Exploring Drivers Shaping the Choice of Alternative-Fueled New Vessels

Abstract

:1. Introduction

2. Literature Review

2.1. Review of Alternative Marine Fuels and Shipowners’ Choices

2.2. Review on Multinomial Logit Model

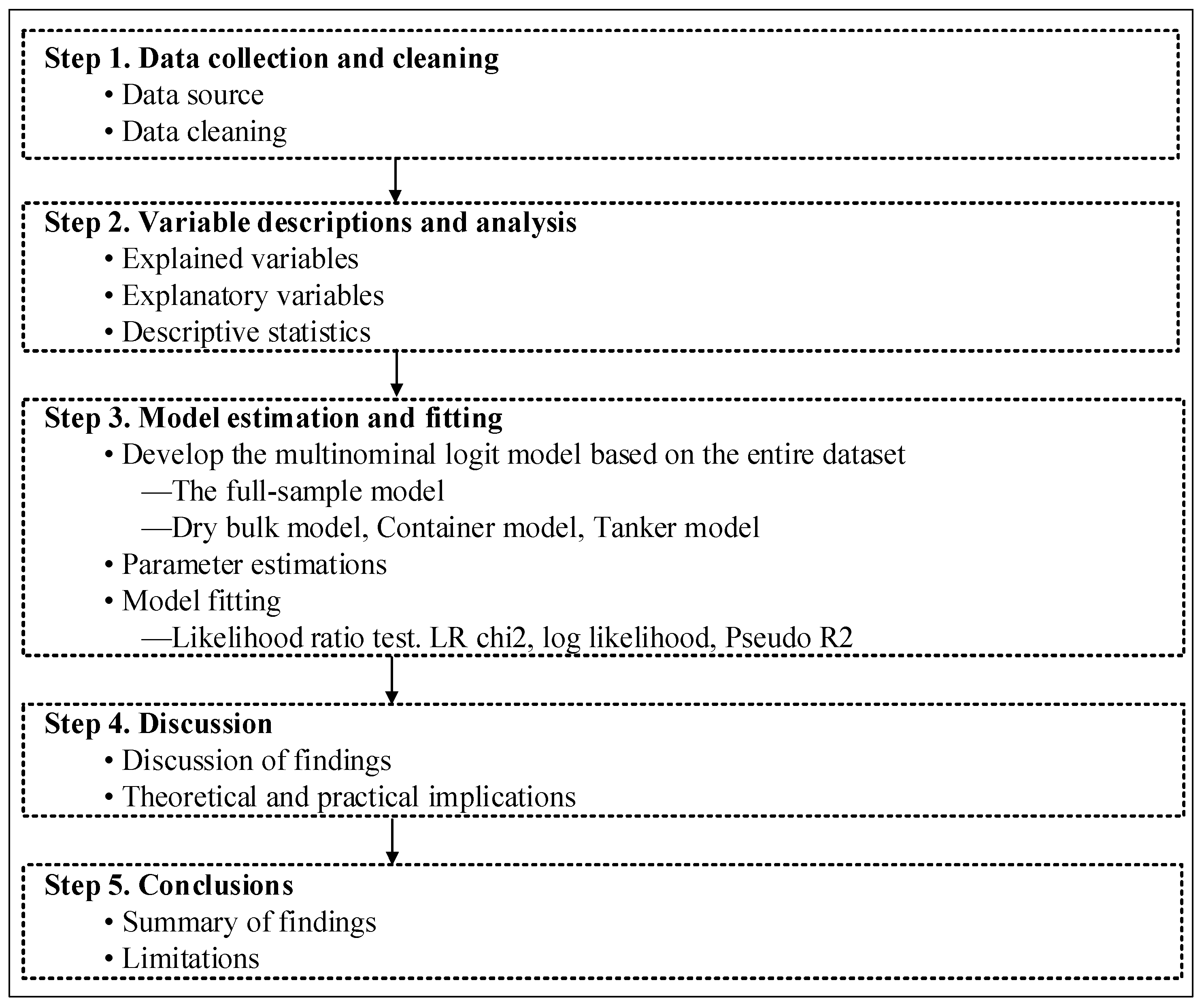

3. Methodology

3.1. Conceptual Framework

3.2. Model Building

4. Descriptions and Analysis of Variables

4.1. Explained and Explanatory Variable

4.1.1. Explained Variables

4.1.2. Explanatory Variables

4.2. Data and Variable Analysis

4.2.1. Data Collection

4.2.2. Descriptive Statistics

- (1)

- Alternative fuels

- (2)

- Vessel type analysis

- (3)

- DWT analysis

- (4)

- Policy analysis

- (5)

- Shipowner analysis

5. Empirical Analysis

5.1. Model Estimation

5.2. Model Fitting

5.3. Discussion

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Zis, T.; Psaraftis, H.N. Operational Measures to Mitigate and Reverse the Potential Modal Shifts Due to Environmental Legislation. Marit. Policy Manag. 2019, 46, 117–132. [Google Scholar] [CrossRef]

