1. Introduction

Agriculture is an engine of economic growth in developing countries, but the lack of access to formal credit for farm households remains a persistent problem that seriously hampers the development prospects of rural economies [

1]. The sustained supply of agricultural credit is challenging in most developing countries [

2], in large part because of the high risk of default and lack of sufficient assets as collateral for farmers to meet the prerequisites for formal credit [

3]. The Chinese government has been committed to promoting rural financial reform, and with the advancement of agricultural industrialization, standardized and large-scale agricultural industry chains are gradually being formed, and the radiation-driven effect of leading agricultural enterprises is increasing, which has a significant effect on both the production and financing activities of farmers. With the horizontal selection, supervision, and commercial incentive of core enterprises, agricultural industry chains can increase the credit of farmers [

4], and can improve the role of financial leverage in promoting the flow of financial factors to farmers and agriculture [

5], playing a significant role in actively promoting financial support to agriculture and improving the credit rationing problems of farmers. However, the current implementation of the agricultural industry chain is not as effective as expected; the problem of credit rationing for farmers is still serious, the availability of formal credit for farmers is still low, and the degree of self-exclusion of financial services for farmers is still high [

6]. Therefore, it is of great theoretical and practical significance to study the problem of farmer credit rationing from the perspective of the agricultural industry chain, analyzing the effect and its influence mechanism, and helping to promote financial support for rural industrial revitalization and agricultural modernization development.

The high risk and low profitability of agricultural operations themselves are the primary reasons why formal financial institutions are reluctant to lend to farmers [

7,

8],while high transaction costs induced by imperfect transaction mechanisms in rural credit markets mean that farmers usually face more severe credit rationing [

9]. The high risk and low profitability of agricultural operations themselves lead to high-income volatility and weak risk resistance among farmers in general; most farmers lack the collateral that meets the requirements of banks, and the rural credit market generally suffers from incomplete information and an inadequate credit evaluation system, which largely exacerbate the information asymmetry between farmers and financial institutions, making profit-oriented banks shy away from lending to farmers. In addition, factors such as cognitive bias, risk aversion, and demand repression from the demand side itself may also lead to the problem of credit rationing for farmers [

10,

11,

12]. On the one hand, the unsound information screening mechanism of financial institutions may send biased market signals to farmers who have borrowed money, resulting in cognitive biases meaning that farmers cannot obtain bank loans even if they apply for them, and voluntarily giving up applying for loans [

13]; on the other hand, most farmers have poor risk-taking ability, and the high credit transaction costs and loan rejection rates make some farmers with potential capital needs voluntarily give up their intention to expand their production through bank borrowing [

14]. Under the effect of both supply rationing and demand repression, the problem of credit rationing for farmers has widely existed for a long time, and the poor financing channels of agricultural financial resources have seriously hindered the transformation and upgrading of farmers’ large-scale operation and the development of the rural economy.

In the context of agricultural industrialization, the emergence of agricultural industry chains provides new ideas to improve the availability of credit to farmers and alleviate their financing dilemmas [

15]. The agricultural industry chain is a multi-linked linkage system based on planting and breeding links, and through the effective organization of agricultural production, operation and marketing links, the overall efficiency and value of the industry chain can be improved [

8]. Joining the agricultural industry chain is the main way to organically connect farmers with modern agriculture, which will inevitably have a significant effect on farmers’ production and operation and credit financing activities. Most of the current studies on the effect of agricultural industry chains on farmers focus on the effect of agricultural industry chains on farmers’ production and operation, and it is found that farmers joining agricultural industry chains can improve agricultural operation efficiency and reduce agricultural operation risks, and that there is a positive effect on alleviating the problem of loan difficulties [

16]. First, the vertically integrated business model of the agricultural industry chain can provide productive services such as production materials, production technology, and market information to farmers [

17,

18], increasing the production factor inputs and the average agricultural income per mu of farmers [

19]; second, the increased organization and production technology diffusion can enable farmers to obtain higher production technical efficiency [

20], which further significantly improves farm household income levels overall [

21]; finally, market-based management can also improve farmers’ market position and bidding ability, provide farmers with stable sales prices for agricultural products, and reduce the market risk of agricultural production [

22].

Some scholars have explored the effect of agricultural industrial chains on farmers’ financing from the perspectives of information asymmetry and credit transaction mechanism. Most studies found through theoretical analysis and case studies that agricultural industry chains can effectively alleviate information asymmetry, form a collateral substitution mechanism for farmers who cannot provide qualified collateral, reduce credit transaction costs, and play a positive role in both improving the overall value of the chain and alleviating farmers’ financing dilemmas through the information flow, logistics, and commercial credit formed by relying on real trading relationships [

16,

23,

24,

25]. Several studies have shown that the agricultural industry chain internal financing model, as a form of credit for endogenous market transactions, has various advantages, such as resolving information asymmetries and reducing transaction costs [

18], and is therefore a good alternative to formal credit; its internal financing model is the main source of credit access for farmers in many regions, and in some regions it is even the only source [

26]. Some other scholars have empirically tested the effects of agricultural industry chains through micro research data. He, Q. et al. (2013) [

27] found that there is a substitution relationship between intra-industrial chain financing and bank credit, which is an important channel for broadening farmers’ credit availability; Zhou, Y. et al. (2019) [

28] argued that joining agricultural industry chain organizations can effectively reduce transaction costs due to information asymmetry and imperfect contract implementation mechanisms, and thus improve farmers’ credit availability; Zou, J. et al. (2019) [

4] proposed that farmers can compensate for the deficiency of insufficient qualified collateral with the credit guarantee provided by the agricultural industry chain network, and that the supervision and incentive mechanism within the chain can improve the probability of farmers’ compliance and realize farmers’ credit enhancement, thus effectively solving farmers’ credit constraint problems.

Scholars’ studies have shown that joining agricultural industry chains can reduce the difficulty of credit risk management for financial institutions, improve the availability of credit for farmers, and have a positive effect on solving farmers’ credit problems. However, such studies have mostly identified credit supply-side factors as the main cause of farmers’ credit financing difficulties and examined the effect of joining agricultural industry chains on alleviating farmers’ financing difficulties caused by financial institutions’ “loan shyness”. However, demand-side rationing is the main form of credit rationing for most farmers in China [

29,

30], as the demand-side repressive behavior formed under long-term supply rationing may cause farmers who meet the credit requirements of banks to give up applying for loans, due to high interest rates, transaction costs, or risk costs [

10,

14]. To truly clarify the effect of joining the agricultural industry chain on the formal credit rationing of farmers and its mechanism of action, it is necessary to focus not only on supply-side factors but also on demand-side factors.

