Exploring the Dynamics of Profitability–Liquidity Relations in Crisis, Pre-Crisis and Post-Crisis

Abstract

:1. Introduction

2. Literature Review and Research Questions

- Is the profitability—liquidity relationship stable in times of crisis?

- What is the profitability of companies with high and low liquidity?

- What is the liquidity of companies with high and low profitability?

3. Methodology

3.1. Sample

3.2. Variables

3.3. Analytical Approach

4. Results

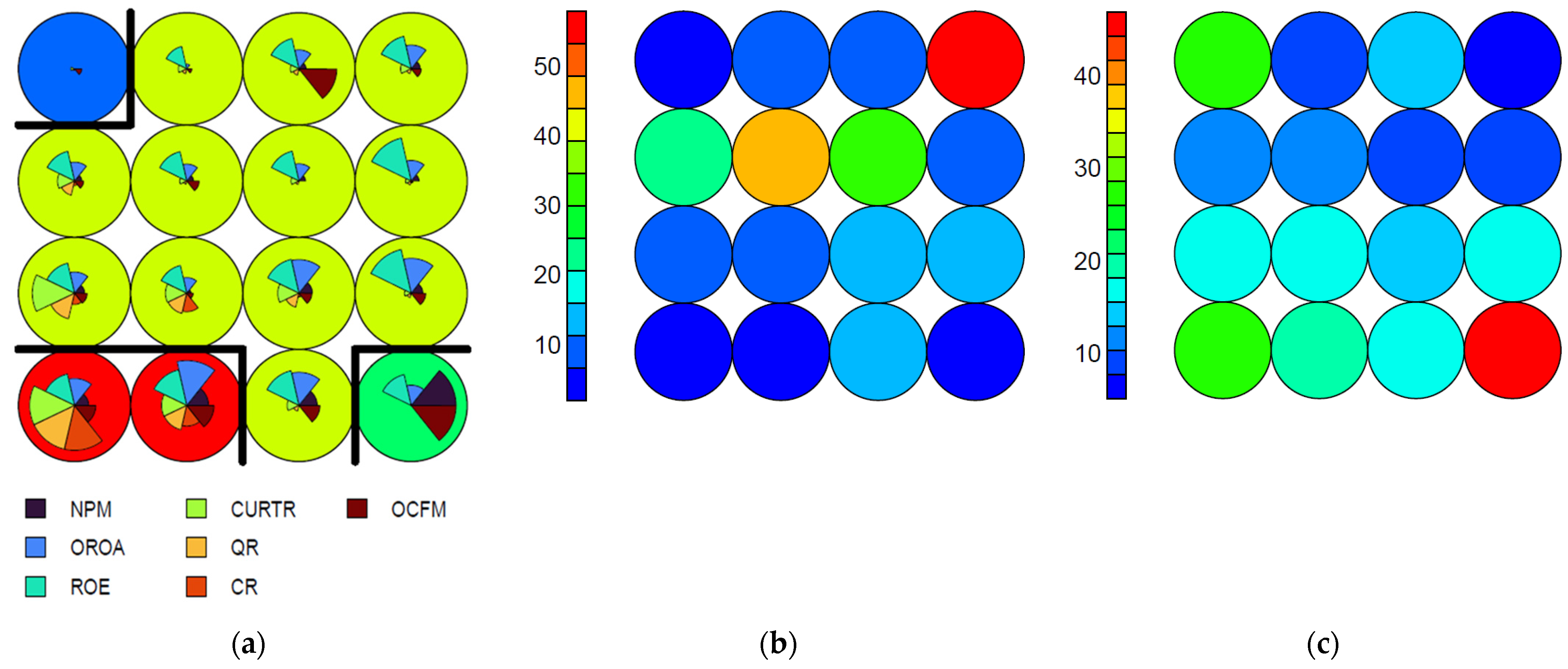

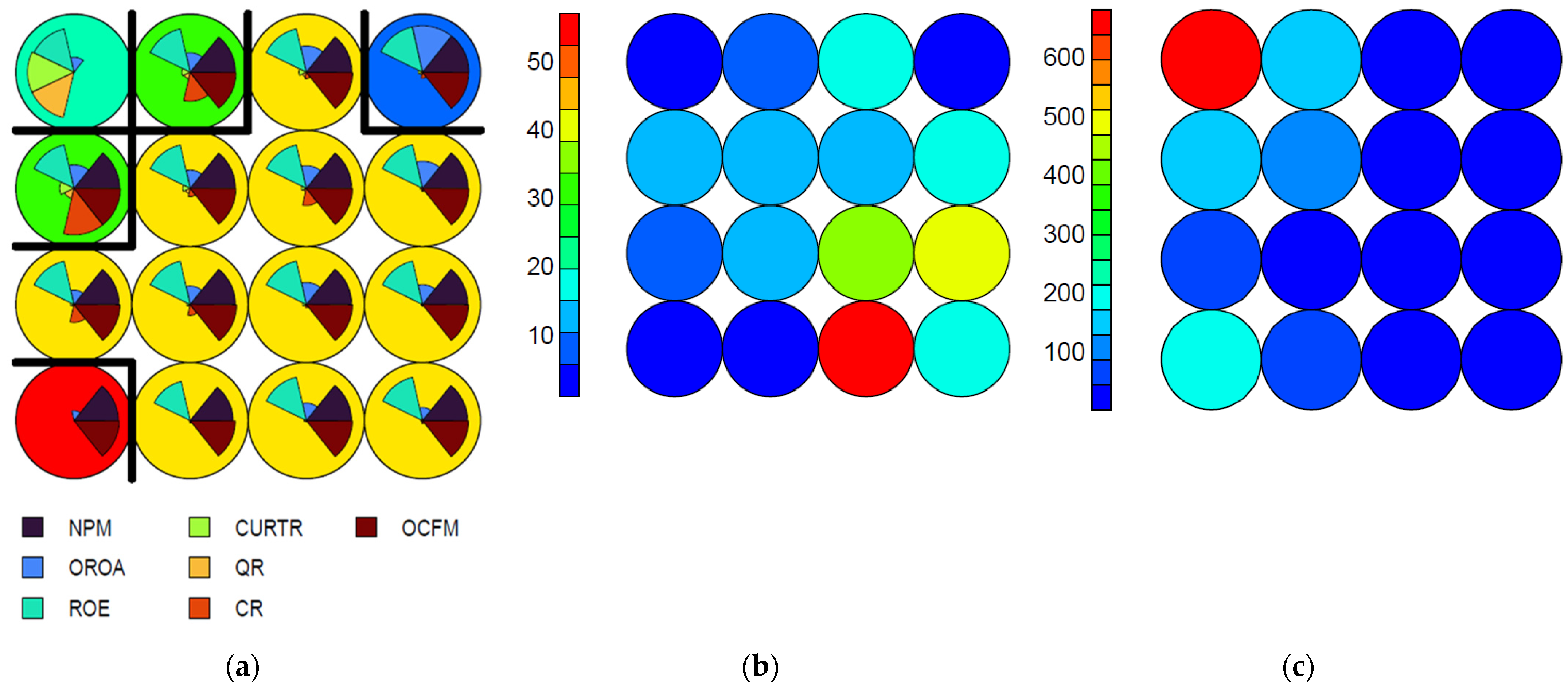

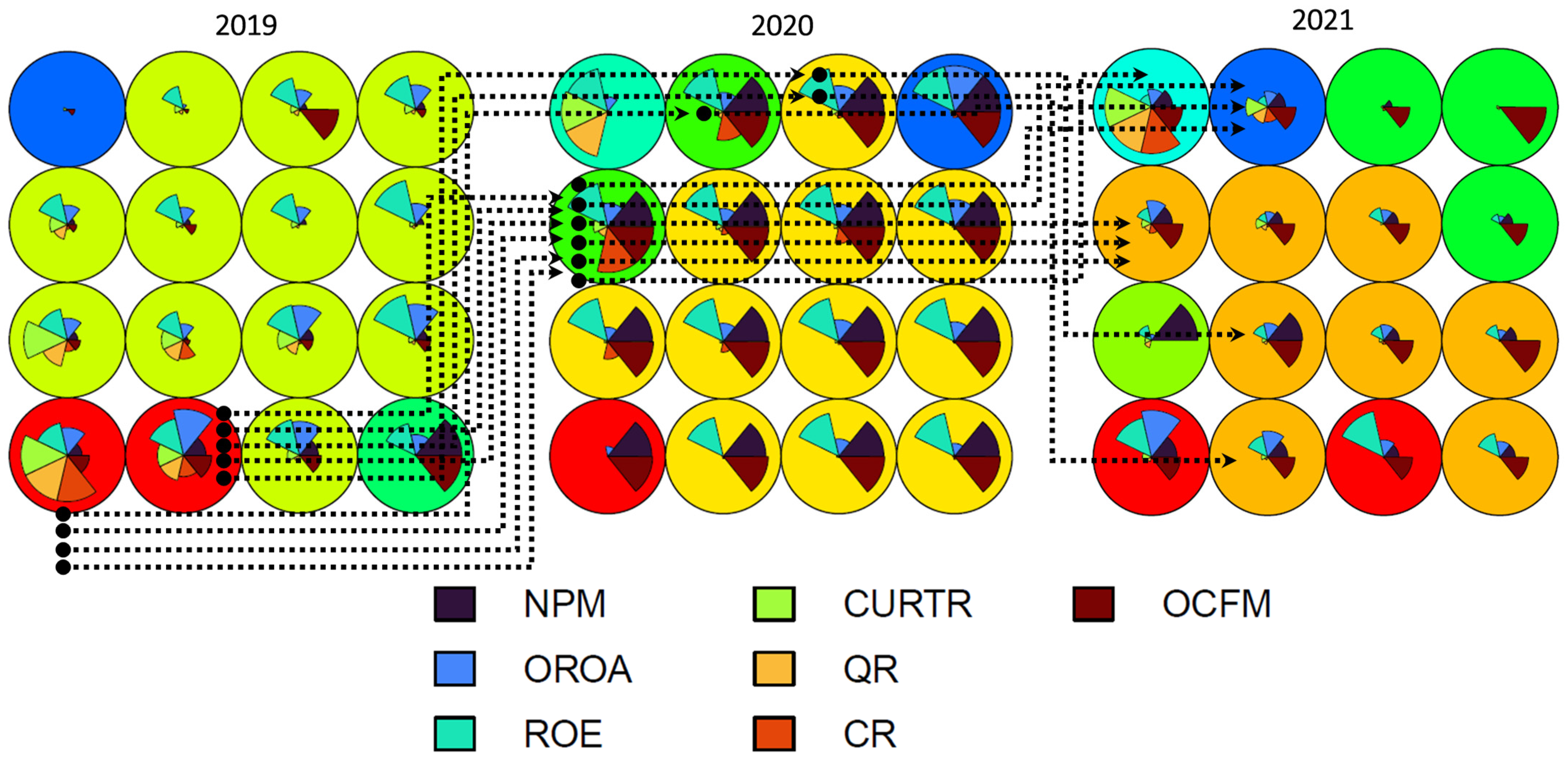

