An Assessment Methodology for the Evaluation of the Impacts of the COVID-19 Pandemic on the Italian Housing Market Demand

,

,  ,

,

Abstract

:1. Introduction

2. Literature Review

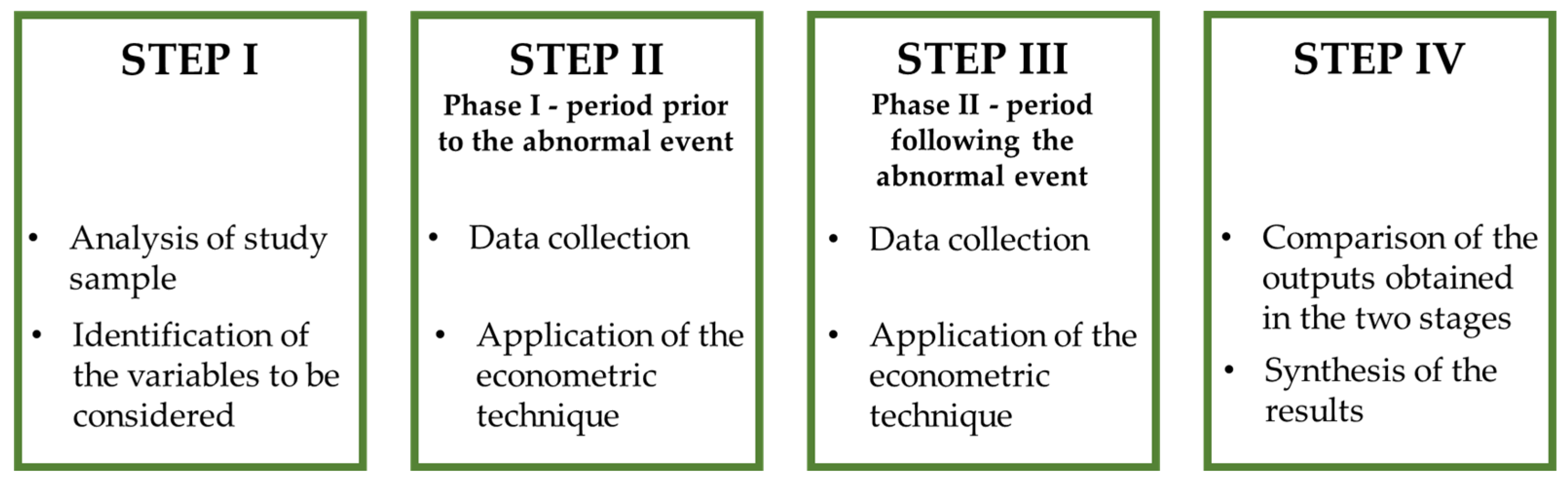

3. Methodology

4. Case Study

4.1. Implementing Step I of the Methodology

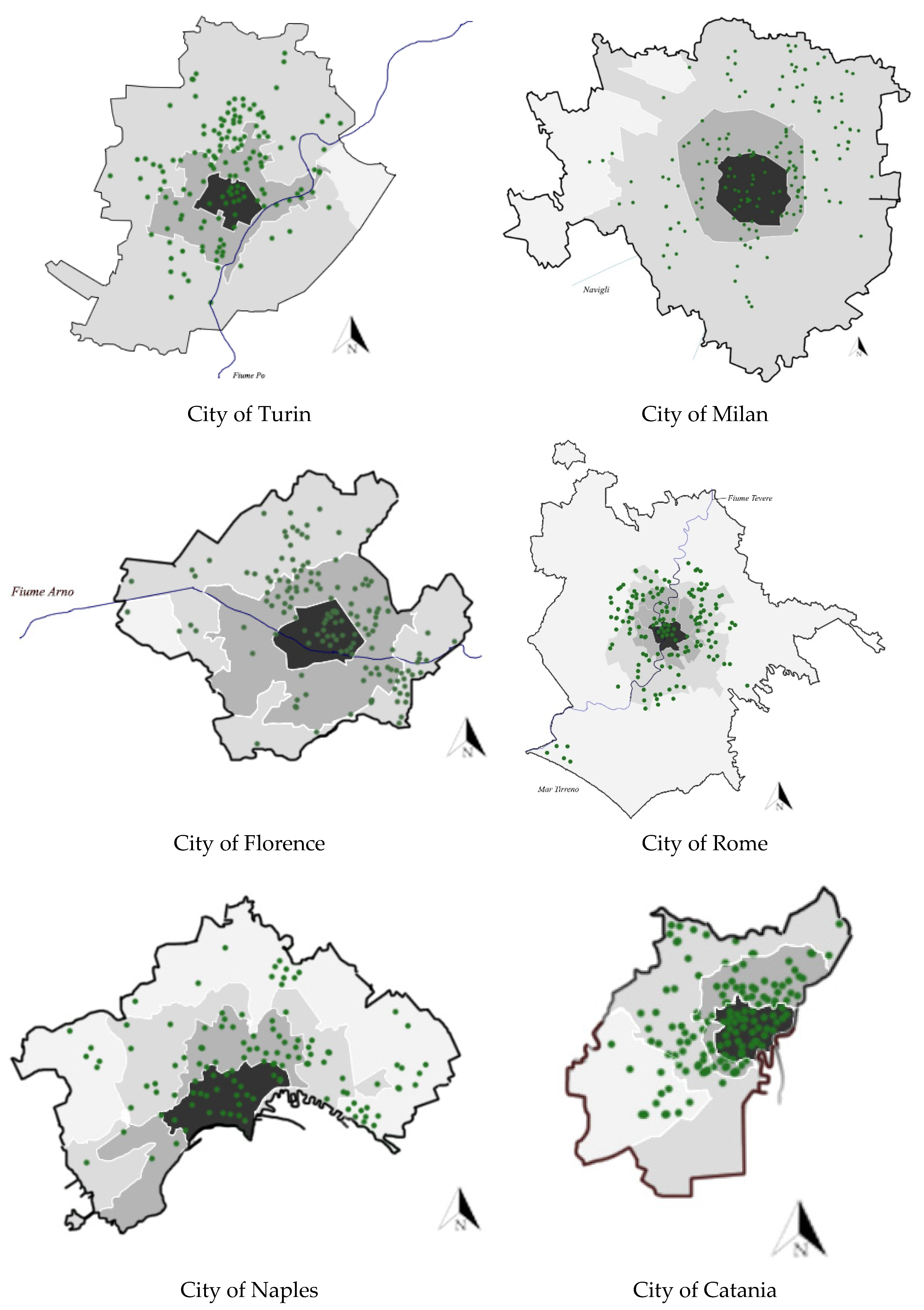

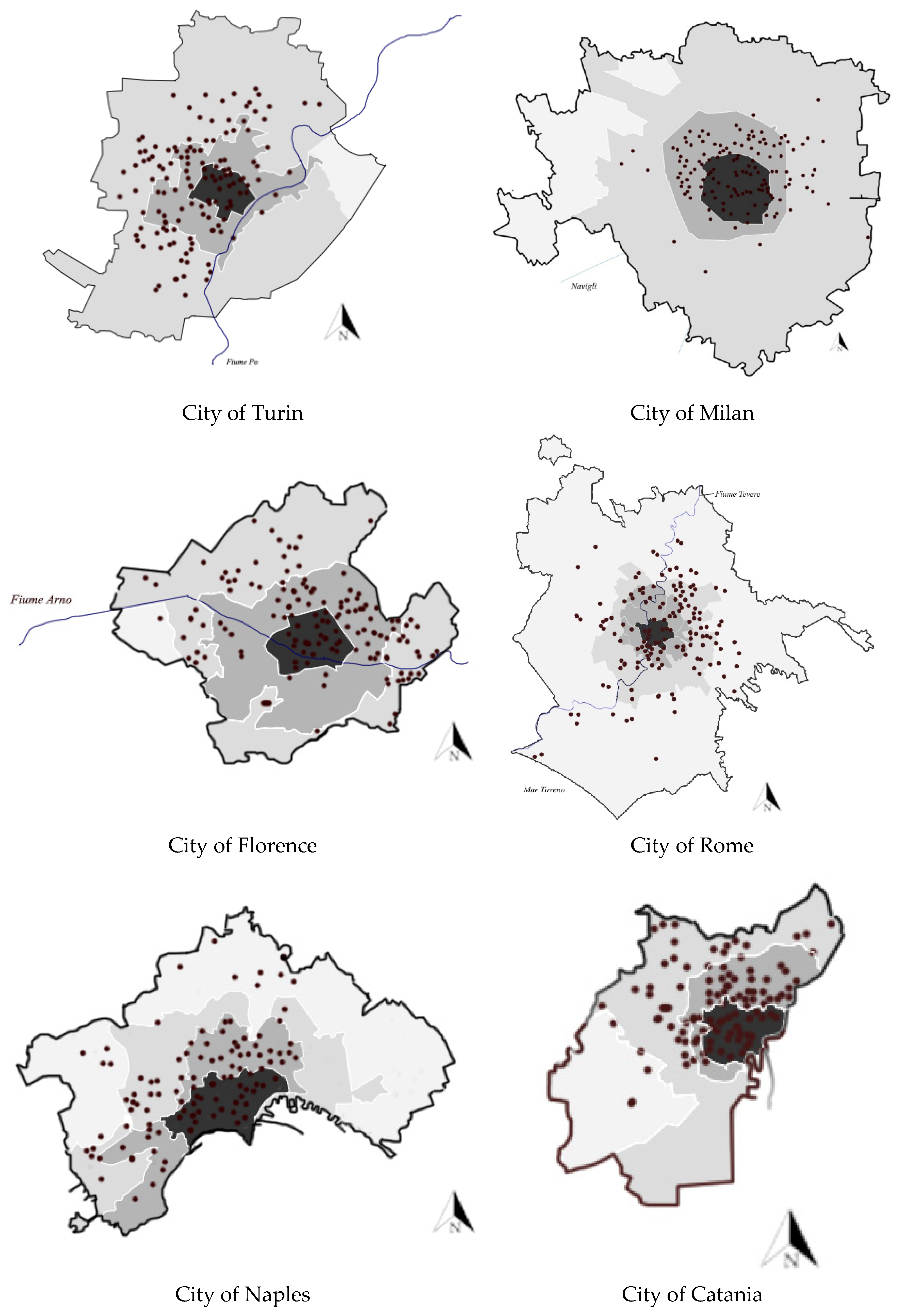

4.1.1. The Study Samples

4.1.2. Variables

4.2. Implementing Step II of the Methodology

4.2.1. Econometric Technique

- a0 is the constant additive term, i.e., the bias;

- n is the number of additive terms, i.e., the length of the polynomial expression (constant additive term excluded);

- ai is the numerical coefficient to be assessed for each additive term;

- Xi is the candidate explanatory variables to be selected by the model;

