Does COVID-19 Affect Farmland Prices? How and Why?

Abstract

:1. Introduction

2. Government Payments to the Agricultural Sector and COVID-19 in Taiwan

3. Data

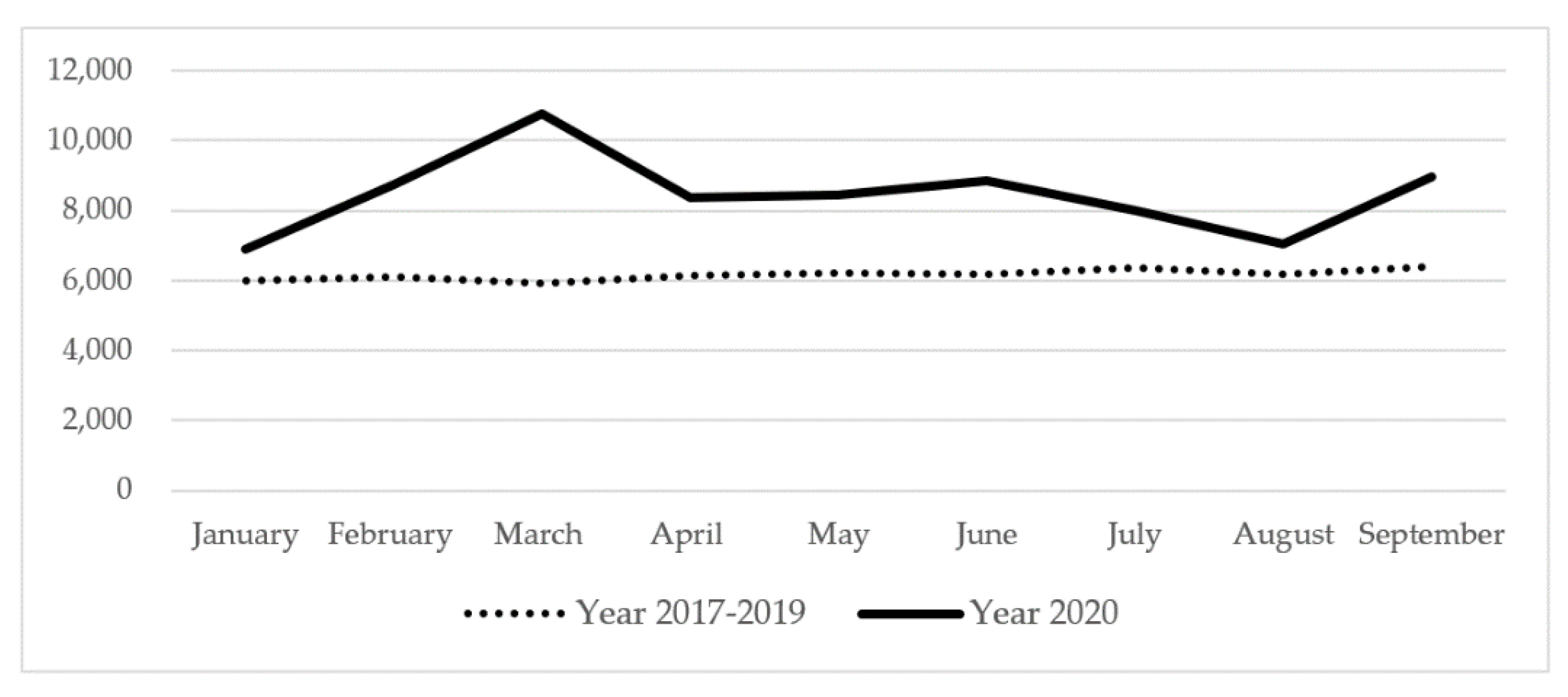

3.1. Data on Farmland Transactions

3.2. Data on Agricultural, Environmental, and Geographic Characteristics

3.3. Data on COVID-19

3.4. Data on Government Payments and Macroeconomic Conditions

3.5. Sample Statistics of the Selected Variables

4. Methodology

5. Empirical Results

5.1. Main Findings

5.2. Urban versus Rural Areas

5.3. Robustness Checks of the Main Findings

5.4. The Impact of COVID-19 on Government Payments

6. Discussions and Conclusions

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- United Nations. COVID-19 to Slash Economic Output by US $8.5 Trillion over Next Two Years. 2020. Available online: https://www.un.org/en/desa/covid-19-slash-global-economic-output-85-trillion-over-next-two-years (accessed on 30 April 2021).

