Pricing Pandemic Bonds under Hull–White & Stochastic Logistic Growth Model

Abstract

:1. Introduction

2. Literature Review

3. The World Bank Issued Pandemic Bond

4. The Future of Pandemic Bonds

5. Materials and Methods

5.1. Proposed CAT Bond

5.2. Trigger

5.2.1. Trigger of World Bank Issued Pandemic Bond

- Total confirmed deaths should be greater than or equal to 2500.

- The rolling total case () amount must be greater than or equal to 250.

- The growth rate () must be positive.

5.2.2. Trigger of Our Model

- The seven-day moving average(MA) for daily new death, , should exceed before the bond maturity time T AND

- At the time when the seven-day moving average for the daily new death, , exceeds , the seven-day moving average for the daily new infection, , should exceed AND

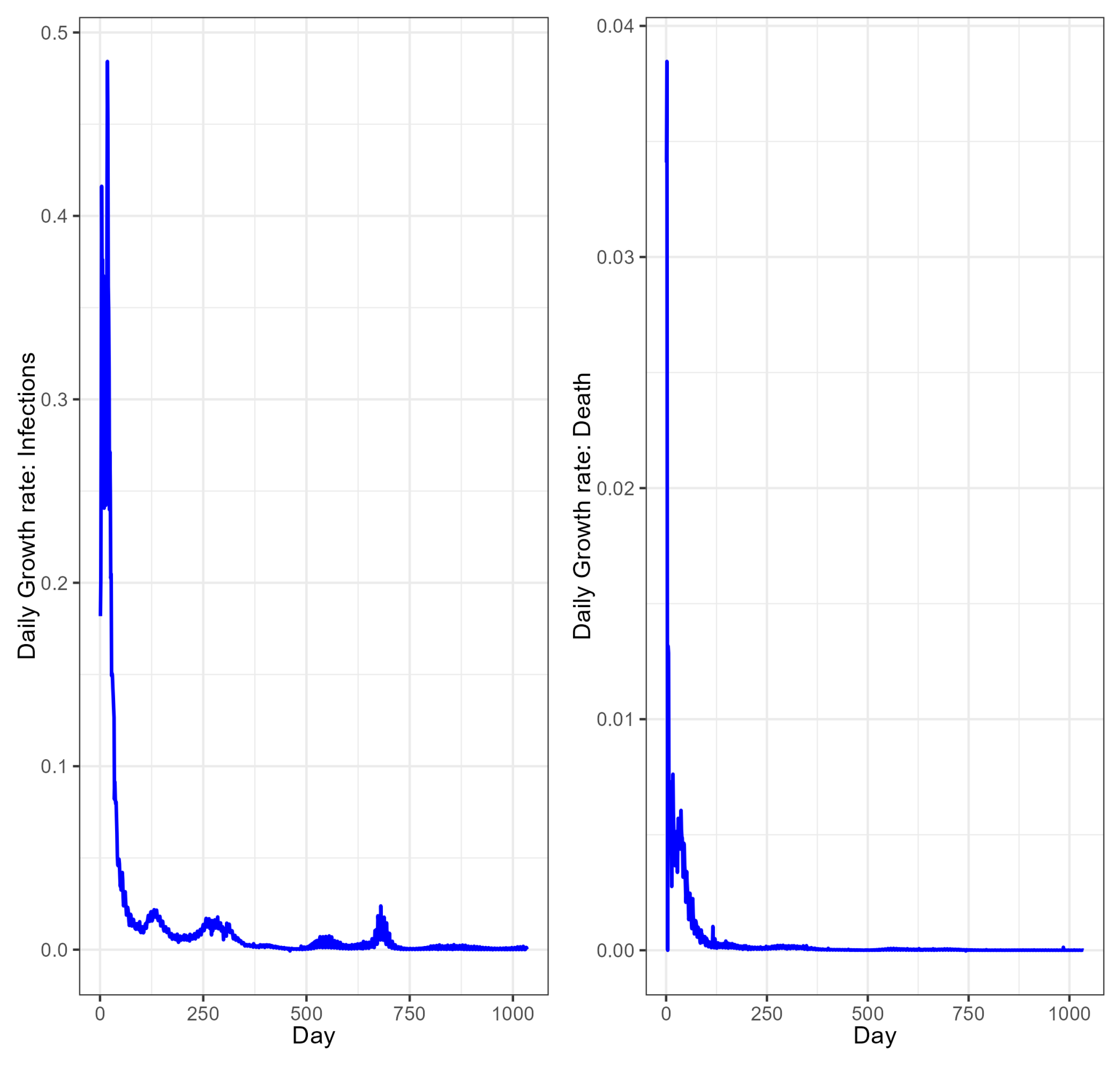

- When seven-day average for the daily new death exceeds and the seven-day average for the daily new infection exceeds , the growth rate, , need to be positive. The outbreak growth rate is defined using the following equation.where stands for the average of daily new infection cases for the past seven days, and stands for the standard deviation of new infection cases for the past seven days.

