An Analysis of the Pass-Through of Exchange Rates in Forest Product Markets

Abstract

:1. Introduction

2. Materials and Methods

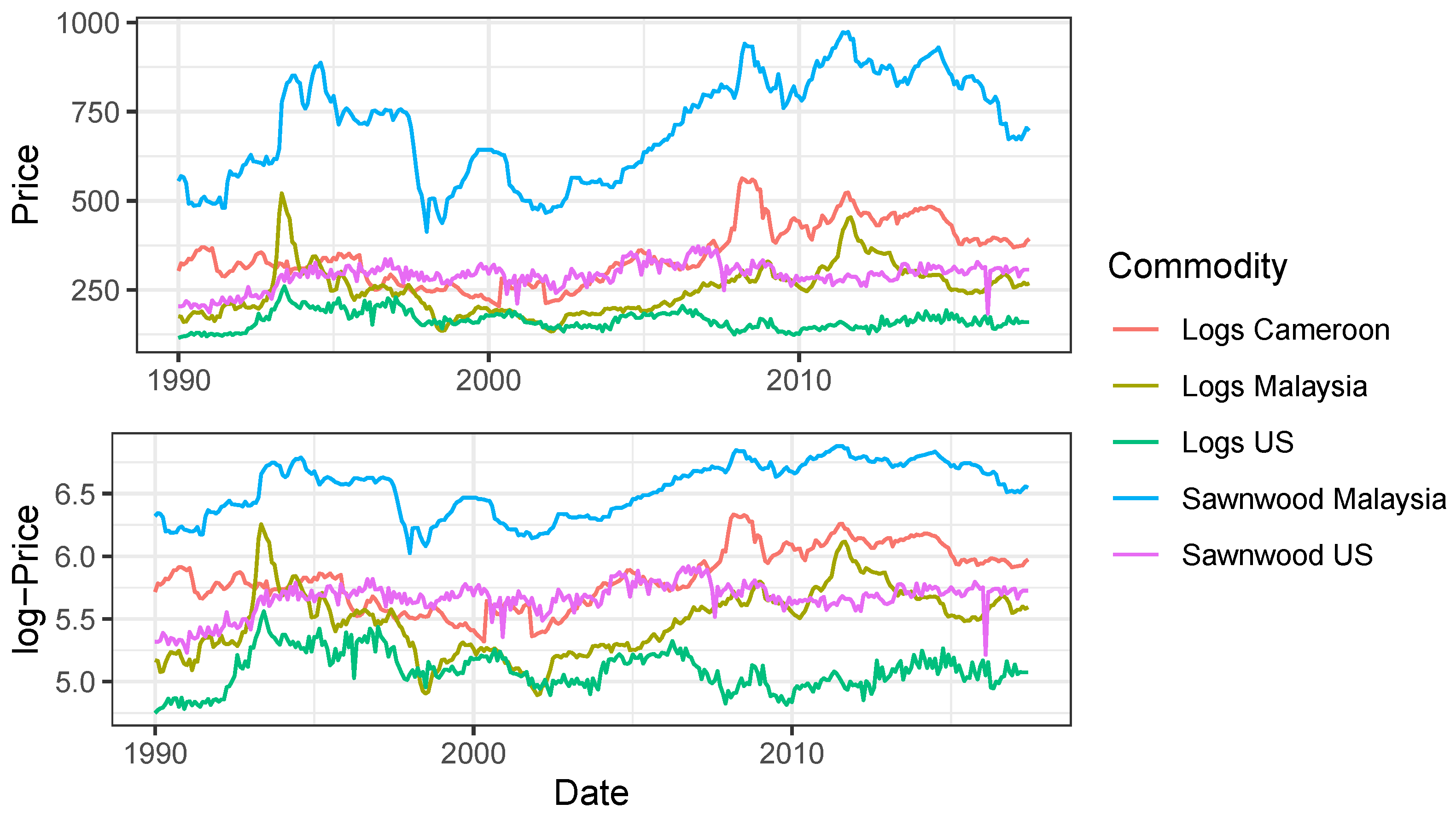

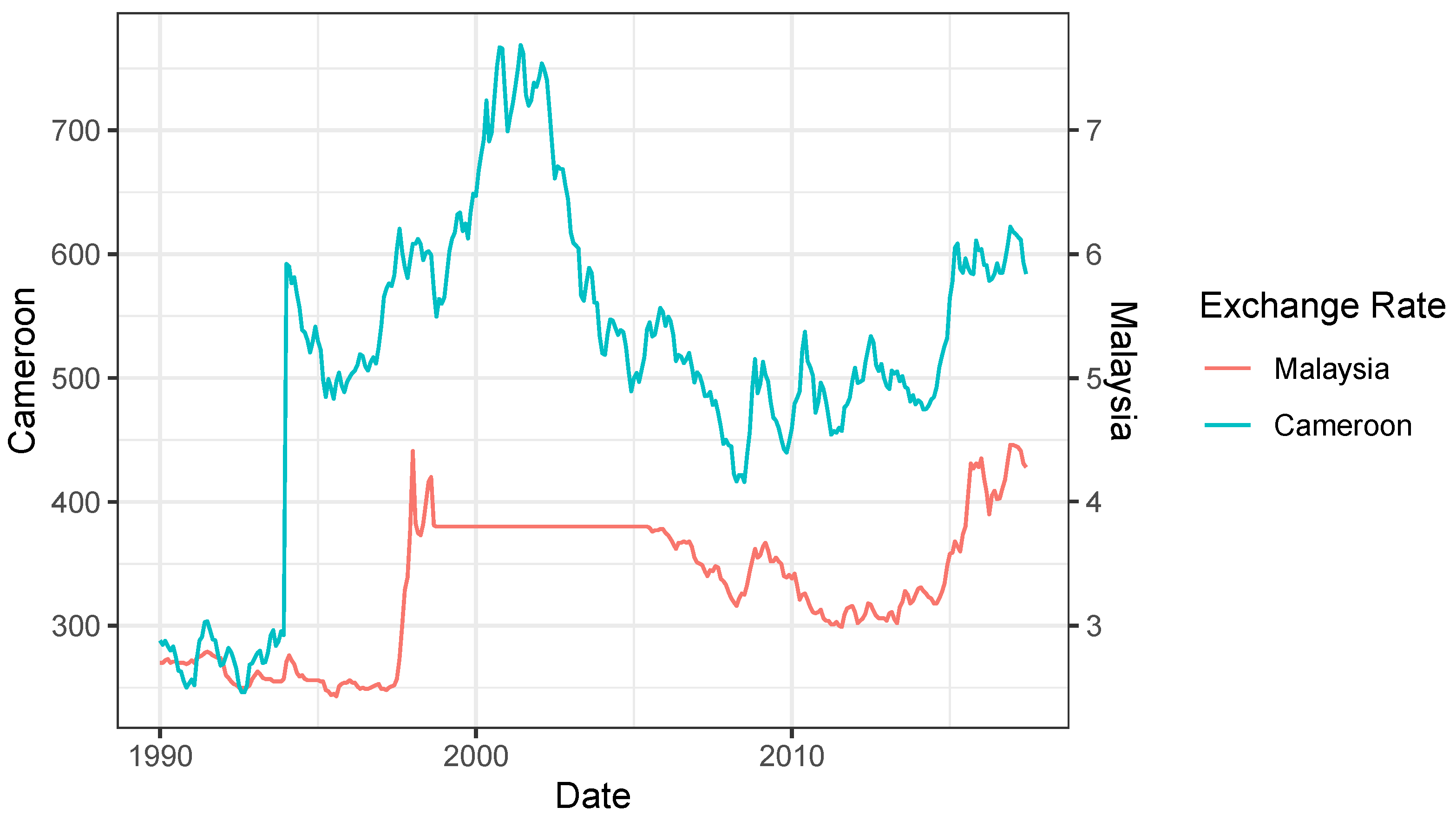

Data

3. Results

4. Discussion

5. Conclusions

Limitations and Future Direction

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Cameroon Timber Export Sarl. Africa’s Biggest Timber Exporter Countries. Available online: https://www.itto.int/biennal_review (accessed on 1 February 2023).

