| 2011 | 1 | 8 | 10 | 3 | 0 | 0 | 22 | 69 | 21 | 2.68 | 0.95 |

| 2012 | 1 | 7 | 11 | 1 | 1 | 0 | 21 | 57 | 20 | 2.71 | 0.95 |

| 2013 | 4 | 1 | 11 | 1 | 0 | 0 | 17 | 43 | 13 | 2.53 | 0.76 |

| 2014 | 2 | 8 | 7 | 2 | 0 | 1 | 20 | 53 | 18 | 2.65 | 0.90 |

| 2015 | 3 | 10 | 7 | 0 | 0 | 0 | 20 | 44 | 17 | 2.20 | 0.85 |

| 2016 | 2 | 4 | 12 | 1 | 0 | 0 | 19 | 50 | 17 | 2.63 | 0.89 |

| 2017 | 1 | 8 | 9 | 0 | 1 | 0 | 19 | 49 | 18 | 2.58 | 0.95 |

| 2018 | 1 | 8 | 4 | 5 | 1 | 0 | 19 | 54 | 18 | 2.84 | 0.95 |

| 2019 | 4 | 5 | 11 | 1 | 0 | 0 | 21 | 51 | 17 | 2.43 | 0.81 |

| 2020 | 6 | 6 | 12 | 5 | 0 | 0 | 29 | 74 | 23 | 2.55 | 0.79 |

| 673 | 1489 | 496 | Ʃ = 2.21 | Ʃ = 0.74 | |||||||

| R. | Institution | Country | General (96–20) | 96–00 | 01–05 | 06–10 | 11–15 | 16–20 | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| ∑fi | C | C/∑fi | h | fi | C | C/fi | fi | C | C/fi | fi | C | C/fi | fi | C | C/fi | fi | C | C/fi | |||

| 1 | Univ. Valencia | Spain | 100 | 381 | 3.81 | 9 | 30 | 113 | 3.8 | 30 | 81 | 2.7 | 13 | 79 | 6.1 | 16 | 77 | 4.8 | 11 | 31 | 2.8 |

| 2 | Univ. Zaragoza | Spain | 59 | 238 | 4.03 | 7 | 25 | 93 | 3.7 | 13 | 43 | 3.3 | 7 | 23 | 3.3 | 8 | 55 | 6.9 | 6 | 24 | 4 |

| 3 | Univ. Sevilla | Spain | 49 | 309 | 6.31 | 10 | 19 | 107 | 5.6 | 16 | 114 | 7.1 | 8 | 46 | 5.8 | 3 | 22 | 7.3 | 3 | 20 | 6.7 |

| 4 | Univ. Oviedo | Spain | 36 | 187 | 5.19 | 8 | 9 | 47 | 5.2 | 8 | 38 | 4.8 | 9 | 57 | 6.3 | 7 | 24 | 3.4 | 3 | 21 | 7 |

| 5 | Univ. Alicante | Spain | 32 | 115 | 3.59 | 6 | 8 | 34 | 4.3 | 9 | 31 | 3.4 | 8 | 30 | 3.8 | 4 | 13 | 3.3 | 3 | 7 | 2.3 |

| 6 | Univ. Cádiz | Spain | 26 | 95 | 3.65 | 6 | 6 | 31 | 5.2 | 7 | 26 | 3.7 | 4 | 8 | 2 | 6 | 24 | 4 | 3 | 6 | 2 |

| 7 | Univ. Murcia | Spain | 24 | 147 | 6.13 | 6 | 2 | 7 | 3.5 | 10 | 52 | 5.2 | 6 | 24 | 4 | 2 | 56 | 28 | 4 | 8 | 2 |

| 8 | Univ. Autónoma Madrid | Spain | 24 | 120 | 5.00 | 5 | 8 | 42 | 5.3 | 2 | 39 | 20 | 7 | 15 | 2.1 | 4 | 17 | 4.3 | 3 | 7 | 2.3 |

| 9 | Univ. Pública Navarra | Spain | 23 | 189 | 8.22 | 7 | 6 | 35 | 5.8 | 1 | 71 | 71 | 7 | 34 | 4.9 | 7 | 40 | 5.7 | 2 | 9 | 4.5 |

| 10 | Univ. Extremadura | Spain | 22 | 63 | 2.86 | 5 | 5 | 17 | 3.4 | 7 | 22 | 3.1 | 4 | 15 | 3.8 | 2 | 7 | 3.5 | 4 | 2 | 0.5 |

