A Quantitative Comparison of Mortality Models with Jumps: Pre- and Post-COVID Insights on Insurance Pricing

Abstract

:1. Introduction

2. Mortality Models

2.1. The Lee–Carter Model

2.2. Renshaw and Haberman Model

2.3. Cairns–Blake–Dowd Model

2.4. Jump Effect Models as Extensions to the Lee–Carter Model

2.4.1. with Permanent Jump Effect

2.4.2. with Transitory Jump Effect

2.4.3. with Exponential Transitory Jumps and Renewal Process Effect

3. Results and Discussion

3.1. Model Comparisons

3.1.1. Parameter Estimation Process

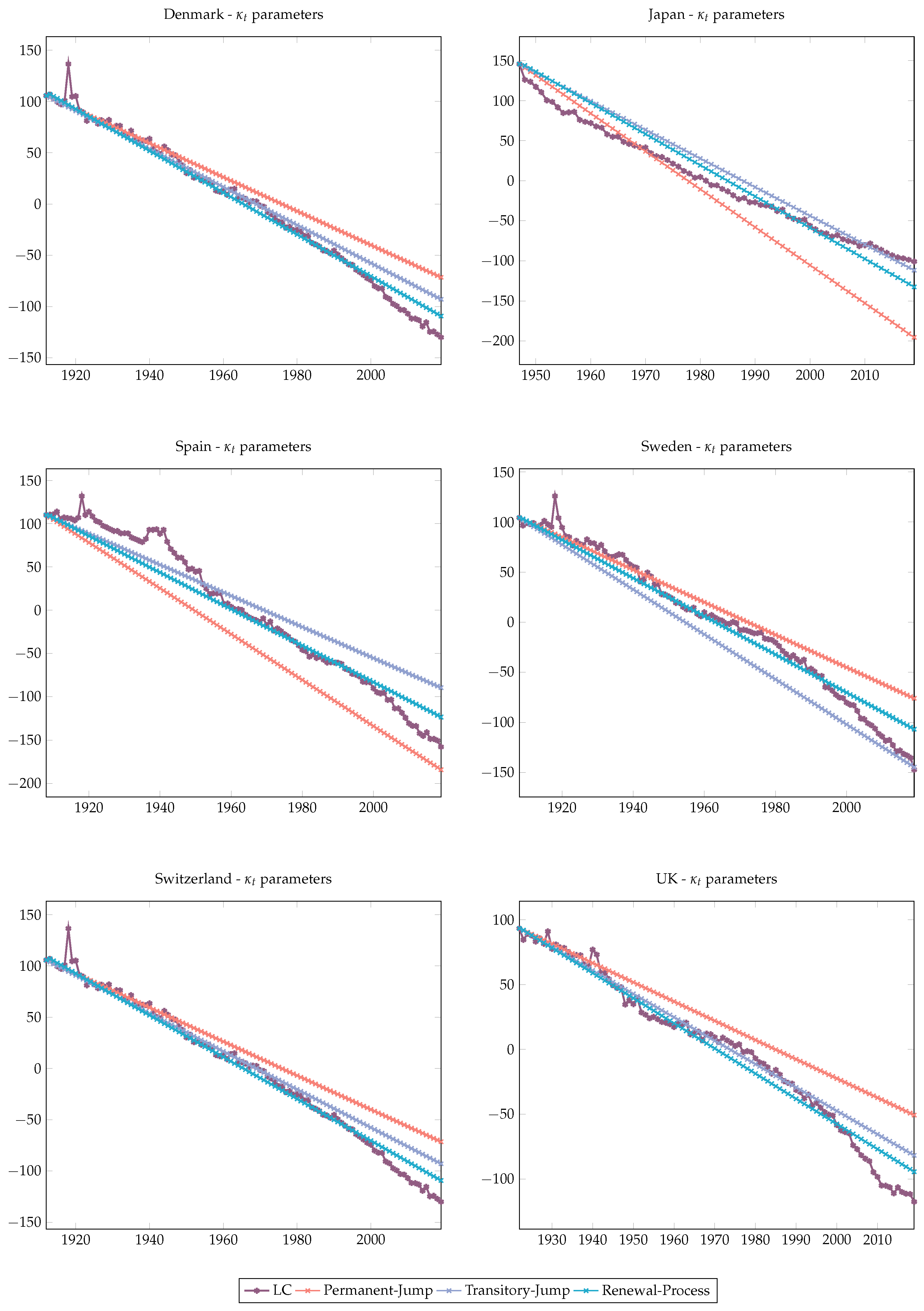

