1. Introduction

In actuarial science and insurance, the Sparre–Andersen risk model plays a crucial role in stochastically modelling a company’s surplus or its available financial resources over time. This model generalises the classical risk model that was introduced by Lundberg (see, e.g.,

Asmussen and Albrecher (

2010);

Schmidli (

2017);

Rolski et al. (

1999)), assuming that the claim number process is a renewal process (see, e.g.,

Labbé and Sendova (

2009);

Li and Garrido (

2005);

Temnov (

2004,

2014);

Willmot (

2007);

Asmussen and Albrecher (

2010)). This model has recently become a focal point for research. A key area of interest is the ruin probability, which essentially means the probability of the company’s surplus turning negative at some point. The complexity of this concept means that there is no straightforward formula for calculating this probability. As a result, researchers are engaged in developing approximations, bounds, and asymptotic formulas to better grasp its characteristics.

In this paper, we will present both the upper and lower bounds for the ruin probability. Specifically, after a mathematical overview of the Sparre–Andersen model, we will present the proof of certain lemmas that will assist us in establishing the proof of the aforementioned bounds. Initially, we will focus on the upper and lower bounds in the case where the adjustment coefficient exists, with the upper bound being a refined version of Lundberg’s famous inequality. Moreover, these bounds serve as enhancements to those previously given by

Psarrakos and Politis (

2009a). Next, we will provide bounds for the ruin probability, using properties from aging classes for the distribution of the claim amounts. Our work offers enhancements to the bounds proposed by

Willmot et al. (

2001);

Willmot (

2002);

Psarrakos and Politis (

2009a). Finally, we will generalize the conditions under which the bounds proposed by

Chadjiconstantinidis and Xenos (

2022), for the cases where the adjustment coefficient does not exist, can be applied.

2. Model Description

Consider the Sparre–Andersen risk model for an insurance surplus process defined as

is the surplus at time

t, where

u is the surplus at time

(also known as the initial surplus) and

c is the rate of premium income per unit of time. With

, we denote the number of claims in the time interval

. The individual claim amounts

(

) are independent, identically distributed (i.i.d.) non-negative random variables with a common distribution function (d.f.)

, tail

, density

and mean

. The claim amounts are also independent of

, and the corresponding interclaim times

are i.i.d. with common mean

. Also, we assume that

, where

is the implied relative security loading. Also,

F is the distribution of the drop in the surplus given that such a drop occurs (see, e.g.,

Willmot (

2002)).

Now, let

be the time of ruin, then the ruin probability is defined as

The probability of ruin

satisfies the defective renewal equation (see, e.g.,

Willmot and Lin (

2001) and

Section 3.2)

with solution

where

is the probability of non-ruin,

,

and

is the tail of the n-fold convolution of the ladder height distribution

F associated with the risk process.

The solution to Equation (

1) is given by the Pollaczek–Khintchine type formula,

i.e.,

is a geometric compound tail with geometric parameter

(see, e.g.,

Willmot and Woo (

2017)).

One of the primary results in the study of ruin probabilities is Lundberg inequality, namely:

where

R is called the adjustment coefficient and is defined as the unique positive solution of the following equation

The last equation is known as the Lundberg condition, and integrating by parts the above gives

Another key result is the Cramer–Lundberg asymptotic formula:

where

In actuarial risk theory, a key variable of interest introduced by

Gerber et al. (

1987), is the deficit at ruin, with distribution defined as

It is a defective distribution function with a right tail:

This satisfies the following defective renewal equation

with solution

3. Definitions, Notation and Preliminary Results

This section outlines all the mathematical tools we will use in subsequent sections to introduce new bounds for the ruin probability in the Sparre–Andersen risk model.

3.1. Definitions and Notation

We denote by

the quantity

We also define

and the function

that serves as a critical component in the proof of Proposition 2.

And lastly, for convenience in algebraic manipulation, we define

3.2. Convolutions and Renewal Equation

For two integrable functions

their convolution

is defined by

while for two distribution functions

the convolution

is defined by

. In either case, the symbol

(

) denotes the

kth convolution product of

f (resp.,

F) by itself.

