1. Introduction

Since the pioneer studies in the 1960s until the financial crisis, the consensus has been reached around the optimal central bank and its independence. Supported by theoretical and empirical evidence, this bank should be independent from the government and focus on price stability. It was generally agreed that an independent central bank positively contributes to reducing inflation. In most countries, the central law was adopted supporting its formal independence. This status quo was shaken as the global financial crisis broke in 2007. Since then, many central banks have focused mainly on financial stability (

De Haan and Eijffinger 2017); in addition, the main advanced economies were facing disinflationary pressure. To handle it, the central banks hold the interest rates close to zero or even at negative levels and, in some cases, also using “unconventional

1” tools (

Aguilar et al. 2020).

The COVID-19 pandemic, followed by war in Ukraine, has again disrupted the global economy and will probably leave long-lasting scars. Aggressive fiscal and monetary policy have helped cushion the economic and social impact of the pandemic. Prior to the invasion, the countries were focused on the health and economic challenges caused by the pandemic and the withdrawal of macroeconomic support was set to continue. The expectation was set on gradually tightening monetary policy, unwinding long-term asset purchases, and raising policy rates. The war outbreak has only added an immediate global adverse impact. In response to Russia’s invasion of Ukraine and subsequent actions, a number of countries have adopted financial, trade, and other sanctions. As a response, several economies in Europe and Central Asia have been hard hit because of strong economic connection via trade, commodity, or confidence channels to Russia/Ukraine. With both countries being major exporters of several commodities, the war has triggered large surges and volatility in the prices. It can be concluded that the war has significantly eroded global economic prospects as it amplifies inflationary pressures, creates financial stress, and weakens long-term growth drivers (

Guénette et al. 2022), and central banks in some countries are facing unexpected persistence of inflationary pressures supplemented by high uncertainty about the outlook (

OECD 2022).

As

Blejer and Wachtel (

2020) point out, the last decade has shown some of the constraints on central bank independence. It is still agreed that so far as monetary policy is concerned, the idea of monetary policy independent of political influences is still accepted. However, just as monetary policy can have political implications, central banks must often work or listen to political authorities.

In the perspective of the recent political and economic changes, we consider it necessary to reinvestigate the issue of central bank independence. In the first part of the paper, we will review recent studies focusing on CBI and its different aspects. In the second part of the paper, we will then proceed to a re-evaluation of de jure and de facto independence of OECD member countries within the 1991–2021 period. Data are constructed using individual central bank laws; indices de facto are based on the generally available information about terms of governors as well as chosen political representatives. The data cover a critical period in central bank governance, as the selected time period covers the de jure transformation of many central banks to their current state; it also includes the time period of global financial crisis and COVID-19. The following section of this paper reviews main empirical findings regarding central bank independence in the last decade. The third chapter presents the methodology of measuring central bank independence, followed by the empirical findings.

2. Literature Review

As

Dall’Orto et al. (

2020) states, since the late 1960s an important consensus has been established on the relationship between inflation and growth/unemployment. The next natural questions which emerged were how to keep inflation low and predictable, and how to set up the institutional environment responsible for this target. The consensus, granting central banks independence to conduct monetary policy and holding them accountable to a well-defined price stability, was finally reached. Since the late 1970s until 2000, many advanced economies have adopted a monetary policy framework with price stability as the primary objective (

IMF 2010).

Central bank independence as an individual topic came again under the scrutiny in the era of the global financial crisis, when governments expanded the core tasks and responsibilities of central banks beyond their original mandate in an effort to contain the crisis (

Bandaogo 2021). As

Dall’Orto et al. (

2020) show, the great financial crisis of 2007 led to important changes to the role, instruments, and mandates of central banks, mainly in advanced economies. Many changes were adopted, mostly without fundamentally modifying central banks’ law and without altering monetary policy objectives. This unprecedented expansion in the central banks’ roles and instruments has been criticized for (i) the level of accountability, (ii) conflicting policy targets, (iii) risks from policy coordination, (iv) transgressing the mandate, and (v) distributional concerns. Additionally,

Balls et al. (

2018) show that while the powers of almost all central banks have increased, they were reached by very different means, creating a substantial diversion in their goals, tools, and institutional structure. Along with gaining new powers and responsibilities, this new set up has thrust them into politically contentious areas of policy, requiring cooperating closely with other institutions including governments. In such an environment, the value of central bank independence was being questioned. They argue that a more nuanced approach to central bank independence should be adopted, with political accountability in terms of mandate-setting and the appointment of officials, and oversight of wider financial stability powers.

Alongside this,

Rogoff (

2019) indicates that central banks are left vulnerable to populist attacks that threaten to undermine their independence. This pressure originates from their effectiveness in reducing inflation, and their ineffectiveness in finding ways to deal with the zero lower bound on interest rates. He highlights that if central bank independence is rescinded and monetary policy politicized, it may be even harder to put the inflation genie back in the bottle, as the trust would be broken. The same view is shared by

Bandaogo (

2021), who points out that widening social inequalities have led to the rise of populist leaders who have vowed to place more oversight over central banks and their operations. In addition,

De Haan et al. (

2018) assess that the balance of power between fiscal and monetary policy changes, as with high public debt levels fiscal authorities may be tempted to rely on monetary policy and the threat of fiscal dominance may be particularly strong. The second risk originates from the consequences of central bank policies; the third threat relates to the set of unconventional monetary policies employed.

Bodea and Garriga (

2022) analyze the potential for delegation reversals on the sample of Latin American countries. Their results show that reforms which de-delegate monetary policy have been minor, and there are incremental changes in legislation without prior major efforts to delegitimize central banks as institutions. Ecuador’s central bank is given as an example of major de-delegation and politicization, while other countries such as Argentina and Venezuela proceeded with only marginal legislation adjustments. As

Kern and Seddon (

2020) point out, CBI has been attacked since the time monetary powers have been delegated. Based on historical evidence of Reichsbank in 1930s, they have provided a theoretical framework showing that weakening international creditors and the diminishing political potency of multilateral organizations substantially reduces the opportunity costs of reigning in central bank independence.

