CSR Disclosures, CSR Awards and Corporate Governance as Determinants of the Cost of Debt: Evidence from Malaysia

Abstract

:1. Introduction

The Malaysian Institutional Setting and the Development of Corporate Social Responsibility

2. Theoretical Framework and Hypothesis Development

2.1. Media Influence, CSR Disclosures and the Cost of Debt

2.2. Board Size, CSR Disclosures and the Cost of Debt

2.3. Political Connections and the Cost of Debt

2.4. Government Ownership and the Cost of Debt

2.5. Non-Governmental Institutional Ownership

2.6. Audit Committee Independence and the Cost of Debt

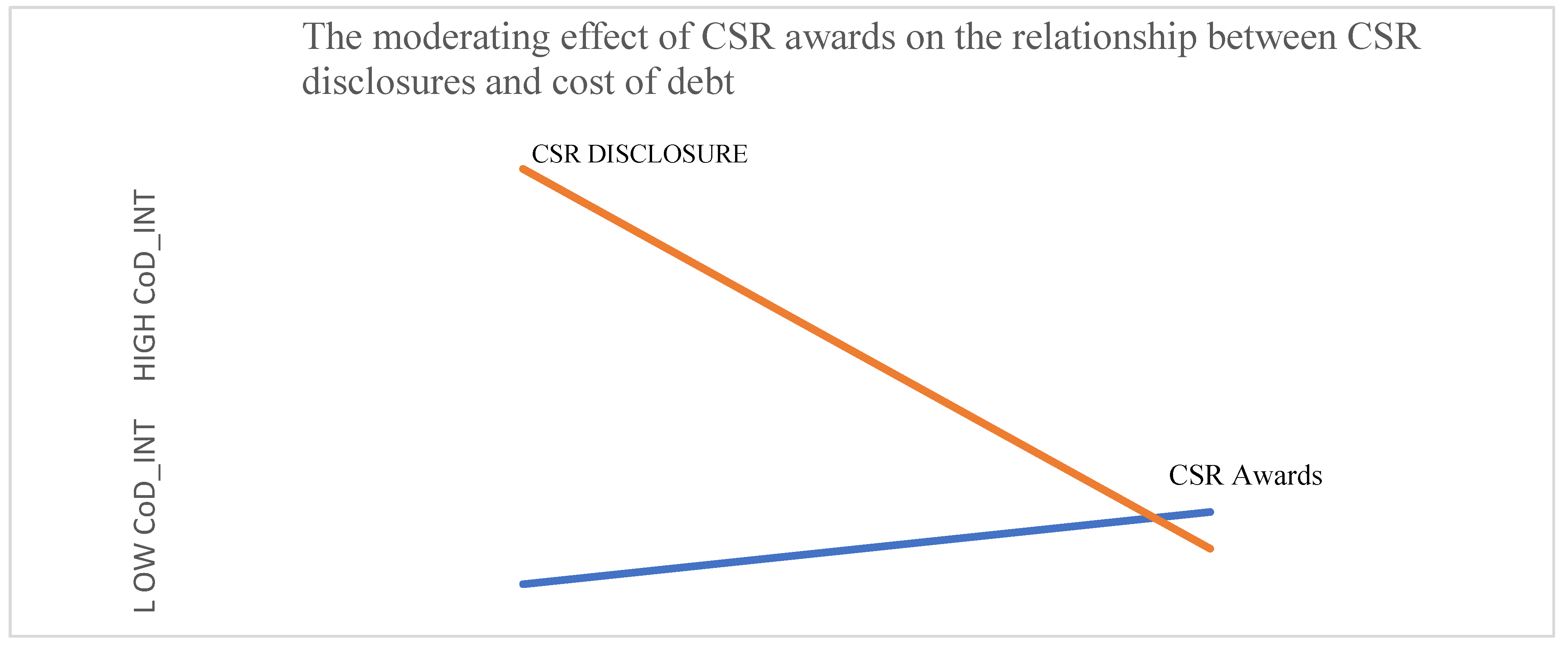

2.7. Moderating the Role of CSR Disclosures and CSR Awards on the Cost of Debt

3. Research Methodology

3.1. Construction of the CSR Index

3.2. Sample Selection

3.3. Measurement of the Dependent, Independent and Control Variables

3.3.1. Dependent Variable

3.3.2. Independent Variables

3.4. Empirical Model Specifications

4. Results and Discussion

4.1. Preliminary Analysis

4.2. Estimation Results

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

- (1)

- Community activities

- (2)

- Workplace: employment conditions

- (3)

- Environment

- (4)