4.1. Codes, Node Counts, and Neighbor Distance Plots in 2019, 2020, and 2021

4.2. The Trajectory of High Profitability—High Liquidity Companies over 2019–2021

5. Discussion, Limitations and Future Research

6. Conclusions

Author Contributions

Funding

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A. Heatmaps for 2019

Appendix B. Heatmaps for 2020

Appendix C. Heatmaps for 2021

Appendix D. The Order of the Nodes

References

- Adamczyk, Adam, and Piotr Waśniewski. 2018. Is Excess Liquidity Real? The Analysis of Relationship between Liquidity and Profitability. Zeszyty Naukowe Uniwersytetu Szczecińskiego Finanse Rynki Finansowe Ubezpieczenia 92: 11–21. [Google Scholar] [CrossRef]

- Adelopo, Ismail, Robert Lloydking, and Venancio Tauringana. 2018. Determinants of Bank Profitability before, during, and after the Financial Crisis. International Journal of Managerial Finance 14: 378–98. [Google Scholar] [CrossRef]

- Arslan-Ayaydin, Özgür, Chris Florackis, and Aydin Ozkan. 2014. Financial Flexibility, Corporate Investment and Performance: Evidence from Financial Crises. Review of Quantitative Finance and Accounting 42: 211–50. [Google Scholar] [CrossRef]