- ITC. List of Importing Markets for Wood Products Exported by the Central African Republic in 2021. Available online: https://www.trademap.org/Country_SelProductCountry_TS.aspx/ (accessed on 15 February 2023).

- Saghir, J.; Santoro, J. Urbanization in Sub–Saharan Africa Meeting Challenges by Bridging Stakeholders. Center for Strategic&International Studies. Available online: https://www.csis.org/analysis/urbanization-sub-saharan-africa (accessed on 15 February 2023).

- FLEGT IMM. Country Profiles Access to Latest Commentary on Timber Industries and Economies of EU and VPA Partner Countries. In FLEGT Independent Market Monitor. 2022. Available online: https://flegtimm.eu/country-profiles/central-african-republic/ (accessed on 6 February 2023).

- NEPCon. Supply Chain Mapping of Malaysian Timber and Wood–Based Industries; Report by NEPCon on behalf of WWF–Malaysia; NEPCon: Aarhus, Denmark, 2016; pp. 1–81. [Google Scholar]

- ITTO. Annual Report 2017; International Tropical Timber Organization: Yokohama, Japan, 2018; Available online: https://www.itto.int/biennal_review/ (accessed on 10 December 2022).

- Statista Research Department. Contribution of the Forestry and Logging Industry to the Gross Domestic Product (GDP) of Malaysia from 2016 to 2021. Available online: https://www.statista.com/statistics/953015/malaysia-forestry-and-logging-share-of-gdp// (accessed on 6 February 2023).

- European Timber Trade Federation. Gateway to International Timbertrade. Available online: https://www.timbertradeportal.com/countries/malaysia/ (accessed on 28 September 2018).

- US Forest Service Research and Development. Forest Products. Available online: https://www.fs.usda.gov/research/forestproducts (accessed on 29 July 2022).

- United States Department of Agriculture. U.S. Agricultural Trade Totals For November 2022. Foreign Agricultural Service 2022. Available online: https://apps.fas.usda.gov/gats/default.aspx (accessed on 6 February 2023).

- Anderl, C.; Caporale, G. Nonlinearities in the exchange rate pass–through: The role of inflation expectations. Int. Econ. 1974, 173, 86–101. [Google Scholar] [CrossRef]

- Goldberg, P.; Knetter, M. Goods Prices and Exchange Rates: What Have We Learned? J. Econ. Lit. 1997, 35, 1243–1277. [Google Scholar]

- Alola, U.; Usman, O.; Alola, A. Is pass through of the exchange rate to restaurant and hotel prices asymmetric in the US? Role of monetary policy uncertainty Uju Violet. Financ. Innov. 2023, 9, 18. [Google Scholar] [CrossRef] [PubMed]

- Caselly, F.; Roitman, A. Non–Linear Exchange Rate Pass-Through in Emerging Markets. IMF Work. Pap. 2016, 1, 1–36. [Google Scholar] [CrossRef]

- Durmaz, N.; Kagochi, J. Asymmetric Exchange Rate Pass–Through in Turkish Imports of Cocoa Beans. J. Risk Financ. Manag. 2022, 15, 184. [Google Scholar] [CrossRef]

- Goodwin, B.; Holt, M.; Prestemon, J. Nonlinear Exchange Rate Pass Through in Timber Products: The case of Oriented Strand Board in Canada and the United States. N. Am. J. Econ. Financ. 2019, 50, 100989. [Google Scholar] [CrossRef] [Green Version]

- Wiseman, T.; Luckstead, J.; Durand–Morat, A. Asymmetric Exchange Rate Pass–Through in Southeast Asian Rice Trade. J. Agric. Appl. Econ. 2021, 53, 341–374. [Google Scholar] [CrossRef]