- Psaraftis, H.N. Decarbonization of Maritime Transport: To Be or Not to Be? Marit. Econ. Logist. 2019, 21, 353–371. [Google Scholar] [CrossRef]

- Hoffmann, P.N.; Eide, M.S.; Endresen, O. Effect of Proposed Co2 Emission Reduction Scenarios on Capital Expenditure. Marit. Policy Manag. 2012, 39, 443–460. [Google Scholar] [CrossRef]

- Kim, K.; Lim, S.; Lee, C.H.; Lee, W.J.; Jeon, H.; Jung, J.W.; Jung, D.H. Forecasting Liquefied Natural Gas Bunker Prices Using Artificial Neural Network for Procurement Management. J. Mar. Sci. Eng. 2022, 10, 1814. [Google Scholar] [CrossRef]

- Vilhelmsen, C.; Lusby, R.; Larsen, J. Tramp Ship Routing and Scheduling with Integrated Bunker Optimization. EURO J. Transp. Logist. 2013, 32, 143–175. [Google Scholar] [CrossRef]

- Xing, H.; Stuart, C.; Spence, S.; Chen, H. Alternative Fuel Options for Low Carbon Maritime Transportation: Pathways to 2050. J. Clean. Prod. 2021, 297, 126651. [Google Scholar] [CrossRef]

- Halim, R.A.; Kirstein, L.; Merk, O.; Martinez, L.M. Decarbonization Pathways for International Maritime Transport: A Model-Based Policy Impact Assessment. Sustainability 2018, 10, 2243. [Google Scholar] [CrossRef]

- Balcombe, P.; Brierley, J.; Lewis, C.; Skatvedt, L.; Speirs, J.; Hawkes, A.; Staffell, I. How to Decarbonise International Shipping: Options for Fuels, Technologies and Policies. Energy Convers. Manag. 2019, 182, 72–88. [Google Scholar] [CrossRef]

- Serra, P.; Fancello, G. Towards the Imo’s Ghg Goals: A Critical Overview of the Perspectives and Challenges of the Main Options for Decarbonizing International Shipping. Sustainability 2020, 12, 3220. [Google Scholar] [CrossRef]

- Romano, A.; Yang, Z. Decarbonisation of Shipping: A State of the Art Survey for 2000–2020. Ocean. Coast. Manag. 2021, 214, 105936. [Google Scholar] [CrossRef]

- Mallouppas, G.; Yfantis, E.A. Decarbonization in Shipping Industry: A Review of Research, Technology Development, and Innovation Proposals. J. Mar. Sci. Eng. 2021, 9, 415. [Google Scholar] [CrossRef]

- Bouman, E.A.; Lindstad, E.; Rialland, A.I.; Strømman, A.H. State-of-the-Art Technologies, Measures, and Potential for Reducing Ghg Emissions from Shipping—A Review. Transp. Res. Part D Transp. Environ. 2017, 52, 408–421. [Google Scholar] [CrossRef]

- Ampah, J.D.; Yusuf, A.A.; Afrane, S.; Jin, C.; Liu, H.F. Reviewing Two Decades of Cleaner Alternative Marine Fuels: Towards Imo’s Decarbonization of the Maritime Transport Sector. J. Clean. Prod. 2021, 320, 128871. [Google Scholar] [CrossRef]

- Tadros, M.; Ventura, M.; Soares, C.G. Review of Current Regulations, Available Technologies, and Future Trends in the Green Shipping Industry. Ocean. Eng. 2023, 280, 114670. [Google Scholar] [CrossRef]

- Moshiul, A.M.; Mohammad, R.; Hira, F.A.; Maarop, N. Alternative Marine Fuel Research Advances and Future Trends: A Bibliometric Knowledge Mapping Approach. Sustainability 2022, 14, 4947. [Google Scholar] [CrossRef]

- Le Fevre, C. A Review of Demand Prospects for Lng as a Marine Transport Fuel; Oxford Institute for Energy Studies: Oxford, UK, 2018. [Google Scholar]

- Hansson, J.; Brynolf, S.; Fridell, E.; Lehtveer, M. The Potential Role of Ammonia as Marine Fuel-Based on Energy Systems Modeling and Multi-Criteria Decision Analysis. Sustainability 2020, 12, 3265. [Google Scholar] [CrossRef]

- Priyanto, E.M.; Olcer, A.I.; Dalaklis, D.; Ballini, F. The Potential of Methanol as an Alternative Marine Fuel for Indonesian Domestic Shipping. Int. J. Marit. Eng. 2020, 162, 115–129. [Google Scholar] [CrossRef]

- Lagouvardou, S.; Lagemann, B.; Psaraftis, H.N.; Lindstad, E.; Erikstad, S.O. Marginal Abatement Cost of Alternative Marine Fuels and the Role of Market-Based Measures. Nat. Energy 2023, 1–12. [Google Scholar] [CrossRef]

- Kim, A.R.; Seo, Y.J. The Reduction of Sox Emissions in the Shipping Industry: The Case of Korean Companies. Mar. Policy 2019, 100, 98–106. [Google Scholar] [CrossRef]