- Awad, Ibrahim, Fahema Jayya, Ibrahim Awad, and Fahema Jayya. 2013. Working Capital Management, Liquidity and Profitability of the Manufacturing Sector in Palestine: Panel Co-Integration and Causality. Modern Economy 4: 662–71. [Google Scholar] [CrossRef]

- Byczkowska, Magdalena, and Andrzej Kuciński. 2018. Ocena Płynności Finansowej Przedsiębiorstw Na Podstawie Analizy Rachunku Przepływów Pieniężnych. Zeszyty Naukowe Małopolskiej Wyższej Szkoły Ekonomicznej w Tarnowie 38: 85–100. [Google Scholar] [CrossRef]

- Chambers, Nurgul, and Atilla Cifter. 2022. Working Capital Management and Firm Performance in the Hospitality and Tourism Industry. International Journal of Hospitality Management 102: 103144. [Google Scholar] [CrossRef]

- Cheong, Carol, Huy Viet Hoang, and David Mcmillan. 2021. Macroeconomic Factors or Firm-Specific Factors? An Examination of the Impact on Corporate Profitability before, during and after the Global Financial Crisis. Cogent Economics & Finance 9: 1959703. [Google Scholar] [CrossRef]

- Chow, Yee Peng, Junaina Muhammad, A. N. Bany-Ariffin, and Fan Fah Cheng. 2018. Macroeconomic Uncertainty, Corporate Governance and Corporate Capital Structure. International Journal of Managerial Finance 14: 301–21. [Google Scholar] [CrossRef]

- Cottrell, Marie, and Patrick Rousset. 1997. The Kohonen Algorithm: A Powerful Tool for Analysing and Representing Multidimensional Quantitative and Qualitative Data. In Biological and Artificial Computation: From Neuroscience to Technology. Lecture Notes in Computer Science (Including Subseries Lecture Notes in Artificial Intelligence and Lecture Notes in Bioinformatics). Berlin and Heidelberg: Springer, vol. 1240 LNCS, pp. 861–71. [Google Scholar] [CrossRef]

- Du Jardin, Philippe, and Eric Séverin. 2012. Forecasting Financial Failure Using a Kohonen Map: A Comparative Study to Improve Model Stability over Time. European Journal of Operational Research 221: 379–96. [Google Scholar] [CrossRef]

- Eljelly, Abuzar M. A. 2004. Liquidity—Profitability Tradeoff: An Empirical Investigation in an Emerging Market. International Journal of Commerce and Management 14: 48–61. [Google Scholar] [CrossRef]

- Gentry, James. 1976. Management Perceptions of the Working Capital Process. Champaign: College of Commerce and Business Administration, University of Illinois at Urbana. Available online: https://core.ac.uk/download/pdf/4835142.pdf (accessed on 10 December 2023).

- Hawawini, Gabriel, Venkat Subramanian, and Paul Verdin. 2003. Is Performance Driven by Industry—Or Firm-Specific Factors? A New Look at the Evidence. Strategic Management Journal 24: 1–16. [Google Scholar] [CrossRef]

- Hirigoyen, Gerard. 1985. Rentabilité et Solvabilité. Direction et Gestion, 3, 13–26.—References—Scientific Research Publishing. Available online: https://www.scirp.org/(S(351jmbntvnsjt1aadkozje))/reference/referencespapers.aspx?referenceid=2170423 (accessed on 5 December 2023).

- Hirsch, Stefan, Jan Schiefer, Adelina Gschwandtner, and Monika Hartmann. 2014. The Determinants of Firm Profitability Differences in EU Food Processing. Journal of Agricultural Economics 65: 703–21. [Google Scholar] [CrossRef]

- Jaworski, Jacek, and Leszek Czerwonka. 2021. Meta-Study on the Relationship between Profitability and Liquidity of Enterprises in Macroeconomic and Institutional Environment. Decision 48: 233–46. [Google Scholar] [CrossRef]

- Jaworski, Jacek, Leszek Czerwonka, and Magdalena Mądra-Sawicka. 2018. Zależność Między Rentownością a Płynnością Finansową w Sektorze Przetwórstwa Spożywczego w Polsce. Roczniki Naukowe Stowarzyszenia Ekonomistów Rolnictwa i Agrobiznesu 20: 58–63. [Google Scholar] [CrossRef]

