Financing Brownfield Redevelopment and Housing Market Dynamics: Evidence from Connecticut

Abstract

:1. Introduction

2. Literature Review

3. Empirical Analysis

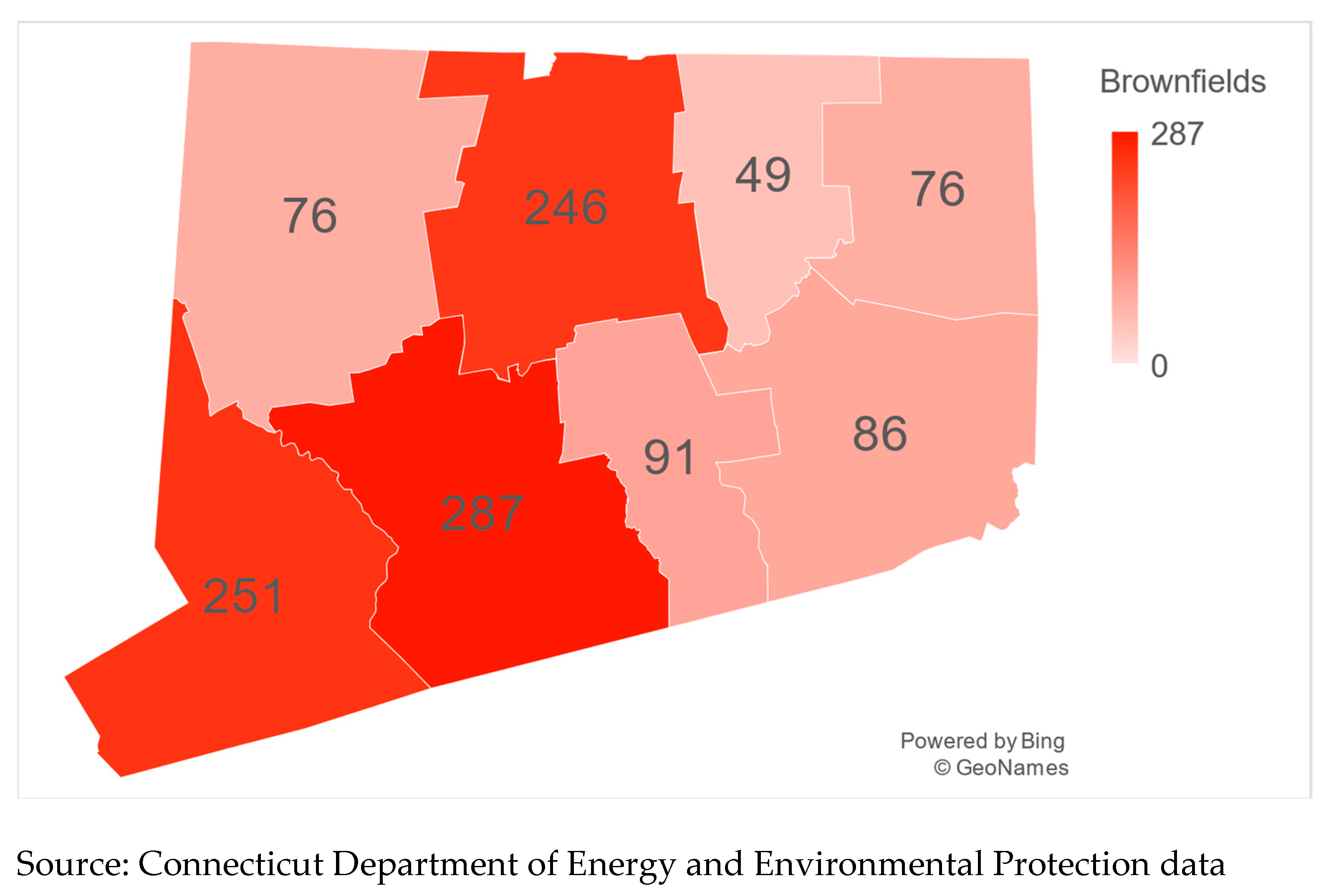

3.1. Sample

3.2. Methodology

3.3. Results

4. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Boyd, J.; Harringtom, W.; Macauley, M.K. The Effects of Environmental Liability on Industrial Real Estate Development. In Economics and Liability for Environmental Problems; Segerson, K., Ed.; Routledge: London, UK, 2002. [Google Scholar]

