1. Introduction

Agricultural production is a risky activity, especially financially, for agribusinesses, which are wary of proposals to insure their crops, vegetables and orchards, believing that the cost of insurance is pointless, and insurance money may find a much more appropriate application. However, it is possible that, due to unforeseen and unplanned cases, farming incomes may become more unstable and unpredictable in coming years. The frequency of adverse weather events and the resulting economic losses have steadily increased over the past few decades [

1]. Agriculture has been recognized as particularly sensitive to climate change [

2]. Forecasts for the future also show that farmers in many parts of the world will face increasingly difficult agricultural production conditions with warmer environments, pest invasion, increasingly irregular rainfall and more frequent extreme natural events [

3], and an increasing number of countries around the world will face food shortages and the need to import it [

4]. Thus, climate change is clearly detrimental both to the world’s population and to farmers in all areas of agriculture, and these conditions are not subject to natural risk factors. Farmers feel the instability of their activities due to the potential loss of income; the risk of income planning alone increases due to the above-mentioned challenges. The global climate in particular tends to increase the losses of agribusinesses [

5], so well-developed crop insurance activities may be the only way to cover unplanned losses, at least partially [

6]. Public sector (state) institutions are also involved in material damage compensation activities, allocating budget funds to cover losses incurred by farmers, although these funds are also required by other state activity entities. This situation affects the viability of insurance systems and challenges the inefficient use of public sector funds, as it increases the unplanned costs of protection and losses of both the public and private insurance sectors [

7]. Direct support from public authorities to agriculture does not encourage the insurance of agricultural holdings; the demand for this service is low, and public authorities’ funds for agricultural compensation could find a much more efficient application [

8].

Insurance risk is borne by both the insurer and the policyholder. According to Falco et al. [

3] and other researchers, the role of insurance in agriculture is the focus of both researchers and politicians, as well as in research on the possibility for public authorities to participate in the insurance system. Additionally, the possibilities of crop insurance in the European Union have not been studied in a comprehensive way; only fragmentary research results are presented, the application of which does not encourage the development of insurance services. Therefore, there is a clear need for an understanding real structure of crop insurance system and to find the best solutions of public authorities in order to activate insurance performance in agriculture [

8]. We want to suggest the technique of identifying opportunities for the crop insurance system development based on the best public authority solution for finding the direction of development. Currently, public authorities do not have a methodology, they do not know the best directions for influencing (encouraging) the crop insurance process, and it is not only a scientific but a political problem for many countries. The majority of publications describe Asian countries’ crop insurance systems [

9,

10,

11,

12]. Additionally, they only explain the process of crop insurance or focus on the benefits of crop insurance. Other authors describe functions of crop insurance elements [

13,

14,

15,

16]

The use of a methodology for the determination of the best solutions of public authorities in order to activate crop insurance system development would help to find the best conditions to promote the insurance service among farmers. A methodology would also help insurance companies to properly expand and promote some business activities according to the priorities of agriculture. So, the aim of the article is to present a methodology for assessing substantiated aims of activity for public authorities in order to create a more active crop insurance system performance. A description of the crop insurance system components and a determination of the relations between these components based on scientific arguments in the article are necessary. The research results would be applicable not only in Lithuanian agriculture, but in other countries as well, because Lithuanian crop insurance activity has had much success in this field.

2. Materials and Methods

From an organizational point of view, the system is described as a set of linked institutions or production units as a whole [

14]; hence, in order to describe the insurance system, it is first necessary to determine the participants and their functions and dependencies. According to the above-mentioned description of insurance activities, the insurance system should also include relations between participants in insurance activities [

14].

The insurance system can be broadly described as an integrated whole of motivated economic entities involved in processes aimed at ensuring financial stability and linked by interdependencies and operating in the insurance market in accordance with certain established procedures [

16]. Insurance activity is a special system of monetary relations between insurers, policyholders and, where appropriate, intermediaries, arising from the selling and purchasing of insurance services, paying contributions (premiums) to insurers and providing the payment of benefits to insurance policyholders from a fund formed in insurance companies, which allows the insurance interests of natural and legal persons (insurance protection) to be ensured and to form the financial basis for the specific business of insurers and reinsurers [

17].

