Corporate Social Responsibility Risk and Firm Performance: A Network Perspective

Abstract

:1. Introduction

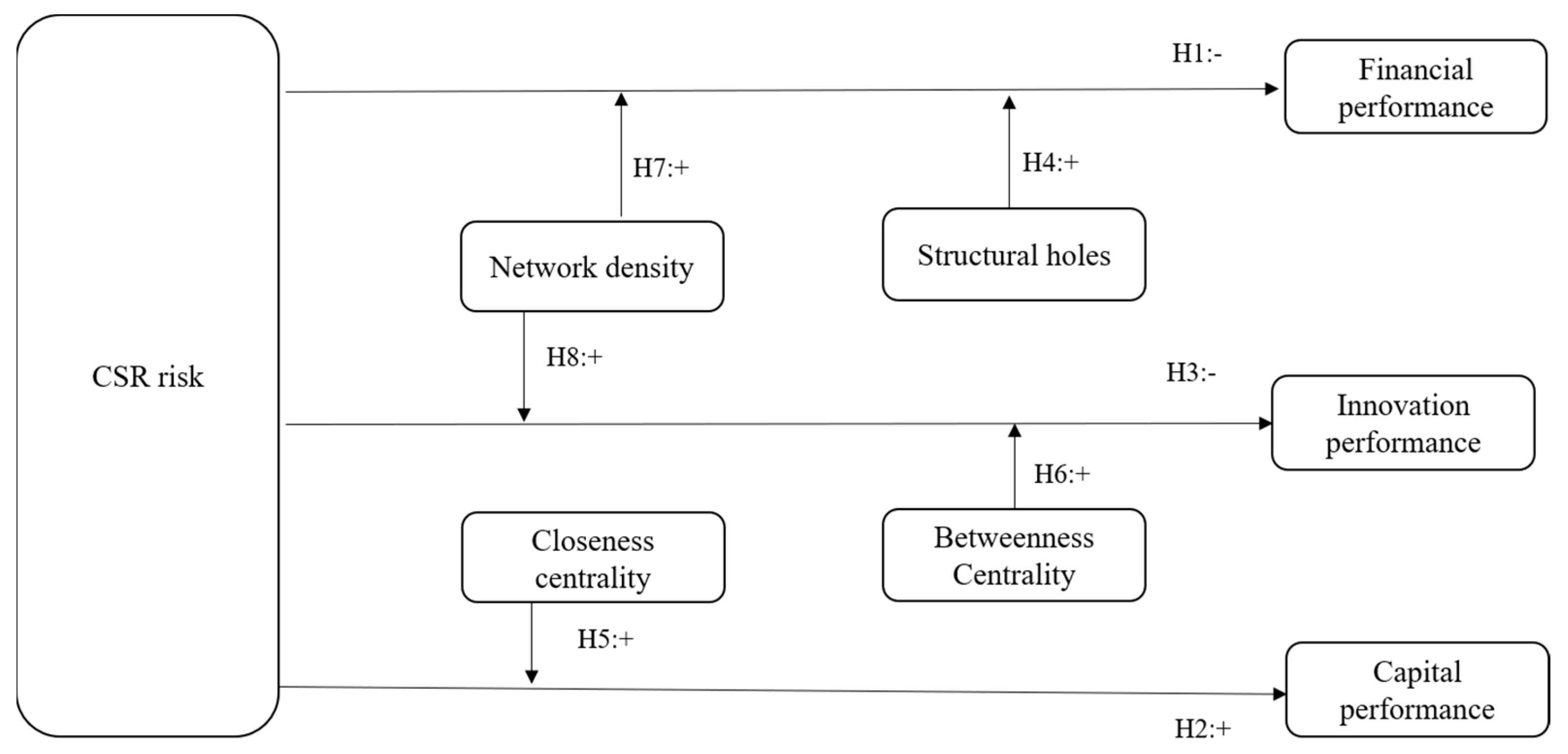

2. Theoretical Background and Hypotheses Development

2.1. CSR Risk and Firm Performance

2.2. The Moderating Role of Social Networks

3. Empirical Design

3.1. Data and Sample

3.2. Measurement

3.2.1. Dependent Variables

3.2.2. Independent Variables

3.2.3. Moderator Variables

3.2.4. Control Variables

3.3. Empirical Models

4. Results

4.1. Preliminary Analysis

4.2. Hypothesis Testing

4.2.1. CSR Risk, Social Networks, and Financial Performance

4.2.2. CSR Risk, Social Networks, and Capital Performance

4.2.3. CSR Risk, Social Networks, and Innovation Performance

4.3. Robustness Checks

5. Discussions

5.1. Theoretical Contributions

5.2. Managerial Implications

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Afuah, Allan. 2013. Are Network Effects Really All about Size? The Role of Structure and Conduct. Strategic Management Journal 34: 257–73. [Google Scholar] [CrossRef] [Green Version]