- Alker, S.; Joy, V.; Roberts, P.; Smith, N. The Definition of Brownfield. J. Environ. Plan. Manag. 2000, 43, 49–69. [Google Scholar] [CrossRef]

- Faber, S. Undesirable Facilities and Property Values: A Summary of Empirical Studies. Ecol. Econ. 1998, 24, 1–14. [Google Scholar] [CrossRef]

- Chan, S. Spatial Lock-In: Do Falling House Prices Constrain Residential Mobility? J. Urban Econ. 2011, 49, 567–586. [Google Scholar] [CrossRef]

- Bartsch, C.; Wells, B. Local Brownfield Financing Tools. Structures and Strategies for Spurring Cleanup and Redevelopment. Northeast-Midwest Institute Report. Available online: https://www.nemw.org/ (accessed on 30 December 2022).

- Kurdila, J.; Rindfleisch, E. Funding opportunities for brownfield redevelopment. Boston Coll. Environ. Aff. 2007, 39, 479. [Google Scholar]

- Schilling, J. Beyond Brownfields Redevelopment: A Policy Framework for Regional Land Recycling Planning. J. Comp. Urban Law Policy 2022, 5, 468–490. [Google Scholar]

- Wernstedt, K.; Meyer, P.B.; Yount, K.R. Insuring Redevelopment at Contaminated Urban Properties. Public Work. Manag. Policy 2003, 8, 85–98. [Google Scholar] [CrossRef]

- Adams, D.; De Sousa, C.; Tiesdell, S. Brownfield Development: A Comparison of North American and British Approaches. Urban Stud. 2010, 47, 75–104. [Google Scholar] [CrossRef]

- Leigland, J. Changing Perceptions of PPP Risk and Return: The Case of Brownfield Concessions. J. Struct. Financ. 2018, 23, 47–56. [Google Scholar] [CrossRef]

- Haninger, K.; Ma, L.; Timmins, C. The value of brownfield remediation. J. Assoc. Environ. Resour. Econ. 2017, 4, 197–224. [Google Scholar] [CrossRef]

- US Environmental Protection Agency (USEPA). Support of Regional Efforts to Negotiate Prospective Purchaser Agreements (PPAs) at Superfund Sites and Clarification of PPA Guidance; Office of Site Remediation Enforcement: Washington, DC, USA, 1996.

- Kiel, K.A. Measuring the impact of the discovery and cleaning of identified hazardous waste sites on house values. Land Econ. 1995, 71, 428–435. [Google Scholar] [CrossRef]

- Han, H.S. Exploring Threshold Effects in the Impact of Housing Abandonment on Nearby Property Values. Urban Aff. Rev. 2019, 55, 772–799. [Google Scholar] [CrossRef]

- Kiel, K.A.; Williams, M. The impact of Superfund sites on local property values: Are all sites the same? J. Urban Econ. 2007, 61, 170–192. [Google Scholar] [CrossRef]

- Mihaescu, O.; Vom Hofe, R. The impact of brownfields on residential property values in Cincinnati, Ohio: A spatial hedonic approach. J. Reg. Anal. Policy 2012, 42, 223–236. [Google Scholar]

- Tajani, F.; Morano, P.; Di Liddo, F. Redevelopment Initiatives on Brownfield Sites: An Evaluation Model for the Definition of Sustainable Investments. Buildings 2023, 13, 724. [Google Scholar] [CrossRef]

