Shareholders in the Driver’s Seat: Unraveling the Impact on Financial Performance in Latvian Fintech Companies

Abstract

:1. Introduction

2. Literature Review and Hypothesis Development

3. Methodology

3.1. Study Design

3.2. Sample Selection and Data Collection

4. Results

4.1. Sample Characteristics and Descriptive Statistics

4.2. Comparative Analysis

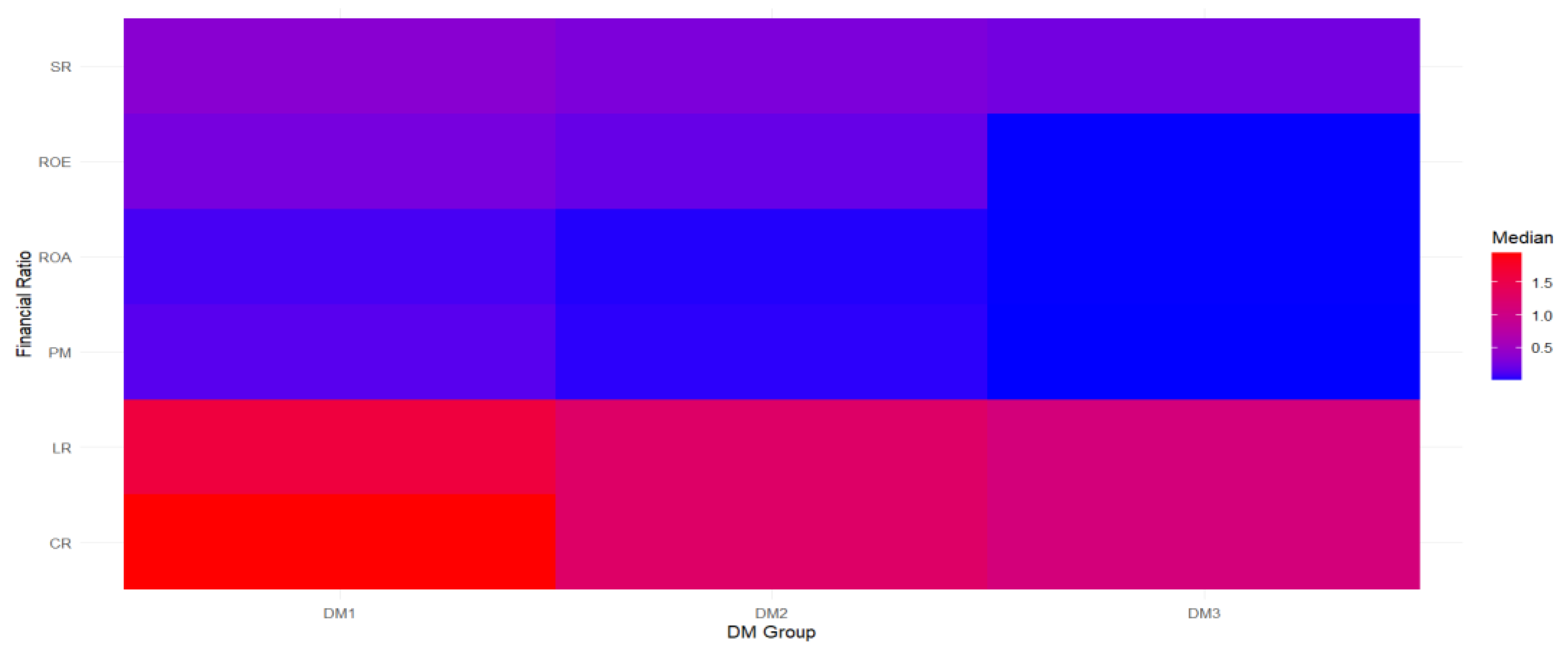

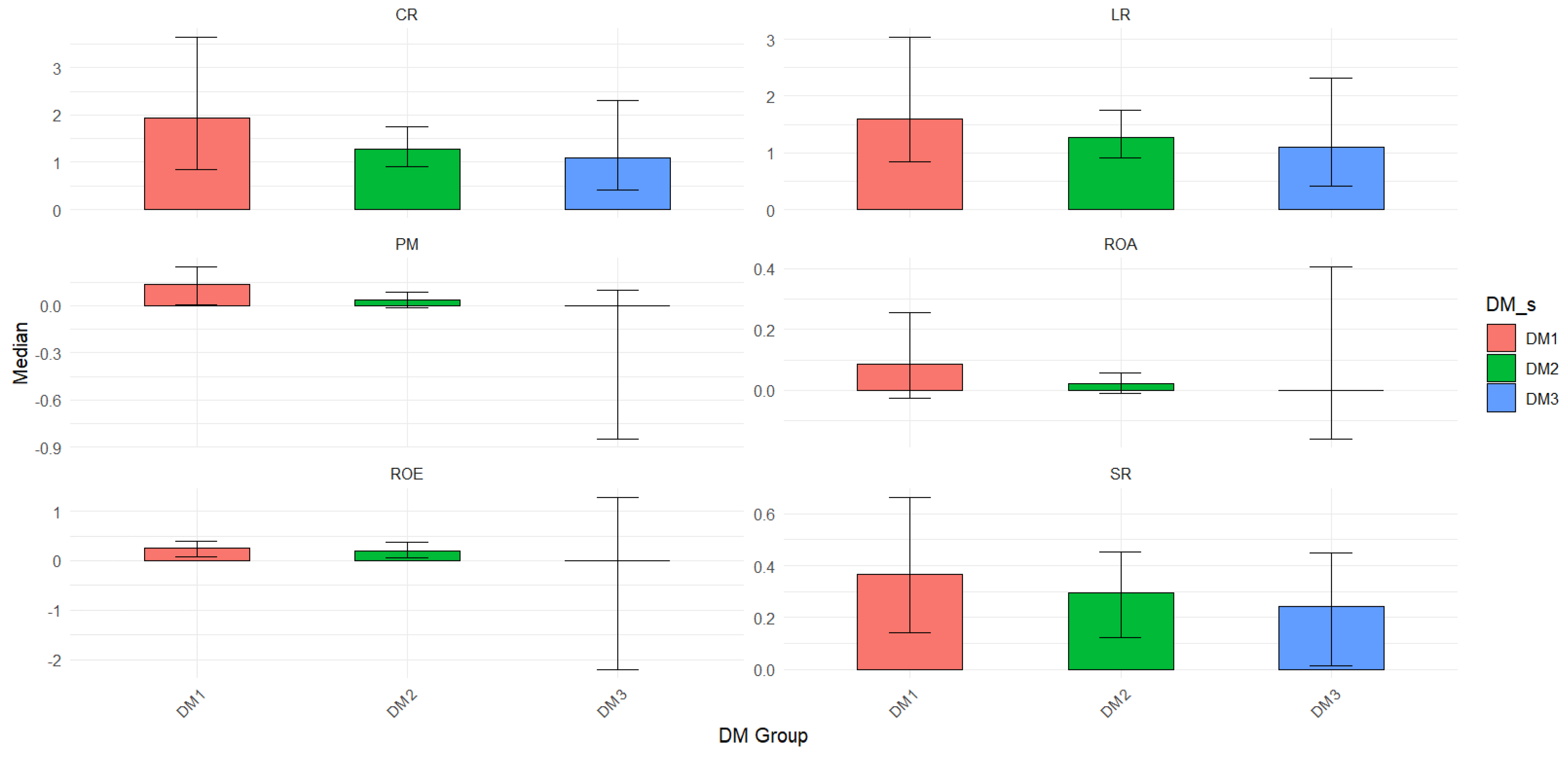

4.3. Visualizing Shareholder Presence and Financial Performance: Exploring Correlations, Metrics, and Distributions

- Profitability: Among the three financial ratios, DM1 consistently outperforms DM2 and DM3 in terms of median values. However, it is essential to consider the precision of these estimates. The confidence intervals for DM1 are relatively wider compared to those for DM2, indicating that there is less certainty in estimating the true population values for DM1. In contrast, the narrower confidence intervals for DM2 imply a more precise estimation of its true population values. Furthermore, the confidence intervals for DM3 overlap with both DM1 and DM2. This suggests that, statistically, there may not be significant differences between DM3 and the other two groups in terms of ROA, ROE, and PM.