Generally, an equation with the following form

for

is called a defective renewal type equation and is known to have the following unique solution (see, e.g.,

Willmot and Lin (

2001) for a detailed discussion of the solution of the defective renewal equation)

where

3.3. Aging Classes

This section introduces the aging classes that we will utilize in

Section 4.2 (see, e.g.,

Willmot and Lin (

2001)). Each aging class contains distributions characterised by particular failure rate properties. These classes have been developed within the field of reliability theory and survival analysis to analyze respective lifespans. Furthermore, these classes are applied in actuarial science and insurance, aiding in the modelling of claim amounts and the number of claims. The classes used here include IFR (DFR), NBU (NWU) and NBUC (NWUC).

The d.f. is said to be decreasing (increasing) failure rate or DFR (IFR) if is nondecreasing (nonincreasing) in y for fixed , i.e., if is log-convex (log-concave). Also, if is absolutely continuous, then DFR (IFR) is equivalent to nonincreasing (nondecreasing) in y, where .

A d.f.

is called new worse (better) than used or NWU (NBU) if

Another class is the new worse (better) than used in convex ordering or NWUC (NBUC) class. The d.f.

is NWUC (NBUC) if

for all

and

is the equilibrium distribution of F.

3.4. Preliminary Results

This section introduces four Lemmas and a Proposition, which are crucial for the proof of the bounds for the ruin probability. In the following result, we present a renewal-type equation for the difference .

Lemma 1. The function h(u) satisfies the following renewal equation Proof. Substituting (

7) and (

8) into (

1) we have:

and after a re-arranging of the terms, the proof is completed. □

Lemma 2. For any , it holds that Proof. Using (

11), we see that the solution of (

12) is given by

Inserting (

2) into the above we obtain

Because of (

7), the above equation could be written as

Dividing by , completes the proof. □

Lemma 3. For , and it is an increasing function of u.

Proof. The first derivative of (

10) gives

which means that

, and that completes the proof. □

Lemma 4. If the d.f. F is NWU (NBU), then Proof. If the d.f. F is NWU (NBU), then it holds

, therefore,

The integral on the left side could be written with the help of (

5) as follows

and the proof is completed by inserting the above into (

14). □

Proposition 1. In the Sparre–Andersen risk model we have that

- i.

If the claim amount d.f. P is DFR, then the function is nonincreasing in u.

- ii.

For any , it holds that - iii.

For any , it holds that - iv.

Let . Then for the function in (9) satisfies the defective renewal equation

4. Bounds for the Ruin Probability

4.1. Improvements of Lundberg’s Upper Bound of Ruin Probability

We assume throughout this section that

F is light-tailed so that

R exists.

Psarrakos and Politis (

2009a) provide a two-sided bound, given in (

17), for the ruin probability. The upper bound is an improvement over Lundberg’s upper bound. In the following result, we improve the lower and upper bounds given in (

17).

Proposition 2. For every and it holds that

- i.

a lower bound for the ruin probability is given by - ii.

an upper bound for the ruin probability is given by

Proof. Inserting (

7) into the lower bound of (

17) we obtain

and then (

12) gives

In view of (

10) the above inequality is written as follows

Inserting the above inequality into (

12) we have

and after repeating the same process

k times (for

) we obtain

and the proof is completed.

Inserting the inequality above into (

18), yields

By reinserting the above inequality into (

18) we derive

Repeating the same process

k times (for

) we have

By inserting the above into (

9) and rearranging the terms we obtain

where

.

Multiplying by

yields that

Taking the limit for

we obtain

Inserting (

23) and (

24) into (

22) we obtain

In view of (

5) and by rearranging the terms the proof is completed.