5.3. Interest Rate Process

Calibration vs. MLE Estimation of Parameters of Hull–White Model

5.4. Payout Structure

5.5. Pricing Model

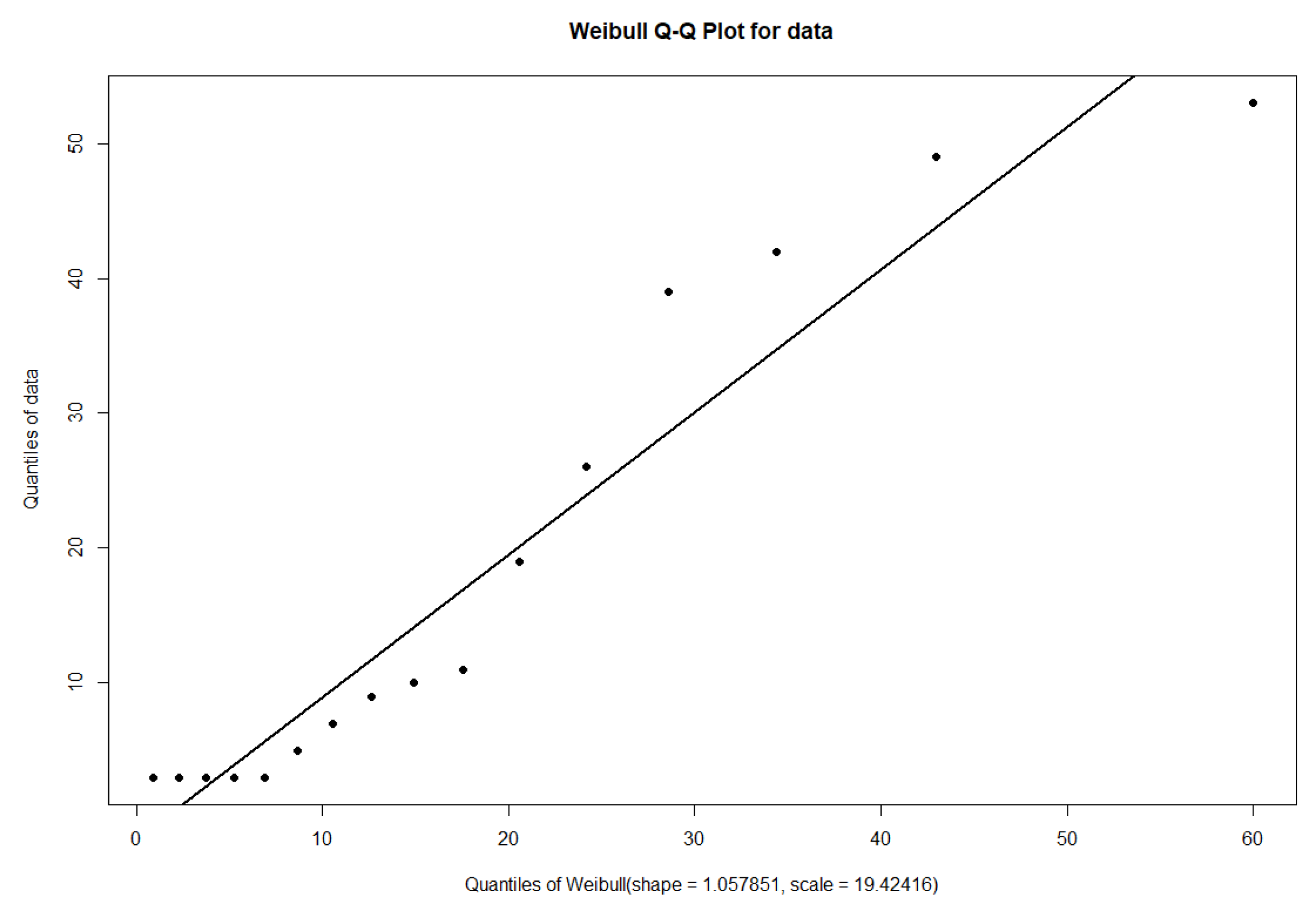

5.6. Probability Distribution for the Pandemic Risk

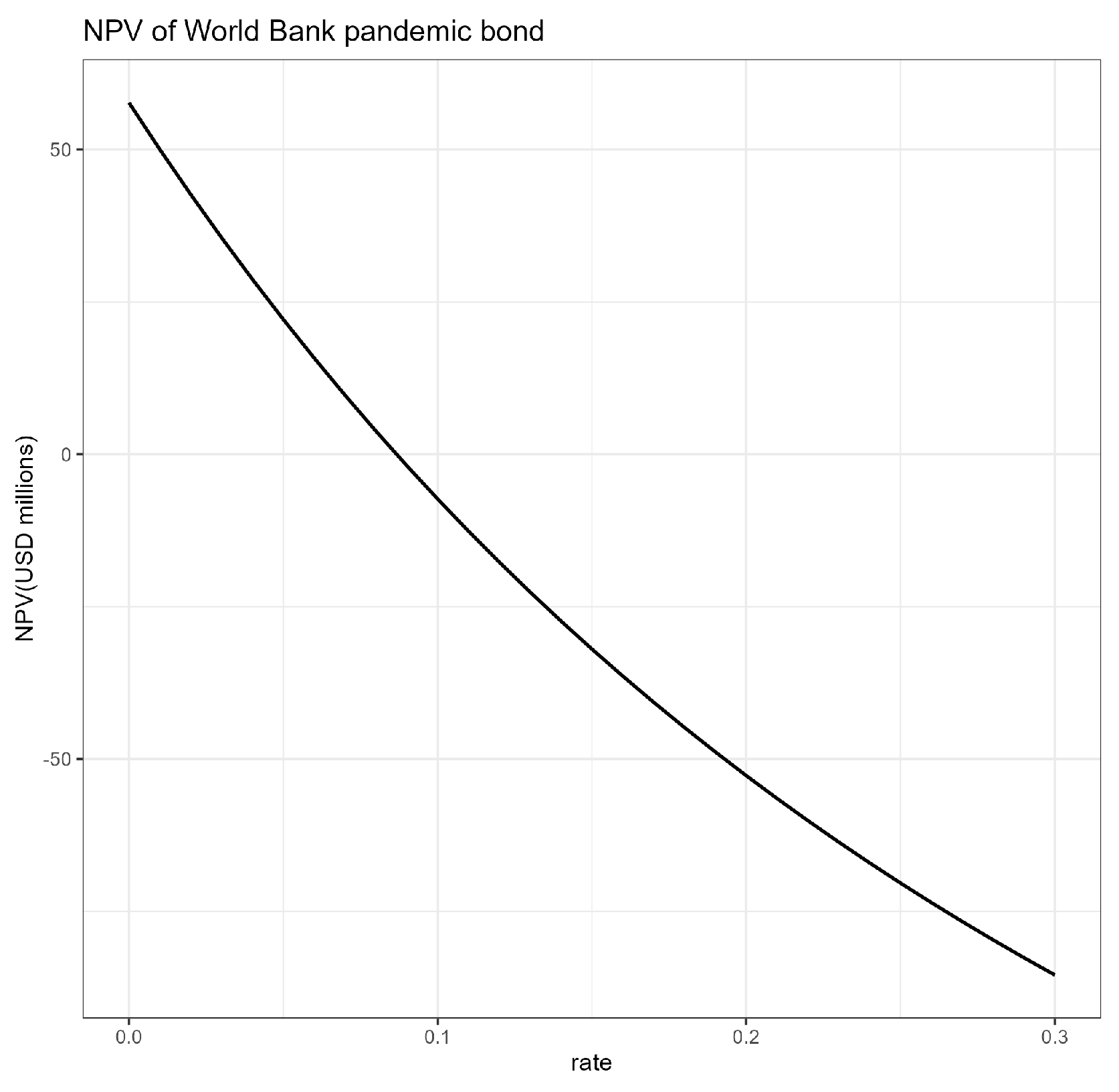