- Elsaid, K.; Olabi, V.; Sayed, E.; Wilberforce, T.; Abdelkareem, M. Effects of COVID-19 on the Environment: An Overview on Air, Water, Wastewater, and Solid Waste. J. Environ. Manag. 2021, 292, 112694. [Google Scholar] [CrossRef] [PubMed]

- Sahraei, M.; Kuskapan, E.; Codur, M. Public Transit Usage and Air Quality Index During the COVID-19 Lockdown. J. Environ. Manag. 2021, 286, 112166. [Google Scholar] [CrossRef] [PubMed]

- Zhang, W.; Li, S.; Gao, Y.; Liu, W.; Jiao, Y.; Zeng, C.; Gao, L.; Wang, T. Travel Changes and Equitable Access to Urban Parks in the Post COVID-19 Pandemic Period: Evidence from Wuhan, China. J. Environ. Manag. 2022, 304, 114217. [Google Scholar] [CrossRef] [PubMed]

- Beckman, J.; Countryman, A. The Importance of Agriculture in the Economy: Impacts from COVID-19. Am. J. Agric. Econ. 2021, 103, 1595–1611. [Google Scholar] [CrossRef] [PubMed]

- Charlton, D. Seasonal Farm Labor and COVID-19 Spread. Appl. Econ. Perspect. Policy 2021, forthcoming. [Google Scholar] [CrossRef] [PubMed]

- Arita, S.; Grant, J.; Sydow, S.; Beckman, J. Has Global Agricultural Trade Been Resilient Under Coronavirus (COVID-19)? Findings from an Economic Assessment of 2020. Food Policy 2022, 107, 102204. [Google Scholar] [CrossRef] [PubMed]

- Borchers, A.; Ifft, J.; Kuethe, T. Linking the Price of Agricultural Land to Use Values and Amenities. Am. J. Agric. Econ. 2014, 96, 1307–1320. [Google Scholar] [CrossRef]

- Zhang, W.; Duffy, M. Agricultural Professional Expect Lower Farmland Values Over the Next 18 Months. 2020. Available online: https://www.extension.iastate.edu/agdm/articles/zhang/ZhaJul20.html (accessed on 30 April 2021).

- Oppedahl, D. AgLetter: February 2021. Available online: https://www.chicagofed.org/publications/agletter/2020-2024/february-2021 (accessed on 30 April 2022).

- Lawley, C. Potential Impacts of COVID-19 on Canadian Farmland Markets. Can. J. Agric. Econ. 2020, 68, 245–250. [Google Scholar] [CrossRef]

- Lawley, C. COVID-19 and Canadian Farmland Markets in 2020. Can. J. Agric. Econ. 2021, 69, 291–298. [Google Scholar] [CrossRef]

- Choi, J.; Painter, G. Self-Reported Vs. Market Estimated House Values: Are Homeowners Misinformed or Are They Purposely Misreporting? Real Estate Econ. 2017, 46, 487–520. [Google Scholar] [CrossRef]

- Zhang, W. Outlook for Land Values in 2021 and Beyond: Results from the 2020 Iowa Land Value Survey. 2021. Available online: https://www.extension.iastate.edu/agdm/articles/zhang/ZhaJan21.html (accessed on 30 April 2021).

- Bureau of Agricultural Finance; Council of Agriculture; Executive Yuan in Taiwan. Measures for Handling Policy-Based Agricultural Project Loans. 2020. Available online: https://www.boaf.gov.tw/view.php?theme=agricultural_development&subtheme=&id=2 (accessed on 30 April 2022).