□

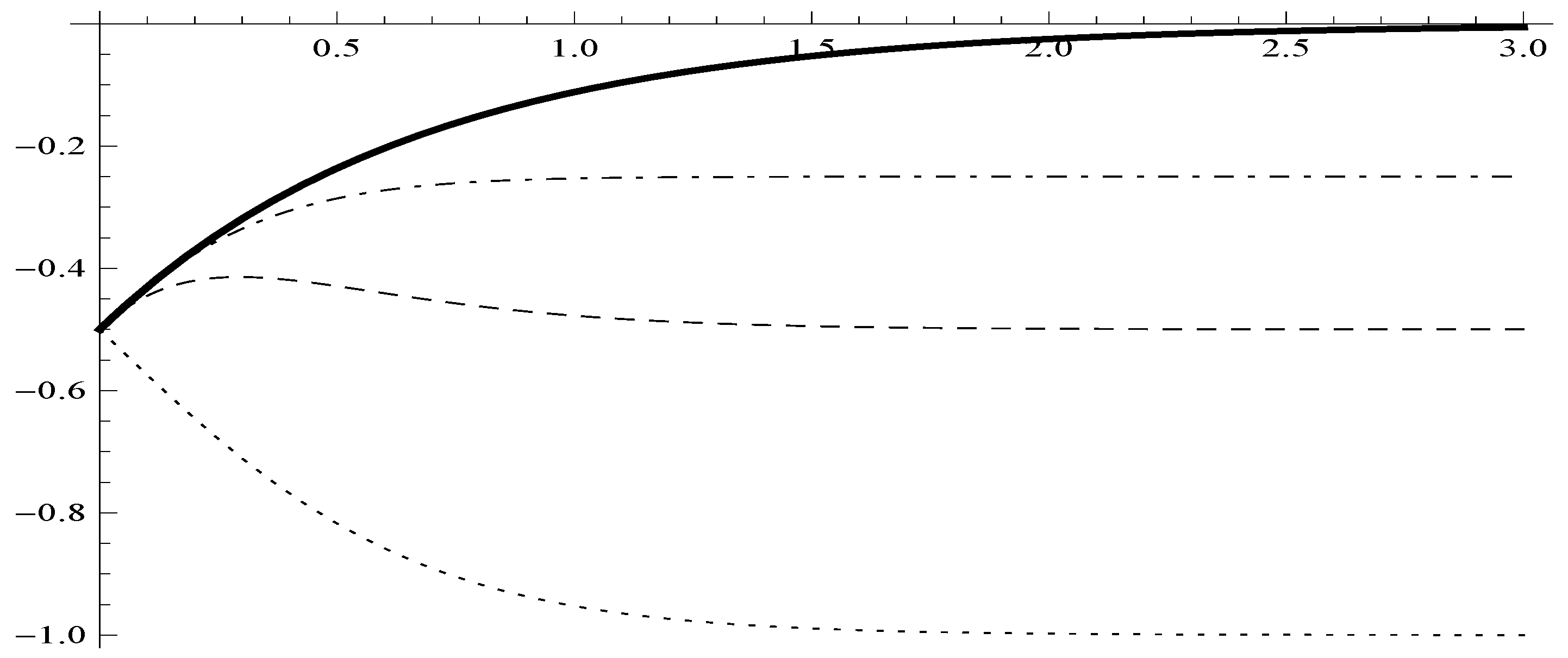

Example 1. Suppose that the d.f. F is an exponential distribution with density and the distribution of the inter-claim times is also an exponential distribution with density In this case, the associated moment generating functions are identical and given by Assuming , the solution of the equation gives , which is the adjustment coefficient, and then (4) gives . The probability of ruin for our example is and . In Figure 1 we illustrate the actual value of the quantity (solid line) and the performance of the bounds given by (19) (dashed line) and (20) (dot-dashed line), finally with dotted line we present the lower bound in (17) obtained by Psarrakos and Politis (2009a). 4.2. Bounds for the Ruin Probability under Aging Properties

For the rest of this section, let us assume that F is light-tailed, so that R exists.

In the next result, we improve the bound given in (

25), under the assumption of NWU (NBU) ladder heights. NWU (NBU) class is a subclass of NWUC (NBUC).