Based on the above analysis, using the micro-survey data from 991 farmers in Shaanxi Province, China, this paper empirically examines the effect of joining agricultural industry chains on farm credit rationing through probit and tobit models, and explores the specific underlying mechanisms that produce the effect. Compared with the existing research literature, the possible marginal contribution of this paper is mainly as follows: firstly, the credit rationing formed by farmers themselves is included in the analysis framework, and the effect of agricultural industry chains on farmers’ financing is investigated from two aspects, supply-based credit rationing and demand-based credit rationing, so as to clarify the real reasons why farmers are rationed out of the credit market and the effects of joining agricultural industry chains on various types of credit rationing of farmers. Secondly, the indicators of credit rationing factors are mostly selected based on the personal characteristics, economic characteristics and business characteristics of farmers, but there is a lack of characteristics of the credit enhancement mechanism of agricultural industry chains, and the selection of indicators of factors affecting farmers’ credit rationing is not targeted enough. In this paper, on the basis of fully analyzing the specific credit enhancement mechanism of agricultural industry chains for farmers, we introduce the characteristic variables related to the credit enhancement mechanism within agricultural industry chains as important control variables to test the specific mechanism of agricultural industry chains on credit rationing of farmers. Thirdly, we consider fully the influence of business scale on the credit rationing of farmers and conduct heterogeneity testing from this perspective to further expand the research on the effect of agricultural industry chain on farmers’ credit rationing problems.

2. Theoretical Analysis and Research Hypothesis

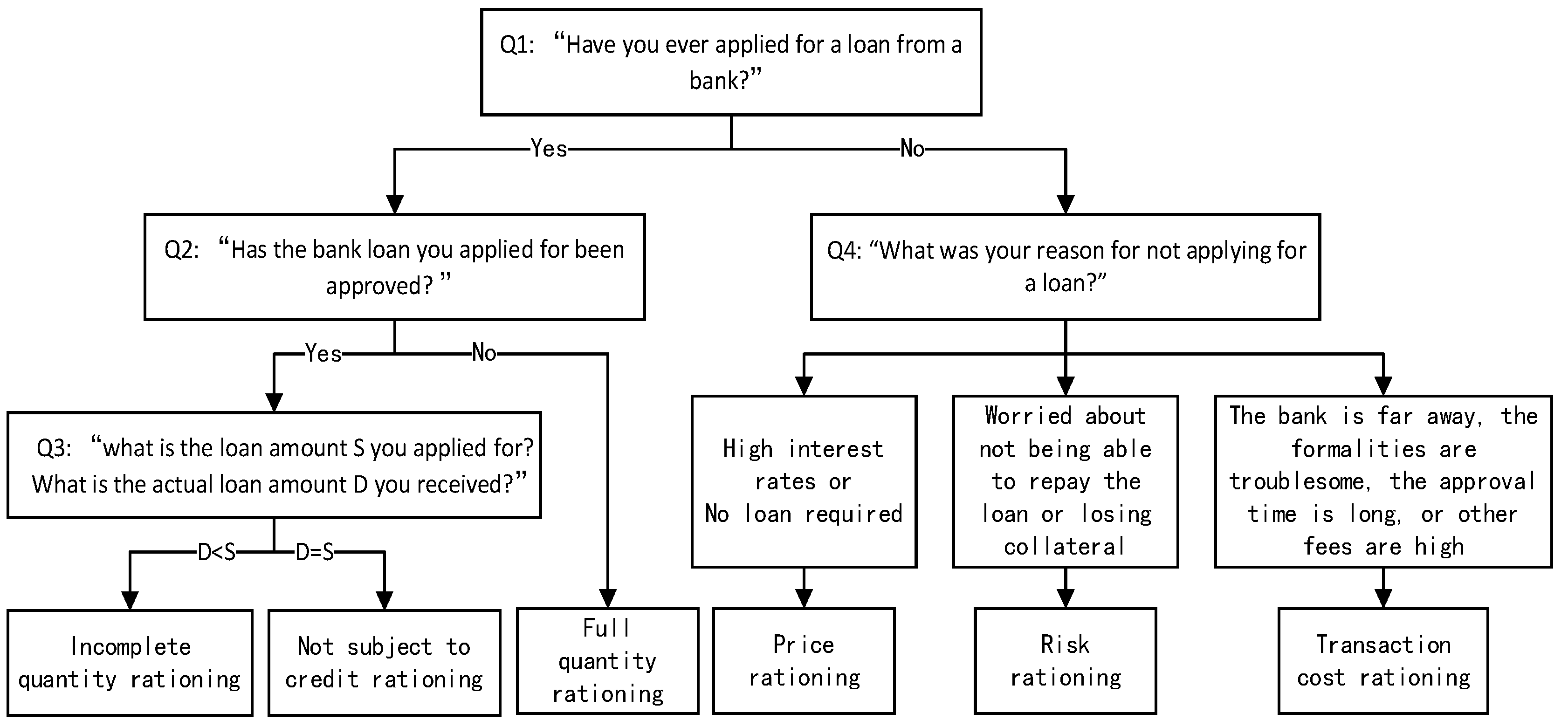

2.1. Farmers’ Credit Rationing Definition

Credit rationing is a phenomenon in which there is excess credit demand in the credit market due to interest rates below the level of market clearing [

31]. Scholars have different understandings of excess credit demand and different definitions of credit rationing. According to Stiglitz et al. [

32], a situation in which farmers’ formal credit demands cannot be met, and the credit rationing involved, consists of two scenarios: (1) from the bank’s point of view, some farmers with the same application conditions can obtain a loan, while some farmers are still denied loans even if they are willing to pay higher interest rates; (2) farmers receive fewer loans than they would like under the prevailing interest rate conditions, and cannot fail to meet the full demand for loans even if they are willing to pay higher interest rates.

Early studies mostly examined the credit rationing of financial institutions to borrowers from the supply perspective, taking quantity rationing as the only form of non-price credit rationing. With the depth of theoretical research, scholars found that, based on their demand repression, cognitive bias, and risk aversion, some borrowers with loan application conditions would actively withdraw from the credit market to form new credit rationing [

13], and that, in addition to supply-based quantity rationing, there existed two other forms of demand-based rationing, namely risk rationing and transaction cost rationing [

10]. Most of the later related studies classified farm credit rationing into two categories, supply-based rationing, and demand-based rationing, according to the different sources of credit rationing [

29,

30,

33].

