A Model to Explain the Impact of Government Revenue on the Quality of Governance and the SDGs †

Abstract

:1. Introduction

2. Literature Review

3. Research Question, Methods, and Data

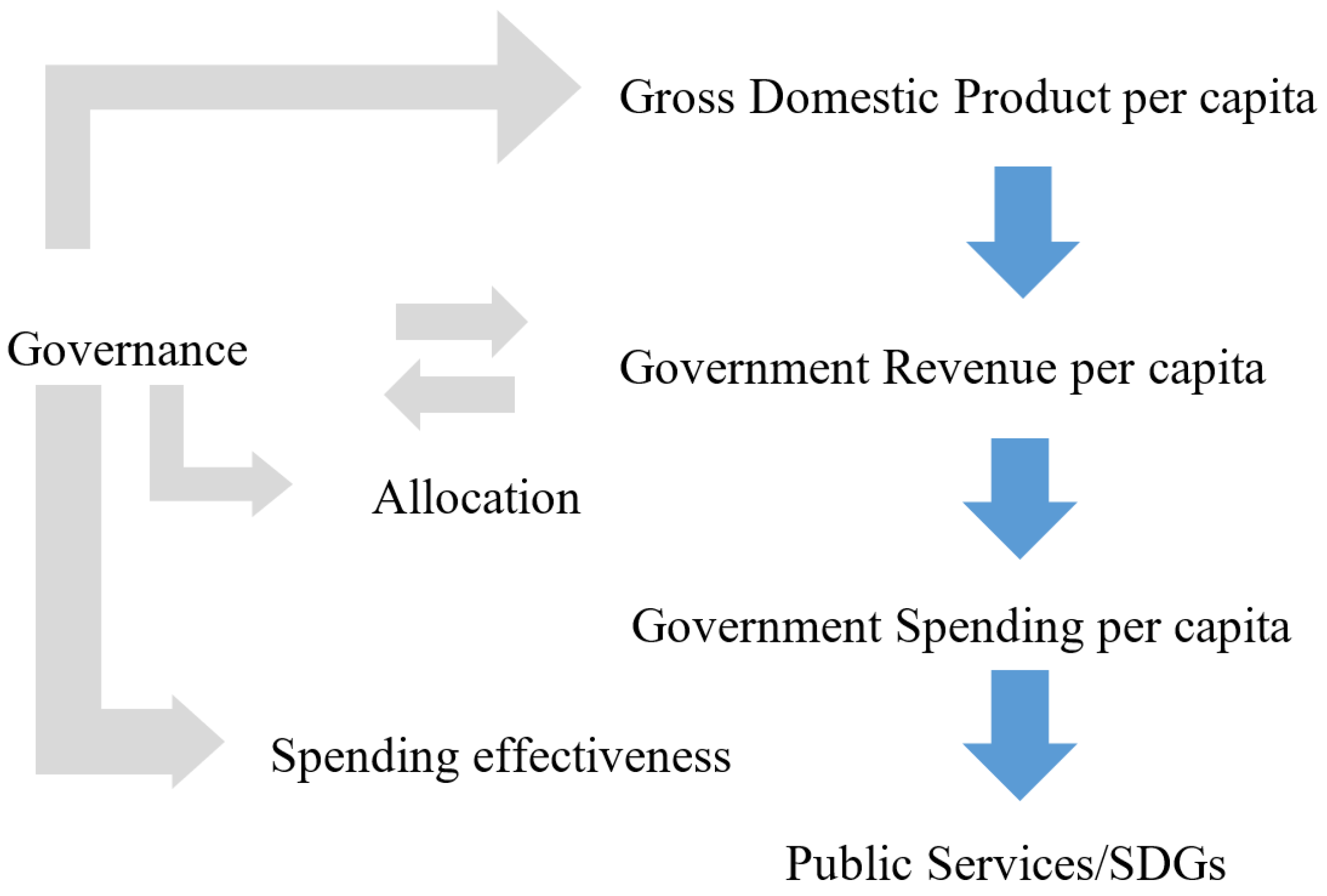

3.1. The Research Question

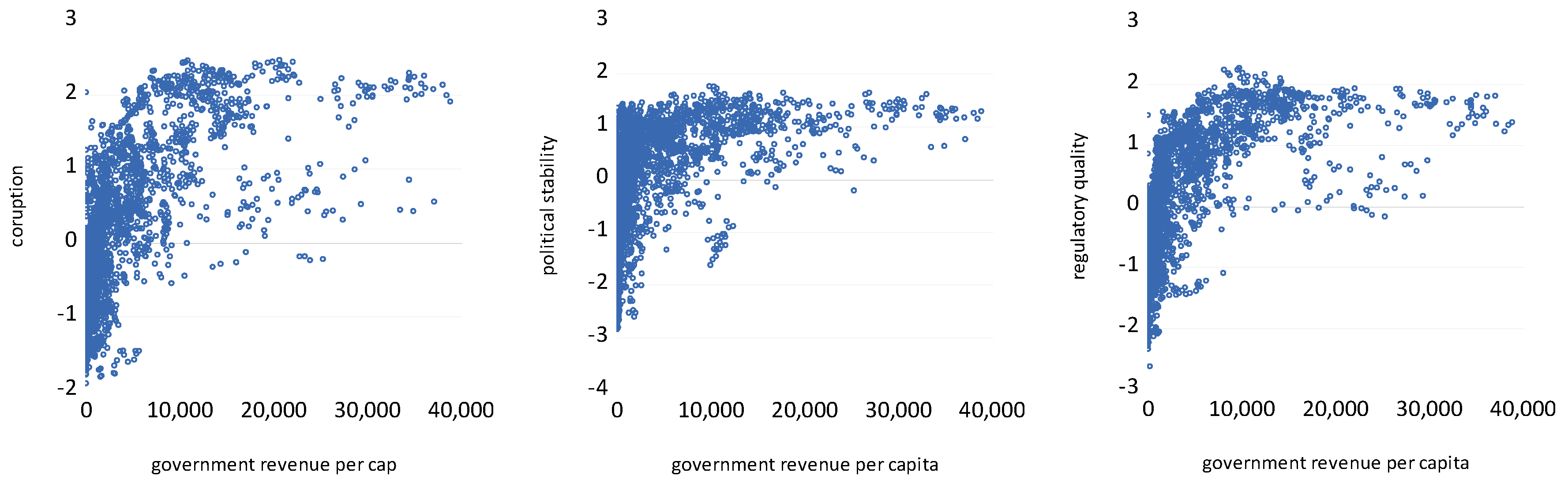

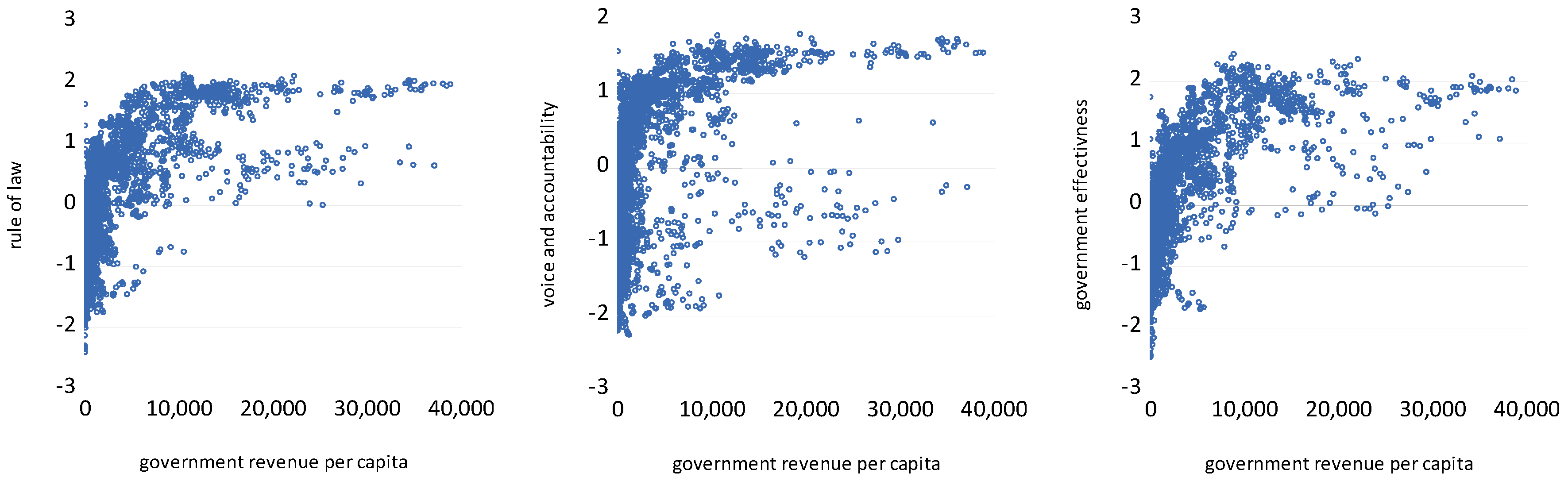

3.2. The Data

3.3. The Methods

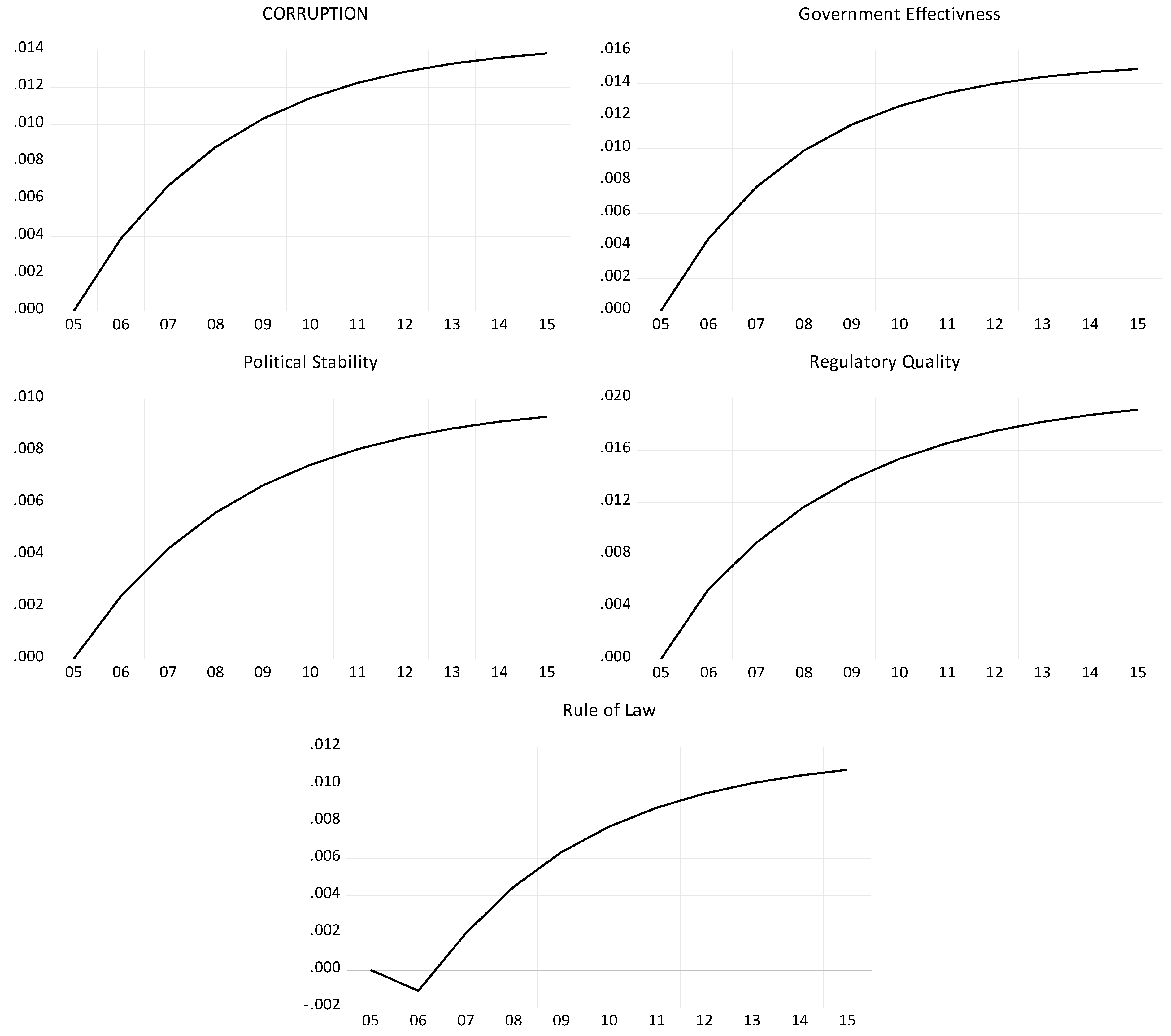

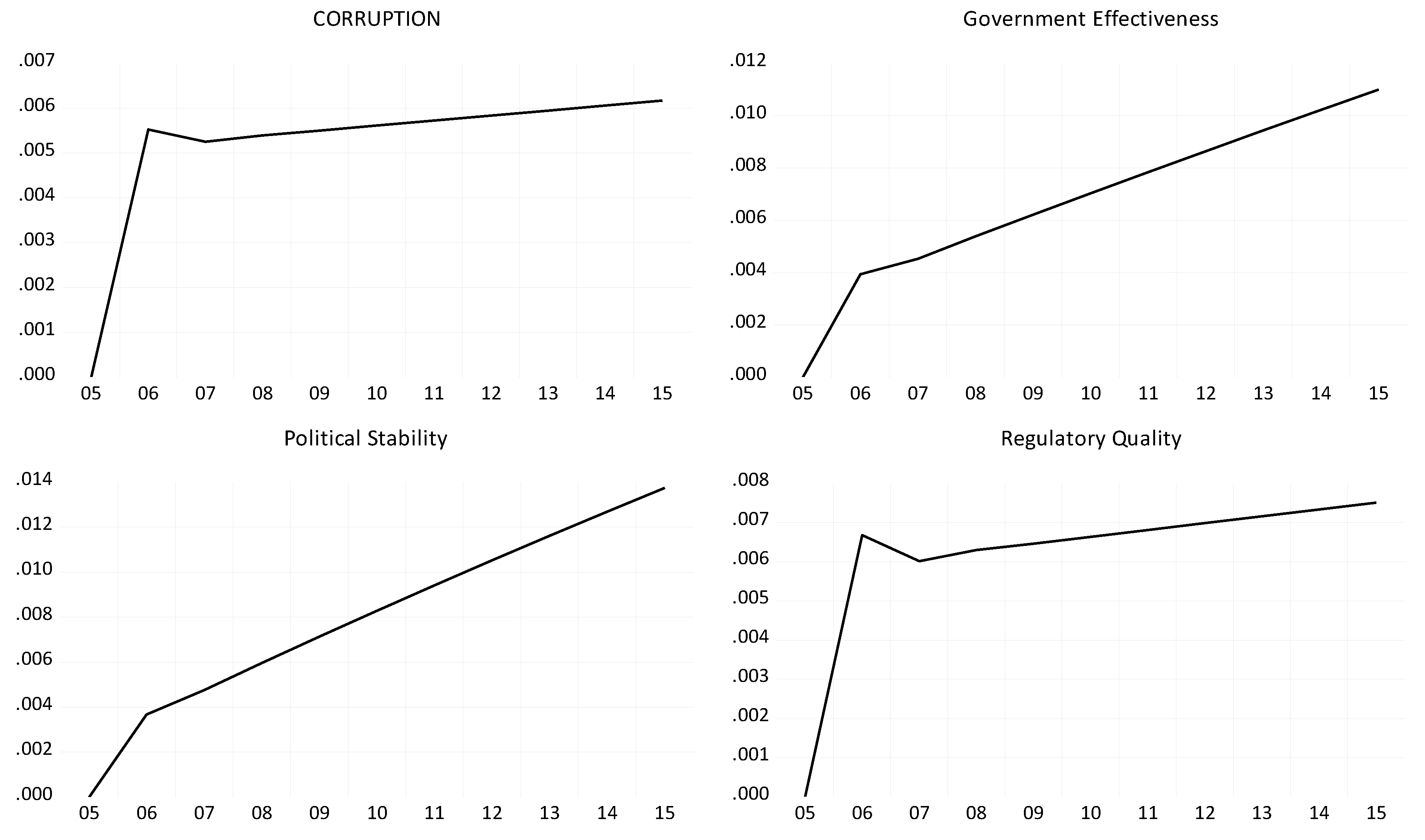

4. The Econometric Analysis and Results

5. Conclusions and Policy Implications

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Dimension of Governance | What It Captures |

|---|---|