3.1.2. Fitted Parameters

3.1.3. Bayes Information Criterion

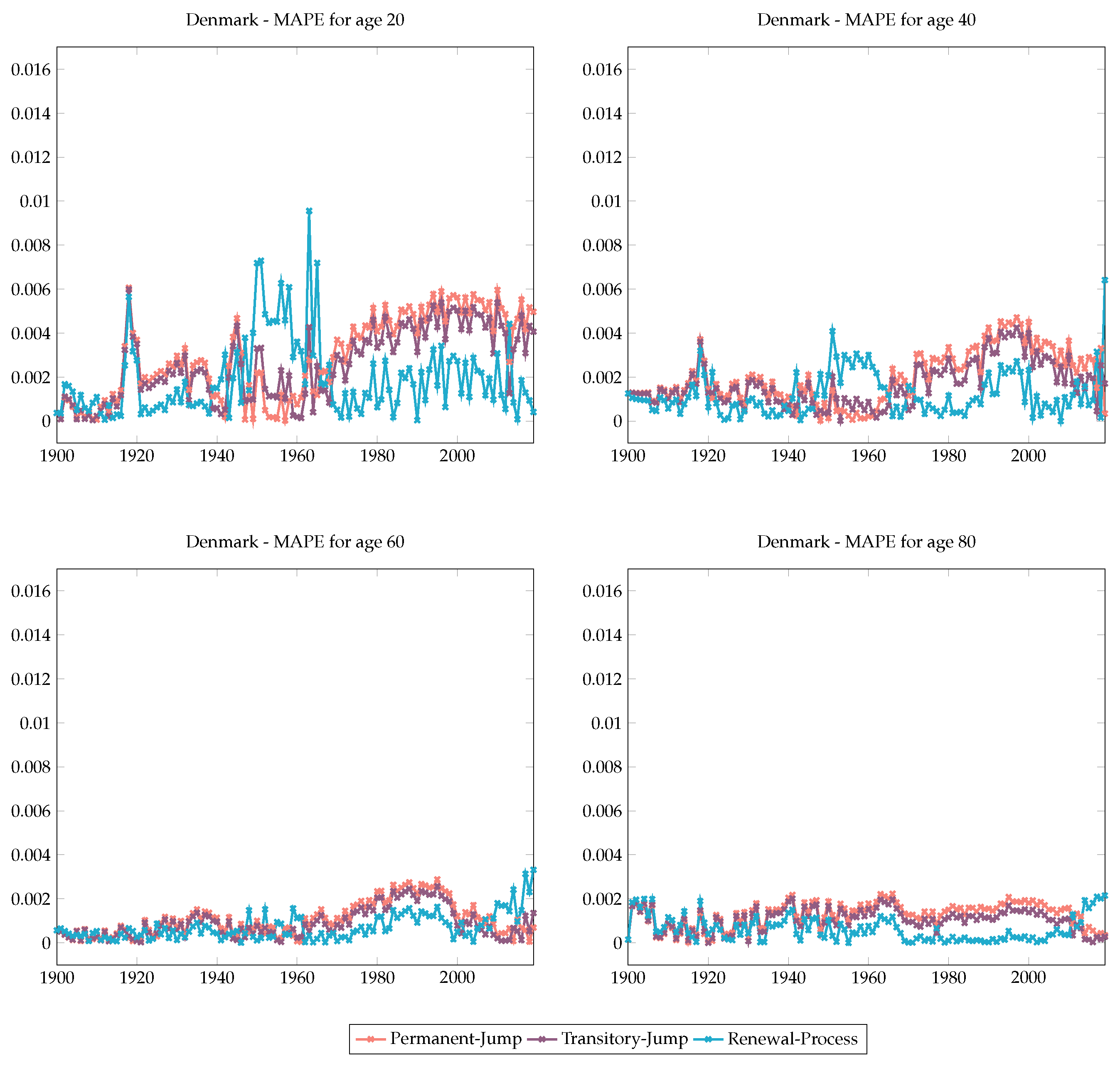

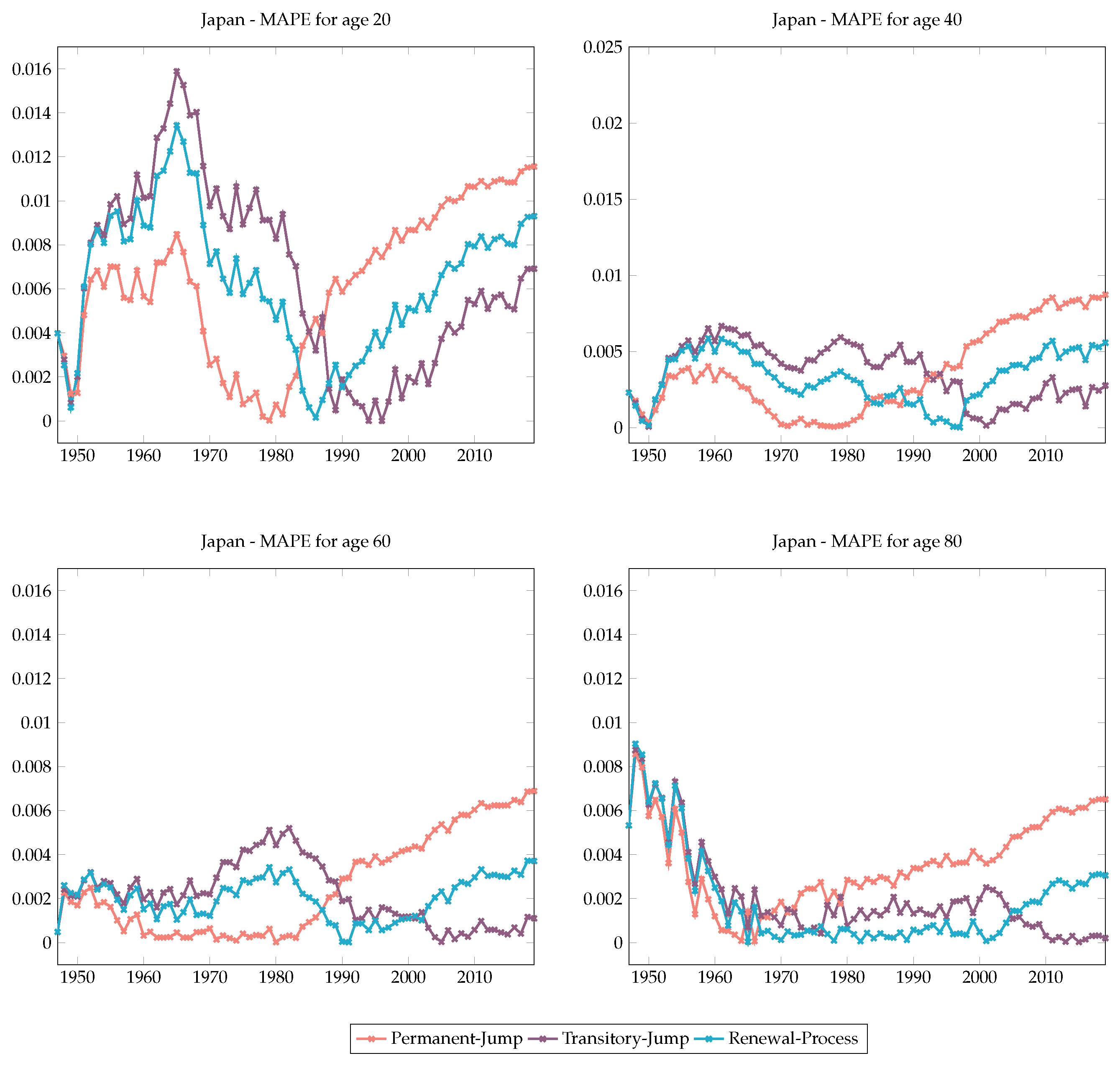

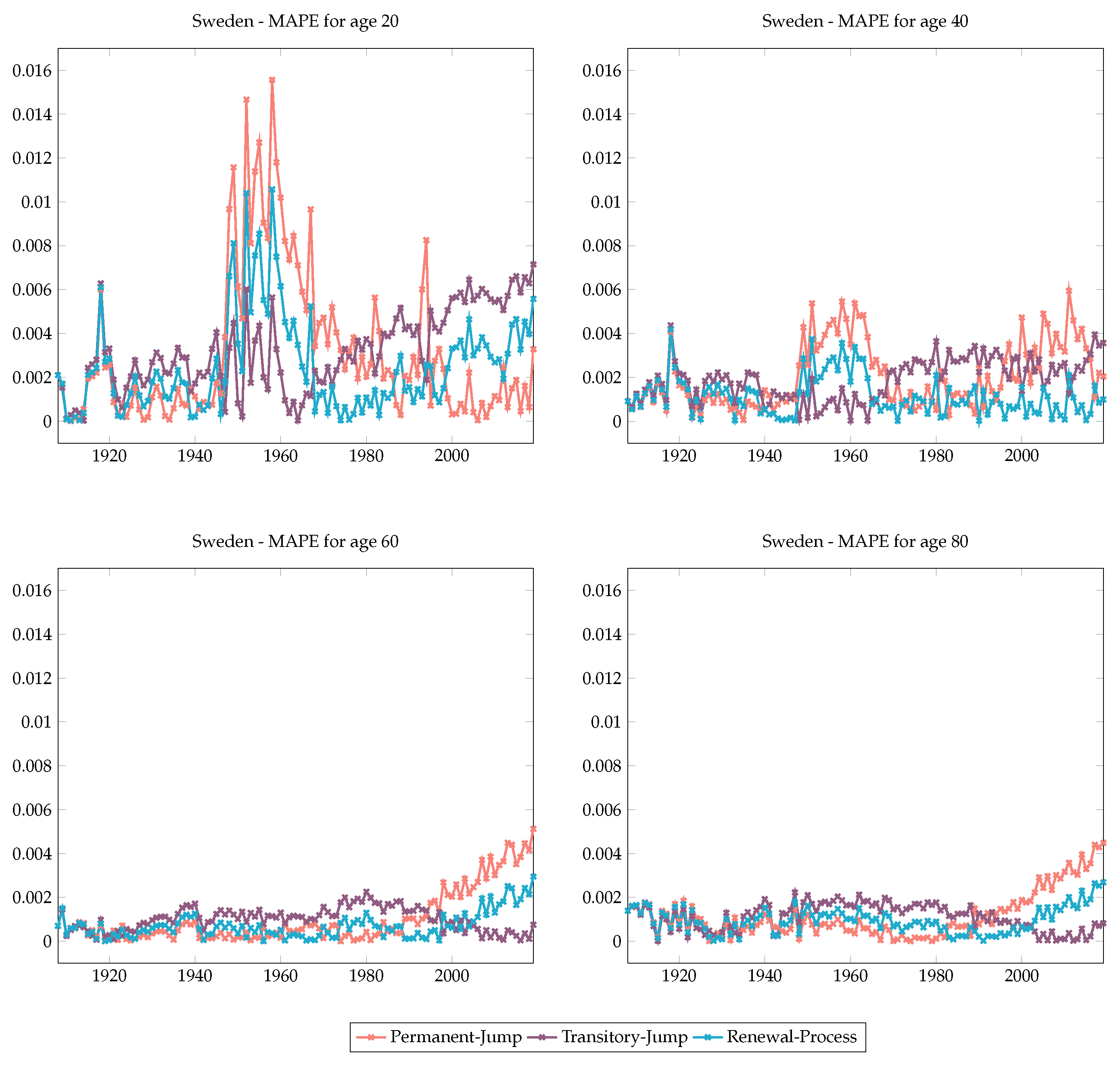

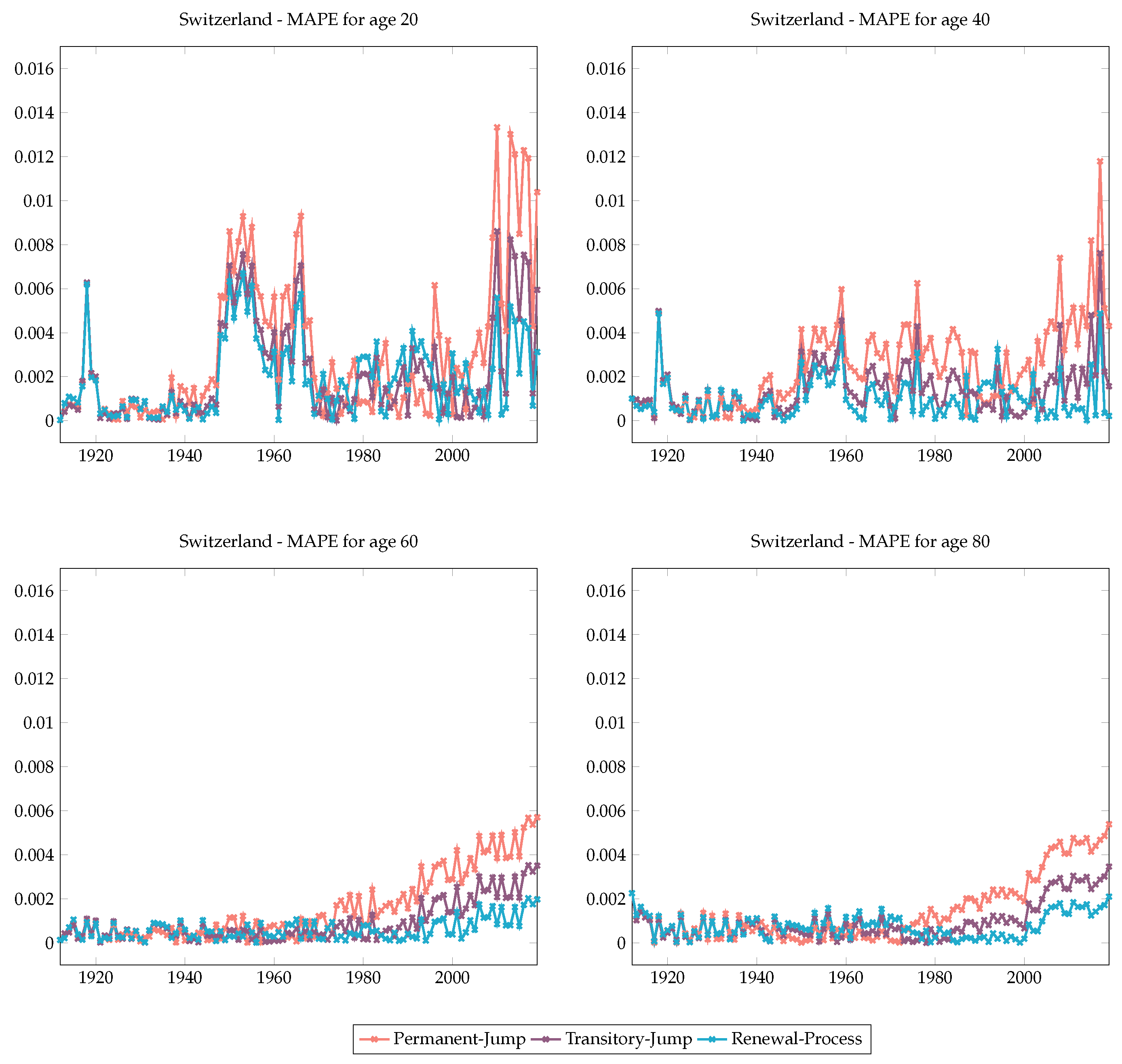

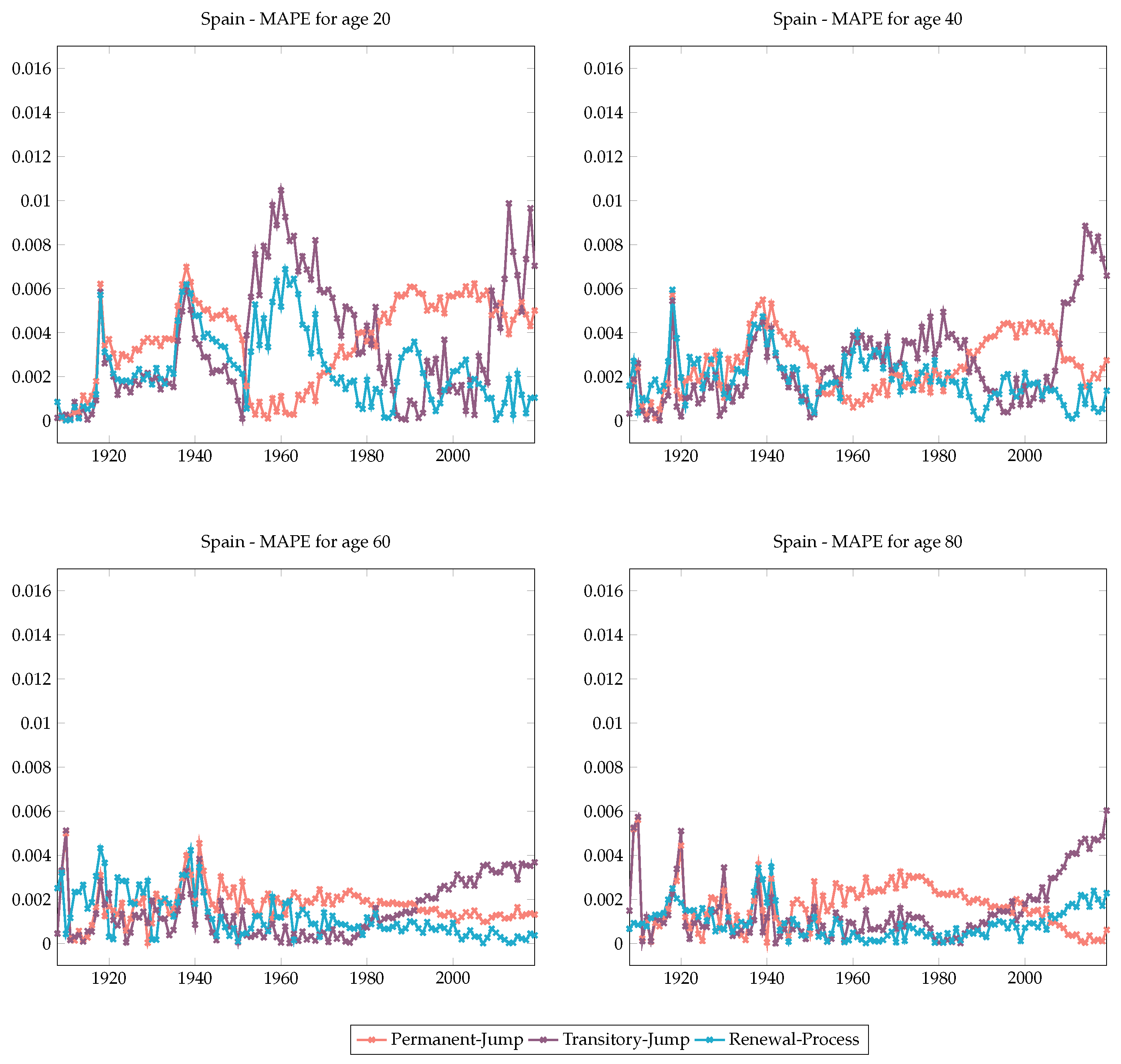

