Cost Modeling from the Contractor Perspective: Application to Residential and Office Buildings

Abstract

:1. Introduction

2. Literature Review

3. Data and Methods

4. Results and Discussion

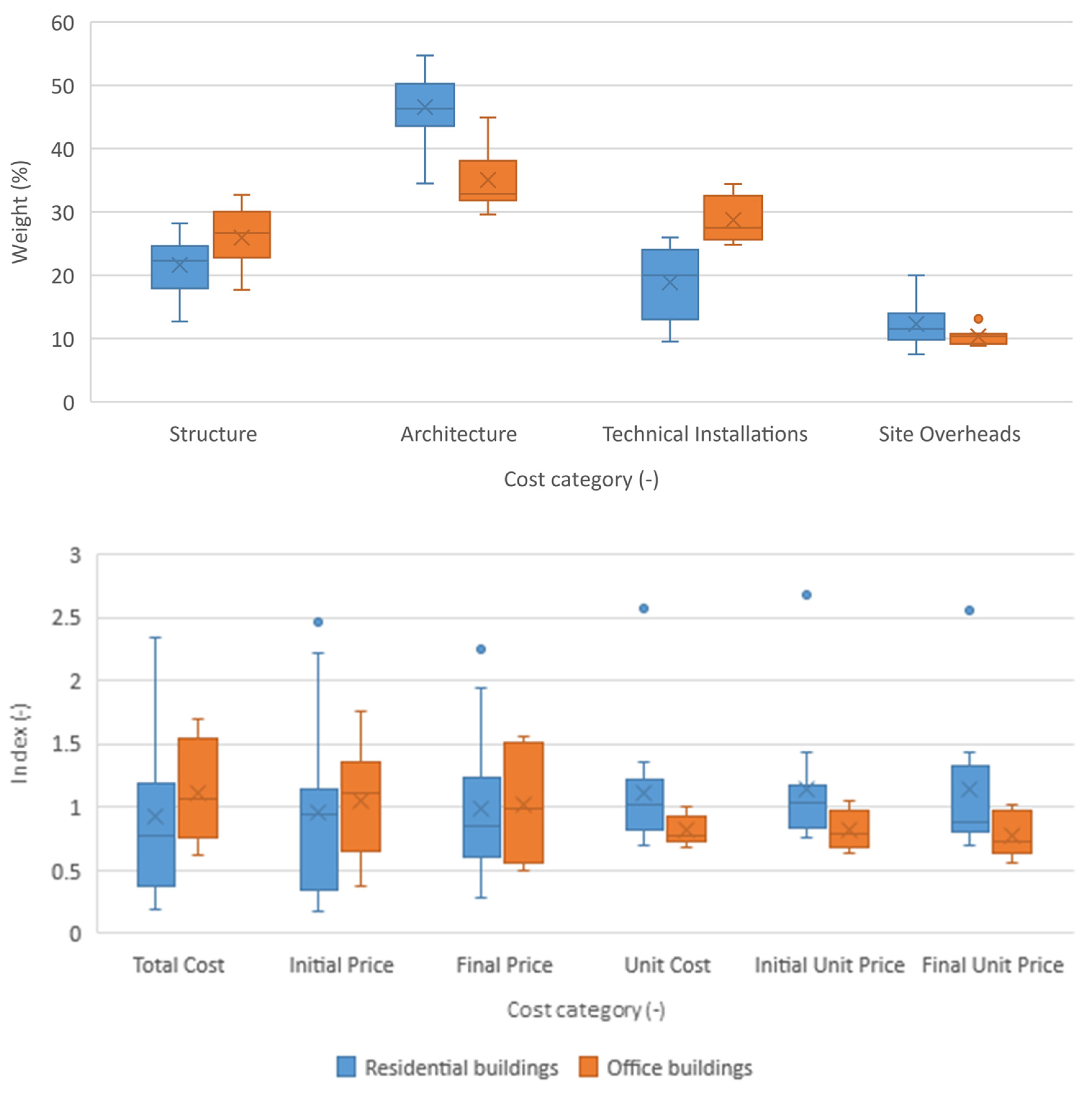

4.1. Preliminary Data Analysis

4.2. Data Modeling

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Hegazy, T.; Ayed, A. Neural Network Model for Parametric Cost Estimation of Highway Projects. J. Constr. Eng. Manag. 1998, 124, 210–218. [Google Scholar] [CrossRef]