- Reporting and standards

Appendix B

| Variable Measurements | |

| Variable | Descriptions |

| Dependent | |

| Cost of Debt (COD_INT) | The interest expense of the firm divided by its average short-term and long-term data during the year. |

| CSR disclosures (CSR_INDEX) | The CSR_INDEX is obtained by calculating the total scores given to each firm under the StarBiz awards criteria. Thereafter, the median adjusted score for each firm within the industry is added to the number of words describing the CSR policy of the firm (items shown in Appendix A). |

| Board Governance | |

| Board Size (BO_SIZE) | Number of directors on the board. |

| Audit Committee Independence (AC_IND) | Percentage of independent directors on the audit committee. |

| Ownership Structure | |

| Government Institutional Investors (GOV_INST) | Percentage of shares of a company held by government-related institutional investors, directly or indirectly (EPF, LTAT, PNB, LTH and SOCSO). |

| Other Institutional Investors (OTH_INST) | Percentage of shares held by all other institutional investors (excluding EPF, LTAT, PNB, LTH and SOCSO) holding at least 5 percent of outstanding shares. |

| Political Connection (POL_CON) | An indicator variable that equals 1 if the company is politically connected and 0 otherwise. |

| Variable Measurements | |

| Variable | Descriptions |

| CSR Awards (CSR_AWARDS) | An indicator variable that equals 1 if the firm was awarded a CSR award during that year and 0 otherwise. |

| Control | |

| Firm Size (FIRM_SIZE) | The log of the book value of total assets at the end of the year. |

| Age of Firm (FIRM_AGE) | Years since the firm began its business activity. |

| Return on Assets (ROA) | Profit after tax, divided by total assets. |

| Growth (GROWTH) | Tobin’s Q as a proxy. Calculated as the market value of equity plus the book value of long-term debts and current liability, scaled by the book value of total assets. |

| Creditors’ Power/Leverage (CRED_POWER) | Long-term debts divided by total assets. |

| 1 | The 10th Malaysia Plan identifies 12 key economic sectors that have the potential to achieve the status of a high-income nation. The sectors identified are oil and gas, palm oil and related products, financial services, tourism, education services, communication, information technology, wholesale and retailing, electric and electronics, business services, private health care, agriculture and the development of Greater Kuala Lumpur. The plan further states that this growth should be economically and environmentally sustainable, meeting the present needs without compromising those of future generations. (https://pmo.gov.my/dokumenattached/RMK/RMK10_Eds.pdf, assessed on 9 June 2022). |

| 2 | Though Malaysia is in the process of harmonizing its accounting standards with the International Accounting Standards, its current accounting standards, FRS 137 and FRS 101, do not consider social and environmental information in the Management Analysis and Discussion section of their annual reports. However, companies have been encouraged to provide information such as contingent liabilities and assets to aid investors in their decision making. Malaysia’s environmental and social reporting practices are presently seen as a Code of Best Practice, and there are no specific accounting standards to address CSR reporting practices. |

| 3 | Under the legitimacy theory, a social contract exists in implicit terms between business and society. Friedman (1970) argued that a firm’s primary purpose is to maximize shareholder wealth. A paradigm shift in the 1980s saw a change in the role of firms to that of meeting the needs of all stakeholders (Freeman 2010). |

| 4 | We believe that even private banks value PLCs with good CSR reputation, because, for example, the CEO of a leading private bank was the brother of the prime minister during the period of our study. |

| 5 | The largest banks in Malaysia are state owned, and most Malaysian PLCs have significant relations with them. |

| 6 | The Edge Billion Ringgit Club (BRC) members comprise about 19% of the number of listed companies in Bursa Malaysia as of 2014. Awards to companies are not only based on their financial performance, but due recognition is also given to companies showing exemplary leadership in building their businesses and creating value for their stakeholders. |

| 7 | The five largest public institutional investors in Malaysia are the Employees’ Provident Fund (EPF), Lembaga Tabung Angkatan Tentera (LTAT), an investment fund (Permodalan Nasional Berhad (PNB)), a pilgrim fund (Lembaga Tabung Haji (LTH)) and the National Social Security Organisation of Malaysia (SOCSO). The Ministry of Finance defines these five institutional investors as the primary government-related institutional owners. |

| 8 | A possible reason for the average cost of debt of 5.2% is due to the reduced cost of borrowing from sources of funding such as grants, feed-in-tariff mechanisms and the Green Technology Financing Scheme (GTFS) offered by commercial banks, Islamic banks, Pembangunan, SME Bank, Agrobank, Bank Rakyat, EXIM Bank and Bank Simpanan Nasional. |

| 9 | We used the Janis–Fadner Coefficient to directly capture the effect of media influence on CSR_INDEX and COD_INT, but unfortunately, it was not significant. |

References

- Abdifatah Ahmed, Haji. 2013. Corporate social responsibility disclosures over time: Evidence from Malaysia. Managerial Auditing Journal 28: 647–76. [Google Scholar] [CrossRef]