- Liquidity: The analysis of liquidity measures presents a similar situation as observed for profitability ratios. DM1 exhibits larger median values for both LR and CR, indicating higher levels of liquidity compared to DM2 and DM3. However, similar to previous findings, the confidence intervals for DM1 are relatively wider, implying less precision in estimating the true population values for LR and CR. It is noteworthy that the confidence intervals for DM1 fully overlap with those of DM2 and partly with DM3 for both LR and CR. This statistical overlap indicates that there might not be significant differences in liquidity levels between DM1 and DM2, and there could be some overlap in liquidity with DM3 as well. While DM1 generally shows higher median values, the overlapping confidence intervals suggest that the differences between the groups may not be substantial.

- The analysis of the solvency ratio reiterates the pattern observed in liquidity ratios, where DM1 tends to have higher median values, indicating stronger solvency compared to DM2 and DM3. However, the wider confidence intervals for DM1 suggest caution in interpreting the results, as there is less precision in estimating its true population values.

5. Discussion

6. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

| Variable Name/ Statistics | ROA | ROE | PM | CR | LR | SR |

|---|---|---|---|---|---|---|

| Group DM1 | ||||||

| Statistics | 0.431 | 0.486 | 0.433 | 0.428 | 0.404 | 0.402 |

| p value | <0.001 | <0.001 | <0.001 | <0.001 | <0.001 | <0.001 |

| Group DM2 | ||||||

| Statistics | 0.200 | 0.148 | 0.283 | 0.355 | 0.355 | 0.241 |

| p value | <0.001 | <0.001 | <0.001 | <0.001 | <0.001 | <0.001 |

| Group DM3 | ||||||

| Statistics | 0.522 | 0.456 | 0.539 | 0.585 | 0.585 | 0.418 |

| p value | <0.001 | <0.001 | <0.001 | <0.001 | <0.001 | <0.001 |

| 1 | In this study, we adopt the Orbis classification of directors and managers, encompassing board members, committee participants, and executives. |

| 2 | Even though very high levels of liquidity can be interpreted as inefficient use of financial resources, we do not consider the liquidity in any of the companies in the dataset as being excessive. |

References

- Adams, John C., Darren K. Hayunga, Sattar Mansi, David M. Reeb, and Vincenzo Verardi. 2018. Identifying and Treating Outliers in Finance. Financial Management 48: 345–84. [Google Scholar] [CrossRef]

- Affes, Wajdi, and Anis Jarboui. 2023. The Impact of Corporate Governance on Financial Performance: A Cross-Sector Study. International Journal of Disclosure and Governance 20: 374–94. [Google Scholar] [CrossRef]

- Al-Matari, Ebrahim Mohammed, Mahfoudh Hussein Mgammal, Mushari Hamdan Alosaimi, Talal Fawzi Alruwaili, and Sultan Al-Bogami. 2022. Fintech, Board of Directors and Corporate Performance in Saudi Arabia Financial Sector: Empirical Study. Sustainability 14: 10750. [Google Scholar] [CrossRef]

- Bachiller, Patricia, Maria Cleofe Giorgino, and Sergio Paternostro. 2015. Influence of Board of Directors on Firm Performance: Analysis of Family and Non-Family Firms. International Journal of Disclosure and Governance 12: 230–53. [Google Scholar] [CrossRef]

- Bank of Latvia. 2020. FINTECH Glossary. Available online: https://www.bank.lv/en/publications-r/other-publications/fintech-glossary (accessed on 7 November 2023).

