The Impact of Sustainability Practices on Share Performance with Mediation of Board Members Experience: A Study on Malaysian Listed Companies

Abstract

:1. Introduction

2. Literature Review

2.1. Sustainability Practices and Board Attributes

2.2. Board Members’ Attributes and the Impact on Firm Performance

2.3. Hypothesis Development

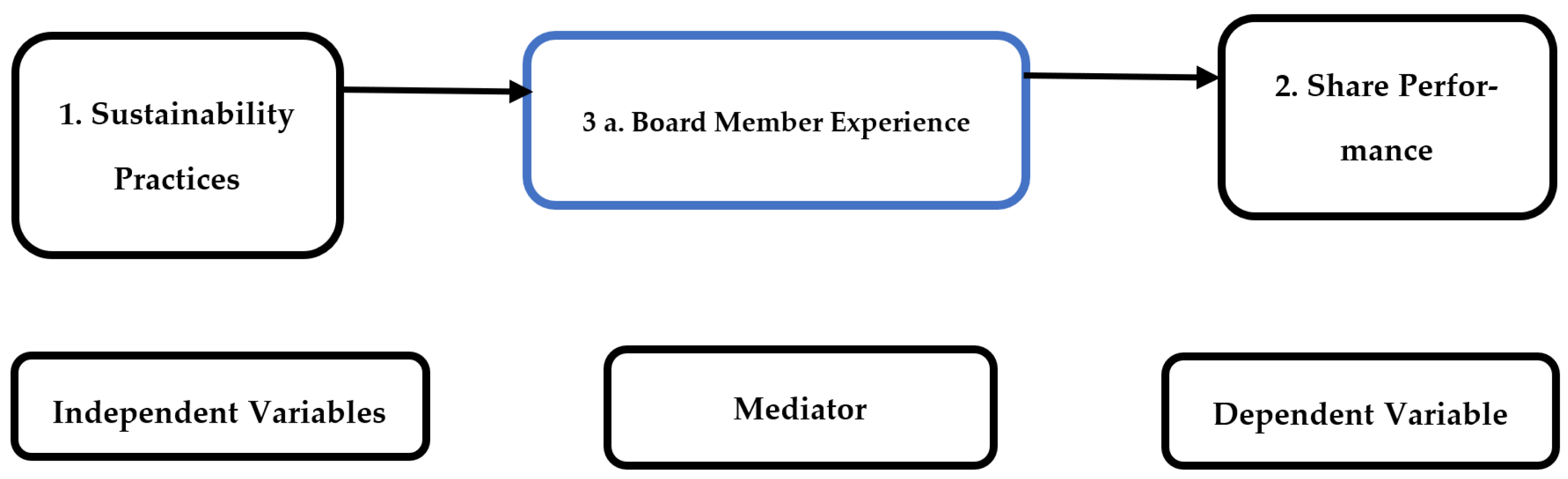

3. Methodology

3.1. Model Specification

3.2. Data Sources

4. Results and Finding

4.1. Descriptive Statistics

4.2. Autoregressive Distribution Lag (ARDL) Model

4.3. Results of Breusch–Godfrey Serial Correlation LM Test

4.4. Wald Test Bound Testing to Check the Longer-Term Association of Variables

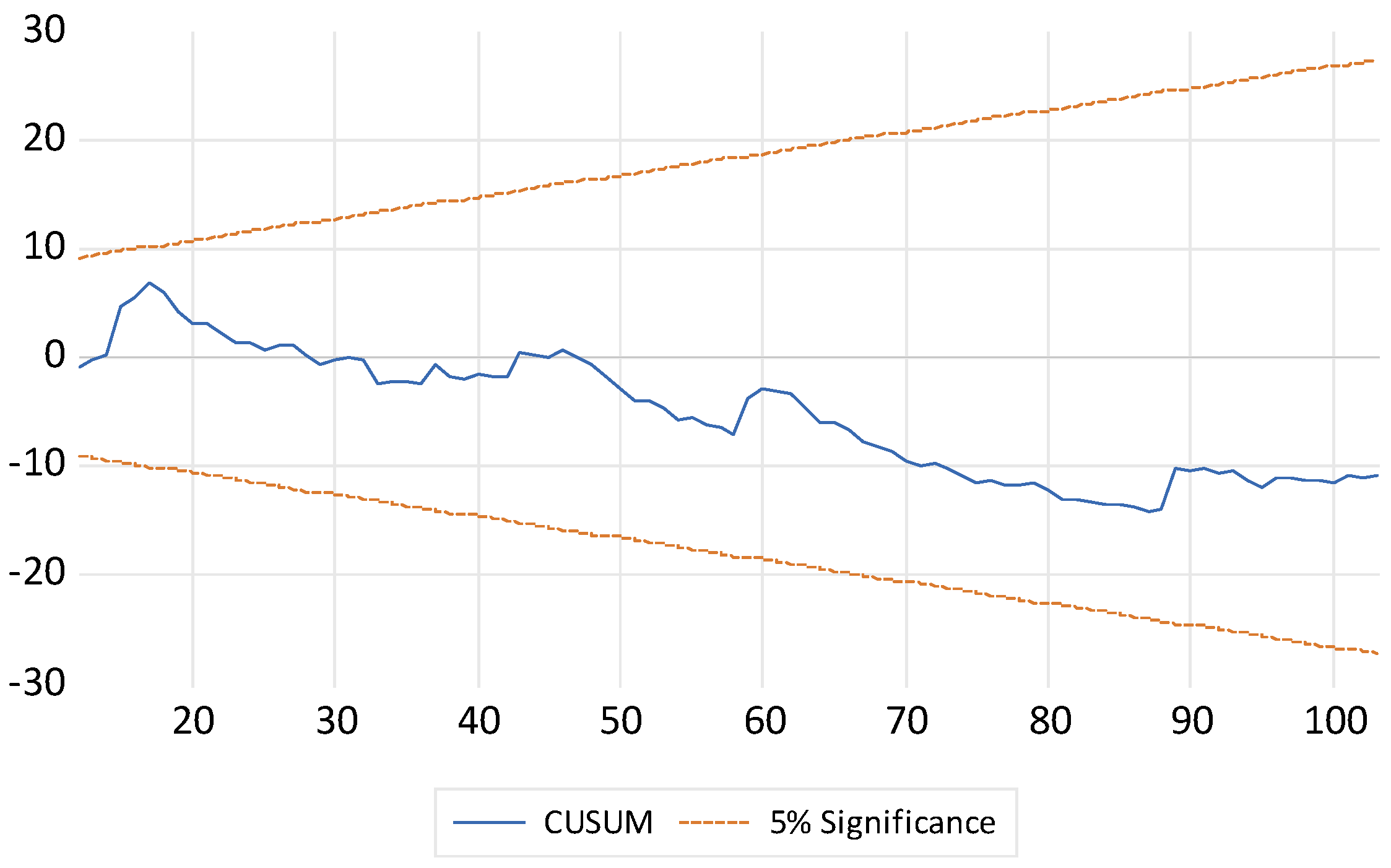

4.5. Dynamic Error Correction Model (ECM)

4.6. Testing Short Run Causality

4.6.1. Experience Short Run Causality Test on the Share Performance

4.6.2. Sustainability Short Run Causality Test on the Share Performance

4.7. Analysis and Interpretation

ARDL Optimum Lag Model

5. Discussion

6. Conclusions

Author Contributions

Funding

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Abiola, Babatunde, and Ajibola Joseph Olusegun. 2017. Appraising the Exchange Rate Volatility, Stock Market Performance and Aggregate Output Nexus in Nigeria. Business and Economics Journal 8: 1–12. [Google Scholar] [CrossRef]

- Ajide, Kazeem Bello. 2014. Quality of governance and stock market performance: The Nigerian experience. Journal of Economics and Development Studies 2: 501–22. [Google Scholar]

- Al-Saadi, Hashil. 2014. Demystifying Ontology and Epistemology in research methods. Research Gate 1: 1–10. [Google Scholar]

- Alshehhi, Ali, Haitham Nobanee, and Nilesh Khare. 2018. The impact of sustainability practices on corporate financial performance: Literature trends and future research potential. Sustainability 10: 494. [Google Scholar] [CrossRef] [Green Version]

- Anderson, David R., Dennis J. Sweeney, Thomas A. Williams, Jeffrey D. Camm, and James J. Cochran. 2015. Quantitative Methods for Business. Boston: Cengage Learning. [Google Scholar]