- Ader, Christine R. 1995. A longitudinal study of agenda setting for the issue of environmental pollution. Journalism & Mass Communication Quarterly 72: 300–11. [Google Scholar]

- Aerts, Walter, and Denis Cormier. 2009. Media legitimacy and corporate environmental communication. Accounting, Organizations and Society 34: 1–27. [Google Scholar] [CrossRef]

- Ali, Waris, Jedrzej George Frynas, and Zeeshan Mahmood. 2017. Determinants of Corporate Social Responsibility (CSR) Disclosure in Developed and Developing Countries: A Literature Review. Corporate Social Responsibility and Environmental Management 24: 273–94. [Google Scholar] [CrossRef]

- Amran, Azlan, and S. Susela Devi. 2008. The impact of government and foreign affiliate influence on corporate social reporting: The case of Malaysia. Managerial Auditing Journal 23: 386–404. [Google Scholar] [CrossRef]

- Anas, Abdirahman, Hafiz Majdi Abdul Rashid, and Hairul Azlan Annuar. 2015. The effect of award on CSR disclosures in annual reports of Malaysian PLCs. Social Responsibility Journal 11: 831–52. [Google Scholar] [CrossRef]

- Anderson, Ronald C., Sattar A. Mansi, and David M. Reeb. 2003. Founding family ownership and the agency cost of debt. Journal of Financial Economics 68: 263–85. [Google Scholar] [CrossRef]

- Antunovich, Peter, David Laster, and Scott Mitnick. 2000. Are High-Quality Firms Also High-Quality Investments? Available online: https://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.200.2453&rep=rep1&type=pdf (accessed on 20 September 2022).

- Atkinson, Anthony B., and Joseph E. Stiglitz. 2015. Lectures on Public Economics. Princeton: Princeton University Press. [Google Scholar]

- Barnea, Amir, and Amir Rubin. 2010. Corporate Social Responsibility as a Conflict Between Shareholders. Journal of Business Ethics 97: 71–86. [Google Scholar] [CrossRef]

- Barnett, Michael L. 2007. Stakeholder influence capacity and the variability of financial returns to corporate social responsibility. Academy of Management Review 32: 794–816. [Google Scholar] [CrossRef]

- Bebbington, Jan, Carlos Larrinaga, and Jose M. Moneva. 2008. Corporate social reporting and reputation risk management. Accounting, Auditing & Accountability Journal 21: 337–61. [Google Scholar]

- Bliss, Mark A., and Ferdinand A. Gul. 2012. Political connection and cost of debt: Some Malaysian evidence. Journal of Banking & Finance 36: 1520–27. [Google Scholar]

- Bliss, Mark A., Ferdinand A. Gul, and Abdul Majid. 2011. Do political connections affect the role of independent audit committees and CEO Duality? Some evidence from Malaysian audit pricing. Journal of Contemporary Accounting & Economics 7: 82–98. [Google Scholar] [CrossRef]

- Boachie, Christopher, and Joseph Emmanuel Tetteh. 2021. Do creditors value corporate social responsibility disclosure? Evidence from Ghana. International Journal of Ethics and Systems 37: 466–85. [Google Scholar] [CrossRef]

- Buniamin, Sharifah. 2010. The quantity and quality of environmental reporting in annual report of public listed companies in Malaysia. Issues in Social and Environmental Accounting 4: 115–35. [Google Scholar] [CrossRef]

- Cai, Ye, Hoje Jo, and Carrie Pan. 2012. Doing well while doing bad? CSR in controversial industry sectors. Journal of Business Ethics 108: 467–80. [Google Scholar] [CrossRef]

- Campbell, John L. 2007. Why Would Corporations Behave In Socially Responsible Ways? An Institutional Theory of Corporate Social Responsibility. Academy of Management Review 32: 946–67. [Google Scholar] [CrossRef]

- Chaney, Paul K., Mara Faccio, and David Parsley. 2011. The quality of accounting information in politically connected firms. Journal of Accounting and Economics 51: 58–76. [Google Scholar] [CrossRef]

- Cheng, Zhihua, Feng Wang, Christine Keung, and Yongxiu Bai. 2017. Will corporate political connection influence the environmental information disclosure level? Based on the panel data of A-shares from listed companies in shanghai stock market. Journal of Business Ethics 143: 209–21. [Google Scholar] [CrossRef]

- Clarkson, Peter M., Xiaohua Fang, Yue Li, and Gordon Richardson. 2013. The relevance of environmental disclosures: Are such disclosures incrementally informative? Journal of Accounting and Public Policy 32: 410–31. [Google Scholar] [CrossRef]

- Coles, Jeffery L., Naveen D. Daniel, and Lalitha Naveen. 2008. Boards: Does one size fit all? Journal of Financial Economics 87: 329–56. [Google Scholar] [CrossRef]