Based on this, this paper classifies farmer credit rationing into supply-side and demand-side, and defines them as follows: (1) supply-based credit rationing is caused by supply-side decisions, mainly quantity rationing, which refers to the situation where a farmer’s loan application is directly rejected by the bank or cannot be fully satisfied; (2) demand-based credit rationing is caused by demand-side decisions, which can be classified into price rationing, transaction cost rationing, and risk rationing, according to specific reasons. Price rationing is when farmers give up applying for loans due to high interest rates or lack of investment opportunities and no capital needs; transaction cost rationing is when farmers give up applying for loans due to their unwillingness to bear non-interest costs (such as time costs, social costs, transportation costs, etc.); risk rationing is when farmers give up applying for loans due to their aversion to potential risks (risk of loss of credit, risk of loss of land, etc.). Risk rationing is a situation in which farmers give up applying for loans because they are averse to the potential risks of loans (risk of losing credit, risk of losing land, etc.).

2.2. Analysis of the Effect of Joining Agricultural Industry Chains on Supply-Based Credit Rationing for Farmers

Stiglitz and Weiss (1981) [

32] first included information asymmetry as a fundamental analytical tool in the analytical framework of neoclassical economics, and in the S-W model they developed, the bank’s expected return curve is non-monotonic, and when the interest rate increases to a certain level, the expected return falls instead. The presence of information asymmetry in the rural credit market makes it difficult for banks to identify the specific risk profile, and the bank risk increases with the interest rate; when banks make interest rate decisions, they do not choose to implement credit rationing at a level higher than the interest rate at which they perform optimal credit rationing. The S-W model suggests that adverse selection and moral hazard due to information asymmetry are the underlying reasons for banks implementing credit rationing. According to the principal–agent theory, if banks are unable to fully identify the potential risks of farmers and exercise complete supervision over farmers’ borrowing, the borrowing farmers may act in their interest to the detriment of banks, and the banks’ implementation of quantity rationing is a rational choice when the function of the interest rate clearing market is limited [

34]. In addition, the high-risk nature of agricultural operations and the weak quality of agriculture determine the high cost and risk of rural credit operations; in the face of farmers’ excess borrowing demand, the banks’ rational credit decision is to reduce credit supply and implement property-based credit rationing [

14]. While most farmers have average resource endowments and a lack of collateral that meets the banks’ requirements, this becomes another major obstacle for farmers obtaining bank credit support [

35]. Thus, the high risk of the agricultural operations and the lack of collateral for farmers exacerbate information asymmetry, and are the main reasons why farmers are subject to quantitative bank rationing, in which the agricultural industry chains have an important mitigating role.

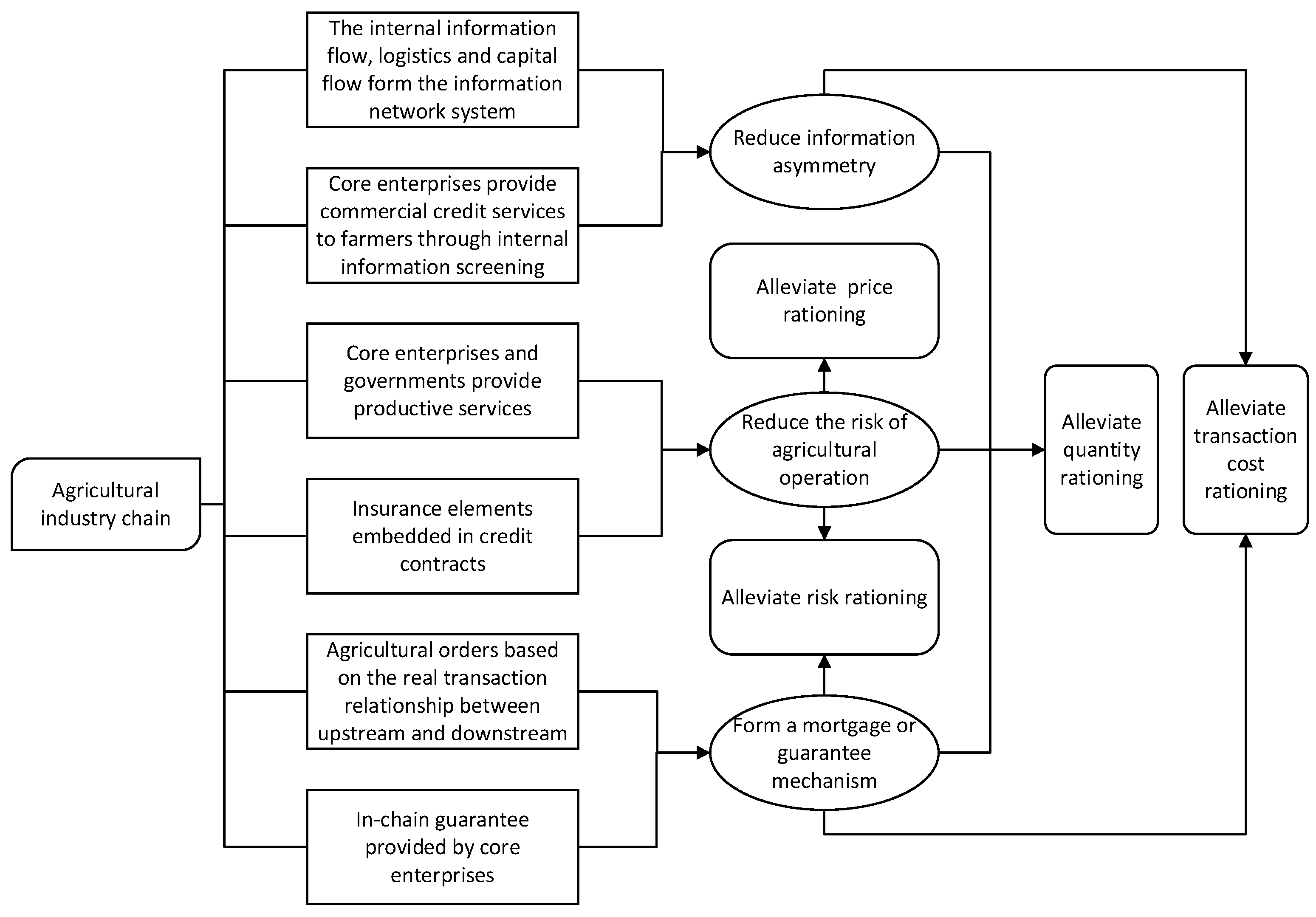

Firstly, the information network system and commercial credit formed by the agricultural industry chain can realize a certain degree of information sharing and alleviate the information asymmetry between farmers and banks. Unlike the traditional decentralized business model of small farmers, the agricultural industry chain is more organized, and the core enterprises can obtain information about the pre-production, production, and post-production stages of agricultural products through the vertically integrated business model of the industry chain; this can form an information network system within the agricultural industry chain [

