Financial Literacy Confidence and Retirement Planning: Evidence from China

Abstract

:1. Introduction

2. Literature Review

3. Data and Description

3.1. Objective Financial Literacy

3.2. Subjective Financial Literacy Measurement

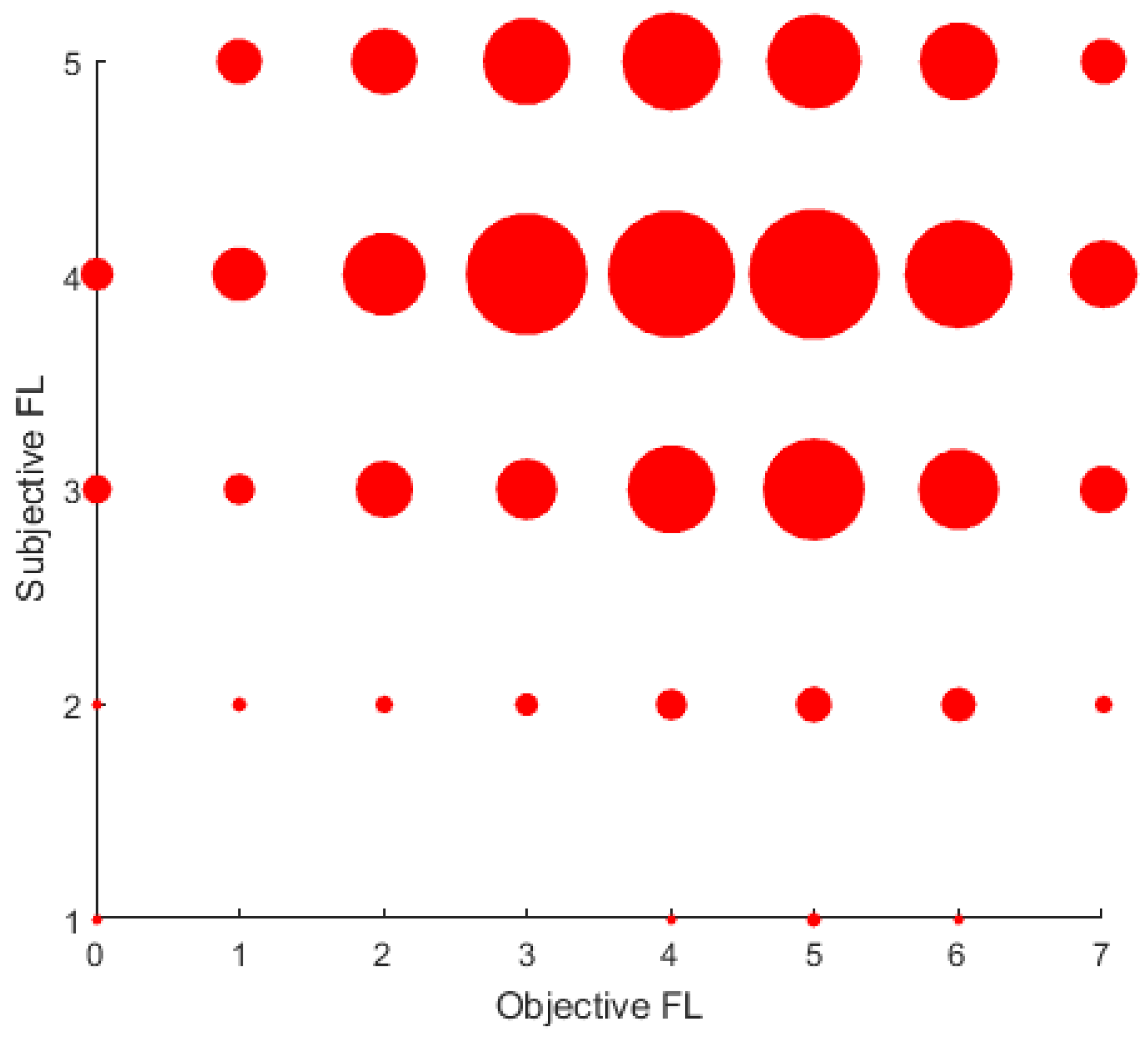

3.3. Financial Literacy Overconfidence and Underconfidence

3.4. Retirement Planning Measurement

4. Empirical Analysis

4.1. Regression Model

+ β3 Objective FL + γ·controls + Fixed effect + ε.