Masciandaro and Romelli (

2015) design a political economy framework explaining how the politicians can shape central bank governance. They argue that the policymaker’s actual choices related to the central bank governance are conditioned by the existing economic and institutional environment.

In addition, some authors use narrative approaches to study political pressure on central banks.

Binder (

2021) introduces a dataset of political pressure faced by central banks around the world. In her study, based on country-level reports, she shows that about 10% of central banks reportedly face political pressure in an average year. This reported pressure is very often connected with higher inflation and inflation persistence and more likely comes from left-wing or nationalist governments.

Blinder et al. (

2017) carried out two surveys of opinions—one of governors of central banks, the other of academic specialists. The results suggest that there are differences between the views of both groups. More than 90% of central bank governors and 80% of academics claim that the central bank independence either did not change or was reduced only “a little”. The following question considered the issue of near-future threats to central bank independence. They found the results slightly surprising, as academics are far more concerned (37% express “a lot” or “a moderate amount”) whereas only 9% of central bankers agree.

Dall’Orto et al. (

2020) collected information, based on news reports and official sources, for 13 central banks. The data were used to assess quantitatively what the direction of de facto independence is of those banks. Where the authors did not identify any significant legal changes, except for the Central bank of the Republic of Türkiye (CBRT), de facto independence was affected in almost half of their samples. Based on the provided evidence, the government attacks or interferes in order to pressure monetary policy to support growth objectives. The results show that de facto independence may have deteriorated in nearly half of the samples, mainly in the area of institutional independence. As the endogenous evolution of monetary institutions caused by the recent crises could be considered as an incentive to undertake reforms, this paper analyzes central bank de jure and de facto independence of a set 38 OECD member countries, covering the period 1989–2021.

Recent studies, analyzing CBI and its implications, commonly put CBI under scrutiny as an explanatory variable for variety of issues. Many studies, while commonly using panel data, have returned to the question of whether there is a relationship between CBI and inflation.

Garriga and Rodrigues (

2020) examine the effect of de jure CBI on inflation in developing countries in a sample of 118 developing countries during the period of 1980–2013. They conclude that CBI is associated with a lower inflation rate and the effect is stronger the more democratic the country is. The same topic is analyzed by

Kokoszczynski and Mackiewicz-Lyziak (

2020) on the sample of 51 countries using a panel fixed model and the Arellano–Bond difference generalized method of moments estimator. Their results confirm a negative significant impact of CBI on inflation mostly for nonadvanced economies; this relationship also endured the financial crisis.

Strong (

2021) develops a de facto measure of CBI based on the turnover rates and measures of alliance with the governor in power. Using 1980–2009 data from 31 African countries, the study shows that traditional de facto measure of CBI explains some of the variation in inflation rate. It also suggests that to better understand the relationship between CBI and inflation in Africa, it is also necessary to consider the occupational and ethnic background of African central bank governors and to understand the importance of fiscal dominance in the politics of central banking due to the authoritarian regimes in some African countries. Additionally,

Lim (

2021), based on a panel of 147 countries during the 1970–2012 period, confirms that central bank independence leads to superior inflation outcomes from the perspective of democratic governance.

The second frequent topic includes different aspects of financial sector.

Agoba et al. (

2020) tested if CBI promotes financial sector development. Using panel data from 1970 to 2012, the conclusion suggests that it seems to be more effective in developed countries than in African countries, and as one of possible reasons they mention political institutional quality. Similarly,

Kwabi et al. (

2020) analyze the effects of CBI and transparency on foreign equity portfolio inflows. Employing a dataset of 42 countries for the period from 2001–2014, the conclusion supports the hypothesis that an independent and transparent central bank has a positive and significant influence on foreign equity investment inflow.

Andries et al. (

2022) investigate the relationship of CBI and banks’ systemic rick measures. The obtained results support CBI, as it is shown that CBI has a negative and significant impact on the contribution and exposure of banks to systemic risk, importantly also on the individual level. Their results show that there might be trade-off between CBI and a central bank’s financial stability mandate, and support evidence that an increase in CBI can ameliorate the effects of environments characterized by a low level of financial freedom or high market power.

Some studies focus on the factors shaping the institutional design of central banks and attempt to explain why and how monetary policy institutions are reformed.

Bodea and Hicks (

2015) conclude that apart from domestic factors, countries reform their central banks towards more independent institutions to attract international capital and affect an investor’s choice.

Berggren et al. (

2016) focus on cultural factors, mainly social trust, empirically showing an inverse u-shaped tendency of countries with low and high social trust to implement central bank reforms earlier. Most recently,

Romelli (

2022) constructs a new dynamic index of central bank independence, where the timing, pace, and magnitude of reforms are investigated in a sample of 154 countries over the period 1972–2017. He concludes that central bank reforms are often implemented after endogenous factors, such as periods of high inflation rates, or after external pressures, such as democratic reforms. Following this line of investigation,

Kern and Seddon (

2021) developed a power–political framework outlining the conditions and processes under which the diminution of CBI can occur. In this novel approach, based on an in-depth historical survey of the German Reichsbank, they argue that increased government demand for monetary policy control in combination with reductions in the power of sovereign lenders can lead to CBI deterioration. The impact of international organizations, mainly the IMF, on the political independence of key administrative units is under scrutiny in

Reinsberg et al. (

2021). Based on sample of 124 countries between 1980 and 2012, they find the that the IMF places CBI conditionality to countries where among others, the central bank is considered less independent. Up-to-date studies also investigate the impact of CBI on different political topics.

Ezzat and Fayed (

2020) empirically examine the potential effects of central bank independence on democracy. Their results indicate that CBI is conducive to democracy, but the relationship is also dependent on the level of central bank transparency, as high levels of transparency could reverse the positive relation and make CBI an obstacle.

Gavin and Manger (

2022) show that when strongly populist governments are in power, their determination and strategic use of public attacks threatens de facto independence of central bank even though legal independence is maintained. In the study, they documented that political pressure is a recurring practice of populists despite strong norms against such pressure and high de jure central bank independence.