- Jensen, Michael. 1986. Agency Costs of Free Cash Flow, Corporate Finance, and Takeovers. American Economic Review 76: 323–29. [Google Scholar]

- Jose, Manuel L., Carol Lancaster, and Jerry L. Stevens. 1996. Corporate returns and cash conversion cycles. Journal of Economics and Finance 20: 33–46. [Google Scholar] [CrossRef]

- Kowerski, Mieczysław. 2016. Zależność Między Rentownością a Płynnością Finansową Ma Kształt Odwróconego U. Prace Naukowe Uniwersytetu Ekonomicznego We Wrocławiu 440: 338–48. [Google Scholar] [CrossRef]

- Lee, Chien Chiang, Mei Ping Chen, and Shao Lin Ning. 2017. Why Did Some Firms Perform Better in the Global Financial Crisis? Economic Research-Ekonomska Istraživanja 30: 1339–66. [Google Scholar] [CrossRef]

- Lynn, Shanel. 2014. Self-Organising Maps for Customer Segmentation Using R. Available online: https://www.shanelynn.ie/self-organising-maps-for-customer-segmentation-using-r/ (accessed on 5 December 2023).

- Maçãs Nunes, Paulo J., Zélia M. Serrasqueiro, and Tiago N. Sequeira. 2009. Profitability in Portuguese Service Industries: A Panel Data Approach. The Service Industries Journal 29: 693–707. [Google Scholar] [CrossRef]

- Makhija, Mona. 2003. Comparing the Resource-Based and Market-Based Views of the Firm: Empirical Evidence from Czech Privatization. Strategic Management Journal 24: 433–51. [Google Scholar] [CrossRef]

- Miljković, Dubravko. 2017. Brief Review of Self-Organizing Maps, 1252–57. Available online: https://ieeexplore.ieee.org/document/7973581 (accessed on 1 December 2023).

- Nanda, Swagatika, and Ajaya Kumar Panda. 2018. The Determinants of Corporate Profitability: An Investigation of Indian Manufacturing Firms. International Journal of Emerging Markets 13: 66–86. [Google Scholar] [CrossRef]

- Notta, Ourania, and Aspasia Vlachvei. 2014. The Impact of Financial Crisis on Firm Performance in Case of Greek Food Manufacturing Firms. Procedia Economics and Finance 14: 454–60. [Google Scholar] [CrossRef]

- Nowicki, Jarosław. 2023. Rentowność czy wydajność gotówkowa? Syntetyczny pomiar efektywności w kontekście działań z zakresu kreatywnej rachunkowości. In Analiza ekonomiczna w warunkach niepewności. Edited by Cezary Kochalski. Poznań: Wydawnictwo Uniwersytetu Ekonomicznego w Poznaniu, pp. 102–17. [Google Scholar] [CrossRef]

- Nunes, Paulo Maçãs, Ana Viveiros, and Zélia Serrasqueiro. 2012. Are the Determinants of Young SME Profitability Different? Empirical Evidence Using Dynamic Estimators. Journal of Business Economics and Management 13: 443–70. [Google Scholar] [CrossRef]

- Pervan, Maja, Ivica Pervan, and Marijana Ćurak. 2019. Determinants of Firm Profitability in the Croatian Manufacturing Industry: Evidence from Dynamic Panel Analysis. Economic Research-Ekonomska Istrazivanja 32: 968–81. [Google Scholar] [CrossRef]

- Ratajczak, Piotr. 2023. Holistyczna koncepcja procesu bankructwa przedsiębiorstwa. In Analiza ekonomiczna w warunkach niepewności. Edited by Cezary Kochalski. Poznań: Wydawnictwo Uniwersytetu Ekonomicznego w Poznaniu, pp. 118–34. [Google Scholar] [CrossRef]

- Shakina, Elena, and Angel Barajas. 2014. The Dynamics of Intellectual Resources during the Economic Crisis. Economic Research-Ekonomska Istrazivanja 27: 861–81. [Google Scholar] [CrossRef]

- Sur, Debasish, and Kaushik Chakraborty. 2011. Evaluating Relationship of Working Capital and Profitability: A Study of Select Multinational Companies in the Indian Pharmaceutical Sector. The IUP Journal of Management Research: IJMR 10: 7. [Google Scholar]