- Cong, Yu, and Martin Freedman. 2011. Corporate governance and environmental performance and disclosures. Advances in Accounting 27: 223–32. [Google Scholar] [CrossRef]

- Cormier, Denis, Michel Magnan, and Bernard Morard. 1993. The impact of corporate pollution on market valuation: Some empirical evidence. Ecological Economics 8: 135–55. [Google Scholar] [CrossRef]

- Cressy, Robert, Douglas Cumming, and Christine Mallin. 2012. Entrepreneurship, Governance and Ethics. In Entrepreneurship, Governance and Ethics. Edited by Robert Cressy, Douglas Cumming and Christine Mallin. Dordrecht: Springer, pp. 117–20. [Google Scholar] [CrossRef]

- Cuadrado-Ballesteros, Beatriz, Isabel-Maria Garcia-Sanchez, and Jennifer Martinez Ferrero. 2016. How are corporate disclosures related to the cost of capital? The fundamental role of information asymmetry. Management Decision 54: 1669–701. [Google Scholar] [CrossRef]

- Deegan, Craig, and Gary Carroll. 1993. An Analysis of Incentives for Australian Firms to Apply for Reporting Excellence Awards. Accounting and Business Research 23: 219–27. [Google Scholar] [CrossRef]

- Deegan, Craig, and Michaela Rankin. 1999. The Environmental Reporting Expectations Gap: Australian Evidence. The British Accounting Review 31: 313–46. [Google Scholar] [CrossRef]

- Deegan, Craig, Michaela Rankin, and John Tobin. 2002. An examination of the corporate social and environmental disclosures of BHP from 1983–1997: A test of legitimacy theory. Accounting, Auditing & Accountability Journal 15: 312–43. [Google Scholar]

- Deephouse, David L., and Suzanne M. Carter. 2005. An examination of differences between organizational legitimacy and organizational reputation. Journal of Management Studies 42: 329–60. [Google Scholar] [CrossRef]

- Dhaliwal, Dan S., Oliver Zhen Li, Albert Tsang, and Yong George Yang. 2011. Voluntary nonfinancial disclosure and the cost of equity capital: The initiation of corporate social responsibility reporting. The Accounting Review 86: 59–100. [Google Scholar] [CrossRef]

- Dhaliwal, Dan S., Suresh Radhakrishnan, Albert Tsang, and Yong George Yang. 2012. Nonfinancial Disclosure and Analyst Forecast Accuracy: International Evidence on Corporate Social Responsibility Disclosure. Accounting Review 87: 723–59. [Google Scholar] [CrossRef]

- DiMaggio, Paul, and Walter W. Powell. 1983. The iron cage revisited: Collective rationality and institutional isomorphism in organizational fields. American Sociological Review 48: 147–60. [Google Scholar] [CrossRef]

- Du, Shuili, and Edward T. Vieira. 2012. Striving for legitimacy through corporate social responsibility: Insights from oil companies. Journal of Business Ethics 110: 413–27. [Google Scholar] [CrossRef]

- Eng, Li Li, and Yuen Teen Mak. 2003. Corporate governance and voluntary disclosure. Journal of Accounting and Public Policy 22: 325–45. [Google Scholar] [CrossRef]

- Ettenson, Richard, and Jonathan Knowles. 2008. Don’t confuse reputation with brand. MIT Sloan Management Review 49: 19. [Google Scholar]

- Faccio, Mara. 2010. Differences between politically connected and nonconnected firms: A cross-country analysis. Financial Management 39: 905–28. [Google Scholar] [CrossRef]

- Fan, Joseph P. H., Oliver Meng Rui, and Mengxin Zhao. 2008. Public governance and corporate finance: Evidence from corruption cases. Journal of Comparative Economics 36: 343–64. [Google Scholar] [CrossRef]

- Fombrun, Charles. 1996. Reputation. Hoboken: Wiley Online Library. [Google Scholar]

- Fombrun, Charles. 2005. A world of reputation research, analysis and thinking—Building corporate reputation through CSR initiatives: Evolving standards. Corporate Reputation Review 8: 7–12. [Google Scholar] [CrossRef]

- Forker, John J. 1992. Corporate Governance and Disclosure Quality. Accounting & Business Research (Wolters Kluwer UK) 22: 111–24. [Google Scholar]

- Freeman, R. Edward. 2010. Strategic Management: A Stakeholder Approach. Cambridge: Cambridge University Press. [Google Scholar]

- Friedman, Milton. 1970. The Social Responsibility of Business is to Increase Profits. New York Times Magazine, September 13, 32–33. [Google Scholar]

- Ghazali, Nazli A. Mohd. 2007. Ownership structure and corporate social responsibility disclosure: Some Malaysian evidence. Corporate Governance: The International Journal of Business in Society 7: 251–66. [Google Scholar] [CrossRef]