Aklin and Kern (

2021) discuss the benefits and disadvantages of CBI. They argue that on one side it solves the inconsistency problem faced by the policymakers with respect to monetary policy. On the other hand, governments are not able to use monetary policy to generate short-term political benefits at the expense of making economies more vulnerable to financial shocks and potentially damaging economic policies. Expanding on this idea,

Aklin et al. (

2021) explore the link between CBI and inequality. They explain that by indirect constriction of fiscal policy, it is weakening a government’s ability to engage in redistribution. Additionally, incentivizing governments to deregulate financial markets leads to generating a boom in assets values, which are mainly in the hands of the wealthier part of population. Finally, to contain inflationary pressures, the governments actively promote policies which are weakening the bargaining power of workers. While consolidating these factors, they show that an independent central bank leads to inequality.

Braun (

2021) concludes that in the case of ECB it is obvious that the bank shapes financial markets, steers the allocation of money and capital, or actively lobbies national governments to implement its preferred labor market and social policies. He argues that these activities go beyond the ECB’s legal mandate to pursue price stability, raising the concern that the financial system and the labor market facilitate the efficient and effective implementation and transmission of monetary policy. He concludes that this is not a rational way of designing an economy as it supports financialization, asset price inflation, and financial instability, while reducing people’s income and life quality.

3. Methodology

The sample presented in the paper includes data for 38 OECD member countries and covers the period 1991–2021. Two different methodologies are applied to obtain the most realistic view on central bank independence. Therefore, we construct de jure and de facto indicators of central bank independence. It is important to note that the indicators of de jure independence assess mainly the governance structure and do not evaluate a central bank’s ability to conduct anti-inflationary independent policy due to financial dominance/fiscal dominance.

To measure de jure CBI, covering slightly different legislative topics, three different indices are constructed based on their own analysis of central banks’ statutes in the period 1991–2021. Three different indices are constructed, as all legal indicators are heavily dependent on the criteria and also on the way in which the assessment is combined, including, e.g., the weights assigned to each criterion. The indices

2 presented by the paper are (i)

Grilli et al. (

1991); (ii)

Loungani and Sheets (

1995); and (iii)

Sergi (

2000). The source for coding is central banks’ legislation and its reforms and relevant sections of the constitutions are available on their official websites. The decision to construct three indicators is based on the conclusion that even though indicators of de jure independence are supposed to measure the same phenomenon and are all based on interpretations of the central bank laws in place, their correlation is sometimes remarkably low (

Eijffinger and De Haan 1996).

Grilli, Maciandaro, and Tabellini (GMT) examine three areas of central bank independence: (i) the procedures regarding the appointment of the central bank board; (ii) the legal relationship that links the central bank to the government in the formulation of monetary policy; and (iii) the central bank’s formal responsibilities concerning monetary policy. The index is fixed weight (i.e., either zero or one). The value of the index rises with the increase of the autonomy in the selection of objectives and, therefore, it can be used as a way how to measure the growing credibility of the central bank’s ability to autonomously pursue a low inflation objective (

Arnone et al. 2006).

Loungani and Sheets (

1995), for the purpose of assessing CBI in transition economies, combine an approach from previous studies (mainly

Grilli et al. (

1991);

Debelle and Fischer (

1993) and

Cukierman et al. (

1992). and construct their own index consisting of three components—(i) goal independence, (ii) economic independence, and (iii) political independence. Covering these chosen areas, they construct a 14-question “test”.

Sergi (

2000) applies a slightly different approach. Using variable weights, he does not differentiate various possible answers within a question but sets up a weight for individual questions based on their importance. His index diversifies between (i) political and (ii) economic independence, covering commonly assessed areas. Similarly, with GMT, the greater value indicates greater independence.

The second approach to proxy central bank independence used by the paper are indicators assessing de facto CBI. The turnover of governor (TOR) and political vulnerability (VUL) are constructed. Both approaches are assessed for the period 1991–2011 and 1991–2021 to better reflect the possible changes of de facto CBI after the global crisis. The turnover rate is assessed applying the following formula:

This indicator is useful based on the assumption that a higher TOR does point to lower CBI, as in the event of a high TOR the term in office of the governor may be shorter than the average term of a government.

The value of TOR is extended by the vulnerability of the governor’s office to political changes (VUL), as constructed by

Cukierman and Webb (

1995). This measure is based on the propensity of the central bank governor to lose his position within a short period of time following a political transformation. The VUL is defined as an indicator of political vulnerability for central banks by estimating the monthly probability of a change in the head of the central bank, starting from the date of political change. As

Cukierman and Webb (

1995) point out, politically motivated changes are defined as those which occur within six months of a political transition. The indicator is defined as follows:

where

i = 1, …, 6.

The VUL index is evaluated for the case of head of state, prime minister, and finance minister, as it is assumed that these are the political figures with the greatest motivation to influence central banks’ decisions, and in some cases can actively participate in the nomination process of governor/board.

Due to the nature of the data—de jure independence is represented by a time series with a very limited number of changes, de facto independence is for individual countries represented by a single number—all the obtained results will be analyzed statistically. The identified outlying values will be put under scrutiny to find the source of anomaly behavior.

4. Results

To answer the question of whether CBI changed since the turbulent changes of global economic and political environment in the last decade, two different types of indicators were applied: (i) legally based indicators of de jure independence; and (ii) indicators intending to reflect the true relationship between central bank and government. Both types of indicators were statistically evaluated, and the outlying values

3 were identified for further investigation.

