Measuring Systemic Governmental Reinsurance Risks of Extreme Risk Events

Abstract

:1. Introduction

2. Literature Review

3. Methodology

3.1. Systemic Excess Loss Reinsurance Model

3.2. Systemic Proportional Reinsurance

3.3. Monte Carlo Simulation

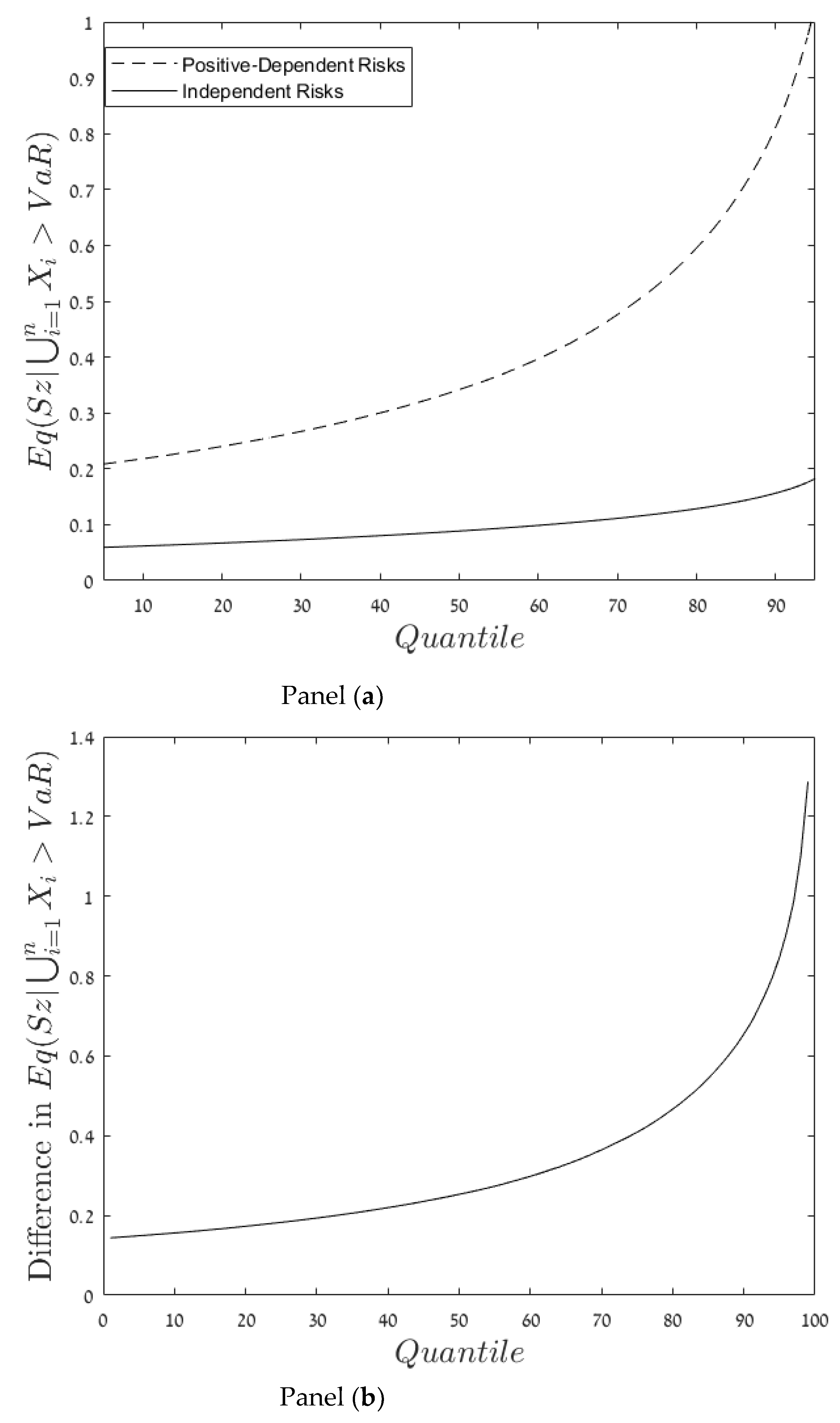

4. Results

5. Summary and Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Asimit, Alexandru Vali, Andrei Badescu, and Ka Chun Cheung. 2013a. Optimal reinsurance in the presence of counterparty default risk. Insurance: Mathematics and Economics 53: 690–97. [Google Scholar]