5.7. Pandemic Bond Price

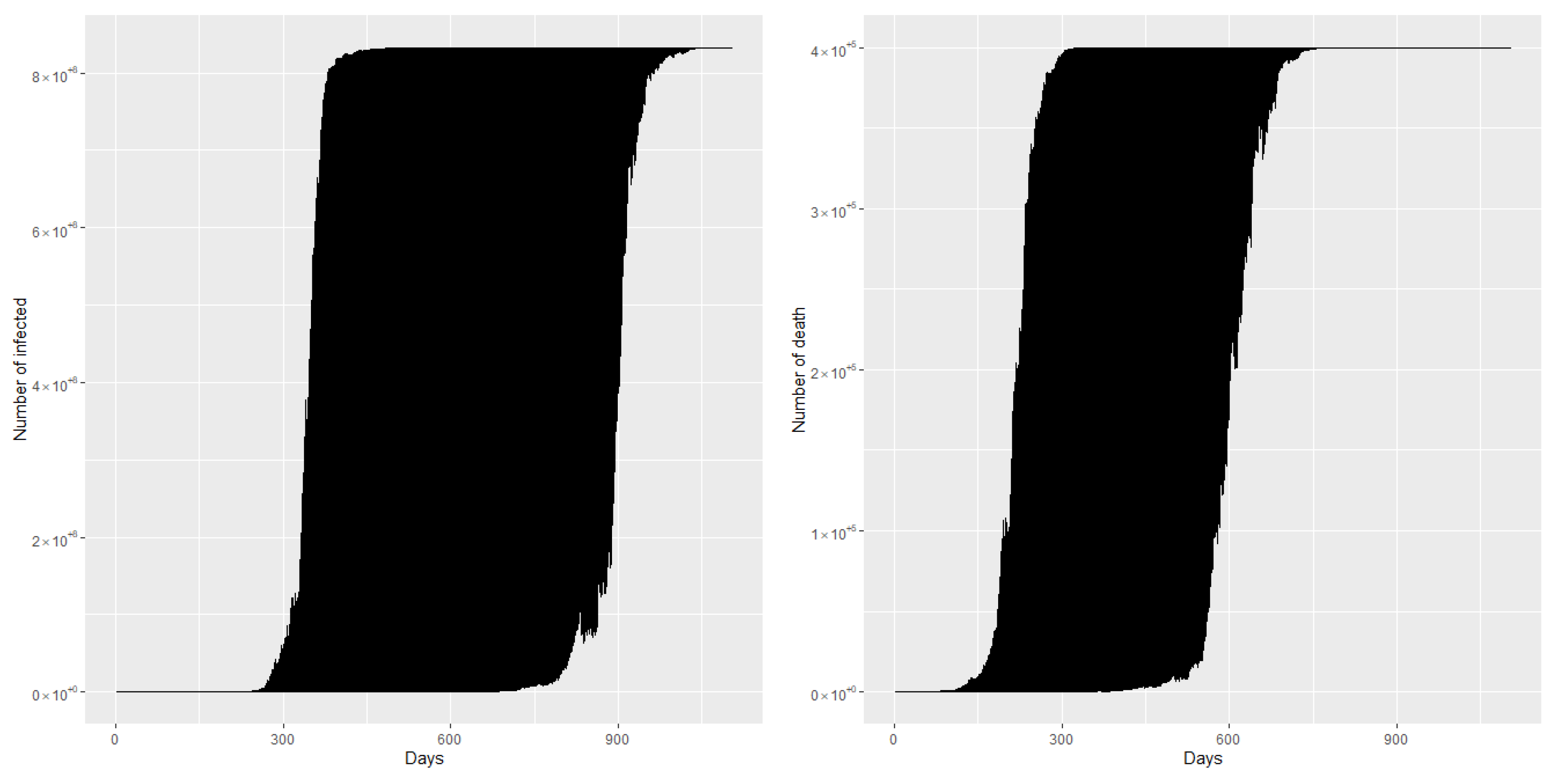

6. Stochastic Logistic Growth Model

The Model

- The zero solution is globally asymptotically stable almost surely if

- The positive equilibrium solution K is globally asymptotically stable almost surely if