28], with information screening and default risk control [

36]. Banks can rely on the core organization to obtain dynamic production and operation information from farmers, achieving continuous updating and the backward and forward verification of information, and avoiding adverse selection and moral hazard problems caused by information asymmetry [

37]. In addition, the core enterprises provide commercial credit services such as credit sales and advance payments, by screening and evaluating high-quality farmers through the information on farmers accumulated by their internal information networks. The essence of commercial credit is mutual trust between the two parties of the transaction, and banks can obtain soft information on credit such as farmers’ performance behavior, credit binding and signaling, and achieve a reciprocal relationship, with the help of the horizontal selection behavior of core enterprises [

4,

16], which can effectively alleviate the information asymmetry between the lending parties. This leads to the research hypothesis H1:

Hypothesis 1 (H1): Joining agricultural industry chains can reduce the degree of information asymmetry between farmers and banks, thus alleviating the quantitative rationing to which farmers are subjected.

Secondly, the agricultural industry chain can improve the availability of agricultural production services and insurance services for farmers, and effectively reduce agricultural business risks. Agricultural industry chains bundle the interests of core enterprises and farmers through the benefit linkage mechanism, help farmers obtain several agricultural social services such as pre-production agricultural products supply, mid-production technical information services, and post-production marketing services, motivate farmers to increase production inputs and adopt new technologies [

18], stabilize agricultural prices and improve the value of agricultural output [

38], and, on the whole, significantly improve the technical efficiency of agricultural operations and income [

21,

39] and reduce agricultural business risks. In addition, most credit contracts of agricultural industry chain financing models have embedded insurance elements, such as the introduction of commercial insurance institutions and the establishment of risk guarantee funds [

15], and it is easier for farmers to obtain insurance services when they join the agricultural industry chain. Agricultural insurance is an important tool for agricultural risk management and risk buffering [

40], which can strengthen farmers’ risk awareness, reduce the frequency and extent of losses from agricultural risks [

41], and help farmers quickly resume reproduction and reduce their business risks, by providing timely insurance compensation when risks occur [

42]. In summary, research hypothesis H2 is proposed:

Hypothesis 2 (H2): Joining agricultural industry chains can reduce the risk of farming operations, thus alleviating the quantitative rationing to which farmers are subjected.

Finally, agricultural orders and intra-chain guarantees formed by agricultural industry chains based on real transactions can generate effective collateral value and solve the problem of farmers’ lack of collateral. Agricultural orders of agricultural industry chains are incorporated into the category of important collateral, and farmers can obtain special loans from banks for acquiring production materials and organizing agricultural production through their stable and reliable contractual relationships with buyers [

43]. Agricultural orders can convey information about farmers’ repayment ability and their liquidation value to banks, thus forming collateral substitution and alleviating the farmers’ dilemma of being unable to obtain bank credit due to a lack of collateral [

28]. Farmers form interest linkage mechanisms with core enterprises of the agricultural industry chain through agricultural orders, and when they apply for loans from banks they can also obtain guarantees from cooperatives or leading enterprises based on contractual relationships, without providing other collateral; the guarantees provided by core enterprises are an effective way of breaking the problem of insufficient collateral for farmers at the front end of the industry chain [

15,

23]. Therefore, research hypothesis H3 is proposed:

Hypothesis 3 (H3): Joining the agricultural industry chain can form an effective collateral guarantee mechanism for farmers and alleviate the quantitative rationing to which they are subjected.

2.3. Analysis of the Effect of Joining Agricultural Industry Chains on Demand-Based Credit Rationing for Farmers

Drawing on the farm household modeling ideas of Guirkinger et al. [

7] and Cheng, Y. et al. [

14], the intensity of farm household credit demand depends largely on the expected rate of return on borrowing; farm households are motivated to apply for loans to expand production only when the expected return on borrowing exceeds the farm household’s unborrowed retained earnings. Suppose the original capital owned by the farm household is

K*,

K* = K + W, where

K is the productive capital of the farm household, including land and farm machinery, etc., and

W is the non-productive capital of the farm household, such as cars, properties, and other properties that can be used as collateral. Assume that the size of formal credit available to the farm household is

B,

B = f (W), and the loan interest rate is

r. The cost for the farm household to apply for a loan includes the interest cost

rB, and the credit transaction cost other than the interest

F. Assume that the production function of the farm household without a loan is

Y = Q(K,

L;

δ), where

L is the labor input and

δ is the farm household characteristics’ variables, including the farm household’s production and business capacity. After obtaining the loan, the farmer can make production investments such as expanding the scale of operation and making technological upgrades. The output level of successful investment is

YS, the output level of failed investment is

Yf, and

Yf < Y < YS. The risk level of the farmer’s investment in the production project is

θ. The project’s output return will not cover the principal and interest cost of the loan if the investment fails, and the farmer will also face losing the collateral property

W. Therefore, the farmer chooses to apply for a loan with the following conditions:

The left side of Equation (1) is the farm household’s return when applying for a loan, and the right side is the retained return when the farm household does not apply for a loan. When the above equation holds, the farm household has the incentive to apply for a loan. When the bank interest rate r and transaction cost F are fixed, the farmers’ willingness to apply for loans depends mainly on the left-hand side of the loan application return. When the farmers’ investment return Ys is relatively low or the level of agricultural investment risk θ is high, the farmers will actively give up applying for loans because the interest rate is too high, thus causing price rationing. According to the previous analysis, the participation of farmers in the agricultural industry chain can significantly improve the technical efficiency of agricultural operations and farmers’ returns on the whole, reduce the risk of agricultural operations, and thus alleviate the price rationing of farmers. Based on the above analysis, research hypothesis H4 is proposed:

Hypothesis 4 (H4): Joining agricultural industry chains can reduce the risk of farming operations, thus alleviating the price rationing to which farmers are subjected.

