Examining the Effects of the Pandemic on Entrepreneurial Activities among Urban Single Mothers: An Exploratory Study

Abstract

:1. Introduction

2. Literature Review

2.1. Theoretical Foundation of the Study

2.2. COVID-19 Pandemic Impact on MSMEs

2.3. Microfinance Programme for Single Mother MSME Entrepreneurs in Malaysia during the COVID-19 Pandemic

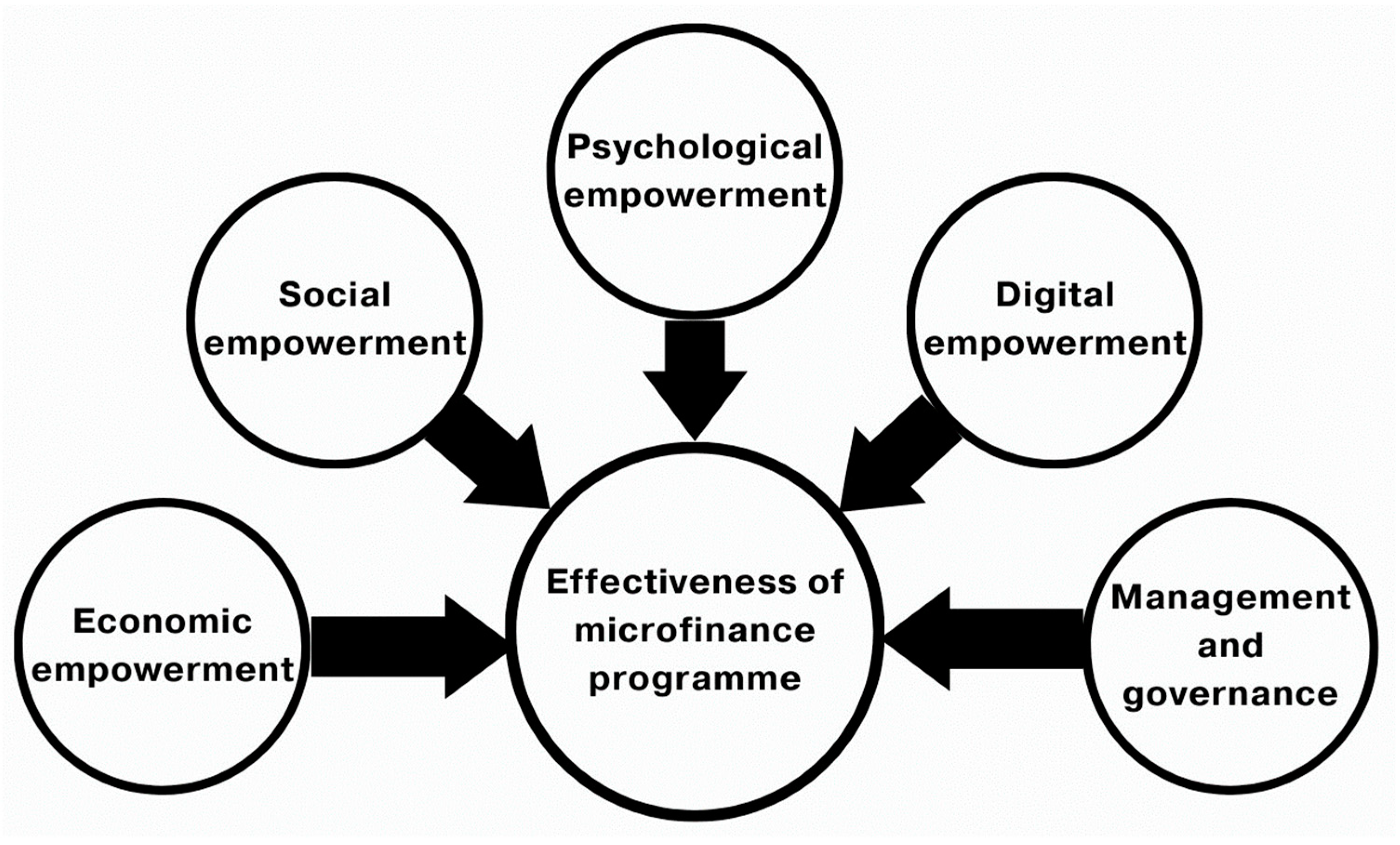

2.4. Effectiveness of Microfinance Programme

2.5. Economic Empowerment

2.6. Social Empowerment

2.7. Psychological Empowerment

2.8. Digital Empowerment

2.9. Management and Governance of Microfinance Programmes

3. Research Methods

3.1. Research Design and Research Framework

3.2. Variable Measurement

3.3. Population and Sample Selection

3.4. Research Instrument

3.5. Data Collection Procedure

3.6. Data Analysis Techniques

4. Results and Discussion

4.1. Respondents Profile

4.2. Descriptive Analysis

4.3. Empirical Assessment

5. Conclusions

5.1. Achievement of Research Question

Research Question

5.2. Theoretical Implications

5.3. Managerial and Practical Implications

5.3.1. Management and Governance of the Microfinance Programme

5.3.2. Economic Empowerment

5.3.3. Digital Empowerment

5.3.4. Social Empowerment

5.3.5. Psychological Empowerment

5.4. Limitations of Study

5.5. Suggestions for Future Research

5.6. Summary

Author Contributions

Funding

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Ab-Rahim, Rossazana, Saif-Ul-Mujahid Shah, and Samira Raki. 2018. Impacts of NGOs microfinance on women empowerment in Northern Pakistan. International Journal of Academi Research in Business and Social Sciences 8: 1–13. [Google Scholar] [CrossRef]

- Addai, Bismark. 2017. Women empowerment through microfinance: Empirical evidence from Ghana. Journal of Finance and Accounting 5: 1–11. [Google Scholar] [CrossRef]