- Kohlhase, J.E. The Impact of Toxic Waste Sites on Housing Values. J. Urban Econ. 1991, 30, 1–26. [Google Scholar] [CrossRef]

- Alberini, A.; Longo, A.; Tonin, S.; Trombetta, F.; Turvani, M. The role of liability, regulation, and economic incentives in brownfield remediation and redevelopment: Evidence from developer surveys. Reg. Sci. Urban Econ. 2005, 35, 327–351. [Google Scholar] [CrossRef]

- Thornton, G.; Franz, M.; Edwards, D.; Pahlen, G.; Nathanail, P. The challenge of sustainability: Incentives for brownfield regeneration in Europe. Environ. Sci. Policy 2007, 10, 116–134. [Google Scholar] [CrossRef]

- Vestbro, D. Rebuilding the City-Managing the Built Environment and Remediation of Brownfields. In Baltic University Urban Forum Urban Management Guidebook VI; Baltic University: Hamburg, Germany, 2007. [Google Scholar]

- Prato, T. Evaluating land use plans under uncertainty. Land Use Policy 2007, 24, 65–174. [Google Scholar] [CrossRef]

- Chen, I.; Ma, H. Using risk maps to link land value damage and risk as basis of flexible risk management for brownfield redevelopment. Chemosphere 2013, 90, 2101–2108. [Google Scholar] [CrossRef]

- Chen, I.; Chuo, Y.; Ma, H. Uncertainty analysis of remediation cost and damaged land value for brownfield investment. Chemosphere 2019, 220, 371–380. [Google Scholar] [CrossRef]

- Wu, H.; Tiwari, P.; Han, S.; Chan, T. Brownfield risk communication and evaluation. J. Prop. Res. 2017, 34, 233–250. [Google Scholar] [CrossRef]

- Lynn, J. The effect of voluntary brownfields programs on nearby property values: Evidence from Illinois. J. Urban Econ. 2013, 78, 1–18. [Google Scholar] [CrossRef]

- Kotval, K.Z. Brownfield Redevelopment: Why Public Investments Can Pay Off. Econ. Dev. Q. 2016, 30, 275–282. [Google Scholar] [CrossRef]

- Banzhaf, H. Panel Data Hedonics: Rosen’s First Stage and Difference-in-Differences as “Sufficient Statistics”, NBER Working Paper, w21485; National Bureau of Economic Research: Cambridge, MA, USA, 2015. [Google Scholar]

- Ihlanfeldt, K.R.; Taylor, L.O. Externality effects of small-scale hazardous waste sites: Evidence from urban commercial property markets. J. Environ. Econ. Manag. 2004, 47, 117–139. [Google Scholar] [CrossRef]

- Zhao, Q.; Liu, M.; Chen, Q. The Impact of Gasoline Stations on Residential Property Values: A Case Study in Xuangcheng, China. J. Sustain. Real Estate 2017, 9, 66–85. [Google Scholar] [CrossRef]

- Winson-Geideman, K.; Krause, A.; Wu, H.; Warren-Myers, G. Non spatial Contagion in Real Estate Markets: The Case of Brookland Greens. J. Sustain. Real Estate 2017, 9, 22–45. [Google Scholar] [CrossRef]

- Woo, A.; Lee, S. Illuminating the impacts of brownfield redevelopments on neighboring housing prices: Case of Cuyahoga County, Ohio in the US. Environ. Plan. A 2016, 48, 1107–1132. [Google Scholar] [CrossRef]

- Zhang, Y.; Wang, C.; Tian, W.; Zhang, G. Determinants of purchase intention for real estate developed on industrial brownfields: Evidence from China. J. Hous. Built Environ. 2020, 35, 1261–1282. [Google Scholar] [CrossRef]

- Gamper-Rabindran, S.; Mastromonaco, R.; Timmins, C. Valuing the Benefits of Superfund Site Remediation: Three Approaches to Measuring Localized Externalities; NBER Working Paper n. 16655; National Bureau of Economic Research: Cambridge, MA, USA, 2011. [Google Scholar]