7. Numerical Simulation 1

7.1. Bond Coupons

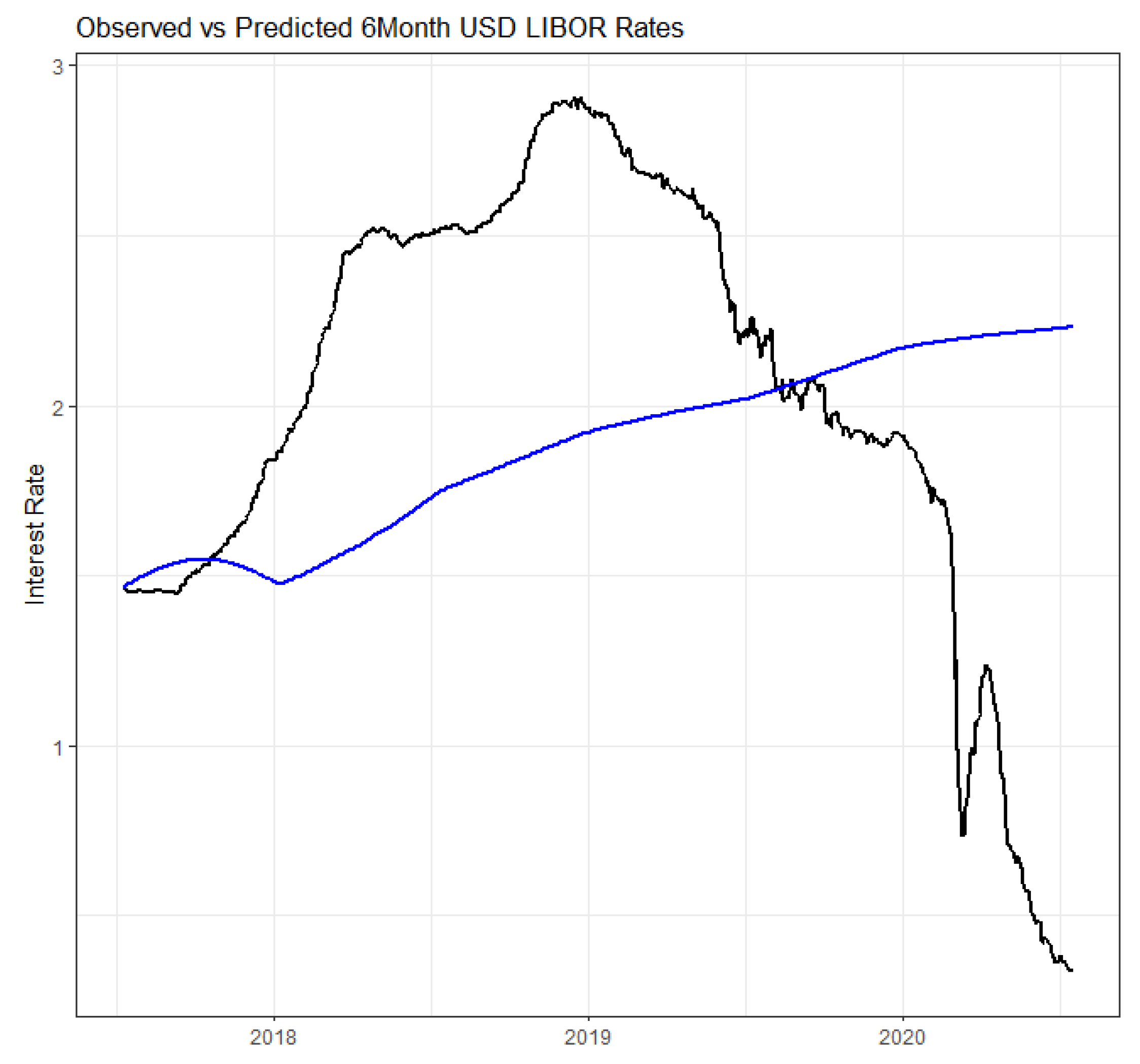

- Model Calibration: In order to calibrate the Hull–White one-factor model, both the term structure of spot rates and implied volatilities are required. Unlike some other interest rate models, which uses historical series data to calculate parameters, the Hull–White model utilizes cross-sectional data from a single point in time Kladívko and Rusý (2023) to calibrate the model. For our calibration, we utilized LIBOR spot rates with various tenors (1D, 1W, 1M, 2M, 3M, and 6M) on July 7, 2017, as well as ICE Swap rates with tenors (1Y, 2Y, 3Y, 4Y, 5Y, 6Y, 7Y, 8Y, 9Y, 10Y, and 15Y) to obtain the full term structure of interest rates for that date ICE Benchmark Administration (2023). Normally, implied volatilities for 7 July 2017 would be obtained using interest rate derivatives such as swaptions. However, since we lack access to these data, we derived historical volatilities from forward rate curves constructed using daily ICE Swap rate curves from 14 August 2014 to 7 July 2017. These historical volatilities were used in place of implied volatilities. The parameter in Equation (8) was established as , based on the values in Table 5 for 2014, 2015, and 2016 in Kladívko and Rusý (2023).

- Simulation: Post-calibration, the model is employed to simulate short rates (instantaneous interest rates at specific points in time) 5000 times within the designated time interval. Our focus lies on the 6-month USD LIBOR rates. For each simulated short rate path, we can obtain the short rate values for the subsequent 6 months and compute the average rate during that period. This average rate can be called as the approximated 6M USD LIBOR rate for that particular date within that path. Since we possess 5000 such rates for that date (derived from 5000 sample paths), we once again calculate the average. This average is considered as the 6M USD LIBOR rate for that date, utilized for subsequent computations. When simulating paths, we assumed that an year is 252 days (trading days) and used 126 days for 6 months.

7.2. Probability of a Pandemic Event

7.3. Trigger Event

| Algorithm 1 The algorithm to calculate bond price under the 2009 H1N1 Influenza pandemic scenario | |

| Require: Predicted bond coupon payments | ▹ see Section 7.1 and Table 3 |

| Require: Investors expected annual return rate y (calculated as 8.2837%) | ▹ see |

| Equation (32) | |

| ▹ see Table 4 | |

| ▹ see Table 4 | |

| ▹ see Table 4 | |

| ▹ we set both rates to be same, since it is not possible to calculate without | |

| real data | |

| ▹ we set both rates to be same | |

| ▹ time step of the simulation is set to 1 day | |

| ▹ Number of steps. This is the number of days between 7 July 2017–15 July 2020. | |

| ▹ This is the trigger for number of infected | |

| ▹ This is the trigger for number of death | |

| ▹ and are correlated stochastic processes. See Equation (29) | |

| ▹ Number of simulation paths | |

| ▹ Number of triggered events | |

| ▹ The time, triggering event occurred, place holder | |

| ▹ Price of the pandemic bond(triggered), place holder | |

| ▹ the price of the bond investor willing to pay if no pandemic occur. | |

| This is the selling price of World Bank pandemic bond | |

| ▹ probability of Pandemic. See Equation (34) | |

| for to M do | |

| Simulate solution to stochastic differential equations with time step size and number of steps N. Solution paths are and Calculate daily increments using and Starting day 7 to day 1104, calculate past seven day average for daily new infections and deaths. | |

| Seven day average paths are | ▹ see Section 5.2.2 |

| Calculate standard deviation of past seven day daily new infections | |

| Calculate growth rate | ▹ see Equation (6) |

| if then | |

| ▹ Add time of the trigger event to the set | |

| Bond Value based on coupons paid until time t | ▹ see Equation (33) |

| end if | |

| end for | |

| average of values in set | |

| ▹ P(H) from above. See Equation (15) | |

8. Numerical Simulation 2

- The investor want to know the fair price based on future interest rate movements, opposed to setting fixed required yield rate.

- Some model parameters are calibrated using COVID-19 data. Most other past pandemics do not have day to day records of number of infections, death, etc. But COVID-19 may be the first pandemic where humans were able to record day-to-day statistics. Therefore, the model can be calibrated using daily data instead of using aggregate numbers.

8.1. Bond Parameters

8.2. Interest Rate Model Parameters

8.3. Calculating Probability of a Pandemic Event and Estimating Parameters for and

- Calculate the maximum. This gives and .

- Calculate the average of nonzero growth rates. This gives and .

- Calculate the average of growth rates up to certain date such as right before the growth rates become close to zero. If we use first the 50 days, then and .

- Fit a parametric distribution such as log normal or gamma and use statistics such as mean or median of the fitted distribution as the growth rate.

9. Discussion

- We proposed a pandemic bond pricing framework based on the stochastic logistic model and the Hull–White interest rate model.