4.2. Main Results

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

| 1 | The reason for restricting the respondents to be non-retired and aged between 25 and 65 is to exclude those in the decumulation or education phases. The sample is balanced in terms of gender with slightly more women (men = 49.1%) and geographically representative. For more details on Aegon’s survey design and research approach, refer to the introduction link (https://www.aegon.com/research/our-research-approach/, accessed on 4 December 2022). The Aegon Retirement Readiness Survey is conducted annually in collaboration with nonprofit academic institutes in some countries, including Australia, Brazil, Canada, China, France, Germany, Hungary, India, Japan, the Netherlands, Poland, Spain, Turkey, the United Kingdom, and the United States. The survey covers a wide range of issues, including attitudes and readiness for retirement, maintaining a healthy lifestyle, and lifelong learning to improve long-term resilience. |

| 2 | Due to limitations of the data, the existing literature commonly lacks discussion on endogeneity issues and identifications such as exogeous shock. |

References

- Agarwal, Sumit, Gene Amromin, Itzhak Ben-David, Souphala Chomsisengphet, and Douglas D. Evanoff. 2015. Financial literacy and financial planning: Evidence from India. Journal of Housing Economics 27: 4–21. [Google Scholar] [CrossRef]

- Alessie, Rob, Maarten Van Rooij, and Annamaria Lusardi. 2011. Financial literacy and retirement preparation in the Netherlands. Journal of Pension Economics & Finance 10: 527–45. [Google Scholar]

- Almenberg, Johan, and Jenny Säve-Söderbergh. 2011. Financial literacy and retirement planning in Sweden. Journal of Pension Economics & Finance 10: 585–98. [Google Scholar]

- Arrondel, Luc. 2021. Financial Literacy and French Behaviour on the Stock Market. Numeracy 14: 1. [Google Scholar] [CrossRef]

- Arrondel, Luc, Majdi Debbich, and Frédérique Savignac. 2015. Stockholding in France: The role of financial literacy and information. Applied Economics Letters 22: 1315–19. [Google Scholar] [CrossRef]

- Barber, Brad M., and Terrance Odean. 2000. Trading is hazardous to your wealth: The common stock investment performance of individual investors. The Journal of Finance 55: 773–806. [Google Scholar] [CrossRef]

- Barber, Brad M., and Terrance Odean. 2001. Boys will be boys: Gender, overconfidence, and common stock investment. The Quarterly Journal of Economics 116: 261–92. [Google Scholar] [CrossRef]

- Behrman, Jere R., Olivia S. Mitchell, Cindy K. Soo, and David Bravo. 2012. How financial literacy affects household wealth accumulation. American Economic Review 102: 300–4. [Google Scholar] [CrossRef] [Green Version]

- Brokesova, Zuzana, Andrej Cupak, and Gueorgui Kolev. 2017. Financial Literacy and Voluntary Savings for Retirement in Slovakia. Research Department, National Bank of Slovakia: Available online: https://ideas.repec.org/p/svk/wpaper/1051.html (accessed on 4 December 2022).

- Brown, Martin, and Roman Graf. 2013. Financial Literacy, Household Investment and Household Debt: Evidence from Switzerland. University of St. Gallen Working Paper on Finance 13-1. St. Gallen: University of St. Gallen. Available online: https://www.alexandria.unisg.ch/Publikationen/Zitation/Martin_Brown/219130 (accessed on 12 February 2022).

- Bucher-Koenen, Tabea, Annamaria Lusardi, Rob Alessie, and Maarten Van Rooij. 2017. How financially literate are women? An overview and new insights. Journal of Consumer Affairs 51: 255–83. [Google Scholar] [CrossRef]

- Bucher-Koenen, Tabea, and Annamaria Lusardi. 2011. Financial literacy and retirement planning in Germany. Journal of Pension Economics & Finance 10: 565–84. [Google Scholar]

- Bumcrot, Christopher B., Judy Lin, and Annamaria Lusardi. 2013. The Geography of Financial Literacy. Numeracy 6: 2. [Google Scholar] [CrossRef] [Green Version]

- Calcagno, Riccardo, Yan Alperovych, and Anita Quas. 2019. Financial literacy and entrepreneurship. New Frontiers in Entrepreneurial Finance Research, 271–97. Available online: https://www.worldscientific.com/doi/abs/10.1142/9789811202766_0010 (accessed on 22 February 2020).