- Hamlin, R.; Hula, R.; Cobarzan, B.; Jackson-Elmoore, C.; Leuca, C. Brownfields: Making Programs Work for Michigan Communities; Urban Policy Research Brief # 5; Center for Community & Economic Development: Lansing, Michigan, 2018. [Google Scholar]

- Schnapf, L. Financing development of contaminated properties. Nat. Resour. Environ. 1999, 13, 465–470. [Google Scholar]

- Maantay, J.; Maroko, A. Brownfields to Greenfields: Environmental Justice Versus Environmental Gentrification. Int. J. Environ. Res. Public Health 2018, 15, 2233. [Google Scholar] [CrossRef]

- Bryan, M. Financing brownfields redevelopment. Am. City Ctry. 1999, 114, 8. [Google Scholar]

- Lange, D.; McNeil, S. Clean It and They Will Come? Defining Successful Brownfield Development. J. Urban Plan. Dev. 2004, 130, 101–108. [Google Scholar] [CrossRef]

- Amekudzi, A.A.; Attoh-Okine, N.O.; Laha, S. Brownfields redevelopment issues at the federal, state, and local levels. J. Environ. Syst. 1997, 25, 97–121. [Google Scholar] [CrossRef]

- Lubell, M.; Feiock, R.C.; Ramirez de la Cruz, E.E. Local institutions and the politics of urban growth. Am. J. Political Sci. 2009, 53, 649–665. [Google Scholar] [CrossRef]

- Greene, L.; Coffin, S. Modeling the relationship among brownfields, property values, and community revitalization. Hous. Policy Debate 2005, 16, 257–280. [Google Scholar]

- Bacot, H.; O’Dell, C. Establishing Indicators to Evaluate Brownfield Redevelopment. Econ. Dev. Q. 2006, 20, 142–161. [Google Scholar] [CrossRef]

- United States of America. Twelfth Census of the United States. Census Bull. 1901, 109, 1–31.

- Connecticut History.org. Available online: http://connecticuthistory.org/ (accessed on 15 October 2023).

- United States Environment Protection Agency. Available online: https://www.epa.gov/brownfields/r1 (accessed on 15 October 2023).

- Trilling, B.; Lemar, A.S. Brownfield Development in Connecticut, A new Chapter: Liability Relief from Purchasers and Sellers of Contaminated Sites in the 2011. Quinnipiac Law Rev. 2012, 30, 331–358. [Google Scholar]

- De Sousa, C.; Wu, C.; Westphal, L. Assessing the Effect of Publicly Assisted Brownfield Redevelopment on Surrounding Property Values. Econ. Dev. Q. 2009, 23, 95–110. [Google Scholar] [CrossRef]

- Green, L. Evaluating predictors for brownfield redevelopment. Land Use Policy 2018, 73, 299–319. [Google Scholar] [CrossRef]

- Weber, B.; Adair, A.; McGreal, S. Solutions to the five key brownfield valuation problems. J. Prop. Invest. Financ. 2008, 26, 8–37. [Google Scholar] [CrossRef]

- Schwarz, P.M.; Gwendolyn, L.G.; Hanning, A.; Cox, C.A. Estimating the effects of brownfields and brownfield remediation on property values in New South City. Contemp. Econ. Policy 2017, 35, 143–164. [Google Scholar] [CrossRef]

- Gibilaro, L.; Mattarocci, G. Brownfield Areas and Housing Value: Evidence from Milan. J. Sustain. Real Estate 2019, 11, 60–83. [Google Scholar] [CrossRef]

- Pagourtzi, E.; Assimakopoulos, V.; Hatzichristos, T.; French, N. Real estate appraisal: A review of valuation methods. J. Prop. Invest. Financ. 2003, 21, 383–401. [Google Scholar] [CrossRef]