- Cruz, C.O.; Branco, F. Reconstruction Cost Model for Housing Insurance. J. Leg. Aff. Disput. Resolut. Eng. Constr. 2020, 12, 05020007. [Google Scholar] [CrossRef]

- Lowe, D.J.; Emsley, M.W.; Harding, A. Predicting Construction Cost Using Multiple Regression Techniques. J. Constr. Eng. Manag. 2006, 132, 750–758. [Google Scholar] [CrossRef] [Green Version]

- Trost, S.M.; Oberlender, G.D. Predicting Accuracy of Early Cost Estimates Using Factor Analysis and Multivariate Regression. J. Constr. Eng. Manag. 2003, 129, 198–204. [Google Scholar] [CrossRef]

- Kim, G.H.; Seo, D.S.; Kang, K.I. Hybrid Models of Neural Networks and Genetic Algorithms for Predicting Preliminary Cost Estimates. J. Comput. Civ. Eng. 2005, 19, 208–211. [Google Scholar] [CrossRef]

- Sonmez, R. Conceptual cost estimation of building projects with regression analysis and neural networks. Can. J. Civ. Eng. 2004, 31, 677–683. [Google Scholar] [CrossRef]

- Soto, B.G.; Streule, T.; Klippel, M.; Bartlomé, O.; Adey, B.T. Improving the planning and design phases of construction projects by using a Case-Based Digital Building System. Int. J. Constr. Manag. 2018, 20, 1–12. [Google Scholar] [CrossRef]

- Jin, R.; Han, S.; Hyun, C.; Cha, Y. Application of Case-Based Reasoning for Estimating Preliminary Duration of Building Projects. J. Constr. Eng. Manag. 2016, 142, 04015082. [Google Scholar] [CrossRef]

- Hu, X.; Xia, B.; Skitmore, M.; Chen, Q. The application of case-based reasoning in construction management research: An overview. Autom. Constr. 2016, 72, 65–74. [Google Scholar] [CrossRef] [Green Version]

- Kim, K.J.; Kim, K. Preliminary Cost Estimation Model Using Case-Based Reasoning and Genetic Algorithms. J. Comput. Civ. Eng. 2010, 24, 499–505. [Google Scholar] [CrossRef]

- Ji, C.; Hong, T.; Hyun, C. CBR Revision Model for Improving Cost Prediction Accuracy in Multifamily Housing Projects. J. Manag. Eng. 2010, 26, 229–236. [Google Scholar] [CrossRef]

- Ahn, J.; Ji, S.-H.; Ahn, S.J.; Park, M.; Lee, H.-S.; Kwon, N.; Lee, E.-B.; Kim, Y. Performance evaluation of normalization-based CBR models for improving construction cost estimation. Autom. Constr. 2020, 119, 103329. [Google Scholar] [CrossRef]

- Kim, G.-H.; An, S.-H.; Kang, K.-I. Comparison of construction cost estimating models based on regression analysis, neural networks, and case-based reasoning. Build. Environ. 2004, 39, 1235–1242. [Google Scholar] [CrossRef]

- Rafiei, M.H.; Adeli, H. Novel Machine-Learning Model for Estimating Construction Costs Considering Economic Variables and Indexes. J. Constr. Eng. Manag. 2018, 144, 04018106. [Google Scholar] [CrossRef]