- We review the details of the World Bank-issued pandemic bond.

- We used past four influenza pandemics to price World Bank issued pandemic bond, and hence demonstrating how to use the model when aggregate information of past pandemics is available. Even though we used information from four pandemics, the example shows how to use all available past pandemic scenarios in the modeling process.

- We used COVID-19 data to calibrate the model parameters using a data-driven approach and price a pandemic bond. Therefore, we demonstrate how to use the model when detailed data are available. The purpose of using COVID-19 data is not to claim that future pandemics would be look like COVID -19 but to demonstrate a data-driven approach.

- We showed how to use a parameter grid to remove any restrictions for and calculate across all possible combinations to obtain the fair price of a pandemic bond.

- We calculate the price of the bond under two different scenarios. First, when an investor knows the required yield, find the price he/she is willing to pay. Second, the fair price of the pandemic bond under the model.

- We created an algorithm to implement the model and made R codes and other data sets available for future research/testing and reproducibility.

10. Conclusions

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Bajardi, Paolo, Chiara Poletto, Jose J. Ramasco, Michele Tizzoni, Vittoria Colizza, and Alessandro Vespignani. 2011. Human mobility networks, travel restrictions, and the global spread of 2009 h1n1 pandemic. PLoS ONE 6: e16591. [Google Scholar] [CrossRef] [PubMed]

- Bevere, Lucia, and Michael Gloor. 2020. Natural catastrophes in times of economic accumulation and climate change. Sigma 2: 1–36, Swiss Re Institute. Available online: https://www.swissre.com/dam/jcr:85598d6e-b5b5-4d4b-971e-5fc9eee143fb/sigma-2-2020-en.pdf (accessed on 2 October 2022).

- Bickis, Mikelis, and Ugis Bickis. 2007. Predicting the next pandemic: An exercise in imprecise hazards. Paper presented at the 5th International Symposium on Imprecise Probability: Theories and Applications, Prague, Czech Republic, July 6–19; Available online: https://isipta07.sipta.org/proceedings/proceedings-optimised.pdf (accessed on 2 October 2022).

- Braun, Alexander. 2012. Determinants of the cat bond spread at issuance. Zeitschrift für Die Gesamte Versicherungswissenschaft 101: 721–36. [Google Scholar] [CrossRef]

- Cori, Anne, Neil M. Ferguson, Christophe Fraser, and Simon Cauchemez. 2013. A new framework and software to estimate time-varying reproduction numbers during epidemics. American Journal of Epidemiology 178: 1505–12. [Google Scholar] [CrossRef]

- Cox, John C., Jonathan E. Ingersoll Jr., and Stephen A. Ross. 1985. A theory of the term structure of interest rates. Econometrica 53: 385–408. [Google Scholar] [CrossRef]

- Cox, Samuel H., Joseph R. Fairchild, and Hal W. Pedersen. 2000. Economic aspects of securitization of risk. ASTIN Bulletin: The Journal of the IAA 30: 157–93. [Google Scholar] [CrossRef]

- Cox, Samuel H., and Hal W. Pedersen. 2000. Catastrophe risk bonds. North American Actuarial Journal 4: 56–82. [Google Scholar] [CrossRef]

- Cummins, J. David. 2008. Cat bonds and other risk-linked securities: State of the market and recent developments. Risk Management and Insurance Review 11: 23–47. [Google Scholar] [CrossRef]

- Cummins, J. David. 2012. Cat bonds and other risk-linked securities: Product design and evolution of the market. In The Geneva Reports. Geneva: The Geneva Association, pp. 39–61. [Google Scholar] [CrossRef]

- Deng, Guoqu, Shiqiang Liu, Li Li, and Chushi Deng. 2020. Research on the pricing of global drought catastrophe bonds. Mathematical Problems in Engineering 2020: 3898191. [Google Scholar] [CrossRef]

- Edesess, Michael. 2015. Catastrophe bonds: An important new financial instrument. Alternative Investment Analyst Review 4: 6–11. Available online: https://caia.org/sites/default/files/AIAR_Q4_2015-02_Edesses_CatBonds_0.pdf (accessed on 2 October 2022).

- Fan, Weili, and Rogemar Mamon. 2021. A hybridized stochastic sir-vasiček model in evaluating a pandemic emergency financing facility. IEEE Transactions on Computational Social Systems 10: 1105–14. [Google Scholar] [CrossRef]

- Financial Times. 2023. After COVID-19: The Future of Pandemic Bonds. Available online: https://www.ft.com/partnercontent/calvert/after-covid-19-the-future-of-pandemic-bonds.html (accessed on 10 June 2023).

- Guidotti, Emanuele, and David Ardia. 2020. COVID-19 data hub. Journal of Open Source Software 5: 2376. [Google Scholar] [CrossRef]

- Gurrieri, Sébastien, Masaki Nakabayashi, and Tony Wong. 2009. Calibration Methods of Hull-White Model. Available at SSRN 1514192. [Google Scholar] [CrossRef]

- Härdle, Wolfgang Karl, and Brenda López Cabrera. 2010. Calibrating cat bonds for mexican earthquakes. Journal of Risk and Insurance 77: 625–50. [Google Scholar] [CrossRef]

- Huang, Shimeng, Ken Seng Tan, Jinggong Zhang, and Wenjun Zhu. 2021. Epidemic financing facilities: Pandemic bonds and endemic swaps. In Nanyang Business School Research Paper Series, Singapore, No. 21–37. [Google Scholar] [CrossRef]

- Hull, John, and Alan White. 1990. Pricing interest-rate-derivative securities. The Review of Financial Studies 3: 573–92. [Google Scholar] [CrossRef]

- Hull, John, and Alan White. 1993. One-factor interest-rate models and the valuation of interest-rate derivative securities. Journal of Financial and Quantitative Analysis 28: 235–54. [Google Scholar] [CrossRef]

- Hull, John C. 2014. Options Futures and Other Derivatives. New York: Pearson Education. ISBN 978-0133456318. [Google Scholar]

- ICE Benchmark Administration. 2023. Administering Global Benchmarks and Data Services. Available online: https://www.theice.com/iba (accessed on 15 March 2023).