- Stalmokaite, I.; Yliskyla-Peuralahti, J. Sustainability Transitions in Baltic Sea Shipping: Exploring the Responses of Firms to Regulatory Changes. Sustainability 2019, 11, 1916. [Google Scholar] [CrossRef]

- Hansson, J.; Mansson, S.; Brynolf, S.; Grahn, M. Alternative Marine Fuels: Prospects Based on Multi-Criteria Decision Analysis Involving Swedish Stakeholders. Biomass Bioenergy 2019, 126, 159–173. [Google Scholar] [CrossRef]

- Zhang, X.; Bao, Z.H.; Ge, Y.E. Investigating the Determinants of Shipowners’ Emission Abatement Solutions for Newbuilding Vessels. Transp. Res. Part D Transp. Environ. 2021, 99, 102989. [Google Scholar] [CrossRef]

- Makitie, T.; Steen, M.; Saether, E.A.; Bjorgum, O.; Poulsen, R.T. Norwegian Ship-Owners’ Adoption of Alternative Fuels. Energy Policy 2022, 163, 112869. [Google Scholar] [CrossRef]

- Chen, S.; Zheng, S.Y.; Sys, C. Policies Focusing on Market-Based Measures Towards Shipping Decarbonization: Designs, Impacts and Avenues for Future Research. Transp. Policy 2023, 137, 109–124. [Google Scholar] [CrossRef]

- Kaya, A.Y.; Erginer, K.E. An Analysis of Decision-Making Process of Shipowners for Implementing Energy Efficiency Measures on Existing Ships: The Case of Turkish Maritime Industry. Ocean. Eng. 2021, 241, 110001. [Google Scholar] [CrossRef]

- Bao, Z.H.; Zhang, X.; Fu, G.Y. Factors Influencing Decision to Sulphur Oxide Emission Abatement for Cruise Shipping Companies. Int. J. Logist. Res. Appl. 2022, 1–20. [Google Scholar] [CrossRef]

- Alizadeh, A.H.; Strandenes, S.P.; Thanopoulou, H. Capacity Retirement in the Dry Bulk Market: A Vessel Based Logit Model. Transp. Res. Part E-Logist. Transp. Rev. 2016, 92, 28–42. [Google Scholar] [CrossRef]

- Fan, L.X.; Xie, J.Q. Identify Determinants of Container Ship Size Investment Choice. Marit. Policy Manag. 2023, 50, 219–234. [Google Scholar] [CrossRef]

- Kanamoto, K.; Liwen, M.R.; Nakashima, M.; Shibasaki, R. Can Maritime Big Data Be Applied to Shipping Industry Analysis? Focussing on Commodities and Vessel Sizes of Dry Bulk Carriers. Marit. Econ. Logist. 2021, 23, 211–236. [Google Scholar] [CrossRef]

- Talluri, K.; van Ryzin, G. Revenue Management under a General Discrete Choice Model of Consumer Behavior. Manag. Sci. 2004, 50, 15–33. [Google Scholar] [CrossRef]

- Louviere, J.J.; Hensher, D.A.; Swait, J.D. Stated Choice Methods: Analysis and Applications; Cambridge University Press: Cambridge, UK, 2000. [Google Scholar]

- Balcombe, P.; Staffell, I.; Kerdan, I.G.; Speirs, J.F.; Brandon, N.P.; Hawkes, A.D. How Can Lng-Fuelled Ships Meet Decarbonisation Targets? An Environmental and Economic Analysis. Energy 2021, 227, 120462. [Google Scholar] [CrossRef]

- Lindstad, E.; Eskeland, G.S.; Rialland, A.; Valland, A. Decarbonizing Maritime Transport: The Importance of Engine Technology and Regulations for Lng to Serve as a Transition Fuel. Sustainability 2020, 12, 8793. [Google Scholar] [CrossRef]

- Wang, S.Y.; Notteboom, T. The Adoption of Liquefied Natural Gas as a Ship Fuel: A Systematic Review of Perspectives and Challenges. Transp. Rev. 2014, 34, 749–774. [Google Scholar] [CrossRef]

- Lee, B.; Lee, H.; Lim, D.; Brigljevic, B.; Cho, W.; Cho, H.S.; Kim, C.H.; Lim, H. Renewable Methanol Synthesis from Renewable H-2 and Captured Co2: How Can Power-to-Liquid Technology Be Economically Feasible? Appl. Energy 2020, 279, 115827. [Google Scholar] [CrossRef]

- Verhelst, S.; Turner, J.W.G.; Sileghem, L.; Vancoillie, J. Methanol as a Fuel for Internal Combustion Engines. Prog. Energy Combust. Sci. 2019, 70, 43–88. [Google Scholar] [CrossRef]

- Inal, O.B.; Zincir, B.; Deniz, C. Investigation on the Decarbonization of Shipping: An Approach to Hydrogen and Ammonia. Int. J. Hydrogen Energy 2022, 47, 19888–19900. [Google Scholar] [CrossRef]