- (i, l)—with l = (1, …, 2j)—is the exponent of the l-th variable within the i-th additive term. It is selected by the technique among a set of possible exponents chosen by the user from a range of candidate real numbers;

- f is a function selected by the user from a set of candidate mathematical expression.

4.2.2. Application of the Technique to the Phase I: “Pre-COVID-19 Pandemic”

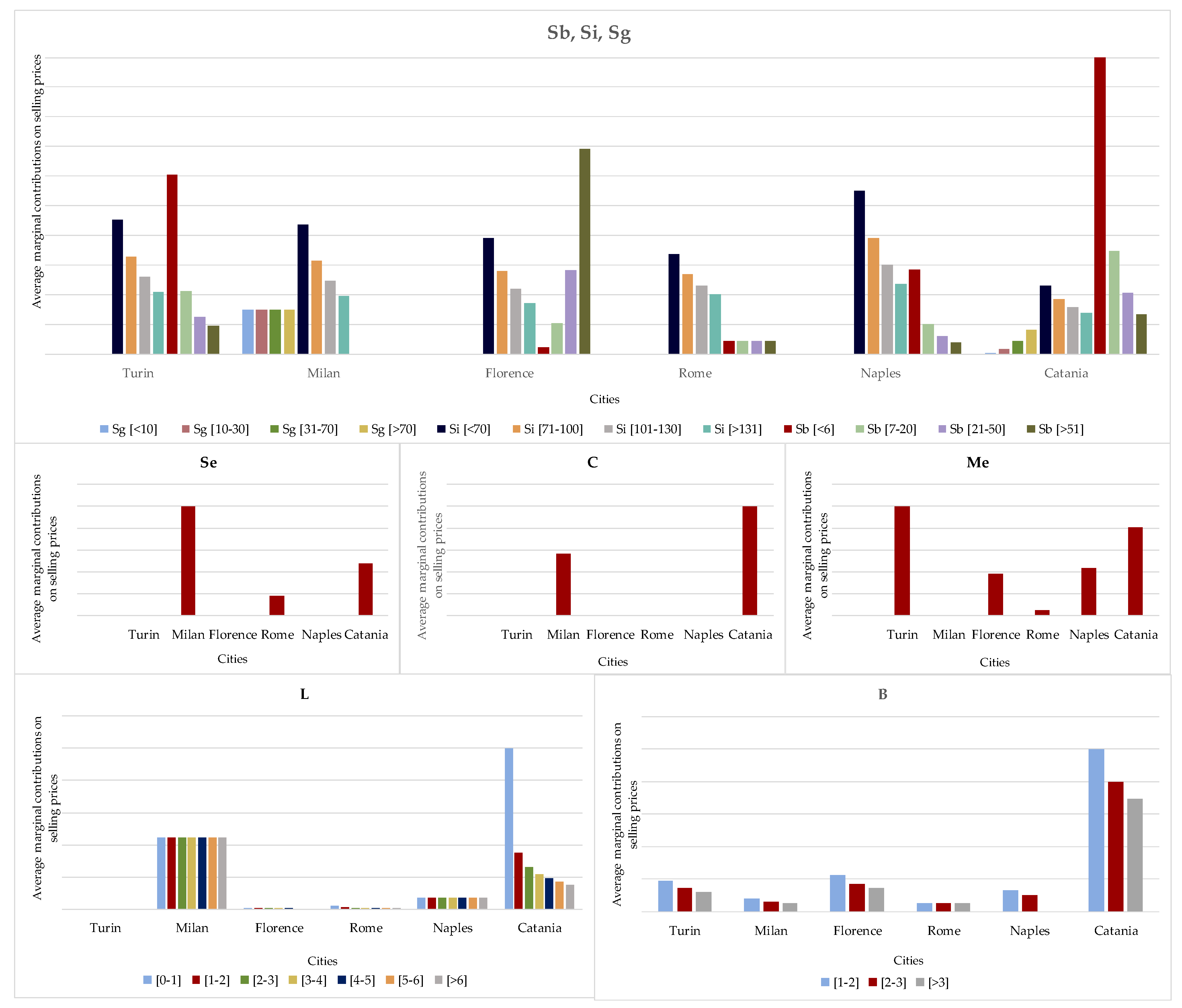

- A direct link between the internal surface and housing prices was detected for the six cities considered (+26% for the city of Turin, +37% for the city of Milan, +20% for the city of Florence, +38% for the city of Naples, +25% for the city of Rome, and + 6% for the city of Catania, considering an average variation of 40 m2).