- Annunziata, Eleonora, Tommaso Pucci, Marco Frey, and Lorenzo Zanni. 2018. The role of organizational capabilities in attaining corporate sustainability practices and economic performance: Evidence from Italian wine industry. Journal of Cleaner Production 171: 1300–11. [Google Scholar] [CrossRef]

- Arora, Akshita. 2022. Gender diversity in boardroom and its impact on firm performance. Journal of Management and Governance 26: 735–55. [Google Scholar] [CrossRef]

- Augustine, Ele Augustine, B. J. Inyang, O. E. Ekpe, Okongo Nsor John, Eja Basil Richard, and Ewah Sunday Felix. 2021. Organizational Development: An Intervention Strategy for Effective Corporate Performance in Nigeria. Development 4: 9–25. [Google Scholar]

- Awaysheh, Amrou, Randall A. Heron, Tod Perry, and Jared I. Wilson. 2020. On the relation between corporate social responsibility and financial performance. Strategic Management Journal 41: 965–87. [Google Scholar] [CrossRef]

- Bakar, Aishah Ghazali, and Maslina Ahmad. 2019. Sustainability reporting and board diversity in Malaysia. International Journal of Academic Research in Business and Social Sciences 9: 91–99. [Google Scholar] [CrossRef]

- Beji, Rania, Ouidad Yousfi, Nadia Loukil, and Abdelwahed Omri. 2021. Board diversity and corporate social responsibility: Empirical evidence from France. Journal of Business Ethics 173: 133–55. [Google Scholar] [CrossRef]

- Bhala, Neeraj, Gwenetta Curry, Adrian R. Martineau, Charles Agyemang, and Raj Bhopal. 2020. Sharpening the global focus on ethnicity and race in the time of COVID-19. The Lancet 395: 1673–76. [Google Scholar] [CrossRef]

- Bhatti, Uzair, and Noralfishah Sulaiman. 2020. Impact of sustainability practices on share performance with mediation of green innovation: A conceptual paper. International Journal of Psychosocial Rehabilitation 24: 1826–36. [Google Scholar] [CrossRef]

- Bhatti, Uzair, and Noralfishah Sulaiman. 2021. The Relationship of Sustainability Reporting and Share Prices with a Mediation of Green Invention: A Conceptual Review Paper. Studies of Applied Economics 39: 25. [Google Scholar] [CrossRef]

- Boffo, Riccardo, and Robert Patalano. 2020. ESG Investing: Practices, Progress and Challenges. Paris: OCDE. [Google Scholar]

- Chong, Lee-Lee, Hway-Boon Ong, and Siow-Hooi Tan. 2018. Corporate risk-taking and performance in Malaysia: The effect of board composition, political connections and sustainability practices. Corporate Governance: The International Journal of Business in Society 18: 635–54. [Google Scholar] [CrossRef]

- Cooper, Donald, and Pamela Schindler. 2013. Business Research Methods, 12th ed. New York: McGraw-Hill Higher Education. [Google Scholar]

- Crane, Andrew, Dirk Matten, Sarah Glozer, and Laura Spence. 2019. Business Ethics: Managing Corporate Citizenship and Sustainability in the Age of Globalization. New York: Oxford University Press. [Google Scholar]

- Cucari, Nicola, Salvatore Esposito de Falco, and Beatrice Orlando. 2018. Diversity of board of directors and environmental social governance: Evidence from Italian listed companies. Corporate Social Responsibility and Environmental Management 25: 250–66. [Google Scholar] [CrossRef]

- Dang, Van Cuong, and Quang Khai Nguyen. 2021. Internal corporate governance and stock price crash risk: Evidence from Vietnam. Journal of Sustainable Finance & Investment, 1–18. [Google Scholar] [CrossRef]

- Daugaard, Dan. 2020. Emerging new themes in environmental, social and governance investing: A systematic literature review. Accounting & Finance 60: 1501–30. [Google Scholar]

- Dembo, Abubakar M. 2017. The impact of sustainability practices on the financial performance: Evidence from listed oil and gas companies in Nigeria. In Dimensional Corporate Governance. Cham: Springer, pp. 215–33. [Google Scholar]

- Dyduch, Justyna, and Joanna Krasodomska. 2017. Determinants of corporate social responsibility disclosure: An empirical study of Polish listed companies. Sustainability 9: 1934. [Google Scholar] [CrossRef] [Green Version]