- Chu, Zhong, Zhengwei Wang, Jing Jian Xiao, and Weiqiang Zhang. 2017. Financial literacy, portfolio choice and financial well-being. Social Indicators Research 132: 799–820. [Google Scholar] [CrossRef] [Green Version]

- Cupák, Andrej, Gueorgui I. Kolev, and Zuzana Brokešová. 2019. Financial literacy and voluntary savings for retirement: Novel causal evidence. The European Journal of Finance 25: 1606–25. [Google Scholar] [CrossRef]

- Fang, Hanming, and Jin Feng. 2018. The Chinese Pension System. National Bureau of Economic Research: Available online: https://www.nber.org/system/files/working_papers/w25088/w25088.pdf (accessed on 8 February 2020).

- Fornero, Elsa, and Chiara Monticone. 2011. Financial literacy and pension plan participation in Italy. Journal of Pension Economics & Finance 10: 547–64. [Google Scholar]

- Glaser, Markus, and Martin Weber. 2010. Overconfidence. In Behavioral Finance: Investors, Corporations, and Markets. New York: John Wiley & Sons, Inc., pp. 241–58. [Google Scholar]

- Grinblatt, Mark, and Matti Keloharju. 2009. Sensation seeking, overconfidence, and trading activity. The Journal of Finance 64: 549–78. [Google Scholar] [CrossRef] [Green Version]

- Guiso, Luigi, and Eliana Viviano. 2015. How much can financial literacy help? Review of Finance 19: 1347–82. [Google Scholar] [CrossRef]

- Kalmi, Panu, and Olli-Pekka Ruuskanen. 2018. Financial literacy and retirement planning in Finland. Journal of Pension Economics & Finance 17: 335–62. [Google Scholar]

- Karakurum-Ozdemir, Kamer, Melike Kokkizil, and Gokce Uysal. 2019. Financial literacy in developing countries. Social Indicators Research 143: 325–53. [Google Scholar] [CrossRef] [Green Version]

- Kendzia, Michael Jan, and Yoan Suozzi Borrero. 2022. Financial Literacy among the Youth in Switzerland. Journal of Financial Risk Management 11: 323–41. [Google Scholar] [CrossRef]

- Kurowski, Łukasz. 2021. Household’s overindebtedness during the COVID-19 crisis: The role of debt and financial literacy. Risks 9: 62. [Google Scholar] [CrossRef]

- Lusardi, Annamaria. 2008. Household Saving Behavior: The Role of Financial Literacy, Information, and Financial Education Programs. National Bureau of Economic Research: Available online: https://www.nber.org/papers/w13824 (accessed on 10 February 2008).

- Lusardi, Annamaria. 2012. Numeracy, Financial Literacy, and Financial Decision-Making. National Bureau of Economic Research: Available online: https://www.nber.org/papers/w17821 (accessed on 10 February 2014).

- Lusardi, Annamaria, and Olivia S. Mitchell. 2006. Financial Literacy and Planning: Implications for Retirement Wellbeing. Pension Research Council Working Paper 1. Philadelphia: The Wharton School. [Google Scholar]

- Lusardi, Annamaria, and Olivia S. Mitchell. 2007a. Baby boomer retirement security: The roles of planning, financial literacy, and housing wealth. Journal of Monetary Economics 54: 205–24. [Google Scholar] [CrossRef] [Green Version]

- Lusardi, Annamaria, and Olivia S. Mitchell. 2007b. Financial literacy and retirement planning: New evidence from the Rand American Life Panel. Available online: https://ssrn.com/abstract=1095869 (accessed on 22 February 2008).

- Lusardi, Annamaria, and Olivia S. Mitchell. 2011a. Financial literacy and retirement planning in the United States. Journal of Pension Economics & Finance 10: 509–25. [Google Scholar]

- Lusardi, Annamaria, and Olivia S. Mitchell. 2011b. Financial literacy around the world: An overview. Journal of Pension Economics & Finance 10: 497–508. [Google Scholar]

- Lusardi, Annamaria, and Olivia S. Mitchell. 2011c. Financial Literacy and Planning: Implications for Retirement Well-Being. National Bureau of Economic Research: Available online: https://www.nber.org/papers/w17078 (accessed on 10 May 2011).