- Lee, T.-H.; Lee, B.; Su, Y.-J.; Chang, H.-H. Green Payment Programs and Farmland Prices—An Empirical Investigation. Agriculture 2022, 12, 207. [Google Scholar] [CrossRef]

- Tay, D.; Chou, C.; Li, S.; Tee, S.; Cheong, S. Bubbles are Departures from Equilibrium Housing Markets: Evidence from Singapore and Taiwan. PLoS ONE 2016, 11, e0166004. [Google Scholar] [CrossRef] [Green Version]

- Rosen, S. Hedonic Prices and Implicit Markets: Product Differentiation in Pure Competition. J. Politic Econ. 1974, 82, 34–55. [Google Scholar] [CrossRef]

- Plantinga, A.; Miller, D. Agricultural Land Values and Future Land Development. Land Econ. 2001, 77, 56–67. [Google Scholar] [CrossRef]

- Chen, Y.; Lee, C.; Chen, G.; Wang, C.; Chen, Y. Factors Causing Farmland Price-Value Distortion and the Implications for Peri-Urban Growth Management. Sustainability 2018, 10, 2701. [Google Scholar] [CrossRef] [Green Version]

- Fang, H.; Wang, L.; Yang, Y. Human Mobility Restrictions and the Spread of the Novel Coronavirus (2019-nCOV) in China. J. Public Econ. 2020, 191, 104272. [Google Scholar] [CrossRef]

- Rodríguez-Planas, N. COVID-19, College Academic Performance, and the Flexible Grading Policy: A Longitudinal Analysis. J. Public Econ. 2022, 207, 104606. [Google Scholar] [CrossRef]

- Barnard, C.; Whittaker, G.; Westenbarger, D.; Ahearn, M. Evidence of Capitalization of Direct Government Payments into U.S. Cropland Values. Am. J. Agric. Econ. 1997, 79, 1642–1650. [Google Scholar] [CrossRef]

- Latrouffe, L.; Mouel, C. Capitalization of Government Support in Agricultural Land Prices: What Do We Know? J. Econ. Surv. 2009, 23, 659–691. [Google Scholar] [CrossRef]

- Fairbairn, M. ‘Like Gold with Yield’: Evolving Intersections Between Farmland and Finance. J. Peasant Stud. 2014, 41, 777–795. [Google Scholar] [CrossRef]

- Stephenson, A. Omicron COVID-19 Variant Concerning for Canadian Food Production, Farm Groups Say. 2022. Available online: https://globalnews.ca/news/8495093/omicron-covid-19-variant-canadian-food-production-concerns/ (accessed on 30 April 2021).

- Hausman, C.; Auffhammer, M.; Berck, P. Farm Acreage Shocks and Crop Prices: A SVAR Approach to Understanding the Impacts of Biofuels. Environ. Resour. Econ. 2012, 53, 117–136. [Google Scholar] [CrossRef]

{kind=link}

| Panel A. Farmland Transaction Data | Panel B. COVID-19 Data | |||||

|---|---|---|---|---|---|---|

| Farmland Prices (TWD/m2) | Number of Transactions | Cumulated Cases | Google Search # | |||

| Year | 2020 | 2017–2019 | 2020 | 2017–2019 | 2020 | 2020 |

| Month | (A) | (B) | (C) | (D) | (E) | (F) |

| January | 6899 | 5989 | 1129 | 1382 | 10 | 48 |

| February | 8725 | 6099 | 1556 | 1004 | 39 | 98 |

| March | 10,775 | 5903 | 2040 | 1572 | 322 | 100 |

| April | 8383 | 6151 | 1614 | 1429 | 429 | 63 |

| May | 8446 | 6218 | 1765 | 1575 | 442 | 22 |

| June | 8846 | 6187 | 1695 | 1461 | 447 | 14 |

| July | 8010 | 6352 | 1503 | 1464 | 467 | 12 |

| August | 7054 | 6167 | 1299 | 1341 | 488 | 12 |

| September | 8953 | 6389 | 1479 | 1286 | 514 | 8 |

| Full Sample | Post = 1 & Treat = 1 | Post = 0 & Treat = 1 | Post = 1 & Treat = 0 | Post = 0 & Treat = 0 | |||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| N*T | 51,624 | 13,106 | 34,607 | 975 | 2936 | ||||||

| Variable | Definition | Mean | S.D | Mean | S.D | Mean | S.D | Mean | S.D | Mean | S.D |

| Post | If year 2020 (=1). | 0.27 | 0.45 | 1 | 0 | 0 | 0 | 1 | 0 | 0 | 0 |

| Treat | If after 22 January (=1). | 0.92 | 0.27 | 1 | 0 | 1 | 0 | 0 | 0 | 0 | 0 |

| Price | Price of the transacted parcel of farmland (TWD/m2). | 6830 | 8753 | 8727 | 10,404 | 6196 | 8056 | 7049 | 8010 | 5763 | 7475 |