- Goss, Allen, and Gordon S. Roberts. 2011. The impact of corporate social responsibility on the cost of bank loans. Journal of Banking & Finance 35: 1794–810. [Google Scholar]

- Greening, Daniel W., and Daniel B. Turban. 2000. Corporate Social Performance as a Competitive Advantage in Attracting a Quality Workforce. Business & Society 39: 254–80. [Google Scholar] [CrossRef]

- Hambrick, Donald C., Sydney Finkelstein, Theresa S. Cho, and Eric M. Jackson. 2004. Isomorphism in reverse: Institutional theory as an explanation for recent increases in intraindustry heterogeneity and managerial discretion. Research in Organizational Behavior 26: 307–50. [Google Scholar] [CrossRef]

- Haniffa, Rozaini Mohd, and Terence E. Cooke. 2002. Culture, corporate governance and disclosure in Malaysian corporations. Abacus 38: 317–49. [Google Scholar] [CrossRef]

- Haniffa, Roszaini Mohd, and Terence E. Cooke. 2005. The impact of culture and governance on corporate social reporting. Journal of Accounting and Public Policy 24: 391–430. [Google Scholar] [CrossRef]

- Hawley, James, and Andrew Williams. 1997. The emergence of fiduciary capitalism. Corporate Governance: An International Review 5: 206–13. [Google Scholar] [CrossRef]

- Ho, Chi-Kun. 2005. Corporate Governance and Corporate Competitiveness: An international analysis. Corporate Governance: An International Review 13: 211–53. [Google Scholar] [CrossRef]

- Ho, Simon S. M., and Kar Shun Wong. 2001. A study of the relationship between corporate governace structures and the extent of voluntary disclosure. Journal of International Accounting, Auditing & Taxation 10: 139. [Google Scholar]

- Holland, Leigh, and Yee Boon Foo. 2003. Differences in environmental reporting practices in the UK and the US: The legal and regulatory context. The British Accounting Review 35: 1–18. [Google Scholar] [CrossRef]

- Jensen, Michael C., and William H. Meckling. 1976. Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics 3: 305–60. [Google Scholar] [CrossRef]

- Jo, Hoje, and Maretno A. Harjoto. 2012. The causal effect of corporate governance on corporate social responsibility. Journal of Business Ethics 106: 53–72. [Google Scholar] [CrossRef]

- Johnson, Simon, and Todd Mitton. 2003. Cronyism and capital controls: Evidence from Malaysia. Journal of Financial Economics 67: 351–82. [Google Scholar] [CrossRef]

- Kansal, Monika, Mahesh Joshi, and Gurdip Singh Batra. 2014. Determinants of corporate social responsibility disclosures: Evidence from India. Advances in Accounting 30: 217–29. [Google Scholar] [CrossRef]

- Khan, Arifur, Mohammad Badrul Muttakin, and Javed Siddiqui. 2013. Corporate Governance and Corporate Social Responsibility Disclosures: Evidence from an Emerging Economy. Journal of Business Ethics 114: 207–23. [Google Scholar] [CrossRef]

- Klein, April. 2002. Audit committee, board of director characteristics, and earnings management. Journal of Accounting and Economics 33: 375–400. [Google Scholar] [CrossRef]

- Lee, Tanya M., and Paul D. Hutchison. 2005. The decision to disclose environmental information: A research review and agenda. Advances in Accounting 21: 83–111. [Google Scholar] [CrossRef]

- Lefort, Fernando, and Eduardo Walker. 2007. Do Markets Penalize Agency Conflicts Between Controlling and Minority Shareholders? Evidence From Chile. The Developing Economies 45: 283–314. [Google Scholar] [CrossRef]

- Li, Hongbin, Lingsheng Meng, Qian Wang, and Li-An Zhou. 2008. Political connections, financing and firm performance: Evidence from Chinese private firms. Journal of Development Economics 87: 283–99. [Google Scholar] [CrossRef]

- Li, Jing, Musa Mangena, and Richard Pike. 2012. The effect of audit committee characteristics on intellectual capital disclosure. The British Accounting Review 44: 98–110. [Google Scholar] [CrossRef] [Green Version]

- Lin, Karen Jingrong, Jinsong Tan, Liming Zhao, and Khondkar Karim. 2015. In the name of charity: Political connections and strategic corporate social responsibility in a transition economy. Journal of Corporate Finance 32: 327–46. [Google Scholar] [CrossRef]

- Lindblom, Cristi K. 1994. The implications of organizational legitimacy for corporate social performance and disclosure. Paper presented at the Critical Perspectives on Accounting Conference, New York, NY, USA. [Google Scholar]

- Lipton, Martin, and Jay W. Lorsch. 1992. A Modest Proposal for Improved Corporate Governance. The Business Lawyer 48: 59–77. [Google Scholar]