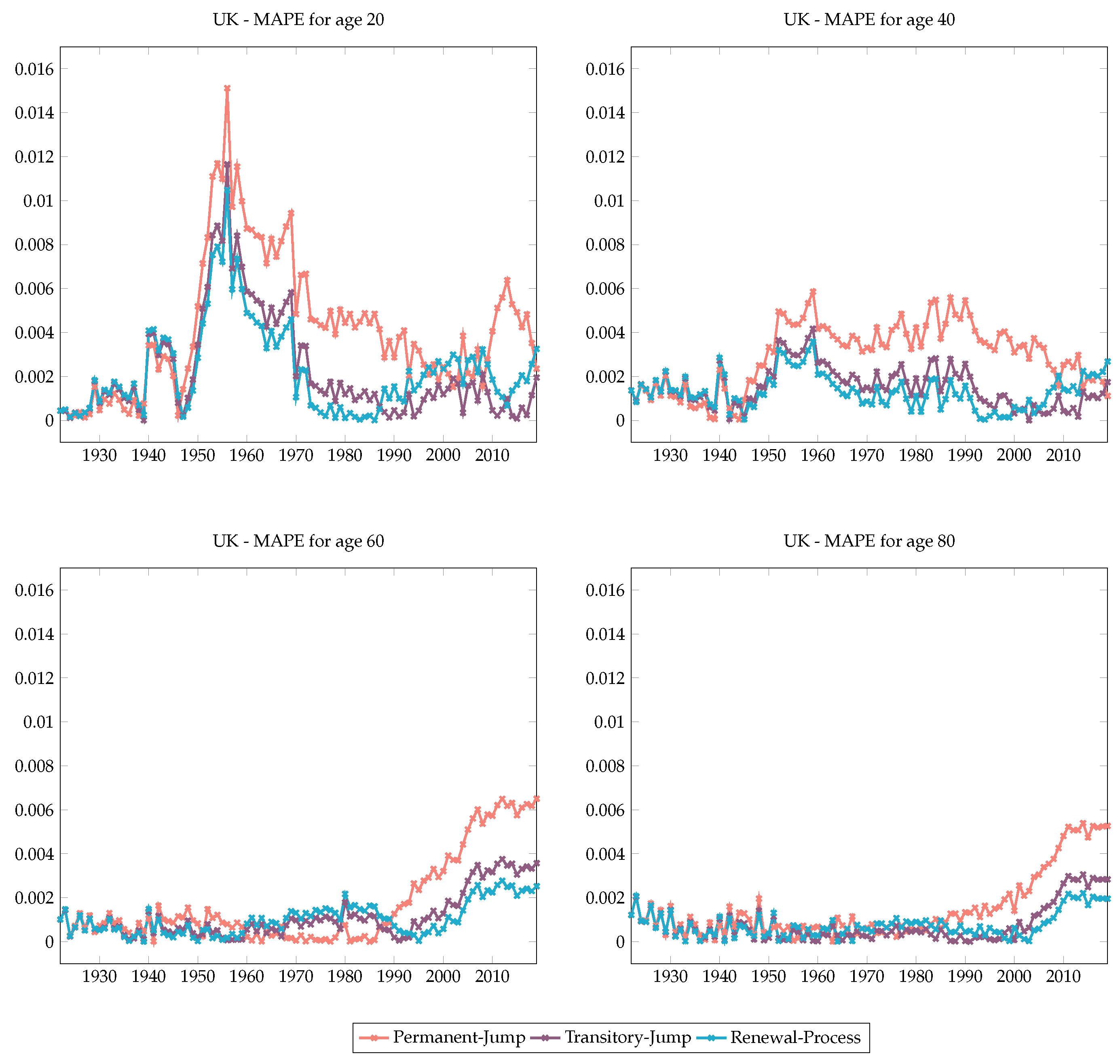

3.1.4. Mean Absolute Percentage Error (MAPE)

3.1.5. Forecasts

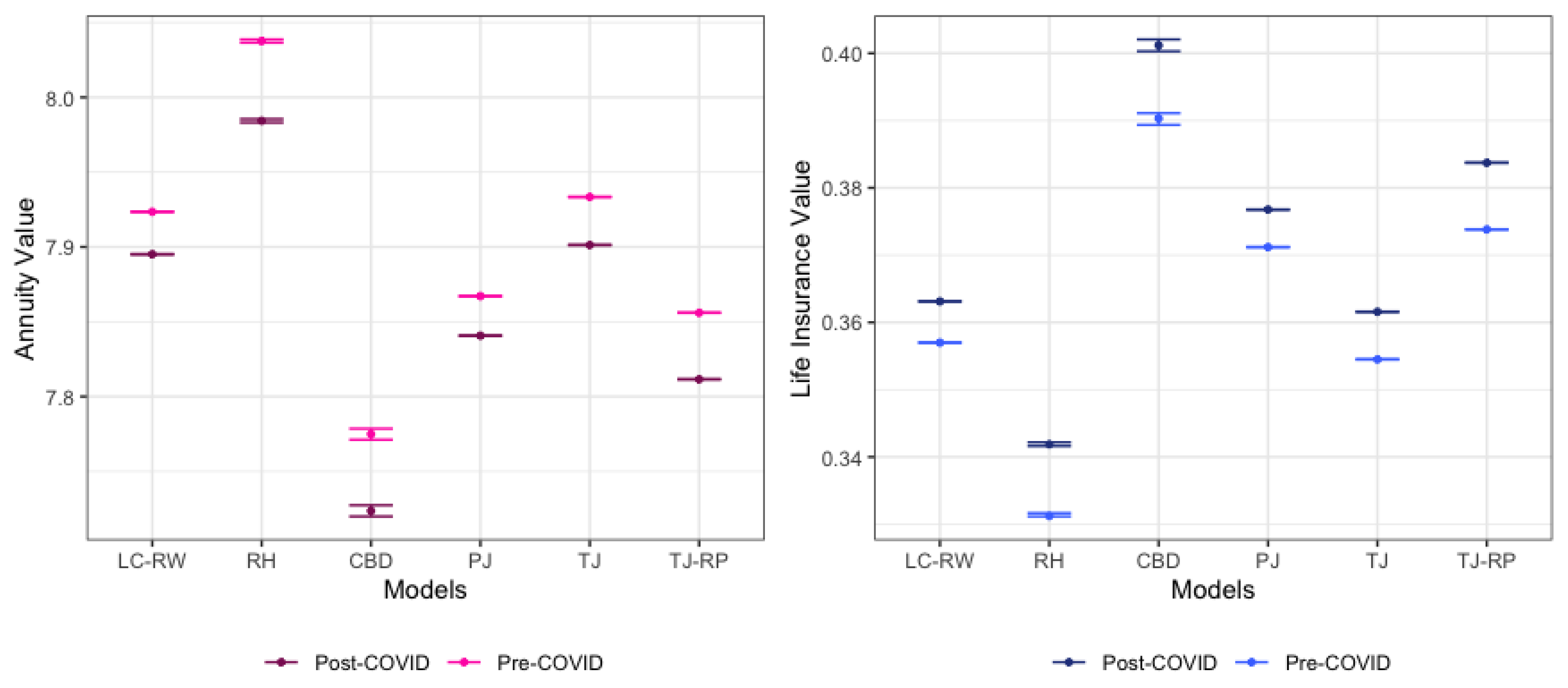

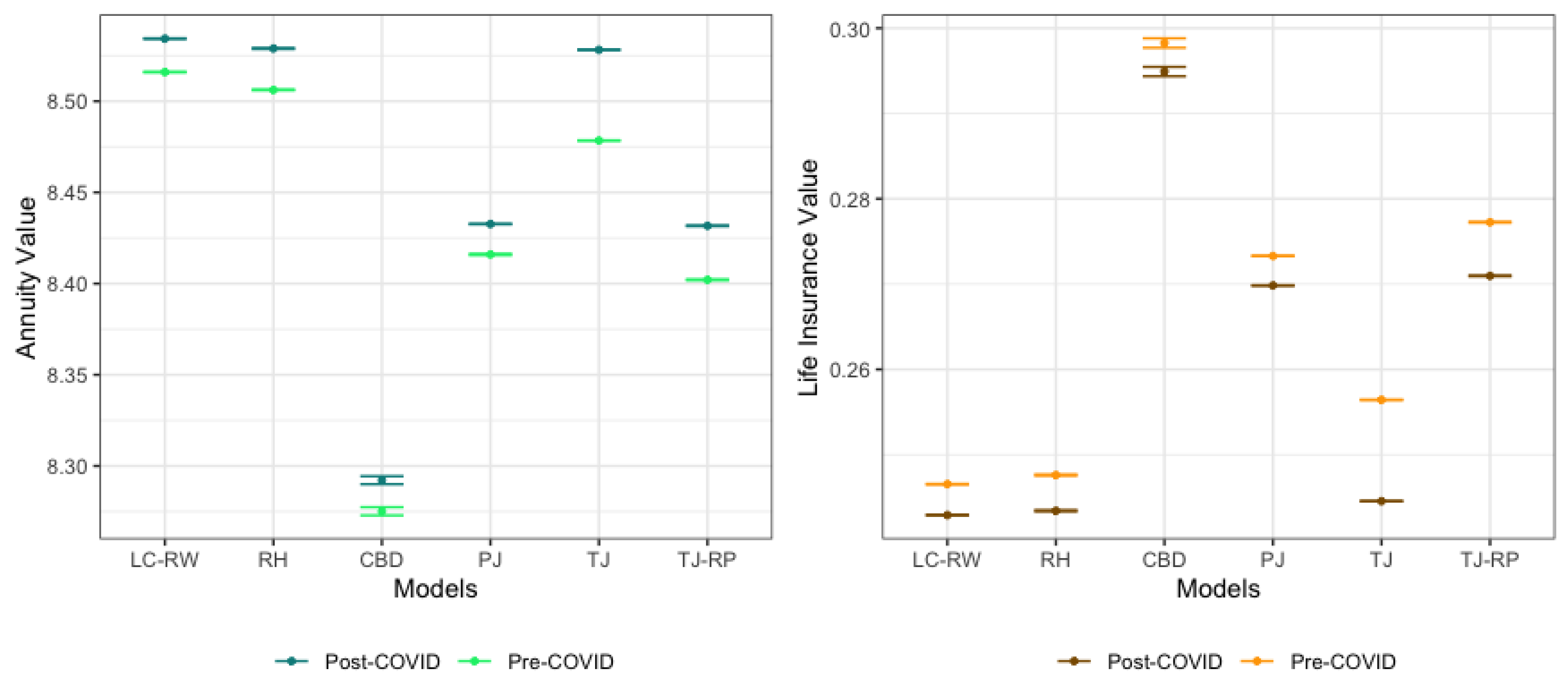

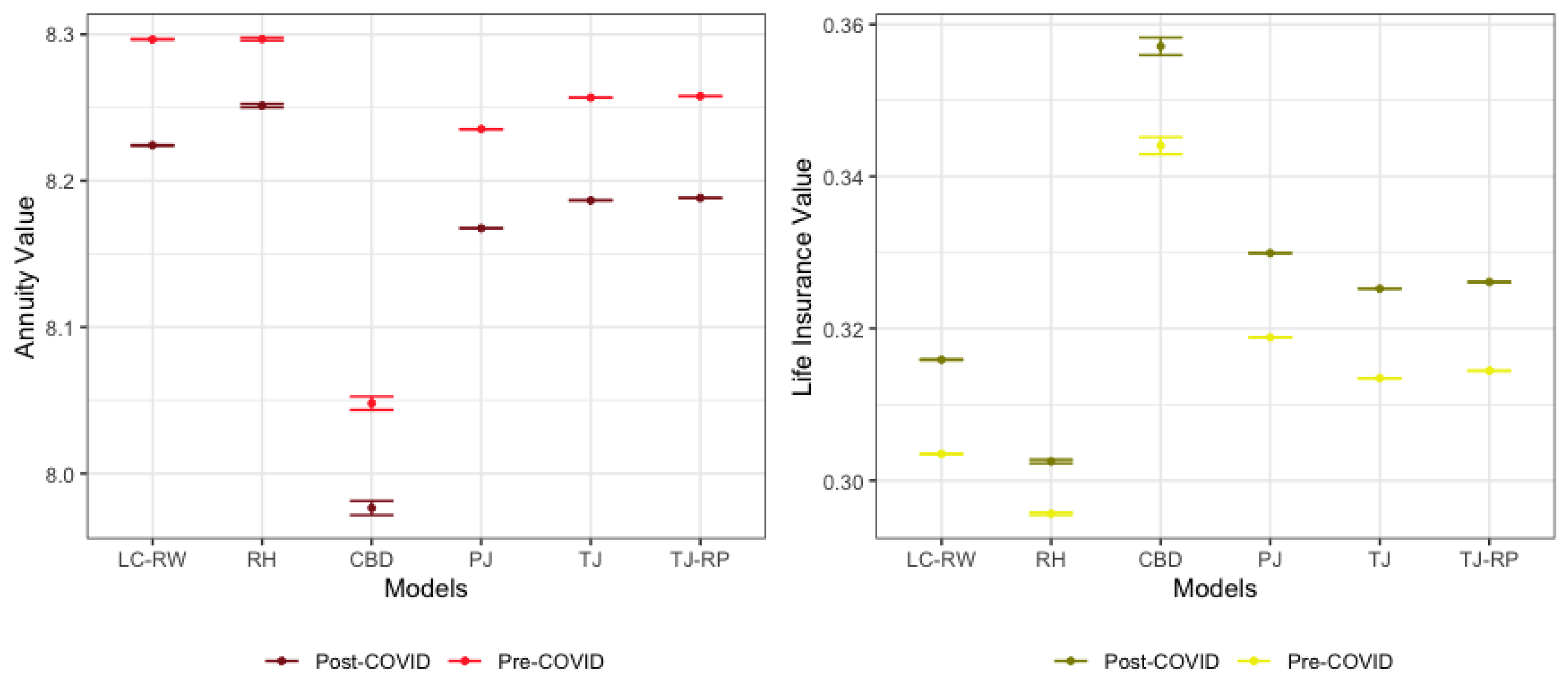

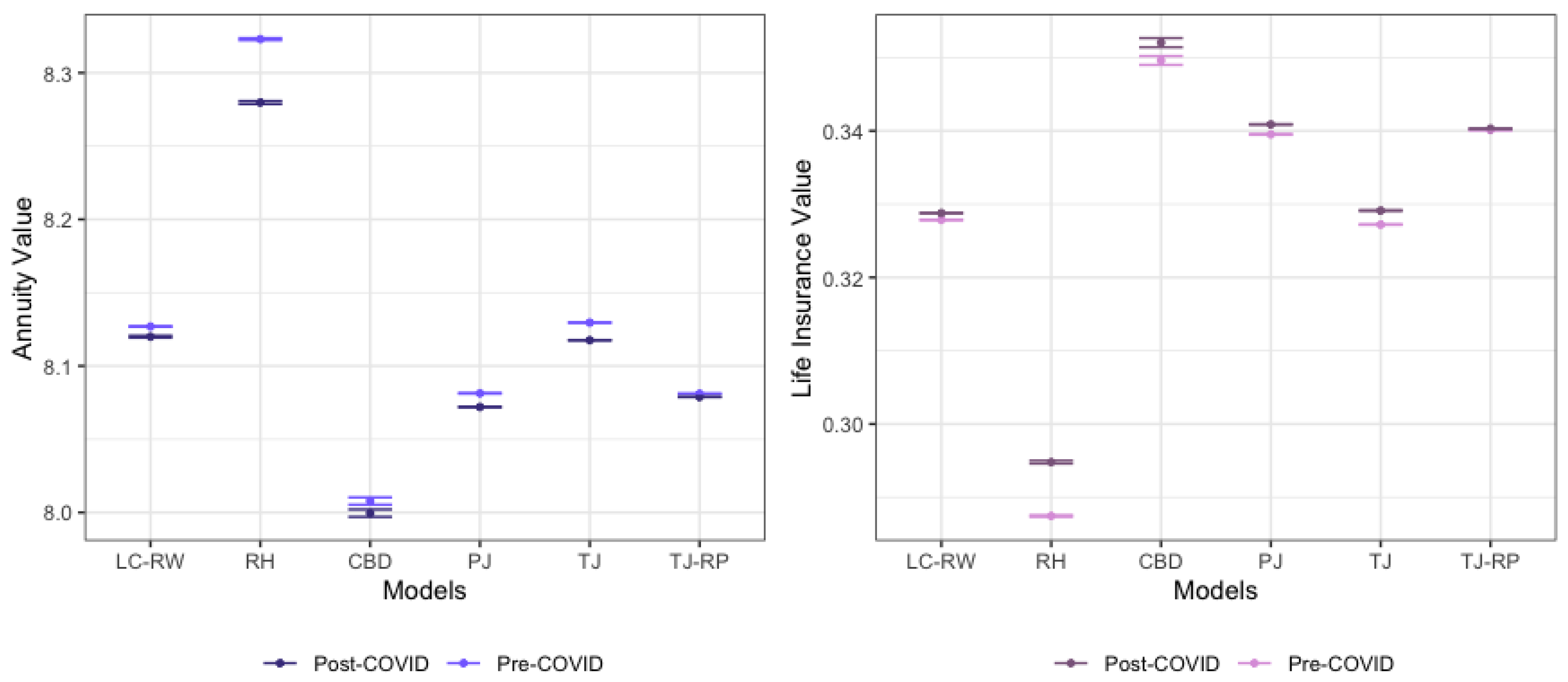