- Asimit, Alexandru Vali, Andrei Badescu, and Tim Verdonck. 2013b. Optimal risk transfer under quantile-based risk measurers. Insurance: Mathematics and Economics 53: 252–65. [Google Scholar] [CrossRef] [Green Version]

- Berger, Lawrence, David Cummins, and Sharon Tennyson. 1992. Reinsurance and the liability insurance crisis. Journal of Risk and Uncertainty 5: 253–72. [Google Scholar] [CrossRef]

- Bernard, Carole, Fangda Liu, and Steven Vanduffel. 2020. Optimal Insurance in the Presence of Multiple Policyholders. Journal of Economic Behavior and Organization 180: 638–656. [Google Scholar] [CrossRef]

- Bernard, Carol, and Mike Ludkovski. 2012. Impact of counterparty risk on the reinsurance market. North American Actuarial Journal 16: 87–111. [Google Scholar] [CrossRef]

- Boonen, Tim J. 2017. Solvency II solvency capital requirement for life insurance companies based on expected shortfall. European Actuarial Journal 7: 405–34. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Boonen, Tim J., and Wenjun Jiang. 2022. Mean–variance insurance design with counterparty risk and incentive compatibility. ASTIN Bulletin: The Journal of the IAA 52: 645–67. [Google Scholar] [CrossRef]

- Cai, Jun, and Yichun Chi. 2020. Optimal reinsurance designs based on risk measures: A review. Statistical Theory and Related Fields 4: 1–13. [Google Scholar] [CrossRef]

- Cai, Jun, Christiane Lemieux, and Fnagda Liu. 2014. Optimal reinsurance with regulatory initial capital and default risk. Insurance: Mathematics and Economics 57: 13–24. [Google Scholar] [CrossRef]

- Cai, Jun, and Ken Seng Tan. 2007. Optimal retention for a stop-loss reinsurance under the VaR and CTE risk measures. ASTIN Bulletin: The Journal of the IAA 37: 93–112. [Google Scholar] [CrossRef] [Green Version]

- Cai, Jun, Ken Seng Tan, Chengguo Weng, and Yi Zhang. 2008. Optimal reinsurance under VaR and CTE risk measures. Insurance: Mathematics and Economics 43: 185–96. [Google Scholar] [CrossRef]

- Cai, Jun, Ying Wang, and Tiantian Mao. 2017. Tail subadditivity of distortion risk measures and multivariate tail distortion risk measures. Insurance: Mathematics and Economics 75: 105–16. [Google Scholar] [CrossRef]

- Cai, Jun, and Wei Wei. 2012. Optimal reinsurance with positively dependent risks. Insurance: Mathematics and Economics 50: 57–63. [Google Scholar] [CrossRef]

- Chang, Chia Chien, Jen Wei Yang, and Min The Yu. 2018. Hurricane risk management with climate and CO2 indices. Journal of Risk and Insurance 85: 695–720. [Google Scholar] [CrossRef]

- Chen, Yiqing, and Kam C. Yuen. 2012. Precise large deviations of aggregate claims in a size-dependent renewal risk model. Insurance: Mathematics and Economics 51: 457–61. [Google Scholar] [CrossRef]

- Cheung, Ka Chun. 2010. Optimal reinsurance revisited—A geometric approach. ASTIN Bulletin: The Journal of the IAA 40: 221–39. [Google Scholar] [CrossRef] [Green Version]

- Cheung, Ka Chun, K. C. J. Sung, and S. C. Philip Yam. 2014. Risk-Minimizing Reinsurance Protection for Multivariate Risks. Journal of Risk and Insurance 81: 219–36. [Google Scholar] [CrossRef]

- Chi, Yichun. 2012. Optimal reinsurance under variance related premium principles. Insurance: Mathematics and Economics 51: 310–21. [Google Scholar] [CrossRef]

- Chi, Yichun, and Ken Seng Tan. 2011. Optimal reinsurance under VaR and CVaR risk measures: A simplified approach. ASTIN Bulletin: The Journal of the IAA 41: 487–509. [Google Scholar]

- Chi, Yichun, and Chengguo Weng. 2013. Optimal reinsurance subject to Vajda condition. Insurance: Mathematics and Economics 53: 179–89. [Google Scholar] [CrossRef]