- Lorca, Carmen, Juan Pedro Sánchez-Ballesta, and Emma García-Meca. 2011. Board Effectiveness and Cost of Debt. Journal of Business Ethics 100: 613–31. [Google Scholar] [CrossRef]

- Magnanelli, Barbara Sveva, and Maria Federica Izzo. 2017. Corporate social performance and cost of debt: The relationship. Social Responsibility Journal 13: 250–65. [Google Scholar] [CrossRef]

- Malik, Mahfuja. 2015. Value-Enhancing Capabilities of CSR: A Brief Review of Contemporary Literature. Journal of Business Ethics 127: 419–38. [Google Scholar] [CrossRef]

- Marinetto, Michael. 1998. The Shareholders Strike Back: Issues in the Research of Shareholder Activism. Abingdon: Taylor & Francis. [Google Scholar]

- Mohd Ghazali, Nazli A., and Pauline Weetman. 2006. Perpetuating traditional influences: Voluntary disclosure in Malaysia following the economic crisis. Journal of International Accounting, Auditing and Taxation 15: 226–48. [Google Scholar] [CrossRef]

- Neu, Dean, Hussein Warsame, and Kathryn Pedwell. 1998. Managing public impressions: Environmental disclosures in annual reports. Accounting, Organizations and Society 23: 265–82. [Google Scholar] [CrossRef]

- Ntim, Collins G., and Teerooven Soobaroyen. 2013. Corporate governance and performance in socially responsible corporations: New empirical insights from a Neo-Institutional framework. Corporate Governance: An International Review 21: 468–94. [Google Scholar]

- Oh, Tick Hui, Shen Yee Pang, and Shing Chyi Chua. 2010. Energy policy and alternative energy in Malaysia: Issues and challenges for sustainable growth. Renewable and Sustainable Energy Reviews 14: 1241–52. [Google Scholar] [CrossRef]

- Padgett, Robert C., and Jose I. Galan. 2010. The Effect of R&D Intensity on Corporate Social Responsibility. Journal of Business Ethics 93: 407–18. [Google Scholar] [CrossRef]

- Pittman, Jeffrey A., and Steve Fortin. 2004. Auditor choice and the cost of debt capital for newly public firms. Journal of Accounting and Economics 37: 113–36. [Google Scholar] [CrossRef]

- Rajan, Raghuram G., and Luigi Zingales. 1995. What do we know about capital structure? Some evidence from international data. The journal of Finance 50: 1421–60. [Google Scholar] [CrossRef]

- Richardson, Alan J., and Michael Welker. 2001. Social disclosure, financial disclosure and the cost of equity capital. Accounting, Organizations and Society 26: 597–616. [Google Scholar] [CrossRef]

- Roberts, Peter W., and Grahame R. Dowling. 2002. Corporate reputation and sustained superior financial performance. Strategic Management Journal 23: 1077–93. [Google Scholar] [CrossRef]

- Sadou, Abdelkader, Fardous Alom, and Hayatullah Laluddin. 2017. Corporate social responsibility disclosures in Malaysia: Evidence from large companies. Social Responsibility Journal 13: 177–202. [Google Scholar] [CrossRef]

- Said, Roshima, Yuserrie Hj Zainuddin, and Hasnah Haron. 2009. The relationship between corporate social responsibility disclosure and corporate governance characteristics in Malaysian public listed companies. Social Responsibility Journal 5: 212–26. [Google Scholar] [CrossRef]

- Saleh, Mustaruddin, Norhayah Zulkifli, and Rusnah Muhamad. 2011. Looking for evidence of the relationship between corporate social responsibility and corporate financial performance in an emerging market. Asia-Pacific Journal of Business Administration 3: 165–90. [Google Scholar] [CrossRef]

- Scott, W. Richard. 2001. Institutions and Organizations. Thousand Oakes: Sage. [Google Scholar]

- Sengupta, Partha. 1998. Corporate Disclosure Quality and the Cost of Debt. The Accounting Review 73: 459–74. [Google Scholar]

- Shailer, Greg, and Kun Wang. 2015. Government ownership and the cost of debt for Chinese listed corporations. Emerging Markets Review 22: 1–17. [Google Scholar] [CrossRef]

- Singh, Ajit. 1991. United Nations Conference on Trade and Development (UNCTAD). Review of Maritime Transport 4: 1–28. [Google Scholar]

- Skeel, David A. 2001. Shaming in corporate law. University of Pennsylvania Law Review 149: 1811–68. [Google Scholar] [CrossRef]

- Smith, Malcolm, Khadijah Yahya, and Ahmad Marzuki Amiruddin. 2007. Environmental disclosure and performance reporting in Malaysia. Asian Review of Accounting 15: 185–99. [Google Scholar] [CrossRef]

- Stiglitz, Joseph E. 1993. The role of the state in financial markets. The World Bank Economic Review 7: 19–52. [Google Scholar] [CrossRef]