| R. | Country | General | 96–00 | 01–05 | 06–10 | 11–15 | 16–20 | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| ∑fi | C | C/∑fi | h | fi | C | C/fi | fi | C | C/fi | fi | C | C/fi | fi | C | C/fi | fi | C | C/fi | ||

| 1 | Spain | 594 | 2587 | 4.36 | 17 | 157 | 577 | 3.68 | 146 | 668 | 4.58 | 116 | 532 | 4.59 | 91 | 557 | 6.12 | 84 | 253 | 3.01 |

| 2 | USA | 15 | 58 | 3.87 | 4 | 3 | 4 | 1.33 | 4 | 6 | 1.50 | 2 | 24 | 12.00 | 3 | 21 | 7.00 | 1 | 3 | 3.00 |

| 3 | Portugal | 13 | 58 | 4.46 | 5 | 0 | 0 | 0.00 | 0 | 0 | 0.00 | 2 | 10 | 5.00 | 5 | 38 | 7.60 | 6 | 10 | 1.67 |

| 4 | UK | 11 | 64 | 5.82 | 5 | 3 | 33 | 11.00 | 1 | 6 | 6.00 | 1 | 3 | 3.00 | 4 | 15 | 3.75 | 2 | 7 | 3.50 |

| 5 | South Korea | 8 | 29 | 3.63 | 3 | 0 | 0 | 0.00 | 0 | 0 | 0.00 | 0 | 0 | 0.00 | 1 | 7 | 7.00 | 7 | 22 | 3.14 |

| 6 | Italy | 6 | 20 | 3.33 | 3 | 0 | 0 | 0.00 | 0 | 0 | 0.00 | 1 | 0 | 0.00 | 2 | 0 | 0.00 | 3 | 20 | 6.67 |

| 7 | Australia | 5 | 24 | 4.80 | 3 | 1 | 4 | 4.00 | 0 | 0 | 0.00 | 0 | 0 | 0.00 | 0 | 0 | 0.00 | 4 | 20 | 5.00 |

| 8 | Argentina | 4 | 3 | 0.75 | 1 | 0 | 0 | 0.00 | 1 | 0 | 0.00 | 2 | 1 | 0.50 | 1 | 2 | 2.00 | 0 | 0 | 0.00 |

| 9 | Austria | 4 | 42 | 10.50 | 2 | 0 | 0 | 0.00 | 1 | 0 | 0.00 | 3 | 42 | 14.00 | 0 | 0 | 0.00 | 0 | 0 | 0.00 |

| 10 | Mexico | 4 | 6 | 1.50 | 2 | 0 | 0 | 0.00 | 0 | 0 | 0.00 | 2 | 4 | 2.00 | 1 | 0 | 0.00 | 1 | 2 | 2.00 |

| R. | Author | Documents | University | Documents | Country | Documents |

|---|---|---|---|---|---|---|

| 1 | García-Sánchez, I.M. | 34 | Univ. Valencia | 145 | Spain | 1214 |

| 2 | Cuadrado-Ballesteros, B. | 16 | Univ. Sevilla | 84 | Portugal | 71 |

| 3 | Rodríguez-Domínguez, L. | 15 | Univ. Zaragoza | 83 | UK | 61 |

| 4 | Gallego-Álvarez, L. | 14 | Univ. Salamanca | 75 | USA | 51 |

| 5 | García-Meca, E. | 12 | Unv. Granada | 69 | Colombia | 42 |

| 6 | Martínez-Ferrero, J. | 11 | Univ. Murcia | 60 | Italy | 42 |

| 7 | Rodrígues, L.L. | 11 | Univ. Extremadura | 56 | Brazil | 38 |

| 8 | Gallardo-Vázquez, S. | 10 | Univ. Polit. Cartegena | 56 | Chile | 33 |

| 9 | Pucheta-Martínez. M.C. | 10 | Univ. Oviedo | 42 | Mexico | 30 |

| 10 | Bravo, F. | 9 | Univ. Pablo Olavide | 40 | Australia | 28 |

| R. | Journal | References | Area (Percentil CiteScore) | |||||

|---|---|---|---|---|---|---|---|---|

| Ʃ | 96–00 | 01–05 | 06–10 | 11–15 | 16–20 | |||

| 1 | Journal of Finance | 960 | 197 | 178 | 211 | 189 | 185 | Business, Management and Accounting (99th) Economics, Econometrics and Finance (99th) |

| 2 | Accounting Review | 713 | 158 | 117 | 115 | 141 | 182 | Economics, Econometrics and Finance (96th) Business, Management and Accounting (95th) |