- Fisch, Jill E. 2018. Making sustainability disclosure sustainable. The Georgetown Law Journal 107: 923. [Google Scholar]

- Font, Xavier, and Jennifer Lynes. 2018. Corporate Social Responsibility in Tourism and Hospitality. Boca Raton: Taylor & Francis, vol. 26, pp. 1027–42. [Google Scholar]

- Galletta, Simona, Sebastiano Mazzù, Valeria Naciti, and Carlo Vermiglio. 2022. Gender diversity and sustainability performance in the banking industry. Corporate Social Responsibility and Environmental Management 29: 161–74. [Google Scholar] [CrossRef]

- Galli, Brian J. 2021. Economic Decision-Making and Risk Management: A Relation From the Banking Perspective. International Journal of System Dynamics Applications (IJSDA) 10: 1–25. [Google Scholar] [CrossRef]

- Garratt, Anthony, Kevin Lee, M. Hashem Pesaran, and Yongcheol Shin. 2012. Global and National Macroeconometric Modelling: A Long-Run Structural Approach. New York: Oxford University Press. [Google Scholar]

- Gerrard, William, and Leslie Godfrey. 1998. Diagnostic Checks for Single-equation Error-correction and Autoregressive Distributed Lag Models. The Manchester School 66: 222–37. [Google Scholar] [CrossRef]

- Gujarati, Damodar N. 2009. Basic econometrics. Noida: Tata McGraw-Hill Education. [Google Scholar]

- Hassan, Hisham Mohamed. 2009. Causal Relations Growth, Inequality and Poverty in Sudan. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=1414147 (accessed on 15 June 2021).

- Hastalona, Dina, and Isfenti Sadalia. 2021. Literature Review ESG and Sustainability Finance. Budapest International Research and Critics Institute (BIRCI-Journal): Humanities and Social Sciences 4: 3548–57. [Google Scholar]

- Hong, Bryan, Zhichuan Li, and Dylan Minor. 2016. Corporate governance and executive compensation for corporate social responsibility. Journal of Business Ethics 136: 199–213. [Google Scholar] [CrossRef] [Green Version]

- Ichsani, Sakina, and Agatha Rinta Suhardi. 2015. The effect of return on equity (ROE) and return on investment (ROI) on trading volume. Procedia-Social and Behavioral Sciences 211: 896–902. [Google Scholar] [CrossRef] [Green Version]

- Jaturat, Malee, Kusuma Dampitakse, and Chanongkorn Kuntonbutr. 2021. The Effect of Corporate Governance on the Board of Directors’ Characteristics and Sustainability Disclosure: An Empirical Study from Thailand. The Journal of Asian Finance, Economics and Business 8: 191–201. [Google Scholar]

- Kamaludin, Kamilah, Izani Ibrahim, Sheela Sundarasen, and Ova Faizal. 2022. ESG in the boardroom: Evidence from the Malaysian market. International Journal of Corporate Social Responsibility 7: 1–15. [Google Scholar] [CrossRef]

- Keesstra, Saskia, Gerben Mol, Jan De Leeuw, Joop Okx, Margot De Cleen, and Saskia Visser. 2018. Soil-related sustainable development goals: Four concepts to make land degradation neutrality and restoration work. Land 7: 133. [Google Scholar] [CrossRef] [Green Version]

- Keskin, Ayşe İrem, Banu Dincer, and Caner Dincer. 2020. Exploring the impact of sustainability on corporate financial performance using discriminant analysis. Sustainability 12: 2346. [Google Scholar] [CrossRef] [Green Version]

- Klakegg, Ole Jonny. 2016. Ontology and epistemology. In Designs, Methods and Practices for Research of Project Management. London: Routledge, pp. 87–96. [Google Scholar]

- Laskar, Najul, and Santi Gopal Maji. 2017. Corporate sustainability reporting practices in India: Myth or reality? Social Responsibility Journal 12: 625–41. [Google Scholar] [CrossRef]

- Loderer, Claudio, René Stulz, and Urs Waelchli. 2017. Firm rigidities and the decline in growth opportunities. Management Science 63: 3000–20. [Google Scholar] [CrossRef] [Green Version]

- Ma, Wanglin, Hongyun Zheng, Yueji Zhu, and Jianling Qi. 2021. Effects of cooperative membership on financial performance of banana farmers in China: A heterogeneous analysis. Annals of Public and Cooperative Economics 93: 5–27. [Google Scholar] [CrossRef]

- Malaysia, Bursa. 2022. Bursa Malaysia Retrieved March 2021, 2017–2021. Available online: https://www.bursamalaysia.com/trade/trading_resources/listing_directory/main_market (accessed on 5 October 2019).