- Günaydın, H.M.; Doğan, S.Z. A neural network approach for early cost estimation of structural systems of buildings. Int. J. Proj. Manag. 2004, 22, 595–602. [Google Scholar] [CrossRef] [Green Version]

- Dogăn, S.Z.; Arditi, D.; Günaydın, H.M. Determining Attribute Weights in a CBR Model for Early Cost Prediction of Structural Systems. J. Constr. Eng. Manag. 2006, 132, 1092–1098. [Google Scholar] [CrossRef] [Green Version]

- Jin, R.; Cho, K.; Hyun, C.; Son, M. MRA-based revised CBR model for cost prediction in the early stage of construction projects. Expert Syst. Appl. 2012, 39, 5214–5222. [Google Scholar] [CrossRef]

- Sousa, V.; Almeida, N.M.; Dias, L.A. Role of Statistics and Engineering Judgment in Developing Optimized Time-Cost Relationship Models. J. Constr. Eng. Manag. 2014, 140, 04014034. [Google Scholar] [CrossRef]

- Sousa, V.; Almeida, N.M.; Dias, L.A.; Branco, F.A. Risk-Informed Time-Cost Relationship Models for Sanitation Projects. J. Constr. Eng. Manag. 2014, 140, 06014002. [Google Scholar] [CrossRef]

- Sousa, V.; Meireles, I. The Influence of the Construction Technology in Time-Cost Relationships of Sewerage Projects. Water Resour. Manag. 2018, 32, 2753–2766. [Google Scholar] [CrossRef]

- Thalmann, P. A low-cost construction price index based on building functions. In Proceedings of the 15th International Cost Engineering Congress, ICEC, Rotterdam, The Netherlands, 1 March 1998. [Google Scholar]

- Elhag, T.M.S.; Boussabaine, A.H. An artificial neural system for cost estimation of construction projects. In Proceedings of the 14th Annual ARCOM Conference, Reading, UK, 9–11 September 1998; pp. 219–226. [Google Scholar]

- Emsley, M.W.; Lowe, D.J.; Duff, A.R.; Harding, A.; Hickson, A. Data modelling and the application of a neural network approach to the prediction of total construction costs. Constr. Manag. Econ. 2002, 20, 465–472. [Google Scholar] [CrossRef]

- Picken, D.H.; Ilozor, B.D. Height and construction costs of buildings in Hong Kong. Constr. Manag. Econ. 2003, 21, 107–111. [Google Scholar] [CrossRef]

- Attalla, M.; Hegazy, T. Predicting Cost Deviation in Reconstruction Projects: Artificial Neural Networks versus Regression. J. Constr. Eng. Manag. 2003, 129, 405–411. [Google Scholar] [CrossRef]

- Skitmore, R.M.; Ng, S.T. Forecast models for actual construction time and cost. Build. Environ. 2003, 38, 1075–1083. [Google Scholar] [CrossRef] [Green Version]

- Elhag, T.; Boussabaine, A.; Ballal, T. Critical determinants of construction tendering costs: Quantity surveyors’ standpoint. Int. J. Proj. Manag. 2005, 23, 538–545. [Google Scholar] [CrossRef]

- Li, H.; Shen, Q.; Love, P.E. Cost modelling of office buildings in Hong Kong: An exploratory study. Facilities 2005, 23, 438–452. [Google Scholar] [CrossRef]

- Stoy, C.; Schalcher, H.-R. Residential Building Projects: Building Cost Indicators and Drivers. J. Constr. Eng. Manag. 2007, 133, 139–145. [Google Scholar] [CrossRef]

- Wheaton, W.C.; Simonton, W.E. The secular and cyclic behavior of ‘true’ construction costs. J. Real Estate Res. 2007, 29, 1–26. Available online: https://www.jstor.org/stable/24888194 (accessed on 1 October 2021). [CrossRef]