- Cummins, John David, Georges Dionne, Robert Gagné, and Abdelhakim Nouira. 2021. The costs and benefits of reinsurance. Geneva Papers on Risk and Insurance-Issues and Practice 46: 177–99. [Google Scholar] [CrossRef]

- Cummins, John David, David Lalonde, and Richard D. Phillips. 2004. The basis risk of catastrophic-loss index securities. Journal of Financial Economics 71: 77–111. [Google Scholar] [CrossRef] [Green Version]

- Cummins, John David, and Philippe Trainar. 2009. Securitization, insurance, and reinsurance. Journal of Risk and Insurance 76: 463–92. [Google Scholar] [CrossRef]

- Denuit, Michel, and Catherine Vermandele. 1998. Optimal reinsurance and stop-loss order. Insurance: Mathematics and Economics 22: 229–33. [Google Scholar] [CrossRef]

- Dhaene, Jan, Steven Vanduffel, Marc. J. Goovaerts, Rob Kaas, Qihe Tang, and David Vyncke. 2006. Risk measures and comonotonicity: A review. Stochastic Models 22: 573–606. [Google Scholar] [CrossRef] [Green Version]

- Drexler, Alejandro, and Richard Rosen. 2022. Exposure to catastrophe risk and use of reinsurance: An empirical evaluation for the US. The Geneva Papers on Risk and Insurance-Issues and Practice 47: 103–24. [Google Scholar] [CrossRef]

- Froot, Kenneth A. 2007. Risk management, capital budgeting, and capital structure policy for insurers and reinsurers. Journal of Risk and Insurance 74: 273–99. [Google Scholar] [CrossRef] [Green Version]

- Huang, Hung His. 2006. Optimal insurance contract under a value-at-risk constraint. Geneva Risk and Insurance Review. 31: 91–110. [Google Scholar] [CrossRef] [Green Version]

- Kaluszka, Marek, and Anrzej Okolewski. 2008. An extension of Arrow’s result on optimal reinsurance contract. Journal of Risk and Insurance 75: 275–88. [Google Scholar] [CrossRef]

- Landsman, Zinoviy, Udi Makov, and Tomer Shushi. 2016. Multivariate tail conditional expectation for elliptical distributions. Insurance: Mathematics and Economics 70: 216–23. [Google Scholar] [CrossRef]

- Lienhard, Stephen. 2023. Multivariate Lognormal Simulation with Correlation, MATLAB Central File Exchange. Available online: https://www.mathworks.com/matlabcentral/fileexchange/6426-multivariate-lognormal-simulation-with-correlation (accessed on 16 January 2023).

- Mao, Tiantian, and Jun Cai. 2018. Risk measures based on behavioural economics theory. Finance and Stochastics 22: 367–393. [Google Scholar] [CrossRef]

- Nowak, Piotr, and Maciej Romaniuk. 2013. Pricing and simulations of catastrophe bonds. Insurance: Mathematics and Economics 52: 18–28. [Google Scholar] [CrossRef]

- Powell, Lawrence Skinner, and David William Sommer. 2007. Internal versus external capital markets in the insurance industry: The role of reinsurance. Journal of Financial Services Research 31: 173–88. [Google Scholar] [CrossRef]

- Verlaak, Robert, and Jan Beirlant. 2003. Optimal reinsurance programs: An optimal combination of several reinsurance protections on a heterogeneous insurance portfolio. Insurance: Mathematics and Economics 33: 381–403. [Google Scholar]

- Wang, Ching Ping, David Shyu, and Hong His Huang. 2005. Optimal insurance design under a value-at-risk framework. Geneva Risk and Insurance Review 30: 161–79. [Google Scholar] [CrossRef]

- Zhao, Yang, Jin Ping Lee, and Min The Yu. 2021. Catastrophe risk, reinsurance and securitized risk-transfer solutions: A review. China Finance Review International 11: 449–73. [Google Scholar] [CrossRef]

- Zhou, Chunyang, and Chongfeng Wu. 2009. Optimal insurance under the insurer’s VaR constraint. Geneva Risk and Insurance Review 34: 140–54. [Google Scholar] [CrossRef] [Green Version]

- Zhu, Yunzhou, Yichun Chi, and Chengguo Weng. 2014. Multivariate reinsurance designs for minimizing an insurer’s capital requirement. Insurance: Mathematics and Economics 59: 144–55. [Google Scholar] [CrossRef]