| Payments | Government payments in the township (TWD million/month). | 10.32 | 14.04 | 15.31 | 20.01 | 8.54 | 10.72 | 7.43 | 9.93 | 10.02 | 11.80 |

| Land | Size of the transacted parcel of farmland (1000 m2). | 2.00 | 2.53 | 2.03 | 2.29 | 1.99 | 2.62 | 1.96 | 2.18 | 2.00 | 2.56 |

| Urban | If in an urban area (=1). | 0.25 | 0.43 | 0.15 | 0.35 | 0.28 | 0.45 | 0.23 | 0.42 | 0.28 | 0.45 |

| Irrigation | Closest distance to the irrigation facility (m). | 0.25 | 0.51 | 0.21 | 0.41 | 0.27 | 0.53 | 0.24 | 0.44 | 0.26 | 0.57 |

| Crop | If in a crop production zone (=1). | 0.48 | 0.50 | 0.57 | 0.50 | 0.45 | 0.50 | 0.42 | 0.49 | 0.42 | 0.49 |

| Productivity | Land productivity (1–10). The higher the score, the better the quality. | 2.74 | 1.87 | 2.55 | 1.83 | 2.80 | 1.87 | 2.63 | 1.80 | 2.83 | 1.90 |

| Farm association | Closest distance to the nearby farm association (m). | 3.03 | 1.82 | 3.16 | 1.79 | 2.98 | 1.82 | 3.07 | 1.82 | 3.03 | 1.84 |

| Railroad | Closest distance to railroad (m). | 7.84 | 6.53 | 8.28 | 6.27 | 7.69 | 6.63 | 7.60 | 6.26 | 7.72 | 6.56 |

| Highway | Closest distance to highway (=1). | 7.96 | 12.34 | 7.37 | 11.59 | 8.14 | 12.57 | 7.74 | 12.02 | 8.42 | 12.94 |

| Road | Closest distance to major road (=1). | 1.55 | 1.64 | 1.54 | 1.55 | 1.55 | 1.67 | 1.49 | 1.50 | 1.62 | 1.68 |

| D_COVID | If during COVID-19 period (=1). | 0.25 | 0.44 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| COVID_case | Number of cumulated confirmed cases of COVID-19 per day. | 36.50 | 117.62 | 143.78 | 197.67 | 0 | 0 | 0 | 0 | 0 | 0 |

| COVID_search | Google Trends Search Index for COVID-19 per month. | 12.00 | 27.28 | 43.70 | 37.65 | 0 | 0 | 48 | 0 | 0 | 0 |

| Food price | Food price index in month. | 96.80 | 3.12 | 95.93 | 2.75 | 96.97 | 3.05 | 103.60 | 0 | 96.41 | 2.84 |

| Interest rate | Average monthly interesting rate. | 2.60 | 0.06 | 2.52 | 0.08 | 2.63 | 0.00 | 2.63 | 0 | 2.63 | 0.000 |

| Stock price | Month average stock price index (10,000). | 1.07 | 0.08 | 1.14 | 0.09 | 1.05 | 0.04 | 1.20 | 0 | 1.00 | 0.07 |

| Model A | Model B | Model C | ||||

|---|---|---|---|---|---|---|

| Variable | Coefficient | S.E | Coefficient | S.E | Coefficient | S.E |

| D_COVID | 0.051 ** | 0.018 | ||||

| COVID_case/1000 | 0.383 ** | 0.151 | ||||

| COVID_search/1000 | 0.866 * | 0.464 | ||||

| Treat | −0.037 | 0.021 | −0.021 | 0.022 | −0.018 | 0.022 |

| Land | −0.019 *** | 0.002 | −0.019 *** | 0.002 | −0.019 *** | 0.002 |

| Urban | 0.514 *** | 0.010 | 0.509 *** | 0.010 | 0.508 *** | 0.010 |

| Irrigation | 0.013 | 0.015 | 0.012 | 0.015 | 0.012 | 0.015 |

| Crop | 0.095 *** | 0.005 | 0.099 *** | 0.005 | 0.101 *** | 0.005 |

| Productivity | 0.025 *** | 0.002 | 0.025 *** | 0.002 | 0.025 *** | 0.002 |

| Farm association | −0.049 *** | 0.002 | −0.049 *** | 0.002 | −0.049 *** | 0.002 |