- Stoy, C.; Pollalis, S.; Schalcher, H.-R. Drivers for Cost Estimating in Early Design: Case Study of Residential Construction. J. Constr. Eng. Manag. 2008, 134, 32–39. [Google Scholar] [CrossRef]

- Jin, R.; Han, S.; Hyun, C.; Kim, J. Improving Accuracy of Early Stage Cost Estimation by Revising Categorical Variables in a Case-Based Reasoning Model. J. Constr. Eng. Manag. 2014, 140, 04014025. [Google Scholar] [CrossRef]

- Bayram, S.; Ocal, M.E.; Oral, E.L.; Atis, C. Comparison of multi layer perceptron (MLP) and radial basis function (RBF) for construction cost estimation: The case of Turkey. J. Civ. Eng. Manag. 2015, 22, 480–490. [Google Scholar] [CrossRef] [Green Version]

- Muratova, A.; Ptukhina, I. BIM as an Instrument of a Conceptual Project Cost Estimation; Springer: Cham, Switzerland, 2020; Volume 70. [Google Scholar] [CrossRef]

- Karaca, I.; Gransberg, D.D.; Jeong, H.D. Improving the Accuracy of Early Cost Estimates on Transportation Infrastructure Projects. J. Manag. Eng. 2020, 36, 04020063. [Google Scholar] [CrossRef]

- Swei, O.; Gregory, J.; Kirchain, R. Construction cost estimation: A parametric approach for better estimates of expected cost and variation. Transport. Res. B-Meth. 2017, 101, 295–305. [Google Scholar] [CrossRef]

- Flyvbjerg, B.; Hon, C.; Fok, W.H. Reference class forecasting for Hong Kong’s major roadworks projects. Proc. Inst. Civ. Eng.-Civ. Eng. 2016, 169, 17–24. [Google Scholar] [CrossRef] [Green Version]

- Gunduz, M.; Ugur, L.O.; Ozturk, E. Parametric cost estimation system for light rail transit and metro trackworks. Expert Syst. Appl. 2011, 38, 2873–2877. [Google Scholar] [CrossRef]

- Al-Tabtabai, H.; Alex, A.P.; Tantash, M. Preliminary cost estimation of highway construction using neural networks. Cost Eng. 1999, 41, 19–24. [Google Scholar]

- Shehu, Z.; Endut, I.R.; Akintoye, A.; Holt, G.D. Cost overrun in the Malaysian construction industry projects: A deeper insight. Int. J. Proj. Manag. 2014, 32, 1471–1480. [Google Scholar] [CrossRef]

- Sweis, G.J.; Sweis, R.; Rumman, M.A.; Hussein, R.A.; Dahiya, S.E. Cost overruns in public construction projects: The case of Jordan. J. Am. Sci. 2013, 9, 134–141. [Google Scholar] [CrossRef] [Green Version]

- Love, P.E.D.; Wang, X.; Sing, C.-P.; Tiong, R.L.K. Determining the probability of cost overruns in Australian construction and engineering projects. J. Constr. Eng. Manag. 2013, 139, 321–330. [Google Scholar] [CrossRef]

- Love, P.; Ahiaga-Dagbui, D. Debunking fake news in a post-truth era: The plausible untruths of cost underestimation in transport infrastructure projects. Transp. Res. Part A Policy Pr. 2018, 113, 357–368. [Google Scholar] [CrossRef]

- Love, P.E.; Ika, L.A.; Ahiaga-Dagbui, D.D. On de-bunking ‘fake news’ in a post truth era: Why does the Planning Fallacy explanation for cost overruns fall short? Transp. Res. Part A Policy Pr. 2019, 126, 397–408. [Google Scholar] [CrossRef]

- Love, P.; Sing, C.P.; Carey, B.; Kim, J.T. Estimating Construction Contingency: Accommodating the Potential for Cost Overruns in Road Construction Projects. J. Infrastruct. Syst. 2015, 21, 04014035. [Google Scholar] [CrossRef]