- Deaton, A.; Laroque, G. Estimating a Nonlinear Rational Expectations Commodity Price Model with Unobservable State Variables. J. Appl. Econ. 1995, 10, S9–S40. [Google Scholar] [CrossRef]

- Tao, C.; Diao, G.; Cheng, B. The Dynamic Impacts of the COVID–19 Pandemic on Log Prices in China: An Analysis Based on the TVP-VAR Model. Forests 2021, 12, 449. [Google Scholar] [CrossRef]

- Lewandrowski, J.; Wohlgenant, M.; Grennes, T. Finished Product Inventories and Price Expectations in the Softwood Lumber Industry. Am. J. Agric. Econ. 1994, 76, 83–93. [Google Scholar] [CrossRef]

- Milas, C.; Legrenzi, G. Non–linear Real Exchange Rate Effects in the UK Labour Market. Stud. Nonlinear Dyn. Econom. Gruyter 2006, 10, 1–34. [Google Scholar] [CrossRef]

- Adewuyi, A.; Ogebe, J.; Oshota, S. The role of exchange rate and relative import price on sawnwood import demand in Africa: Evidence from modified heterogeneous panel data methods. J. Econ. Asymmetries 2021, 24, e00231. [Google Scholar] [CrossRef]

- Fan, R.; Talavera, O.; Tran, V. Information flows and the law of one price. Int. Rev. Financ. Anal. 2023, 85, 102466. [Google Scholar] [CrossRef]

- Holmes, M. The Response of Exchange Rate Pass–Through to the Macroeconomic Environment. Open Bus. J. 2009, 2, 1–6. [Google Scholar] [CrossRef]

- Teräsvirta, T. Specification, Estimation, and Evaluation of Smooth Transition Autoregressive Models. J. Am. Stat. Assoc. 1994, 89, 208–218. [Google Scholar]

- Teräsvirta, T. Modeling Economic Relationships with Smooth Transition Regression. In Handbook of Applied Economic Statistics; Marcel Dekker: New York, NY, USA, 1998; pp. 507–522. [Google Scholar]

- Bhat, J.; Nain, M.; Bhat, S. Exchange rate pass-through to consumer prices in India–nonlinear evidence from a smooth transition model. Int. J. Financ. Econ. 2022, 1–16. [Google Scholar] [CrossRef]

- Cheikh, N.; Younes, B. Revisiting the Pass–Through of Exchange Rate in the Transition Economies: New Evidence from New EU Member States. J. Int. Money Financ. 2020, 100, 102093. [Google Scholar] [CrossRef]

- Shintani, M.; Terada–Hagiwara, A.; Yabu, T. Exchange Rate Pass-through and Inflation: A Nonlinear Time Series Analysis. J. Int. Money Financ. 2013, 32, 512–527. [Google Scholar] [CrossRef]

- Hansen, B.E. Inference in TAR Models. Stud. Nonlinear Dyn. Econom. 1997, 2, 1–14. [Google Scholar] [CrossRef]

- Nogueira, R.; León–Ledesma, M. Does Exchange Rate Pass–through Respond to Measures of Macroeconomic Instability? J. Appl. Econ. 2011, 14, 167–180. [Google Scholar] [CrossRef] [Green Version]

- Cheikh, N. Non–linearities in Exchange Rate Pass–through: Evidence from Smooth Transition Models. Econ. Bull. 2012, 32, 2530–2545. [Google Scholar]

- Wu, P.; Liu, S.; Yang, M. Nonlinear Exchange Rate Pass–Through: The Role of National Debt. Glob. Econ. Rev. 2017, 46, 1–17. [Google Scholar] [CrossRef]

- Haggan, V.; Ozaki, T. Modeling Nonlinear Random Vibrations Using an Amplitude–Dependent Autoregressive Time Series Model. Biometrika 1981, 68, 189–196. [Google Scholar] [CrossRef]

- Tsay, R. Testing and Modeling Threshold Autoregressive Process. J. Am. Stat. Assoc. 1989, 84, 231–240. [Google Scholar] [CrossRef]