- Subramaniam, Ravichandran, and Mahenthiran Sakthi. 2022. Board performance and its relation to dividend payout: Evidence from Malaysia. International Journal of Managerial Finance 18: 286–316. [Google Scholar] [CrossRef]

- Subramaniam, Ravichandran K., Shyamala Dhoraisingham Samuel, and Sakthi Mahenthiran. 2016. Liquidity Implications of Corporate Social Responsibility Disclosures: Malaysian Evidence. Journal of International Accounting Research 15: 133–53. [Google Scholar] [CrossRef]

- Upadhyay, Arun, and Ram Sriram. 2011. Board size, corporate information environment and cost of capital. Journal of Business Finance & Accounting 38: 1238–61. [Google Scholar]

- Wahab, Effiezal A. Abdul, Janice C. Y. How, and Peter Verhoeven. 2007. The impact of the Malaysian code on corporate governance: Compliance, institutional investors and stock performance. Journal of Contemporary Accounting & Economics 3: 106–29. [Google Scholar]

- Wong, Woei Chyuan, Jonathan A. Batten, Shamsul Bahrain Mohamed-Arshad, Sabariah Nordin, and Azira Abdul Adzis. 2021. Does ESG certification add firm value? Finance Research Letters 39: 101593. [Google Scholar] [CrossRef]

- Ye, Kangtao, and Ran Zhang. 2011. Do Lenders Value Corporate Social Responsibility? Evidence from China. Journal of Business Ethics 104: 197. [Google Scholar] [CrossRef]

- Yermack, David. 1996. Higher market valuation of companies with a small board of directors. Journal of Financial Economics 40: 185–211. [Google Scholar] [CrossRef]

- Zulkifli, Norhayah, and Azlan Amran. 2006. Realising corporate social responsibility in Malaysia: A view from the accounting profession. The Journal of Corporate Citizenship 24: 101–14. [Google Scholar] [CrossRef]

{kind=link}

| Panel A: Data and Sample | ||||

| Selection Criteria | No. of Companies | |||

| Billion Ringgit Club (BRC) companies as of 31 March 2010 | 163 | |||

| Less: | ||||

| Banking and Financial Services | 25 | |||

| Companies ceasing to be part of the BRC due to delisting or merging | 34 | |||

| Usable sample | 104 | |||

| Panel B: Industry Distribution | ||||

| Sector | Industry Category | No. of Companies | Frequency | |

| Absolute | Relative (%) | |||

| 1 | Trading and services | 33 | 231 | 31.7 |

| 2 | Properties | 6 | 42 | 5.8 |

| 3 | Industrial Production | 24 | 168 | 23.1 |

| 4 | Plantation | 10 | 70 | 9.6 |

| 5 | Consumer Products | 14 | 98 | 13.5 |

| 6 | Technology | 5 | 35 | 4.8 |

| 7 | Construction/Infrastructure | 8 | 56 | 7.7 |

| 8 | Oil and Energy | 1 | 7 | 0.97 |

| 9 | Airline/Shipping | 1 | 7 | 0.97 |

| 10 | Retail | 2 | 14 | 1.9 |

| Total | 104 | 728 | 100 | |

| Variables | Mean | Median | Std. Dev. | Minimum | Maximum |

|---|---|---|---|---|---|

| COD_INT | 0.067 | 0.052 | 0.057 | 0.023 | 0.087 |

| CSR_INDEX | 64.371 | 55.000 | 53.191 | 32.00 | 85.750 |

| AC_IND | 0.900 | 1.000 | 0.140 | 1.000 | 1.000 |

| BO_SIZE | 8.279 | 8.000 | 1.804 | 7.000 | 9.000 |

| GOV_INST | 0.121 | 0.069 | 0.178 | 0.000 | 1.000 |

| OTH_INST | 0.114 | 0.089 | 0.112 | 0.000 | 1.000 |

| POL_CON | 0.327 | 0.000 | 0.469 | 0.000 | 1.000 |

| CSR_AWARDS | 0.209 | 0.000 | 0.411 | 0.000 | 1.000 |

| AGE_FIRM | 35.491 | 33.000 | 22.037 | 20.000 | 45.000 |

| GROWTH | 1.234 | 0.730 | 1.791 | 0.000 | 14.000 |

| ROA | 0.149 | 0.076 | 0.558 | 1.180 | 8.300 |

| LNSIZE | 14.96 | 14.70 | 1.22 | 12.550 | 18.58 |

| CRED_POWER | 1.339 | 0.854 | 2.341 | 0.040 | 27.120 |

| N | 728 | 728 | 728 |

| COD_ INT | CSR_ INDEX | CSR_ AWARD | BO_ SIZE | AC_ IND | POL_ CON | GOV_ INST | OTH_ INST | ROA | GROWTH | LNSIZE | AGE_ FIRM | CRED_ POWER | ||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| COD_INT | 1 | |||||||||||||