- Love, P.E.D.; Sing, X.C.P.; Tiong, R.L.K. Determining the Probability of Project Cost Overruns. J. Constr. Eng. Manag. 2020, 146, 04020060. [Google Scholar] [CrossRef]

- Kaming, P.F.; Olomolaiye, P.O.; Holt, G.; Harris, F.C. Factors influencing construction time and cost overruns on high-rise projects in Indonesia. Constr. Manag. Econ. 1997, 15, 83–94. [Google Scholar] [CrossRef]

- AbuSafiya, H.A.M.; Suliman, S.M.A. Causes and Effects of Cost Overrun on Construction Project in Bahrain: Part I (Ranking of Cost Overrun Factors and Risk Mapping). Mod. Appl. Sci. 2017, 11, 20. [Google Scholar] [CrossRef] [Green Version]

- Derakhshanalavijeh, R.; Teixeira, J.M.C. Cost overrun in construction projects in developing countries, Gas-Oil industry of Iran as a case study. J. Civ. Eng. Manag. 2016, 23, 125–136. [Google Scholar] [CrossRef] [Green Version]

- Annamalaisami, C.D.; Kuppuswamy, A. Reckoning construction cost overruns in building projects through methodological consequences. Int. J. Constr. Manag. 2019, 1, 1–11. [Google Scholar] [CrossRef]

- Balali, A.; Moehler, R.C.; Valipour, A. Ranking cost overrun factors in the mega hospital construction projects using Delphi-SWARA method: An Iranian case study. Int. J. Constr. Manag. 2020, 1, 1–9. [Google Scholar] [CrossRef]

- Shrestha, P.P.; Fathi, M. Impacts of Change Orders on Cost and Schedule Performance and the Correlation with Project Size of DB Building Projects. J. Leg. Aff. Disput. Resolut. Eng. Constr. 2019, 11, 04519010. [Google Scholar] [CrossRef]

- Flyvbjerg, B.; Holm, M.K.S.; Buhl, S.L. What Causes Cost Overrun in Transport Infrastructure Projects? Transp. Rev. 2004, 24, 3–18. [Google Scholar] [CrossRef] [Green Version]

- Flyvbjerg, B.; Holm, M.S.; Buhl, S. Underestimating Costs in Public Works Projects:Error or Lie? J. Am. Plan. Assoc. 2002, 68, 279–295. [Google Scholar] [CrossRef] [Green Version]

- Pearl, R.G.; Akintoye, A.; Bowen, P.A.; Hardcastle, C. Analysis of tender sum forecasting by quantity surveyors and contractors in South Africa. J. Phys. Dev. Sci. Acta Stuctilla 2003, 10, 5–35. [Google Scholar]

- Bucciol, A.; Chillemi, O.; Palazzi, G. Cost overrun and auction format in small size public works. Eur. J. Political Econ. 2013, 30, 35–42. [Google Scholar] [CrossRef]

- Reyers, J.; Mansfield, J. The assessment of risk in conservation refurbishment projects. Struct. Surv. 2001, 19, 238–244. [Google Scholar] [CrossRef]

- Catalão, F.P.; Cruz, C.O.; Sarmento, J.M. Exogenous determinants of cost deviations and overruns in local infrastructure projects. Constr. Manag. Econ. 2019, 37, 697–711. [Google Scholar] [CrossRef]

- Catalão, F.P.; Cruz, C.O.; Sarmento, J.M. The determinants of cost deviations and overruns in transport projects, an endogenous models approach. Transp. Policy 2019, 74, 224–238. [Google Scholar] [CrossRef]

- Catalão, F.P.; Cruz, C.O.; Sarmento, J.M. Public management and cost overruns in public projects. Int. Public Manag. J. 2020, 1–27. [Google Scholar] [CrossRef]