- Granger, C.; Teräsvirta, T. Modeling Nonlinear Economic Relationships; Oxford University Press: Oxford, UK, 1993; pp. 1–198. [Google Scholar]

- Tong, H. Nonlinear Time Series Analysis. In International Encyclopedia of Statistical Science; Lovric, M., Ed.; Springer: New York, USA, 2012. [Google Scholar]

- Baharumshah, A.; Habibullah, M. The Efficiency of the Spot Foreign Exchange Market: Evidence from the Malaysian Currency Market. In Proceedings of the Third Malaysian Econometric Conference, Kuala Lumpur, Malaysia, 14 June 1995. [Google Scholar]

- Bolkesjo, T.F.; Buongiorno, J. Short and Long-run Exchange Rate Effects on Forest Product Trade: Evidence from Panel Data. J. For. Econ. 2006, 11, 205–221. [Google Scholar] [CrossRef]

- Hänninen, R.; Craig, S.; Toppinen, A. Long–run Price Effects of Exchange Rate Changes in Finnish Pulp and Paper Exports. Appl. Econ. 1999, 31, 947–956. [Google Scholar] [CrossRef]

- Hänninen, R.; Craig, S.; Toppinen, A. EMU and Forest Products Pricing in Europe; Western Agricultural Economics Association Annual Meetings: Vancouver, BC, Canada, 2000. [Google Scholar]

- Powers, W.; Riker, D. Exchange Rate Pass–through in Global Value Chains: The Effects of Upstream Suppliers; U.S. International Trade Commission Office of Economics Working Paper; U.S. International Trade Commission: Washington, DC, USA, 2013; pp. 1–21.

- Tutueanu, G. Measuring the Influence of the J–Curve Effect on Trade in Romanian Forest Products. Ecoforum J. 2015, 4, 75–84. [Google Scholar]

- Terheggen, A. The Tropical Timber Industry in Gabon: A Forward Linkages Approach to Industrialization. MMCP Discuss. Pap. 2011. [Google Scholar]

- Güney, S. An Analysis of the Pass–Through of Exchange Rates in Tropical Forest Product Markets: A Smooth Transition Approach. In Proceedings of the 2015 AAEA & WAEA Joint Annual Meeting, San Francisco, CA, USA, 26 July 2015. [Google Scholar]

- Balagtas, J.; Holt, M. The Commodity Terms of Trade, Unit Roots, and Nonlinear Alternatives: A Smooth Transition Approach. Am. J. Agric. Econ. 2009, 91, 87–105. [Google Scholar] [CrossRef] [Green Version]

- Enders, W.; Holt, M. Sharp Breaks or Smooth Shifts? An Investigation of the Evolution of Commodity Prices. Am. J. Agric. Econ. 2012, 94, 659–673. [Google Scholar] [CrossRef] [Green Version]

- Cheikh, N.B.; Zaied, Y.B.; Houssam, B.; Pascal, N. Nonlinear Exchange Rate Pass–Through: Does Business Cycle Matter? J. Econ. Integr. 2018, 33, 1235–1260. [Google Scholar] [CrossRef] [Green Version]

- Goodwin, B.; Holt, M.; Prestemon, J. North American Oriented Strand Board Markets, Arbitrage Activity and Market Price Dynamics: A Smooth Transition Approach. Am. J. Agric. Econ. 2011, 93, 993–1014. [Google Scholar] [CrossRef] [Green Version]

- Chambers, R.; Just, E. A Critique of Exchange Rate Treatment in Agricultural Trade Models: Reply. Am. J. Agric. Econ. 1980, 62, 255–259. [Google Scholar] [CrossRef]

- Franses, P.; van Dijk, D. Non–Linear Time Series Models in Empirical Finance; Cambridge University Press: Cambridge, UK, 2000; pp. 1–280. [Google Scholar]

- Buncic, D. Identification and Estimation Issues in Exponential Smooth Transition Autoregressive Models. Oxf. Bull. Econ. Stat. 2019, 81, 667–685. [Google Scholar] [CrossRef]

- US Bureau of Labor Statistics. Producer Price Index by Commodity: Lumber and Wood Products: Plywood [WPU083()]. FRED, Federal Reserve Bank of St. Louis. Available online: https://fred.stlouisfed.org/series/WPU083 (accessed on 4 January 2021).