Insurance activities are strictly controlled, licensed and supervised in accordance with the law on insurance of the country. The regulation, management and supervision of the crop insurance market are generally the responsibility of the public authorities concerned. In Lithuania, such activities are carried out by the Supervisory Department of the Bank of Lithuania, and the reimbursement of insurance premiums, accounting and the distribution of funds are handled by the Ministry of Agriculture of the Republic of Lithuania. We will call all these public organizations public authorities, and this participant of the crop insurance market is named the first component of the insurance system. Its activities are aimed at ensuring that insurance companies, which are usually for-profit insurance companies, have sufficient funds to pay insurance benefits and have qualified and reliable managers who smoothly organize the activities of the insurance company and comply with the Bank of Lithuania Supervision Department and other state regulations.

Thus, another participant in the insurance market, as a component of the insurance system, would be the object of the supervisory department of the Republican Bank—insurance companies (insurer, insurance broker, insurance intermediary or reinsurer). Insurer—a legal person, who has the right to perform insurance activities in accordance with the procedure established by legal acts. Reinsurer—an insurance or reinsurance company which takes over part of the risk from another insurance or reinsurance company [

18]. The insurer usually carries out (or can carry out) its activities through intermediaries: insurance brokers, consultants who are closest to the object of insurance, know best and understand their needs [

19]. Distribution channels of insurance products are available by contacting the insurer (insurance company) or the insurance intermediary directly [

16]. It has already been mentioned that an insurance intermediary—an intermediate link between an insurance service provider (insurance company) and an insurance service recipient (policyholder, insured)—is not a legally necessary link, but is attractive and frequently used by consumers [

20]. Insurance intermediaries typically receive a fee for mediation (commission) from insurance companies [

21]. Insurance intermediation activities consist not only of the moment of concluding the contract, but also by providing assistance to insurance service users in choosing the insurance company, the most optimal insurance conditions and price. Insurance intermediaries (brokers) can also administer insured events, advise and represent the interests of policyholders in relations with other components of the insurance system [

21].

Thus, insurance intermediaries can also be considered a component of the insurance system, the success and intensity of which largely determine the performance of insurance companies. By interacting with each other, they try to balance the supply and demand of insurance services.

In order for insurance activities to be successful, the other most important market player is the policyholder. The policyholder is a person (can be both legal and natural) who has applied to the insurer for the conclusion of an insurance contract or to whom the insurer has offered to conclude an insurance contract, or who has already concluded an insurance contract with the insurer [

14]. Continuing the idea of banning crops, vegetables or orchards, farmers who grow crops, vegetables or orchards can be identified as policyholders, who usually face crop losses due to meteorological phenomena.

The state of the crop insurance system is largely determined by the relationships between the components of the system, so in order to further analyze its development, these relationships cannot be left out, as the influence of the components on each other may even affect the solutions for public authorities and insurance company. Our decision is determined by the definition of a system, which states that a system cannot be understood only by analyzing its individual components [

14], because their interaction creates a new quality—a synergistic effect, when the whole is greater than the sum of its parts. Systems theory emphasizes that what matters is not how the components of a system differ, but how they relate to each other [

15].

Therefore, with regard to the development of the crop insurance system, it can be argued that even the development of each element of the system will, in one way or another, lead to the development of the whole system, and the development of a larger number of system components will lead to greater system development. According to the aim of the article, we will describe only the possible impact of the public authorities on the insurance system by determining the best solution of the public authorities’ activity. In order to determine the best solution for public authorities to activate crop insurance performance, a dialog with farmers is necessary. Farmers need to be interviewed on the suitability of the ways to intensify crop insurance activities. The results of the survey could show possible directions for development or whether they are suitable for application in general.

It is mentioned that public authorities allocate budget funds to cover the losses of agricultural sector. It is certainly not the most appropriate way to use these funds. Such conditions reduce farmers’ responsibility for the results of their commercial activity and do not encourage crop insurance. Direct support from public authorities to the agricultural sector does not also encourage the insurance of agricultural holdings; the demand for this service is too low, and public authorities’ funds for agricultural compensation really could find a much more efficient application [

8].

