1. Introduction

The modern financial securities markets are populated with a wide array of market players, such as hedge funds, high-frequency firms, and other institutional and retail traders, who execute trades at various timescales, from several milliseconds to multiple days. Therefore, asset prices are driven by multiscale forces. Depending on the timescales, their price patterns may be quite different. These observations lead us to examine the multiscale properties of financial time series.

The original Brownian motion stock model by [

1] intrinsically determines return distribution at any timescale as a result of independent increments and memory-less properties. Fractional Brownian motion has been proposed to challenge the efficient market hypothesis (EMH) and replace the standard Brownian motion model for asset prices (see [

2,

3]). It leads to a much wider class of stochastic processes with additional scaling and long-memory properties, and also allows for arbitrage opportunities, as pointed out by [

4]. Fractional Brownian motion has become an important tool in financial modeling with various applications (see [

5,

6], among others).

As high-frequency data become increasingly available, more sophisticated models are needed to capture their dynamics. Multiscale models designed for low-frequency daily data, such as those by [

7,

8,

9], can hardly fit the complex structure of high-frequency data, especially for (co)variance modeling (see [

10,

11]). It also leads to a host of new research problems, ranging from stochastic models for intraday prices and their estimations to price dependency and portfolio management implications (see, e.g., [

12]).

Various approaches have been proposed to analyze the complex structure of high-frequency prices, especially their realized volatility (see, for example, [

10,

13]). Nevertheless, market microstructure research by [

14,

15], among others, suggests that there is noise at a higher frequency. As a consequence, the market microstructure noise can potentially bias estimation of the scaling parameters. For example, as shown by [

16], the discrepancy between realized and instantaneous volatility can lead to bias in the estimation of the Hurst exponent ([

17]). A common idea in various approaches is to conduct measurement at multiple timescales, and then, assimilate the outputs to arrive at an estimate (see [

11,

18,

19,

20,

21]).

In our companion paper [

22], we investigate the theoretical and empirical properties of multiscale volatility of high-frequency data. Using a fractional Brownian motion model, we estimate the Hurst exponent and noise level and illustrate the time-varying intraday patterns. In this paper, we investigate the connections between correlations and timescales of high-frequency prices. In addition, we incorporate market microstructure noise into our model to better understand how noise can affect the multiscale behaviors and associated statistical properties of correlations. This also allows us to estimate the microstructure noise realized at different times of the day, or compare the noise levels among various traded assets.

Our study begins with the definitions of multiscale correlation and some important properties in several stochastic models. In order to model high-frequency price processes, a class of multivariate noisy fractional Brownian motion models is introduced. Our analysis on multiscale correlation leads us to an equation that connects correlation and frequency. Moreover, the effect of microstructure noise is expressed analytically and examined empirically. Using intraday high-frequency price data, we illustrate the estimated correlation–frequency relationship and microstructure noise level for a collection of ETFs and stocks.

We present the definition and properties of multiscale covariance and correlation in

Section 2. A fractional Brownian motion model with microstructure noise is introduced in

Section 3. This leads to an analysis of the asymptotic behaviors and timescale dependence of multiscale correlation. Several illustrative examples are provided to show the correlation structures over different timescales. In

Section 4, the model is estimated using empirical data. We conclude the paper in

Section 5.

2. Multiscale Correlation

We consider a collection of

p financial assets whose prices at time

t are denoted by the vector

. Converting to log prices

, the log return vector over the time interval from

t to

is given by

All operations are applied element-wise. The multiscale covariance matrix can be defined as

We remark that if

is a stationary multivariate process, then

must be a matrix dependent on the time increment

only at any time

t. Next, we define the notions of multiscale pair-wise covariance and correlation.

2.1. Definition and Properties

Definition 1. Let the pair of log prices and be stationary processes on . For , the multiscale covariance between X and Y is defined asIn turn, their multiscale correlation is defined as Although there is no restriction on the form of the function, the multiscale correlation behavior is limited for a wide class of processes.

Proposition 1 (uncorrelated increments)

. For any pair of stationary random processes has jointly uncorrelated increments, i.e., For any , the correlation function must be a constant in τ. Proof. We first show that the covariance

scales linearly with

:

For any

; let us show the additive-ness

. Consider that

; then,

Then,

. Following the same derivation, the multiscale variance of the two processes also satisfies

and

. Therefore, the correlation must remain a fixed constant for all values of

:

□

This means that, for the stationary processes in Proposition 1, the mulstiscale correlation stays the same at any time scale over which the correlation is computed.

Example 1 (stochastic volatility model)

. Let and be independent standard Brownian motions. For and , define the following pair of correlated stochastic processes: where the volatility processes areIn the stochastic volatility model above, , and are independent Brownian motions. The processes are correlated through a shared Brownian motion, so they do not have independent increments. Nevertheless, their increments are jointly uncorrelated given thatfor any . Therefore, the correlation between and is scale-independent. Proposition 2. Let be a sequence of independent processes, and be another sequence of independent processes. Further, assume that . Denote the sequence summations by and Then, the multiscale correlation between the summation of the two sequences is given by Proof. Direct computation of the covariance yields the covariance

The variance terms in the denominator of (

5) follow from the independence of

and

. □

Remark 1. Note that in Equation (5), even if is constant for all , the correlation of the two summations can still be scale-dependent if the variance scaling behavior is different among the pairs . 2.2. Numerical Estimation

In order to estimate the multiscale correlation function from discrete observations, we consider a given pair of time series, , for . The multiscale correlation can be estimated as follows.

For :

Compute variance

using

where

are estimated drifts.

We will apply these expressions in the sections below.

3. Multivariate High-Frequency Models

In this section, we discuss multiscale volatility in the intraday setting with high-frequency prices. The definitions of fractional Brownian motions are based on the seminal work of [

3]. Then, we incorporate additional elements into the fractional Brownian motion model to create interesting scaling behaviors.

3.1. Correlated Fractional Brownian Motions

Definition 2. A fractional Brownian motion (fBm) , is a continuous-time Gaussian process that satisfies , and has the following covariance function:where , and is called the Hurst exponent. As is well know, in the case of , we obtain the standard Brownian motion. When , the fractional Brownian motion is called anti-persistent or mean-reverting, and its increments are negatively correlated. When , the fBm has positively correlated increments and is called persistent or trending.

A fractional Brownian motion adopts various forms of stochastic integral representation, which can be found in Chapter 1.2 of [

23] and references therein. In this study, we focus on the following representation to construct a fractional Brownian motion from an underlying standard Brownian motion:

where

is the underlying Brownian motion. We will apply this representation to define correlated fractional Brownian motions and generate sample paths of fractional Brownian motions.

The correlation between Brownian motions has been well established for a long time. Like any random walk with stationary and independent increments, Brownian motion also has scale-independent correlation, as shown in Proposition 1. The correlation between fractional Brownian motions was studied more recently in the setting of multivariate fractional Brownian motion (mfBm) [

24,

25,

26,

27]. To begin with, let us first define a pair of correlated fractional Brownian motions using Equation (

7) and study their correlation property.

Proposition 3. For any Hurst exponent pair , and for any correlation coefficient , define the following pair of correlated fractional Brownian motions:where and are independent standard Brownian motions, and the operator is defined in Equation (7). Then their multiscale correlation function is as follows: Proof. Without loss of generality, let us take

in Equation (

3) and analyze the increments from 0 to

. The covariance between

and

is

Note that we have used linearity of the

operator. To compute the expectation of the product of two stochastic integrals, we apply the generalized Ito isometry to obtain

Using a change in variable

, we can write

where

is the integral

In turn, we obtain the covariance

Here, we refer to [

28] for canceling the integral

with the normalizing factor. The variance terms can be verified by taking

:

And by the definition of correlation,

□

More general multivariate fractional Brownian motion can be defined through self-similarity in vector form. Its covariance structure is given in Theorem 2.1 of [

29]. One can show that the pair-wise correlation will still be constant.