- Jackson, Charlotte, Emilia Vynnycky, and Punam Mangtani. 2010. Estimates of the transmissibility of the 1968 (hong kong) influenza pandemic: Evidence of increased transmissibility between successive waves. American Journal of Epidemiology 171: 465–78. [Google Scholar] [CrossRef]

- Khodabin, M., Khosrow Maleknejad, M. Rostami, and M. Nouri. 2012. Interpolation solution in generalized stochastic exponential population growth model. Applied Mathematical Modelling 36: 1023–33. [Google Scholar] [CrossRef]

- Kladívko, Kamil, and Tomáš Rusý. 2023. Maximum likelihood estimation of the hull–white model. Journal of Empirical Finance 70: 227–47. [Google Scholar] [CrossRef]

- Klugman, Stuart A., Harry H. Panjer, and Gordon E. Willmot. 2012. Loss Models: From Data to Decisions, 4th ed. Hoboken: John Wiley & Sons. ISBN 978-1118315323. [Google Scholar]

- Lauer, Stephen A., Kyra H. Grantz, Qifang Bi, Forrest K. Jones, Qulu Zheng, Hannah R. Meredith, Andrew S. Azman, Nicholas G. Reich, and Justin Lessler. 2020. The incubation period of coronavirus disease 2019 (COVID-19) from publicly reported confirmed cases: Estimation and application. Annals of Internal Medicine 172: 577–82. [Google Scholar] [CrossRef]

- Lee, Jin-Ping, and Min-Teh Yu. 2002. Pricing default-risky cat bonds with moral hazard and basis risk. Journal of Risk and Insurance 69: 25–44. [Google Scholar] [CrossRef]

- Lee, Sang-heon. 2021. Hull-White 1-Factor Model Using R Code. Available online: https://www.r-bloggers.com/2021/06/hull-white-1-factor-model-using-r-code/ (accessed on 10 March 2023).

- Li, F. C. K., B. C. K. Choi, T. Sly, and A. W. P. Pak. 2008. Finding the real case-fatality rate of h5n1 avian influenza. Journal of Epidemiology & Community Health 62: 555–59. [Google Scholar] [CrossRef]

- Li, Han, Haibo Liu, Qihe Tang, and Zhongyi Yuan. 2023. Pricing extreme mortality risk in the wake of the COVID-19 pandemic. Insurance: Mathematics and Economics 108: 84–106. [Google Scholar] [CrossRef] [PubMed]

- Liu, Meng, and Ke Wang. 2013. A note on stability of stochastic logistic equation. Applied Mathematics Letters 26: 601–6. [Google Scholar] [CrossRef]

- Liu, Ying, Albert A Gayle, Annelies Wilder-Smith, and Joacim Rocklöv. 2020. The reproductive number of COVID-19 is higher compared to sars coronavirus. Journal of Travel Medicine 27. [Google Scholar] [CrossRef]

- Ma, Junling. 2020. Estimating epidemic exponential growth rate and basic reproduction number. Infectious Disease Modelling 5: 129–41. [Google Scholar] [CrossRef]

- Ma, Zong-Gang, and Chao-Qun Ma. 2013. Pricing catastrophe risk bonds: A mixed approximation method. Insurance: Mathematics and Economics 52: 243–54. [Google Scholar] [CrossRef]

- Makariou, Despoina, Pauline Barrieu, and Yining Chen. 2021. A random forest based approach for predicting spreads in the primary catastrophe bond market. Insurance: Mathematics and Economics 101: 140–62. [Google Scholar] [CrossRef]

- Manathunga, Vajira. 2023. Pricing Pandemic Bonds under Stochastic Logistic Growth Model. Available online: https://github.com/cvajira/Pricing-Pandemic-Bonds-under-Stochastic-Logistic-Growth-Model (accessed on 21 July 2023).

- Mills, Christina E., James M. Robins, and Marc Lipsitch. 2004. Transmissibility of 1918 pandemic influenza. Nature 432: 904–6. [Google Scholar] [CrossRef]

- Morton N., Lane. 2018. Pricing Cat Bonds: Regressions and Machine Learning: Some Observations; Working Paper. Lane Financial LLC. Available online: http://www.lanefinancialllc.com/content/view/402/50/ (accessed on 10 March 2023).

- Nishiura, Hiroshi. 2010. Case fatality ratio of pandemic influenza. The Lancet Infectious Diseases 10: 443–44. [Google Scholar] [CrossRef]

- Otunuga, Olusegun Michael, and Oluwaseun Otunuga. 2022. Stochastic modeling and forecasting of COVID-19 deaths: Analysis for the fifty states in the united states. Acta Biotheoretica 70: 25. [Google Scholar] [CrossRef] [PubMed]

- Patterson, Karl David. 1986. Pandemic Influenza, 1700–1900: A Study in Historical Epidemiology. Lanham: Rowman & Littlefield Pub Incorporated. ISBN 0847675122. [Google Scholar]

- Privault, Nicolas. 2013. Stochastic Finance: An Introduction with Market Examples. Boca Raton: CRC Press. ISBN 978-1466594029. [Google Scholar]

- R Core Team. 2022. R: A Language and Environment for Statistical Computing. Vienna: R Foundation for Statistical Computing. [Google Scholar]

- Reuters. 2017. World Bank Launches ’Pandemic Bond’ to Tackle Major Outbreaks. Available online: https://www.reuters.com/article/us-global-pandemic-insurance/world-bank-launches-pandemic-bond-to-tackle-major-outbreaks-idUSKBN19J2JJ (accessed on 2 October 2022).

- Schwarcz, Steven L. 2021. Insuring the’uninsurable’: Catastrophe bonds, pandemics, and risk securitization. Wash. UL Rev. 99: 853. [Google Scholar]

- Shao, Jia, Apostolos D. Papaioannou, and Athanasios A. Pantelous. 2017. Pricing and simulating catastrophe risk bonds in a markov-dependent environment. Applied Mathematics and Computation 309: 68–84. [Google Scholar] [CrossRef]

- Shen, Christopher Y. 2020. Logistic growth modelling of COVID-19 proliferation in china and its international implications. International Journal of Infectious Diseases 96: 582–89. [Google Scholar] [CrossRef]

- Shinh, Roshni. 2021. Pandemic bonds: What Are They and How do They Work? Available online: https://actuaries.blog.gov.uk/2021/03/02/pandemic-bonds-what-are-they-and-how-do-they-work/ (accessed on 2 October 2022).

- Swiss Re Institute. 2023. In 5 Charts: Continued High Losses from Natural Catastrophes in 2022. Available online: https://www.swissre.com/institute/research/sigma-research/sigma-2023-01/5-charts-losses-natural-catastrophes.html (accessed on 10 June 2023).