Due to information asymmetry, realistically it is difficult for banks to effectively screen the credit risk of the borrowing farmers. Assuming that the probability of a bank wrongly rejecting a good borrower due to information misjudgment is

p (0 <

p < 1

), then only

(1 −

p) valid borrowing farmers can obtain loans, at which point Equation (1) becomes:

From Equation (3), it can be seen that when the credit transaction cost F is too high, even though the benefits from applying for a loan may be higher than the retained benefits from not applying for a loan, farmers will actively give up applying for a loan because of the lower expected benefits from high transaction costs, thus forming transaction cost rationing. In addition, since 0 < p < 1, it can be seen that the misjudgment of bank information caused by information asymmetry will lead to higher loan application costs for farmers, which will further exacerbate the extent to which farmers implement self-rationing due to high transaction costs. From the previous analysis, it can be seen that agricultural industry chains can alleviate information asymmetry and form effective collateral and guarantee mechanisms, thus reducing the excessive transaction costs transferred to farmers by banks due to information asymmetry and insufficient collateral of farmers, and alleviating the transaction cost rationing suffered by farmers. Based on the above analysis, hypothesis H5 is proposed:

Hypothesis 5 (H5): Joining the agricultural industry chain can reduce the degree of information asymmetry and form an effective collateral guarantee mechanism, thus alleviating the transaction cost rationing suffered by farmers.

The risk of investment failure faced by the loan application causes loss of collateral and loss of creditworthiness, making farmers with risk-averse preferences demand a certain risk discount compensation

v (

v > 0); a certain amount of fixed wealth is needed to compensate for the uncertainty risk. Assuming that the farmer is risk averse to the risk faced by the loan application, then Equation (2) will become:

Since v > 0, it can be seen that the cost of a loan application by farmers who have considered risk discount compensation is further increased, and when farmers’ income after applying for loans cannot compensate for the risk discount required due to risk aversion, farmers will also actively give up applying for loans, thus causing risk rationing. From the previous section, it is clear that the agricultural industry chain can reduce the business risk of farmers; with the help of real trading relationships and reasonable contractual relationships between different subjects in the chain, effective collateral, and guarantee mechanisms are formed to share the agricultural credit risk and reduce the probability of farmers being subject to risk rationing. Based on the above analysis, hypothesis H6 is proposed:

Hypothesis 6 (H6): Joining the agricultural industry chain can reduce the risk of agricultural operations and form an effective collateral guarantee mechanism, thus alleviating the risk rationing to which farmers are subjected.

4. Result

4.1. Analysis of Regression Results of Supply-Based Rationing for Farmers

Before conducting the regression tests, to prevent the problem of multicollinearity between variables, this paper uses the variance inflation factor (VIF) to test the multicollinearity problem.

Table 4 shows the VIF test values for all explanatory variables from largest to smallest, with larger values of VIF indicating more severe covariance. The test results show that the maximum value of VIF is 1.33, which is less than the critical value of 10, and the mean value of VIF is 1.21, which is less than the critical value of 2. This fully indicates that there is no multicollinearity problem among the variables involved in the paper, and regression analysis can be conducted.

The regression results of the Heckman two-stage model are shown in

Table 5. The inclusion of agricultural industry chains positively affects the application of loans to farmers and negatively affects the quantity rationing of farmers at the 1% significance level, indicating that the inclusion of agricultural industry chains may reduce the probability of farmers being rationed from the demand side as well as the supply side, to some extent. Among these results, the

p-value of the inverse Mills ratio of the Heckman two-stage model is 0.28, which does not pass the significance test, indicating that the problem of self-selection bias in the sample may not exist. Therefore, the probit model is considered to continue the regression test for quantity rationing. The results of the probit regression on quantity rationing are shown in

Table 4. From the results, it can be seen that joining agricultural industry chains has a significant negative effect on the quantity rationing of farmers, and for every 1% increase in the probability of farmers joining agricultural industry chains, the probability of receiving quantity rationing decreases by 0.11%; joining agricultural industry chains has a significant positive effect on the number of loans received by farmers, and for every 1% increase in the probability of joining agricultural industry chains, the amount of loans received by farmers decreases by 0.11%. The number of loans received by farmers increased by CNY 196.26 for every 1% increase in the probability of joining agricultural industry chains. This indicates that joining agricultural industry chains can alleviate the quantity credit rationing of farmers from the supply side and improve the level of bank credit supply. This is consistent with the findings of Zhu, G. et al. (2022) [

46], which suggest that farmers’ participation in agricultural industry chains linked to core enterprises has a credit spillover effect that can increase financial institutions’ perception of farmers’ credit, which in turn has a catalytic effect on enhancing the credit size of farmers.

Among the significant control variables, the information system and commercial credit have a significant negative effect on quantity rationing, and every 1% increase in the probability that farmers are equipped with an information system decreases the probability that they are subject to quantity rationing by 0.13%. This indicates that the production and transaction information of a digital information platform effectively alleviates the information asymmetry between financial institutions and farmers, reducing the information identification cost before lending and the supervision cost after lending by financial institutions, and improving the probability of farmers being subject to quantity rationing: this is reduced by 0.22% for every 1% increase in the probability of farmers receiving commercial credit services. This further verifies the findings of Wu, B. et al. (2018) [

25], indicating that commercial credit has information advantages; core enterprises in the agricultural industry chain can use the advantages of localized information, industrial information, risk control, and low transaction costs to reduce the default risk of commercial credit ex ante and ex post, and screen out high-quality farmers, to achieve low-cost commercial credit services. These, in turn, can transmit farmers’ credit information to banks, and is a useful complement to the increase in farmers’ formal lending credit which can significantly reduce the degree of information asymmetry between farmers and banks and alleviate the quantitative rationing to which farmers are subjected, and the research hypothesis H1 is verified.

Production services have a significant negative effect on quantity rationing, indicating that farmers can improve their agricultural production, operation efficiency, and risk resistance by relying on the agricultural industry chain to obtain production and operation guidance and technical support from core enterprises, thus improving their solvency. The more production service support farmers receive, the better their agricultural operation management and development ability, and the easier it is to obtain bank loans; government support has a significant negative effect on quantity rationing, indicating that the government’s policy guidance and high level of support for the agricultural industry can enhance farmers’ confidence in technological upgrading and agricultural production and reduce agricultural business risks; agricultural insurance has a negative but insignificant effect on quantity rationing, probably because the development of the rural insurance business is not yet perfect and the risk-sharing effect of agricultural insurance is limited. Agricultural insurance has a significant positive effect on the loan amount, and every 1% increase in the probability of farmers purchasing agricultural insurance increases the number of loans obtained by CNY 120.37, indicating that agricultural insurance can improve farmers’ ability to cope with risks. The embedded insurance element in credit contracts can effectively share credit risks and help improve farmers’ ability to obtain loans. Therefore, the inclusion of agricultural industry chains can reduce agricultural risk and alleviate the quantitative rationing to which farmers are subjected, and the research hypothesis H2 is verified.