- Variables related to direct and private accessory surfaces, i.e., balconies or terraces and gardens, had different influences; for example, for the city of Turin the presence of balconies was strongly appreciated up to a surface of 9.50 m2 (+22%), beyond which the contribution on the prices progressively decreased (an average +5%). The marginal contribution on selling prices provided by the biggest balconies or terraces and gardens surfaces was confirmed by the microeconomics principle, for which the relevance of a good was strongly associated with the need of it (known as law of decreasing marginal utility). Moreover, the variable was also directly linked to the selling prices in the city of Milan, for which the variation between the absence and the presence of balconies was higher (+14%), compared with the subsequent balconies area (+4%). The model selected for the city of Florence proved a growth of the residential values in correspondence with the presence of balconies (+31% compared with its absence), and a progressive attenuation in prices increase for larger balcony surface areas (+17%). Similarly, for the city of Catania, a direct correlation between the variable related to the surface of balconies Sb and housing prices was found, with a relevant initial variation equal to +19% between the properties without balconies and those characterized by the balcony presence. Then, the percentage variation decreased, and was equal on average to +4%. The presence of private gardens was not included in the models of the city of Turin, Naples, Catania and Milan, due to the most common residential typology sold in those markets, i.e., residential units located in apartment buildings. A decrease in housing prices was found for the city of Florence model (−11%), in correspondence with properties with private gardens. With reference to the study sample collected, only 6% of the total individuals included were characterized by this domestic space, and all were localized in the higher hydrogeological risk areas of the city. Furthermore, a significant influence of private green area was detected for the city of Rome, especially due to the position of the sample residential units, in particular, valued urban zones (in the proximity of the Appia Antica Regional Park).

- The models selected showed a lack of appreciation for the presence of condominium areas, in the second half of 2019, in the cites of Naples, Turin, Florence and Rome. On the other hand, the price functions generated by the EPR-MOGA technique for the cities of Catania and Milan denoted a relevant contribution—positive for the first city, negative for the second—deriving from the presence of these spaces on selling prices. In particular, for the city of Catania, it should be outlined that most properties collected in the study sample were located in prestigious residential complexes, in which the shared gardens were in excellent conservative conditions, and were for the exclusive use of inhabitants. On the other hand, for the city of Milan, most residential units in the study samples considered for the external condominium area (41% of the total sample individuals) were constituted by economic buildings, for which other factors could negatively influence the selling prices.

- The floor level on which each residential property was located influenced the housing dynamics in the cities of Florence, Rome, Naples and Catania. The model selected for the city of Naples indicated an average variation on selling prices equal to +7%, and a higher significance in correspondence with the passage from the ground floor to the first floor (+25%), and an attenuation for the highest floors, from level eight upward (+5%). For the city of Catania, a direct functional correlation was found on average equal to +2%, and a relevant appreciation for the ground floor was detected, if the properties were characterized by condominium areas, compared with the higher floors. The same positive link typology was revealed with regards to the study sample collected for the city of Rome, for which the highest floor levels were those most appreciated, compared with the lowest ones. In addition, in the central trade area, the location on the highest floors allowed panoramic views that implied a strong influence on housing values. A moderate contribution on selling prices was observed for the city of Florence, with a marginal price equal to 4%.

- The central municipal trade area variable was included in the models selected for the cities of Rome and Catania; the semi-central areas appeared in the models of the cities of Turin, Catania and Naples, and the peripheral area factor was also present in the price functions of Turin, Florence and Naples. It should be outlined that the semi-central municipal trade area was particularly appreciated in the context of the city of Naples (+25%) and in the city of Catania (+52%), whereas a negative influence was given by the position of housing properties in the semi-central trade area and peripheral area of the city of Turin (−33% and −38%, respectively). In the city of Florence, the selling price variation determined by the localization of the property in the peripheral area was equal to –18%, whereas for the city of Naples a decrease in housing prices equal to –20% was recorded for the peripheral trade area. The location of properties in the central municipal trade area of the city of Rome determined an increase in selling price equal to +13%, whereas this was equal to +5% in the central area of Catania.

4.3. Implementating Step III of the Methodology

4.4. Implementing Step IV of the Methodology

5. Conclusions

Supplementary Materials

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Banerjee, D.; Rai, M. Social isolation in COVID-19: The impact of loliness. Int. J. Soc. Psychiatry 2020, 66, 525–527. [Google Scholar] [CrossRef]

- Cvetković, D.; Nešović, A.; Terzić, I. Impact of people’s behavior on the energy sustainability of the residential sector in emergency situations caused by COVID-19. Energy Build. 2021, 230, 110532. [Google Scholar] [CrossRef]

- D’Alessandro, D.; Gola, M.; Appolloni, L.; Dettori, M.; Fara, G.M.; Rebecchi, A.; Settimo, G.; Capolongo, S. COVID-19 and living space challenge. Well-being and public health recommendations for a healthy, safe, and sustainable housing. Acta Biomed. 2020, 91, 61–75. [Google Scholar]

- Il Sole 24 Ore. Covid e Crisi Economica, Perchè l’Italia sta Pagando Più di Altri Paesi. Available online: https://www.ilsole24ore.com/art/covid-e-crisi-economica-perche-l-italia-sta-pagando-piu-altri-paesi-ADkpbDVB (accessed on 25 July 2021).

- International Monetary Fund (IMF). Annual Report. Available online: https://www.imf.org/external/pubs/ft/ar/2020/eng/downloads/imf-annual-report-2020.pdf (accessed on 25 May 2021).

- Forbes. Available online: https://www.forbes.com/sites/petertaylor/2020/10/11/covid-19-has-changed-the-housing-market-forever-heres-where-americans-are-moving-and-why/?sh=3d840be461fe (accessed on 25 October 2021).

- Inoue, H.; Todo, Y. The propagation of economic impacts through supply chains: The case of a mega-city lockdown to prevent the spread of COVID-19. PLoS ONE 2020, 15, e0239251. [Google Scholar] [CrossRef]

- Urban Index. Available online: https://www.urbanindex.it/indicatori/indice-di-affollamento-delle-abitazioni/ (accessed on 25 October 2021).

- Ugeo Urbistat. Available online: https://ugeo.urbistat.com/AdminStat/it/it/classifiche/componenti-della-famiglia/province/italia/380/1 (accessed on 25 October 2021).