- Triambak, S., D. P. Mahapatra, N. Mallick, and R. Sahoo. 2021. A new logistic growth model applied to COVID-19 fatality data. Epidemics 37: 100515. [Google Scholar] [CrossRef] [PubMed]

- Verhulst, Pierre-François. 1838. Notice sur la loi que la population suit dans son accroissement. Correspondence Mathematique et Physique 10: 113–26. [Google Scholar]

- Vynnycky, Emilia, and W. J. Edmunds. 2008. Analyses of the 1957 (asian) influenza pandemic in the united kingdom and the impact of school closures. Epidemiology & Infection 136: 166–79. [Google Scholar] [CrossRef]

- Wolfram Research, Inc. 2023. Mathematica. Version 13.3. Champaign: Wolfram Research Inc. [Google Scholar]

- World Bank. 2017a. World Bank Launches First-Ever Pandemic Bonds to Support 500 Million Dollars Pandemic Emergency Financing Facility. Available online: https://www.worldbank.org/en/news/press-release/2017/06/28/world-bank-launches-first-ever-pandemic-bonds-to-support-500-million-pandemic-emergency-financing-facility (accessed on 2 October 2022).

- World Bank. 2017b. World Bank PEF Prospectus Supplement. Available online: https://thedocs.worldbank.org/en/doc/f355aa56988e258a350942240872e3c5-0240012017/original/PEF-Final-Prospectus-PEF.pdf (accessed on 2 October 2022).

- World Bank. 2018. Operations Manual—Pandemic Emergency Financing Facility. Available online: https://pubdocs.worldbank.org/en/842101571243529089/PEF-Operations-Manual-approved-10-15-18.pdf (accessed on 15 September 2022).

- World Bank. 2019. Pandemic Emergency Financing Facility (PEF): Operational Brief for Eligible Countries. Available online: https://pubdocs.worldbank.org/en/478271550071105640/PEF-Operational-Brief-Feb-2019.pdf (accessed on 2 October 2022).

- World Bank. 2020. Fact Sheet: Pandemic Emergency Financing Facility. Available online: https://www.worldbank.org/en/topic/pandemics/brief/fact-sheet-pandemic-emergency-financing-facility (accessed on 2 October 2022).

- World Health Organization. 2013. Pandemic Influenza Risk Management who Interim Guidance. Geneva: World Health Organization, pp. 6–7. Available online: https://www.who.int/publications/i/item/pandemic-influenza-risk-management (accessed on 2 October 2022).

- World Health Organization. 2015. Summary of Probable SARS Cases with Onset of Illness from 1 November 2002 to 31 July 2003. Available online: https://www.who.int/publications/m/item/summary-of-probable-sars-cases-with-onset-of-illness-from-1-november-2002-to-31-july-2003 (accessed on 2 October 2022).

- Wu, Ke, Didier Darcet, Qian Wang, and Didier Sornette. 2020. Generalized logistic growth modeling of the COVID-19 outbreak: Comparing the dynamics in the 29 provinces in china and in the rest of the world. Nonlinear Dynamics 101: 1561–81. [Google Scholar] [CrossRef]

- Young, Virginia R. 2004. Pricing in an incomplete market with an affine term structure. Mathematical Finance: An International Journal of Mathematics, Statistics and Financial Economics 14: 359–81. [Google Scholar] [CrossRef]

- Zheng, Xiyuan, and Rogemar Mamon. 2023. Assessment of a pandemic emergency financing facility. Progress in Disaster Science 18: 100281. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| i | |

|---|---|

| 1 | |

| 2 | |

| 3 | |

| 4 | |

| 5 |

| Face Value | Settl. Date | Maturity Date | Issue Price | Bond Coupon | Day Count | Coupon Payment Dates |

|---|---|---|---|---|---|---|

| USD 225M | 7 July 2017 | 15 July 2020 | 100% | 6 month USD LIBOR +6.50% | Actual/360 | 15th day of each month |

| including 15 August 2017 | ||||||

| to 15 July 2020 |

| Date | Real 6M.LIBOR | Real.Coupon (USD Million) | Predicted 6M.LIBOR | Pred.Coupon (USD Million) | |