- Lusardi, Annamaria, and Olivia S. Mitchell. 2017. How ordinary consumers make complex economic decisions: Financial Literacy and retirement readiness. Quarterly Journal of Finance 7: 1750008. [Google Scholar] [CrossRef] [Green Version]

- Malmendier, Ulrike, and Geoffrey Tate. 2005. CEO overconfidence and corporate investment. The Journal of Finance 60: 2661–700. [Google Scholar] [CrossRef] [Green Version]

- Reiter, Sarah, and Elisabeth Beckmann. 2020. How financially literate is CESEE? Insights from the OeNB Euro Survey. Oesterreichische Nationalbank Focus on European Economic Integration (Austria) 3: 36–59. [Google Scholar]

- Sarpong-Kumankoma, Emmanuel. 2021. Financial literacy and retirement planning in Ghana. Review of Behavioral Finance 15: 103–18. [Google Scholar] [CrossRef]

- Sekita, Shizuka. 2011. Financial literacy and retirement planning in Japan. Journal of Pension Economics & Finance 10: 637–56. [Google Scholar]

- Stolper, Oscar A., and Andreas Walter. 2017. Financial literacy, financial advice, and financial behavior. Journal of Business Economics 87: 581–643. [Google Scholar] [CrossRef] [Green Version]

- Van Rooij, Maarten C. J., Annamaria Lusardi, and Rob J. M. Alessie. 2012. Financial literacy, retirement planning and household wealth. The Economic Journal 122: 449–78. [Google Scholar] [CrossRef] [Green Version]

- Xia, Tian, Zhengwei Wang, and Kunpeng Li. 2014. Financial literacy overconfidence and stock market participation. Social Indicators Research 119: 1233–45. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Questions | Answers |

|---|---|

| 1. Suppose you have 100 yuan in a savings account and the interest rate was 2% per year. After 5 years, how much do you think you would have in the account if you leave the money to grow? | (i) More than 102 yuan (ii) Exactly 102 yuan (iii) Less than 102 yuan (iv) Do not know |

| 2. Imagine that the interest rate on your savings account is 1% per year and inflation is 2% per year. After 1 year, how much will you be able to buy with the money in this account? | (i) More than today (ii) Exactly the same (iii) Less than today (iv) Do not know |

| 3. Please tell me whether this statement is true or false. ‘Buying a single company’s stock usually provides a safer return than a stock mutual fund’. | (i) True (ii) False (iii) Do not know |

| 4. Suppose you take a mortgage loan from the bank. One repayment term option would require you to repay the mortgage over 15 years and the other option is to repay the mortgage over 30 years. Both loans have the same interest rate (4%). Then the monthly mortgage repayment of the 15-year loan is higher than the 30-year loan. | (i) This statement is right (ii) The statement is wrong (iii) I don’t know |

| 5. Imagine that you want to take out a mortgage loan from your bank today. You anticipate that interest rates are set to rise over over the next few months. Which type of mortgage loan would you choose to take out? | (i) Fixed rate loan (ii) Floating rate loan (iii) I don’t know |

| 6. Imagine that you buy a bond today for a price of 97 yuan. In a year’s time when the bond reaches maturity it is expected to be worth 100 yuan. If interest rates rise tomorrow, then how will the market price of this bond change? | (i) Its price will rise (ii) Its price will drop (iii) Its price will remain unchanged (iv) I don’t know |

| 7. Imagine that your income puts you in the 25% tax bracket. You earn 5000 yuan per month and contribute 1000 yuan before tax to cover all of your social security and pension plan payments. What would your take-home pay be? | (i) 5000 yuan (ii) 4000 yuan (iii) 3000 yuan (iv) 2000 yuan (v) I don’t know |

| Question | Correct Responses (%) | Wrong Responses (%) | Do Not Know (%) |

|---|---|---|---|

| Q1: Compound interest | 78.1 | 17.7 | 4.2 |

| Q2: Inflation | 71.9 | 23.0 | 5.1 |

| Q3: Risk diversification | 43.3 | 27.4 | 29.3 |

| Q4: Mortgage repayment | 67.3 | 21.6 | 11.1 |

| Q5: Choosing a mortgage loan | 70.0 | 24.2 | 5.8 |

| Q6: Bond pricing | 28.4 | 60.4 | 11.2 |

| Q7: Income tax | 58.2 | 35.0 | 6.8 |

| Financial Literacy Overconfidence (%) | Financial Literacy Underconfidence (%) | |