4.1. De Jure Independence

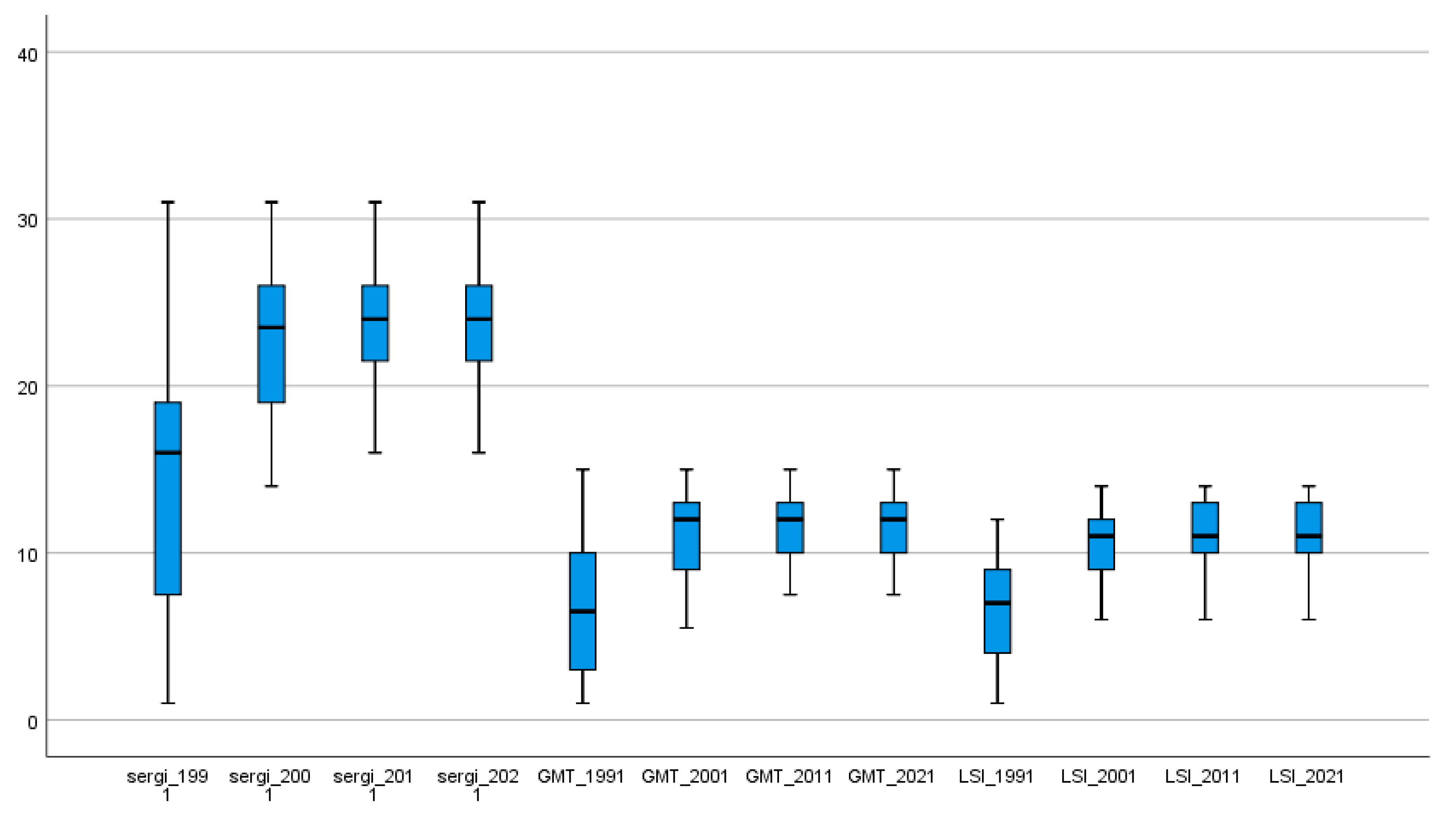

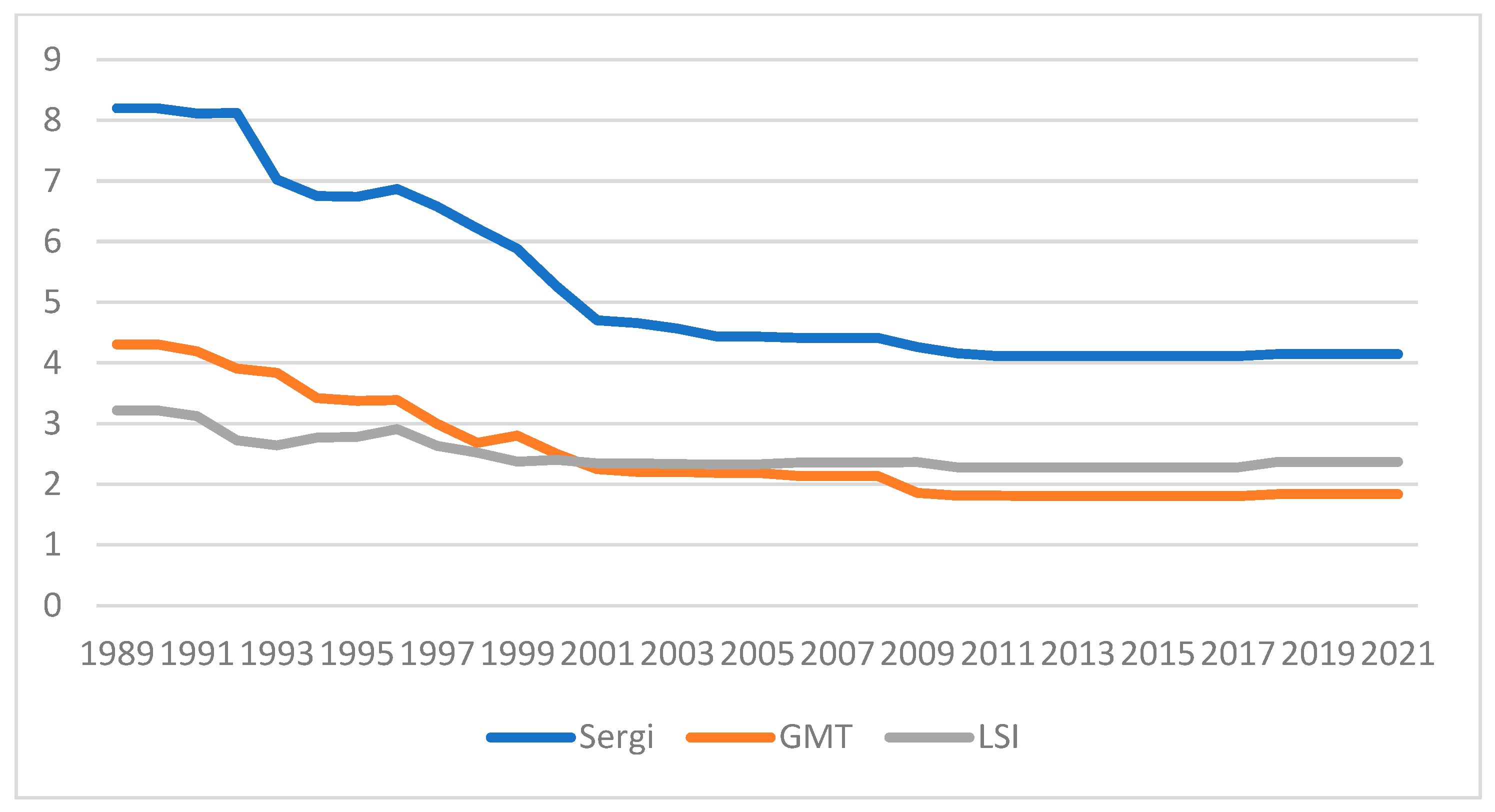

We constructed three different indicators assessing central bank de jure independence. Our result presents an original data set that codes independence annually and covers legislation changes in the last twenty years. The results are based on the central bank law analysis and reflect the central bank independence provided by law. The shortage of this method is our limited understanding of legal systems in the individual countries and their legislative environment.

The main conclusion from all de jure CBI indicators is that the formal independence of central banks was mainly formed in the 1990s, and since 2000 only minor adjustments have been adopted (

Figure 1). It is obvious that the level of independence increased rapidly since 1990, reaching its peak in 2000. This finding confirms the conclusion of studies investigating the role of the International Monetary Fund in promoting central bank independence (e.g.,

Kern et al. 2019), as the IMF targets central bank governance structures in its lending operations.

Since the global financial crisis, the level of de jure independence has remained untouched with the only exception of the CBRT, where its level dropped. CBRT, which only gained its institutional independence in 2001, lost part of it a few years later in 2018. The adopted legal changes in the Republic of Türkiye weakened both the financial and personal independence of the bank. A statutory decree established that the president can directly appoint the central bank governor, deputies, and members of the Monetary