- Ahmad, Naila Masood, and Moazzam Ahmad. 2016. Role of microfinance towards socio-economic empowerment of Pakistani Urban women. Anthropologist 26: 189–97. [Google Scholar] [CrossRef]

- Ahmad, Nurul Wajhi Binti, Nor Hakimah Binti Hj. Mohd Nor, Nor Fadilah Binti Bahari, Nuzul Akhtar Binti Baharudin, and Norazlina Binti Ripain. 2019. Tahap dan indeks keberkesanan programme mikrokredit terhadap pemberdayaan ibu tunggal di Selangor. Petaling Jaya: Institut Wanita Berdaya. [Google Scholar]

- Al Mamun, Abdullah, Mohd Asrul Hery Bin Ibrahim, Rajennd Muniady, Mohammad Bin Ismail, Noorshella Binti Che Nawi, and Noorul Azwin Binti Md Nasir. 2018. Development programme, household income and economic vulnerability: A study among low-income households in Peninsular Malaysia. World Journal of Entrepreneurship, Management and Sustainable Development 14: 353–66. [Google Scholar] [CrossRef]

- Al-shami, Sayed Samer Ali, Izaidin Bin Adbul Majid, Nurulizwa Abdul Rashid, and Mohd Syaiful Rizal Bin Abdul Hamid. 2014. Conceptual framework: The role of microfinance on the well-being of poor people cases studies from Malaysia and Yemen. Asian Social Science 10: 230–42. [Google Scholar] [CrossRef]

- Al-shami, Sayed Samer Ali, Izaidin Majid, Mohd Razali Mohamad, and Nurulizwa Rashid. 2017a. Household welfare and women empowerment through microfinance financing: Evidence from Malaysia microfinance. Journal of Human Behavior in the Social Environment 27: 894–910. [Google Scholar] [CrossRef]

- Al-shami, Sayed Samer Ali, R. M. Razali, and Nurulizwa Rashid. 2017b. The effect of microfinance on women empowerment in welfare and decision-making in Malaysia. Social Indicators Research 137: 1073–90. [Google Scholar] [CrossRef]

- Amanah Ikhtiar Malaysia. 2020a. Bengkel Keusahawanan Sahabat AIM 2020. Available online: https://www.facebook.com/AmanahIkhtiarMalaysia/videos/345318113531945/?__tn__=%2Cd%2CPR&eid=ARBJvJYCvKPodUCsvpu2Jq_mKqHS0OHoce3XaNCieNK48oIoKmeAOCTDLWDraIFdf_2IUUPw9En3-YL (accessed on 24 July 2020).