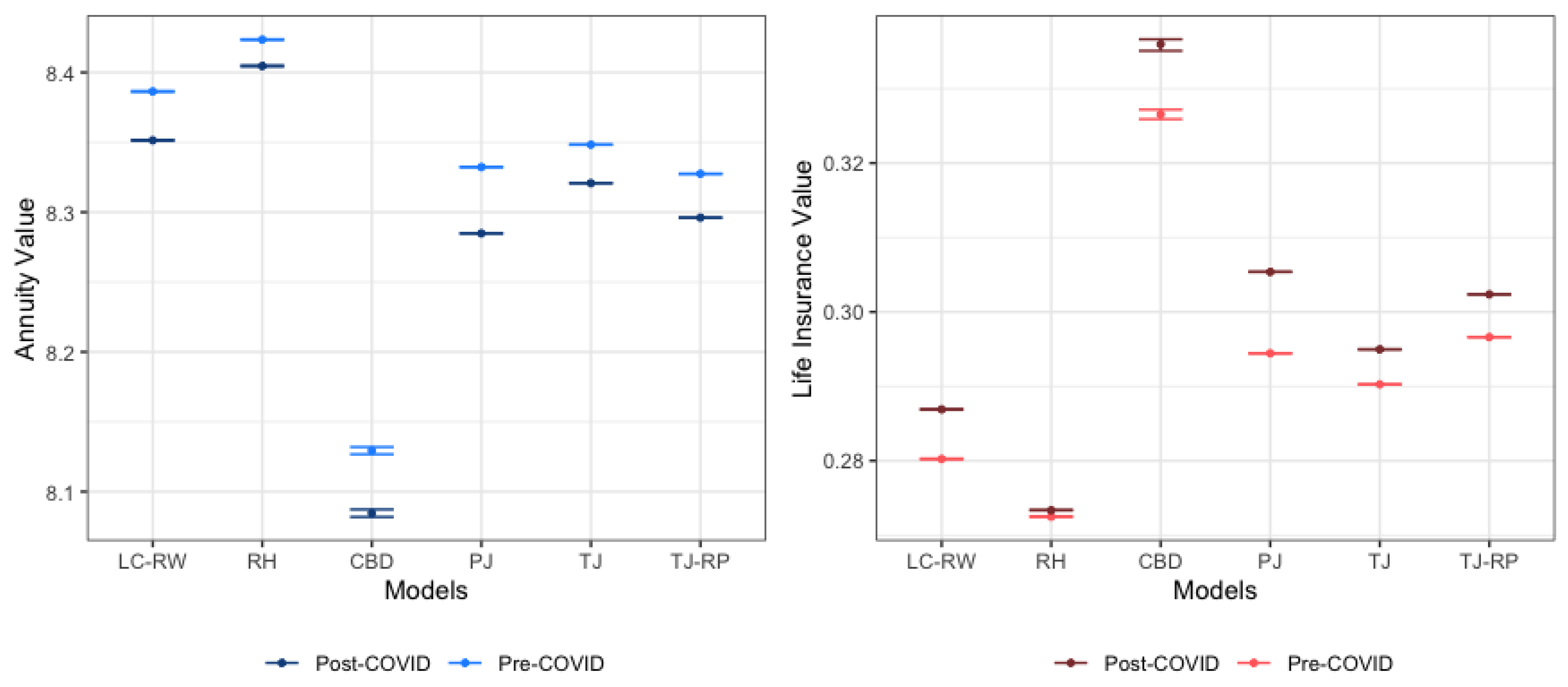

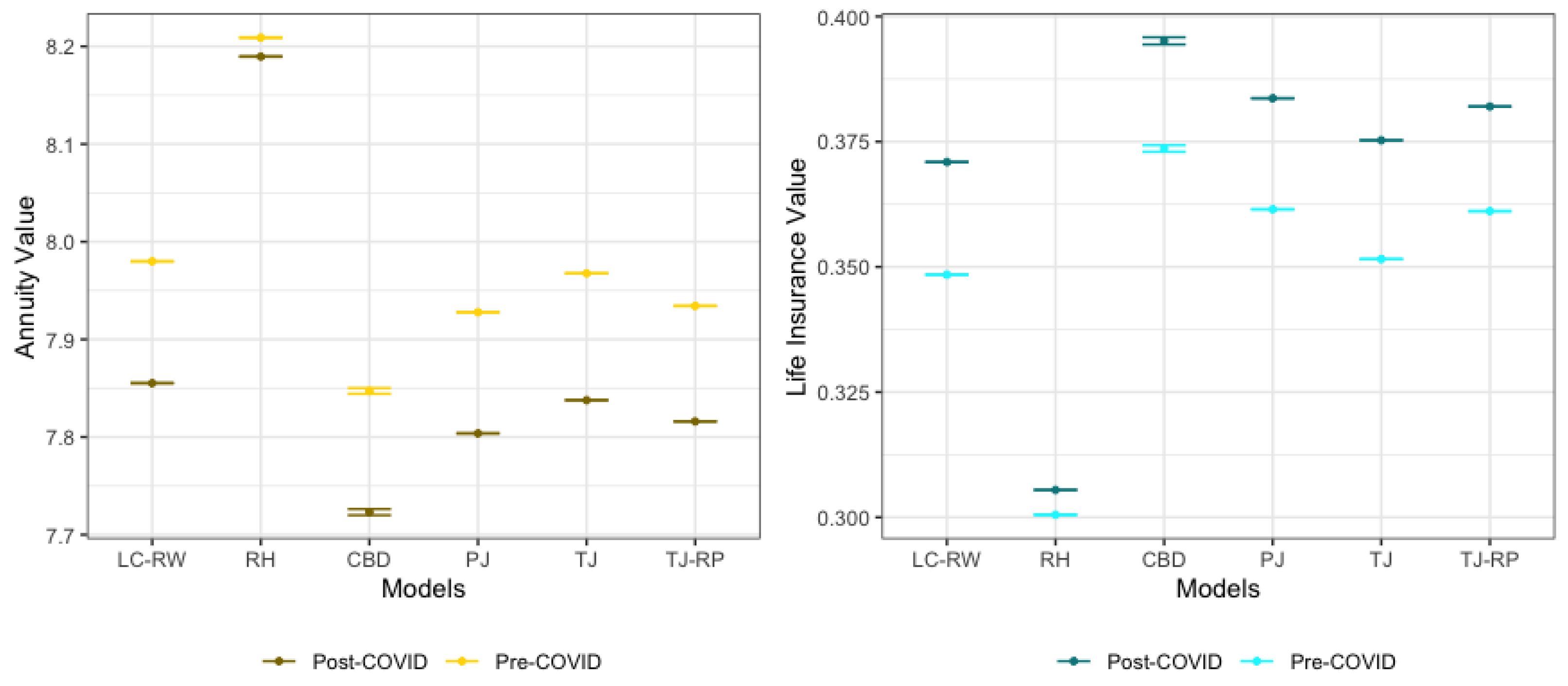

4. Valuation of Mortality-Related Insurance Contracts

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Appendix A. Transitory Mortality Model with Exponential Jumps and Renewal Process