- Barnes, Paul. 1982. Methodological implications of non-normally distributed financial ratios. Journal of Business Finance and Accounting 9: 51–62. Available online: https://www.academia.edu/10486283/METHODOLOGICAL_IMPLICATIONS_OF_NON_NORMALLY_DISTRIBUTED_FINANCIAL_RATIOS (accessed on 14 August 2023). [CrossRef]

- Berle, Adolf Augustus, and Gardiner C. Means. 1991. The Modern Corporation and Private Property. New Brunswick: Transaction Publishers. [Google Scholar]

- Bonazzi, Livia, and Sardar M. N. Islam. 2007. Agency Theory and Corporate Governance: A Study of the Effectiveness of Board in Their Monitoring of the CEO. Journal of Modelling in Management 2: 7–23. [Google Scholar] [CrossRef]

- Brickley, James A., Jeffrey L. Coles, and Gregg Jarrell. 1997. Leadership Structure: Separating the CEO and Chairman of the Board. Journal of Corporate Finance 3: 189–220. [Google Scholar] [CrossRef]

- Caselli, Stefano, Stefano Gatti, Carlo Chiarella, Gimede Gigante, and Giulia Negri. 2023. Do Shareholders Really Matter for Firm Performance? Evidence from the Ownership Characteristics of Italian Listed Companies. International Review of Financial Analysis 86: 102544. [Google Scholar] [CrossRef]

- Chiavarini, Lorenzo, Renat Lokomet, Pierre Bonvalot, and Gayane Chagharyan. 2023. Latvian Fintech Landscape List|Dealroom. Co. Available online: https://app.dealroom.co/lists/19839 (accessed on 22 July 2023).

- Chrisman, James J. 2019. Stewardship Theory: Realism, Relevance, and Family Firm Governance. Entrepreneurship Theory and Practice 43: 1051–66. [Google Scholar] [CrossRef]

- Davis, James H., F. David Schoorman, and Lex Donaldson. 1997. Toward a Stewardship Theory of Management. The Academy of Management Review 22: 20–47. [Google Scholar] [CrossRef]

- Donaldson, Lex, and James H. Davis. 1991. Stewardship Theory or Agency Theory: CEO Governance and Shareholder Returns. Australian Journal of Management 16: 49–64. [Google Scholar] [CrossRef]

- Dospinescu, Octavian, Nicoleta Dospinescu, and Daniela-Tatiana Agheorghiesei. 2021. FinTech Services and Factors Determining the Expected Benefits of Users: Evidence in Romania for Millennials and Generation Z. E&M Economics and Management 24: 101–18. [Google Scholar] [CrossRef]

- Fama, Eugene F. 1980. Agency Problems and the Theory of the Firm. Journal of Political Economy 88: 288–307. [Google Scholar] [CrossRef]

- Fama, Eugene F., and Michael C. Jensen. 1983. Separation of Ownership and Control. The Journal of Law and Economics 26: 301–25. [Google Scholar] [CrossRef]

- Grima, Simon, Ramona Rupeika-Apoga, Murat Kizilkaya, Inna Romānova, Rebecca Dalli Gonzi, and Mihajlo Jakovljevic. 2021. A Proactive Approach to Identify the Exposure Risk to COVID-19: Validation of the Pandemic Risk Exposure Measurement (PREM) Model Using Real-World Data. Risk Management and Healthcare Policy 14: 4775–87. [Google Scholar] [CrossRef]

- Hoi, Chun-Keung, and Ashok Robin. 2010. Agency Conflicts, Controlling Owner Proximity, and Firm Value: An Analysis of Dual-Class Firms in the United States. Corporate Governance: An International Review 18: 124–35. [Google Scholar] [CrossRef]

- Hollander, Myles, Douglas A. Wolfe, and Eric Chicken. 2014. Nonparametric Statistical Methods, 3rd ed. Hoboken: John Wiley & Sons, Inc. [Google Scholar]

- Jain, Ruchika, Satinder Kumar, Kiran Sood, Simon Grima, and Ramona Rupeika-Apoga. 2023. A Systematic Literature Review of the Risk Landscape in Fintech. Risks 11: 36. [Google Scholar] [CrossRef]