- World Economic Forum (WEF). Resetting the Future of Work Agenda: Disruption and Renewal in a Post-COVID World. Available online: https://www.weforum.org/whitepapers/resetting-the-future-of-work-agenda-disruption-and-renewal-in-a-post-covid-world (accessed on 25 July 2021).

- Istituto Nazionale di Statistica (ISTAT). Il Mercato del Lavoro 2020. Una Lettura Integrata. Available online: https://www.istat.it/it/archivio/253812 (accessed on 25 May 2021).

- Il Sole 24 Ore. Il Cnr Studia le Relazioni tra Verde Urbano e Impatto Della Pandemia Nelle Città. Available online: https://www.ilsole24ore.com/art/il-cnr-studia-relazioni-verde-urbano-e-impatto-pandemia-citta-AD7uv2EB (accessed on 25 July 2021).

- Capuano, A.; Lanzetta, A. #Curacittà Roma. La Sapienza della Cura Urbana; Quodlibet: Rome, Italy, 2020; pp. 59–62. [Google Scholar]

- Amerio, A.; Brambilla, A.; Morganti, A.; Aguglia, A.; Bianchi, D.; Santi, F.; Costantini, L.; Capolongo, S. COVID-19 Lockdown: Housing Built Environment’s. Effects on Mental Health. Int. J. Environ. Res. Public Health 2020, 17, 5973. [Google Scholar] [CrossRef]

- Mattiacci, A.; Nocenzi, M.; Sfodera, F.; Sofia, C. Le conseguenze sull’attività professionale: Tra incertezze e opportunità. In La Società Catastrofica, vita e Relazioni Sociali ai Tempi dell’Emergenza COVID-19; Lombardo, C., Mauceri, S., Eds.; FrancoAngeli: Milan, Italy, 2020; pp. 100–130. [Google Scholar]

- Osservatorio Residenziale Tecnocasa. Available online: https://news.tecnocasagroup.it/ufficio-studi/osservatorio_residenziale/ (accessed on 15 January 2021).

- Centro Studi Gabetti—Report Real Estate—I Trend Post COVID Settore per Settore. Available online: https://www.gabettigroup.com/it-it/ufficio-studi (accessed on 28 June 2021).

- Casa.it—La Casa Che Vorrei. I Desideri, I Sogni, le Aspettative Degli Italiani per la Casa del Domani. Available online: https://blog.casa.it/2021/01/21/classifica-case-cercate-2020 (accessed on 25 July 2021).

- Banca d’Italia—Indagine sul Mercato Delle Abitazioni. Available online: https://www.bancaditalia.it/pubblicazioni/sondaggio-abitazioni/index.html (accessed on 25 July 2021).

- Awada, M.; Becerik-Gerber, B.; Hoque, S.; O’Neill, Z.; Pedrielli, G.; Wen, J.; Wu, T. Ten questions concerning occupant health in buildings during normal operations and extreme events including the COVID-19 pandemic. Build. Environ. 2020, 18815, 107480. [Google Scholar] [CrossRef]

- Cheshmehzangi, A. Housing and Health evaluation related to general comfort and indoor thermal comfort satisfaction during the COVID-19 lockdown. J. Hum. Behav. Soc. Environ. 2020, 31, 184–209. [Google Scholar] [CrossRef]

- ASVIS. Available online: https://asvis.it/public/asvis/files/traduzione_ITA_SDGs_&_Targets.pdf (accessed on 10 November 2021).

- Belasen, A.R.; Polachek, S.W. How disasters affect local labor markets: The effects of hurricanes in Florida. J. Hum. Resour. 2020, 44, 251–276. [Google Scholar] [CrossRef]

- Manganelli, B.; Vona, M.; De Paola, P. Evaluating the cost and benefits of earthquake protection of buildings. J. Eur. Real Estate Res. 2018, 11, 263–278. [Google Scholar] [CrossRef]

- Dell, M.; Jones, B.F.; Olken, B.A. Temperature shocks and economic growth: Evidence from the last half century. Am. Econ. J. Macroecon. 2012, 4, 66–95. [Google Scholar] [CrossRef] [Green Version]

- Dell, M.; Jones, B.F.; Olken, B.A. What do we learn from the weather? The new climate-economy literature. J. Econ. Lit. 2014, 52, 740–798. [Google Scholar] [CrossRef] [Green Version]

- Cavallo, E.; Galiani, S.; Noy, I.; Pantano, J. Catastrophic natural disasters and economic growth. Rev. Econ. Stat. 2013, 95, 1549–1561. [Google Scholar] [CrossRef] [Green Version]

- Hsiang, S.M.; Jina, A.S. The Causal Effect of Environmental Catastrophe on Long-Run Economic Growth: Evidence from 6.700 Cyclones; Working Paper n. 20352; National Bureau of Economic Research: Cambridge, MA, USA, 2014. [Google Scholar]

- Burke, M.; Hsiang, S.M.; Miguel, E. Global non-linear effect of temperature on economic production. Nature 2015, 527, 235–239. [Google Scholar] [CrossRef]

- Cattaneo, C.; Peri, G. The migration response to increasing temperatures. J. Dev. Econ. 2016, 122, 127–146. [Google Scholar] [CrossRef] [Green Version]

- Boustan, L.P.; Kahn, M.E.; Rhode, P.W.; Yanguas, M.L. The effect of natural disasters on economic activity in US counties: A century of data. J. Urban Econ. 2020, 118, 103257. [Google Scholar] [CrossRef]

- Naoi, M.; Seko, M.; Sumita, K. Earthquake risk and housing prices in Japan: Evidence before and after massive earthquakes. Reg. Sci. Urban Econ. 2009, 39, 658–669. [Google Scholar] [CrossRef] [Green Version]

- Nakagawa, M.; Saito, M.; Yamaga, H. Earthquake risks and land prices: Evidence from the Tokyo Metropolitan Area. Jpn. Econ. Rev. 2009, 60, 87–99. [Google Scholar] [CrossRef] [Green Version]

- Nakagawa, M.; Saito, M.; Yamaga, H. Earthquake Risks and Housing Rents: Evidence from the Tokyo Metropolitan Area. Reg. Sci. Urban Econ. 2007, 37, 87–99. [Google Scholar] [CrossRef] [Green Version]

- Del Giudice, V. Estimo e Valutazione Economica dei Progetti, Profili Metodologici e Applicazioni al Settore Immobiliare; Paolo Loffredo Iniziative Editoriali: Naples, Italy, 2015. [Google Scholar]

- Beron, K.J.; Murdoch, J.C.; Thayer, M.A.; Vijverberg, W.P.M. An analysis of the housing market before and after the 1989 Loma Prieta earthquake. Land Econ. 1997, 73, 101–113. [Google Scholar] [CrossRef]

- Kawawaki, Y.; Ota, M. The influence of the Great Hanshin-Awaji Earthquake on the local housing market. Rev. Urban Reg. Dev. Stud. 1996, 8, 220–233. [Google Scholar] [CrossRef]

- Sardaro, R.; La Sala, P.; Roselli, L. How does the land market capitalize environmental, historical and cultural components in rural areas? Evidences from Italy. J. Environ. Manag. 2020, 269, 110776. [Google Scholar] [CrossRef]

- Dube, J.; AbdelHalim, M.; Devaux, N. Evaluating the impact of floods on housing price using a spatial matching difference-in-difference approach. Sustainability 2021, 13, 804. [Google Scholar] [CrossRef]