Policy Committee. In 2019, the central bank was also forced to reduce its legal reserves and transfer to the Treasury the amount accumulated from the previous period; this act can be also viewed as a weakening of financial independence. The obtained results are also consistent and share the trends with indicators presented by

Romelli (

2022)

4 and

Garriga (

2016)

5, who published the data coding of statutory reforms affecting central bank independence. To our best knowledge, no other data are publicly available for the period 2017 onwards.

Figure 1 and

Figure 2 show that not only has the average level of independence increased remarkably, but the variance has also increased over the time, reflecting similar trends in all the analyzed countries.

4.2. De Facto Independence

To assess de facto independence, we constructed four different indicators. As already mentioned, even the central banks with a high degree of legal independence can face political pressures. Therefore, we evaluated and created an original data set of turnover rates for individual OECD member countries

6 and the outlying values were identified for further investigation.

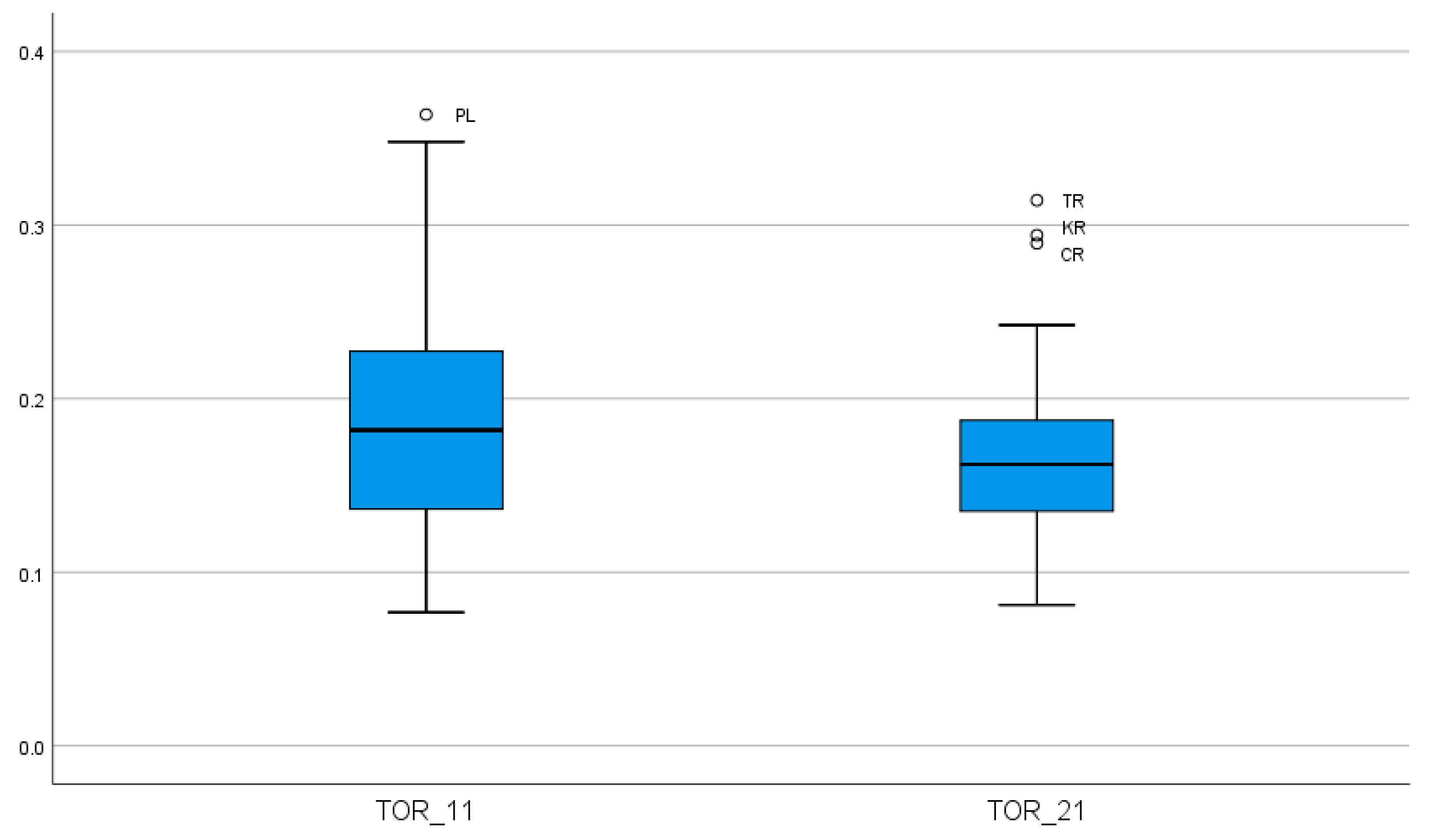

Figure 3 shows both the average turnover rates of the central bank governor until 2011 and the same data extended up to 2021, therefore reflecting the impact of the global financial crisis and the COVID-19 pandemic on de facto CBI in the last decade. The figure does not suggest that de facto CBI has significantly decreased in recent years but, on the contrary, the average length of term in the office of central bank governors has increased.

