2.1. CAT Bond Pricing Model

This paper considers the pricing of catastrophe bonds due to a single disaster, where both the coupon and the principal are at risk in the case of a serious disaster. We refer to the main idea in

Chao and Zou (

2018) to consider a coupon-paying CAT bond triggered by

m dependent catastrophe indicators

. The investors may receive a portion of the coupon at the end of each year and a portion of the principal back at the maturity date. These proportions are determined by the accumulated excesses of the trigger indicators

over their attachment levels

. Different from

Chao and Zou (

2018), we incorporate a triple of quantities

to determine the step-wise coupon and principal triggered. The triple plays an important role in the pricing of the CAT bond, which depends on the stressful indicators vector

and the counting process of the disaster

, i.e., an integer-valued, non-negative, and non-decreasing stochastic process. We will develop a pricing mechanism reflecting both exceeding magnitude of the trigger indicators and its occurrence of the potential disaster below. We list all notations with explanations involved in

Table 1.

Supposing that the observations of the

m-dimensional indicator vector

are independent of the counting process

(

Chao and Zou 2018;

Goda 2021;

Ibrahim et al. 2022), we define the overall catastrophe risk severity in year

t as below:

where

, a component-wise, non-decreasing, non-negative, and right-continuous function defined on a filtered physical probability space. We make

f a general function so as to allow for different designs of CAT bonds. In general, we may suppose the coupon retention

to be the yearly average of the cumulative non-excess proportion caused by each disaster or its maxima as below.

- (i)

The average coupon retention proportion due to the disaster in year

t is modeled by

- (ii)

The maximum coupon retention proportion due to the disaster in year

t is modeled by

Remark 1. Note that each . The case with shows that in the jth disaster, all trigger indicators are below the attachment levels. The smaller is, the more likely indicator is to be far larger than its attachment level . It follows by the component-wise non-decreasing property of the function f that the is appropriate to quantify the coupon retention proportion.

To further trigger partial principal caused by multiple stressful indicators, i.e., more than one indicator being over its attachment level, we define the following two new indices

and

. Similar to

and the function

f in Equation (

1), we define

where

g and

h are two functions that are component-wise, non-decreasing, non-negative, and right-continuous functions from

to

. The following proposition gives the properties of

and

.

Proposition 1. Let be defined by Equations (1)–(3) and be in obtained by the three component-wise, non-decreasing, non-negative, and right-continuous functions from to . - (i)

It follows that range over . The case with (or ) implies that in the jth disaster, among all m trigger indicators, there are at least two (or three) indicators above its attachment levels simultaneously. Similar to , the values of and quantify the concurrent exceeding magnitude over its thresholds.

- (ii)

Quantitatively, we have . It follows further thatwhen the three functions , and h are taken as the same. - (iii)

It follows by the component-wise non-decreasing monotonicity of the functions , and h that the quantities are negatively associated with both the severity and the frequency of the disaster in the given year t.

Proposition 1 is key for our new pricing mechanism. The triple of resulting quantities

gives us the insight to trigger a partial coupon and principal when more indicators are triggered simultaneously. The proof of Proposition 1 is deferred to

Appendix A. We will design below the cashflow of a CAT bond based on Proposition 1. Suppose that the investor buys a CAT bond with a face value of

F in year

t and maturity in year

T. Denote by

the coupon paid in year

s and

the redemption value in year

T. We define

where

are defined by Equations (

1)–(

3) and

, the coupon paid according to a fixed coupon rate

R for a bond with the face value of

F. We can see from Equation (

4) that the coupon paid will be

times the initial coupon if there is at most one indicator triggered; otherwise, the principal will be wiped out and the coupon will be reduced accordingly. In this scenario, there are two cases: the first is that exactly two indicators are triggered simultaneously (i.e.,

), and the second is that at least three indicators are triggered simultaneously, i.e.,

. We differentiate these two cases with principal wipe-out by

and

, respectively. This measure safeguards the initial investment capital of investors by ensuring that a portion of the principal remains preserved (

Tang and Yuan 2019), thus increasing the investor’s interest in the investment of the CAT bond.

Remark 2. - (a)

We see that the coupon retained in year t is closely related to inter-annual variation of the catastrophe risks via the accumulative principal , as well as the intra-annual risk via with operational flexibility via the induction of functions , and h.