Next, we discuss the scale-independent correlation in a more general case, with multivariate fractional Brownian motion being a special example. To this end, let us define self-similarity formally in a multivariate scenario.

Definition 3 (self-similarity)

. A p-dimensional multivariate random process is self-similar if there exists a vector , s.t. Proposition 4. For any p-dimensional multivariate random process that is self-similar, the pair-wise multiscale correlation between any must be a constant.

Proof. We prove this by showing that for any

,

. Due to self-similarity, their variance functions satisfy

The covariance is given by

Then, we have

□

Example 2 (multivariate fractional Brownian motion). A multivariate fractional Brownian motion (mfBm) is a p-dimensional Gaussian process with stationary increments and satisfies self-similarity with . According to Proposition 4, it has scale-independent pair-wise correlation.

3.2. Microstructure Noise in Correlated Prices

In markets with high-frequency prices, the notion of microstructure noise has been proposed and studied; see the early work by [

30], for example. The intuition is that activities by agents in the market that result in transactions, along with various frictions in the trading process, may give rise to “noise” in the observed prices (see [

31]). In the literature, there are different approaches to modeling this. In the recent work by [

16], noise is implicitly modeled based on the discrepancy between stochastic volatility and realized volatility, and it has an effect on estimating the Hurst exponent of the volatility process.

To avoid any confusion on the concept of “market microstructure noise”, we fix our modeling to be the same as the form in [

14,

19,

20], among others. In this section, we are going to establish the multiscale behaviors of microstructure noise generalized into a multivariate case.

Definition 4. Let be a p-dimensional stochastic process. We denote the multivariate noisy price process aswherefor , and is the independent random noise vector such that , , , and i.i.d., for . The covariance matrix is a positive semi-definite matrix. Property 1. For any p-dimensional noisy price processthe pair-wise multiscale correlation between i and j, , is Proof. The multiscale covariance in the noise is

The rest of the process is to apply Proposition 2 and calculate the denominator in the same manner. □

Note that even if is scale-independent, can still be scale-dependent, as long as the multiscale variance of the underlying process is not constant. We remark that the multiscale variance is most likely to depend on the timescale unless the price is pure noise. Therefore, for almost all price processes, its noisy process will have scale-dependent correlation.

Lastly, the off-diagonal entries of the covariance matrix, , for , reflect the correlations among the microstructure noises from different price processes. If the noises are independent, then these entries are zero. Our framework, without further assumptions or specifications, does not require them to be zero.

3.3. Noisy Fractional Brownian Motion

We now consider a bivariate noisy fractional Brownian motion model for a pair of asset price processes. This leads to the analytical and numerical studies of the associated correlation structure and asymptotic behaviors.

Definition 5. For Hurst exponents , drift coefficients ; volatility parameters ; initial values ; and correlation coefficient define the pair of noisy fractional Brownian motions:where and are independent Brownian motions, and and are microstructure noises with variance , , and correlation . 3.3.1. Correlation Curve

Applying Proposition 3 and Property 1 gives the multiscale correlation of noisy fractional Brownian motions. Denote

:

as the noise ratios. As a general case, let us first consider the microstructure noise

to be correlated, i.e., the noise correlation

. The multiscale correlation is given by

If the microstructure noises are assumed to be independent, then

and the above formula can be simplified to

We can see from Equation (

12) that the noisy correlation is just the underlying correlation times a scaling factor, which depends on the noise ratios and the Hurst exponents of the underlying processes. In the special case where

, i.e., the log price processes are noisy Brownian motions, we have

3.3.2. Asymptotic Behavior

Next we consider the asymptotic behavior of multiscale correlation. Results are derived for a general case assuming that the microstructure noises could possibly be correlated, followed by a special case of independent noise.

The correlation converges to the correlation between the two underlying fractional Brownian motions.

Unlike volatility, the limit of correlation exists when the timescale is approaching zero. The intercept depends on the correlation between the noises, which can be used to determine if there are correlated noises. Also, note that the asymptotic behavior of correlation does not depend on the Hurst exponent H at both ends, which is different from the volatility function. The Hurst exponent only affects the rate at which correlation to the underlying value increases.

In order to better understand the speed of correlation scaling, let us further look at the derivative of the correlation function. We can derive

The form is rather complicated, with one fBm correlation term and one noise correlation term. Let us look at its asymptotic behaviors under certain conditions.

,

- –

Case

:

where

as the minimizer of

. We can see that the noise correlation term doesn’t affect the asymptotic behavior at a large scale, and the limiting behavior is controlled by the smaller Hurst exponent.

- –

This function form is the same as the case; however, it is surprising that the noise correlation term plays a part in the asymptotic behavior even at very large scale. A positive correlation in the noise will actually decrease the speed of correlation convergence.

,

- –

Again, the smaller Hurst exponent controls the limiting behavior. Also, note that positive noise correlation leads to a negative derivative in the correlation at small scale.

- –

As in the large-scale limit scenario, equal Hurst exponents make the derivative contribution of fBm correlation and noise correlation balanced throughout the whole correlation curve.

In general, the contribution of the fBm and the noise terms to the correlation derivative is sensitive to the difference between the Hurst exponents. If the Hurst exponents are different, it is always the smaller one dominating the asymptotic behavior at both small and large scales. The dominant term is different at the two ends though. When the two processes have identical Hurst exponents, the fBm and the noise terms are balanced at any scale and weighted according to the arithmetic mean and the geometric mean of the noise ratios.