- Hallstrom, D.G.; Smith, V.K. Market responses to hurricanes. J. Environ. Econ. Manag. 2005, 50, 541–561. [Google Scholar] [CrossRef]

- Seo, J.; Oh, J.; Kim, J. Flood risk awareness and property values: Evidences from Seoul, South Korea. Int. J. Urban Sci. 2020, 25, 233–251. [Google Scholar] [CrossRef]

- Kim, S.K. The economic effects of climate change adaptation measures: Evidence from Miami-Dade County and New York City. Sustainability 2020, 12, 1097. [Google Scholar] [CrossRef] [Green Version]

- Rehse, D.; Riordan, R.; Rottke, N.; Zietz, J. The effects of uncertainty on market liquidity: Evidence from Hurricane Sandy. J. Financ. Econ. 2019, 134, 318–332. [Google Scholar] [CrossRef]

- Keskin, B.; Dunning, R.; Watkins, C. Modelling the impact of earthquake activity on real estate values: A multi-level approach. J. Eur. Real Estate Res. 2017, 10, 73–90. [Google Scholar] [CrossRef]

- Kinoshita, S. Conjoint analysis of Japanese households’ energy-saving behavior after the earthquake: The role of the preferences for renewable energy. Energy Environ. 2020, 31, 676–691. [Google Scholar] [CrossRef]

- Caputo, M. The memory response of populations and markets to extreme events. Econ. Politica 2012, 29, 261–282. [Google Scholar]

- Caputo, M. The role of memory in modeling social and economic cycles of extreme events. In A Handbook of Alternative Theories of Public Economics; Edward Elgar Publishing: Northampton, MA, USA, 2014; pp. 245–259. [Google Scholar]

- Anand, P. Foundations of Rational Choice Under Risk; Clarendon Press: Oxford, UK, 1993. [Google Scholar]

- Kay, D.; Geisler, C.; Bills, N. Residential preferences: What’s terrorism got to do with it? Rural. Sociol. 2010, 75, 426–454. [Google Scholar] [CrossRef]

- Dittmar, H.; Campbell, S.C. Will September 11 bring us together or push us apart? The war on terror and metropolitan stability. Transp. Q. 2002, 56, 43–49. [Google Scholar]

- Abadie, A.; Dermisi, S. Is terrorism eroding agglomeration economies in Central Business Districts? Lessons from the office real estate market in downtown Chicago. J. Urban Econ. 2008, 64, 451–463. [Google Scholar] [CrossRef]

- Morita, T.; Managi, S. Consumers’ willingness to pay for electricity after the Great East Japan Earthquake. Econ. Anal. Policy 2015, 48, 82–105. [Google Scholar] [CrossRef]

- Luktkepohl, H. New Introduction to Multiple Time Series Analysis; Springer: Berlin/Heidelberg, Germany, 2005. [Google Scholar]

- Christiano, L.J.; Eichenbaum, M.; Evans, C.L. Monetary policy shocks: What have we learned and to what end? In Handbook of Macroeconomics; Elsevier: Amsterdam, The Netherlands, 1999; Volume 1, pp. 65–148. [Google Scholar]

- Liu, C.; Hoi, S.C.; Zhao, P.; Sun, J. Online ARIMA algorithms for time series prediction. In Proceedings of the Thirtieth AAAI Conference on Artificial Intelligence, Phoenix, AZ, USA, 12–17 February 2016. [Google Scholar]

- Chavleishvili, S.; Manganelli, S. Forecasting and Stress Testing with Quantile Vector Autoregression; Working Paper Series 2330; ECB: Frankfurt, Germany, 2019. [Google Scholar]

- Stanghellini, S.; Breglia, M. Valutare Nell’incertezza, un Modello Previsivo 2020–2025. Available online: https://www.scenari-immobiliari.it/2020/04/30/valutare-nellincertezza-un-modello-previsivo-2020-2025/ (accessed on 25 July 2021).

- Tedesco, M.; McAlpine, S.R.; Porter, J. Exposure of real estate properties to the 2018 Hurricane Florence flooding. Nat. Hazards Earth Syst. Sci. 2020, 20, 907–920. [Google Scholar] [CrossRef] [Green Version]

- Fischer, T.; Su, B.; Wen, S. Spatio-Temporal Analysis of Economic Losses from Tropical Cyclones in Affected Provinces of China for the Last 30 Years (1984–2013). Nat. Hazards Rev. 2015, 16, 04015010. [Google Scholar] [CrossRef]

- Cheema, A.R.; Mehmood, A.; Imran, M. Learning from the past: Analysis of disaster management structures, policies and institutions in Pakistan. Disaster Prev. Manag. 2016, 25, 449–463. [Google Scholar] [CrossRef]

- Aderibigbe, T.; Chi, H. Investigation of Florida housing prices using predictive time series model. In Proceedings of the Practice and Experience on Advanced Research Computing, Pittsburgh, PA, USA, 22–26 July 2018. [Google Scholar]

- Tanrıvermiş, H. Possible impacts of COVID-19 outbreak on real estate sector and possible changes to adopt: A situation analysis and general assessment on Turkish perspective. J. Urban Manag. 2020, 9, 263–269. [Google Scholar] [CrossRef]

- Wang, B. How Does COVID-19 Affect House Prices? A Cross-City Analysis. J. Risk Financ. Manag. 2021, 14, 47. [Google Scholar] [CrossRef]

- Li, X.; Zhang, C. Did the COVID-19 Pandemic Crisis Affect Housing Prices Evenly in the U.S.? Sustainability 2021, 13, 12277. [Google Scholar] [CrossRef]

- Nuredini, B. Impact of the COVID-19 Pandemic on the Global Real Estate Market; University for Business and Technology: Pristina, Kosovo, 2020. [Google Scholar]

- Atlantic Council. Available online: https://www.atlanticcouncil.org/blogs/new-atlanticist/can-we-compare-the-covid-19-and-2008-crises/ (accessed on 10 November 2021).

- ISTAT—Istituto Nazionale di Statistica—Banca Dati. Available online: http://dati.istat.it/ (accessed on 23 June 2021).

- Observatory of the Real Estate Market OMI of the Italian Revenue Agency. Available online: https://www.agenziaentrate.gov.it/portale/web/guest/schede/fabbricatiterreni/omi/banche-dati/quotazioni-immobiliari (accessed on 21 May 2021).