- (b)

Our trigger mechanism in Equation (4) with the hierarchical proportional coupon and principal paid out may attract more investors in comparison with the hybrid trigger mechanism given by Wei et al. (2022), since therein the current and future coupons will be paid out once one of the indicators is triggered and the principal at maturity will be completely wiped out once both indicators are triggered simultaneously.

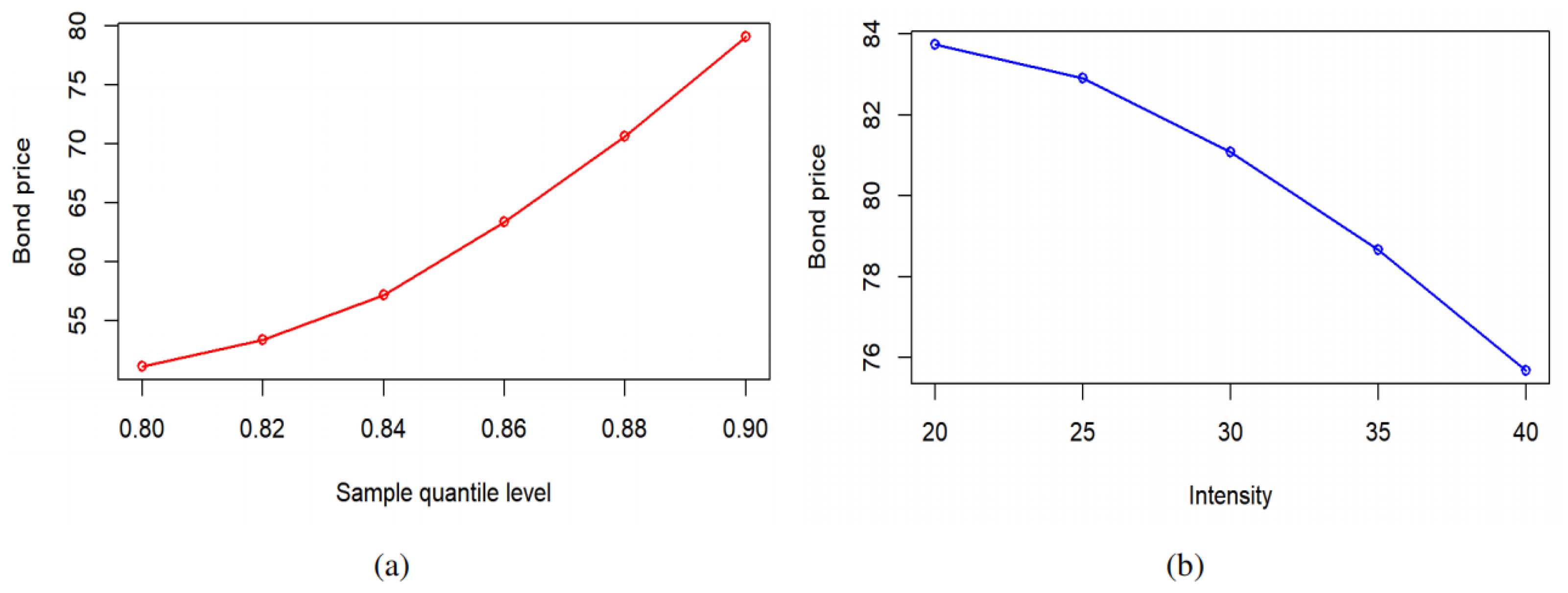

Finally, the price of the CAT bond, as the present value of all future cashflows, denoted by

, is given by

where

represents the discount factor at time

t of the zero-coupon bond with a redemption value of 1 at time

, given by

with interest rate process

. In the following, we consider a CIR model for the interest rate risk, which will lead to an explicit expression of the discount factor.