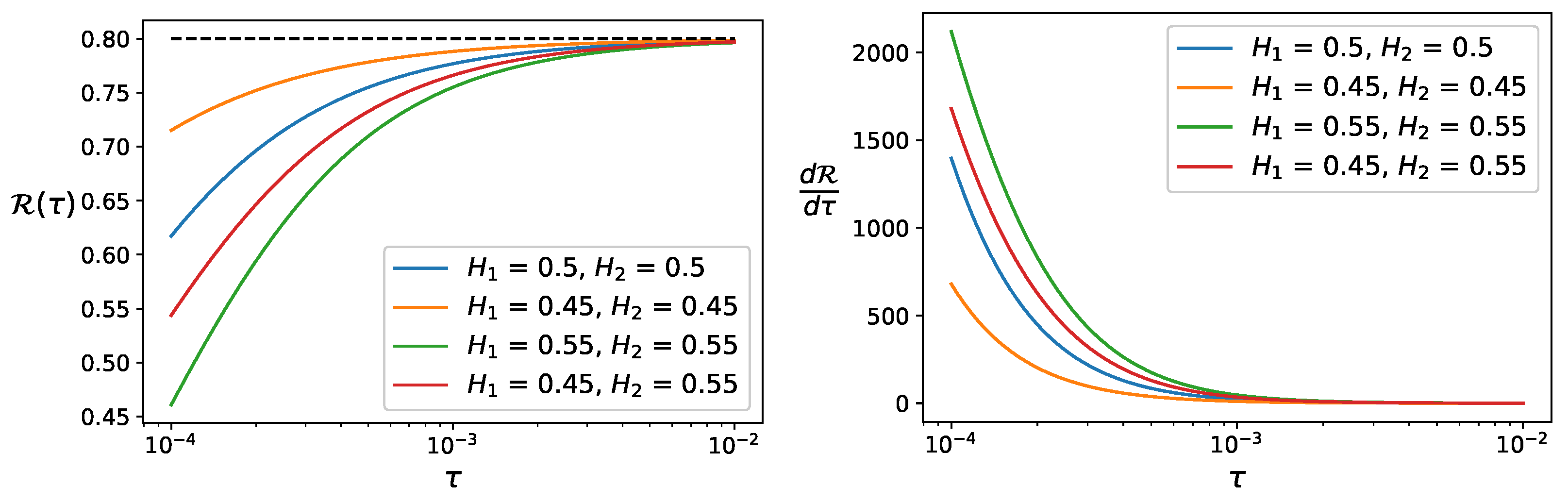

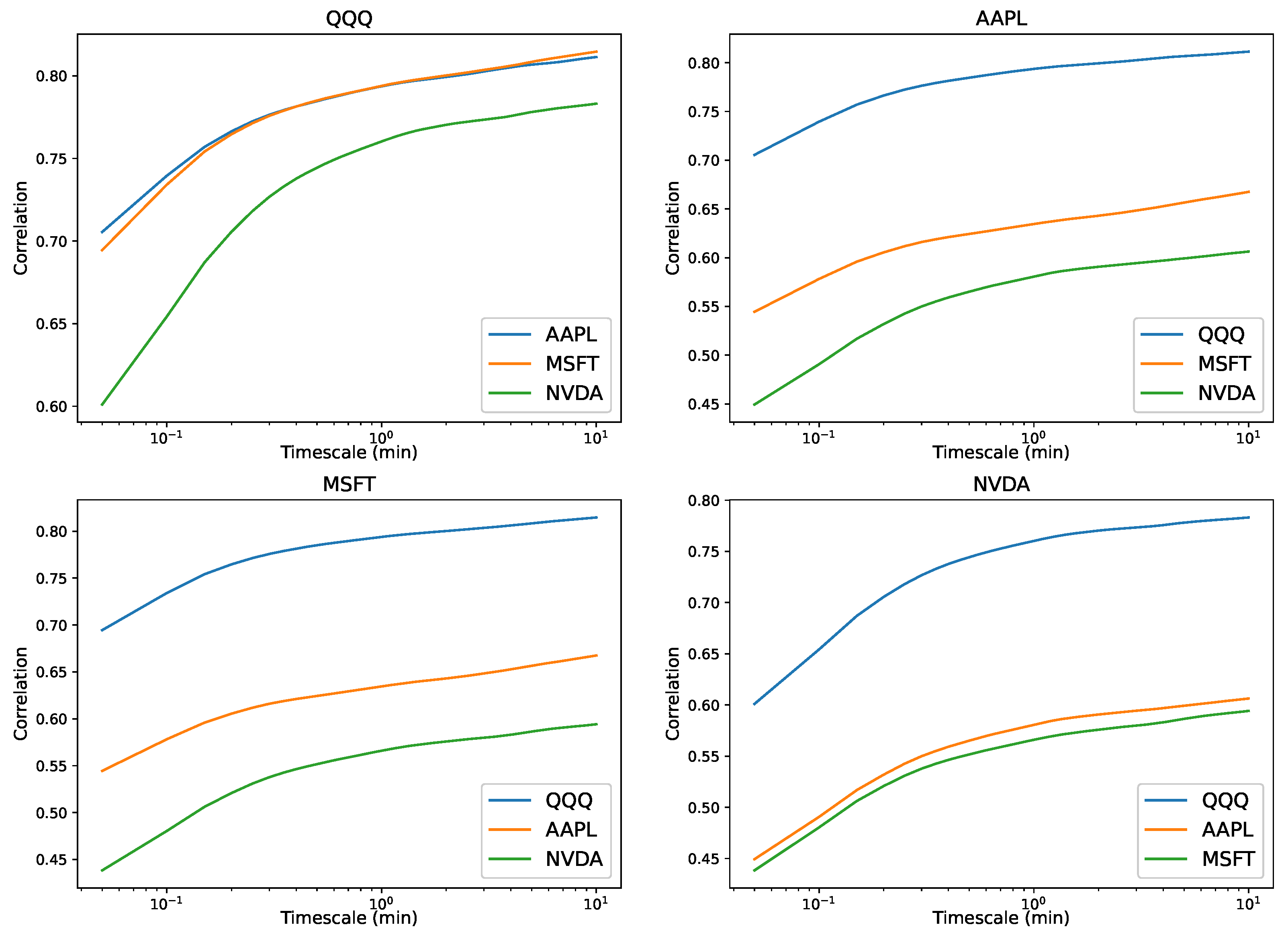

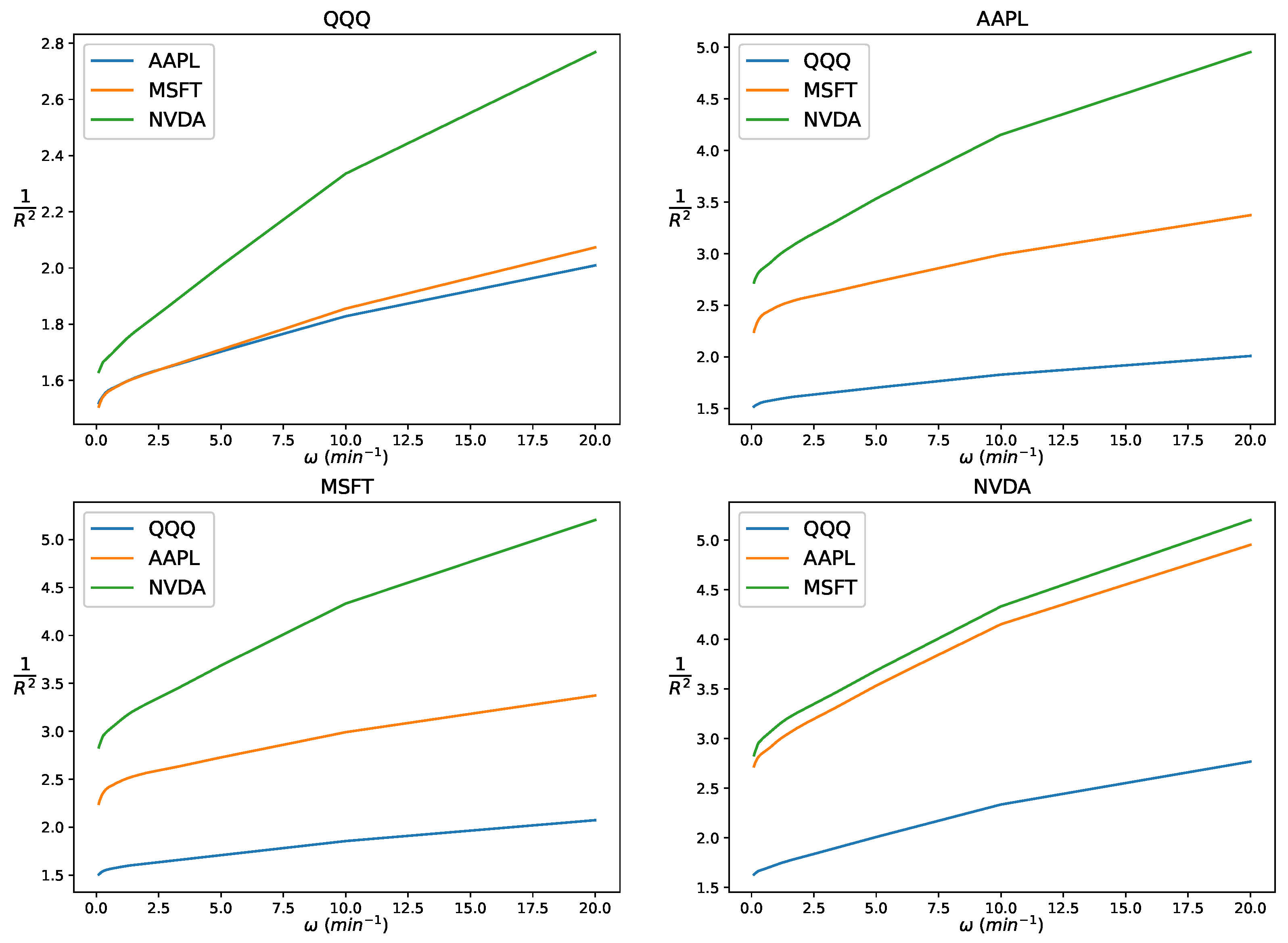

Figure 1 shows the correlation and derivative as a function of

in the noisy fractional Brownian motion model under different combinations of Hurst exponents. The parameters are