|---|---|---|---|---|---|

| 2017-07-07 | 1.40000 | NA | NA | NA | |

| 1 | 2017-08-15 | 1.45333 | 1.941576 | 1.514160 | 1.941576 |

| 2 | 2017-09-15 | 1.47111 | 1.540958 | 1.541704 | 1.552743 |

| 3 | 2017-10-16 | 1.53316 | 1.544403 | 1.547542 | 1.558080 |

| 4 | 2017-11-15 | 1.61810 | 1.506217 | 1.534158 | 1.508914 |

| 5 | 2017-12-15 | 1.77443 | 1.522144 | 1.501944 | 1.506405 |

| 6 | 2018-01-15 | 1.89875 | 1.603171 | 1.481613 | 1.550377 |

| 7 | 2018-02-15 | 2.09644 | 1.627258 | 1.519304 | 1.546438 |

| 8 | 2018-03-15 | 2.34175 | 1.504377 | 1.556905 | 1.403378 |

| 9 | 2018-04-16 | 2.50313 | 1.768350 | 1.598791 | 1.611381 |

| 10 | 2018-05-15 | 2.49250 | 1.631817 | 1.644671 | 1.467906 |

| 11 | 2018-06-15 | 2.50375 | 1.742297 | 1.700423 | 1.578030 |

| 12 | 2018-07-16 | 2.51850 | 1.744477 | 1.751601 | 1.588832 |

| 13 | 2018-08-15 | 2.51063 | 1.690969 | 1.783887 | 1.547175 |

| 14 | 2018-09-17 | 2.57075 | 1.858442 | 1.815619 | 1.708552 |

| 15 | 2018-10-15 | 2.65375 | 1.587381 | 1.844416 | 1.455233 |

| 16 | 2018-11-15 | 2.86019 | 1.773539 | 1.877727 | 1.616731 |

| 17 | 2018-12-17 | 2.90463 | 1.872038 | 1.909304 | 1.675545 |

| 18 | 2019-01-15 | 2.84581 | 1.704589 | 1.931655 | 1.524186 |

| 19 | 2019-02-15 | 2.75375 | 1.810751 | 1.950721 | 1.633633 |

| 20 | 2019-03-15 | 2.67175 | 1.619406 | 1.966666 | 1.478876 |

| 21 | 2019-04-15 | 2.63763 | 1.777027 | 1.982977 | 1.640417 |

| 22 | 2019-05-15 | 2.55088 | 1.713306 | 1.996944 | 1.590558 |

| 23 | 2019-06-17 | 2.30875 | 1.866744 | 2.012034 | 1.752495 |

| 24 | 2019-07-15 | 2.21713 | 1.541531 | 2.027451 | 1.489606 |

| 25 | 2019-08-15 | 2.01400 | 1.688944 | 2.054883 | 1.652194 |

| 26 | 2019-09-16 | 2.07800 | 1.702800 | 2.080081 | 1.710977 |

| 27 | 2019-10-15 | 1.97725 | 1.554763 | 2.105046 | 1.555140 |

| 28 | 2019-11-15 | 1.91850 | 1.642467 | 2.132781 | 1.667228 |

| 29 | 2019-12-16 | 1.89338 | 1.631084 | 2.157987 | 1.672601 |

| 30 | 2020-01-15 | 1.86500 | 1.573759 | 2.176524 | 1.623373 |

| 31 | 2020-02-17 | 1.72488 | 1.725281 | 2.189160 | 1.789533 |

| 32 | 2020-03-16 | 0.84375 | 1.439354 | 2.199016 | 1.520603 |

| 33 | 2020-04-15 | 1.15013 | 1.376953 | 2.207977 | 1.631066 |

| 34 | 2020-05-15 | 0.65900 | 1.434399 | 2.216058 | 1.632746 |

| 35 | 2020-06-15 | 0.43088 | 1.387056 | 2.223039 | 1.688736 |

| 36 | 2020-07-15 | NA | 1.299540 | NA | 1.635570 |

| 2017-07-07 | real yield (no COVID): 8.8978% | pred. yield (no COVID): 8.6734% | |||

| Year | Virus Type | Estimated Reproduction Number () | Estimated Total Death | Case Fatality Rate (%) | Average Infectious Period () | Growth Rate for Infection () | Estimated Total Infections |

|---|---|---|---|---|---|---|---|

| 1918 | H1N1 | 1.2–3.0 | 20–50 M | 2.5 | 4.1 days | 0.049–0.488 | 800–2000 M |

| 1957 | H2N1 | 1.5 | 1–4 M | 0.1–0.4 | 4 days | 0.125 | 1000 M |

| 1968 | H3N2 | 1.3–1.6 | 1–4 M | 0.1–0.4 | 4 days | 0.075–0.150 | 1000 M |

| 2009 | H1N1 | 1.1–1.8 | 0.1–0.4 M | 0.048 | 2.5 days | 0.040–0.320 | 208–833 M |

| Scenario | Spanish Flu (1918) | Asian Flu (1957) | HongKong Flu (1968) | Swine Flu (2009) |

|---|---|---|---|---|

| 2000 M | 1000 M | 1000 M | 833 M | |

| 50 M | 4 M | 4 M | 0.4 M | |

| 0.049 | 0.125 | 0.075 | 0.04 | |

| Bond Price | 195.5866 | 194.2548 | 194.8468 | 201.4460 M |

| 0.1392 | 0.1393 | 0.1391 | 0.1132 | |

| Average price: 196.5335 | ||||

| 0.04 | 0.08 | 0.12 | 0.16 | 0.20 | 0.24 | 0.28 | 0.32 | 0.36 | 0.40 | |

|---|---|---|---|---|---|---|---|---|---|---|

| Bond.Price | 195.70 | 198.92 | 203.54 | 207.80 | 212.93 | 220.20 | 224.46 | 224.99 | 225.00 | 225.00 |

| Prob.Trigger | 0.14 | 0.12 | 0.10 | 0.08 | 0.06 | 0.02 | 0.00 | 0.00 | 0.00 | 0.00 |

| Parameter | Value |

|---|---|

| Settle Date | 6 January 2023 |

| Maturity Date | 15 January 2026 |

| Term | 3 years |

| M | USD 225M |

| Coupons | 6 month USD LIBOR + 6.5% |

| Payment Date | 15th day of each month including 15 February 2023 to 15 January 2026 |

| Day convention | Actual/360 |

| Hull–White Model | Calibrated to 6 January 2023 |

| Stochastic-logistic growth model | Calibrated using COVID-19 data |

| 5000 | |

| 2500 |

| Scenario | I | II | III |

|---|---|---|---|

| # Simulations | 5000 | 5000 | 5000 |

| 100.46 M | 100.46 M | 100.46 M | |

| 1.1 M | 1.1 M | 1.1 M | |

| 1 | 1 | 1 | |

| 1 | 1 | 1 | |

| 0.4842 | 0.0147 | 0.2064 | |

| 0.0521 | 0.0522 | 0.1309 | |

| 0.0020 | 0.0020 | 0.0067 | |

| 0.5 | 0.5 | 0.5 | |

| Bond Price | 192.3830 | 205.3894 | 192.4687 |

| 0.1468 | 0.1161 | 0.1468 | |

| 0.1468 | 0.1468 | 0.1468 | |

| Average price: USD 196.747 million | |||

| 0.1, 0.2, 0.3, 0.4 | |

| 0.1, 0.2, 0.3, 0.4 | |

| 0.02, 0.04, 0.06, 0.08, 0.10, 0.12, 0.14, 0.16, 0.18, 0.20 | |

| 0.02, 0.04, 0.06, 0.08, 0.10, 0.12, 0.14, 0.16, 0.18, 0.20 | |

| 0.1, 0.2, 0.3, 0.4, 0.5, 0.6, 0.7, 0.8, 0.9 | |

| # of parameter combinations | 14,400 |

| # Simulations | each combination 100 times |

| Average bond price under this grid | USD 205.3762 million |

| Average probability for trigger activation | 0.0887 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Manathunga, V.; Deng, L. Pricing Pandemic Bonds under Hull–White & Stochastic Logistic Growth Model. Risks 2023, 11, 155. https://doi.org/10.3390/risks11090155

Manathunga V, Deng L. Pricing Pandemic Bonds under Hull–White & Stochastic Logistic Growth Model. Risks. 2023; 11(9):155. https://doi.org/10.3390/risks11090155

Chicago/Turabian StyleManathunga, Vajira, and Linmiao Deng. 2023. "Pricing Pandemic Bonds under Hull–White & Stochastic Logistic Growth Model" Risks 11, no. 9: 155. https://doi.org/10.3390/risks11090155