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Denmark | Time Series Model | ARIMA(1,1,0) | ||||||

| (1900–2022) | ||||||||

| Year | 1909 | 1921 | 1977 | 2011 | 2019 | |||

| Japan | Time Series Model | ARIMA(0,2,2) | ||||||

| (1947–2021) | ||||||||

| Year | 1949 | 1957 | ||||||

| Spain | Time Series Model | ARIMA(1,1,0) | ||||||

| (1908–2021) | ||||||||

| Year | 1918 | 1919 | 1942 | 1952 | 1958 | 2016 | 2020 | 2021 |

| Sweden | Time Series Model | ARIMA(1,0,0) | ||||||

| (1908–2019) | ||||||||

| Year | 1917 | 1919 | 1920 | 1921 | 2003 | 2018 | 2021 | |

| Switzerland | Time Series Model | ARIMA(1,1,0) | ||||||

| (1912–2022) | ||||||||

| Year | 1918 | 1919 | 1921 | 1923 | 1964 | 2016 | 2021 | 2022 |

| UK | Time Series Model | ARIMA(1,1,2) | ||||||

| (1922–2021) | ||||||||

| Year | 1931 | 1942 | 1944 | 2021 | ||||

Appendix B. Estimated Model Parameters Including COVID Years

| Country | RW without Jumps | Permanent Jumps | Transitory Jumps | Transitory Jumps & Renewal Process |

|---|---|---|---|---|

| Denmark | ||||

| (1900–2022) | ||||

| BIC = −333.57 | BIC = −414.61 | BIC = −319.25 | BIC = −161.77 | |

| MAPE = 62.56 | MAPE = 16.22 | MAPE = 15.58 | MAPE = 14.74 | |

| Japan | ||||

| (1947–2021) | ||||

| BIC = −198.36 | BIC = −279.15 | BIC = −224.42 | BIC = −119.25 | |

| MAPE = 39.54 | MAPE = 29.86 | MAPE = 27.36 | MAPE = 26.15 | |

| Spain | ||||

| (1908–2021) | ||||

| BIC = −363.86 | BIC = −1111.99 | BIC = −267.23 | BIC = −247.34 | |

| MAPE = 72.09 | MAPE = 28.75 | MAPE = 23.81 | MAPE = 17.34 | |

| Sweden | ||||

| (1908–2022) | ||||

| BIC = −358.00 | BIC = −373.77 | BIC = −257.46 | BIC = −216.69 | |

| MAPE = 68.97 | MAPE = 16.56 | MAPE = 15.94 | MAPE = 14.63 | |

| Switzerland | ||||

| (1912–2022) | ||||

| BIC = −356.85 | BIC = −1733.09 | BIC = −239.34 | BIC = −223.75 | |

| MAPE = 73.87 | MAPE = 21.81 | MAPE = 14.18 | MAPE = 13.06 | |

| The UK | ||||

| (1922–2021) | ||||

| BIC = −300.16 | BIC = −638.11 | BIC = −265.86 | BIC = −236.81 | |

| MAPE = 62.13 | MAPE = 34.56 | MAPE = 16.13 | MAPE = 13.96 |

Appendix C. MAPE Values for Different Ages and Mortality Models for Different Countries

References

- Brouhns, Natasha, Michel Denuit, and Jeroen K. Vermunt. 2002. A Poisson Log-Bilinear Regression Approach to the Construction of Projected Lifetables. Insurance: Mathematics and Economics 31: 373–93. [Google Scholar] [CrossRef]

- Cairns, Andrew J. G. 2023. The Common Cohort Effect Model for Cause of Death Data. “Modelling Measurement and Management of Longevity and Morbidity Risk” research program. London: The Institute and Faculty of Actuaries. [Google Scholar]

- Cairns, Andrew J. G., David Blake, and Kevin Dowd. 2006. A Two-Factor Model for Stochastic Mortality with Parameter Uncertainty: Theory and Calibration. Journal of the Risk and Insurance 73: 687–718. [Google Scholar] [CrossRef]

- Cairns, Andrew J. G., David Blake, Kevin Dowd, Guy D. Coughlan, Alen Ong, and Igor Balevich. 2007. A Quantitative Comparison of Stochastic Mortality Models Using Data From England and Wales and the United States. North American Actuarial Journal 13: 1–35. [Google Scholar] [CrossRef]

- Chen, Hua, and Samuel H. Cox. 2009. Modeling Mortality with Jumps: Applications to Mortality Securitization. The Journal of the Risk and Insurance 3: 727–51. [Google Scholar] [CrossRef]

- Chung, Chen, and Lon-Mu Liu. 1993. Joint Estimation of Model Parameters and Outlier Effects in Time Series. Journal of the American Statistical Association 3: 187–211. [Google Scholar]

- Cox, Samuel H., Yijia Lin, and Shaun Wang. 2006. Multivariate Exponential Tilting and Pricing Implications for Mortality Securitization. Journal of Risk and Insurance 73: 719–36. [Google Scholar] [CrossRef]

- Currie, Iain D., Maria Durban, and Paul H. C. Eilers. 2004. Smoothing and forecasting mortality rates. Statistical Modelling 4: 279–98. [Google Scholar] [CrossRef]

- Deng, Yinglu, Patrick L. Brocket, and Richard D. MacMinn. 2012. Longevity/Mortality Risk Modeling and Securities Pricing. The Journal of Risk and Insurance 3: 697–721. [Google Scholar] [CrossRef]

- Haberman, Steven, and Arthur E. Renshaw. 2012. Parametric mortality improvement rate modelling and projecting. Insurance: Mathematics and Economics 50: 309–33. [Google Scholar] [CrossRef]

- Human Mortality Database. 2023. Available online: https://www.mortality.org (accessed on 1 December 2023).

- Li, Ronald D., and Lawrence R. Carter. 1992. Modeling and Forecasting U.S. Mortality. Journal of the American Statistical Association 87: 659–71. [Google Scholar]

- Li, Siu-Hang, and Wai-Sum Chan. 2005. Outlier Analysis and Mortality Forecasting: The United Kingdom and Scandinavian Countries. Scandinavian Actuarial Journal 3: 187–211. [Google Scholar] [CrossRef]

- Liu, Yanxin, and Johnny S. H. Li. 2015. The Age Pattern of Transitory Mortality Jumps and Its Impact on the Pricing of Catastrophic Mortality Bonds. Insurance: Mathematics and Economics 64: 135–50. [Google Scholar] [CrossRef]

- McShane, Blake, Moshe Adrian, Eric T. Bradlow, and Peter S. Fader. 2008. Count Models Based on Weibull Interarrival Times. Journal of Business and Economic Statistics 26: 369–78. [Google Scholar] [CrossRef]

- Özen, Selin, and Şule Şahin. 2020. Transitory Mortality Jump Modeling with Renewal Process and Its Impact on Pricing of Catastrophic Bonds. Journal of Computational and Applied Mathematics 376: 112829. [Google Scholar] [CrossRef]

- Özen, Selin, and Şule Şahin. 2021. A Two-Population Mortality Model to Assess Longevity Basis Risk. Risks 9: 44. [Google Scholar] [CrossRef]

- Regis, Luca, and Petar Jevtic. 2022. Stochastic Mortality Models and Pandemic Shocks. In Pandemics: Insurance and Social Protection. Edited by Maria C. Boado-Penas, Julia Eisenberg and Şule Şahin. Springer Actuarial Series; Cham: Springer, pp. 61–73. [Google Scholar]

- Renshaw, Arthur E., and Steven Haberman. 2003. Lee–Carter Mortality Forecasting with Age-Specific Enhancement. Insurance: Mathematics and Economics 33: 255–72. [Google Scholar] [CrossRef]

- Renshaw, Arthur E., and Steven Haberman. 2006. A Cohort-Based Extension to the Lee–Carter Model for Mortality Reduction Factors. Insurance: Mathematics and Economics 38: 556–70. [Google Scholar] [CrossRef]

- Richards, Stephan J. 2023. Robust Mortality Forecasting in the Presence of Outliers. Presented to the Faculty of Actuaries. Edinburgh: Longevitas Ltd., pp. 1–28. [Google Scholar]

- Schnürch, Simon, Torsten Kleinow, and Andreas Wagner. 2023. Accounting for COVID-19-type shocks in mortality modeling: A comparative study. Journal of Demographic Economics 89: 483–512. [Google Scholar] [CrossRef]

- Schnürch, Simon, Torsten Kleinow, Ralf Korn, and Andreas Wagner. 2022. The impact of mortality shocks on modelling and insurance valuation as exemplified by COVID-19. Annals of Actuarial Science 16: 498–526. [Google Scholar] [CrossRef]

- Venter, Gary. 2022. A Mortality Model for Pandemics and Other Contagion Events. In Pandemics: Insurance and Social Protection. Edited by Maria C. Boado-Penas, Julia Eisenberg and Şule Şahin. Springer Actuarial Series; Cham: Springer, pp. 75–94. [Google Scholar]

- Villegas, Andres M., Pietro Millossovich, and Vladimir K. Kaishev. 2018. StMoMo: Stochastic Mortality Modeling in R. Journal of Statistical Software 84: 1–38. [Google Scholar] [CrossRef]

| Denmark | Time Series Model | ARIMA(1,1,0) | MAPE | 46.14 | |||

| (1900–2019) | |||||||

| Years | 1909 | 1921 | 1977 | 2011 | 2019 | ||

| Japan | Time Series Model | ARIMA(0,2,2) | MAPE | 90.97 | |||

| (1947–2019) | |||||||

| Years | 1949 | 1957 | |||||

| Spain | Time Series Model | ARIMA(1,1,0) | MAPE | 44.82 | |||

| (1908–2019) | |||||||

| Years | 1918 | 1919 | 1942 | 1952 | 1958 | 1972 | 2016 |

| Sweden | Time Series Model | ARIMA(1,0,0) | MAPE | 49.91 | |||

| (1908–2019) | |||||||

| Years | 1917 | 1919 | 1920 | 1921 | 2003 | 2018 | 2019 |

| Switzerland | Time Series Model | ARIMA(1,1,0) | MAPE | 38.75 | |||

| (1912–2019) | |||||||

| Years | 1918 | 1919 | 1921 | 1923 | 1950 | 1964 | 2016 |

| UK | Time Series Model | ARIMA(1,1,2) | MAPE | 48.16 | |||

| (1922–2019) | |||||||

| Years | 1931 | 1942 | 1944 | ||||

| Country | Permanent Jumps | Transitory Jumps | Transitory Jumps & Renewal Process |