- Ahuja, Gautam, and Riitta Katila. 2001. Technological Acquisitions and the Innovation Performance of Acquiring Firms: A Longitudinal Study. Strategic Management Journal 22: 197–220. [Google Scholar] [CrossRef]

- Bagul, Avinash, and Indrajit Mukherjee. 2018. An Insight into Centralised Sourcing Strategy for Enhancing Performance and Sustainability of Multi-Tier Supply Network. International Journal of Intelligent Enterprise 5: 18–49. [Google Scholar] [CrossRef]

- Becchetti, Leonardo, Ciciretti Rocco, and Dalò Ambrogio. 2018. Fishing the Corporate Social Responsibility Risk Factors. Journal of Financial Stability 37: 25–48. [Google Scholar] [CrossRef]

- Becchetti, Leonardo, Rocco Ciciretti, Iftekhar Hasan, and Nada Kobeissi. 2012. Corporate Social Responsibility and Shareholder’s Value. Journal of Business Research 65: 1628–35. [Google Scholar] [CrossRef]

- Blowfield, Michael, and Jedrzej George Frynas. 2005. Editorial Setting New Agendas: Critical Perspectives on Corporate Social Responsibility in the Developing World. International Affairs 81: 499–513. [Google Scholar] [CrossRef]

- Boubaker, Sabri, Alexis Cellier, Riadh Manita, and Asif Saeed. 2020. Does Corporate Social Responsibility Reduce Financial Distress Risk? Economic Modelling 91: 835–51. [Google Scholar] [CrossRef]

- Boubaker, Sabri, Zhenya Liu, and Yaosong Zhan. 2022. Customer Relationships, Corporate Social Responsibility, and Stock Price Reaction: Lessons from China During Health Crisis Times. Finance Research Letters, 102699. [Google Scholar] [CrossRef]

- Boukattaya, Sonia, and Omri Abdelwahed. 2021. Corporate Social Practices and Firm Financial Performance: Empirical Evidence from France. International Journal of Financial Studies 9: 54. [Google Scholar] [CrossRef]

- Burt, Ronald S. 1992. Structural Holes: The Social Structure of Competition. Cambridge: Harvard University Press. [Google Scholar]

- Chen, Yunsen. 2014. Directors’ Social Networks and Firm Efficiency: A Structural Embeddedness Perspective. China Journal of Accounting Studies 2: 53–73. [Google Scholar] [CrossRef]

- Chen, Yunsen. 2015. Social Network and Trade Credit: Evidence Based on Structural Holes. China Accounting and Finance Review 17: 1–71. [Google Scholar]

- Cheng, Beiting, Ioannis Ioannou, and George Serafeim. 2014. Corporate Social Responsibility and Access to Finance. Strategic Management Journal 35: 1–23. [Google Scholar] [CrossRef]

- Choi, Jaepil, and Heli Wang. 2009. Stakeholder Relations and the Persistence of Corporate Financial Performance. Strategic Management Journal 30: 895–907. [Google Scholar] [CrossRef]

- El Ghoul, Sadok, Omrane Guedhami, Chuck C. Y. Kwok, and Dev R. Mishra. 2011. Does Corporate Social Responsibility Affect the Cost of Capital? Journal of Banking & Finance 35: 2388–406. [Google Scholar]

- Fatemi, Ali, Martin Glaum, and Stefanie Kaiser. 2018. ESG Performance and Firm Value: The Moderating Role of Disclosure. Global Finance Journal 38: 45–64. [Google Scholar] [CrossRef]

- Folkes, Valerie S, and Michael A. Kamins. 1999. Effects of Information About Firms’ Ethical and Unethical Actions on Consumers’ Attitudes. Journal of Consumer Psychology 8: 243–59. [Google Scholar] [CrossRef]