- Zincir, B. Environmental and Economic Evaluation of Ammonia as a Fuel for Short-Sea Shipping: A Case Study. Int. J. Hydrogen Energy 2022, 47, 18148–18168. [Google Scholar] [CrossRef]

- Foretich, A.; Zaimes, G.G.; Hawkins, T.R.; Newes, E. Challenges and Opportunities for Alternative Fuels in the Maritime Sector. Marit. Transp. Res. 2021, 2, 100033. [Google Scholar] [CrossRef]

- Lindstad, E.; Lagemann, B.; Rialland, A.; Gamlem, G.M.; Valland, A. Reduction of Maritime Ghg Emissions and the Potential Role of E-Fuels. Transp. Res. Part D Transp. Environ. 2021, 101, 103075. [Google Scholar] [CrossRef]

- Solakivi, T.; Paimander, A.; Ojala, L. Cost Competitiveness of Alternative Maritime Fuels in the New Regulatory Framework. Transp. Res. Part D Transp. Environ. 2022, 113, 103500. [Google Scholar] [CrossRef]

- Steen, M.; Bach, H.; Bjørgum, Ø.; Hansen, T.; Kenzhegaliyeva, A. Greening the Fleet: A Technological Innovation System (Tis) Analysis of Hydrogen, Battery Electric, Liquefied Biogas, and Biodiesel in the Maritime Sector; SINTEF: Trondheim, Norway, 2019. [Google Scholar]

- Li, K.; Wu, M.; Gu, X.H.; Yuen, K.F.; Xiao, Y. Determinants of Ship Operators’ Options for Compliance with Imo 2020. Transp. Res. Part D Transp. Environ. 2020, 86, 102459. [Google Scholar] [CrossRef]

- Beenstock, M. A Theory of Ship Prices. Marit. Policy Manag. 1985, 12, 215–225. [Google Scholar] [CrossRef]

- Xu, J.J.; Yip, T.L. Ship Investment at a Standstill? An Analysis of Shipbuilding Activities and Policies. Appl. Econ. Lett. 2012, 19, 269–275. [Google Scholar] [CrossRef]

- Jiang, L.; Kronbak, J.; Christensen, L.P. The Costs and Benefits of Sulphur Reduction Measures: Sulphur Scrubbers Versus Marine Gas Oil. Transp. Res. Part D Transp. Environ. 2014, 28, 19–27. [Google Scholar] [CrossRef]

- Zhu, M.; Yuen, K.F.; Ge, J.W.; Li, K.X. Impact of Maritime Emissions Trading System on Fleet Deployment and Mitigation of Co2 Emission. Transp. Res. Part D Transp. Environ. 2018, 62, 474–488. [Google Scholar] [CrossRef]

- Yang, J.L.; Zhang, X.; Ge, Y.E. Measuring Risk Spillover Effects on Dry Bulk Shipping Market: A Value-at-Risk Approach. Marit. Policy Manag. 2022, 49, 558–576. [Google Scholar] [CrossRef]

- Mazzanti, M. Discrete Choice Models and Valuation Experiments. J. Econ. Stud. 2003, 30, 584–604. [Google Scholar] [CrossRef]

- Law, P.K. A Theory of Reasoned Action Model of Accounting Students’ Career Choice in Public Accounting Practices in the Post-Enron. J. Appl. Account. Res. 2010, 11, 58–73. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Explanatory Variables | Description | |

|---|---|---|

| Ship-related | DWT | Deadweight tonnage of the vessel |

| Type | Ship type in the orderbook; 1 if ship type is dry bulker; 2 if container vessel; 3 if tanker; 4 if multipurpose; 5 if gas carrier; 6 if ro-ro; 7 if general cargo vessel | |

| Shipowner-related | Nation | China, Japan, Greece, Singapore, Republic of Korea, Germany, Norway, France etc. The selected countries account for over 75% of all orders |

| Market-related | Earnings (USD/day) | Monthly value of ClarkSea Index for full sample model (composite index of freight market performance). For the dry bulk model, container model, and tanker model, Clarkson Average Earnings are used for dry bulks, containers, and tankers, respectively. |

| LNG/FO | The ratio of monthly LNG bunker prices over very low sulfur fuel oil prices | |

| SOFR (%) | Secured overnight financing rate | |

| Idle rate (%) | The ratio of the idle fleet over the total | |

| CO2 price (USD/day) | CO2 European Union Allowances price | |

| Regulation-related | Policy | Dummy variables of decarbonization policies |

| Vessel Type | Number of Orders | Proportion |

|---|---|---|

| Bulk | 1467 | 31.13% |

| Container | 1152 | 24.45% |

| Tanker | 890 | 18.89% |

| Multi-purpose | 108 | 2.29% |

| Gas carrier | 545 | 11.56% |

| Ro-ro | 185 | 3.92% |

| General cargo | 365 | 7.74% |

| Total | 4712 | 100% |

| Alternative Fuels | Number of Orders | Proportion | Tonnage (Million) | Proportion |