|---|---|---|

| Age | ||

| 25–29 | 41.8 | 10.4 |

| 30–34 | 43.2 | 12.8 |

| 35–39 | 44.3 | 16.9 |

| 40–44 | 32.4 | 21.7 |

| 45–49 | 38.9 | 14.5 |

| 50–54 | 45.8 | 14.2 |

| 55–59 | 45.0 | 8.3 |

| 60–64 | 56.5 | 8.7 |

| Sex | ||

| Male | 38.0 | 16.2 |

| Female | 45.5 | 12.1 |

| Education | ||

| <College | 56.6 | 10.1 |

| College graduate | 40.6 | 14.4 |

| Postgraduate | 31.9 | 17.2 |

| Questions | Answers (%) |

|---|---|

| 1. Which of the following best describes your retirement planning? (Retirement plan) | (i) I do not have a plan (24.16%) (ii) I have a plan, but it is not written down (62.78%) (iii) I have a written plan (13.06%) |

| 2. To what extent (1–5) do you agree with the statement: I have a very good idea of the total value of all my personal retirement savings and investments? (Retirement assets awareness) | (i) Strongly disagree (0.75%) (ii) Somewhat disagree (5.30%) (iii) Neither agree or disagree (22.12%) (iv) Somewhat agree (49.05%) (v) Strongly agree (22.78%) |

| 3. Are you currently participating in a private pension to prepare for your retirement? (Private pension) | (i) Yes (43.79%) (ii) No (56.21%) |

| 4. Are you currently having a variable annuity to prepare for your retirement? (Variable annuity) | (i) Yes (91.88%) (ii) No (8.12%) |

| Variable | Variables Description |

|---|---|

| Retirement plan | Readiness of retirement planning (range 1–3) |

| Retirement asset awareness | Awareness of total value of retirement savings and investments (range 1–5) |

| Private pension | Participation in a private pension to prepare for retirement, 1 indicating yes and 0 indicating no |

| Variable annuity | Having a variable annuity to prepare for retirement, 1 indicating yes and 0 indicating no |

| FL overconfidence | For respondents with objective FL < 4.209 and subjective FL > 3.957, overconfidence = 1, otherwise = 0 |

| FL underconfidence | For Respondents with objective FL > 4.209 and subjective FL < 3.957, underconfidence = 1, otherwise = 0 |