Noting

Figure 3, in 2011 there was reported one outlier—Poland—as a data point that is located outside the whiskers of the box plot. In 2021, the total number of three outliers was identified, representing the Republic of Türkiye, South Korea, and Costa Rica.

The reason for National Bank of Poland being identified as an outlier is based on three factors (

Table 1 provides an overview). At the beginning of observed period, the central bank’s governor was suspended and later arrested after an accusation of foreign debt fraud

7, and subsequently the acting president was designated until new governor was elected. In 1998, the governor resigned to take the post of the deputy chairman of the European Bank for Reconstruction and Development. The second reason is based on the tragic death of the National Bank of Poland’s president in Smolensk in unclear circumstances in the crash of the Presidential airplane (2010) when he was replaced by his first deputy. Subsequently, the new president of the NBP was approved just a month after

8 In our understanding, the above-mentioned reasons do not qualify the National Bank of Poland to be represented as a case of a central bank where the independence is threatened.

In the case of CBRT, the situation until 2016 was quite stable from the point of de facto independence. It is worth mentioning that two governors resigned prior end of the term in the 1990s for different reasons. Whereas in 1994 the governor resigned over a policy dispute with the Prime Minister, the following governor resigned in order to allow himself to stand in the general elections in 1995.

Interestingly, none of the governors completed their term in office since 2016. After weakening the de jure independence of the bank, the governor (along with several top officials) was removed from his position and no official reason was given. It was reported that there was a disagreement over interest rates which the government wanted lower in a bid to boost economic growth

9. His fate also followed his successor who left his office one year later (

Coskun et al. 2022)

10. The third appointed governor “broke the record” and left his office in four months

11. Details about the central bank’s governors and the reasons for their removal are presented in

Table 2.

As

Tecimer (

2020) notes, that decision to fire the governors was based only on “(1) an emergency decree (which has the force of law) that vaguely states that top bureaucrats at state agencies can be dismissed for reasons set forth in their relevant laws as well as for underperforming and (2) a presidential decree (which, per the Constitution, should be superseded by laws in the event of conflict) that generously provides that the President may simply dismiss top-level bureaucrats at his/her will, which dubiously relies on the Constitution’s Article 104 on the President’s duties that includes hiring and firing top-level bureaucrats (although there is no mention of firing at will)”. He also points out that the presidential decree is not only inferior to laws but also contradicts the law. For these reasons, we consider the case of CBRT independence to be threatened by politicians.

In the case of Costa Rica, the president of the Central Bank is appointed by the Governing Council for a term of four years. This designation will be made twelve months after the start of the constitutional term of the President of the Republic (also elected for a term of four years) and, therefore, the governor’s position is tightly connected to the president’s.

Table 3 illustrates the situation; we consider it obvious that governor’s selection is directly connected with the presidential decision, but this is prevailing for the whole observed period.

In the case of South Korea, none of its governors in the last decade were removed from its position; South Korea being the outlier is reasoned by the quite short term of the governor (four years) as opposed to the usual six years in the office for governors of other central banks.

After close analysis of the outlying values, we concluded that based on the turnover of the governor, de facto independence is threatened by politicians in the case of central bank of Costa Rica and Central bank of Republic of Türkiye.