- Amanah Ikhtiar Malaysia. 2020b. Pakej Rangsangan Ekonomi Amanah Ikhitar Malaysia (AIM) Bagi Membantu Peminjam-Peminjam Amanah Ikhtiar Malaysia (Sahabat AIM). Available online: https://www.facebook.com/AmanahIkhtiarMalaysia/photos/pcb.3200868319947214/3200867069947339/?type=3&theater (accessed on 25 March 2020).

- Anthony, Ntr, Rosliza Abdul Manaf, and P. C. Lai. 2019. The literature review of the governance frameworks in the health system. Journal of Public Administration and Governance 9: 252–60. [Google Scholar]

- Bartik, Alexander W., Marianne Bertrand, Zoe Cullen, and Christopher Stanton. 2020. The impact of Covid-19 on small business outcomes and expectations. Proceedings of the National Academy of Sciences of the United States of America (P.N.A.S.) 117: 17656–66. [Google Scholar] [CrossRef] [PubMed]

- Bartz, Wiebke, and Adalbert Winkler. 2016. Flexible or fragile? the growth performance of small and young businesses during the global financial crisis—Evidence from Germany. Journal of Business Venturing 31: 196–215. [Google Scholar] [CrossRef]

- Booth, Simon A. 1993. Crisis Management Strategy: Competition and change in modern enterprises. London and New York: Routledge. [Google Scholar]

- Büchi, Moritz. 2020. A Proto-Theory of Digital Well-Being. Working Paper, Department of Communication & Media Research and Digital Society Initiative, University of Zurich, Zurich, Switzerland. [Google Scholar]

- Che Omar, Ahmad Raflis, Suraiya Ishak, and Mohd Abdullah Jusoh. 2020. The impact of COVID-19 Movement Control Order on S.M.E.s’ businesses and survival strategies. Malaysian Journal of Society and Space 16: 139–50. [Google Scholar] [CrossRef]

- Cook, Jack. 2015. A six-stage business continuity and disaster recovery planning cycle. S.A.M. Advanced Management Journal 80: 22–33. [Google Scholar]

- Diefenbach, Sarah. 2018. The potential and challenges of digital well-being interventions: Positive technology research and design in light of the bitter-sweet ambivalence of change. Frontiers in. Psychology 9: 1–16. [Google Scholar] [CrossRef] [PubMed]

- Fairlie, Robert. 2020. The impact of COVID-19 on small business owners: Evidence from the first three months after widespread social-distancing restrictions. Journal of Economics and Management Strategy 29: 727–40. [Google Scholar] [CrossRef]

- Fabeil, Noor Fzlinda, Khairul Hanim Pazim, and Juliana Langgat. 2020. The impact of the COVID-19 pandemic crisis on Micro-Enterprises: Entrepreneurs’ perspective on business continuity and recovery strategy. Journal of Economics and Business 3: 837–44. [Google Scholar]

- Garland, Ron. 1991. The Mid-Point on a Rating Scale: Is it Desirable? Marketing Bulletin 2: 66–70. [Google Scholar]

- Guberina, Tajana, Ai Min Wang, and Bojan Obrenovic. 2023. An empirical study of entrepreneurial leadership and fear of COVID-19 impact on psychological well-being: A mediating effect of job insecurity. PLoS ONE 18: e0284766. [Google Scholar] [CrossRef]

- Guilford, Joy Paul. 1973. Fundamental Statistics in Psychology and Education. New York: McGraw Hill. [Google Scholar]

- Hamdan, Nur Hazirah, P C Lai, and Salina Kassim. 2021. The COVID-19 pandemic crisis on microentrepreneurs in Malaysia: Impact and mitigation approaches. Journal of Global Business and Social Entrepreneurship 7: 52–64. [Google Scholar]

- Hashim, Maryam Jameelah, Mohammad Izzat Naqib Yusof, and Nur Dina Athia Ramley. 2023. The effectiveness of microfinance programme on women’s empowerment: Location as moderator. Information Management and Business Review 15: 1–13. [Google Scholar] [CrossRef]

- Ilieva-Koleva, Daniela, and Julia Dobreva. 2021. Social entrepreneurship as a form of social responsibilities in Bulgaria. International Journal of Operations Management 1: 25–31. [Google Scholar] [CrossRef]