- De Sousa, C. Turning Brownfields into Green Space in the City of Toronto. Landsc. Urban Plan. 2003, 62, 181–198. [Google Scholar] [CrossRef]

- Hoover, E.M.; Vernon, R. Anatomy of a Metropolis; Harvard University Press: Cambridge, UK, 1959. [Google Scholar]

- Cerasoli, M.; Mattarocci, G. Rigenerazione Urbana E Mercato Immobiliare; RomaTre Press: Roma, Italy, 2018. [Google Scholar]

- Kinga, X.H.N.; Tihamér-Levente, S. Sustainable brownfield regeneration in Baia Mare, Romania. Constructing place attachment through co-creation and co-development. In Preserving and Constructing Place Attachment in Europe; Ilovan, O.R., Markuszewska, I., Eds.; Springer: Cham, Switzerland, 2022; pp. 311–328. [Google Scholar]

- EEA. Progress in the Management of Contaminated Sites in Europe. Available online: https://www.eea.europa.eu/ (accessed on 30 December 2022).

- Gyourko, J.; Hartley, J.S.; Lrimmel, J. The local residential land use regulatory environment across U.S. housing markets: Evidence from a new Wharton index. J. Urban Econ. 2021, 124, 103337. [Google Scholar] [CrossRef]

- Moore, T.; Doyon, A. Sustainable Housing in Practice. In A Transition to Sustainable Housing; Moore, T., Doyon, A., Eds.; Palgrave Macmillan: Singapore, 2023; pp. 197–238. [Google Scholar]

- Squires, G.; Hutchison, N. Barriers to affordable housing on brownfield sites. Land Use Policy 2021, 102, 10527. [Google Scholar] [CrossRef]

{kind=link}

| County | N° of Towns | N° of Towns with Brownfield | Average Percentage Financed by the Special Programs |

|---|---|---|---|

| Fairfield | 23 | 19 | 15.33% |

| Hartford | 29 | 18 | 19.08% |

| Litchfield | 26 | 17 | 8.16% |

| Middlesex | 15 | 15 | 11.56% |

| New Haven | 27 | 25 | 15.92% |

| New London | 21 | 13 | 33.92% |

| Tolland | 13 | 11 | 13.64% |

| Windham | 15 | 11 | 7.38% |

| Overall | 169 | 129 | 15.64% |

| Formula | Towns without Brownfields | Towns with Brownfields | Towns with Brownfields Redevelopment | |