|---|---|---|---|---|

| Conventional fuel | 3203 | 67.98% | 179.24 | 56.47% |

| LNG capable | 771 | 16.36% | 78.5 | 24.76% |

| Methanol | 141 | 2.99% | 16.9 | 5.33% |

| Ready | 326 | 6.92% | 32.8 | 10.35% |

| Other fuels | 271 | 5.75% | 9.74 | 3.07% |

| Total | 4712 | 100% | 317.18 | 100% |

| Vessel Type | Conventional | LNG Capable | Methanol | Ready | Other Fuels |

|---|---|---|---|---|---|

| Bulk | 92.2% | 4.9% | 0.5% | 2.2% | 0.1% |

| Container | 60.3% | 18.1% | 9.5% | 11.3% | 0.7% |

| Tanker | 70.3% | 8.7% | 2.5% | 13.5% | 5.1% |

| Multi-purpose | 83.3% | 2.8% | 0.0% | 9.3% | 4.6% |

| Gas carrier | 14.7% | 53.4% | 0.0% | 1.5% | 30.5% |

| Ro-ro | 13.0% | 59.5% | 1.1% | 13.5% | 13.0% |

| General cargo | 66.2% | 1.8% | 27.9% | 0.0% | 4.2% |

| Alternative Fuel | DWT | ||||

|---|---|---|---|---|---|

| Mean | Std. Dev. | Max. | Min. | Median | |

| Conventional fuel | 55,962.04 | 51,921.87 | 319,202 | 72 | 49,000 |

| LNG capable | 101,803.74 | 67,689.98 | 321,020 | 2500 | 96,000 |

| Methanol | 119,532.93 | 68,809.73 | 225,000 | 4000 | 140,000 |

| Ready | 100,661.84 | 89,198.77 | 320,000 | 110 | 63,598 |

| Other fuels | 35,936.34 | 22,722.50 | 64,012 | 900 | 30,108 |

| Total | 67,305.98 | 61,627.50 | 321,020 | 72 | 55,077 |

| Year | Milestone Actions |

|---|---|

| 2020.11 | Encouraging member states to develop and submit voluntary National Action Plans to address GHG emissions from ships |

| 2021.06 | Three additional measures adopted including a mandatory Carbon Intensity Indicator (CII), an Energy Efficiency Existing Ship Index (EEXI), and a strengthening SEEMP |

| 2021.12 | Initiating the revision of the Initial IMO Strategy on Reduction of GHG Emissions from Ships |

| 2022.06 | A series of 10 technical Guidelines adopted to support the implementation of the short-term GHG reduction measure |

| 2022.12 | Amendments adopted to MARPOL Annex VI to revise the data collection system for fuel oil consumption for the implementation of the EEXI and the CII framework |

| 2023.07 | Resolution adopted on Guidelines on lifecycle GHG intensity of marine fuels (LCA guidelines) |

| Rank | Shipowners | Conventional Fuel | LNG Capable | Methanol | Ready | Other Fuels | Total |

|---|---|---|---|---|---|---|---|

| 1 | Eastern Pacific Shpg | 35 | 36 | 0 | 2 | 34 | 107 |

| 2 | CMA CGM | 16 | 55 | 24 | 0 | 0 | 95 |

| 3 | CDB Leasing | 81 | 0 | 0 | 0 | 0 | 81 |

| 4 | MSC | 12 | 60 | 0 | 3 | 0 | 75 |

| 5 | Evergreen Marine | 47 | 0 | 24 | 0 | 0 | 71 |

| 6 | Seaspan Corporation | 40 | 25 | 0 | 0 | 0 | 65 |

| 7 | BoCom Leasing | 44 | 18 | 0 | 0 | 0 | 62 |

| 8 | Nisshin Shipping | 50 | 0 | 0 | 0 | 0 | 50 |

| 9 | Wan Hai Lines | 48 | 0 | 0 | 0 | 0 | 48 |

| 10 | SITC | 47 | 0 | 0 | 0 | 0 | 47 |

| Rank | Top 7 | Conventional Fuel | LNG Capable | Methanol | Ready | Other Fuels | Total |