Agricultural orders have a negative but insignificant effect on quantity rationing, probably because there is currently no unified standard paradigm for agricultural orders, and it is difficult for contracts signed between farmers and agricultural enterprises or cooperatives to serve as a reference for banks’ lending, making the extent of alleviating quantity rationing limited. Agricultural orders have a significant positive effect on the loan amount; for every 1% increase in the probability that banks use agricultural orders as a basis for lending, the loan amount received by farmers increases by CNY 224.15, indicating that agricultural orders that meet banks’ lending conditions can be used as collateral substitutes to significantly increase farmers’ loan amount. Guarantee behavior has a significant negative effect on quantity rationing; for every 1% increase in the probability of core enterprises providing guarantees for farmers, the probability of farmers being subject to quantity rationing decreases by 0.07%, indicating that guarantees provided by core enterprises can form an effective collateral substitute and alleviate the probability of farmers being subject to quantity rationing. The positive but insignificant effect of guarantee behavior on loan amount may be because the number of farmers who can obtain guarantees from core enterprises is currently a minority, and the effect on enhancing farmers’ loan accessibility is insignificant. Therefore, the inclusion of agricultural industry chains can form effective collateral and guarantees for farmers and alleviate the quantitative rationing suffered by farmers, and the research hypothesis H3 is verified.

Among the other control variables, age has a significant negative effect on quantity rationing, which may be explained by the fact that as farmers get older, their agricultural productivity and solvency decrease significantly, and banks tend to lend to younger farmers to control default risk. Social capital has a significant negative effect on quantity rationing, which again confirms previous studies by scholars [

45], suggesting that relational lending is still prevalent in rural credit markets and that farmers with more social capital have a higher probability of receiving formal credit support through social network support. Age and education level have a significant positive effect on quantity rationing; household income and farmland area have a significant positive effect on quantity rationing, which indicates that large-scale farmers have a stronger demand for production funds and are more inclined to upgrade their production through formal borrowing; this also validates the study by Zhang, L. et al. (2018) [

9], indicating that currently, due to the restricted function of farmland management rights collateral, the access to formal credit of farmers with larger agricultural operations is not improved, and thus they are instead more vulnerable to quantity rationing from the supply side; total household assets and farmland cultivation area are significantly and positively related to the number of loans obtained by farmers. Total household assets and acreage of farmland are important reference factors for bank lending, and are also important collateral for farmers for applying for loans, which can increase the number of loans obtained by farmers. Past credit experience has a significant positive effect on quantity rationing, which is also in line with the basic logic that people who have credit experience and frequent contact with creditors have a better understanding of loan processes and policies, and are more likely to turn to banks when they encounter financial problems. Credit rating and past credit experience have a significant positive effect on the amount of loans farmers receive. Farmers with credit ratings or who have received bank loans before have a better understanding of their personal status and business situation, and the degree of information asymmetry is lower, which can improve the level of bank credit supply.

4.2. Analysis of Regression Results of Demand-Based Rationing for Farmers

The regression results of the probit model for demand-based rationing of farmers are shown in

Table 6, which shows that joining agricultural industry chains has a significant negative effect on demand-based rationing of farmers. As shown in

Table 7, the regression results of the probit model for each type of demand-based rationing of farmers show that joining agricultural industry chains has a significant negative effect on the price rationing, transaction cost rationing, and risk rationing of farmers. For every 1% increase in the probability of farmers joining agricultural industry chains, the probability of price rationing, transaction cost rationing, and risk rationing decreases by 0.20%, 0.13%, and 0.04%, respectively, indicating that, regardless of the reasons for farmers giving up loan applications, joining agricultural industry chains can increase farmers’ willingness to apply for loans and effectively alleviate credit rationing, due to demand-side reasons.

The regression results of different types of demand-based rationing in

Table 7 show that price rationing is significantly and negatively affected by production services and government support, and for every 1% increase in the probability of farmers receiving productive services and government support from core enterprises, the probability of being subject to price rationing decreases by 0.02% and 0.03%, respectively. This further confirms the study of Wu, B. et al. (2016) [

22], which shows that the participation of farmers in the agricultural industry chain with core enterprises helps them to obtain productive services and policy support, which has a significant positive effect on agricultural technology diffusion and production technology improvement. Thus, it can significantly reduce the agricultural business risk of farmers, which in turn increases their productive profitability expectations and investment intentions, and alleviates the price rationing to which farmers are subjected, and the research hypothesis H4 is verified.

Transaction cost rationing is significantly and negatively affected by information systems and agricultural orders, and for every 1% increase in the probability of having information systems and agricultural orders available as a reference for borrowing, the probability of farmers being subject to price rationing decreases by 0.09% and 0.19%, respectively. This further validates the study of Zhou, Y. et al. (2019) [

28], which shows that farmers’ participation in agricultural industry chains can rely on internal information network systems and core business organizations to more easily transmit their soft credit information to banks, which in turn can reduce the degree of information asymmetry. At the same time, it can form an effective collateral and guarantee credit enhancement mechanism by relying on the contractual relationship with the core enterprises or the guarantee provided by them. Therefore, it can significantly reduce the credit transaction costs between farmers and banks, and thus alleviate the transaction cost rationing to which farmers are subjected, and the research hypothesis H5 is verified. In addition, government support also has a significant negative effect on transaction cost rationing; with each 1% increase in government policy support for farmers’ production and operation, the probability of farmers being subject to price rationing decreases by 0.02%. This may be explained by the obvious policy orientation of China’s agriculture, in which strong government support can enhance confidence in agricultural production and operation, motivate banks to take the initiative to carry out credit operations, and reduce farmers’ application for loans transaction costs.

Risk rationing is significantly and negatively influenced by information systems, government support, and agricultural orders, and for every 1% increase in the probability of having information systems, government policy support for farmers’ production and operation, and agricultural orders as a reference for borrowing, the probability of farmers being subject to risk rationing decreases by 0.08%, 0.02%, and 0.07%, respectively. This further validates the findings of Liu, S. et al. (2019) [

20], indicating that farmers’ participation in the agricultural industry chain equipped with information systems and access to government support helps them obtain accurate market information and access to more advanced production technologies. These have significant effects on reducing both market risk and production risk, and can therefore reduce the potential risks that farmers need to bear when engaging in agricultural production and operation, thus reducing the probability that farmers will not apply for loans for fear that they will not be able to repay the loans, due to business failure. The agricultural orders signed between farmers and core enterprises or the guarantees obtained can form effective collateral substitution, which can also significantly reduce the probability of losing collateral and mitigate and compensate the risk of agricultural production and operation; thus, the risk rationing to farmers is alleviated, and the research hypothesis H6 is verified.