- Simonotti, M. Un’applicazione dell’analisi di regressione multipla nella stima di appartamenti. GenioRurale 1991, 2, 209–227. [Google Scholar]

- Curto, R. La quantificazione e costruzione di variabili qualitative stratificate nella multiple regression analysis (MRA) applicata ai mercati immobiliari. Aestimum 1994, 2, 195–223. [Google Scholar]

- Del Giudice, V.; De Paola, P. Spatial analysis of residential real estate rental market with Geoadditive Models. In Advances in Automated Valuation Modeling; D’Amato, M., Kauko, T., Eds.; Springer: Cham, Switzerland, 2017. [Google Scholar]

- D’Amato, M. Location value response surface model as Automated Valuation Methodology: A case in Bari. In Advances in Automated Valuation Modeling; D’Amato, M., Kauko, T., Eds.; Springer: Cham, Switzerland, 2017. [Google Scholar]

- Green, S.B. How many subjects does it take to do a regression analysis? Multivar. Behav. Res. 1991, 26, 499–510. [Google Scholar] [CrossRef]

- Bourassa, S.; Hoesli, M.; Peng, V.S. Do Housing submarkets really matter? J. Hous. Econ. 2003, 12, 12–28. [Google Scholar] [CrossRef] [Green Version]

- Morano, P.; Guarini, M.R.; Tajani, F.; Di Liddo, F.; Anelli, D. Incidence of Different Types of Urban Green Spaces on Property Prices. A Case Study in the Flaminio District of Rome (Italy). In Computational Science and Its Applications; Lecture Notes in Computer Science; Springer: Singapore, 2019; Volume 11622, pp. 23–34. [Google Scholar]

- Guarini, M.R.; Chiovitti, A. Definition of luxury dwellings features for regulatory purposes and for formation of market price. In Computational Science and Its Applications; Lecture Notes in Computer Science; Springer: Singapore, 2016; Volume 9788, pp. 503–518. [Google Scholar]

- Bengochea Morancho, A. A hedonic valuation of urban green areas. Landsc. Urban Plan. 2003, 66, 35–41. [Google Scholar] [CrossRef]

- Sirmans, G.; MacDonald, L.; Macpherson, A.; Zietz, E. The Value of Housing Characteristics: A Meta Analysis. J. Real Estate Finan. Econ. 2006, 33, 215–240. [Google Scholar] [CrossRef]

- Zietz, J.; Zietz, E.; Sirmans, G. Determinants of House Prices: A Quantile Regression Approach. J. Real Estate Financ. Econ. 2008, 37, 317–333. [Google Scholar] [CrossRef]

- Bui, T.N. A study of factors influencing the price of apartments: Evidence from Vietnam. Manag. Sci. Lett. 2020, 10, 2287–2292. [Google Scholar] [CrossRef]

- Wing Chau, K.; Kei Wong, S.; Yim Yiu, C. The value of the provision of a balcony in apartments in Hong Kong. Prop. Manag. 2004, 22, 250–264. [Google Scholar] [CrossRef] [Green Version]

- Taltavull, P.; McGreal, S. Measuring price expectations: Evidence from the Spanish housing market. J. Eur. Real Estate Res. 2009, 2, 186–209. [Google Scholar] [CrossRef]

- Goodman, A.C.; Thibodeau, T.G. The Spatial Proximity of Metropolitan Area Housing Submarkets. Real Estate Econ. 2007, 35, 209–232. [Google Scholar] [CrossRef]

- Locurcio, M.; Morano, P.; Tajani, F.; Di Liddo, F. An Innovative GIS-Based Territorial Information Tool for the Evaluation of Corporate Properties: An Application to the Italian Context. Sustainability 2020, 12, 5836. [Google Scholar] [CrossRef]

- Giustolisi, O.; Savic, D. Advances in data-driven analyses and modelling using EPR-MOGA. J. Hydroinform. 2009, 11, 225–236. [Google Scholar] [CrossRef]

- Tajani, F.; Morano, P.; Torre, C.M.; Di Liddo, F. An analysis of the influence of property tax on housing prices in the Apulia region (Italy). Buildings 2017, 7, 67. [Google Scholar] [CrossRef] [Green Version]

- Morano, P.; Rosato, P.; Tajani, F.; Di Liddo, F. An Analysis of the Energy Efficiency Impacts on the Residential Property Prices in the City of Bari (Italy). In Values and Functions for Future Cities; Springer: Berlin/Heidelberg, Germany, 2020; pp. 73–88. [Google Scholar]

- Di Liddo, F.; Morano, P.; Tajani, F.; Torre, C.M. An innovative methodological approach for the analysis of the effects of urban interventions on property prices [Un approccio metodologico innovativo per l’analisi degli effetti degli interventi di trasformazione urbana sui valori immobiliari]. Valori e Valutazioni 2020, 26, 25–49. [Google Scholar] [CrossRef]

- Lynch, A.K.; Rasmussen, D.W. Proximity, neighborhood and the efficacy of exclusion. Urban Stud. 2004, 41, 285–298. [Google Scholar] [CrossRef]

- Draper, N.R.; Smith, H. Applied Regression Analysis; John Wiley and Sons: Hoboken, NJ, USA, 2014. [Google Scholar]

- Frew, J.; Wilson, B. Estimating the connection between location and property value. J. Real Estate Pract. Educ. 2002, 5, 17–25. [Google Scholar] [CrossRef]

- Malpezzi, S.; Chun, G.H.; Green, R.K. New Place-to-Place Housing Price Indexes for U.S. Metropolitan Areas, and Their Determinants. Real Estate Econ. 1998, 26, 235–274. [Google Scholar] [CrossRef]

- Selim, H. Determinants of house prices in Turkey: Hedonic regression versus artificial neural network. Expert Syst. Appl. 2009, 36, 2843–2852. [Google Scholar] [CrossRef]

- Efron, B. Estimating the error rate of a prediction rule: Improvement on cross-validation. J. Am. Stat. Assoc. 1983, 78, 316–330. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Factor | Turin | Milan | Florence | Rome | Naples | Catania |

|---|---|---|---|---|---|---|

| Number of inhabitants (n.) | 870,952 | 1,396,059 | 372,038 | 2,837,332 | 962,589 | 311,402 |

| Surface (km2) | 130.01 | 181.67 | 102.32 | 1287.36 | 119.02 | 182.90 |

| Population density (inhabitant/km2) | 6699.12 | 7684.59 | 3636.02 | 2203.99 | 8087.62 | 1702.58 |

| Old age index | 204.10 | 196.30 | 220.40 | 162.60 | 114.40 | 139.60 |

| Square meters per occupant in occupied residential units (m2) | 41.00 | 41.50 | 41.40 | 29.40 | 31.70 | 37.10 |

| Number of residential buildings (n.) | 36,158 | 42,980 | 31,070 | 137,021 | 40,755 | 28,988 |

| Empty residential properties (n.) | 36,779 | 37,073 | 5164 | 118,531 | 14,140 | 28,567 |

| Per capita income (€) | 25,015 | 34,046 | 26,503 | 28,241 | 22,434 | 20,179 |

| Category | Acronym | Denomination | Description | Measurement Unit | Variable Typology | References |

|---|---|---|---|---|---|---|

| Surfaces | Si | Internal area | Internal surface of the property | m2 | Quantitative continuous | [77,78,79,80] |

| Sb | Surface of balconies or terraces | Net external surface of balconies or terraces directly accessible from the property. | m2 | Quantitative continuous | [80,81] | |

| Sg | Surface of private garden | Net external surface of gardens directly accessible from the property. | m2 | Quantitative continuous | [77,82] | |

| Se | Presence of condominium areas | External surfaces accessible from the condominium areas of the building and not for the exclusive use of the property. | - | Dummy (1 or 0) | [82] | |

| Maintenance conditions of the property | Me | Excellent | The “excellent” state are related to properties characterized by high construction and aesthetic quality. | - | Dummy (1 or 0) | [78,80,82] |

| Mg | Good | The “good” state refers to properties whose maintenance conditions are acceptable and whose functions can be carried out without heavy refurbishment interventions. | - | Dummy (1 or 0) | ||