|---|---|---|---|

| Denmark | 1.4054 | 1.0077 | 0.3170 |

| Japan | 2.0522 | 2.7480 | 1.8036 |

| Spain | 3.0178 | 1.1210 | 0.4981 |

| Sweden | 0.9383 | 2.6750 | 0.7685 |

| Switzerland | 0.6871 | 0.2040 | 0.2951 |

| The UK | 0.9079 | 0.3451 | 0.5801 |

| Country | LC-RW | Permanent Jumps | Transitory Jumps | Transitory Jumps & Renewal Process |

|---|---|---|---|---|

| Denmark | ||||

| (1900–2019) | ||||

| BIC = −327.96 | BIC = −442.84 | BIC = −310.67 | BIC = −52.49 | |

| Japan | ||||

| (1947–2019) | ||||

| BIC = −194.69 | BIC = −524.00 | BIC = −253.92 | BIC = −114.70 | |

| Spain | ||||

| (1908–2019) | ||||

| BIC = −344.09 | BIC = −1193.27 | BIC = −337.24 | BIC = −227.74 | |

| Sweden | ||||

| (1908–2019) | ||||

| BIC = −345.18 | BIC = -366.61 | BIC = −254.07 | BIC = −181.07 | |

| Switzerland | ||||

| (1912–2019) | ||||

| BIC = −344.30 | BIC = −933.11 | BIC = −251.97 | BIC = −216.12 | |

| The UK | ||||

| (1922–2019) | ||||

| BIC = −282.35 | BIC = −1329.75 | BIC = −202.59 | BIC = −160.36 |

| Country | LC-RW | RH | CBD | Permanent Jumps | Transitory Jumps | Transitory Jumps & Renewal Process |

|---|---|---|---|---|---|---|

| Denmark | ||||||

| (1900–2019) | ||||||

| BIC | −2,507,517 | −12,625,099 | −1,438,469 | −201,649.80 | −153,532.60 | −87,829.99 |

| MAPE | 62.88 | 83.54 | 48.58 | 23.83 | 20.12 | 14.45 |

| Japan | ||||||

| (1947–2019) | ||||||

| BIC | −9,185,253 | −123,725,040 | −8,915,135 | −3,577,544 | −1,416,897 | −1,316,616 |

| MAPE | 39.12 | 107.58 | 39.48 | 29.58 | 27.62 | 25.57 |

| Spain | ||||||

| (1908–2019) | ||||||

| BIC | −30,767,472 | −81,396,057 | −16,432,829 | −3,162,232 | −1,661,928 | −1,503,534 |

| MAPE | 70.20 | 85.77 | 67.91 | 29.65 | 28.57 | 17.90 |

| Sweden | ||||||

| (1908–2019) | ||||||

| BIC | −4,805,222 | −23,712,707 | −1,462,889 | −198,654.20 | −185,479.60 | −130,953.20 |

| MAPE | 68.71 | 96.72 | 37.17 | 21.75 | 20.58 | 14.40 |

| Switzerland | ||||||

| (1912–2019) | ||||||

| BIC | −5,164,856 | −23,625,717 | −1,099,357 | −178,031 | −106,925.90 | −83,879.52 |

| MAPE | 73.32 | 240.19 | 40.09 | 26.55 | 16.86 | 12.82 |

| The UK | ||||||

| (1922–2019) | ||||||

| BIC | −21,466,019 | −223,085,156 | −9,488,580 | −1,255,758 | −487,732.40 | −413,783.10 |

| MAPE | 60.82 | 102.76 | 36.01 | 27.44 | 14.35 | 13.85 |

| Country | Fitting Years | Estimation Years | Number of Deaths | Models | Quantiles | |||||

|---|---|---|---|---|---|---|---|---|---|---|

| Range (Max–Min) | ||||||||||

| Denmark | 1908–2019 | 2019 | 1626 | LC-RW | ||||||

| 2020 | 1706 | 1621.18 | 1744.51 | 1767.26 | 1789.93 | 1918.09 | 296.91 | |||

| 2021 | 1694 | 1695.29 | 1824.26 | 1848.04 | 1871.75 | 2005.77 | 310.48 | |||

| 2022 | 1810 | 1671.20 | 1798.33 | 1821.78 | 1845.14 | 1977.26 | 306.07 | |||

| RH Model | ||||||||||

| 2020 | 1706 | 1566.56 | 1668.90 | 1691.56 | 1715.90 | 1796.69 | 230.12 | |||

| 2021 | 1694 | 1586.52 | 1715.75 | 1752.28 | 1787.91 | 1911.63 | 325.12 | |||

| 2022 | 1810 | 1501.65 | 1643.75 | 1687.70 | 1729.13 | 1883.70 | 382.05 | |||

| CBD Model | ||||||||||

| 2020 | 1706 | 1450.23 | 1778.39 | 1848.16 | 1925.84 | 2285.08 | 834.85 | |||

| 2021 | 1694 | 1356.64 | 1841.02 | 1947.10 | 2056.25 | 2648.28 | 1291.65 | |||

| 2022 | 1810 | 1266.58 | 1803.29 | 1927.64 | 2066.76 | 3051.36 | 1784.78 | |||

| Permanent Jump | ||||||||||

| 2020 | 1706 | 1701.90 | 1760.59 | 1776.49 | 1812.32 | 1833.70 | 131.80 | |||

| 2021 | 1694 | 1794.54 | 1856.43 | 1873.19 | 1910.97 | 1933.52 | 138.97 | |||

| 2022 | 1810 | 1783.79 | 1845.31 | 1861.97 | 1899.52 | 1921.94 | 138.14 | |||

| Transitory Jump | ||||||||||

| 2020 | 1706 | 1631.42 | 1744.15 | 1768.56 | 1782.46 | 1902.55 | 271.14 | |||

| 2021 | 1694 | 1703.46 | 1821.17 | 1846.66 | 1861.17 | 1986.57 | 283.11 | |||

| 2022 | 1810 | 1676.76 | 1792.62 | 1817.71 | 1831.99 | 1955.43 | 278.67 | |||

| Transitory Jump & Renewal Process | ||||||||||

| 2020 | 1706 | 1660.49 | 1786.18 | 1798.32 | 1813.64 | 1973.36 | 312.87 | |||

| 2021 | 1694 | 1769.20 | 1903.11 | 1916.05 | 1932.36 | 2102.55 | 333.35 | |||

| 2022 | 1810 | 1776.99 | 1911.50 | 1924.49 | 1940.88 | 2111.82 | 334.82 | |||

| Country | Fitting Years | Estimation Years | Number of Deaths | Models | Quantiles | |||||

|---|---|---|---|---|---|---|---|---|---|---|

| Range (Max–Min) | ||||||||||

| Japan | 1908–2019 | 2019 | 29,155 | |||||||

| LC-RW | ||||||||||

| 2020 | 24,872 | 21,699.04 | 24,043.47 | 24,483.26 | 24,923.81 | 27,456.24 | 5757.20 | |||

| 2021 | 21,721 | 19,085.54 | 21,147.60 | 21,534.42 | 21,921.90 | 24,149.32 | 5063.78 | |||

| RH Model | ||||||||||

| 2020 | 24,872 | 24,294.98 | 24,690.13 | 24,775.16 | 24,865.60 | 25,158.96 | 863.98 | |||

| 2021 | 21,721 | 23,598.63 | 24,420.09 | 24,699.85 | 24,964.62 | 25,369.29 | 1770.66 | |||

| CBD Model | ||||||||||

| 2020 | 24,872 | 24,681.36 | 27,674.07 | 28,495.50 | 29,401.69 | 32,135.47 | 7454.11 | |||

| 2021 | 21,721 | 21,094.40 | 24,446.49 | 25,595.23 | 26,712.20 | 31,410.11 | 10,315.71 | |||

| Permanent Jump | ||||||||||

| 2020 | 24,872 | 23,673.72 | 24,540.85 | 25,208.52 | 25,287.34 | 25,603.97 | 1930.25 | |||

| 2021 | 21,721 | 21,256.45 | 22,035.03 | 22,634.53 | 22,705.30 | 22,989.60 | 1733.15 | |||

| Transitory Jump | ||||||||||

| 2020 | 24,872 | 23,598.63 | 24,420.09 | 24,699.85 | 24,964.62 | 25,369.29 | 1770.66 | |||

| 2021 | 21,721 | 20,921.00 | 21,649.25 | 21,897.27 | 22,132.00 | 22,490.74 | 1569.74 | |||

| Transitory Jump & Renewal Process | ||||||||||

| 2020 | 24,872 | 18,610.96 | 24,552.99 | 25,010.20 | 25,477.16 | 33,364.09 | 14,753.13 | |||

| 2021 | 21,721 | 16,724.19 | 22,063.81 | 22,474.66 | 22,894.29 | 29,981.65 | 13,257.46 | |||

| Country | Fitting Years | Estimation Years | Number of Deaths | Models | Quantiles | |||||

|---|---|---|---|---|---|---|---|---|---|---|

| Range (Max–Min) | ||||||||||

| Spain | 1908–2019 | 2019 | 8036 | |||||||

| LC-RW | ||||||||||

| 2020 | 9662 | 6492.15 | 7530.46 | 7730.47 | 7932.42 | 9123.90 | 2631.75 | |||

| 2021 | 8868 | 6478.52 | 7514.65 | 7714.23 | 7915.76 | 9104.74 | 2626.22 | |||

| RH Model | ||||||||||

| 2020 | 9662 | 6990.11 | 8089.89 | 8318.55 | 8551.43 | 9759.31 | 2769.20 | |||

| 2021 | 8868 | 6582.57 | 7926.64 | 8246.59 | 8565.35 | 10,468.82 | 3886.25 | |||

| CBD Model | ||||||||||

| 2020 | 9662 | 7263.43 | 9490.06 | 10,044.10 | 10,653.01 | 13,502.91 | 6239.48 | |||

| 2021 | 8868 | 6347.46 | 9403.35 | 10,195.60 | 11,066.72 | 16,026.08 | 9678.62 | |||