| Control of corruption | Perceptions of the extent to which public power is exercised for private gain, including both petty and grand forms of corruption, as well as “capture” of the state by elites and private interests |

| Government effectiveness | Perceptions of the quality of public services, the quality of the civil service and the degree of its independence from political pressures, the quality of policy formulation and implementation, and the credibility of the ’government’s commitment to such policies |

| Political stability | Perceptions of the likelihood that the government will be destabilised or overthrown by unconstitutional or violent means, including politically motivated violence and terrorism |

| Regulatory quality | Perceptions of the ability of the government to formulate and implement sound policies and regulations that permit and promote private sector development |

| The Rule of aw | Perceptions of the extent to which agents have confidence in and abide by the rules of society, and, in particular, the quality of contract enforcement, property rights, the police, and the courts, as well as the likelihood of crime and violence |

| Voice and accountability | Perceptions of the extent to which a country’s citizens are able to participate in selecting their government, as well as freedom of expression, freedom of association, and a free media |

| Summary Statistics | Log of GovRevenue | Corruption | Government Effectiveness | Political Stability | Regulatory Quality | Rule of Law | Voice |

|---|---|---|---|---|---|---|---|

| Mean | 6.615058 | −0.025456 | −0.027234 | −0.023309 | −0.027688 | −0.026333 | −0.020176 |

| Median | 6.737415 | −0.260044 | −0.168511 | 0.075102 | −0.151505 | −0.166980 | 0.017095 |

| Maximum | 10.56818 | 2.469991 | 2.436975 | 1.965062 | 2.260543 | 2.129668 | 1.800992 |

| Minimum | 0.698960 | −1.905176 | −2.475142 | −2.43999 | −2.445041 | −2.496445 | −2.313395 |

| Std. Dev. | 1.856025 | 0.999715 | 0.995194 | 1.000297 | 0.995114 | 0.995753 | 0.999529 |

| Obs. | 5255 | 4393 | 4379 | 4410 | 4379 | 4451 | 4445 |

| 1 | In general, for a VAR with 1 lag, the VECM will not include lagged dynamic terms; where the VAR has 2 lags, there will be 1 lagged dynamic term. |