| 3 | Journal of Financial Economics | 704 | 102 | 121 | 150 | 150 | 181 | Business, Management and Accounting (99th) Economics, Econometrics and Finance (97th) |

| 4 | Revista Española De Financiación Y Contabilidad | 627 | 110 | 107 | 129 | 132 | 149 | Economics, Econometrics and Finance (54th) Business, Management and Accounting (42th) |

| 5 | Journal of Accounting Research | 612 | 145 | 129 | 106 | 105 | 127 | Business, Management and Accounting (96th) Economics, Econometrics and Finance (96th) |

| 6 | Journal of Accounting And Economics | 561 | 92 | 120 | 99 | 110 | 140 | Business, Management and Accounting (97th) Economics, Econometrics and Finance (96th) |

| 7 | Accounting Organizations And Society | 441 | 83 | 89 | 68 | 67 | 134 | Social Sciences (97th) Business, Management and Accounting (93th) Decision Sciences (83th) |

| 8 | Journal of Banking And Finance | 389 | 34 | 62 | 68 | 87 | 138 | Economics, Econometrics and Finance (86th) |

| 9 | Accounting And Business Research | 263 | 71 | 66 | 44 | 33 | 49 | Economics, Econometrics and Finance (88th) Business, Management and Accounting (85th) |

| 10 | European Accounting Review | 252 | 20 | 40 | 59 | 43 | 90 | Arts and Humanities (99th) Economics, Econometrics and Finance (89th) Business, Management and Accounting (80th) Engineering (Engineering-miscel) (73th) |

| R. | Global (1996–2020) | 1996–2000 | 2001–2005 | |||

|---|---|---|---|---|---|---|

| Keyword | fi | Keyword | fi | Keyword | fi | |

| 1 | Earnings management | 20 | Stock market | 5 | Accounting history | 9 |

| 2 | Corporate governance | 16 | Accounting regulation | 4 | Management accounting | 6 |

| 3 | Accounting history | 15 | Valuation | 4 | Earnings management | 5 |

| 4 | Performance | 13 | Accounting history | 3 | Capital market | 4 |

| 5 | Efficiency | 12 | Arbitrage | 3 | Discretionary accruals | 4 |

| 6 | Stock market | 12 | Discriminant analysis | 3 | Efficiency | 4 |

| 7 | Valuation | 12 | Earnings | 3 | Management control | 4 |

| 8 | Auditing | 11 | Financial ratios | 3 | Performance | 4 |

| 9 | Management accounting | 10 | Term struct, inter, rates | 3 | Accounting choice | 3 |

| 10 | Size | 10 | Volatility | 3 | Auditing | 3 |

| 2006–2010 | 2011–2015 | 2016–2020 | ||||

| Keyword | fi | Keyword | fi | Keyword | fi | |

| 1 | Abnormal returns | 5 | Corporate governance | 5 | Earnings management | 8 |

| 2 | Auditing | 4 | Earnings management | 5 | Audit quality | 4 |

| 3 | Derivatives | 4 | Capital structure | 4 | Board Of directors | 4 |

| 4 | Efficiency | 4 | Spain | 4 | Corporate governance | 4 |

| 5 | Accounting history | 3 | Audit quality | 3 | Financial crisis | 4 |

| 6 | Accounting regulation | 3 | Corp. coc. respons. | 3 | Performance | 4 |

| 7 | Collective bargaining | 3 | Panel data | 3 | Transparency | 4 |

| 8 | Corporate governance | 3 | Performance | 3 | Asset pricing | 3 |

| 9 | Disclosure | 3 | Valuation | 3 | Efficiency | 3 |

| 10 | Size | 3 | Asymmetric information | 2 | M41 | 3 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Álvarez-García, J.; Durán-Sánchez, A.; Montalván-Burbano, N.; del Río-Rama, M.d.l.C. Spanish Journal of Finance and Accounting (SJFA): Mapping of Knowledge over the Last 25 Years. Publications 2023, 11, 11. https://doi.org/10.3390/publications11010011

Álvarez-García J, Durán-Sánchez A, Montalván-Burbano N, del Río-Rama MdlC. Spanish Journal of Finance and Accounting (SJFA): Mapping of Knowledge over the Last 25 Years. Publications. 2023; 11(1):11. https://doi.org/10.3390/publications11010011

Chicago/Turabian StyleÁlvarez-García, José, Amador Durán-Sánchez, Néstor Montalván-Burbano, and María de la Cruz del Río-Rama. 2023. "Spanish Journal of Finance and Accounting (SJFA): Mapping of Knowledge over the Last 25 Years" Publications 11, no. 1: 11. https://doi.org/10.3390/publications11010011