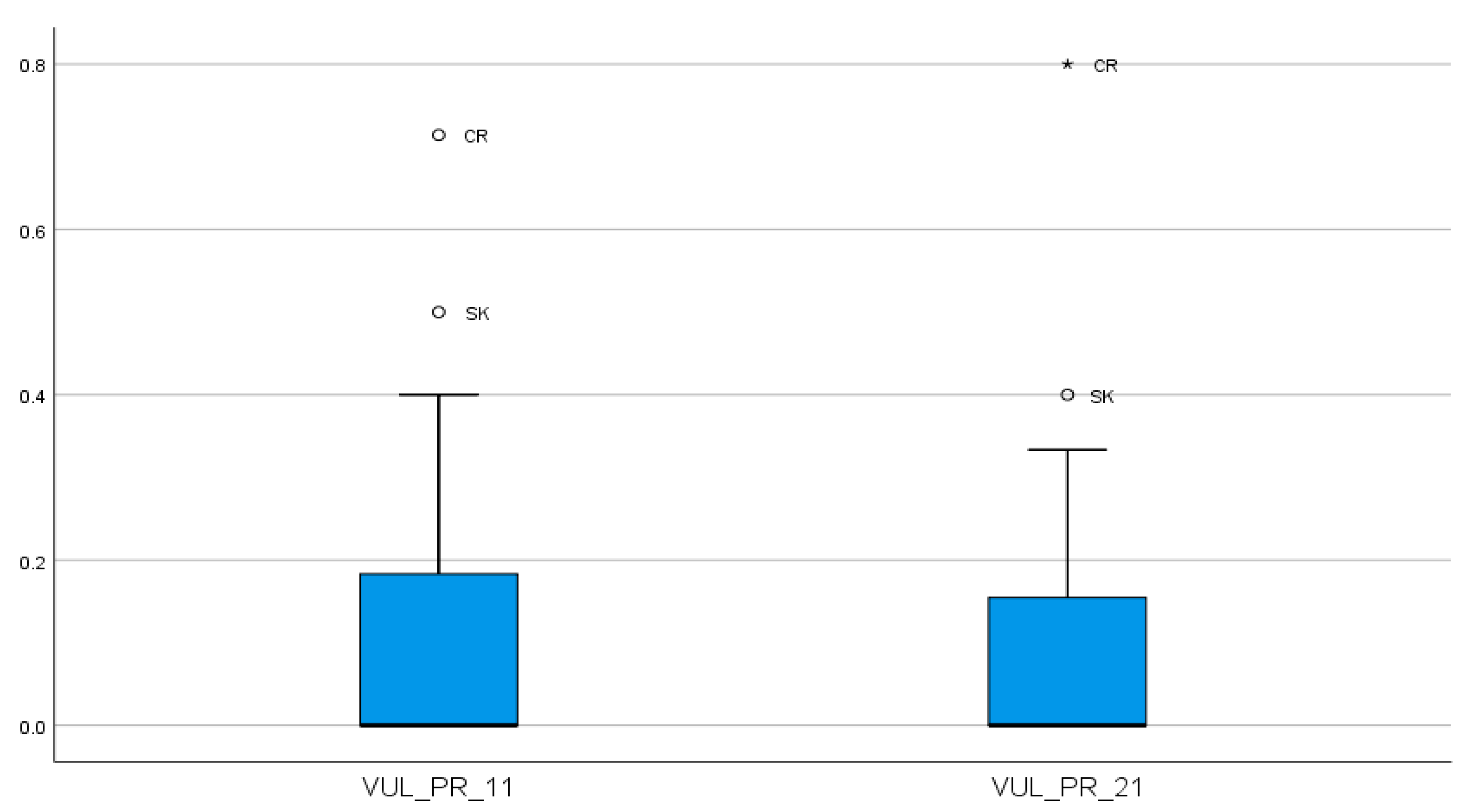

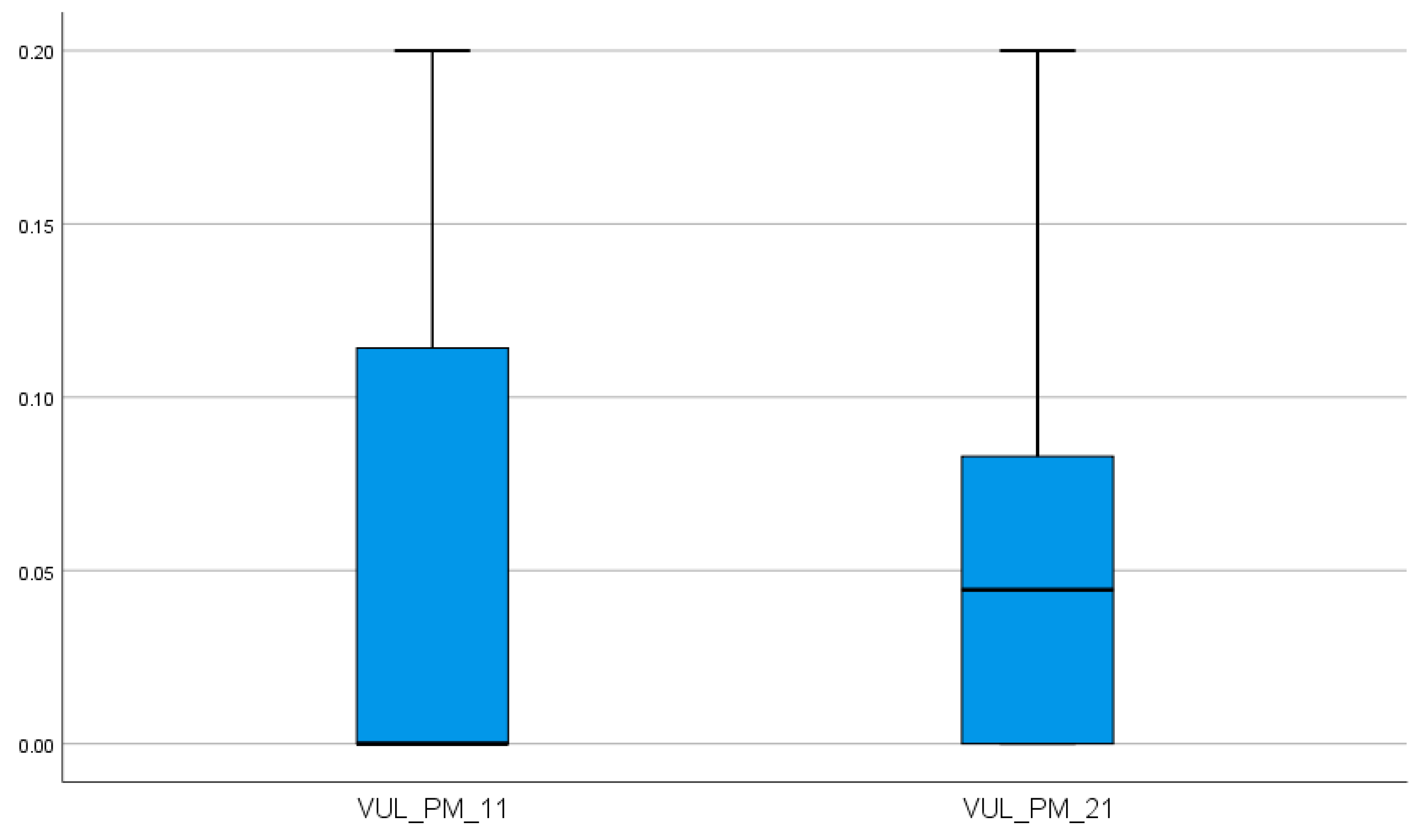

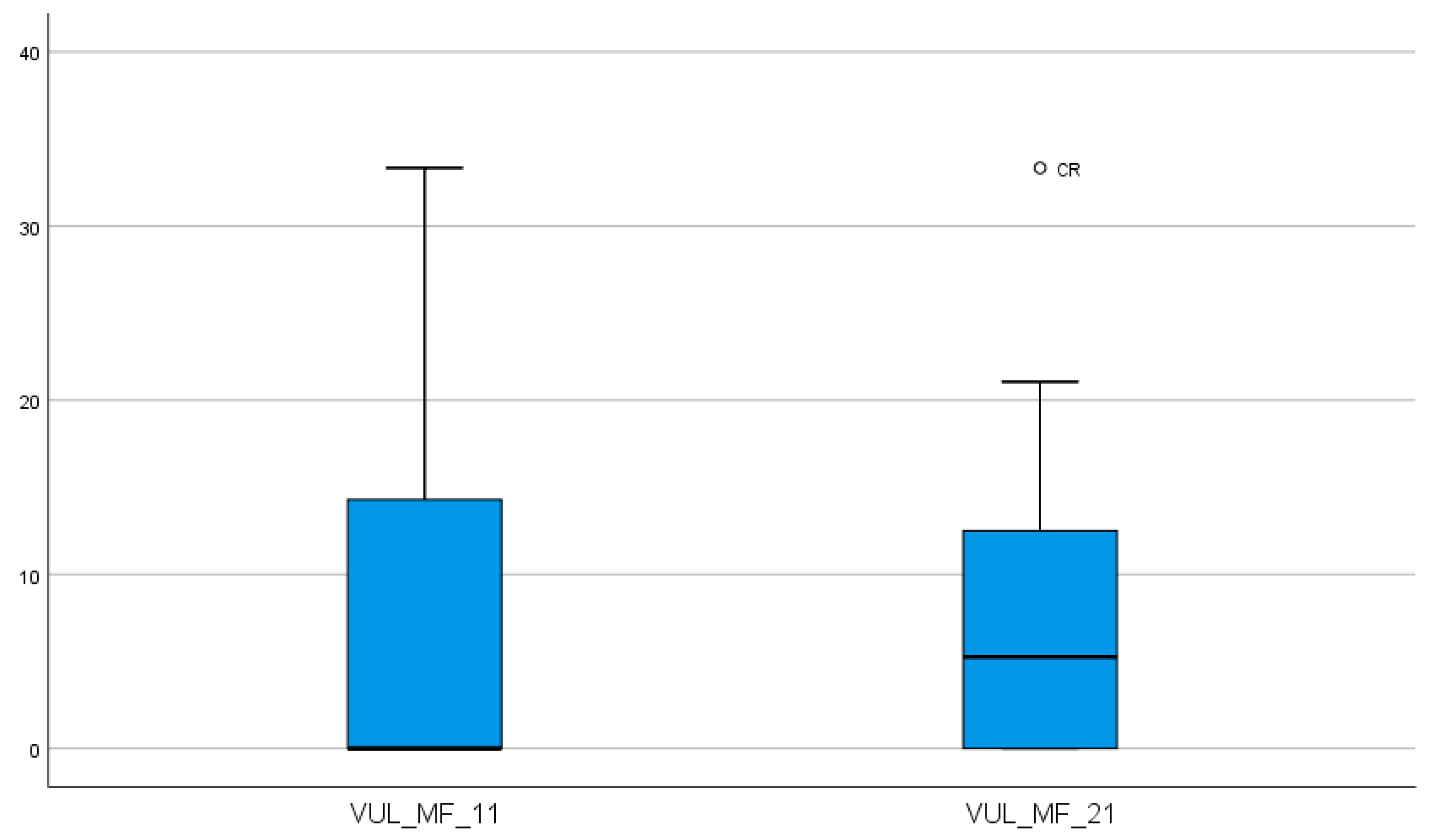

The results for political vulnerability towards the president (VUL_PR), the prime minister (VUL_PM), and the finance/economy minister (VUL_MF) for time periods 1991–2011 and 1991–2021 are presented in

Figure 4,

Figure 5 and

Figure 6.

Figure 4 shows the boxplot of political vulnerability towards the president. The outlying values for the period 1991–2011 represent Slovakia and Costa Rica. Costa Rica’s results correspond with the governor turnover and were explained earlier.

In the case of Slovakia, the outlying value is caused by fact that Slovakia was established in 1993. In the same year, the first president was elected and, following this, the central bank governor was appointed. Six years later, when the governor’s term in office ended, a new governor was appointed. In the same year, a new president was elected (5-year term in the office), the delay of the presidential election was caused by the inability to gain a majority of votes for any presidential candidates. It can be therefore concluded that the high value of TOR was not caused by politicians trying to influence the central bank but by quite a short time period in which the representatives of the newly created institutions (the central bank and the presidential office) were appointed. Due to the length of term in office in the relation to the observed period, the result is considered an outlying value; nevertheless, we decided to omit it. The same outliers were identified for the period 1991–2021. In the case of Slovakia, no new cases were identified, and the outlying value is noted due to impact of changes in the previous period.

Figure 5 displays data of political vulnerability towards the prime minister and