Proposition 3. If the d.f. F is NWU (NBU), then Proof. By

Psarrakos (

2008), we know that if the labber height d.f. F is NWU (NBU) then a lower (upper) bound for the tail of the deficit

is

Inserting the above inequality into (

6) and applying (

1) we obtain

Inserting the above inequality into (

16), we have

Then by (

5) and (

15), we derive that

Solving by

we obtain the upper (lower) bound in (

26). □

Another bound for the probability of ruin

, under the assumption of NWUC (NBUC) ladder heights, is given by

Psarrakos and Politis (

2009a), namely:

Inserting the above into (

28) and assuming NWU (NBU) ladder heights we have

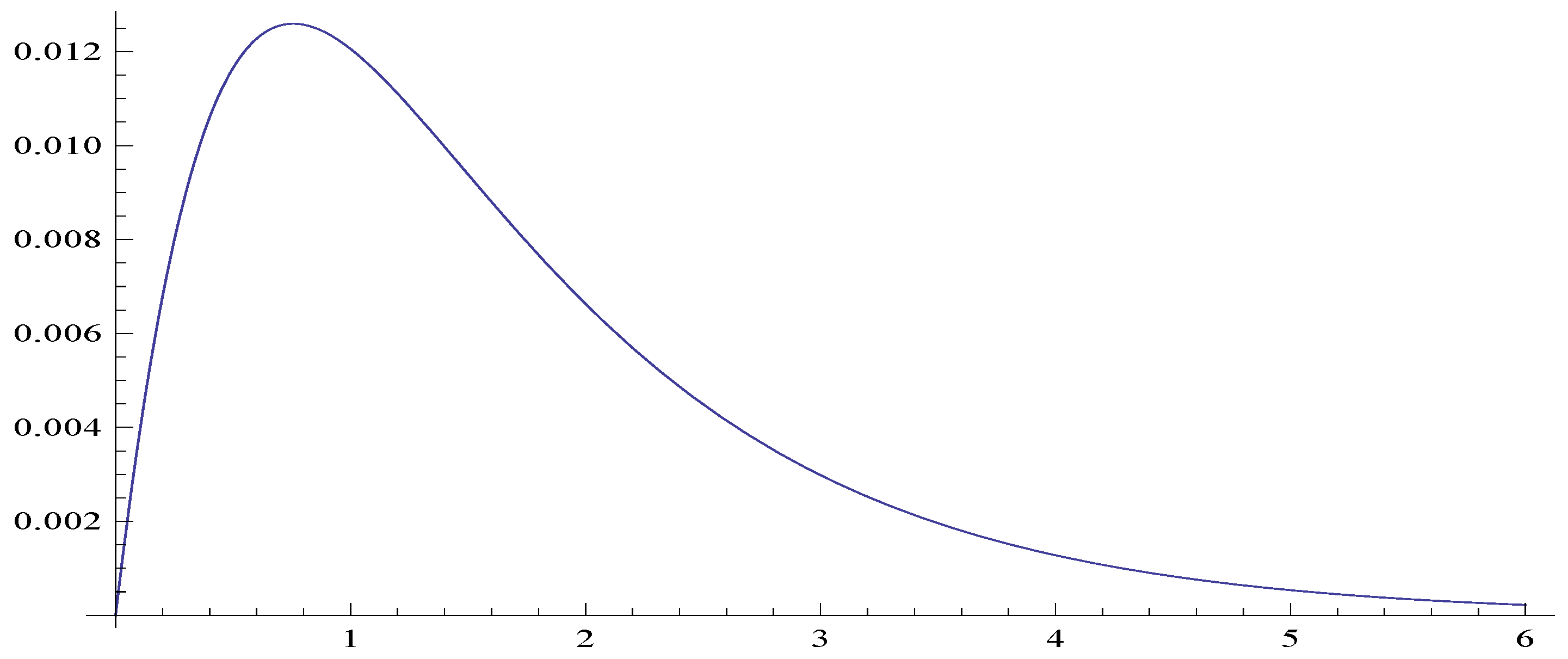

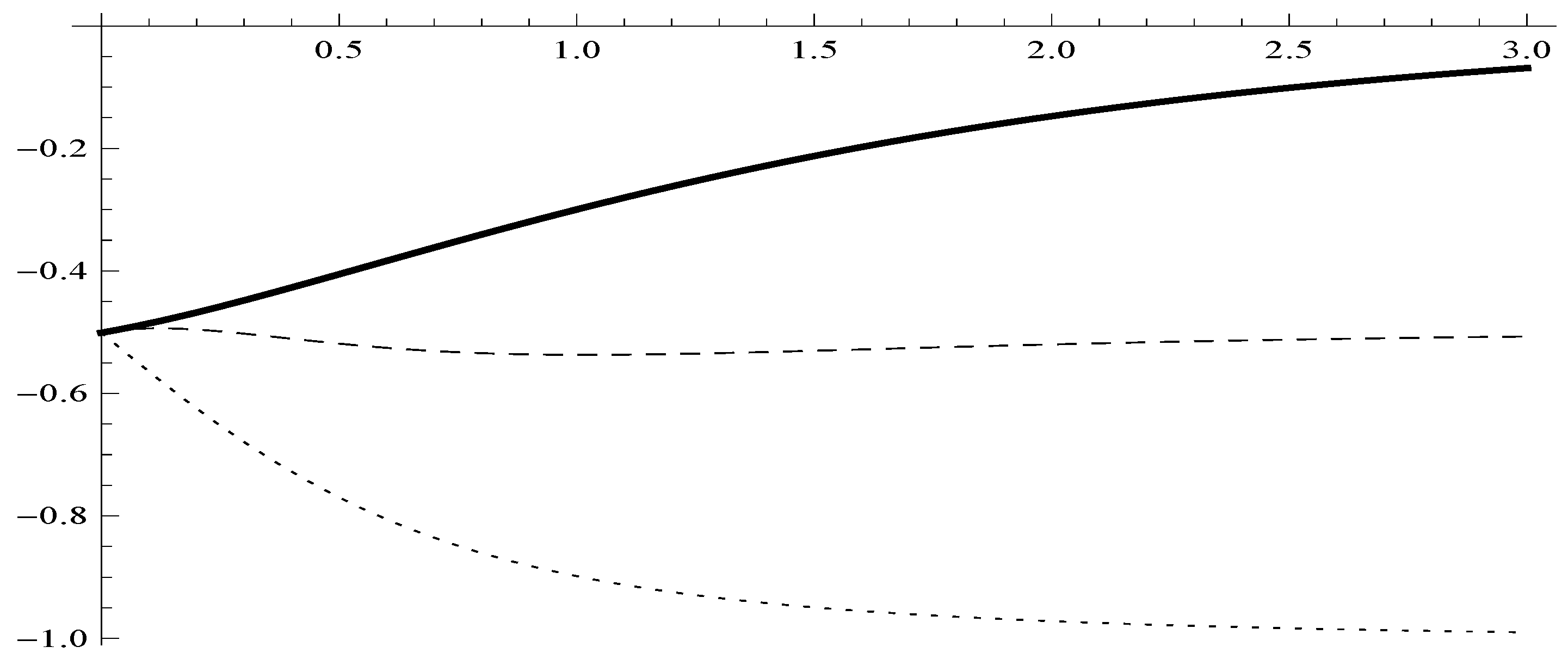

Example 2. Suppose that the claim amount distribution is a mixture of exponential distributions with density and the distribution of inter-claim times is an Erlang(2,2) distribution with density We also assume . In this case, the density of F is Because of (26) and (28) we note that our proposed bounds perform better than the one given by Willmot et al. (2001); Psarrakos and Politis (2009a) only when . In Lemma 4, we prove that the sign of the function is linked with NWU (NBU) ladder heights. The mixture of exponential is always DFR (Willmot and Lin (2001, p. 10)), so we expect for . Also, from (27) we expect for . In Figure 2 we depict the quantity . In the following Table 1 we present the values of the ruin probability and we compare it against and . Example 3. Let us consider the case where the claim amount distribution is a mixture of exponential distributions with density and the d.f. P of the inter-claim times is a Pareto distribution with density We also assume . In this case, we have In Figure 3 we illustrate the actual value of the quantity (solid line) and the performance of the bounds given by (19) (dashed line) and with the dotted line we present the lower bound in (17) obtained by Psarrakos and Politis (2009a). In the following Table 2 we present the values of the ruin probability and we compare it against and . In what follows, we present an upper bound for the probability of ruin under the condition that the ladder height d.f. F is IFR.