, and

. In other words, the two processes are correlated through the fractional Brownian motions, but their microstructure noises are independent. The correlation curves

all increase in

and approach the constant correlation coefficient

. This can be seen on the right panel as the slopes

start from a high value and decay to zero as

goes from

to

. The one associated with the highest Hurst exponent pair

has the lowest correlation but also increases most rapidly as

increases.

3.3.3. Correlation Curve Evaluation and Fitting

The correlation curve given by Equation (

11) can be rather complicated, with six parameters, making it hard to evaluate against observation from real-world data. One practical approach is to consider the noisy Brownian motion model so that the correlation is given by Formula (

13). Starting from this expression with only three parameters,

, a simple rearrangement yields

Next, if we define the frequency variable

:

and assume that

, we have

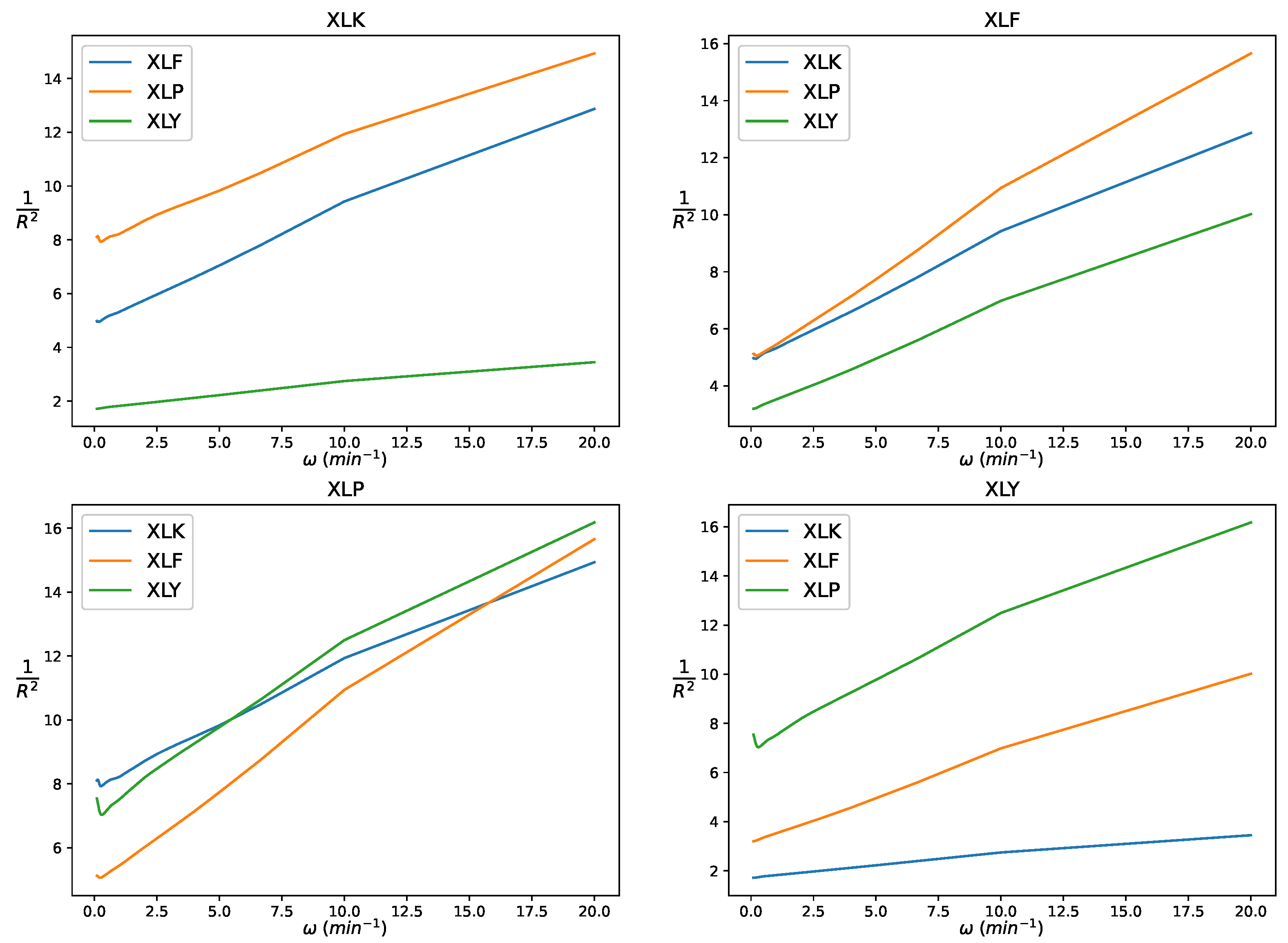

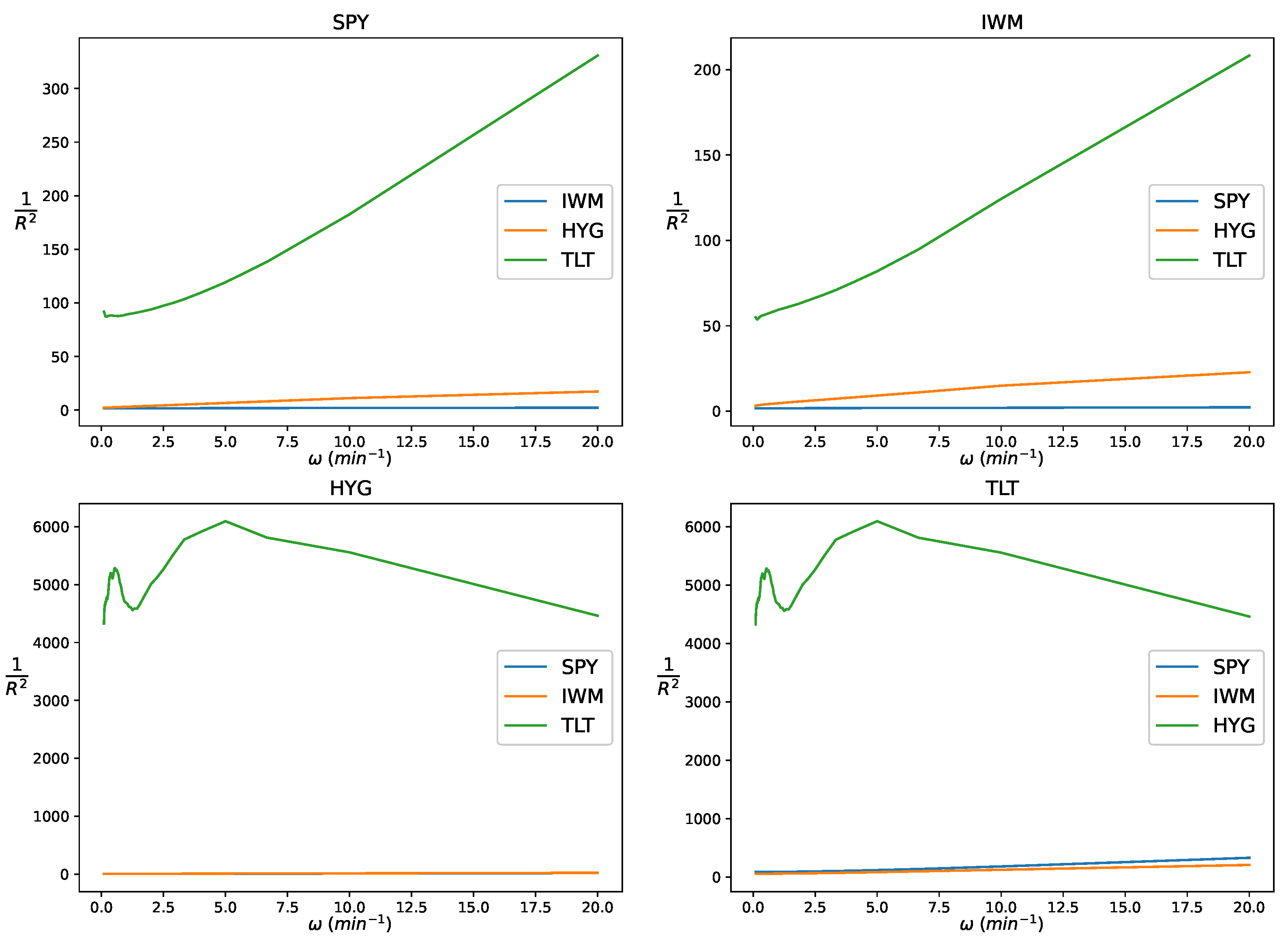

From (15), we observe that the inverse of the correlation squared can be approximated by a linear function in frequency . The intercept is determined by , and the slope is positive and depends on the summation of the two noise ratios . We will return to this as we empirically verify this property with real-world data in the next section

Consider a collection of p noisy Brownian motions , with corresponding noise ratios . Suppose the correlation coefficient between the latent processes of and is ; we can evaluate the parameters following the following procedure:

Compute

,

using Equation (

6), and

, for

.

Fit linear regressions for .

Estimate the correlation .

Define the index mapping function , for . The values of are .

Construct the vector , s.t. for .

Construct the matrix , s.t. if there exists s.t. or s.t. ; otherwise, .

Estimate the noise ratio vector

Here, represents the pseudo-inverse of A. For to be solvable, there must be noisy Brownian motions in the collection. When , A is invertible. When , the matrix is over-determined.