| Railroad | −0.013 *** | 0.001 | −0.013 *** | 0.001 | −0.013 *** | 0.001 |

| Highway | −0.013 *** | 0.002 | −0.013 *** | 0.002 | −0.012 *** | 0.002 |

| Road | −0.031 *** | 0.003 | −0.031 *** | 0.003 | −0.031 *** | 0.003 |

| Food Price | 0.004 | 0.003 | 0.004 | 0.003 | 0.004 | 0.003 |

| Interest rate | −0.232 ** | 0.115 | −0.299 ** | 0.115 | −0.603 *** | 0.222 |

| Stock price | −0.220 * | 0.114 | −0.268 ** | 0.112 | −0.216 * | 0.112 |

| Constant | 8.341 *** | 0.020 | 8.357 *** | 0.020 | 8.339 *** | 0.020 |

| Control for years | Yes | Yes | Yes | |||

| Control for months | Yes | Yes | Yes | |||

| Control townships | Yes | Yes | Yes | |||

| Adjusted R2 | 0.773 | 0.773 | 0.773 | |||

| N | 51,624 | 51,624 | 51,624 | |||

| Panel A. Urban Farmland | ||||||

|---|---|---|---|---|---|---|

| Key Variable | Coefficient | S.E | Coefficient | S.E | Coefficient | S.E |

| D_COVID | 0.038 * | 0.021 | ||||

| COVID_case/1000 | 0.279 * | 0.141 | ||||

| COVID_search/1000 | 0.613 * | 0.316 | ||||

| Other variables | Yes | Yes | Yes | |||

| Adjusted R2 | 0.071 | 0.071 | 0.071 | |||

| N | 12,683 | 12,683 | 12,683 | |||

| Panel B. Rural farmland | ||||||

| Key variable | Coefficient | S.E | Coefficient | S.E | Coefficient | S.E |

| D_COVID | 0.063 *** | 0.018 | ||||

| COVID_case/1000 | 0.490 ** | 0.231 | ||||

| COVID_search/1000 | 0.913 * | 0.528 | ||||

| Other variables | Yes | Yes | Yes | |||

| Adjusted R2 | 0.781 | 0.780 | 0.781 | |||

| N | 38,919 | 38,919 | 38,919 | |||

| Hypothetical Shock | Year 2019 | Year 2018 | Year 2017 | |||

|---|---|---|---|---|---|---|

| Variable | Coefficient | S.E | Coefficient | S.E | Coefficient | S.E |

| D_COVID | 0.003 | 0.012 | −0.012 | 0.022 | 0.019 | 0.022 |

| Treat | −0.033 | 0.220 | −0.025 | 0.020 | −0.028 | 0.020 |

| Other variables # | Yes | Yes | Yes | |||

| Adjusted R2 | 0.751 | 0.751 | 0.751 | |||

| Model A | Model B | Model C | ||||

|---|---|---|---|---|---|---|

| Key Variable | Coef. | S.E | Coef. | S.E | Coef. | S.E |

| D_COVID | 2.7462 *** | 0.5472 | ||||

| COVID_case | 0.0005 *** | 0.0008 | ||||

| COVID_search | 0.0335 *** | 0.0118 | ||||

| Other variables # | Yes | Yes | Yes | |||

| Adjusted R2 | 0.477 | 0.476 | 0.476 | |||

| N | 51,624 | 51,624 | 51,624 | |||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Lee, B.; Cheng, P.-Y.; Sun, L.-C.; Hsieh, Y.-T.; Chang, H.-H. Does COVID-19 Affect Farmland Prices? How and Why? Agriculture 2022, 12, 2163. https://doi.org/10.3390/agriculture12122163

Lee B, Cheng P-Y, Sun L-C, Hsieh Y-T, Chang H-H. Does COVID-19 Affect Farmland Prices? How and Why? Agriculture. 2022; 12(12):2163. https://doi.org/10.3390/agriculture12122163

Chicago/Turabian StyleLee, Brian, Po-Yuan Cheng, Lih-Chyun Sun, Yi-Ting Hsieh, and Hung-Hao Chang. 2022. "Does COVID-19 Affect Farmland Prices? How and Why?" Agriculture 12, no. 12: 2163. https://doi.org/10.3390/agriculture12122163