- Marn, Joel Tham Kah, and Dondjio Fomedjou Romuald. 2012. The impact of corporate governance mechanism and corporate performance: A study of listed companies in Malaysia. Journal for the Advancement of Science & Arts 3: 31–45. [Google Scholar]

- Masud, Md, Abdul Kaium, Seong Mi Bae, Javier Manzanares, and Jong Dae Kim. 2019. Board directors’ expertise and corporate corruption disclosure: The moderating role of political connections. Sustainability 11: 4491. [Google Scholar] [CrossRef] [Green Version]

- Merendino, Alessandro, Sally Dibb, Maureen Meadows, Lee Quinn, David Wilson, Lyndon Simkin, and Ana Canhoto. 2018. Big data, big decisions: The impact of big data on board level decision-making. Journal of Business Research 93: 67–78. [Google Scholar] [CrossRef] [Green Version]

- Naciti, Valeria. 2019. Corporate governance and board of directors: The effect of a board composition on firm sustainability performance. Journal of Cleaner Production 237: 117727. [Google Scholar] [CrossRef]

- Nguyen, Ninh, and Lester W. Johnson. 2020. Consumer behaviour and environmental sustainability. Journal of Consumer Behaviour 19: 539–41. [Google Scholar] [CrossRef]

- Nguyen, Quang Khai. 2022. Determinants of bank risk governance structure: A cross-country analysis. Research in International Business and Finance 60: 101575. [Google Scholar] [CrossRef]

- O’Dwyer, Brendan, and Jeffrey Unerman. 2020. Shifting the focus of sustainability accounting from impacts to risks and dependencies: Researching the transformative potential of TCFD reporting. Accounting, Auditing & Accountability Journal 33: 1131–41. [Google Scholar]

- Ojeka, Stephen, Alex Adegboye, Kofo Adegboye, Olaoluwa Umukoro, Olajide Dahunsi, and Emmanuel Ozordi. 2019. Corruption perception, institutional quality and performance of listed companies in Nigeria. Heliyon 5: e02569. [Google Scholar] [CrossRef]

- Oncioiu, Ionica, Anca-Gabriela Petrescu, Florentina-Raluca Bîlcan, Marius Petrescu, Delia-Mioara Popescu, and Elena Anghel. 2020. Corporate Sustainability Reporting and Financial Performance. Sustainability 12: 4297. [Google Scholar] [CrossRef]

- Oziegbe, David Jerry, and Okenwa Ogbodo Cy. 2021. Board attributes and firm performance of Nigerian quoted banks with international authorization. International Journal of Economics, Business and Management Research 5: 302–17. [Google Scholar]

- Pajunen, Nani, Gary Watkins, Maaria Wierink, and Kari Heiskanen. 2012. Drivers and barriers of effective industrial material use. Minerals Engineering 29: 39–46. [Google Scholar] [CrossRef]

- Pesaran, M. Hashem, Yongcheol Shin, and Richard J. Smith. 2001. Bounds testing approaches to the analysis of level relationships. Journal of Applied Econometrics 16: 289–326. [Google Scholar] [CrossRef]

- Pfeffer, Jeffrey. 1972. Size and composition of corporate boards of directors: The organization and its environment. Administrative Science Quarterly 17: 218–28. [Google Scholar] [CrossRef]

- Pfeffer, Jeffrey, and G. R. Salancik. 1978. A resource dependence perspective. In Intercorporate Relations. The Structural Analysis of Business. Cambridge: University Press Cambridge. [Google Scholar]

- Pfeffer, Jeffrey, and Gerald Salancik. 2015. External Control of Organizations—Resource Dependence Perspective. In Organizational Behavior 2. London: Routledge, pp. 373–88. [Google Scholar]

- Praveen, Goyal, Rahman Zillur, and A. A. Kazmi. 2013. Corporate sustainability performance and firm performance research: Literature review and future research agenda. Management Decision 51: 361–79. [Google Scholar]