- Jensen, Michael C., and William H. Meckling. 1976. Theory of the Firm: Managerial Behavior, Agency Costs and Ownership Structure. Journal of Financial Economics 3: 305–60. [Google Scholar] [CrossRef]

- Katalkina, Oksana, and Svetlana Saksonova. 2022. Crowdfunding Cross-Border Business Financing Practice: The Evidence from the Baltic States. Lecture Notes in Networks and Systems 410 LNNS. Cham: Springer, pp. 472–81. [Google Scholar] [CrossRef]

- Marx, Axel. 2016. Qualitative Comparative Analysis (QCA). Oxford: Oxford University Press. [Google Scholar] [CrossRef]

- Menyah, Kojo. 2013. Stewardship Theory. In Encyclopedia of Corporate Social Responsibility. Edited by Samuel O. Idowu, Nicholas Capaldi, Liangrong Zu and Ananda Das Gupta. Berlin/Heidelberg: Springer, pp. 2322–29. [Google Scholar] [CrossRef]

- Najaf, Khakan, Philip Sinnadurai, K. S. Devi, and Mohamed M. Dhiaf. 2022. Does Electronic Economics Matter to Financial Technology Firms? Electronic Commerce Research, 1–34. [Google Scholar] [CrossRef]

- Neralla, Narsa Goud. 2022. Can Corporate Governance Structure Effect on Corporate Performance: An Empirical Investigation from Indian Companies. International Journal of Disclosure and Governance 19: 282–300. [Google Scholar] [CrossRef]

- Ramachandran, Kandethody M., and Chris P. Tsokos. 2021. Chapter 13—Empirical Methods. In Mathematical Statistics with Applications in R, 3rd ed. Edited by Kandethody M. Ramachandran and Chris P. Tsokos. New York: Academic Press, pp. 531–68. [Google Scholar] [CrossRef]

- Raschka, Sebastian. 2013. Instant Heat Maps in R How-To. Birmingham: Packt Publishing. [Google Scholar]

- Rupeika-Apoga, Ramona, and Irina Solovjova. 2016. Profiles of SMEs as Borrowers: Case of Latvia. Contemporary Studies in Economic and Financial Analysis 98: 63–76. [Google Scholar] [CrossRef]

- Rupeika-Apoga, Ramona, and Stefan Wendt. 2022. FinTech Development and Regulatory Scrutiny: A Contradiction? The Case of Latvia. Risks 10: 167. [Google Scholar] [CrossRef]

- Rupeika-Apoga, Ramona, Emīls Dārziņš, Deniss Filipovs, and Stefan Wendt. 2023. Competitors and Partners at the Same Time: On the Role of Fintech Companies in the Latvian Financial Market. In The Fintech Disruption. Edited by Thomas Walker, Elaheh Nikbakht and Maher Kooli. Palgrave Studies Financial Services Technology. Cham: Springer International Publishing, pp. 115–38. [Google Scholar] [CrossRef]

- Sahid, Abdelkebir, Yassine Maleh, Shahram Atashi Asemanjerdi, and Pedro Antonio Martín-Cervantes. 2023. A Bibliometric Analysis of the FinTech Agility Literature: Evolution and Review. International Journal of Financial Studies 11: 123. [Google Scholar] [CrossRef]

- Saksonova, Svetlana, and Tatiana Papiashvili. 2021. Micro and Small Businesses Access to Finance and Financial Literacy of Their Owners: Evidence from Latvia, Estonia and Georgia. Lecture Notes in Networks and Systems 195: 667–77. [Google Scholar] [CrossRef]

- Sharma, Sachin Kumar, P. Vigneswara Ilavarasan, and Stan Karanasios. 2023. Small Businesses and FinTech: A Systematic Review and Future Directions. Electronic Commerce Research, 1–41. [Google Scholar] [CrossRef]

- Smith, Wendy K., Andy Binns, and Michael L. Tushman. 2010. Complex Business Models: Managing Strategic Paradoxes Simultaneously. Long Range Planning, Business Models 43: 448–61. [Google Scholar] [CrossRef]