- Koh, Her Loke, Sakiru Adebola Solarin, Yee Yen Yuen, and Suganthi Ramasamy. 2021. The impact of microfinance services on the socioeconomic welfare of urban vulnerable households in Malaysia. International Journal of Business and Society 22: 696–712. [Google Scholar]

- Krejcie, Robert V., and Daryle W. Morgan. 1970. Determining sample size for research activities. Educational and Psychological Measurement 30: 607–10. [Google Scholar] [CrossRef]

- Lai, P. C. 2020. Intention to Use a Drug Reminder App: A Case Study of Diabetics and High Blood Pressure Patients. In SAGE Research Methods Cases: Medicine and Health. London: SAGE Publications Ltd., pp. 1–19. [Google Scholar]

- Lythreatis, Sophie, Sanjay Singh, and Abdul-Nasser El-Kassar. 2021. The digital divide: A review and future research agenda. Technological Forecasting & Social Change 175: 1–11. [Google Scholar]

- Mariyono, Joko. 2019. Micro-credit as a catalyst for improving rural livelihoods through the agribusiness sector in Indonesia. Journal of Entrepreneurship in Emerging Economies 11: 98–121. [Google Scholar] [CrossRef]

- Meng, Qian, and Fangfang Sun. 2019. The impact of psychological empowerment on work engagement among university faculty members in China. Psychological Research Behaviour Management 12: 983–90. [Google Scholar] [CrossRef] [PubMed]

- Mohammad, Zam Zuriyati, Juliana Abu Bakar, Sharmeela Banu Thahir, and Hatijah Mohd Salleh. 2022. Pandemic to endemic: A review of key enablers of small medium enterprise resilience. The Journal of Management and Theory Practice 3: 7–17. [Google Scholar]

- Nazier, Hanan, and Racha Ramadan. 2018. What empowers Egyptian women: Resources versus social constraints? Review of Economics and Political Science 3: 153–75. [Google Scholar] [CrossRef]

- Nunnally, Jum, and Ira Bernstein. 1994. Psychometric Theory. New York: McGraw Hill. [Google Scholar]

- Rahman, Mohammad Mafizur, Rasheda Khanam, and Son Hong Nghiem. 2018. The effects of microfinance on women’s empowerment: New evidence from Bangladesh. International Journal of Social Economics 44: 1745–57. [Google Scholar] [CrossRef]

- Ran, Li, Xuyu Chen, Ying Wang, Wenwen Wu, Ling Zhang, and Xiaodong Tan. 2020. Risk factors of healthcare workers with coronavirus disease 2019: A retrospective cohort study in a designated hospital of Wuhan in China. Clinical Infectious Diseases 71: 2218–21. [Google Scholar] [CrossRef]

- Riduwan, M.B.A. 2012. Skala Pengukuran Variable-Variable: Penelitian. Bandung: Alfabeta. [Google Scholar]

- Roffarello, Alberto Monge, and Luigi De Russis. 2019. The race towards digital wellbeing: Issues and opportunities. Paper presented at C.H.I. Conference on Human Factors in Computing Systems. Proceedings of Association for Computing Machinery, Glasgow, Scotland, May 4–9. [Google Scholar]

- Salia, Samuel, Javed Hussain, Ishmael Tingbani, and Oluwaseun Kolade. 2018. Is women empowerment a zero-sum game? Unintended consequences of microfinance for women’s empowerment in Ghana. International Journal of Entrepreneurial Behavior & Research 24: 273–89. [Google Scholar]

- Sipahutar, Mangasa Augustinus, Rina Oktaviani, Hermanto Siregar, and Bambang Juanda. 2016. Effects of credit on economic growth, unemployment and poverty. Jurnal Ekonomi Pembangunan: Kajian Masalah Ekonomi dan Pembangunan 17: 37–49. [Google Scholar] [CrossRef]

- Sri Rahayu, Ninik, Masduki, and E. R. Nur Ellyanawati. 2023. Women entrepreneurs’ struggles during the COVID-19 pandemic and their use of social media. Journal of Innovation and Entrepreneurship 12: 51. [Google Scholar] [CrossRef]