| CSR_INDEX | −0.133 | 1 | ||||||||||||

| CSR_AWARD | 0.007 ** | 0.071 * | 1 | |||||||||||

| BO_SIZE | −0.039 ** | 0.022 ** | 0.203 | 1 | ||||||||||

| AC_IND | 0.045 ** | −0.007 * | −0.074 * | −0.027 ** | 1 | |||||||||

| POL_CON | 0.108 | −0.071 * | 0.211 | 0.080 * | −0.074 * | 1 | ||||||||

| GOV_INST | −0.003 ** | 0.054 ** | 0.253 | 0.171 | −0.182 | 0.395 | 1 | |||||||

| OTH_INST | −0.077 * | −0.039 ** | 0.157 | 0.269 | −0.128 | 0.059 * | 0.066 * | 1 | ||||||

| ROA | 0.099 * | −0.193 | −0.013 ** | −0.007 * | −0.037 ** | −0.003 ** | −0.055 * | 0.133 | 1 | |||||

| GROWTH | −0.202 | −0.101 | 0.239 | 0.005 ** | −0.179 | 0.023 ** | −0.034 ** | 0.088 * | 0.120 | 1 | ||||

| LNSIZE | 0.204 | 0.031 ** | 0.270 | 0.240 | −0.016 ** | 0.250 | 0.317 | 0.246 | 0.008 * | −0.157 | 1 | |||

| AGE_FIRM | −0.112 | 0.160 | −0.065 * | −0.159 | −0.030 ** | −0.035 ** | −0.076 * | −0.104 * | −0.096 * | 0.040 ** | −0.082 | 1 | ||

| CRED_POWER | 0.117 | 0.007 * | 0.064 * | 0.029 ** | −0.058 * | −0.010 ** | 0.011 ** | −0.003 ** | −0.007 * | 0.002 ** | 0.070 | −0.054 ** | 1 | |

| Model 1 | Model 2 | |||

|---|---|---|---|---|

| Variable | Coefficient | t-Statistic | Coefficient | t-Statistic |

| Constant | −0.004 | −0.489 | −0.006 | −0.681 |

| CSR_INDEX | −0.001 | −3.360 *** | 0.000 | −1.566 |

| CSR_AWARDS | 0.001 | 0.910 | 0.006 | 2.772 ** |

| CSR_INDEX*CSR_AWARDS | 0.000 | −2.900 *** | ||

| BO_SIZE | −0.001 | −1.660 * | 0.000 | −1.440 |

| AC_IND | −0.001 | 0.952 | −0.001 | −0.303 |

| POL_CON | 0.003 | 2.503 ** | 0.003 | 2.689 *** |

| GOV_INST | −0.008 | −2.350 ** | −0.008 | −2.474 ** |

| OTH_INST | −0.017 | −3.407 *** | −0.016 | −3.256 *** |

| ROA | 0.003 | 2.962 ** | 0.004 | 3.225 *** |

| GROWTH | −0.002 | −5.205 *** | −0.002 | −5.589 *** |

| LNSIZE | 0.002 | 4.886 *** | 0.002 | 4.995 *** |

| AGE_FIRM | −0.001 | −2.322 ** | 0.000 | −2.138 ** |

| CRED_POWER | 0.001 | 2.885 *** | 0.000 | 2.921 *** |

| Period | Yes | Yes | ||

| Industry | Yes | Yes | ||

| R2 | 0.156 | 0.167 | ||

| Adjusted R2 | 0.135 | 0.144 | ||

| No. of observations | 728 | 728 | ||

| F-Ratio | 7.326 | 7.456 | ||

| Probability | 0.000 | 0.000 | ||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Dhoraisingam Samuel, S.; Mahenthiran, S.; Ramasamy, R. CSR Disclosures, CSR Awards and Corporate Governance as Determinants of the Cost of Debt: Evidence from Malaysia. Int. J. Financial Stud. 2022, 10, 87. https://doi.org/10.3390/ijfs10040087

Dhoraisingam Samuel S, Mahenthiran S, Ramasamy R. CSR Disclosures, CSR Awards and Corporate Governance as Determinants of the Cost of Debt: Evidence from Malaysia. International Journal of Financial Studies. 2022; 10(4):87. https://doi.org/10.3390/ijfs10040087

Chicago/Turabian StyleDhoraisingam Samuel, Shyamala, Sakthi Mahenthiran, and Ravindran Ramasamy. 2022. "CSR Disclosures, CSR Awards and Corporate Governance as Determinants of the Cost of Debt: Evidence from Malaysia" International Journal of Financial Studies 10, no. 4: 87. https://doi.org/10.3390/ijfs10040087