For example, over the past 5 years, the Lithuanian Ministry of Agriculture has already paid out more than EUR 40 million in direct payments to farmers who have suffered losses due to unfavorable natural phenomena. Direct payments to farmers are becoming a problematic tradition in many countries of Eastern Europe, where crop insurance is not yet widely applied. The situation has arisen as many farmers do not understand, do not know and, most importantly, do not believe the insurance process and, as a result of that, do not trust insurance companies because of their commercial activity. It should be noted that the age of farmers in Lithuania is increasing because young people are attracted to cities. Therefore, the involvement of public authorities at least to a minimum in the insurance process would make the insurance process itself much clearer and more reliable for the farmers.

The results were obtained from a survey of Radviliškis district farmers (87 farmers and agricultural companies) of Lithuania. This district was selected for the study because the activities of farmers in the district, the size of farms and the composition of the population are relatively in line with the current situation in Lithuania. The survey was conducted from November 2021 until February 2022. The public authorities’ contribution of at least 20% to the reimbursement of insurance costs could potentially encourage insurance activity, and the loss of liability would be recouped through higher taxes paid by the farmers [

21].

Insurance companies can reduce the insurance fee and thus encourage farmers to insure. However, such a solution increases the risk for insurance companies. Taking the risk (concluding the insurance contract), the insurance company does not always have the ability to cover it, to pay possible insurance losses [

22]. The mentioned authors also claim that insurance organizations, for proper development of insurance activity, use reinsurance, which is one of the methods of reducing and dividing insurance risk. Thus, reinsurance could also be provided by public authorities, and it would be another way to promote crop insurance. The benefits of reinsurance of public authorities would be easily explained to farmers, would be a credible action and would encourage them to insure their crops and also develop a crop insurance system.

In one form or another, however, it is clear that public funds are needed to encourage the development of the insurance system. Thus, two directions of development of the insurance system are mentioned, and a survey of farmers should show whether they are, in principle, interested in such decisions or not. In general, a third solution is also possible—to leave the development to self-propel. This means leaving the development without extraneous stimuli, that is, do nothing and wait for possible development. Such a solution would be most appropriate in the absence of climate change challenges or other crop losses. In this case, no insurance benefits should be paid. Such a solution is the riskiest, but is possible [

23]. Thus, finding the best development solution for the public authorities is a multi-criteria task. The first question in any multicriteria task is the determination the characteristic criteria for assessment.

2.1. Criteria Determination for Assessment Directs of Public Authorities Activity Development

We will determine the best development solution of the public authorities, but using explanations of the insurance system as a whole to determine criteria also typical of the other components of the system. According to the structure of the crop insurance system, it is clear that the possible biggest impact of the key element of the system is on other participants of the system. It has already been mentioned that public authorities are the main actors in the system, so their impact on other elements of the system can be measured and assessed according to typical criteria. Therefore, it is appropriate to group the criteria. So, 3 groups of criteria were defined: the criteria according to which the impact on farmers, impact on insurance companies and impact on the public authorities can be assessed. Every criterion was explained and reasoned by scientific approach, and the results are presented in

Table 1.

The benefits of developing a crop insurance system are unquestionable for all participants in this system. For example, the state’s contribution to these insurance activities allowed not only the economic situation of farmers, but also the economic performance of insurance companies to improve, and such circumstances promote a better image of the state, greater satisfaction of farmers and the possibility to recover some of the costs from insurance companies. It is necessary for the experts to understand the system and its benefits, as they have to determine the significance of the criteria and make final assessments of the possible directions of development. The table also presents possible development results according to scientific literature that can be identified as criteria for selecting the most appropriate development direction. Recommended units of assessment are also given in

Table 1. It is appropriate to group the criteria according to impact to the farmers, insurance companies and public authorities. So, assessment according to these criteria (

Table 1) is possible to find the best result on the direction of development.

The determination of a criterion’s significance and the final assessment need to be performed by experts’ assessment [

25]. Determining the number of experts is guided by the methodological assumptions formulated in the classical test theory, which states that the reliability of aggregated decisions and the number of decision makers (in this case, experts) are linked by a non-linear relationship. It has been proven that in the modules of aggregated expert evaluations with equal weights, the accuracy of decisions and evaluations of a small group of experts is not inferior to the accuracy of decisions and evaluations of a large group of experts [

38,

39,

40].