References

- Abbas, Qamar, Li Junqing, Muhammad Ramzan, and Sumbal Fatima. 2021. Role of governance in debt-growth relationship: Evidence from panel data estimations. Sustainability 13: 5954. [Google Scholar] [CrossRef]

- Acemoglu, Daron, and James A. Robinson. 2012. Why Nations Fail: The Origins of Power, Prosperity and Poverty. London: Profile Books. [Google Scholar]

- Almustafa, Hamza, Quang Khai Nguyen, Jia Liu, and Van Cuong Dang. 2023. The impact of COVID-19 on firm risk and performance in MENA countries: Does national governance quality matter? PLoS ONE 18: e0281148. [Google Scholar] [CrossRef]

- Anyanwu, John C., and Andrew E. O. Erhijakpor. 2009. Health Expenditures and Health Outcomes in Africa. African Development Review 21: 400–33. [Google Scholar] [CrossRef]

- Arif, Imtiaz, and Amna Sohail Rawat. 2018. Corruption, Governance, and Tax Revenue: Evidence from EAGLE Countries. Journal of Transnational Management 23: 119–33. [Google Scholar] [CrossRef]

- Asteriou, Dimitrios, and Stephen G. Hall. 2021. Applied Econometrics. New York: Palgrave Macmillan. [Google Scholar]

- Baldacci, Emanuele, Benedict Clements, Sanjeev Gupta, and Qiang Cui. 2008. Social Spending, Human Capital, and Growth in Developing Countries. World Development 36: 1317–41. [Google Scholar] [CrossRef]

- Baskaran, Thushyanthan, and Arne Bigsten. 2013. Fiscal Capacity and the Quality of Government in Sub-Saharan Africa. World Development 45: 92–107. [Google Scholar] [CrossRef]

- Besley, Timothy, and Torsten Persson. 2014. Why Do Developing Countries Tax So Little? Journal of Economic Perspectives 28: 99–120. [Google Scholar] [CrossRef] [Green Version]

- Çevik, Savaş, and M. Okan Taşar. 2013. Public Spending on Health Care and Health Outcomes: Cross Country Comparison. Journal of Business, Economics & Finance 2: 82–100. [Google Scholar]

- Chan, Sok-Gee, Zulkufly Ramly, and Mohd Zaini Abd Karim. 2017. Government Spending Efficiency on Economic Growth: Roles of Value-Added Tax. Global Economic Review 46: 162–88. [Google Scholar] [CrossRef]

- Chong, Alberto, and César Calderón. 2000. Institutional Quality and Poverty Measures in a Cross-Section of Countries. Economics of Governance 1: 123–35. [Google Scholar] [CrossRef]

- Cooray, Arusha, Ratbek Dzhumashev, and Friedrich Schneider. 2017. How Does Corruption Affect Public Debt? An Empirical Analysis. World Development 90: 115–27. [Google Scholar] [CrossRef] [Green Version]

- Cuthbertson, Keith, Stephen G. Hall, and Mark P. Taylor. 1992. Applied Econometric Techniques. London: Philip Allan. [Google Scholar]

- Dang, Van Cuong, Quang Khai Nguyen, and Xuan Hang Tran. 2022. Corruption, institutional quality and shadow economy in Asian countries. Applied Economics Letters, 1–6. [Google Scholar] [CrossRef]

- Delavallade, Clara. 2006. Corruption and Distribution of Public Spending in Developing Countries. Journal of Economics and Finance 30: 222–39. [Google Scholar] [CrossRef]

- Dhrifi, Abdelhafidh. 2020. Public Health Expenditure and Child Mortality: Does Institutional Quality Matter? Journal of the Knowledge Economy 11: 692–706. [Google Scholar] [CrossRef]

- Factor, Roni, and Minah Kang. 2015. Corruption and Population Health Outcomes: An Analysis of Data from 133 Countries Using Structural Equation Modeling. International Journal of Public Health 60: 633–41. [Google Scholar] [CrossRef] [PubMed]

- Farag, Marwa, A. K. Nandakumar, Stanley Wallack, Dominic Hodgkin, Gary Gaumer, and Can Erbil. 2013. Health Expenditures, Health Outcomes and the Role worldwidernance. International Journal of Health Care Finance and Economics 13: 33–52. [Google Scholar] [CrossRef]

- Fisher, Ronald A. 1922. On the Interpretation of Χ2 from Contingency Tables, and the Calculation of P. Royal Statistical Society 85: 87–94. [Google Scholar] [CrossRef]