| Mp | Poor | The “poor” state refers to properties whose maintenance conditions are not acceptable and heavy refurbishment interventions are needed. | - | Dummy (1 or 0) | ||

| Internal services | B | Number of bathrooms | Number of toilets for the exclusive use of the property. | n. | Quantitative discrete | [77,78,79,80] |

| Localization in the building | L | Floor level | Floor level on which the property is located. | n. | Quantitative discrete | [77,79] |

| Building age | Yc | Building construction year | Construction year of the building within which the residential unit is located. The variable is assessed as the difference between the year 2019 (Phase I) or 2021 (Phase II) and the construction year. | n. | Quantitative continuous | [77,79] |

| Municipal trade area | C | Central | Municipal trade area in which the property is located according to the geographical distribution developed by the Real Estate Market Observatory (OMI) of the Italian Revenue Agency. | - | Dummy (1 or 0) | [83,84] |

| Sc | Semi-central | - | Dummy (1 or 0) | |||

| P | Peripheral | - | Dummy (1 or 0) | |||

| Sub | Suburban | - | Dummy (1 or 0) | |||

| OMI quotation | Vm | Average market value | Average quotation between the maximum value and the minimum value for civil properties determined for the Phase I (“pre-COVID-19 pandemic”) and the Phase II (“COVID-19 pandemic in progress”) by consulting the Real Estate Market Observatory (OMI) of the Italian Revenue Agency. | € | Quantitative continuous | [84] |

| City | Model | CoD (%) |

|---|---|---|

| Turin | Y = + 2.3105 · Vm0.5 − 0.39501 · Sc0.5 · Mg0.5 − 15.6167 · Yc2 · P2 · Mg0.5 + − 38.8898 · Sb0.5 · Yc · P2 · Me2 · Vm2 + 1.402 · Sb0.5 · B + 3.1882 · Si0.5 + 8.4518 | 81.48 |

| Milan | Y = + 0.92925 · Vm0.5 − 2.1509 · Se0.5 · Yc0.5 − 0.72176 · Sb0.5 · Mg0.5 + 8.6914 · · Sb0.5 · B2 · Yc + 8.9345 · Si0.5 + 7.7893 · Si0.5 · Se2 · Yc − 5.0165 · Si + 9.146 | 66.44 |

| Florence | Y = + 1.8883 · B0.5 · Vm − 2.3554 · B · Yc0.5 · Vm − 19.929 · Sg · Sb0.5 · Yc0.5 + + 2.2829 Si0.5 + 48.0618 · Si0.5 · Sg · Yc2 + 4.2736 · (Si + Sb + Sg)0.5 · L0.5 · Yc · Vm + + 2.3275 · (Si + Sb + Sg)0.5 · Sb0.5 · B0.5 · Me2 − 3.0961 · (Si + Sb + Sg) · Si · L0.5 · P 0.5 + + 10.5998 | 84.02 |

| Rome | Y = + 2.0813 · Vm0.5 + 0.77051 · L0.5 · B · Me0.5 + 7.5564 · L0.5 · B2 · Yc + + 2833.437 · Sg ·L2 · Mg0.5 · Vm2 + 2.6857 · Si0.5 + 579.0223 · (Si + Sb + Sg)0.5 · Sb2 · L2 · B0.5 · C0.5 · Mg0.5 + 9.7199 | 86.23 |

| Naples | Y = + 1.6557 · Sc0.5 · Me0.5 · Vm + 2.8709 · B0.5 · Vm0.5 + 4.2863 · Si0.5 − + 22.669 · Si · Yc2 · Mg0.5 + 75.9095 · Si2 · L0.5 · Yc · P0.5 + 9.1516 | 83.13 |

| Catania | Y = − 0.85036 · Yc0.5 + 0.90016 · L0.5 · Sc2 · Me0.5 + 8.2726 · L · Yc2 · C2 · Vm0.5 + + 3.147 · Sb0.5 · B · Vm + 25.5332 · Sb · Se · L0.5 + 2.6756 · Si0.5 − 9880.7007 · Si2 · · Sb2 · Se0.5 · L2 · Vm0.5 + 10.2077 | 74.08 |

| No. Iteration | Turin | Milan | Florence | Rome | Naples | Catania | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Training Set | Validation Set | Training Set | Validation Set | Training Set | Validation Set | Training Set | Validation Set | Training Set | Validation Set | Training Set | Validation Set | |

| Iteration 1 | 2.121 | 2.235 | 2.899 | 2.899 | 2.196 | 2.318 | 2.121 | 2.121 | 2.256 | 2.256 | 3.801 | 3.821 |

| Iteration 2 | 2.845 | 2.922 | 3.584 | 3.584 | 2.845 | 2.845 | 2.845 | 2.845 | 2.845 | 2.845 | 3.125 | 3.225 |

| Iteration 3 | 2.058 | 2.134 | 2.889 | 2.889 | 2.058 | 2.058 | 2.058 | 2.058 | 2.665 | 2.665 | 3.004 | 3.087 |

| Iteration 4 | 2.329 | 3.120 | 2.789 | 2.789 | 2.329 | 2.329 | 2.329 | 2.329 | 2.015 | 2.015 | 2.997 | 3.102 |

| Iteration 5 | 2.279 | 3.089 | 3.256 | 3.256 | 2.279 | 2.279 | 3.345 | 3.345 | 2.058 | 2.058 | 2.279 | 2.279 |

| Iteration 6 | 2.228 | 3.310 | 3.658 | 3.658 | 2.228 | 2.228 | 2.228 | 2.228 | 2.987 | 2.987 | 2.228 | 2.228 |

| Iteration 7 | 3.123 | 3.531 | 3.987 | 3.987 | 3.123 | 3.123 | 3.004 | 3.004 | 2.753 | 2.753 | 3.123 | 3.123 |

| Iteration 8 | 2.127 | 2.178 | 3.854 | 3.854 | 2.127 | 2.127 | 2.127 | 2.127 | 2.861 | 2.861 | 2.127 | 2.127 |

| Iteration 9 | 3.404 | 3.650 | 3.145 | 3.145 | 3.404 | 3.404 | 2.767 | 2.767 | 2.001 | 2.001 | 3.404 | 3.404 |

| Iteration 10 | 2.026 | 2.077 | 3.521 | 3.521 | 2.026 | 2.026 | 2.026 | 2.198 | 3.021 | 3.021 | 2.026 | 2.026 |

| No. | City | N. Variables | Si | Sg | Sb | Se | L | B | Yc | C | Sc | P | Mg | Me | Vm |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | Turin | 9 | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ||||

| 2 | Milan | 7 | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ||||||

| 3 | Florence | 9 | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ||||

| 4 | Rome | 10 | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |||

| 5 | Naples | 9 | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ||||

| 6 | Catania | 10 | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ |

| City | Model | CoD (%) |

|---|---|---|

| Turin | Y = + 2.434 · Vm0.5 + 0.3733 · Me0.5 + 0.99371 · Sb0.5 · B0.5 · Vm0.5 − + 4.4136 · Sb0.5 · B0.5 · Yc0.5 · P0.5 · Me0.5 + 7.617 · Si0.5 − 4.1752 · Si · Vm0.5 + + 7.4833 | 85.53 |