Among other control variables, age and the proportion of the labor force are significantly positively correlated with price rationing, which may be because older families with a large proportion of family labor often lack the motivation to expand agricultural production, are more sensitive to interest rates, and are more vulnerable to price rationing. The annual household income, land cultivation area, and production technology level are significantly and negatively correlated with price rationing, and new agricultural management subjects such as large-scale farmers or family farms with high annual household income, large land cultivation area, and high production technology have a strong willingness to invest in production, and are less likely to be subject to price rationing, due to high production efficiency and agricultural profitability; social capital is significantly and positively correlated with transaction cost rationing. The possible explanation is that farmers with rich social ties have more financing channel options and are more likely to give up formal borrowing applications due to high transaction costs; land cultivation area and production technology level are significantly and positively related to risk rationing, probably because professional farmers with high production technology and who are operating large land areas are more afraid of the risk of land loss and are more cautious about borrowing behavior; credit rating has a significant negative effect on price rationing, transaction cost rationing and risk rationing, indicating that the improvement in the rural credit evaluation system can significantly improve farmers’ willingness to finance. Past credit experience has a significant negative effect on price rationing and risk rationing, and a negative but insignificant effect on transaction cost rationing, indicating that farmers with borrowing experience are more inclined to turn to formal financial institutions to obtain loans when they encounter financial difficulties, and to actively give up borrowing from banks, and the probability of actively giving up lending from banks is relatively low.

4.3. Robustness Tests

Extreme values in the survey data can affect the stability of the estimation results, and to exclude the influence of extreme values this paper refers to the treatment of Li, Q. et al. (2018) [

47] and Sun, G. et al. (2021) [

48] to rank the sample farm households according to their household income, and exclude the samples whose household income is in the poorest 5% and the richest 5%. After the treatment, the OLS model and the logistic model regressions were conducted for loan amounts and various types of credit rationing, respectively, and the results are shown in

Table 8. After excluding the extreme values, it is still confirmed that the inclusion of an agricultural industry chain can effectively reduce the probability of farmers being subject to various types of credit rationing, which is consistent with the conclusion of the benchmark regression; the significance and direction of other important control variables also remain consistent with the results of the benchmark regression, indicating that the results are robust.

4.4. Heterogeneity Test

Since the effect of agricultural industry chains on the credit rationing of farmers of different operation sizes is heterogeneous, this paper divides farmers into small and large-scale farmers, based on their operation sizes, and conducts heterogeneity tests. The Chinese National Bureau of Statistics (NBS) defines large farmers as those with a planting area of 50 mu or more, and the sample farmers in this paper mainly grow cash crops such as apples or kiwis, which are three-to-five times more labor-intensive than food crops [

49], so farmers with a planting area of fewer than 10 mu are defined as small farmers and those with 10 mu or more are defined as large-scale farmers. The model regression results are shown in

Table 9 and

Table 10. They show that the inclusion of agricultural industry chains has a significant negative effect on both supply-based rationing and demand-based rationing for small and large-scale farmers, but that the credit rationing for large-scale farmers is mitigated to a deeper extent. This may be explained by the different credit values of agricultural industry chains for farmers of different cultivation scales and by the fact that large-scale farmers, compared with small farmers, have significant advantages in terms of production efficiency, marketing channels, and risk resistance. The effect of joining the agricultural industry chain on the demand-based rationing of small farmers is mainly reflected in price rationing and transaction cost rationing, while the effect on the demand-based rationing of large-scale farmers is mainly reflected in risk rationing; this may be explained by the fact that for small farmers, the small percentage of agricultural income has low returns, and, due to their insufficient demand, they are likely to be reluctant to bear the interest and excessive costs. The small-scale farmers are more likely to forgo loans, because they are unwilling to bear high-interest rates and costs, and are therefore subject to higher price rationing and transaction cost rationing; large-scale farmers are subject to higher risk rationing because of the higher value of their land assets and their greater control over production and investment decisions. The large-scale farmers have stronger productive investment demand, larger and more efficient credit demand, and can spread the fixed costs of credit transactions, so they are subject to lower price rationing and transaction cost rationing.

5. Discussion

In this study, we reveal the effects of joining agricultural industry chains on farmers’ credit rationing in terms of both supply and demand, and find that joining agricultural industry chains can significantly alleviate farmers’ supply-based quantity rationing and demand-based price rationing, risk rationing and transaction cost rationing. The specific mechanisms of agricultural industry chains on farmers’ credit rationing are also explored. It is found that agricultural industry chains can alleviate farmers’ quantity rationing by reducing information asymmetry, decreasing agricultural business risks and forming a collateral guarantee mechanism; alleviate farmers’ price rationing by reducing agricultural business risks; alleviate farmers’ transaction cost rationing by reducing information asymmetry and forming a collateral guarantee mechanism to alleviate farmers’ transaction cost rationing; and alleviate farmers’ risk rationing by reducing agricultural business risks and forming mortgage guarantee mechanisms. In addition, by introducing the characteristic variables of credit enhancement mechanisms within the agricultural industry chain, it is found that credit enhancement mechanisms such as information systems, commercial credit, orders, guarantees, productive services and government support in the agricultural industry chain have a significant effect on alleviating the credit rationing of farmers, and insurance has a limited effect on alleviating the credit rationing of farmers. Finally, by examining the alleviating effect of joining agricultural industry chains on credit rationing of farmers with heterogeneous in scale, it is found that joining agricultural industry chains has a more significant effect on alleviating supply-based and demand-based credit rationing for large-scale farmers compared to small farmers.

Joining agricultural industry chains has a significant alleviating effect on farmers’ supply-based quantity rationing, agreeing with numerous scholars’ findings [

16,

27,

46]. The conclusion that agricultural industry chains alleviate supply-based quantity rationing by farmers through reducing information asymmetry verifies the findings of Zhou, Y. et al. (2019) [

28], while the specific mechanism of agricultural industry chains affecting bank credit supply is expanded to suggest that agricultural industry chains can also alleviate the quantity rationing suffered by farmers by reducing agricultural business risks and forming collateral guarantee mechanisms. In contrast to Zhou, Y. et al. (2019) [

50], who conclude that agricultural industry chains have no significant effect on farmers’ demand-based credit constraints from a social capital perspective, we classify demand-based credit rationing into price rationing, transaction cost rationing, and risk rationing, according to their causes, and explore the specific mechanisms of agricultural industry chains for each type of demand-based credit rationing, arguing that agricultural industry chains also have a significant mitigating effect on farmers’ demand-based credit rationing. The heterogeneity test reveals that there is variability in the mitigation effect of agricultural industry chains on various types of credit rationing for large-scale heterogeneous farmers also verifies the findings of Zhu, G. et al. (2022) [

46], indicating that strengthening the role of industry chains in absorbing small farmers and optimizing financial services for agricultural industry chains should be the focus of policy choices.