2.2. Reasoning the Method for Finding the Best Direction for Public Authorities Development

Prior to assessment, it is necessary to establish the significance of the criteria for the assessment in order that the assessment could be as objective as possible [

24]. To do this, we proposed a scale of 100 points, and total estimates are calculated as follows [

37,

38]:

where

H𝑖𝑒 is an estimate of the

i-th criterion by the

e-th expert, n is the number of experts, and

H𝑖 is the sum of all

i criterion estimates by all experts.

The equation below is used to establish the relative importance of the criteria [

24]:

In this case, the sum of criteria importance (significance) will always equal one:

If the result is different, there must be a calculation error.

The results of the experts’ assessment are better presented in in the form of table.

Then, the assessment value of possible directions for development according to the determined criteria have to be calculated by the following (Simple Additive Weighting—SAW) formula [

31]:

where

Z—total value of the possible directions of development according to criteria chosen,

K—value of every direct separately according to every criteria.

Thus, possible directions for development should be further clarified.

The SAW method is simple to use, so it is suitable for public institutions. They will not need to hire external companies to perform such evaluations, and this would allow reducing costs of public authorities’ activity.

3. Results and Discussion

A feature of an insurance system is that the relationships of its components can affect not only the development of individual components but also the development of the system as a whole. Additionally, the development system should show the relationship between the development possibilities of insurance components, i.e., how much the development of one component will affect the development of other components. The crop insurance development system can be understood as the relationship between the development of its components, i.e., the main task in modeling such a system is to identify development relationships. With the approval of farmers, this insurance promotion activity could be included in the assessment.

The first mentioned component of the insurance system is the public authorities that supervise the legality and fairness of the insurance market activities management of participants and distribute the funds of insurance premiums reimbursed to farmers. As the function of the Supervisory Department of the Bank of Lithuania is not only to control the activities of insurance market participants, but also to create legal documents regulating these activities, this institution has a direct influence on crop insurance companies and intermediaries of this service. Another state institution (Ministry of Agriculture), as the holder of budget funds, is intended to partially reimburse the insurance premiums paid by farmers, the amount of which is determined by the insurance companies after assessing the possibility of risk occurrence by coordinating these premiums with the said funds holder.

Other insurance market participants become dependent on the conditions created by the aforementioned first component of the insurance system (public authorities). Only the favorable conditions created by public authorities can lead to the development of the insurance system, so insurance companies form associations to represent them in negotiations with public authorities on favorable conditions. On the other hand, favorable insurance conditions also encourage insurers, i.e., growers of crops, vegetables and orchards to insure against potential risks. In today’s world, many European countries are at least partially compensating farmers for insurance premiums for crop losses due to increasing climate change, attracting centralized European funding. In the meantime, it would be logical for insurance companies to also receive at least part of the public funding to cover farmers’ losses, thus better meeting farmers’ needs to cover their losses and expanding not only their company but also the whole system. The insurance conditions in this way would encourage farmers to insure, as they would be better able to cover losses due to adverse climatic events. Such a development of the system would be of particular benefit to all insurance market participants. Synergies between their activities would be relevant and effective, at least in cases where farmers’ losses are particularly high due to natural disasters, unforeseen and uninsured risks. Agreement between these components of the insurance system is necessary, and the relationship between insurance companies and public authorities is of a pre-contractual nature [

11]. Public authorities in the control function clearly have more bargaining power [

34,

35], but the state’s willingness to compensate farmers for at least part of the loss and public attitudes on this issue do not unequivocally dictate its potential disadvantages due to persistent budget shortages and for the implementation of other state projects. Therefore, at present, public authorities only reimburse farmers for insurance premiums, although the compensation could be higher. Such circumstances encourage listening to the suggestions of insurance companies in order to find the best solutions for farmers. Thus, public authorities are like a monopolist in this field of insurance, able to coordinate both the costs of insurance companies and the monetary compensation of farmers. The development of the insurance system is possible, first of all, through the improvement of insurance conditions dictated by the above-mentioned state institutions and in the relations of these organizations with other participants in the insurance market, which require a compromise that satisfies all stakeholders [