- Swift, Carolyn, and Gloria Levin. 1987. Empowerment an emerging mental health technology. Journal of Primary Prevention 8: 71–94. [Google Scholar] [CrossRef] [PubMed]

- Walid, L’hocine, and Huatao Peng. 2022. Entrepreneurial risk perception and sustainable entrepreneurship intention among S.M.E. in Algeria: A multidimensional approach. Journal of Entrepreneurship and Business Development 1: 7–15. [Google Scholar] [CrossRef]

- Wellalage, Nirosha Hewa, and Stuart M. Locke. 2017. Access to credit by S.M.E.s in South Asia: Do women entrepreneurs face discrimination? Research in International Business and Finance 41: 336–46. [Google Scholar] [CrossRef]

- Yukongdi, Vimolwan, and Nusrat Zahan Lopa. 2017. Entrepreneurial intention: A study of individual, situational and gender differences. Journal of Small Business Enterprise Development 24: 333–52. [Google Scholar] [CrossRef]

- Zaleskiewicz, Tomasz, Adriana Bernady, and Jakub Traczyk. 2020. Entrepreneurial risk-taking is related to mental imagery: A fresh look at the old issue of entrepreneurship and risk. Journal of Applied Psychology 69: 1438–69. [Google Scholar] [CrossRef]

- Zimmerman, Marc A. 1995. Psychological empowerment: Issues and illustration. American Journal of Community Psychology 23: 581–600. [Google Scholar] [CrossRef] [PubMed]

{kind=link}

| Variables Definition | Acronym | Sources |

|---|---|---|

| Dependent Variable: The effectiveness of the A.I.M. Microfinance Programme during the COVID-19 pandemic and the Movement Control Order (MCO) | E.M.F.P. | Ahmad et al. (2019) |

| Independent Variable: Economic Empowerment in an individual appraisal of household income, savings, cost of living, expenses, insurance coverage, business income, and business performance | EE | Ahmad et al. (2019). Al-shami et al. (2017a), Al-shami et al. (2017b) |

| Social Empowerment is an individual appraisal of social recognition, well-being, and interaction | SE | Ahmad et al. (2019), Ab-Rahim et al. (2018), Ahmad and Ahmad (2016) |

| Digital Empowerment is an individual appraisal of digital literacy, proficiency, and competencies | DE | Büchi (2020), Roffarello and Russis (2019), Diefenbach (2018) |

| Psychological Empowerment is an individual appraisal of self-confidence, self-skills, self-image, self-control, and mental well-being | P.E. | Ahmad et al. (2019), Salia et al. (2018), Ab-Rahim et al. (2018) |

| The management and governance factors of the A.I.M. microfinance programme cover aspects of administration, operation, and management | M.G.M.F.P. | Ahmad et al. (2019) |