- Freeman, Linton C. 1978. Centrality in Social Networks Conceptual Clarification. Social Networks 1: 215–39. [Google Scholar] [CrossRef] [Green Version]

- Granovetter, Mark. 1985. Economic Action and Social Structure: The Problem of Embeddedness. American Journal of Sociology 91: 481–510. [Google Scholar] [CrossRef]

- Gregory-Smith, Ian, Brian G. M. Main, and Charles A. O’Reilly III. 2014. Appointments, Pay and Performance in Uk Boardrooms by Gender. Economic Journal 124: F109–F128. [Google Scholar] [CrossRef] [Green Version]

- Groening, Christopher, and Vamsi Krishna Kanuri. 2013. Investor Reaction to Positive and Negative Corporate Social Events. Journal of Business Research 66: 1852–60. [Google Scholar] [CrossRef]

- Hasan, Mostafa Monzur, and Ahsan Habib. 2017. Corporate Life Cycle, Organizational Financial Resources and Corporate Social Responsibility. Journal of Contemporary Accounting & Economics 13: 20–36. [Google Scholar]

- Hill, Charles W. L., and Thomas M. Jones. 1992. Stakeholder-Agency Theory. Journal of Management Studies 29: 131–54. [Google Scholar] [CrossRef]

- Hong, Harrison, and Marcin Kacperczyk. 2009. The Price of Sin: The Effects of Social Norms on Markets. Journal of Financial Economics 93: 15–36. [Google Scholar] [CrossRef]

- Huang, Jiawen. 2019. Is Social Network of Enterprise Always Useful: A Literature Review. Science Research Management 40: 57–64. (In Chinese). [Google Scholar]

- Hunjra, Ahmed Imran, Sabri Boubaker, Murugesh Arunachalam, and Asad Mehmood. 2021. How Does CSR Mediate the Relationship between Culture, Religiosity and Firm Performance? Finance Research Letters 39: 101587. [Google Scholar] [CrossRef]

- Jackson, Matthew O. 2010. Social and Economic Networks. Princeton: Princeton University Press. [Google Scholar]

- Jo, Hoje, and Haejung Na. 2012. Does Csr Reduce Firm Risk? Evidence from Controversial Industry Sectors. Journal of Business Ethics 110: 441–56. [Google Scholar] [CrossRef]

- Kanouse, David E., and Reid L. Hanson Jr. 1987. Negativity in Evaluations. In Attribution: Perceiving the Causes of Behavior. Mahwah: Lawrence Erlbaum Associates, Inc., pp. 47–62. [Google Scholar]

- Kim, Yongtae, Haidan Li, and Siqi Li. 2014. Corporate Social Responsibility and Stock Price Crash Risk. Journal of Banking & Finance 43: 1–13. [Google Scholar]

- Krasnikov, Alexander, Saurabh Mishra, and David Orozco. 2009. Evaluating the Financial Impact of Branding Using Trademarks: A Framework and Empirical Evidence. Journal of Marketing 73: 154–66. [Google Scholar] [CrossRef] [Green Version]

- Krüger, Philipp. 2015. Corporate Goodness and Shareholder Wealth. Journal of Financial Economics 115: 304–29. [Google Scholar] [CrossRef]

- Larcker, David, Eric So, and Charles Wang. 2013. Boardroom Centrality and Firm Performance. Journal of Accounting and Economics 55: 2–3. [Google Scholar] [CrossRef] [Green Version]

- Li, Jinglin, and Zhen Yang. 2019. Board Gender Diversity, Corporate Social Responsibility and Technological Innovation: An Empirical Study Based on Listed Firms in China. Science of Science and Management of S.&T. 40: 34–51. (In Chinese). [Google Scholar]

- Li, Ming, and Lili Bao. 2017. Construction and Application of Corporate Social Responsibility Risk Evaluation System. Finance and Accounting Monthly, 61–66. (In Chinese). [Google Scholar]

- Li, Ming, and Wei Guan. 2017. The Intertemporal Impact of Corporate Social Responsibility Risk and Corporate Performance: Based on the Analysis of 171 Listed Manufacturing Companies. Enterprise Economy 36: 27–34. (In Chinese). [Google Scholar]