| Objective FL | The objective financial literacy score (range 0–7) |

| Subjective FL | The subjective financial literacy score (range 1–5) |

| Gender | 1 for male, 0 for female |

| Personal income | Annual income (the amount is categorized into range 1–9) |

| Children | Number of children |

| Marriage | Marital status, 1 means married, and 0 otherwise |

| Age | Age (range 25–65) |

| <College | Education below college = 1, otherwise = 0 (benchmark) |

| College graduate | College diploma = 1, otherwise = 0 |

| Postgraduate | Education above college = 1, otherwise = 0 |

| Risk aversion dummy 1 (low) | Degree of risk aversion (range 1–4) |

| Risk aversion dummy 2 | Degree of risk aversion (range 1–4) |

| Risk aversion dummy 3 | Degree of risk aversion (range 1–4) |

| Risk aversion dummy 4 (high) | Degree of risk aversion (range 1–4) |

| Variable | Mean | Std. Dev. | Min | Max |

|---|---|---|---|---|

| Retirement plan | 1.889 | 0.600 | 1 | 3 |

| Retirement asset awareness | 3.878 | 0.845 | 1 | 5 |

| Private pension | 0.573 | 0.495 | 0 | 1 |

| Variable annuity | 0.083 | 0.276 | 0 | 1 |

| FL overconfidence | 0.417 | 0.493 | 0 | 1 |

| FL underconfidence | 0.142 | 0.349 | 0 | 1 |

| Objective FL | 4.209 | 1.585 | 0 | 7 |

| Subjective FL | 3.957 | 0.804 | 1 | 5 |

| Gender | 0.514 | 0.500 | 0 | 1 |

| Personal income | 7.165 | 2.173 | 1 | 9 |

| Children | 0.969 | 0.544 | 0 | 4 |

| Marriage | 0.878 | 0.327 | 0 | 1 |

| Age | 41.675 | 10.034 | 25 | 64 |

| <College | 0.132 | 0.339 | 0 | 1 |

| College graduate | 0.754 | 0.431 | 0 | 1 |

| Postgraduate | 0.114 | 0.318 | 0 | 1 |

| Risk aversion dummy 1 (low) | 0.359 | 0.480 | 0 | 1 |

| Risk aversion dummy 2 | 0.286 | 0.452 | 0 | 1 |

| Risk aversion dummy 3 | 0.134 | 0.341 | 0 | 1 |

| Risk aversion dummy 4 (high) | 0.153 | 0.360 | 0 | 1 |

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| Dependent Variable | Retirement Plan | Retirement Asset Awareness | ||||

| FL overconfidence | 0.248 *** | 0.304 *** | 0.263 *** | 0.272 *** | 0.573 *** | 0.508 *** |

| (0.035) | (0.042) | (0.042) | (0.058) | (0.067) | (0.067) | |

| FL underconfidence | −0.311 *** | −0.508 *** | ||||

| (0.045) | (0.086) | |||||

| Objective FL | 0.028 ** | 0.046 *** | 0.154 *** | 0.179 *** | ||

| (0.014) | (0.014) | (0.022) | (0.022) | |||

| Gender | 0.021 | 0.017 | 0.021 | 0.128 ** | 0.116 ** | 0.124 ** |

| (0.033) | (0.033) | (0.032) | (0.053) | (0.053) | (0.052) | |

| Personal income | 0.073 *** | 0.072 *** | 0.071 *** | 0.049 *** | 0.045 *** | 0.046 *** |

| (0.008) | (0.008) | (0.008) | (0.014) | (0.014) | (0.013) | |

| Children | 0.042 | 0.041 | 0.041 | −0.004 | −0.001 | −0.014 |

| (0.036) | (0.035) | (0.035) | (0.056) | (0.054) | (0.054) | |

| Marriage | −0.009 | −0.010 | −0.020 | 0.114 | 0.110 | 0.096 |

| (0.057) | (0.056) | (0.054) | (0.093) | (0.091) | (0.091) | |

| Age | −0.000 | −0.001 | −0.001 | 0.010 *** | 0.007 ** | 0.007 ** |

| (0.002) | (0.002) | (0.002) | (0.003) | (0.003) | (0.003) | |

| College graduate | −0.057 | −0.065 | −0.067 | 0.194 ** | 0.157 * | 0.148 |

| (0.055) | (0.054) | (0.054) | (0.096) | (0.093) | (0.094) | |

| Postgraduate | 0.018 | 0.005 | 0.005 | 0.260 ** | 0.198 * | 0.187 |

| (0.073) | (0.073) | (0.073) | (0.123) | (0.120) | (0.120) | |

| Risk aversion dummy 1 (low) | 0.193 *** | 0.155 ** | 0.121 * | 0.235 ** | 0.022 | −0.023 |

| (0.068) | (0.068) | (0.067) | (0.117) | (0.118) | (0.113) | |

| Risk aversion dummy 2 | 0.279 *** | 0.249 *** | 0.221 *** | 0.217 * | 0.052 | 0.019 |

| (0.070) | (0.070) | (0.069) | (0.118) | (0.118) | (0.113) | |

| Risk aversion dummy 3 | 0.114 | 0.082 | 0.052 | 0.155 | −0.024 | −0.062 |

| (0.075) | (0.075) | (0.074) | (0.130) | (0.129) | (0.124) | |

| Risk aversion dummy 4 (high) | 0.142 * | 0.100 | 0.078 | 0.261 ** | 0.026 | 0.000 |

| (0.075) | (0.075) | (0.075) | (0.132) | (0.134) | (0.129) | |

| Constant | 0.898 *** | 0.826 *** | 0.871 *** | 2.628 *** | 2.184 *** | 2.278 *** |

| (0.159) | (0.163) | (0.166) | (0.304) | (0.309) | (0.284) | |

| Region Effect | YES | YES | YES | YES | YES | YES |

| Observations | 1266 | 1266 | 1266 | 1063 | 1063 | 1063 |

| R-squared | 0.180 | 0.183 | 0.209 | 0.100 | 0.140 | 0.171 |

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| Dependent Variable | Private Pension | Variable Annuity | ||||