5. Conclusions

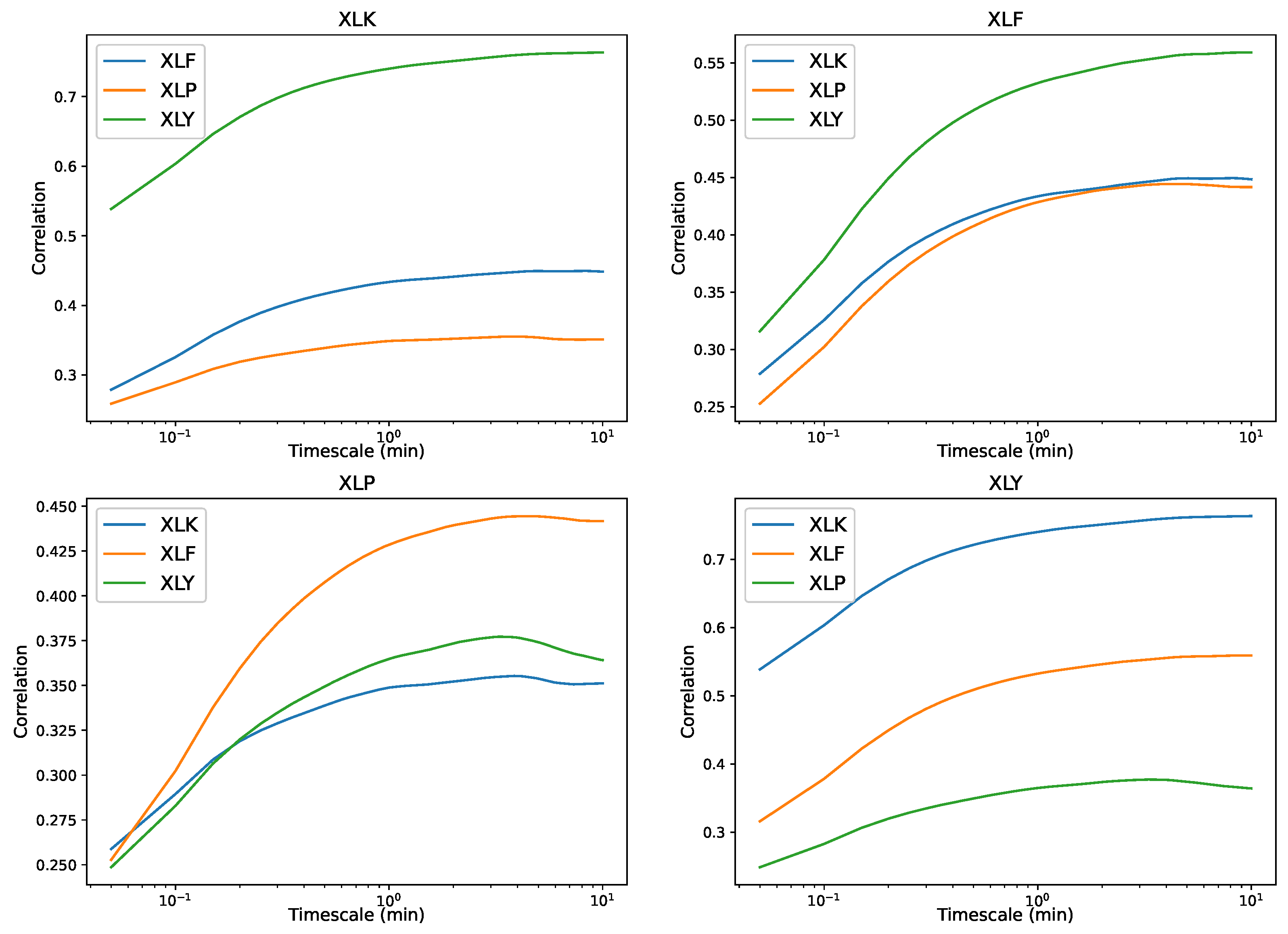

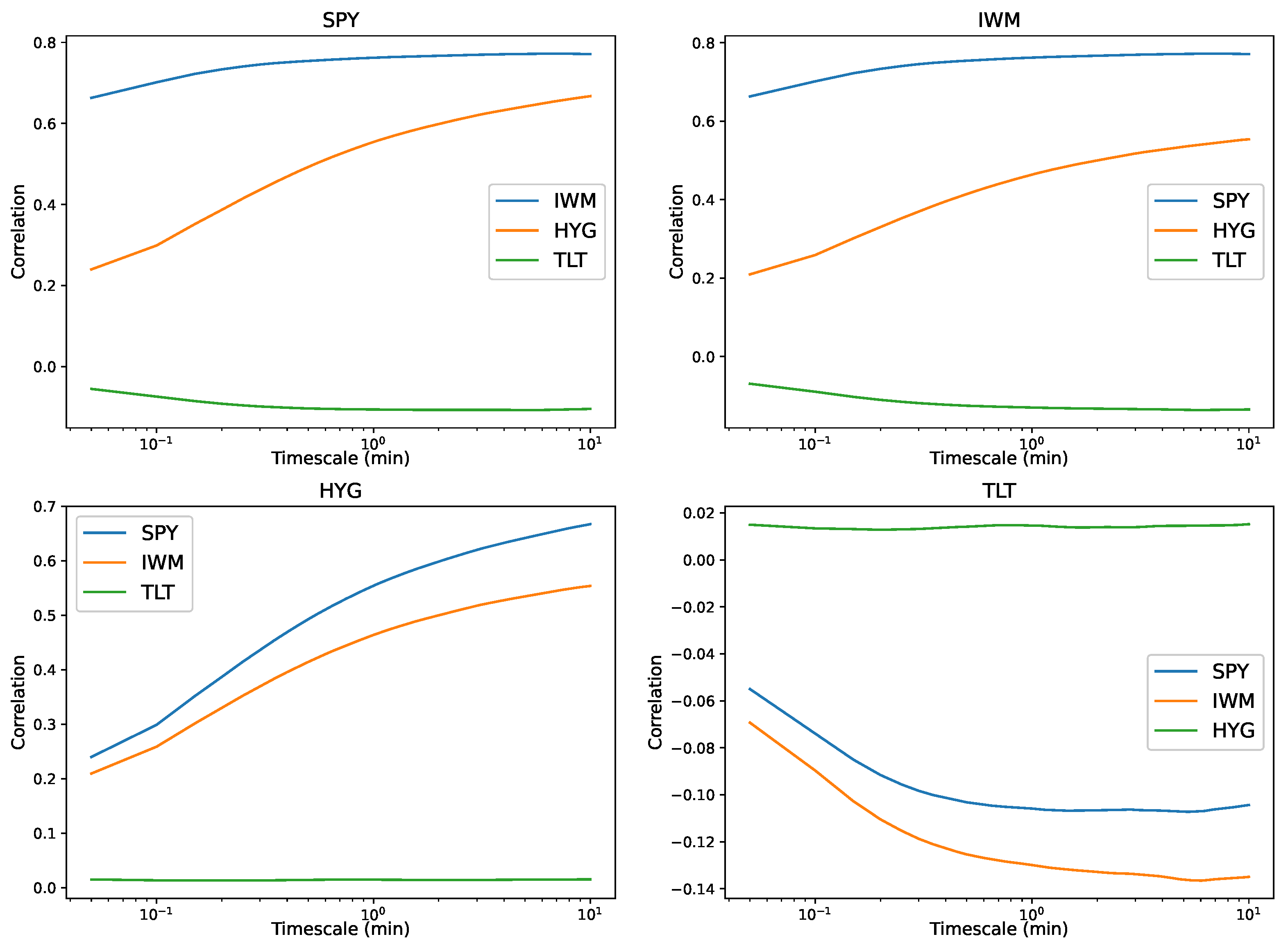

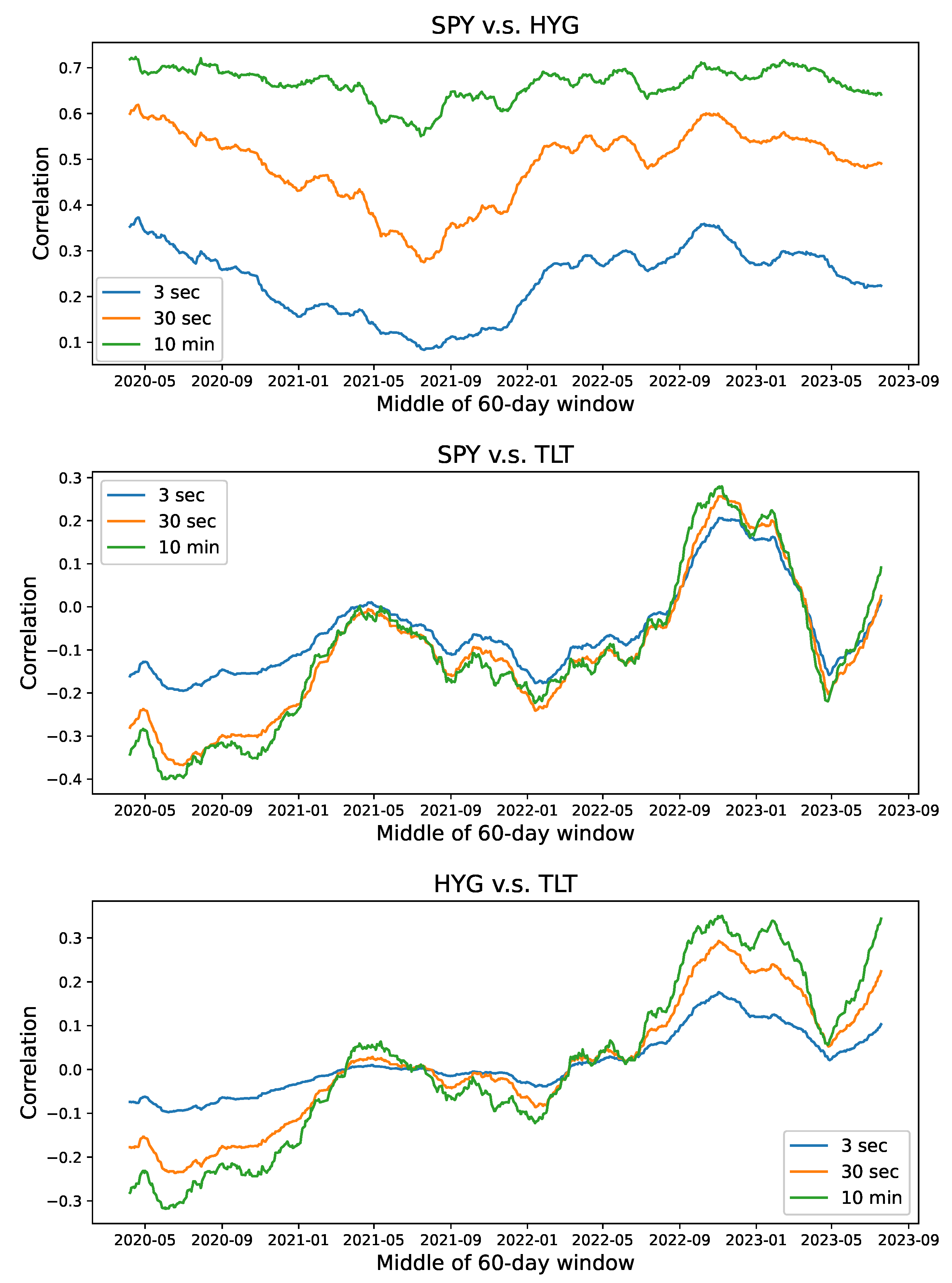

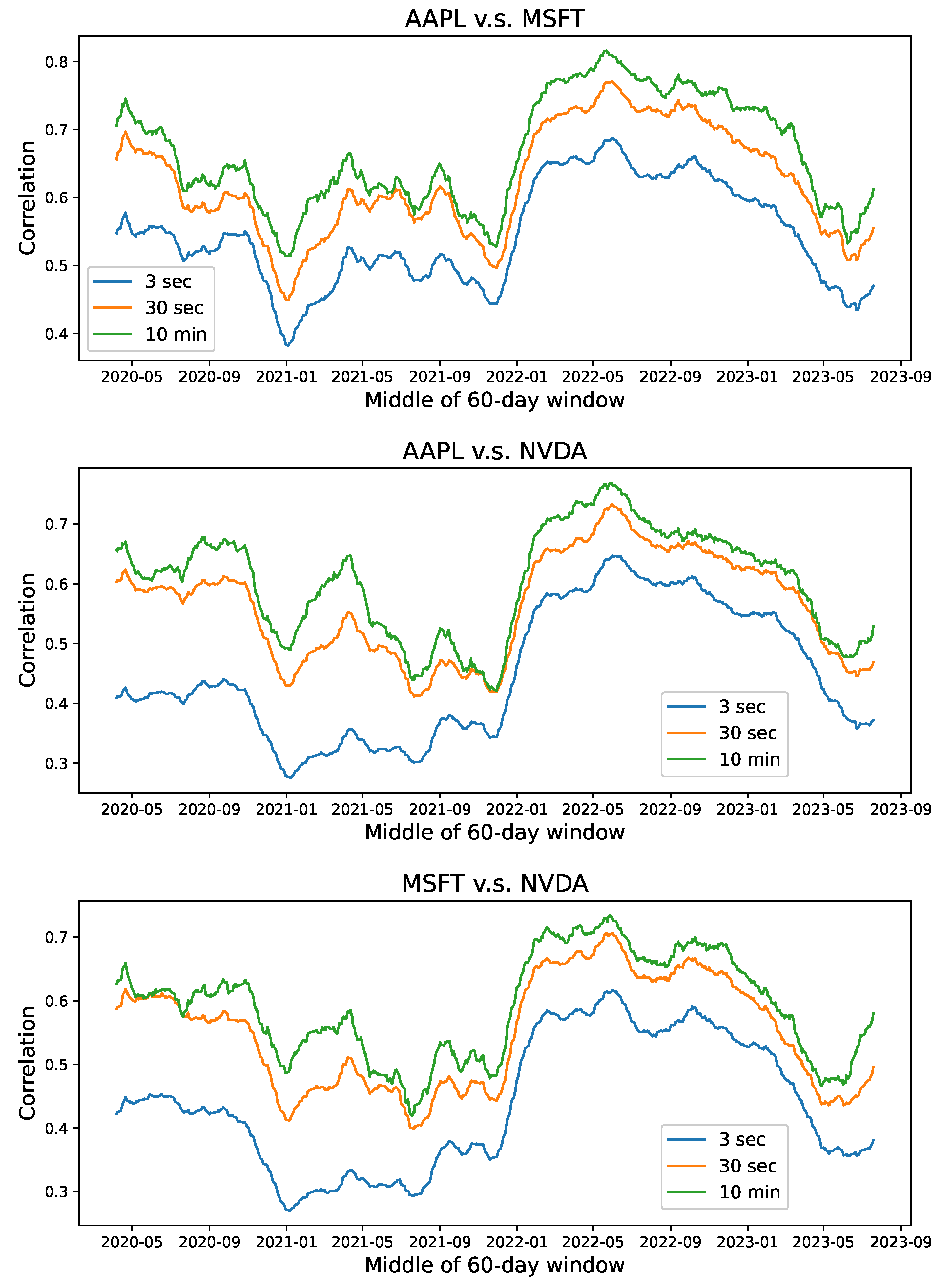

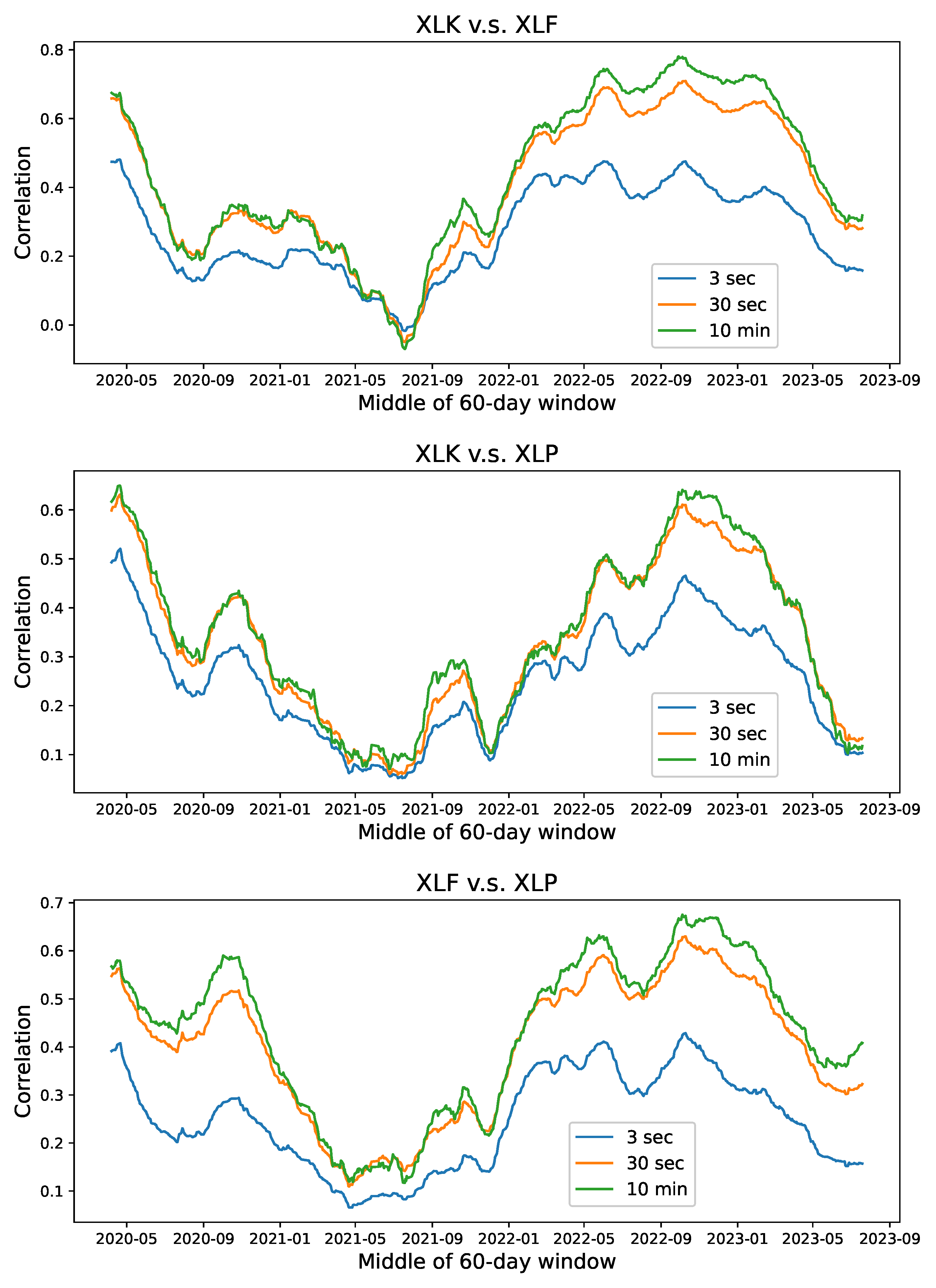

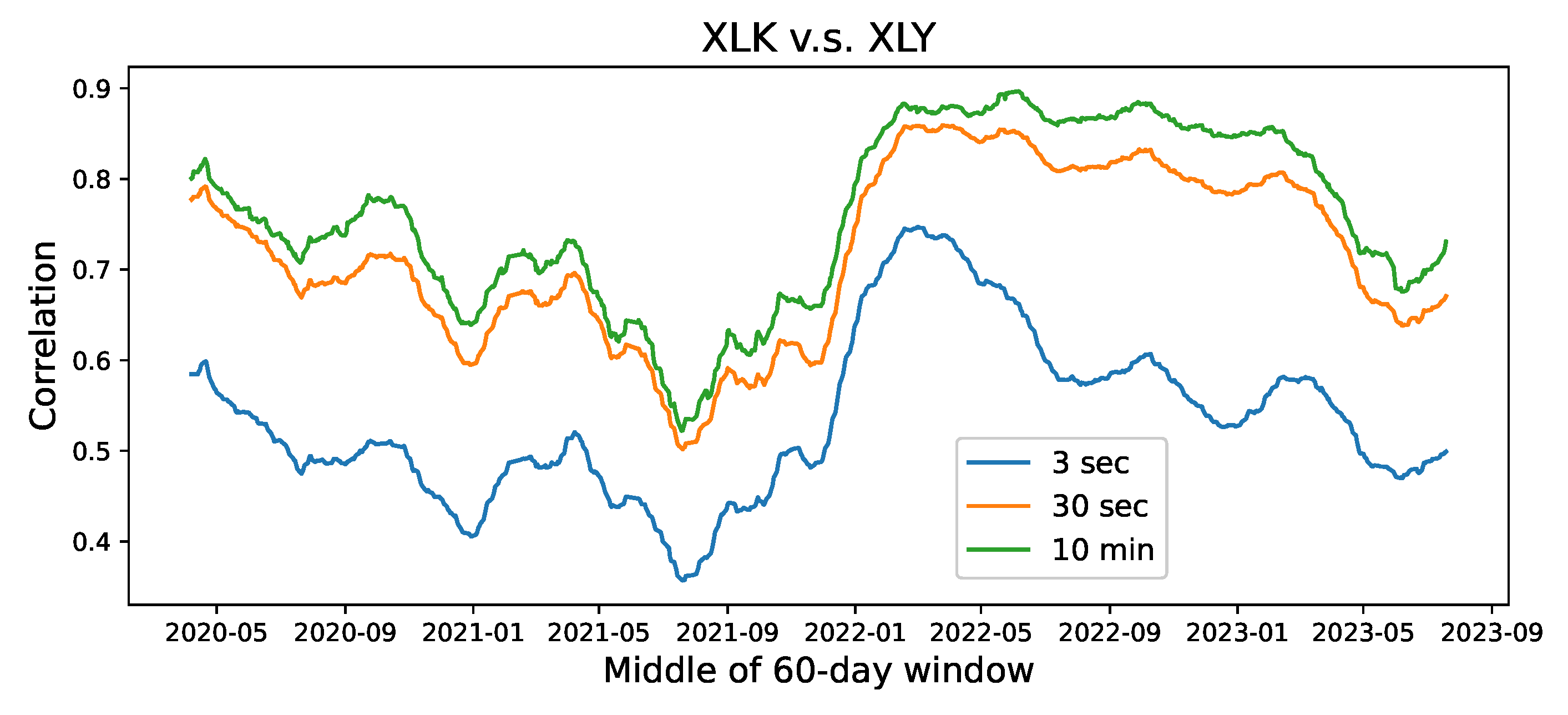

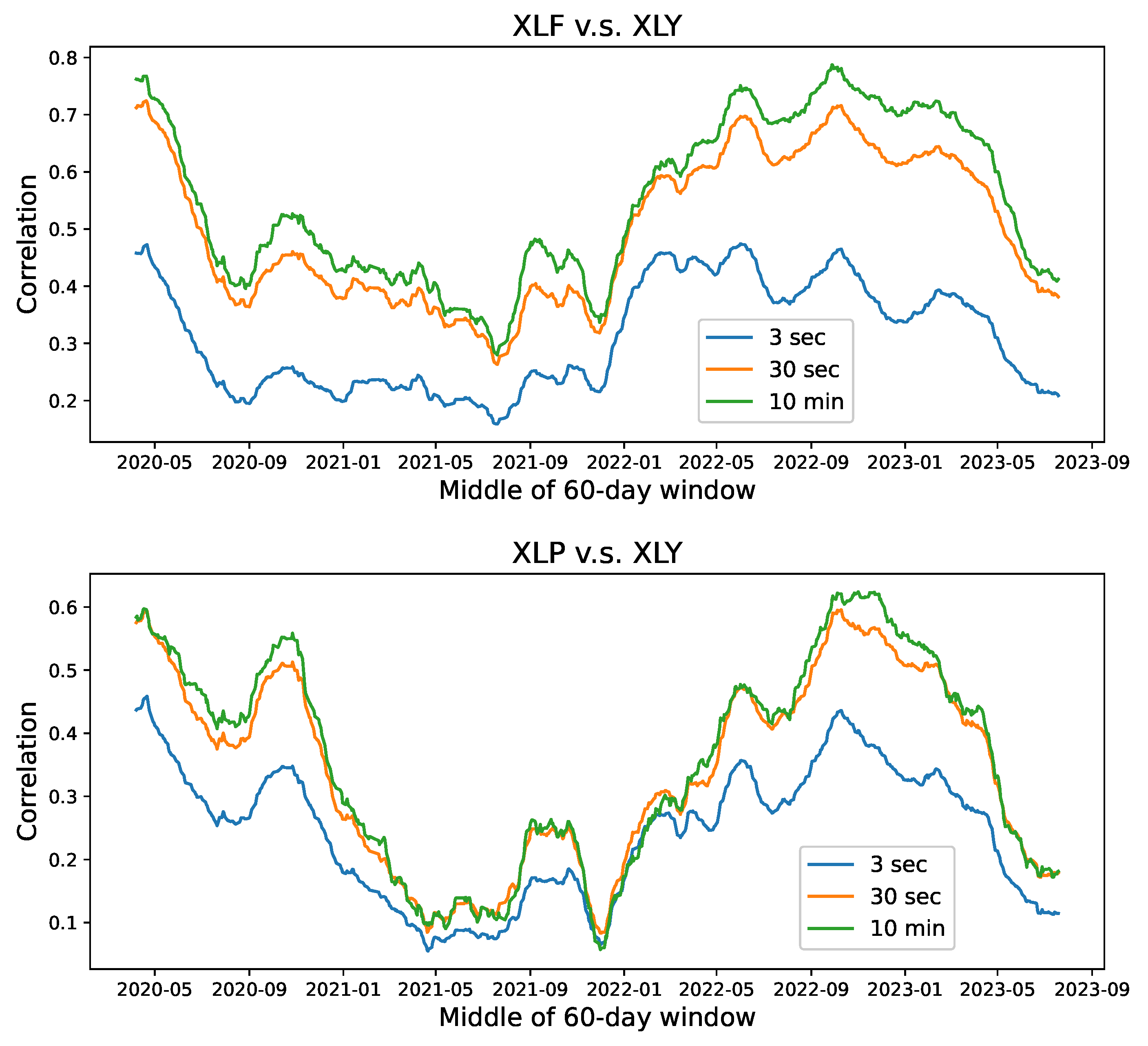

In this paper, we have presented a multiscale correlation analysis of noisy high-frequency financial data. The stochastic model studied herein is shown to possess a variety of statistical properties suitable for real-world intraday prices. To extract the correlation structure from prices, we devise a novel Hurst exponent estimator based on our model and estimate the exponent using a collection of major US stocks and ETFs. This helps better the understanding of the intraday correlations among asset prices and also the evolution of correlations over time.

The current study also suggests several future directions for further investigation. For instance, machine learning models can be designed to harness the Hurst exponents and other estimates from our model as useful inputs. There are a number of practical applications, including portfolio optimization and risk management at different timescales. Our current study illustrates that the Hurst exponent for different assets may vary significantly. This should motivate authors to conduct research on finding and understanding the factors that give rise to this phenomenon.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}