| Permanent Jump | ||||||||||

| 2020 | 9662 | 7480.59 | 7791.20 | 7865.86 | 7907.20 | 8067.95 | 587.36 | |||

| 2021 | 8868 | 7575.63 | 7890.18 | 7965.79 | 8007.66 | 8170.45 | 594.82 | |||

| Transitory Jump | ||||||||||

| 2020 | 9662 | 7674.47 | 7783.17 | 7804.81 | 7826.34 | 7915.62 | 241.16 | |||

| 2021 | 8868 | 7732.77 | 7842.30 | 7864.11 | 7885.80 | 7975.76 | 243.00 | |||

| Transitory Jump & Renewal Process | ||||||||||

| 2020 | 9662 | 6983.00 | 7740.11 | 7792.54 | 7823.82 | 8630.57 | 1647.57 | |||

| 2021 | 8868 | 7012.47 | 7772.77 | 7825.42 | 7856.83 | 8666.99 | 1654.52 | |||

| Country | Fitting Years | Estimation Years | Number of Deaths | Models | Quantiles | |||||

|---|---|---|---|---|---|---|---|---|---|---|

| Range (Max–Min) | ||||||||||

| Sweden | 1908–2019 | 2019 | 2333 | |||||||

| LC-RW | ||||||||||

| 2020 | 2565 | 2292.49 | 2533.12 | 2578.19 | 2623.31 | 2882.30 | 589.81 | |||

| 2021 | 2474 | 2292.79 | 2533.46 | 2578.53 | 2623.66 | 2882.68 | 589.89 | |||

| 2022 | 2363 | 2266.27 | 2504.15 | 2548.71 | 2593.31 | 2849.34 | 583.07 | |||

| RH Model | ||||||||||

| 2020 | 2565 | 2281.03 | 2331.33 | 2344.34 | 2358.40 | 2406.55 | 125.52 | |||

| 2021 | 2474 | 2252.26 | 2316.40 | 2334.74 | 2354.90 | 2427.10 | 174.83 | |||

| 2022 | 2363 | 2171.52 | 2245.50 | 2267.20 | 2288.41 | 2370.01 | 198.49 | |||

| CBD Model | ||||||||||

| 2020 | 2565 | 2302.35 | 2688.60 | 2769.43 | 2857.39 | 3255.75 | 953.40 | |||

| 2021 | 2474 | 2115.58 | 2672.46 | 2788.39 | 2905.83 | 3515.22 | 1399.64 | |||

| 2022 | 2363 | 2015.34 | 2630.63 | 2768.92 | 2921.12 | 3964.05 | 1399.64 | |||

| Permanent Jump | ||||||||||

| 2020 | 2565 | 2284.33 | 2580.00 | 2593.84 | 2619.82 | 2946.18 | 661.85 | |||

| 2021 | 2474 | 2302.68 | 2600.73 | 2614.67 | 2640.86 | 2969.85 | 667.17 | |||

| 2022 | 2363 | 2294.03 | 2590.95 | 2604.84 | 2630.93 | 2958.68 | 664.66 | |||

| Transitory Jump | ||||||||||

| 2020 | 2565 | 2418.95 | 2556.07 | 2588.30 | 2599.30 | 2728.74 | 309.79 | |||

| 2021 | 2474 | 2420.08 | 2557.27 | 2589.51 | 2600.52 | 2730.02 | 309.94 | |||

| 2022 | 2363 | 2392.89 | 2528.54 | 2560.41 | 2571.30 | 2699.34 | 306.45 | |||

| Transitory Jump & Renewal Process | ||||||||||

| 2020 | 2565 | 2429.93 | 2582.63 | 2592.95 | 2599.76 | 2754.19 | 324.26 | |||

| 2021 | 2474 | 2442.43 | 2595.91 | 2606.29 | 2613.13 | 2768.36 | 325.93 | |||

| 2022 | 2363 | 2426.27 | 2578.74 | 2589.05 | 2595.85 | 2750.05 | 323.78 | |||

| Country | Fitting Years | Estimation Years | Number of Deaths | Models | Quantiles | |||||

|---|---|---|---|---|---|---|---|---|---|---|

| Range (Max–Min) | ||||||||||

| Switzerland | 1908–2019 | 2019 | 1436 | |||||||

| LC-RW | ||||||||||

| 2020 | 1607 | 1334.22 | 1583.49 | 1632.14 | 1681.47 | 1976.30 | 642.10 | |||

| 2021 | 1540 | 1351.00 | 1603.41 | 1652.68 | 1702.63 | 2001.17 | 650.20 | |||

| 2022 | 1571 | 1340.45 | 1590.88 | 1639.76 | 1689.32 | 1985.53 | 645.10 | |||

| RH Model | ||||||||||

| 2020 | 1607 | 1346.29 | 1425.05 | 1447.22 | 1468.09 | 1559.83 | 213.50 | |||

| 2021 | 1540 | 1308.42 | 1418.55 | 1446.46 | 1476.90 | 1612.00 | 303.60 | |||

| 2022 | 1571 | 1291.43 | 1426.18 | 1464.13 | 1500.61 | 1678.52 | 387.10 | |||

| CBD Model | ||||||||||

| 2020 | 1607 | 1441.97 | 1699.35 | 1755.47 | 1814.77 | 2093.26 | 651.30 | |||

| 2021 | 1540 | 1336.12 | 1715.81 | 1794.80 | 1877.06 | 2305.43 | 969.30 | |||

| 2022 | 1571 | 1287.48 | 1700.38 | 1795.57 | 1899.35 | 2626.87 | 1339.40 | |||

| Permanent Jump | ||||||||||

| 2020 | 1607 | 1561.12 | 1630.64 | 1648.38 | 1675.00 | 1717.65 | 156.50 | |||

| 2021 | 1540 | 1597.92 | 1669.08 | 1687.23 | 1714.46 | 1758.14 | 160.20 | |||

| 2022 | 1571 | 1602.64 | 1674.01 | 1692.21 | 1719.53 | 1763.33 | 160.70 | |||

| Transitory Jump | ||||||||||

| 2020 | 1607 | 1611.28 | 1637.60 | 1646.44 | 1651.73 | 1668.10 | 56.82 | |||

| 2021 | 1540 | 1644.18 | 1671.03 | 1680.05 | 1685.45 | 1702.16 | 57.98 | |||

| 2022 | 1571 | 1643.94 | 1670.80 | 1679.81 | 1685.22 | 1701.91 | 57.97 | |||

| Transitory Jump & Renewal Process | ||||||||||

| 2020 | 1607 | 1460.02 | 1636.64 | 1648.65 | 1659.09 | 1831.28 | 371.26 | |||

| 2021 | 1540 | 1492.68 | 1673.24 | 1685.52 | 1696.20 | 1872.24 | 379.56 | |||

| 2022 | 1571 | 1495.32 | 1676.20 | 1688.50 | 1699.20 | 1875.55 | 380.23 | |||

| Country | Fitting Years | Estimation Years | Number of Deaths | Models | Quantiles | |||||

|---|---|---|---|---|---|---|---|---|---|---|

| Range (Max–Min) | ||||||||||

| UK | 1908–2019 | 2019 | 14,170 | |||||||

| LC-RW | ||||||||||

| 2020 | 15,992 | 13,686.88 | 15,158.56 | 15,434.55 | 15,711.00 | 17,299.71 | 3612.80 | |||

| 2021 | 15,549 | 13,237.87 | 14,661.27 | 14,928.21 | 15,195.58 | 16,732.18 | 3494.30 | |||

| RH Model | ||||||||||

| 2020 | 15,992 | 13,241.54 | 13,596.61 | 13,673.88 | 13,750.68 | 14,134.80 | 893.30 | |||

| 2021 | 15,549 | 12,585.80 | 13,003.17 | 13,110.20 | 13,212.98 | 13,675.61 | 1089.80 | |||

| CBD Model | ||||||||||

| 2020 | 15,992 | 13,533.46 | 15,975.05 | 16,515.76 | 17,098.27 | 19,717.18 | 6183.70 | |||

| 2021 | 15,549 | 12,018.17 | 15,377.84 | 16,117.66 | 16,900.17 | 20,921.38 | 8903.20 | |||

| Permanent Jump | ||||||||||

| 2020 | 15,992 | 15,190.85 | 15,508.81 | 15,574.37 | 15,625.62 | 15,885.62 | 694.80 | |||

| 2021 | 15,549 | 14,816.62 | 15,126.75 | 15,190.70 | 15,240.69 | 15,494.28 | 677.70 | |||

| Transitory Jump | ||||||||||

| 2020 | 15,992 | 14,557.63 | 15,334.88 | 15,511.35 | 15,576.93 | 16,327.32 | 1769.70 | |||

| 2021 | 15,549 | 14,108.89 | 14,862.19 | 15,033.22 | 15,096.78 | 15,824.03 | 1715.10 | |||

| Transitory Jump & Renewal Process | ||||||||||

| 2020 | 15,992 | 14,443.32 | 15,452.89 | 15,523.14 | 15,567.87 | 16,596.26 | 2152.90 | |||

| 2021 | 15,549 | 14,037.59 | 15,018.80 | 15,087.08 | 15,130.56 | 16,130.06 | 2092.50 | |||

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Şahin, Ş.; Özen, S. A Quantitative Comparison of Mortality Models with Jumps: Pre- and Post-COVID Insights on Insurance Pricing. Risks 2024, 12, 53. https://doi.org/10.3390/risks12030053

Şahin Ş, Özen S. A Quantitative Comparison of Mortality Models with Jumps: Pre- and Post-COVID Insights on Insurance Pricing. Risks. 2024; 12(3):53. https://doi.org/10.3390/risks12030053

Chicago/Turabian StyleŞahin, Şule, and Selin Özen. 2024. "A Quantitative Comparison of Mortality Models with Jumps: Pre- and Post-COVID Insights on Insurance Pricing" Risks 12, no. 3: 53. https://doi.org/10.3390/risks12030053