- Gupta, Abhijit Sen. 2007. Determinants of Tax Revenue Efforts in Developing Countries. IMF Working Paper 07/184. Singapore: International Monetary Fund. [Google Scholar]

- Gupta, Sanjeev, Marijn Verhoeven, and Erwin R Tiongson. 2002. The Effectiveness of Government Spending on Education and Health Care in Developing and Transition Economies. European Journal of Political Economy 18: 717–37. [Google Scholar] [CrossRef]

- Haile, Fiseha, and Miguel Niño-Zarazúa. 2018. Does Social Spending Improve Welfare in Low-Income and Middle-Income Countries? Journal of International Development 30: 367–98. [Google Scholar] [CrossRef] [Green Version]

- Hall, Stephen, Janine Illian, Innocent Makuta, Kyle McNabb, Stuart Murray, Bernadette A. M. O’Hare, Andre Python, Syed Haider Ali Zaidi, and Naor Bar-Zeev. 2020. Government Revenue and Child and Maternal Mortality. Open Economies Review 32: 213–29. [Google Scholar] [CrossRef]

- Hanf, Matthieu, Mathieu Nacher, Chantal Guihenneuc, Pascale Tubert-Bitter, and Michel Chavance. 2013. Global Determinants of Mortality in under 5s: 10 Year Worldwide Longitudinal Study. BMJ 347: f6427. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Hu, Bingjie, and Ronald U. Mendoza. 2013. Public Health Spending, Governance and Child Health Outcomes: Revisiting the Links. Journal of Human Development and Capabilities 14: 285–311. [Google Scholar] [CrossRef]

- Igbinovia, Ikponmwosa, and Chizoba Marcella Ekwueme. 2020. A Study on the Contributions of Corruption and Governance to the Productivity of Tax Systems in Sub-Saharan Africa. The Journal of Accounting and Management 10: 59–60. [Google Scholar]

- Jahnke, Björn. 2017. How Does Petty Corruption Affect Tax Morale in Sub-Saharan Africa? An Empirical Analysis Standard-Nutzungsbedingungen. UNU Wider Working Paper 2017/8. Helsinki: UNU-WIDER. [Google Scholar] [CrossRef] [Green Version]

- Kao, Chihwa. 1999. Spurious Regression and Residual-Based Tests for Cointegration in Panel Data. Journal of Econometrics 90: 1–44. [Google Scholar] [CrossRef]

- Kaufmann, Daniel, and Aart Kraay. 2013. World Governance Indicators. Available online: https://info.worldbank.org/governance/wgi/ (accessed on 13 February 2023).

- Kaufmann, Daniel, and Aart Kraay. 2020. Worldwide Governance Indicators. Available online: http://info.worldbank.org/governance/wgi/ (accessed on 13 February 2023).

- Kaufmann, Daniel, Aart Kraay, and Massimo Mastruzzi. 2010. The Worldwide Governance Indicators Methodology and Analytical Issues. Washington, DC: Development Research Group, The World Bank. [Google Scholar]

- Kuruvilla, Shyama, Julian Schweitzer, David Bishai, Sadia Chowdhury, Daniele Caramani, Laura Frost, Rafael Cortez, Bernadette Daelmans, Andres de Francisco, Taghreed Adam, and et al. 2014. Success Factors for Reducing Maternal and Child Mortality. Bull World Health Organ 92: 533–44. [Google Scholar] [CrossRef] [PubMed]

- Langnel, Zechariah, and Ponlapat Buracom. 2020. Governance, Health Expenditure and Infant Mortality in Sub-Saharan Africa. African Development Review 32: 673–85. [Google Scholar] [CrossRef]

- Larsson, Rolf, Johan Lyhagen, and Mickael Löthgren. 2001. Likelihood-based Cointegration Tests in Heterogeneous Panels. The Econometrics Journal 4: 109–42. [Google Scholar] [CrossRef]

- Long, Cathal, and Mark Miller. 2017. Taxation and the Sustainable Development Goals: Do Good Things Come to Those Who Tax More? Available online: https://odi.org/en/publications/taxation-and-the-sustainable-development-goals-do-good-things-come-to-those-who-tax-more/ (accessed on 13 February 2023).

- Makuta, Innocent, and Bernadette O’Hare. 2015. Quality of Governance, Public Spending on Health and Health Status in Sub Saharan Africa: A Panel Data Regression Analysis. BMC Public Health 15: 932. [Google Scholar] [CrossRef] [Green Version]

- Mauro, Paolo. 1998. Corruption and the Composition of Government Expenditure. Journal of Public Economics 69: 263–79. [Google Scholar] [CrossRef]

- Moore, Mick. 2007. How Does Taxation Affect the Quality of Governance? IDS WP 280. Available online: https://opendocs.ids.ac.uk/opendocs/handle/20.500.12413/12795 (accessed on 13 February 2023).