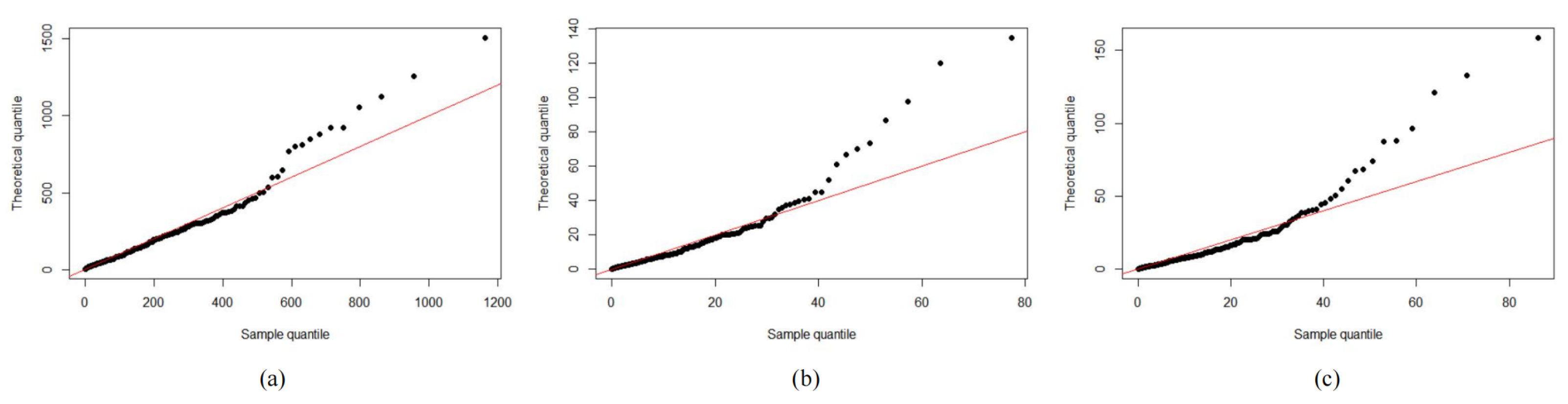

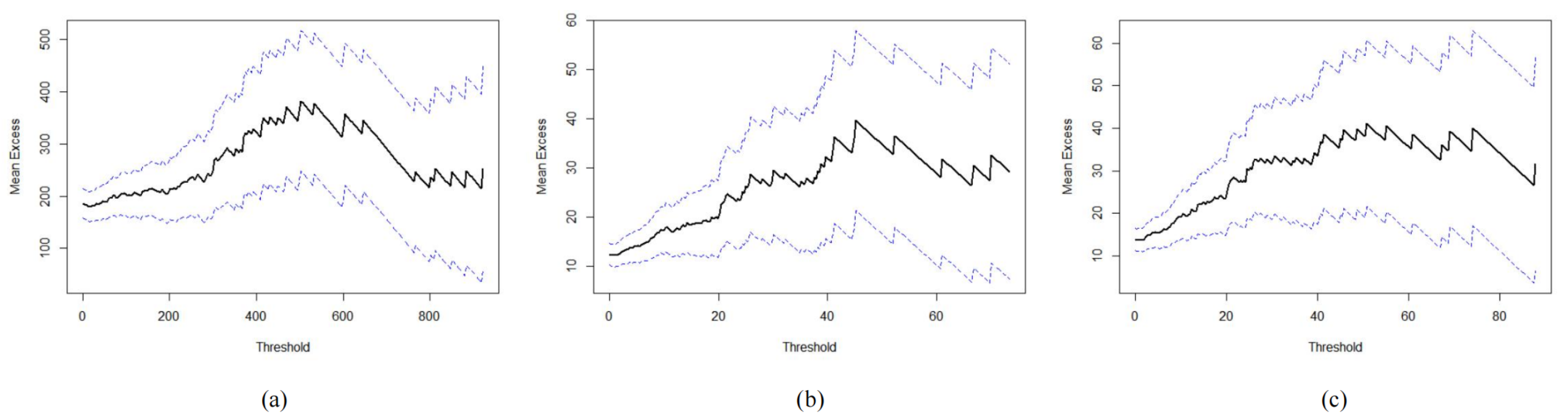

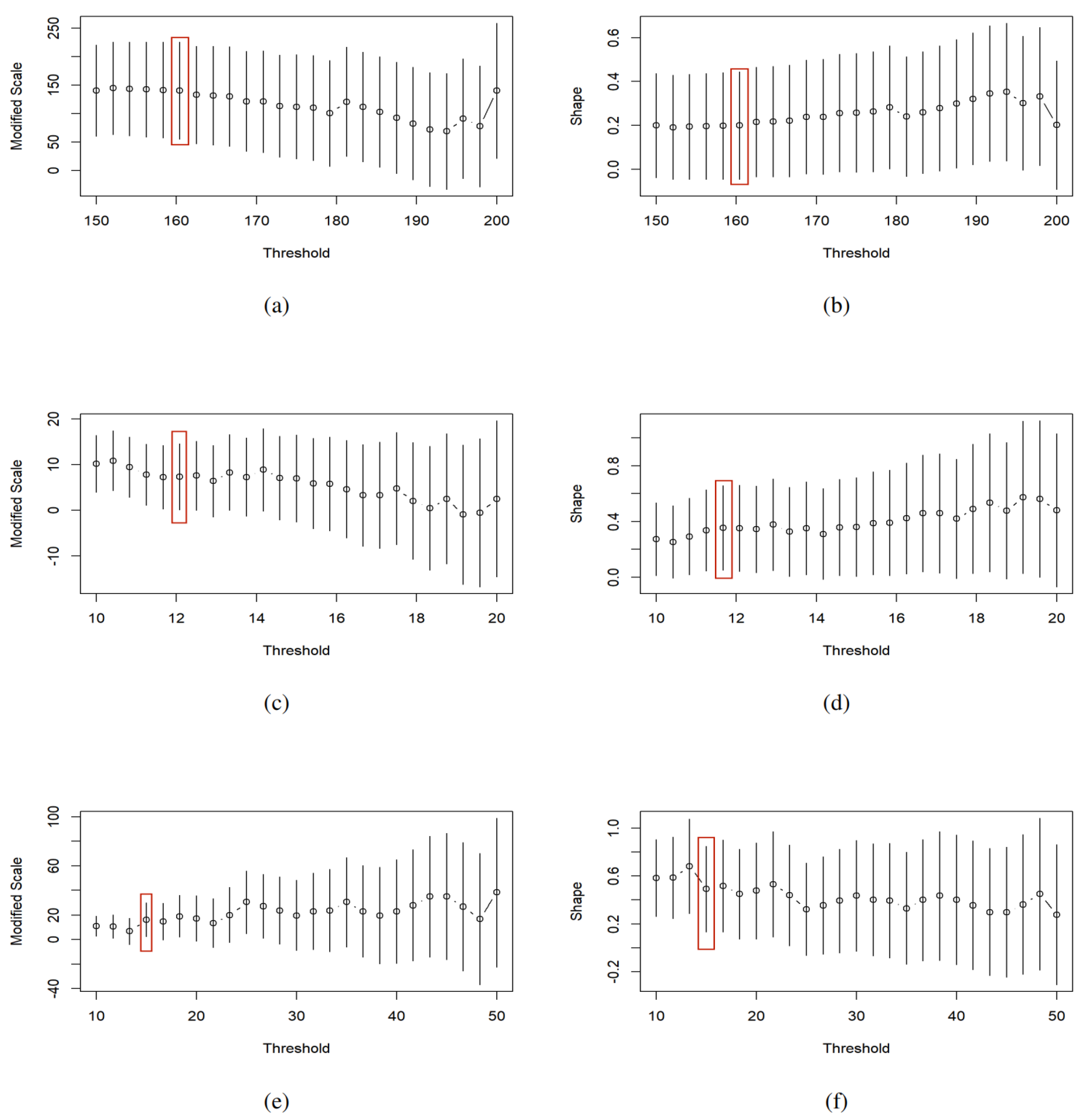

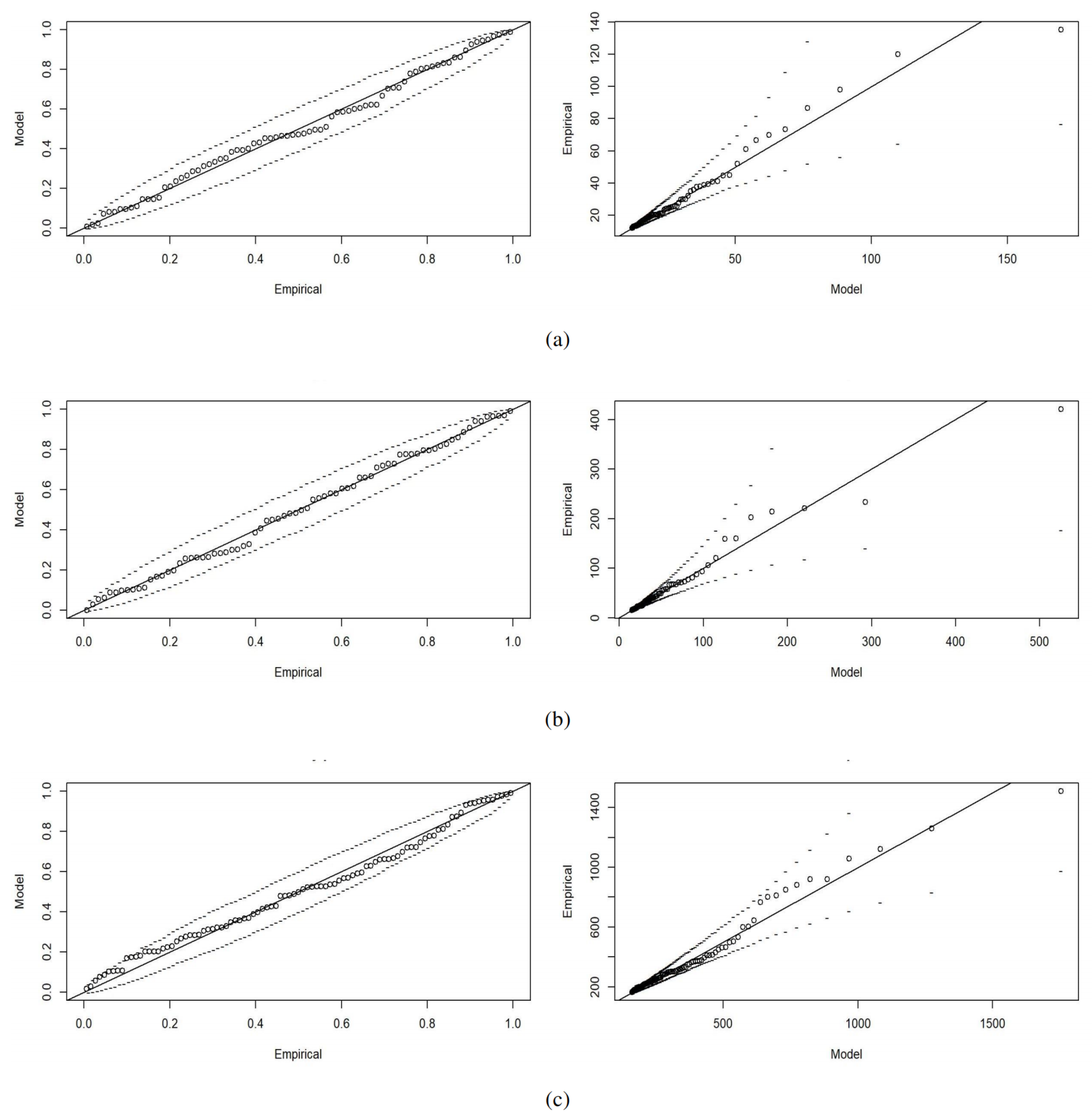

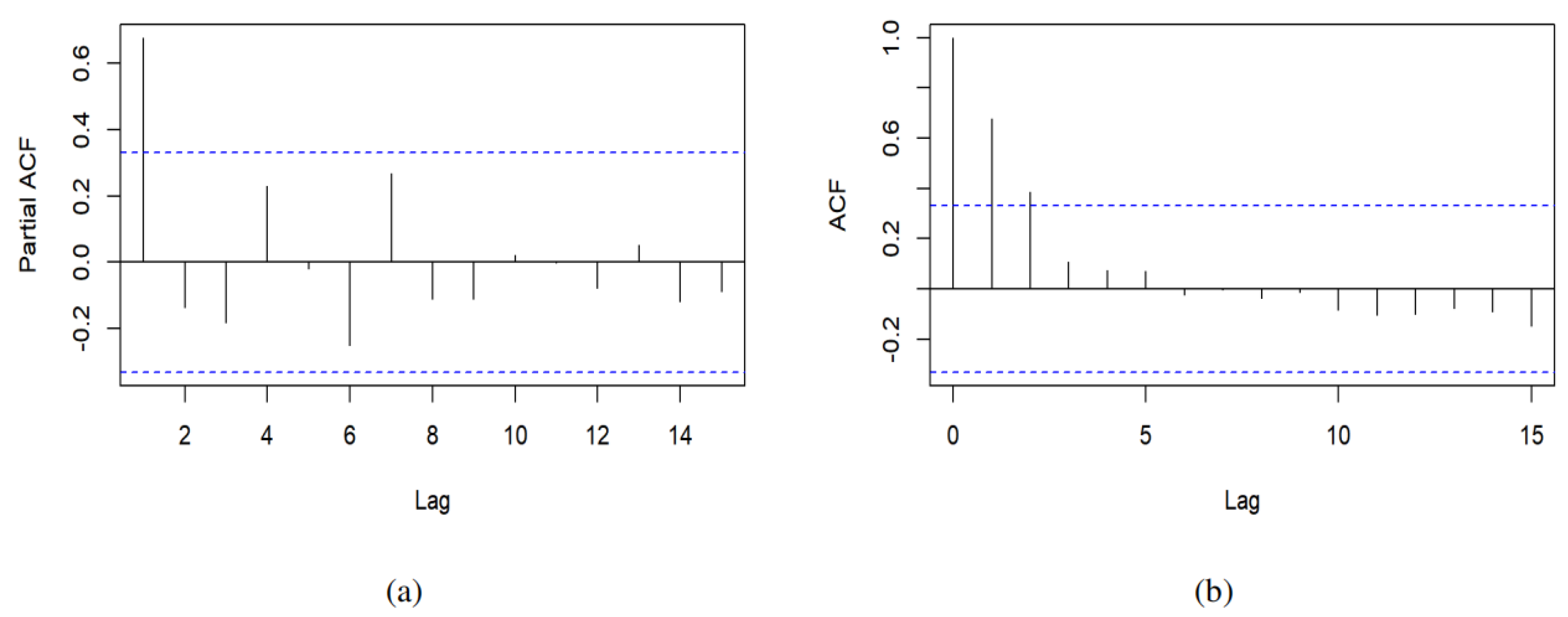

2.3. POT Model

The extreme value theory plays an important role in analysing statistical patterns of extreme-value events. There are two typical approaches to extract the extreme samples: the block maximum (BM) method and the peaks-over-threshold (POT) model. As the POT model can make full use of the extreme-value data in comparison with the BM model, it is widely used in the fields of insurance, hydrology, and finance (

Ma et al. 2021).

Suppose that

is a random sample from parent

, i.e., the

values are independent and identically distributed with a common distribution function (df)

. Given a threshold