12]. Private insurance companies always aim to increase profits, but receiving at least part of the state funds for crop, vegetable and orchard insurance would be mutually beneficial, as practice shows that private institutions use funds more responsibly and efficiently to benefit both parties’ result [

36]. The proposed scheme is simple: public authorities reimburse part of the costs of insurance companies, thereby increasing the commercial performance of these companies, while insurance companies pay higher business taxes, and farmers who receive compensation are able to channel funds into profitable activities and therefore can also pay higher taxes. In that case, the main participants in the insurance system (insurers and policyholders) would reimburse the public authorities for the loss compensation [

38,

39,

40].

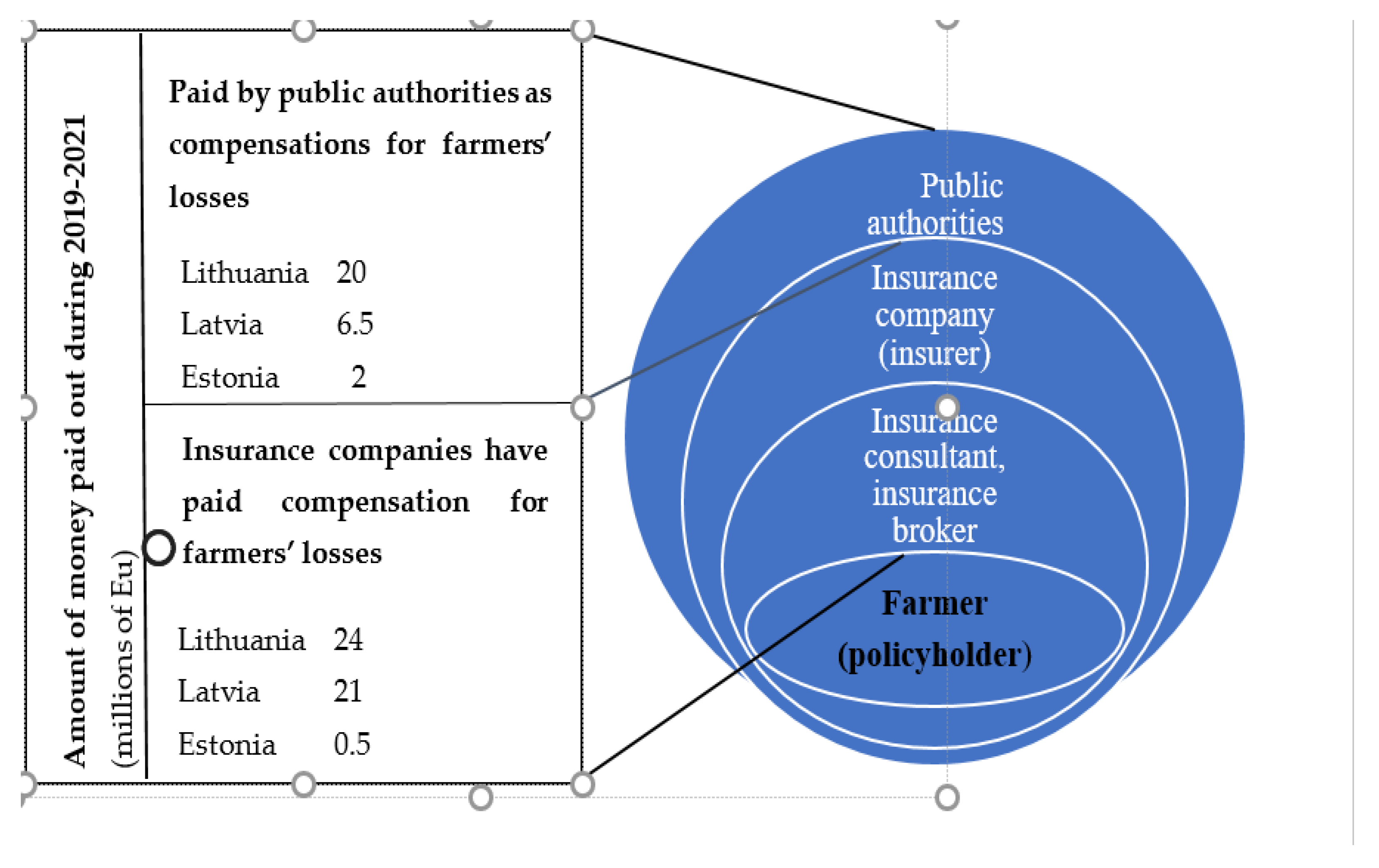

The structure of insurance system participants is shown in

Figure 1.