- Leamer, E. Housing IS the Business Cycle. In NBER Working Papers 13428; National Bureau of Economic Research, Inc: Cambridge, MA, USA, 2007; pp. 1–72. [Google Scholar]

- Stock, J.; Watson, M. How Did Leading Indicator Forecasts Perform During the 2001 Recession? FRB Richmond Econ. Q. 2003, 89/3, 71–90. [Google Scholar]

- Weinstock, L. Introduction to U.S. Economy: Housing Market. CRS In Focus IF11327. Available online: https://crsreports.congress.gov/product/pdf/IF/IF11327/10 (accessed on 4 January 2021).

- FAO/UNECE. Forest Products Annual Market Review 2003–2004. Timber Bulletin; FAO/UNECE: Geneva, Switzerland, 2004; pp. 1–71. [Google Scholar]

- S&P Dow Jones Indices LLC. S&P/Case–Shiller 20–City Composite Home Price Index [SPCS20RSA()]. FRED, Federal Reserve Bank of St. Louis. Available online: https://fred.stlouisfed.org/series/SPCS20RSA (accessed on 4 January 2021).

- Teräsvirta, T.; Lin, C.; Granger, C. Power of the Neural Network Linearity Test. J. Time Ser. Anal. 1993, 14, 209–220. [Google Scholar] [CrossRef]

- Lee, T.; White, H.; Granger, C. Testing for Neglected Nonlinearity in Time Series Models. J. Econ. 1993, 56, 269–290. [Google Scholar] [CrossRef]

- Keenan, D. A Tukey nonadditivity–type Test for Time Series Nonlinearity. Biometrika 1985, 72, 39–44. [Google Scholar] [CrossRef]

- McLeod, A.; Li, W. Diagnostic Checking ARMA Time Series Models Using Squared Residual Autocorrelations. J. Time Ser. Anal. 1983, 4, 269–273. [Google Scholar] [CrossRef]

- Tsay, R. Nonlinearity Test for Time Series. Biometrika 1986, 73, 461–466. [Google Scholar] [CrossRef]

- Chan, K. Percentage Points of Likelihood Ratio Tests for Threshold Autoregression. J. R. Stat. Soc. B 1990, 53, 691–696. [Google Scholar] [CrossRef]

- Engle, R.; Granger, C. Co–Integration and Error–Correction: Representation, Estimation, and Testing. Econometrica 1987, 55, 251–276. [Google Scholar] [CrossRef]

- Banerjee, A.; Dolado, J.J.; Galbraith, J.W.; Hendry, D.F. Cointegration, Error Correction, and the Econometric Analysis of Non–Stationary Data; Oxford University Press: Oxford, UK, 1993. [Google Scholar]

- Akaike, H. A New Look at the Statistical Model Identification. IEEE Trans. Autom. Control 1974, 19, 716–723. [Google Scholar] [CrossRef]

- Schwarz, G. Estimating the Dimension of a Model. Ann. Stat. 1978, 6, 461–464. [Google Scholar] [CrossRef]

- Shibata, R. Selection of the Order of an Autoregressive Model by Akaike’s Information Criterion. Biometrika 1976, 63, 117–126. [Google Scholar] [CrossRef]

- Hannan, E.; Quinn, B. The Determination of the Order of an Autoregression. J. R. Stat. Soc. Ser. 1979, 41, 190. [Google Scholar] [CrossRef]

- Goodwin, B.; Piggott, N. Spatial Market Integration in the Presence of Threshold Effects. Am. J. Agric. Econ. 2001, 83, 302–317. [Google Scholar] [CrossRef] [Green Version]

- Juvenal, L.; Taylor, M. Threshold Adjustment of Deviations from the Law of One Price. Stud. Nonlinear Dyn. Econom. 2008, 12, 1–44. [Google Scholar]

- Koop, G.; Pesaran, M.; Potter, M. Impulse Response Analysis in Nonlinear Multivariate Models. J. Econom. 1996, 74, 119–147. [Google Scholar] [CrossRef]

- Ghalanos. Twinkle: Dynamic Smooth Transition ARMAX Models, R package Version 0.9–3. 2009.