u, the distribution

of the excess

is thus given by

For sufficiently high thresholds,

Pickands (

1975) pointed out that the distribution of the threshold-excess threshold

can be approximated by a generalized Pareto (GP) distribution

, i.e., for the right endpoint

Therefore, the tail distribution function

of

X can be approximated by

Here

and

are the shape and scale parameters of the GP distribution

. In practice, the exceedance probability

gives the insight into the potential risk. Its estimate can be obtained through the extrapolation approach via Equation (

7): we obtain the approximate tail probability of the GP model using the maximum likelihood estimation of

based on the excesses

with

exceeding the threshold

u and the estimate of

as

. Theoretically, the threshold

u can be determined by minimizing the mean square error of the Hill estimator of

, balancing the model bias and variance. A common graphical approach to the determination of the threshold is to check both the linearity of the empirical mean excess function

and its derived stable estimates of both scale and shape parameters.

2.4. Copula

The concept of a copula, proposed by

Abe (

1973), serves as a tool for describing the dependence structure among the marginal variables. Namely, for a joint distribution

with marginal df

for the

ith component, the copula

C is thus determined by

Table 2 lists common Archimedean copulas, including the Clayton, Gumbel, and Frank copulas, with a convex and decreasing generator

satisfying

. Its tail dependence is controlled by the parameter

and its copula is given by

Given the analytic tractability of Archimedean copulas, they are widely applied in insurance, finance, hydrology, survival analysis, etc. In this paper, we consider hierarchical (or nested) Archimedean copulas representing the different dependence among the components (

Hofert 2010). Namely, the nested Archimedean copula is of the form

where the inner and outer copulas could be one of the three Archimedean copulas in

Table 2. The tail dependence could be measured by the parameters

and

. As shown in

Charpentier and Segers (

2009), the larger

involved in the Gumbel, Clayton, or Frank copulas indicates a stronger dependence among these variables.

Combining the above pricing model and statistical model, this paper derives a rainstorm catastrophe bond. An empirical analysis together with a numerical analysis is given in

Section 3.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}