Unlike the selection of indicators regarding credit-rationing influencing factors in the past, which were mostly based on the personal characteristics, economic characteristics and business characteristics of farmers [

11,

29,

30], to use a common-sense approach that distinguishes them from what is known from past studies, we introduced characteristic variables related to the credit enhancement mechanism within the agricultural industry chain as important control variables. These were based on the study of the specific credit enhancement mechanism of the agricultural industry chain, in order for farmers to verify the specific effects of information systems, commercial credit, production services, government support, agricultural insurance, agricultural orders, and guarantee behavior on credit rationing for farmers, to further clarify the objectives and key directions of financial innovation based on agricultural industry chains.

Of course, this study still has some flaws and limitations. Firstly, all the variables used in the empirical test were collected through questionnaire surveys of farmers. Although this method is often used in related studies and is widely accepted by academics, such a collection method may miss some more detailed and deeper information, which may lead to some systematic biases. In future studies, we can use a combined questionnaire survey of farmers and agricultural enterprises to obtain multidimensional indicator data to correct the systematic bias caused by this. Secondly, the paper focuses on the positive effects of agricultural industry chains on farmers’ credit rationing, while other possible effects, such as the threshold, enthusiasm and cooperative stickiness of farmers’ participation in agricultural industry chains, the benefit linkage distribution mechanism between small farmers and core enterprises of agricultural industry chains and the moral hazard in the game between the participants of agricultural industry chains, etc., quantify these influencing factors and incorporate them into the research framework of farmers’ credit rationing through various game models, which is the key focus of future research. Finally, future research should focus more on how to distinguish and compare in detail the advantages and disadvantages of various ways for farmers to join agricultural industry chains and their respective suitable geographical areas and types of agricultural operations, so as to provide sufficient theoretical guidance for the design and development of agricultural industry projects in different regions.

Nevertheless, this study provides some theoretical reference and a factual basis for deepening the reform of the rural financial system and giving full play to the effect of credit and financial funds in supporting and helping farmers by elaborating the influence of joining the agricultural industry chain on the credit rationing of farmers and analyzing the specific mechanism of the agricultural industry chain on the credit rationing of farmers. In the context of modernization of the agricultural industry, improving the financial system of agricultural industry chain, strengthening the radiation-driven role of core enterprises and innovating the financing mode of the agricultural industry chain are important strategic choices to strengthen financial services for rural revitalization in the new era.

6. Conclusions

6.1. Conclusions

Based on farmers’ research data, we study the effect of joining agricultural industry chains on different types of credit rationing of farmers, and analyze the effects and mechanisms of credit financing in agricultural industry chains of farmers, and obtain the following conclusions.

First, joining agricultural industry chains can increase farmers’ credit by reducing the degree of information asymmetry, reducing agricultural business risks, and forming collateral and guarantee mechanisms, thus alleviating the supply-based quantity rationing to which they are subjected.

Second, regardless of the reasons for farmers to give up their loan applications, joining agricultural industry chains can enhance farmers’ willingness to apply for loans and alleviate price rationing, risk rationing, and transaction cost rationing from the demand side.

Third, the credit enhancement mechanisms such as information systems, commercial credit, order, guarantee, productive service, and government support in the agricultural industry chain can significantly improve farmers’ credit and alleviate the supply-oriented and demand-oriented credit rationing of farmers.

Fourth, insurance elements embedded in credit contracts can effectively share credit risks and enhance farmers’ ability to obtain loans, but their effect in alleviating farmers’ credit rationing is limited, due to the current level of insurance development.

Fifth, the effect of agricultural industry chains on alleviating various types of credit rationing for farmers of heterogeneous scales varies. Compared with small farmers, the alleviation effect of joining agricultural industry chains on supply-based and demand-based credit rationing is more obvious.

6.2. Implications

Based on the research results of this paper, we provide the following policy implications.

First, the government should increase support for new business entities such as large-scale farmers, cooperatives and leading enterprises, encourage the establishment and development of cooperative economic organizations, and support leading agricultural enterprises. It should establish and improve the whole agricultural industry chain system in line with the characteristics of the local agricultural industry, give full play to the main role of leading agricultural enterprises and the driving role of farmers’ professional cooperatives, and encourage them to effectively provide production, technical and financial services for farmers.

Second, financial institutions should fully explore the credit-enhancing function of the agricultural industry chain and develop innovative credit products and financial services based on the structural characteristics of the agricultural industry chain and the financing needs of farmers of different cultivation scales. At the same time, they should strengthen the cooperation and interest linkage mechanism with the core enterprises of the agricultural industry chain, give full play to the guarantee role of agricultural credit, and strengthen the market-based sharing and compensation of credit risks related to agriculture, so as to enhance the strength and effectiveness of the banks’ financial support for the development of rural industries.

Third, government policies should establish a long-term mechanism to support the development of agricultural industry chains, and implement a full range of policy implementation measures to promote the integration of agricultural industry chains, value chains and capital chains. At the same time, government policies should fully exploit the invisible guarantee function for farmers’ credit, strengthen the supervision and regulation function for organizations of agricultural industrial chains, and bring into play the risk compensation function of supporting policies, to enhance the development resilience of agricultural industry chains.

Fourth, the government financial sector should actively develop the agricultural insurance and reinsurance business to promote the high-quality development of agricultural insurance. Based on the development of the agricultural industry chain, it should precisely design agricultural industry insurance products, improve the synergy mechanism between insurance and credit and, technology promotion and marketing, and give full play to the risk mitigation function of insurance for agricultural business risks. We will increase the support for policy insurance, expand the width and depth of agricultural insurance coverage, raise farmers’ awareness of insurance to increase the purchase rate and risk coverage of agricultural insurance, and optimize the risk protection function of insurance.

Fifth, farmers and core enterprises of the agricultural industry chain should strive to build standardized business management mechanisms in their production and operation, strengthen the construction of information technology platforms, and empower the modernization and development of rural industries with digital technology. They should actively develop the agricultural industry chain data center to provide a chain of information services such as agricultural product production, technical services, market information and disaster protection, to enhance risk response capability while improving information transparency with financial institutions.

{kind=link}

{kind=link}