- Tonidandel, Scott, Eden B. King, and Jose M. Cortina. 2018. Big Data Methods: Leveraging Modern Data Analytic Techniques to Build Organizational Science. Organizational Research Methods 21: 525–47. [Google Scholar] [CrossRef]

- Varum, Celeste Amorim, and Vera Catarina Rocha. 2013. Employment and SMEs during Crises. Small Business Economics 40: 9–25. [Google Scholar] [CrossRef]

- Vieira, Renato Schwambach. 2010. The Relationship between Liquidity and Profitability. An Exploratory Study of Airline Companies between 2005 and 2008. Unpublished Master’s thesis, Umeå University, Umeå, Sweden. Available online: http://www.diva-portal.org/smash/get/diva2:409560/FULLTEXT01.pdf (accessed on 7 December 2023).

- Wehrens, Ron. 2007. Self- and Super-organizing Maps in R: The Kohonen Package. JSS Journal of Statistical Software 21: 1–19. Available online: http://www.jstatsoft.org/ (accessed on 7 December 2023).

- Wehrens, Ron, and Kruisselbrink Johannes. 2023. Package ‘kohonen’ Title Supervised and Unsupervised Self-Organising Maps. Available online: https://cran.r-project.org/web/packages/kohonen/kohonen.pdf (accessed on 2 December 2023).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Node | NPM | OROA | ROE | CURTR | QR | CR | OCFM |