|---|---|---|---|---|---|---|---|

| 1 | China | 1133 | 111 | 16 | 50 | 38 | 1348 |

| 2 | Japan | 746 | 100 | 12 | 22 | 36 | 916 |

| 3 | Greece | 312 | 76 | 0 | 70 | 19 | 477 |

| 4 | Singapore | 113 | 55 | 19 | 6 | 39 | 232 |

| 5 | Republic of Korea | 86 | 70 | 10 | 31 | 21 | 218 |

| 6 | Germany | 120 | 19 | 2 | 35 | 11 | 187 |

| 7 | Norway | 49 | 58 | 0 | 11 | 22 | 140 |

| Explanatory Variable | Full | Dry Bulk | Container | Tanker | ||||

|---|---|---|---|---|---|---|---|---|

| Chi-Square | Sig | Chi-Square | Sig | Chi-Square | Sig | Chi-Square | Sig | |

| Nation | 491.77 | 0.000 | 67.58 | 0.000 | 501.27 | 0.000 | 177.55 | 0.000 |

| Type | 2097.35 | 0.000 | (-) | (-) | (-) | (-) | (-) | (-) |

| DWT | 460.81 | 0.000 | 25.65 | 0.000 | 263.23 | 0.000 | 93.54 | 0.000 |

| Idle | 29.34 | 0.000 | 16.67 | 0.000 | 54.59 | 0.000 | 7.93 | 0.09 |

| SOFR | 95.88 | 0.000 | 6.68 | 0.03 | 27.18 | 0.000 | 10.76 | 0.03 |

| LNG/FO | 22.23 | 0.000 | 0.16 | 0.92 | 37.02 | 0.000 | 7.29 | 0.12 |

| CO2 price | 26.40 | 0.000 | 2.01 | 0.37 | 35.53 | 0.000 | 10.57 | 0.03 |

| Earnings | 39.72 | 0.000 | 9.61 | 0.000 | 14.99 | 0.000 | 6.71 | 0.15 |

| Policy1 | 5.46 | 0.24 | 9.60 | 0.000 | 11.16 | 0.02 | 23.50 | 0.000 |

| Policy2 | 53.32 | 0.000 | 6.19 | 0.04 | 33.37 | 0.000 | 10.26 | 0.03 |

| LNG Capable | Methanol | Ready | Other Fuels | |||||

|---|---|---|---|---|---|---|---|---|

| Parameters | RRR | Parameters | RRR | Parameters | RRR | Parameters | RRR | |

| Nation (China) | −1.105 *** (0.172) | 0.331 | −0.928 *** (0.333) | 0.395 | −0.819 *** (0.193) | 0.441 | −1.488 *** (0.246) | 0.226 |

| Nation (Japan) | −1.172 *** (0.197) | 0.310 | −0.704 * (0.379) | 0.495 | −1.096 *** (0.258) | 0.334 | −1.829 *** (0.270) | 0.161 |

| Nation (Greece) | −1.162 *** (0.214) | 0.313 | −16.39 (678.3) | 0 | 0.0404 (0.197) | 1.041 | −1.935 *** (0.331) | 0.144 |

| Nation (Singapore) | 0.489 ** (0.217) | 1.631 | 0.821 ** (0.343) | 2.273 | −1.298 *** (0.441) | 0.273 | 1.136 *** (0.275) | 3.114 |

| Nation (Republic of Korea) | −0.185 (0.262) | 0.831 | 0.717 (0.449) | 2.048 | 0.697 *** (0.255) | 2.008 | −0.750 ** (0.357) | 0.472 |

| Nation (Germany) | 0.356 (0.296) | 1.428 | −0.574 (0.779) | 0.563 | 1.222 *** (0.253) | 3.394 | −0.239 (0.447) | 0.787 |

| Nation (Norway) | 1.151 *** (0.287) | 3.161 | −13.94 (1037) | 0 | 0.945 ** (0.384) | 2.573 | 0.856 ** (0.352) | 2.354 |

| Nation (France) | 2.100 *** (0.287) | 8.166 | 1.472 *** (0.430) | 4.358 | −19.62 (7574) | 0 | 0.102 (0.769) | 1.107 |

| TYPE (Dry Bulk) | −2.393 *** (0.420) | 0.091 | 12.18 (729.0) | 1.94 × 105 | 14.42 (836.5) | 1.83 × 106 | −3.977 *** (0.772) | 0.019 |

| TYPE (Container) | −1.098 *** (0.411) | 0.334 | 15.70 (729.0) | 6.58 × 106 | 16.47 (836.5) | 1.42 × 107 | −2.377 *** (0.472) | 0.093 |

| TYPE (Tanker) | −1.086 ** (0.425) | 0.338 | 14.04 (729.0) | 1.25 × 106 | 16.49 (836.5) | 1.45 × 107 | −0.367 (0.326) | 0.693 |

| TYPE (Multipurpose) | −1.586 ** (0.711) | 0.205 | −0.685 (1615) | 0.504 | 15.79 (836.5) | 7.20 × 106 | −0.698 (0.547) | 0.498 |

| TYPE (Gas carrier) | 2.675 *** (0.412) | 14.512 | −1.481 (1854) | 0.242 | 16.04 (836.5) | 9.25 × 106 | 3.679 *** (0.318) | 39.607 |

| TYPE (Ro-ro) | 3.915 *** (0.438) | 50.149 | 15.04 (729.0) | 3.40 × 106 | 18.79 (836.5) | 1.45 × 108 | 2.397 *** (0.401) | 10.990 |

| DWT 1 | 1.355 *** (0.0794) | 1.014 | 0.681 *** (0.129) | 1.007 | 0.440 *** (0.0699) | 1.004 | 0.110 (0.0743) | 1.001 |

| Earnings 1 | 1.599 *** (0.378) | 1.016 | −1.428 (0.883) | 0.986 | 1.926 *** (0.425) | 1.0169 | 1.327 *** (0.496) | 1.013 |