|---|---|---|---|---|

| Income | 0.71 | 0.65 | 0.57 ** | |

| (0.17) | (0.23) | (0.17) | ||

| Population | 1.00 | 1.83 | 2.60 ** | |

| (1.85) | (2.00) | (2.41) | ||

| Homeownership | 0.32 | 0.31 | 0.31 | |

| (0.07) | (0.07) | (0.07) | ||

| Housing value | 1.21 | 1.17 | 0.98 ** | |

| (0.42) | (0.76) | (0.37) | ||

| Vacancy rate | 0.14 | 0.10 | 0.10 | |

| (0.09) | (0.07) | (0.05) | ||

| Rent value | 1.12 | 1.07 | 1.03 | |

| (0.33) | (0.26) | (0.18) | ||

| Crime rate | 1.00 ** | 1.54 | 1.97 ** | |

| (0.97) | (1.08) | (1.18) | ||

| Housing permits | 0.99 ** | 3.48 | 4.09 | |

| (1.79) | (5.92) | (6.67) |

| Distance from the CBD | 0.01 | 0.01 | 0.01 | 0.01 |

| Income | −1.54 ** | 0.08 | 0.56 | 0.07 |

| Population | 0.06 ** | −0.01 * | −0.03 * | −0.01 * |

| Homeownership | 0.62 * | 0.01 * | 0.87 * | 0.10 |

| Crime Rate | 0.11 * | −0.01 | −0.01 | −0.02 |

| Housing Value | −0.09 * | −0.06 * | −0.10 * | −0.02 |

| Vacancy rate | −0.75 * | −0.37 * | −1.04 * | −0.07 * |

| Rent Value | 0.21 | −0.11 | −0.14 | 0.06 |

| Housing permits | −0.03 ** | −0.06 | −0.01 | 0.01 |

| Financial support | - | −0.02 * | −0.14 ** | −0.17 ** |

| Constant | −0.53 | 0.24 * | 0.28 ** | 2.94 ** |

| Pseudo R2 | 10.48% | 28.55% | 33.52% | 22.09% |

| N° Observations | 1347 | 291 | 291 | 291 |

| Before Brownfield Refinancing | After Brownfield Refinancing | Before Brownfield Refinancing | After Brownfield Refinancing | |

|---|---|---|---|---|

| Average | 0.87% | 0.55% | 89.89% | 96.29% |

| St. Dev. | 0.73% | 0.59% | 18.16% | 17.58% |

| Minimum | 0.05% | 0.00% | 18.16% | 17.58% |

| Maximum | 3.97% | 4.11% | 167.08% | 220.36% |

| t + 0 | t + 1 | t + 2 | t + 0 | t + 1 | t + 2 | |

|---|---|---|---|---|---|---|

| Incomeit | 0.00 | 0.00 | 0.00 | −0.32 ** | −0.36 ** | −0.34 * |

| Populationit | 0.00 ** | 0.00 ** | 0.00 ** | 0.01 ** | 0.01 ** | 0.01 ** |

| Homeownershipit | −0.01 ** | −0.01 ** | −0.01 ** | 0.42 ** | 0.50 ** | 0.48 ** |

| Crime rateit | 0.01 ** | 0.01 ** | 0.01 ** | −0.04 ** | −0.04 ** | −0.04 ** |

| Housing valueit | 0.03 | 0.01 | 0.01 | 0.03 ** | 0.03 * | 0.02 |

| Vacancy rate | 0.01 | 0.01 | 0.01 | 0.38 ** | 0.33 ** | 0.34 ** |

| Rent valueit | 0.01 | 0.01 | 0.01 | 0.00 | 0.00 | 0.00 |

| Housing permitsit | 0.01 ** | 0.01 ** | 0.01 ** | −0.00 ** | −0.00 ** | −0.00 ** |

| Brownfield financingit | −0.01 ** | −0.01 ** | −0.01 ** | 0.02 ** | 0.07 ** | 0.07 ** |

| Constant | 0.01 * | 0.01 * | 0.01 | 0.82 ** | 1.01 ** | 1.01 ** |

| Pseudo R2 | 0.75 | 0.76 | 0.76 | 0.21 | 0.11 | 0.11 |

| Fixed effects for the town | ☑ | ☑ | ☑ | ☑ | ☑ | ☑ |

| Fixed effects per year per year | ☑ | ☑ | ☑ | ☑ | ☑ | ☑ |

| N° towns | 169 | 169 | 169 | 169 | 169 | 169 |

| N° Observations | 2197 | 2018 | 1849 | 2197 | 2018 | 1849 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Gibilaro, L.; Mattarocci, G. Financing Brownfield Redevelopment and Housing Market Dynamics: Evidence from Connecticut. Buildings 2023, 13, 2791. https://doi.org/10.3390/buildings13112791

Gibilaro L, Mattarocci G. Financing Brownfield Redevelopment and Housing Market Dynamics: Evidence from Connecticut. Buildings. 2023; 13(11):2791. https://doi.org/10.3390/buildings13112791

Chicago/Turabian StyleGibilaro, Lucia, and Gianluca Mattarocci. 2023. "Financing Brownfield Redevelopment and Housing Market Dynamics: Evidence from Connecticut" Buildings 13, no. 11: 2791. https://doi.org/10.3390/buildings13112791