|---|---|---|---|---|---|---|---|

| V1 | 0.91 | 0.54 | −0.03 | 3.35 | 4.24 | 5.39 | 1.03 |

| V2 | 2.28 | 2.54 | 0.67 | 1.31 | 1.95 | 2.25 | 1.65 |

| V3 | 1.64 | 1.23 | 0.53 | −0.06 | −0.26 | −0.32 | 1.00 |

| V4 | 6.44 | −0.21 | −0.12 | −1.29 | −0.92 | −0.38 | 3.49 |

| V5 | 0.17 | −0.10 | −0.26 | 3.08 | 2.09 | 1.04 | 0.12 |

| V6 | −0.87 | −0.72 | −0.65 | 0.92 | 1.45 | 1.97 | −0.53 |

| V7 | 0.78 | 1.28 | 0.39 | 0.91 | 0.71 | 0.05 | 0.16 |

| V8 | 0.46 | 1.43 | 2.04 | −0.59 | −0.40 | −0.37 | 0.33 |

| V9 | −0.34 | −0.36 | −0.31 | 0.48 | 0.74 | 0.16 | −0.25 |

| V10 | −0.42 | −0.58 | −0.37 | −0.56 | −0.55 | −0.38 | 0.10 |

| V11 | −0.46 | −0.55 | −0.30 | −0.47 | −0.52 | −0.41 | −1.19 |

| V12 | −0.23 | −0.17 | 1.91 | −0.70 | −0.47 | −0.19 | −0.98 |

| V13 | −1.65 | −2.47 | −5.31 | −0.90 | −0.72 | −0.42 | −0.44 |

| V14 | −1.58 | −1.95 | −1.56 | −0.41 | −0.35 | −0.34 | −0.66 |

| V15 | −0.37 | −0.35 | −0.22 | −0.39 | −0.19 | −0.18 | 2.75 |

| V16 | −0.01 | 0.18 | 0.15 | −0.19 | −0.36 | −0.33 | −0.14 |

| Node | NPM | OROA | ROE | CURTR | QR | CR | OCFM |

|---|---|---|---|---|---|---|---|

| V1 | −0.27 | −1.75 | −14.50 | −0.94 | −0.64 | −0.62 | −0.25 |

| V2 | −0.77 | −3.44 | −1.40 | −0.67 | −0.46 | −0.44 | −0.23 |

| V3 | 0.04 | −0.44 | 0.06 | −0.41 | −0.36 | −0.54 | 0.04 |

| V4 | −0.03 | −1.19 | 0.01 | −0.51 | −0.44 | −0.36 | 0.04 |

| V5 | −0.02 | −0.98 | 0.03 | −0.14 | −0.13 | 0.99 | 0.00 |

| V6 | 0.06 | −0.30 | 0.06 | −0.12 | −0.05 | 0.35 | 0.18 |

| V7 | 0.10 | 0.32 | 0.08 | −0.05 | −0.17 | −0.35 | 0.07 |

| V8 | 0.06 | −0.05 | 0.09 | −0.58 | −0.50 | −0.47 | 0.05 |

| V9 | 0.16 | 0.59 | 0.07 | 2.42 | 2.05 | 3.57 | 0.14 |

| V10 | 0.05 | −0.31 | 0.05 | 0.78 | 0.72 | 0.12 | −0.06 |

| V11 | 0.09 | 0.45 | 0.08 | 0.19 | 0.16 | 0.93 | 0.07 |

| V12 | 0.15 | 1.21 | 0.15 | −0.39 | −0.28 | −0.36 | 0.18 |

| V13 | −15.60 | −0.88 | 0.04 | 9.94 | 11.52 | −0.63 | −15.73 |

| V14 | 0.06 | −0.11 | 0.06 | 1.01 | 1.11 | 1.99 | −0.01 |

| V15 | 0.15 | 1.06 | 0.09 | 0.79 | 0.55 | −0.06 | 0.12 |

| V16 | 0.45 | 4.51 | 0.70 | 0.04 | 0.10 | −0.09 | 0.11 |

| Node | NPM | OROA | ROE | CURTR | QR | CR | OCFM |

|---|---|---|---|---|---|---|---|

| V1 | 1.55 | 3.55 | 2.29 | 0.64 | 0.30 | −0.10 | 0.18 |

| V2 | 0.68 | 1.24 | 0.51 | 0.19 | −0.04 | −0.34 | −0.15 |

| V3 | −0.15 | 0.26 | 2.96 | −0.82 | −0.44 | −0.26 | 0.11 |

| V4 | −0.11 | 0.08 | 0.75 | −0.68 | −0.53 | −0.39 | 0.08 |

| V5 | 4.89 | −0.98 | −0.12 | 0.21 | 0.86 | −0.51 | −5.78 |

| V6 | 3.06 | 0.27 | −0.06 | 0.07 | 0.22 | −0.17 | 1.23 |

| V7 | −0.07 | 0.08 | −0.20 | −0.08 | 0.02 | 0.37 | 0.29 |

| V8 | 0.12 | −0.49 | −0.06 | −0.70 | −0.37 | −0.39 | 2.51 |

| V9 | 0.80 | 0.92 | −0.04 | 0.77 | 0.91 | 1.56 | 0.66 |

| V10 | −0.15 | −0.32 | −0.56 | 1.08 | 0.72 | 0.17 | −0.20 |

| V11 | −0.22 | −0.11 | 0.01 | −0.31 | −0.40 | −0.42 | −0.47 |

| V12 | −0.52 | −0.81 | −0.66 | −0.67 | −0.60 | −0.34 | −0.08 |

| V13 | 0.84 | 0.32 | −0.36 | 6.79 | 8.58 | 9.67 | 0.66 |

| V14 | 0.29 | 0.08 | −0.50 | 2.75 | 2.67 | 2.74 | 0.06 |

| V15 | −1.24 | −1.49 | −1.44 | −0.43 | −0.26 | 0.26 | −0.41 |

| V16 | −2.59 | −1.66 | −1.60 | −0.29 | −0.08 | −0.28 | 3.74 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ratajczak, P.; Szutowski, D.; Nowicki, J. Exploring the Dynamics of Profitability–Liquidity Relations in Crisis, Pre-Crisis and Post-Crisis. Int. J. Financial Stud. 2024, 12, 16. https://doi.org/10.3390/ijfs12010016

Ratajczak P, Szutowski D, Nowicki J. Exploring the Dynamics of Profitability–Liquidity Relations in Crisis, Pre-Crisis and Post-Crisis. International Journal of Financial Studies. 2024; 12(1):16. https://doi.org/10.3390/ijfs12010016

Chicago/Turabian StyleRatajczak, Piotr, Dawid Szutowski, and Jarosław Nowicki. 2024. "Exploring the Dynamics of Profitability–Liquidity Relations in Crisis, Pre-Crisis and Post-Crisis" International Journal of Financial Studies 12, no. 1: 16. https://doi.org/10.3390/ijfs12010016