- So, Jacky. 2006. Some Empirical Evidence On the Outliers and the Non-Normal Distribution of Financial Ratios. Journal of Business Finance & Accounting 14: 483–96. [Google Scholar] [CrossRef]

- Stano, Miron. 1975. Executive Ownership Interests and Corporate Performance. Southern Economic Journal 42: 272–78. [Google Scholar] [CrossRef]

- Startin. 2023. Latvian Startup Database. Latvian Startup Association Startin. LV. Available online: https://startin.lv/startup-database/ (accessed on 27 July 2023).

- Tzanaki, Anna, Liudmila Alekseeva, and José Azar. 2023. Common Ownership in Fintech Markets. New Working Paper Series, No. 329; Chicago, IL: University of Chicago Booth School of Business, Stigler Center for the Study of the Economy and the State. [Google Scholar]

- Zaidi, Syeda Hina, and Ramona Rupeika-Apoga. 2021. Liquidity Synchronization, Its Determinants and Outcomes under Economic Growth Volatility: Evidence from Emerging Asian Economies. Risks 9: 43. [Google Scholar] [CrossRef]

- Zhang, Jichang, Jing Long, and Alexandra Martina Eugenie von Schaewen. 2021. How Does Digital Transformation Improve Organizational Resilience?—Findings from PLS-SEM and fsQCA. Sustainability 13: 11487. [Google Scholar] [CrossRef]

| Variable Name/ Statistics | ROA | ROE | PM | CR | LR | SR |

|---|---|---|---|---|---|---|

| Min. | −5.442 | −3.502 | −20.765 | 0.043 | 0.043 | −10.626 |

| 1st | −0.145 | −0.027 | −0.240 | 0.635 | 0.635 | 0.005 |

| Median | 0.021 | 0.193 | 0.068 | 1.375 | 1.327 | 0.295 |

| 3rd | 0.247 | 0.621 | 0.257 | 4.223 | 4.035 | 0.686 |

| Max. | 1.294 | 3.116 | 0.673 | 23.888 | 20.162 | 0.960 |

| not available | - | - | 6 | 2 | 2 | 2 |

| Variable Name/ Statistics | ROA | ROE | PM | CR | LR | SR |

|---|---|---|---|---|---|---|

| Chi-Square | 1.1785 | 1.5866 | 3.9195 | 1.2924 | 1.0098 | 0.41495 |

| Df | 2 | 2 | 2 | 2 | 2 | 2 |

| Asymp. Sig. | 0.5547 | 0.4524 | 0.1409 | 0.524 | 0.6036 | 0.8126 |

| Variable Name/ Statistics | ROA | ROE | PM | CR | LR | SR |

|---|---|---|---|---|---|---|

| DM1–DM2 | negligible | negligible | 0.194 (small) | negligible | negligible | negligible |

| DM1–DM3 | negligible | 0.222 (small) | 0.333 (medium) | 0.186 (small) | 0.214 (small) | negligible |

| DM2–DM3 | negligible | 0.245 (small) | 0.214 (small) | 0.195 (small) | 0.195 (small) | negligible |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Rupeika-Apoga, R.; Wendt, S.; Geyfman, V. Shareholders in the Driver’s Seat: Unraveling the Impact on Financial Performance in Latvian Fintech Companies. Risks 2024, 12, 54. https://doi.org/10.3390/risks12030054

Rupeika-Apoga R, Wendt S, Geyfman V. Shareholders in the Driver’s Seat: Unraveling the Impact on Financial Performance in Latvian Fintech Companies. Risks. 2024; 12(3):54. https://doi.org/10.3390/risks12030054

Chicago/Turabian StyleRupeika-Apoga, Ramona, Stefan Wendt, and Victoria Geyfman. 2024. "Shareholders in the Driver’s Seat: Unraveling the Impact on Financial Performance in Latvian Fintech Companies" Risks 12, no. 3: 54. https://doi.org/10.3390/risks12030054