- Moyer, Jonathan D., and Steve Hedden. 2020. Are We on the Right Path to Achieve the Sustainable Development Goals? World Development 127: 104749. [Google Scholar] [CrossRef]

- Murshed, Muntasir, and Ashraf Ahmed. 2018. An Assessment of the Marginalizing Impact of Poor Governance on the Efficacy of Public Health Expenditure in LMICS. World Review of Business Research 8: 147–60. [Google Scholar]

- Musa, Kazi, Kazi Sohag, Jamaliah Said, Farha Ghapar, and Norli Ali. 2023. Public Debt, Governance, and Growth in Developing Countries: An Application of Quantile via Moments. Mathematics 11: 650. [Google Scholar] [CrossRef]

- Nketiah-Amponsah, Edward. 2019. The Impact of Health Expenditures on Health Outcomes in Sub-Saharan Africa. Journal of Developing Societies 35: 134–52. [Google Scholar] [CrossRef]

- Nyamongo, M. E., and Nicolaas Johannes Schoeman. 2010. The Quality of Governance and Education Spending in Africa. African Business 14: 1–23. Available online: https://www.ajol.info/index.php/sabr/article/view/76361 (accessed on 13 February 2023).

- O’Hare, Bernadette, and Steve G. Hall. 2022. The Impact of Government Revenue on the Achievement of the Sustainable Development Goals and the Amplification Potential of Good Governance. The Central European Journal of Economic Modelling and Econometrics 14: 109–29. [Google Scholar]

- O’Hare, Bernadette, Stephen Hall, and Stuart Murray. 2020. The Government Revenue and Development Estimations (GRADE). Available online: http://medicine.st-andrews.ac.uk/grade/ (accessed on 13 February 2023).

- Rajkumar, Andrew Sunil, and Vinaya Swaroop. 2008. Public Spending and Outcomes: Does Governance Matter? Journal of Development Economics 86: 96–111. [Google Scholar] [CrossRef] [Green Version]

- Reeves, Aaron, Yannis Gourtsoyannis, Sanjay Basu, David McCoy, Martin McKee, and David Stuckler. 2015. Financing Universal Health Coverage—Effects of Alternative Tax Structures on Public Health Systems: Cross-National Modelling in 89 Low-Income and Middle-Income Countries. The Lancet 386: 274–80. [Google Scholar] [CrossRef] [Green Version]

- Sanoussi, Yacobou, and Mamadou Boukari. 2020. Analysis of the Link between Health Expenditures and Health Outcomes in Africa. Ann. Univ. Lomé, série Sc. Eco. Gest XVII: 51–66. [Google Scholar]

- Tamarappoo, Ramji, Pooja Pokhrel, Muthu Raman, and Jincy Francy. 2016. Analysis of the Linkage Between Domestic Revenue Mobilization and Social Analysis of the Linkage Between Domestic Revenue Mobilization and Social Sector Spending. Available online: https://pdf.usaid.gov/pdf_docs/pbaae640.pdf (accessed on 13 February 2023).

- The World Bank. 2022. Databank: World Development Indicators. Available online: http://databank.worldbank.org/data/source/world-development-indicators (accessed on 13 February 2023).

- Ugur, Mehmet. 2014. Corruptions Direct Effects on per Capita-Income Growth; A Meta-Analysis. Journal of Economic Surveys 28: 472–90. [Google Scholar] [CrossRef] [Green Version]

- United Nations—Office of the High Commissioner of Human Rights. 2021. Sustainable Development Goals and Human Rights. Available online: https://www.ohchr.org/EN/Issues/SDGS/Pages/The2030Agenda.aspx (accessed on 13 February 2023).

- UNU-WIDER. 2022. Data for Tax Revenue Mobilization. Available online: https://www.wider.unu.edu/opportunity/data-tax-revenue-mobilization (accessed on 13 February 2023).