| Milan | Y = + 0.49351 · C0.5 · Vm − 0.88769 · Yc0.5 · P − 0.56312 · L0.5 · B0.5 · Mg + + 24.1533 · Sg0.5 · Se2 · L + 1.2286 · Sg · Vm + 8.1673 · Si0.5 − 4.1711 · Si + + 2.8284 · Si · L · B0.5 + 10.7489 | 96.04 |

| Florence | Y = + 23.2683 · Vm0.5 − 13.2187 · Vm + 0.61728 · B0.5 · Me 0.5 · Vm2 + + 1.8377 · Sb2 + 5.8364 · Si0.5 + 170.3596 · Si0.5 · Sb2 · L · Yc − + 2.2608 · Si + 0.18337 | 93.00 |

| Rome | Y = + 2.3773 · Vm0.5 + 0.27166 · Me − 0.66914 · Yc0.5 · Me2 + + 9.5008 · Se · Yc2 · P2 + 1.7449 · Sb · L0.5 · B + 3.0846 · Si0.5 + + 2.5818 · Si0.5 · L0.5 · Yc2 · Me2 + 9.402 | 89.84 |

| Naples | Y = + 4.3382 · Vm − 2.0486 · Vm2 + 0.98283 · L · Yc0.5 · Me2 + 0.75291 · Sb0.5 · B0.5 · · Me0.5 + 9.3479 · Si0.5 − 4.2403 · Si + 7.4542 | 93.72 |

| Catania | Y = + 1.9795 · Vm0.5 + 0.38123 · Me2 + 1.0016 · B0.5 + 13.2376 · L0.5 · B2 · Yc2 · Mg + + 2.5865 · Sb0.5 · Se2 · B · Yc · C · Me2 + 2.1141 · Sg2 · Yc0.5 · Vm2 + 2.762 · Si0.5 + + 8.1768 | 84.73 |

| No. Iteration | Turin | Milan | Florence | Rome | Naples | Catania | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Training Set | Validation Set | Training Set | Validation Set | Training Set | Validation Set | Training Set | Validation Set | Training Set | Validation Set | Training Set | Validation Set | |

| Iteration 1 | 2.217 | 2.351 | 2.551 | 2.614 | 2.292 | 2.434 | 2.227 | 2.237 | 2.125 | 2.136 | 2.660 | 2.667 |

| Iteration 2 | 2.872 | 2.889 | 2.121 | 2.179 | 2.880 | 2.887 | 2.917 | 2.938 | 2.884 | 2.894 | 3.201 | 3.212 |

| Iteration 3 | 2.091 | 2.078 | 2.889 | 2.985 | 3.210 | 3.221 | 2.156 | 2.208 | 2.485 | 2.506 | 2.998 | 3.008 |

| Iteration 4 | 2.373 | 2.348 | 2.789 | 2.843 | 2.384 | 2.394 | 2.385 | 2.448 | 2.444 | 2.496 | 2.581 | 2.602 |

| Iteration 5 | 2.299 | 2.364 | 3.256 | 3.258 | 2.309 | 2.330 | 3.345 | 3.403 | 2.252 | 2.315 | 2.411 | 2.463 |

| Iteration 6 | 2.247 | 2.231 | 2.543 | 2.653 | 2.268 | 2.320 | 2.273 | 2.369 | 2.987 | 3.045 | 3.012 | 3.075 |

| Iteration 7 | 3.208 | 3.138 | 2.852 | 2.985 | 3.260 | 3.323 | 3.004 | 3.058 | 2.101 | 2.197 | 2.589 | 2.647 |

| Iteration 8 | 2.130 | 2.129 | 2.998 | 2.895 | 2.193 | 2.251 | 2.184 | 2.186 | 2.001 | 2.055 | 2.875 | 2.971 |

| Iteration 9 | 3.201 | 3.321 | 3.145 | 3.145 | 3.259 | 3.355 | 2.767 | 2.782 | 2.589 | 2.591 | 3.001 | 3.055 |

| Iteration 10 | 2.028 | 2.080 | 3.521 | 3.521 | 2.124 | 2.178 | 2.049 | 2.198 | 3.021 | 3.036 | 2.498 | 2.500 |

| No. | City | N. Variables | Si | Sg | Sb | Se | L | B | Yc | C | Sc | P | Mg | Me | Vm |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | Turin | 7 | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ||||||

| 2 | Milan | 10 | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |||

| 3 | Florence | 7 | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ||||||

| 4 | Rome | 9 | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ||||

| 5 | Naples | 7 | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ||||||

| 6 | Catania | 11 | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ |

| City | No. Phase | Si | Sb | Sg | Se | Me | Mg | B | L | Yc | C | Sc | P | Vm |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Turin | Phase I | ✔ | ✔ | ✔ | ✔ | ✔ | ✔ | ✔ | ✔ | ✔ | ||||

| Phase II | ✔ | ✔ | ✔ | ✔ | ✔ | ✔ | ✔ | |||||||

| Milan | Phase I | ✔ | ✔ | ✔ | ✔ | ✔ | ✔ | ✔ | ||||||

| Phase II | ✔ | ✔ | ✔ | ✔ | ✔ | ✔ | ✔ | ✔ | ✔ | ✔ | ||||

| Florence | Phase I | ✔ | ✔ | ✔ | ✔ | ✔ | ✔ | ✔ | ✔ | ✔ | ||||

| Phase II | ✔ | ✔ | ✔ | ✔ | ✔ | ✔ | ✔ | |||||||

| Rome | Phase I | ✔ | ✔ | ✔ | ✔ | ✔ | ✔ | ✔ | ✔ | ✔ | ✔ | |||

| Phase II | ✔ | ✔ | ✔ | ✔ | ✔ | ✔ | ✔ | ✔ | ✔ | |||||

| Naples | Phase I | ✔ | ✔ | ✔ | ✔ | ✔ | ✔ | ✔ | ✔ | ✔ | ||||

| Phase II | ✔ | ✔ | ✔ | ✔ | ✔ | ✔ | ✔ | |||||||

| Catania | Phase I | ✔ | ✔ | ✔ | ✔ | ✔ | ✔ | ✔ | ✔ | ✔ | ✔ | |||

| Phase II | ✔ | ✔ | ✔ | ✔ | ✔ | ✔ | ✔ | ✔ | ✔ | ✔ | ✔ |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Tajani, F.; Liddo, F.D.; Guarini, M.R.; Ranieri, R.; Anelli, D. An Assessment Methodology for the Evaluation of the Impacts of the COVID-19 Pandemic on the Italian Housing Market Demand. Buildings 2021, 11, 592. https://doi.org/10.3390/buildings11120592

Tajani F, Liddo FD, Guarini MR, Ranieri R, Anelli D. An Assessment Methodology for the Evaluation of the Impacts of the COVID-19 Pandemic on the Italian Housing Market Demand. Buildings. 2021; 11(12):592. https://doi.org/10.3390/buildings11120592

Chicago/Turabian StyleTajani, Francesco, Felicia Di Liddo, Maria Rosaria Guarini, Rossana Ranieri, and Debora Anelli. 2021. "An Assessment Methodology for the Evaluation of the Impacts of the COVID-19 Pandemic on the Italian Housing Market Demand" Buildings 11, no. 12: 592. https://doi.org/10.3390/buildings11120592