Figure 6 shows political vulnerability towards the finance/economy minister. It is notable that values are lower compared to the political vulnerability towards the president, which can be explained by the much higher rate of change of prime ministers/economy ministers in the office compared to the president. The only outlier—Costa Rica—was identified in the case of political vulnerability towards the economy minister in the period 1991–2021. As mentioned above, the president of the Central Bank is appointed by the Governing Council for a term of four years after the president is elected; the president also elects the economy minister and, therefore, the indicator has higher value.

The results do not suggest that de jure CBI has decreased after the financial crisis and following decade. It is important to note that even the results of de facto CBI do not suggest that the turnover of governors changed significantly, but, on the contrary, the independence of central banks measured by chosen indices is higher.

While measuring the turnover rate of central bankers, it is important to note that some economies experienced political turmoil at the beginning of the measured period, leading to a higher exit rate of central bank governors. On one side, a high exit rate of central bank governors may be just a reflection of the overall instability of the government in the country, instead of an attack on central bank independence. Based on the survey (

Blinder et al. 2017), more than 90% of central bank governors and 80% of academics claim that the central bank independence either did not change or was reduced only “a little”; but only 9% of central bankers expressed their worries about near-future threats to CBI. On the other side,

Masciandaro and Passareli (

2018) consider whether a populist reform

14 is likely to emerge and its effects on CBI. They find a complementary relationship only if most of the citizens are bank stakeholders and are indifferent to the risk of monetary instability. Importantly, populist policy will promote a politically controlled central bank.

Goodhard and Lastra (

2018) argue that populist movements and national identity politics could erode support for CBI.

Gavin and Manger (

2022) proposed a model predicting that populist politicians could bring a nominally independent central bank to its heels without needing to change its legal status.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}