- Pugna, Irina Bogdana, Adriana Duțescu, and Oana Georgiana Stănilă. 2019. Corporate attitudes towards big data and its impact on performance management: A qualitative study. Sustainability 11: 684. [Google Scholar] [CrossRef] [Green Version]

- Rahman, Haseeb Ur, Muhammad Zahid, and Musa Khan. 2022. Corporate sustainability practices: A new perspective of linking board with firm performance. Total Quality Management & Business Excellence 33: 929–46. [Google Scholar]

- Rao, Kathyayini, and Carol Tilt. 2016. Board composition and corporate social responsibility: The role of diversity, gender, strategy and decision making. Journal of Business Ethics 138: 327–47. [Google Scholar] [CrossRef]

- Ryan, Gemma. 2018. Introduction to positivism, interpretivism and critical theory. Nurse Researcher 25: 41–49. [Google Scholar] [CrossRef] [Green Version]

- Saggar, Ridhima, Nischay Arora, and Balwinder Singh. 2021. Gender diversity in corporate boardrooms and risk disclosure: Indian evidence. Gender in Management: An International Journal 37: 182–201. [Google Scholar] [CrossRef]

- Samontaray, Durga Prasad. 2010. Impact of corporate governance on the stock prices of the nifty 50 broad index listed companies. International Research Journal of Finance and Economics 41: 7–18. [Google Scholar]

- Schmitt, Eugenia. 2017. Effective risk culture in banks: Responsibilities and boundaries of the risk management. In European Financial Systems 2017, Proceedings of the 14th International Scientific Conference. Brno: Masaryk University, p. 239. [Google Scholar]

- Shen, Wei, Yuliya Ponomareva, and Timur Uman. 2022. Can you catch two birds with one stone? The impacts of nominating committee composition on board monitoring and resource provision. Long Range Planning 55: 102127. [Google Scholar] [CrossRef]

- Sumner, Jennifer. 2017. Sustainability and the Civil Commons. Toronto: University of Toronto Press. [Google Scholar]

- Tejerina-Gaite, Fernando A., and Miguel A. Fernández-Temprano. 2020. The influence of board experience on firm performance: Does the director’s role matter? Journal of Management and Governance 25: 685–705. [Google Scholar] [CrossRef]

- Tran, Ben. 2019. Corporate social responsibility. In Advanced Methodologies and Technologies in Business Operations and Management. Hershey: IGI Global, pp. 270–81. [Google Scholar]

- Unruh, Gregory, David Kiron, Nina Kruschwitz, Martin Reeves, Holger Rubel, and Alexander Meyer Zum Felde. 2016. Investing for a sustainable future: Investors care more about sustainability than many executives believe (No. 1532-9194). MIT Sloan Management Review 57: 1–32. [Google Scholar]

- van Schaaijk, Art, Adnan Noor Baloch, Sara Thomée, Monique Frings-Dresen, Mats Hagberg, and Karen Nieuwenhuijsen. 2020. Mediating factors for the relationship between stress and work ability over time in young adults. International Journal of Environmental Research and Public Health 17: 2530. [Google Scholar] [CrossRef] [Green Version]

- Whitler, Kimberly A., Ryan Krause, and Donald R. Lehmann. 2018. When and how board members with marketing experience facilitate firm growth. Journal of Marketing 82: 86–105. [Google Scholar] [CrossRef]

- Yong, Jing Yi, Mohd-Yusoff Yusliza, Thurasamy Ramayah, Charbel Jose Chiappetta Jabbour, Simone Sehnem, and Venkatesh Mani. 2020. Pathways towards sustainability in manufacturing organizations: Empirical evidence on the role of green human resource management. Business Strategy and the Environment 29: 212–28. [Google Scholar] [CrossRef]

- Zaragoza-Sáez, Patrocinio, Enrique Claver-Cortés, Bartolomé Marco-Lajara, and Mercedes Úbeda-García. 2016. Influence of intellectual capital upon knowledge creation in Spanish subsidiaries: An empirical study. Knowledge Management Research & Practice 14: 489–501. [Google Scholar]