- Li, Qian, Jie Xiong, and Han Huang. 2018. An Empirical Research of Corporate Social Irresponsibility on Financial Performance. Chinese Journal of Management 15: 255–61. (In Chinese). [Google Scholar]

- Li, Wan, Rajaram Veliyath, and Justin Tan. 2013. Network Characteristics and Firm Performance: An Examination of the Relationships in the Context of a Cluster. Journal of Small Business Management 51: 1–22. [Google Scholar] [CrossRef]

- Lin-Hi, Nick, and Karsten Müller. 2013. The CSR Bottom Line: Preventing Corporate Social Irresponsibility. Journal of Business Research 66: 1928–36. [Google Scholar] [CrossRef]

- Liu, Bai, Tao Ju, and Simon S. S. Gao. 2021a. The Combined Effects of Innovation and Corporate Social Responsibility on Firm Financial Risk. Journal of International Financial Management & Accounting 32: 283–310. [Google Scholar]

- Liu, Jihan, and Jianqiong Wang. 2016. Similar Behavior of Corporate Social Responsibility Performance in the Social Network. Chinese Journal of Management Science 24: 115–23. (In Chinese). [Google Scholar] [CrossRef]

- Liu, Yi, Xingping Jia, Xingzhi Jia, and Xenophon Koufteros. 2021b. CSR Orientation Incongruence and Supply Chain Relationship Performance—A Network Perspective. Journal of Operations Management 67: 237–60. [Google Scholar] [CrossRef]

- Lu, Yingjun, and Indra Abeysekera. 2021. Do Investors and Analysts Value Strategic Corporate Social Responsibility Disclosures? Evidence from China. Journal of International Financial Management & Accounting 32: 147–81. [Google Scholar]

- Luo, Jiaqi, Mingxiao Bi, and Haibo Kuang. 2021. Design of Evaluation Scheme for Social Responsibility of China’s Transportation Enterprises from the Perspective of Green Supply Chain Management. Sustainability 13: 3390. [Google Scholar] [CrossRef]

- Luo, Xueming, Christian Homburg, and Jan Wieseke. 2010. Customer Satisfaction, Analyst Stock Recommendations, and Firm Value. Journal of Marketing Research 47: 1041–58. [Google Scholar] [CrossRef]

- Martin, Geoffrey, Remzi Gözübüyük, and Manuel Becerra. 2015. Interlocks and Firm Performance: The Role of Uncertainty in the Directorate Interlock-Performance Relationship. Strategic Management Journal 36: 235–53. [Google Scholar] [CrossRef]

- Merton, Robert C. 1974. On the Pricing of Corporate Debt: The Risk Structure of Interest Rates. Journal of Finance 29: 449–70. [Google Scholar]

- Merton, Robert C. 1987. A Simple Model of Capital Market Equilibrium with Incomplete Information. Journal of Finance 42: 483–509. [Google Scholar] [CrossRef]

- Nahapiet, Janine, and Sumantra Ghoshal. 1998. Social Capital, Intellectual Capital, and the Organizational Advantage. Academy of Management Review 23: 242–66. [Google Scholar] [CrossRef]

- Oliver, Christine. 1991. Strategic Responses to Institutional Processes. Academy of Management Review 16: 145–79. [Google Scholar] [CrossRef]

- Pan, Xin, Xuanjin Chen, and Lutao Ning. 2018. The Roles of Macro and Micro Institutions in Corporate Social Responsibility (CSR): Evidence from Listed Firms in China. Management Decision 56: 955–71. [Google Scholar] [CrossRef]

- Pfeffer, Jeffrey, and Gerald R. Salancik. 1978. The External Control of Organizations: A Resource Dependence Perspective. Bloomington: Stanford University Press. [Google Scholar]

- Price, Joseph M., and Wenbin Sun. 2017. Doing Good and Doing Bad: The Impact of Corporate Social Responsibility and Irresponsibility on Firm Performance. Journal of Business Research 80: 82–97. [Google Scholar] [CrossRef]

- Sun, Wenbin, and Zhihua Ding. 2021. Is Doing Bad Always Punished? A Moderated Longitudinal Analysis on Corporate Social Irresponsibility and Firm Value. Business & Society 60: 1811–48. [Google Scholar]