Figure 1 also presents the contribution of insurance system participants in the Baltic States. Payments to farmers for losses caused by rains and droughts are indicated. In addition, the data show that the need for payments continues to grow due to climate change.

After a deeper analysis of the loss compensation data in the mentioned Baltic countries, it can be stated that the existing trend is favorable: every year, the amounts paid out by insurance companies increase faster than the compensations of state institutions. However, this process is not fast enough in terms of the implementation of reforms. The system development process could be improved by appropriate and reasonable decisions of state institutions, provided as the object of this article. The illustrative structure of the participants in the insurance system (

Figure 1) demonstrates that the state supervisory authorities seem to cover all insurance activities, and the farmer at the center is the main participant in the system, whose decision may determine the results of other components of the system.

The Supervisory Department of the Bank of Lithuania and the Ministry of Agriculture of the Republic of Lithuania on the one hand, and insurance companies on the other, must find a solution favorable to farmers and act in a way that does not harm the interests of both parties. Such a compromise needs to be found through negotiations between all insurance market participants, and such negotiations should be initiated by insurance companies as the organizer of insurance activities in the country [

41]. The implementation of the proposed scheme would be a clear positive outcome of the development of the insurance system. The lack of flexibility of public authorities does not yet allow for the full implementation of the proposed relationship between the participants in the system.

Musshoff et al. [

42] state that the development of the insurance system is also possible by activating the activities of insurance companies. To this end, the factors that encourage the activity of insurance companies and the factors that negatively affect the activity should be identified. Knowing the nature of such factors and the reasons for their occurrence, it is possible to further activate the motivating factors and eliminate the negative ones. These factors can be divided into internal and external. Internal factors are related to the structural processes of selling the service, the range of services offered, the organization of staff work in the company, the microclimate, the use of motivational tools, etc., aspects specific to the insurance company [

36].

External factors: inflation in the country, unemployment rate, personal characteristics of potential policyholders (age, education, income, etc.). The impact of the above factors on the development of the insurance system is unquestionable [

43]; therefore, it is first necessary to promote the internal factors that positively affect this system, as the impact of insurance companies on external factors can be only minimal [

39,

44]. The development of the insurance system is possible by involving as many policyholders as possible in this process, encouraging the choice of insurance products with a wider range, developing new crop insurance services and increasing the sum insured. It has already been mentioned that this development process is influenced by the supervisors and drafters of insurance rules—the Supervision Department of the Bank of Lithuania and the Ministry of Agriculture of the Republic of Lithuania. However, insurance companies must be active also in the market in order to increase the income from insurance activities and the market volume.

These companies also must research consumer needs in order to satisfy them, to cooperate more actively with scientific institutions in developing innovative risk management tools, to apply modern marketing tools to promote the sale of services, to develop loss assessment methodologies and to properly assess and administer losses and to offer the widest possible range of crop insurance products for farmers.

Below, we provide farmers’ views on the state’s contribution for the possible partial compensation of the losses (20%), which should be provided for in the insurance contract between the farmer and the insurance company. We created the questionnaire for the farmers by taking into consideration the specific situation of agriculture in Lithuania and the problems we found in the crop insurance system (

Table 2). So, the results obtained from the survey of farmers in Lithuania are presented in

Table 1. According to the survey of the respondents, we found that 38 farmers already used the services of insurance companies to insure crops; the remaining 49 did not use crop insurance. The answers to the questions are worded as follows: highly encouraged by crop, vegetable and orchard insurance (5), encouraged (4), have no opinion on insurance conditions (3), not encouraged (2), not at all encouraged because I do not trust the state’s obligations (1). The results of the study showed that at least a partial commitment of state institutions to compensate farmers for losses would clearly encourage the development of the insurance system; as many as 22% of farmers would be encouraged crop insurance under the state commitment. The commitment of public authorities to compensate for potential losses gives farmers at least a partial sense of security, and they can be more confident in making responsible financial decisions. In addition, a significant number of farmers do not yet have an opinion on the benefits of insurance and question the benefits of insurance. The activation of insurance companies may attract undecided farmers to insure crops; therefore, the use of insurance companies’ commercial opportunities will affect the development of the insurance system.