| Worldwide Governance Indicators | Levin, Lin, and Chu | Im, Pessaran, and Shin | ADF-Fisher Chi-Square | Phillips and Peron Chi-Sq |

|---|---|---|---|---|

| Corruption | −7.7 (0.0) | −5.3 (0.0) | 637.6 (0.0) | 620.6 (0.0) |

| Government effectiveness | −10.7 (0.0) | −7.4 (0.0) | 794.3 (0.0) | 694.6 (0.0) |

| Political stability | −11.7 (0.0) | −11.8 (0.0) | 838.7 (0.0) | 861.7 (0.0) |

| Regulatory quality | −13.0 (0.0) | −7.6 (0.0) | 719.5 (0.0) | 689.3 (0.0) |

| The rule of law | −9.8 (0.0) | −6.7 (0.0) | 641.7 (0.0) | 639.5 (0.0) |

| Voice | −9.3 (0.0) | −8.2 (0.0) | 731.5 (0.0) | 665.7 (0.0) |

| Log of Government revenue per capita | −0.83 (0.2) | −1.7 (0.04) | 301.1 (0.0) | 242.1 (0.1) |

| Cointegration Tests | Control of Corruption | Government Effectiveness | Political Stability | Regulatory Quality | Rule of Law | Voice and Accountability |

|---|---|---|---|---|---|---|

| Kao test (null No cointegration) | 7.1 (0.0) | 7.1 (0.0) | 7.0 (0.0) | 7.1 (0.0) | 7.2 (0.0) | 7.0 (0.0) |

| Fisher Trace test | ||||||

| r = 0 | 423.3 (0.0) | 523.3 (0.0) | 528.0 (0.0) | 461.5 (0.0) | 432.2 (0.0) | 570.0 (0.0) |

| r = 1 | 374 (0.0) | 455.7 (0.0) | 405.5 (0.0) | 429.0 (0.0) | 364.0 (0.0) | 435.8 (0.0) |

| Fisher max-eigen test | ||||||

| r = 0 | 347.9 (0.0) | 402.4 (0.0) | 432.0 (0.0) | 357.1 (0.0) | 362.3 (0.0) | 467.5 (0.0) |

| r = 1 | 374.0 (0.0) | 455.7 (0.0) | 405.5(0.0) | 429.0 (0.0) | 364.0 (0.0) | 435.8 (0.0) |

| Coefficients | Control of Corruption | Government Effectiveness | Political Stability | Regulatory Quality | Rule of Law | Voice and Accountability |

|---|---|---|---|---|---|---|

| - | - | - | - | −0.04 *** (3.0) | - | |

| - | - | - | - | - | - | |

| - | - | - | −0.06 *** (3.3) | 0.036 * (1.9) | 0.13 *** (7.0) | |

| −0.26 *** (19.5) | −0.30 *** (19.9) | −0.24 *** (18.2) | −0.24 *** (17.1) | −0.25 *** (18.5) | −0.25 *** (19.7) | |

| 0.04 *** (4.1) | 0.04 *** (4.5) | 0.03 * (1.6) | 0.04 *** (4.1) | 0.03 *** (3.5) | 0.003 (0.3) | |

| 0.002 | 0.013 | 0.001 | 0.002 | 0.001 | 0.001 | |

| Hanson J-statistic p-value | 0.26 | 0.8 | 0.72 | 0.34 | 0.71 | 0.63 |

| Worldwide Governance Indicators | FPE | AIC | SC | HQ | Chosen |

|---|---|---|---|---|---|

| Control of Corruption | 7 | 7 | 1 | 1 | 1 |

| Government Effectiveness | 7 | 7 | 1 | 1 | 1 |

| Political Stability | 8 | 8 | 1 | 1 | 1 |

| Regulatory Quality | 7 | 7 | 1 | 2 | 1 |

| Rule of Law | 7 | 7 | 1 | 1 | 1 |

| Voice and Accountability | 7 | 7 | 2 | 2 | 2 |

| All six | 2 | 2 | 1 | 1 | 2 |

| Worldwide Governance Indicators | |||

|---|---|---|---|

| Control of Corruption | 0.015 (11.4) | −0.0006 (0.5) | 0.12 (8.6) |

| Government Effectiveness | 0.0084 (15.3) | −0.01 (4.9) | 0.03 (8.3) |

| Political Stability | 0.0073 (13.1) | −0.18 (4.9) | 0.02 (8.3) |

| Regulatory Quality | 0.016 (10.6) | −0.0012 (1.1) | 0.01 (8.12) |

| Rule of Law | 0.0135 (11.5) | 0.00017 (0.13) | 0.014 (8.3) |

| Voice and Accountability | 0.0265 (10.6) | 0.002 (4.3) | 0.005 (7.8) |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Hall, S.; O’Hare, B. A Model to Explain the Impact of Government Revenue on the Quality of Governance and the SDGs. Economies 2023, 11, 108. https://doi.org/10.3390/economies11040108

Hall S, O’Hare B. A Model to Explain the Impact of Government Revenue on the Quality of Governance and the SDGs. Economies. 2023; 11(4):108. https://doi.org/10.3390/economies11040108

Chicago/Turabian StyleHall, Stephen, and Bernadette O’Hare. 2023. "A Model to Explain the Impact of Government Revenue on the Quality of Governance and the SDGs" Economies 11, no. 4: 108. https://doi.org/10.3390/economies11040108