- Tichy, Noel, Michael Tushman, and Charles Fombrun. 1979. Social Network Analysis for Organizations. Academy of Management Review 4: 507–19. [Google Scholar] [CrossRef]

- Vilanova, Marc, Josep Maria Lozano, and Daniel Arenas. 2009. Exploring the Nature of the Relationship between CSR and Competitiveness. Journal of business Ethics 87: 57–69. [Google Scholar] [CrossRef]

- Wan, Shouyi, and Feifei Liu. 2015. Study on the Causes and Economic Consequences of Corporate Social Irresponsibility. Friends of Accounting, 15–25. (In Chinese). [Google Scholar]

- Wang, Zhihong, and Joseph Sarkis. 2017. Corporate Social Responsibility Governance, Outcomes, and Financial Performance. Journal of Cleaner Production 162: 1607–16. [Google Scholar] [CrossRef]

- Xie, Deren, and Yunsen Chen. 2012. Board Network: Definition, Characteristics and Measurement. Accounting Research 95: 44–51. (In Chinese). [Google Scholar]

- Xie, Hongming. 2005. The Impacts of Network Structural Properties on the Dynamic Competition Actions. Science Research Management, 104–12. (In Chinese). [Google Scholar]

- Xu, Jianzhong, and Yingying Xu. 2015. Enterprise’s Collaborative Competence, Network Location and Technology Innovation Performance—Empirical Analysis of Manufacturing Enterprises in the Bohai Coastal Region. Management Review 27: 114–25. (In Chinese). [Google Scholar]

{kind=link}

| Variables | Mean Standard | Deviation | Minimum | Maximum |

|---|---|---|---|---|

| NP (CNY 100 million) | 6.68 | 40.8 | −467 | 1510 |

| Stock | 0.0948 | 0.514 | −0.878 | 11.85 |

| Inno | 51.19 | 144.7 | 0 | 1082 |

| CSIR | 15.27 | 9.455 | 0 | 58.11 |

| Med | 0.000556 | 0.000560 | 0 | 0.00282 |

| Close | 0.114 | 0.0550 | 0.0000567 | 0.173 |

| SH | 0.286 | 0.0869 | 0.141 | 0.570 |

| Density | 0.000461 | 0.0000767 | 0.000360 | 0.000552 |

| Age | 2.853 | 0.343 | 0.693 | 3.714 |

| Top10 | 0.541 | 0.159 | 0.0132 | 0.986 |

| Lev | 0.531 | 0.831 | −0.195 | 63.97 |

| Broad | 8.877 | 1.805 | 3 | 20 |

| Variables | NP | Stock | Inno | CSIR | Med | Close | SH | Density | Age | Top10 | Property | Lev | Broad | Indep | MY | Industry |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| NP | 1 | |||||||||||||||

| Stock | 0.016 ** | 1 | ||||||||||||||

| Inno | 0.383 *** | −0.00800 | 1 | |||||||||||||

| CSIR | −0.123 *** | −0.053 *** | −0.173 *** | 1 | ||||||||||||

| Med | 0.032 *** | 0.015 * | 0.062 *** | −0.095 *** | 1 | |||||||||||

| Close | 0.017 ** | 0.132 *** | 0.026 *** | −0.093 *** | 0.350 *** | 1 | ||||||||||

| SH | −0.058 *** | −0.032 *** | −0.099 *** | 0.145 *** | −0.536 *** | −0.427 *** | 1 | |||||||||

| Density | −0.025 *** | 0.099 *** | −0.033 *** | 0.084 *** | 0.063 *** | 0.215 *** | −0.0110 | 1 | ||||||||

| Age | −0.035 *** | −0.016 * | −0.056 *** | −0.014 * | −0.060 *** | −0.033 *** | −0.068 *** | −0.229 *** | 1 | |||||||

| Top10 | 0.192 *** | 0.024 *** | 0.126 *** | −0.162 *** | 0.075 *** | 0.048 *** | −0.126 *** | −0.037 *** | −0.179 *** | 1 | ||||||

| Property | −0.058 *** | 0.042 *** | −0.042 *** | 0.072 *** | −0.024 *** | −0.047 *** | 0.105 *** | −0.022 *** | −0.021 *** | −0.108 *** | 1 | |||||