| LNG/FO | 0.153 (0.0933) | 1.165 | −0.0936 (0.171) | 0.911 | −0.468 *** (0.141) | 0.626 | 0.194 (0.127) | 1.214 |

| SOFR | 0.0612 (0.0509) | 1.063 | 0.630 *** (0.099) | 1.878 | 0.388 *** (0.0604) | 1.474 | 0.348 *** (0.0714) | 1.416 |

| Idle Rate | −1.107 *** (0.249) | 0.331 | −0.252 (0.448) | 0.777 | −0.905 *** (0.313) | 0.405 | 0.123 (0.351) | 1.131 |

| CO2 Price 1 | −1.180 *** (0.396) | 0.988 | −3.880 *** (0.951) | 0.962 | −0.974 ** (0.461) | 0.990 | −1.224 ** (0.551) | 0.988 |

| Policy1 | −0.207 (0.327) | 0.813 | −0.388 (0.984) | 0.678 | −0.104 (0.400) | 0.901 | 0.904 * (0.470) | 2.469 |

| Policy2 | 0.896 *** (0.303) | 2.450 | 5.694 *** (1.090) | 297.08 | 0.0585 (0.338) | 1.060 | 0.772 * (0.426) | 2.164 |

| Constant | −23.02 *** (3.598) | 2.239 (729.1) | −34.24 (836.5) | −12.89 *** (4.718) | ||||

| Traditional_fuel (based outcome) | ||||||||

| Observations | 4712 | 4712 | 4712 | 4712 | ||||

| LNG Capable | Other Alternative Fuels | |||

|---|---|---|---|---|

| Parameters | RRR | Parameters | RRR | |

| Nation (China) | −0.959 *** (0.312) | 0.383 | −2.312 *** (0.517) | 0.099 |

| Nation (Japan) | −1.363 *** (0.338) | 0.256 | −2.090 *** (0.512) | 0.124 |

| Nation (Greece) | −0.872 * (0.475) | 0.418 | −15.99 (578.9) | 0 |

| DWT 1 | 0.481 ** (0.189) | 1.004 | 1.411 *** (0.335) | 1.014 |

| Earnings 1 | −1.902 *** (0.622) | 0.981 | −1.008 (0.936) | 0.989 |

| LNG/VLSFO | 0.00925 (0.209) | 1.010 | 0.0866 (0.214) | 1.090 |

| SOFR | −0.401 ** (0.183) | 0.670 | 0.318 (0.247) | 1.374 |

| Idle Rate | −1.591 *** (0.434) | 0.234 | 0.267 (0.408) | 1.306 |

| CO2 Price 1 | 1.026 (0.895) | 1.010 | −1.267 (1.610) | 0.987 |

| Policy1 | 2.266 *** (0.760) | 9.641 | 0.276 (1.397) | 1.318 |

| Policy2 | −0.795 (0.503) | 0.452 | 2.147 * (1.248) | 8.559 |

| Constant | 13.44 ** (6.315) | −6.943 (10.08) | ||

| Traditional_fuel (based outcome) | ||||

| Observations | 1467 | 1467 | ||

| LNG Capable | Methanol | Ready | Other Fuels | |||||

|---|---|---|---|---|---|---|---|---|

| Parameters | RRR | Parameters | RRR | Parameters | RRR | Parameters | RRR | |

| Nation (China) | −0.802 * (0.418) | 0.448 | −1.700 * (0.901) | 0.183 | −1.207 *** (0.327) | 0.299 | −2.727 *** (0.526) | 0.065 |

| Nation (Greece) | −1.435 *** (0.361) | 0.238 | −16.96 (1667) | 0 | −0.667 ** (0.271) | 0.513 | −16.52 (1086) | 0 |

| Nation (Japan) | −1.663 *** (0.586) | 0.190 | −1.480 (0.981) | 0.228 | −17.84 (1053) | 0 | −3.771 *** (0.875) | 0.023 |

| Nation (Singapore) | 0.0807 (0.407) | 1.084 | 0.912 (0.708) | 2.489 | −1.936 *** (0.551) | 0.144 | −1.146 * (0.644) | 0.318 |

| Nation (Republic of Korea) | −18.19 (1833) | 0 | −16.58 (3897) | 0 | −1.153 ** (0.470) | 0.316 | −17.40 (1715) | 0 |

| DWT 1 | 0.864 *** (0.141) | 1.009 | −0.373 (0.232) | 1.003 | 0.252 *** (0.0957) | 1.003 | −0.924 *** (0.176) | 0.991 |

| Earnings 1 | 0.525 * (0.302) | 1.005 | −4.804 ** (2.342) | 0.953 | −6.5e−04 (0.252) | 1.000 | −0.483 (0.450) | 1.005 |

| LNG/VLSFO | 0.303 (0.289) | 1.354 | 2.216 ** (0.959) | 9.171 | −0.416 (0.320) | 1.516 | 0.503 * (0.282) | 1.654 |

| SOFR | 0.0208 (0.168) | 1.021 | 3.090 ** (1.249) | 21.977 | 0.162 (0.148) | 1.176 | 0.596 *** (0.223) | 1.815 |

| Idle Rate | −0.995 ** (0.399) | 0.369 | −3.879 ** (1.837) | 0.021 | −0.0348 (0.304) | 0.966 | −0.422 (0.519) | 0.656 |