- Żelazna, Anna, Matylda Bojar, and Ewa Bojar. 2020. Corporate Social Responsibility towards the Environment in Lublin Region, Poland: A comparative study of 2009 and 2019. Sustainability 12: 4463. [Google Scholar] [CrossRef]

- Zorio-Grima, Ana, Laura Sierra-García, and Maria A Garcia-Benau. 2017. Sustainability reporting experience by universities: A causal configuration approach. International Journal of Sustainability in Higher Education 19: 337–52. [Google Scholar] [CrossRef]

- Zraqat, Omar. 2019. Sustainability practices disclosure and value relevance: Evidence from Jordan. Modern Applied Science 13: 75–86. [Google Scholar]

{kind=link}

{kind=link}

| Sustainability 2017 | Sustainability 2018 | Sustainability 2019 | Sustainability 2020 | Share Performance 2017 | Share Performance 2018 | Share Performance 2019 | Share Performance 2020 | Experience | Education | |

|---|---|---|---|---|---|---|---|---|---|---|

| Mean | 89.8 | 90.3 | 91.4 | 89.4 | 2.8 | 3.4 | 3.8 | 2.5 | 56.6 | 2.5 |

| Median | 94.5 | 95.0 | 96.0 | 94.0 | 1.5 | 1.9 | 2.5 | 1.2 | 57.0 | 2.0 |

| Maximum | 99.3 | 99.5 | 100.0 | 99.0 | 33.9 | 34.5 | 35.6 | 33.3 | 83.0 | 5.0 |

| Minimum | 0.3 | 1.5 | 3.8 | 1.0 | 0.1 | 0.2 | 0.3 | 0.0 | 32.0 | 1.0 |

| Std. Dev. | 20.4 | 20.3 | 20.0 | 20.2 | 4.7 | 4.9 | 5.2 | 4.6 | 11.2 | 1.5 |

| Probability | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.4 | 0.0 |

| Sum | 9253.4 | 9305.0 | 9409.2 | 9208.5 | 289.4 | 345.5 | 389.8 | 260.4 | 5832.0 | 258.0 |

| Obs | 103.0 | 103.0 | 103.0 | 103.0 | 103.0 | 103.0 | 103.0 | 103.0 | 103.0 | 103.0 |

| ARDL Lag Selection | ||||||||

|---|---|---|---|---|---|---|---|---|

| Year | Lag 4 | Lag 3 | Lag 2 | Lag 1 | ||||

| AIC | SIC | AIC | SIC | AIC | SIC | AIC | SIC | |

| 2017 | −6.08 | −6.64 | −6.14 * | −6.69 * | −6.07 | −6.41 | −5.99 | −6.23 |

| 2018 | −6.45 * | −7.06 * | −6.37 | −6.85 | −6.26 | −6.62 | −6.29 | 6.54 |

| 2019 | −6.25 * | −6.82 * | −6.23 | −6.71 | −6.19 | −6.53 | −6.12 | −6.35 |

| 2020 | −6.19 * | −6.76 * | −6.17 | −6.62 | −6.16 | −6.5 | −6.1 | −6.36 |

| Breusch–Godfrey Serial Correlation LM Test: | |||

|---|---|---|---|

| Null Hypothesis: No Serial Correlation at up to 3 Lags | |||

| Fstatistic | 0.917249 | Prob. F(3,77) | 0.06436 |

| Obs*R-squared | 3.346878 | Prob. Chi-Square(3) | 0.06343 |

| Pesaran et al. (2001) | Hassan (2009) | |||

|---|---|---|---|---|

| Critical Value | Lower Bound Value | Upper Bound Value | Lower Bound Value | Upper Bound Value |

| 1% | 3.74 | 5.06 | 4.59 | 6.37 |

| 5% | 2.86 | 4.01 | 3.28 | 4.63 |

| 10% | 2.45 | 3.52 | 2.70 | 3.90 |

| Coefficient Bound Testing Wald Test (2017–2020) | |||

|---|---|---|---|

| Year | F Statistics | Bound Testing | Remark |

| 2017 | 23.41 | >4.01 | Long-term association |

| 2018 | 20.48 | >4.01 | Long-term association |

| 2019 | 5 | >4.01 | Long-term association |

| 2020 | 4.89 | >4.01 | Long-term association |

| Year | ECT (−1) | p Value | Serial Correlation (p Value) | Remarks |

|---|---|---|---|---|

| 2017 | −0.934889 | 0.0000 | 0.2671 | Negative, Significant, No Serial Correl |

| 2018 | −0.93714 | 0.0000 | 0.2351 | Negative, Significant, No Serial Correl |

| 2019 | −0.941358 | 0.0000 | 0.1576 | Negative, Significant, No Serial Correl |

| 2020 | −0.90208 | 0.0000 | 0.1636 | Negative, Significant, No Serial Correl |

| Year | Probability Value | Null Hypothesis | Optimum Lags | Remarks (5% Significance Level) |