- Uusivuori, J.; Buongiorno, J. Pass–Through of Exchange Rates on Prices of Forest Product Exports from the United States to Europe and Japan. For. Sci. 1991, 37, 931–948. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

| Logs | Logs | Logs | Sawnwood | |

|---|---|---|---|---|

| Cameroon | Cameroon | Malaysia | Malaysia | |

| Prices | ||||

| Logs Malaysia | *** | |||

| Logs USA | *** | *** | ||

| Sawnwood USA | *** | |||

| Exchange Rates | ||||

| Cameroon | *** | *** | ||

| Malaysia | *** | |||

| R | ||||

| Adj. R | ||||

| Num. obs. | 330 | 330 | 330 | 330 |

| Teräsvirta | White | Keenan | McLeod-Li | Tsay | LR-Threshold | |

|---|---|---|---|---|---|---|

| (Logs Cameroon/Logs Malaysia): | . | |||||

| (Logs Cameroon/Logs US): | . | |||||

| (Logs Malaysia/Logs US): | . | |||||

| (Sawnwood Malaysia/Sawndwood US): | . | |||||

| Level | First Difference | |||||||

|---|---|---|---|---|---|---|---|---|

| log–Ratio | ADF Test | PP Test | ADF Test | PP Test | ||||

| Statistic | p-Value | Statistic | p-Value | Statistic | p-Value | Statistic | p-Value | |

| Logs Cameroon/Logs Malaysia | <0.01 | <0.01 | <0.01 | |||||

| Logs Cameroon/Logs US | <0.01 | <0.01 | ||||||

| Logs Malaysia/Logs US | <0.01 | <0.01 | ||||||

| Sawnwood Malaysia/Sand wood US | <0.01 | <0.01 | ||||||

| Price (Domestic/Foreign) | EG Statistic | p-Value |

|---|---|---|

| Logs Cameroon/Logs Malaysia | ||

| Logs Cameroon/Logs US | >0.100 | |

| Logs Malaysia/Logs US | ||

| Sawnwood Malaysia/Sawnwood US | >0.100 |

| Parameter | Logs Cameroon | Logs Cameroon | Logs Malaysia | Sawnwood Malaysia |

|---|---|---|---|---|

| Logs Malaysia | Logs US | Logs US | Sawnwood USA | |

| (1) | (2) | (3) | (4) | |

| *** | *** | *** | ||

| *** | *** | |||

| *** | ||||

| *** | *** | *** | ||

| *** | *** | *** | ||

| c | *** | *** | *** | *** |

| *** | *** | *** | *** | |

| LogL | ||||

| Akaike | ||||

| Bayes | ||||

| Shibatta | ||||

| Hannan–Quinn | ||||

| R-Squared | ||||

| R-Squared (adj) | ||||

| RSS | ||||

| Skewness (res) | ||||

| Ex.Kurtosis (res) |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Güney, S.; Riquelme, A.; Goodwin, B. An Analysis of the Pass-Through of Exchange Rates in Forest Product Markets. Agriculture 2023, 13, 515. https://doi.org/10.3390/agriculture13030515

Güney S, Riquelme A, Goodwin B. An Analysis of the Pass-Through of Exchange Rates in Forest Product Markets. Agriculture. 2023; 13(3):515. https://doi.org/10.3390/agriculture13030515

Chicago/Turabian StyleGüney, Selin, Andrés Riquelme, and Barry Goodwin. 2023. "An Analysis of the Pass-Through of Exchange Rates in Forest Product Markets" Agriculture 13, no. 3: 515. https://doi.org/10.3390/agriculture13030515