| CO2 Price 1 | −2.771 *** (1.004) | 0.973 | 4.359 (3.325) | 1.045 | −0.953 (0.834) | 0.991 | −1.692 (1.603) | 0.983 |

| Policy1 | 3.792 *** (0.920) | 44.345 | −2.997 (2.096) | 0.050 | 1.353 * (0.698) | 3.869 | −0.724 (1.508) | 2.063 |

| Policy2 | −0.742 (0.815) | 0.476 | −3.482 (3.357) | 0.031 | −0.137 (0.708) | 0.872 | 3.325 ** (1.420) | 28.560 |

| Constant | −11.50 ** (5.503) | 41.47 (28.05) | −0.0912 (4.549) | 17.38 ** (8.821) | ||||

| Traditional_fuel (based outcome) | ||||||||

| Observations | 890 | 890 | 890 | 890 | ||||

| LNG Capable | Methanol | Ready | ||||

|---|---|---|---|---|---|---|

| Parameters | RRR | Parameters | RRR | Parameters | RRR | |

| Nation (China) | −3.981 *** (0.805) | 0.019 | −1.698 *** (0.614) | 0.183 | 0.406 (0.351) | 1.501 |

| Nation (France) | 4.572 *** (0.472) | 96.737 | 3.309 *** (0.574) | 27.358 | −16.61 (4926) | 0 |

| Nation (Singapore) | 3.059 *** (0.448) | 21.306 | 2.690 *** (0.553) | 14.732 | 0.470 (0.777) | 1.600 |

| Nation (Italy) | 3.364 *** (0.487) | 28.904 | −17.00 (2428) | 0 | 1.032 (0.710) | 2.807 |

| Nation (Republic of Korea) | 0.821 (0.670) | 2.273 | 1.449 ** (0.593) | 4.259 | 2.636 *** (0.392) | 13.957 |

| Nation (Greece) | −0.787 (0.794) | 2.197 | −16.76 (1645) | 0 | 2.427 *** (0.379) | 11.325 |

| Nation (Germany) | 2.467 *** (0.572) | 11.787 | 1.405 (0.858) | 4.076 | 3.358 *** (0.409) | 28.732 |

| DWT 1 | 2.979 *** (0.274) | 1.030 | 2.008 *** (0.268) | 1.020 | 0.869 *** (0.146) | 1.009 |

| Earnings 1 | 3.338 *** (0.980) | 1.034 | 0.984 (1.052) | 1.010 | 1.552 ** (0.756) | 1.016 |

| LNG/VLSFO | 0.00525 (0.301) | 1.005 | 0.259 (0.308) | 1.296 | −1.890 *** (0.378) | 0.151 |

| SOFR | 1.134 *** (0.283) | 3.108 | 1.268 *** (0.291) | 3.554 | 0.429 ** (0.215) | 1.536 |

| Idle Rate | −1.053 *** (0.339) | 0.349 | −0.710 ** (0.341) | 0.492 | 1.401 *** (0.281) | 4.059 |

| CO2 Price 1 | −7.390 *** (1.374) | 0.929 | −6.028 *** (1.630) | 0.942 | −1.048 (1.083) | 0.989 |

| Policy1 | 2.704 *** (0.835) | 14.939 | 2.428 (1.985) | 11.336 | 0.356 (0.972) | 1.428 |

| Policy2 | 2.300 *** (0.881) | 9.974 | 3.55 *** (1.91) | 34.81 | 1.691 *** (0.577) | 5.425 |

| Constant | −42.90 *** (8.031) | −30.60 (1731) | −27.03 *** (6.089) | |||

| Observations | 1144 | 1144 | 1144 | |||

| Regression Model | LR chi2 | Prob > chi2 | −2 Log Likelihood | Pseudo R2 |

|---|---|---|---|---|

| Full sample model | 3854.57 | 0.00 | 5688.57 | 0.40 |

| Dry bulk model | 185.82 | 0.00 | 7765.62 | 0.21 |

| Container model | 1264.04 | 0.00 | 1219.92 | 0.51 |

| Tanker model | 399.53 | 0.00 | 1330.23 | 0.23 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Chen, S.; Wang, X.; Zheng, S.; Chen, Y. Exploring Drivers Shaping the Choice of Alternative-Fueled New Vessels. J. Mar. Sci. Eng. 2023, 11, 1896. https://doi.org/10.3390/jmse11101896

Chen S, Wang X, Zheng S, Chen Y. Exploring Drivers Shaping the Choice of Alternative-Fueled New Vessels. Journal of Marine Science and Engineering. 2023; 11(10):1896. https://doi.org/10.3390/jmse11101896

Chicago/Turabian StyleChen, Shun, Xingjian Wang, Shiyuan Zheng, and Yuantao Chen. 2023. "Exploring Drivers Shaping the Choice of Alternative-Fueled New Vessels" Journal of Marine Science and Engineering 11, no. 10: 1896. https://doi.org/10.3390/jmse11101896