| Lev | −0.013 * | −0.018 ** | 0.00900 | 0.081 *** | −0.0100 | −0.00800 | −0.00500 | 0 | 0.039 *** | −0.035 *** | 0.00100 | 1 | ||||

| Broad | 0.083 *** | −0.018 ** | 0.082 *** | −0.073 *** | 0.062 *** | 0.103 *** | −0.468 *** | 0.040 *** | −0.030 *** | 0.124 *** | −0.173 *** | 0.00700 | 1 | |||

| Indep | 0.065 *** | 0 | 0.080 *** | −0.036 *** | 0.046 *** | −0.00200 | 0.133 *** | −0.028 *** | −0.023 *** | 0.00200 | 0.038 *** | 0.00500 | −0.407 *** | 1 | ||

| MY | −0.015 * | 0.521 *** | −0.026 *** | −0.149 *** | −0.00200 | 0.116 *** | −0.072 *** | 0.110 *** | 0.058 *** | −0.018 ** | 0.025 *** | −0.00300 | −0.031 *** | 0.0110 | 1 | |

| Industry | −0.046 *** | 0.023 *** | −0.083 *** | 0.070 *** | 0.059 *** | 0.043 *** | −0.042 *** | 0 | 0.114 *** | 0.00700 | 0.029 *** | 0.025 *** | −0.013 * | 0.00600 | 0.00200 | 1 |