Proposition 4. If the d.f. F is IFR, then Proof. Let the ladder height d.f. F be IFR, then by

Willmot (

2002, Corollary 3.2) it holds that

Inserting the above into (

16) we obtain

Willmot (

2002) proves that

, where

In view of (

29) the above inequality could be written as

After some algebra and solving by completes the proof. □

4.3. Bounds for the Probability of Ruin When R Does Not Exist

Chadjiconstantinidis and Xenos (

2022) consider the random sum

is a d.f., where for the counting random variable

it holds

, and

is of d.f. with

By introducing the tail probability of the compound geometric sum

as follows:

they gave the following formula for the probability of ruin:

For convenience, we define

.

Chadjiconstantinidis and Xenos (

2022) gave bounds for the probability of ruin under the assumption of NBU and DFR ladder heights, in more detail: If the d.f.

F is DFR, then for any

it holds

and for any

while for the case of NBU ladder heights, the above bounds hold with the reverse inequality.

In what follows, we improve those bounds, regarding the aging class, by employing the bounds we introduced in

Section 4.2. Specifically, under the assumption that the d.f.

F is NWU (NBU) it holds

If

F is NWU (NBU), then

is NWU (NBU) (see

Chadjiconstantinidis and Xenos (

2022)) and references therein). Applying the above inequality to

, and by replacing

and

R with

,

we, respectively, obtain:

where

In view of (

34), (

31) and (

32) could be written as follows:

and for any

The above bounds are expressed in terms of the ladder height d.f. F. Although these are smoothly translated for the classical risk model in terms of the claim-size d.f. P, in the Sparre–Andersen model, the d.f. F of the ladder heights may not be available analytically. In this case bounds under assumptions regarding the claim-size d.f, P could be useful.

In the following result, we provide a refinement of the previously mentioned bound assuming that the claim-size distribution P is DFR.

Proposition 5. If the d.f. P is DFR, then for any it holds Proof. Szekli (

1986, Lemma 3.2) proves that if the claim-size d.f. P is DFR, then the same holds for the ladder-height d.f. F, thus F is NWU. Inserting (

33) into (

30) we obtain (

35). By letting

in (

35) we obtain (

36). □

Chadjiconstantinidis and Xenos (

2022) gave the following lower bound for the probability of ruin:

where

(for

) is the tail probability of a compound geometric sum. In more detail, it holds:

and for

they also prove that

where

Proposition 6. If the d.f. F is , then the ratio is nondecreasing.

Proof. Dividing (

37) by

we obtain:

Barlow and Proschan (

1996) prove that if

F is IFR, then for

,

is also

. Also,

Psarrakos and Politis (

2009b) prove that if a d.f.

F is

, then for any

, the quantity

is nondecreasing. Replacing

with

completes the proof. □

In view of (

3) and (

37) we note that

.

4.4. Concluding Remarks

In this paper, we first introduce a renewal-type equation for the difference , and using this result, we improve the Lundberg upper bound for the ruin probability by offering a general two-sided bound for the .

Next, using assumptions expressed in terms of the ladder height d.f.

F, we derive bounds for the probability of ruin, refining the ones previously obtained by

Willmot et al. (

2001). These results are based on the assumption that the d.f

F belongs to certain aging classes; however, in the Sparre–Andersen model,

F may not be available analytically. For this reason, in

Section 4.3, we offer bounds by making assumptions for the d.f

P of the claim size.

Someone might wonder about specific conditions needed for the d.f.

F to be DFR.

Szekli (

1986, Lemma 3.2), provided a sufficient condition for

F to be DFR. Specifically, if the d.f.

P is DFR, then

F is DFR. In the classical risk model, a weaker assumption is that if

P is IMRL, characterised by the condition that

is nondecreasing for

, then it follows that

F is DFR (see, e.g.,

Willmot and Lin (

2001)). In this case, the results of

Chadjiconstantinidis and Xenos (

2022) that assume DFR ladder heights, hold true by considering that the d.f.

P is IMRL.

{kind=link}

{kind=link}

{kind=link}