| FL overconfidence | 0.149 * | 0.309 *** | 0.281 *** | 0.380 *** | 0.632 *** | 0.644 *** |

| (0.078) | (0.100) | (0.101) | (0.113) | (0.149) | (0.152) | |

| FL underconfidence | −0.204 * | 0.065 | ||||

| (0.114) | (0.175) | |||||

| Objective FL | 0.081 ** | 0.092 *** | 0.119 ** | 0.117 ** | ||

| (0.032) | (0.033) | (0.053) | (0.053) | |||

| Gender | 0.025 | 0.013 | 0.016 | −0.028 | −0.031 | −0.033 |

| (0.075) | (0.075) | (0.075) | (0.109) | (0.110) | (0.110) | |

| Personal income | 0.034 * | 0.033 * | 0.032 * | 0.046 | 0.044 | 0.044 |

| (0.019) | (0.019) | (0.019) | (0.030) | (0.031) | (0.031) | |

| Children | 0.072 | 0.068 | 0.069 | 0.325 *** | 0.325 *** | 0.324 *** |

| (0.078) | (0.077) | (0.077) | (0.103) | (0.105) | (0.105) | |

| Marriage | 0.080 | 0.077 | 0.070 | −0.352 * | −0.348 * | −0.347 * |

| (0.129) | (0.128) | (0.128) | (0.201) | (0.200) | (0.201) | |

| Age | 0.001 | −0.001 | −0.001 | 0.016 *** | 0.014 ** | 0.014 ** |

| (0.004) | (0.004) | (0.004) | (0.006) | (0.006) | (0.006) | |

| College graduate | −0.001 | −0.027 | −0.027 | 0.001 | −0.033 | −0.032 |

| (0.121) | (0.121) | (0.121) | (0.163) | (0.167) | (0.166) | |

| Postgraduate | 0.085 | 0.048 | 0.050 | 0.432 * | 0.380 * | 0.383 * |

| (0.162) | (0.163) | (0.163) | (0.222) | (0.225) | (0.224) | |

| Risk aversion dummy 1 (low) | 0.622 *** | 0.522 *** | 0.501 *** | 0.096 | −0.019 | −0.011 |

| (0.157) | (0.162) | (0.163) | (0.257) | (0.269) | (0.266) | |

| Risk aversion dummy 2 | 0.533 *** | 0.458 *** | 0.441 *** | 0.430 * | 0.337 | 0.343 |

| (0.160) | (0.163) | (0.164) | (0.253) | (0.259) | (0.257) | |

| Risk aversion dummy 3 | 0.545 *** | 0.465 ** | 0.446 ** | 0.457 * | 0.349 | 0.356 |

| (0.177) | (0.181) | (0.181) | (0.271) | (0.277) | (0.274) | |

| Risk aversion dummy 4 (high) | 0.597 *** | 0.484 *** | 0.471 *** | 0.187 | 0.056 | 0.062 |

| (0.173) | (0.179) | (0.180) | (0.276) | (0.289) | (0.286) | |

| Constant | −0.875 ** | −1.085 *** | −1.061 *** | −2.768 *** | −3.148 *** | −3.163 *** |

| (0.378) | (0.391) | (0.390) | (0.498) | (0.526) | (0.526) | |

| Region Effect | YES | YES | YES | YES | YES | YES |

| Observations | 1263 | 1263 | 1263 | 1232 | 1232 | 1232 |

| Pseudo R-squared | 0.051 | 0.055 | 0.057 | 0.100 | 0.107 | 0.107 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Chen, B.; Chen, Z. Financial Literacy Confidence and Retirement Planning: Evidence from China. Risks 2023, 11, 46. https://doi.org/10.3390/risks11020046

Chen B, Chen Z. Financial Literacy Confidence and Retirement Planning: Evidence from China. Risks. 2023; 11(2):46. https://doi.org/10.3390/risks11020046

Chicago/Turabian StyleChen, Bingzheng, and Ze Chen. 2023. "Financial Literacy Confidence and Retirement Planning: Evidence from China" Risks 11, no. 2: 46. https://doi.org/10.3390/risks11020046