| Variables | 0a | 1a | 2a | 3a | 4a |

|---|---|---|---|---|---|

| NP | NP | NP | NP | NP | |

| CSIR | −0.020 *** | −0.021 *** | −0.023 *** | −0.023 *** | |

| (0.006) | (0.006) | (0.006) | (0.006) | ||

| CSIR*SH | 0.009 ** | 0.009 ** | |||

| (0.004) | (0.004) | ||||

| CSIR*Density | 0.023 *** | 0.023 *** | |||

| (0.004) | (0.004) | ||||

| SH | 0.001 | 0.001 | 0.000 | −0.000 | |

| (0.005) | (0.005) | (0.005) | (0.005) | ||

| Density | 0.126 | 0.089 | 0.046 | 0.054 | |

| (0.104) | (0.104) | (0.104) | (0.104) | ||

| Age | 0.040 *** | 0.040 *** | 0.040 *** | 0.037 ** | 0.037 ** |

| (0.016) | (0.016) | (0.016) | (0.015) | (0.015) | |

| Top10 | 0.063 *** | 0.063 *** | 0.063 *** | 0.065 *** | 0.065 *** |

| (0.007) | (0.007) | (0.007) | (0.007) | (0.007) | |

| Lev | −0.013 *** | −0.013 *** | −0.013 *** | −0.012 *** | −0.012 *** |

| (0.004) | (0.004) | (0.004) | (0.004) | (0.004) | |

| Broad | 0.036 *** | 0.035 *** | 0.035 *** | 0.033 *** | 0.034 *** |

| (0.008) | (0.008) | (0.008) | (0.008) | (0.008) | |

| Indep | 0.025 *** | 0.025 *** | 0.025 *** | 0.024 *** | 0.025 *** |

| (0.006) | (0.006) | (0.006) | (0.006) | (0.006) | |

| MY | 0.007 | 0.007 | 0.007 | 0.008 | 0.008 |

| (0.009) | (0.009) | (0.009) | (0.009) | (0.009) | |

| Controls | 0.055 | 0.022 | −0.099 | −0.024 | −0.018 |

| (0.279) | (0.278) | (0.251) | (0.278) | (0.278) | |

| N | 15,930 | 15,930 | 15,930 | 15,930 | 15,930 |

| R2 | 0.1957 | 0.1991 | 0.1997 | 0.2006 | 0.2013 |

| Industry | Control | Control | Control | Control | Control |

| Year | Control | Control | Control | Control | Control |

| Property | Control | Control | Control | Control | Control |

| Variables | 0b | 1b | 2b |

|---|---|---|---|

| Stock | Stock | Stock | |

| CSIR | 0.014 * | 0.014 ** | |

| (0.007) | (0.007) | ||

| CSIR*Close | 0.027 *** | ||

| (0.007) | |||

| Close | −0.000 | 0.001 | −0.004 |

| (0.010) | (0.010) | (0.010) | |

| Age | 0.027 *** | 0.026 *** | 0.026 *** |

| (0.008) | (0.008) | (0.008) | |

| Top10 | 0.063 *** | 0.064 *** | 0.064 *** |

| (0.007) | (0.007) | (0.007) | |

| Lev | −0.014 ** | −0.014 ** | −0.014 ** |

| (0.006) | (0.006) | (0.006) | |

| Broad | −0.001 | 0.000 | 0.000 |

| (0.008) | (0.008) | (0.008) | |

| Indep | −0.005 | −0.005 | −0.005 |

| (0.007) | (0.007) | (0.007) | |

| MY | 0.200 *** | 0.201 *** | 0.201 *** |

| (0.015) | (0.015) | (0.015) | |

| Controls | 0.125 | 0.113 | 0.117 |

| (0.084) | (0.084) | (0.084) | |

| N | 15,930 | 15,930 | 15,930 |

| R2 | 0.3524 | 0.3525 | 0.3532 |

| Industry | Control | Control | Control |

| Year | Control | Control | Control |

| Property | Control | Control | Control |

| Variables | 0c | 1c | 2c | 3c | 4c |

|---|---|---|---|---|---|

| Inno | Inno | Inno | Inno | Inno | |

| CSIR | −0.013 ** | −0.012 ** | −0.013 ** | −0.013 ** | |

| (0.006) | (0.006) | (0.006) | (0.006) | ||

| CSIR*Med | 0.008 ** | 0.008 * | |||

| (0.004) | (0.004) | ||||

| CSIR*Density | 0.009 ** | 0.009 ** | |||

| (0.004) | (0.004) | ||||

| Med | −0.006 | −0.006 | −0.006 | −0.006 | |

| (0.005) | (0.005) | (0.005) | (0.005) | ||

| Density | 1.035 *** | 1.017 *** | 1.006 *** | 1.004 *** | |

| (0.103) | (0.104) | (0.104) | (0.104) | ||

| Age | 0.060 *** | 0.059 *** | 0.059 *** | 0.058 *** | 0.057 *** |

| (0.016) | (0.015) | (0.015) | (0.016) | (0.015) | |

| Top10 | 0.036 *** | 0.036 *** | 0.036 *** | 0.036 *** | 0.037 *** |

| (0.007) | (0.007) | (0.007) | (0.007) | (0.007) | |

| Lev | 0.003 | 0.003 | 0.003 | 0.004 | 0.004 |

| (0.004) | (0.004) | (0.004) | (0.004) | (0.004) | |

| Broad | 0.027 *** | 0.027 *** | 0.026 *** | 0.026 *** | 0.026 *** |

| (0.008) | (0.008) | (0.008) | (0.008) | (0.008) | |

| Indep | 0.012 ** | 0.012 ** | 0.012 ** | 0.012 * | 0.012 * |

| (0.006) | (0.006) | (0.006) | (0.006) | (0.006) | |

| MY | −0.008 | −0.008 | −0.008 | −0.008 | −0.007 |

| (0.009) | (0.009) | (0.009) | (0.009) | (0.009) | |

| Controls | 0.957 *** | 0.942 *** | −0.399 | 0.932 *** | 0.930 *** |

| (0.280) | (0.278) | (0.251) | (0.278) | (0.277) | |

| N | 15,930 | 15,930 | 15,930 | 15,930 | 15,930 |

| R2 | 0.168 | 0.1713 | 0.1708 | 0.1723 | 0.1712 |

| Industry | Control | Control | Control | Control | Control |

| Year | Control | Control | Control | Control | Control |

| Property | Control | Control | Control | Control | Control |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Luo, J.; Bi, M.; Jia, D. Corporate Social Responsibility Risk and Firm Performance: A Network Perspective. Int. J. Financial Stud. 2022, 10, 40. https://doi.org/10.3390/ijfs10020040

Luo J, Bi M, Jia D. Corporate Social Responsibility Risk and Firm Performance: A Network Perspective. International Journal of Financial Studies. 2022; 10(2):40. https://doi.org/10.3390/ijfs10020040

Chicago/Turabian StyleLuo, Jiaqi, Mingxiao Bi, and Dandan Jia. 2022. "Corporate Social Responsibility Risk and Firm Performance: A Network Perspective" International Journal of Financial Studies 10, no. 2: 40. https://doi.org/10.3390/ijfs10020040