According to the results of the survey, it can be concluded that 20% compensation would be of general interest to farmers, and more of them would agree to insure their crops. Such an incentive could be seen as a possible direction for the activity development of public authorities.

Another direction of development that would potentially encourage crop insurance would be public authorities’ provisions to reinsure insurance risks. The results of the survey conducted in the same district of Lithuania (

Table 3) also confirmed this fact.

The results of the survey also showed that crop reinsurance would be of interest to farmers, and that they would be more active in insuring their crops under these conditions. Therefore, reinsurance could also be seen as a possible direction for the activity development of public authorities.

Six experts, representing all institutions participating in the crop insurance system, were invited to determine the significance of the criteria. According to Drejeris and Samolaitis [

38], six experts would suggest a decision reliability of not less than 85%. That would be sufficient for decision making in the social sciences area [

24,

28]. E1 and E2 represented the international crop insurance company “Vereinigte Hagel”, E3 and E4 represented the Lithuanian Association of Farmers, and E5 with E6 represented the Lithuanian Agriculture Ministry. The results of criteria significance determination according to expert assessment are presented in

Table 4.

Then, the assessment of every mentioned direction for public authorities’ activity development is possible. The results of assessment are also better presented in the form of a table. These assessments need to be made by experts as well. The same six experts took part in the assessment. All of them completed questions asked in the form sent by email. The results of their answers are presented in

Table 5, and calculations were performed according to Formula (4).

The results of assessment showed that the best direction for activity development of public authorities is reinsurance. Reinsurance would be the most appropriate direction for the activity development of public institutions in the current conditions and in the present situation.

The data mentioned in

Table 1 showed that it is more beneficial for the state to contribute to the compensation of funds to insurance companies than to pay benefits directly to farmers. It is more appropriate to provide summary data on the impact of the development of the insurance system on farmers, insurance companies and state institutions (

Table 2). The data presented in

Table 2 clearly confirm that the development of the insurance system is most beneficial for farmers. Additionally, by further promoting the development of farmers’ relations (as a component of the insurance system) with other participants of this market, it is possible to further activate the distribution of insurance services and the development of the insurance system. Consequently, the greatest responsibility for the development of the insurance system lies with insurance companies as the most active component of this system, which can directly influence farmers’ decision to use insurance services. The data in

Table 2 can be published to activate the development of insurance services, with particular emphasis on its benefits for each participant of the insurance market.

Consequently, the development of crop insurance provides direct benefits to the state. Insurance companies have the direct benefits of the development of this system; in addition, there is an opportunity to invest in the development of new insurance products, market development, infrastructure improvement and the application of innovative marketing tools, thus creating an opportunity to expand their circle of policyholders. The most important impact of the development of the insurance system on farmers is that transactions with insurance companies reduce the risk of disasters. The greatest benefits of the development of the insurance system are obviously received by policyholders (farmers). For example, receiving an insurance benefit creates a lower need for borrowing, makes it possible to diversify income strategies, accumulate assets and settle with creditors more quickly and gives greater freedom of commercial activity, i.e., the opportunity to invest properly and increase farm activity performance. In this way, farmers can be more flexible in adapting to climate change.

Our suggested methodology is entirely clear, logical and simple to use. We suggest assessment according to the original formulated substantiated scientific criteria, which are related to all participants of the insurance system. This is a new and original solution in the area of crop insurance system development. Additionally, this characteristic will only add objectivity to the methodology. Another innovation of the methodology is that we propose to invite experts from all three institutions participating in the insurance system. This solution will also have a positive impact on objectivity. Our further research would be related to the search for development directions of other participants in the insurance system and finding the best solutions for implementation.

{kind=link}