|---|---|---|---|---|

| 2017 | 23.57% | C(7) = C(8) = C(9) = 0 | 3 | Null hypothesis accepted (No short run causality) |

| 2018 | 18.82% | C(9) = C(10) = C(11) = C(12) = 0 | 4 | Null hypothesis accepted (No short run causality) |

| 2019 | 29.87% | C(9) = C(10) = C(11) = C(12) = 0 | 4 | Null hypothesis accepted (No short run causality) |

| 2020 | 21.31% | C(9) = C(10) = C(11) = C(12) = 0 | 4 | Null hypothesis accepted (No short run causality) |

| Year | Probability Value | Null Hypothesis | Optimum Lags | Remarks (5% Significance Level) |

|---|---|---|---|---|

| 2017 | 10.30% | C(10) = C(11) = C(12) = 0 | 3 | Null hypothesis accepted (No short run causality) |

| 2018 | 13.78% | C(13) = C(14) = C(15) = C(16) = 0 | 4 | Null hypothesis accepted (No short run causality) |

| 2019 | 26.39% | C(13) = C(14) = C(15) = C(16) = 0 | 4 | Null hypothesis accepted (No short run causality) |

| 2020 | 14.83% | C(13) = C(14) = C(15) = C(16) = 0 | 4 | Null hypothesis accepted (No short run causality) |

| Year | Optimum Lag | ECT (−1) | Coefficient of Bound Testing > 4.01 | Sustainability (ESG)-Short Run Causality (5% Sig Level) | Experience-Short Run Causality | Adjusted R Square | Durbin Watson | Prob F Stat |

|---|---|---|---|---|---|---|---|---|

| 2017 | 3 | −0.93 | 23.41 | 10.30% | 24% | 42.26% | 2.923 | 0.000 |

| 2018 | 4 | −0.94 | 20.48 | 13.78% | 19% | 50.50% | 2.199 | 0.000 |

| 2019 | 4 | −0.94 | 5 | 26.39% | 30% | 50.23% | 2.141 | 0.000 |

| 2020 | 4 | −0.90 | 4.89 | 14.83% | 21% | 56.76% | 2.389 | 0.000 |

| Year | Items | Coefficient | T Statistics | Prob | Results |

|---|---|---|---|---|---|

| 2017 | Experience | −0.03 | 2.65 | 4.6% | Significant |

| Sustainability | 0.01 | 2.38 | 3.4% | Significant | |

| 2018 | Experience | −0.03 | 2.62 | 4.4% | Significant |

| Sustainability | 0.03 | −2.24 | 3.2% | Significant | |

| 2019 | Experience | −0.02 | 0.56 | 3.8% | Significant |

| Sustainability | −0.05 | −2.23 | 2.8% | Significant | |

| 2020 | Experience | 0.08 | −2.87 | 2.8% | Significant |

| Sustainability | 0.00 | 2.19 | 3.4% | Significant |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Bhatti, U.; Sulaiman, N. The Impact of Sustainability Practices on Share Performance with Mediation of Board Members Experience: A Study on Malaysian Listed Companies. Int. J. Financial Stud. 2023, 11, 4. https://doi.org/10.3390/ijfs11010004

Bhatti U, Sulaiman N. The Impact of Sustainability Practices on Share Performance with Mediation of Board Members Experience: A Study on Malaysian Listed Companies. International Journal of Financial Studies. 2023; 11(1):4. https://doi.org/10.3390/ijfs11010004

Chicago/Turabian StyleBhatti, Uzair, and Noralfishah Sulaiman. 2023. "The Impact of Sustainability Practices on Share Performance with Mediation of Board Members Experience: A Study on Malaysian Listed Companies" International Journal of Financial Studies 11, no. 1: 4. https://doi.org/10.3390/ijfs11010004