| Mean Score | Interpretation |

|---|---|

| 2.50–3.75 | Less relevant |

| 3.76–6.25 | Low |

| 6.26–8.75 | Moderate |

| 8.76–10.00 | High |

| Demographic Attributes | Frequency | Percentage (%) |

|---|---|---|

| Business Location | ||

| Selangor | 301 | 71.3 |

| Wilayah Persekutuan—Kuala Lumpur | 99 | 23.5 |

| Wilayah Persekutuan—Labuan | 13 | 3.1 |

| Wilayah Persekutuan—Putrajaya | 9 | 2.1 |

| Monthly household income | ||

| B40 | ||

| Less than MYR 2500 | 210 | 49.8 |

| 3170–3169 | 105 | 24.9 |

| 3170–3969 | 40 | 9.5 |

| 3970–4849 | 24 | 5.7 |

| M40 | ||

| 4850–5879 | 20 | 4.7 |

| 5880–7099 | 6 | 1.4 |

| 7100–8699 | 4 | 0.9 |

| 8700–10,959 | 7 | 1.7 |

| T20 | ||

| 10,960–15,039 | 4 | 0.9 |

| More than 15,040 | 2 | 0.5 |

| Number of dependents | ||

| 1 to 4 | 303 | 71.8 |

| 5 to 9 | 4 | 0.9 |

| More than 10 | 77 | 18.2 |

| No dependents | 38 | 9 |

| Respondent status | ||

| Divorcee | 230 | 54.5 |

| Death of husband | 133 | 31.5 |

| Taking over husband’s roles | 59 | 14 |

| Accommodation status | ||

| Poor People Housing Project | 9 | 2.1 |

| People Housing Project | 40 | 9.5 |

| Bungalow | 3 | 0.7 |

| Twin | 4 | 0.9 |

| High-rise | 121 | 28.7 |

| Village | 114 | 27 |

| Single-storey house | 58 | 13.7 |

| Double-storey house | 73 | 17.3 |

| Family status | ||

| Mixed | 6 | 1.4 |

| Dyad | 2 | 0.5 |

| Single parent | 215 | 50.9 |

| Cohabitation | 23 | 5.5 |

| Extended | 14 | 3.3 |

| Nucleus | 162 | 38.4 |

| No | Variables | Min | Max | SD | Mean |

|---|---|---|---|---|---|

| 1 | Effectiveness of Microfinance Programme (E.M.F.P.) | 2.50 | 10.00 | 1.6347 | 8.054 |

| 2 | Economic Empowerment (E.E.) | 3.75 | 10.00 | 1.448 | 7.649 |

| 3 | Social Empowerment (S.E.) | 2.75 | 10.00 | 1521 | 8.903 |

| 4 | Digital Empowerment (D.E.) | 3.64 | 10.00 | 1.351 | 8.208 |

| 5 | Psychological Empowerment (P.E.) | 4.23 | 10.00 | 1.423 | 8.069 |

| 6 | Management and Governance of Microfinance Programme (M.G.M.F.P.) | 3.27 | 10.00 | 1.358 | 8.073 |

| EMFP | M.G.M.F.P. | P.E. | E.E. | S.E. | D.E. | |

|---|---|---|---|---|---|---|

| EMFP | 1 | |||||

| M.G.M.F.P. | 0.714 ** <0.001 | 1 | ||||

| P.E. | 0.490 ** <0.001 | 0.550 ** <0.001 | 1 | |||

| E.E. | 0.571 ** <0.001 | 0.623 ** <0.001 | 0.728 ** <0.001 | 1 | ||

| S.E. | 0.418 ** <0.001 | 0.563 ** <0.001 | 0.595 ** <0.001 | 0.843 ** <0.001 | 1 | |

| D.E. | 0.436 ** <0.001 | 0.470 ** <0.001 | 0.538 ** <0.001 | 0.612 ** <0.001 | 0.608 ** <0.001 | 1 |

| Item | Results |

|---|---|

| α | 0.825 |

| MGMFP | 0.721 *** |

| PE | 0.0000 |

| EE | 0.460 *** |

| S.E. | −0.035 *** |

| DE | 0.127 ** |

| Adjusted R2 | 0.566 |

| Model | Sum of Squares | df | Mean Square | F | Sig. |

|---|---|---|---|---|---|

| Regression | 630.870 | 5 | 126.174 | 107.268 | <0.001 b |

| Residual | 483.441 | 411 | 1.176 | ||

| Total | 1114.311 | 416 |

| Item | VIF |

|---|---|

| MGMFP | 1.725 |

| PE | 2.249 |

| EE | 4.934 |

| SE | 3.632 |

| DE | 1.759 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Abdullah Salim, A.S.; Md Yatim, N.; Md Zahid, S. Examining the Effects of the Pandemic on Entrepreneurial Activities among Urban Single Mothers: An Exploratory Study. Int. J. Financial Stud. 2024, 12, 30. https://doi.org/10.3390/ijfs12020030

Abdullah Salim AS, Md Yatim N, Md Zahid S. Examining the Effects of the Pandemic on Entrepreneurial Activities among Urban Single Mothers: An Exploratory Study. International Journal of Financial Studies. 2024; 12(2):30. https://doi.org/10.3390/ijfs12020030

Chicago/Turabian StyleAbdullah Salim, Abdullah Sallehhuddin, Norzarina Md Yatim, and Salmi Md Zahid. 2024. "Examining the Effects of the Pandemic on Entrepreneurial Activities among Urban Single Mothers: An Exploratory Study" International Journal of Financial Studies 12, no. 2: 30. https://doi.org/10.3390/ijfs12020030