{kind=link}

| Risk 1 | Risk 2 | Risk 3 | Risk 4 | Risk 5 | Risk 6 | Risk 7 | Risk 8 | Risk 9 | Risk 10 |

|---|---|---|---|---|---|---|---|---|---|

| 1.000 | 0.904 | 0.890 | 0.920 | 0.885 | 0.924 | 0.932 | 0.929 | 0.901 | 0.903 |

| 0.904 | 1.000 | 0.895 | 0.859 | 0.865 | 0.889 | 0.893 | 0.945 | 0.938 | 0.859 |

| 0.890 | 0.895 | 1.000 | 0.903 | 0.909 | 0.918 | 0.939 | 0.883 | 0.909 | 0.861 |

| 0.920 | 0.859 | 0.903 | 1.000 | 0.876 | 0.920 | 0.889 | 0.917 | 0.865 | 0.864 |

| 0.885 | 0.865 | 0.909 | 0.876 | 1.000 | 0.894 | 0.927 | 0.894 | 0.870 | 0.918 |

| 0.924 | 0.889 | 0.918 | 0.920 | 0.894 | 1.000 | 0.890 | 0.933 | 0.891 | 0.900 |

| 0.932 | 0.893 | 0.939 | 0.889 | 0.927 | 0.890 | 1.000 | 0.927 | 0.925 | 0.869 |

| 0.929 | 0.945 | 0.883 | 0.917 | 0.894 | 0.933 | 0.927 | 1.000 | 0.933 | 0.900 |

| 0.901 | 0.938 | 0.909 | 0.865 | 0.870 | 0.891 | 0.925 | 0.933 | 1.000 | 0.865 |

| 0.903 | 0.859 | 0.861 | 0.864 | 0.918 | 0.900 | 0.869 | 0.900 | 0.865 | 1.000 |

| Percentile | Risk 1 | Risk 2 | Risk 3 | Risk 4 | Risk 5 | Risk 6 | Risk 7 | Risk 8 | Risk 9 | Risk 10 |

|---|---|---|---|---|---|---|---|---|---|---|

| Independent insurance claims | ||||||||||

| 10% | 0.005 | 0.008 | 0.010 | 0.005 | 0.005 | 0.005 | 0.007 | 0.006 | 0.003 | 0.006 |

| 25% | 0.006 | 0.010 | 0.011 | 0.006 | 0.006 | 0.006 | 0.008 | 0.007 | 0.003 | 0.007 |

| 50% | 0.008 | 0.012 | 0.014 | 0.008 | 0.008 | 0.007 | 0.010 | 0.009 | 0.004 | 0.009 |

| 75% | 0.010 | 0.016 | 0.019 | 0.011 | 0.010 | 0.010 | 0.014 | 0.012 | 0.005 | 0.012 |

| 90% | 0.013 | 0.021 | 0.024 | 0.014 | 0.013 | 0.013 | 0.018 | 0.016 | 0.007 | 0.015 |

| Positive-Dependent insurance claims | ||||||||||

| 10% | 0.019 | 0.030 | 0.034 | 0.019 | 0.019 | 0.018 | 0.025 | 0.022 | 0.010 | 0.022 |

| 25% | 0.022 | 0.035 | 0.039 | 0.022 | 0.022 | 0.021 | 0.029 | 0.026 | 0.012 | 0.025 |

| 50% | 0.030 | 0.047 | 0.053 | 0.030 | 0.029 | 0.029 | 0.040 | 0.035 | 0.016 | 0.034 |

| 75% | 0.047 | 0.072 | 0.082 | 0.046 | 0.045 | 0.045 | 0.062 | 0.055 | 0.024 | 0.051 |

| 90% | 0.072 | 0.109 | 0.126 | 0.070 | 0.069 | 0.069 | 0.096 | 0.086 | 0.036 | 0.078 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Hadad, E.; Shushi, T.; Yosef, R. Measuring Systemic Governmental Reinsurance Risks of Extreme Risk Events. Risks 2023, 11, 50. https://doi.org/10.3390/risks11030050

Hadad E, Shushi T, Yosef R. Measuring Systemic Governmental Reinsurance Risks of Extreme Risk Events. Risks. 2023; 11(3):50. https://doi.org/10.3390/risks11030050

Chicago/Turabian StyleHadad, Elroi, Tomer Shushi, and Rami Yosef. 2023. "Measuring Systemic Governmental Reinsurance Risks of Extreme Risk Events" Risks 11, no. 3: 50. https://doi.org/10.3390/risks11030050