- Flyvbjerg, B.; Ansar, A.; Budzier, A.; Buhl, S.; Cantarelli, C.; Garbuio, M.; Glenting, C.; Holm, M.S.; Lovallo, D.; Molin, E.; et al. On de-bunking “Fake News” in the post-truth era: How to reduce statistical error in research. Transp. Res. Part A Policy Pr. 2019, 126, 409–411. [Google Scholar] [CrossRef]

- Flyvbjerg, B.; Ansar, A.; Budzier, A.; Buhl, S.; Cantarelli, C.; Garbuio, M.; Glenting, C.; Holm, M.S.; Lovallo, D.; Molin, E.; et al. Five things you should know about cost overrun. Transp. Res. Part A Policy Pr. 2018, 118, 174–190. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Reference | [21] | [22] | [23] | [24] | [25] | [26] | [27] | [28] | [29] | [30] | [31] | [32] | [33] |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Method | |||||||||||||

| Regression Analysis | X | X | X | X | X | X | X | X | X | ||||

| Artificial Neural Network | X | X | X | X | |||||||||

| Case-Based Reasoning | X | ||||||||||||

| Other | X | ||||||||||||

| Variables | |||||||||||||

| Project related | |||||||||||||

| Building type | X | X | X | X | |||||||||

| Area | X | X | X | X | X | X | X | X | |||||

| Number of stories | X | X | X | X | X | ||||||||

| Number of households | X | ||||||||||||

| Height | X | X | X | X | X | ||||||||

| Duration | X | X | X | X | X | ||||||||

| Location | X | X | |||||||||||

| Above ground external envelope characteristics | X | X | X | ||||||||||

| Underground external envelope characteristics | X | X | |||||||||||

| Number of lifts | X | X | X | ||||||||||

| Number of piloti floors | X | ||||||||||||

| Structural characteristics | X | ||||||||||||

| Other | X | X | X | X | X | X | |||||||

| Management related | |||||||||||||

| Type of contract | X | X | X | ||||||||||

| Procurement strategy | X | X | X | X | |||||||||

| Other | X | X | |||||||||||

| Other | |||||||||||||

| Type of client | X | X | |||||||||||

| Construction year | X | X | |||||||||||

| Designer characteristics | X | ||||||||||||

| Contractor characteristics | X | ||||||||||||

| Site characteristics | X | ||||||||||||

| Sample | |||||||||||||

| Size | 15 | 30 | 288 | 36 | 50 | 93 | - | 30 | 290 | 42,340 18,469 | 75 | 91 | 232 |

| Type | R | S | R | - | O | R O | R | R | |||||

| Variable | Sample | Range | Minimum | Maximum | Sum | Mean | Std. Dev. | Skewness | Kurtosis | |

|---|---|---|---|---|---|---|---|---|---|---|

| Floors (-) | Underground | 19 | 4 | 1 | 5 | 64 | 3.37 | 1.065 | −0.849 | 1.152 |

| Above Ground | 21 | 20 | 3 | 23 | 153 | 7.29 | 4.880 | 2.162 | 4.987 | |

| Total | 19 | 16 | 5 | 21 | 189 | 9.95 | 3.837 | 1.424 | 2.528 | |

| Ratio | 19 | 6.25 | 0.75 | 7.00 | 42.48 | 2.24 | 1.531 | 1.944 | 4.278 | |

| Area (m2) | Underground | 22 | 16,893.00 | 420.00 | 17,313.00 | 131,353.75 | 5970.63 | 4184.18 | 0.905 | 0.926 |

| Above Ground | 22 | 10,342.00 | 1557.00 | 11,899.00 | 142,095.44 | 6458.88 | 2983.97 | 0.221 | −0.740 | |

| Total | 23 | 26,136.00 | 1977.00 | 28,113.00 | 294,621.19 | 12,809.62 | 6671.70 | 0.287 | −0.311 | |

| Ratio | 22 | 3.08 | 0.62 | 3.71 | 33.14 | 1.51 | 0.833 | 0.935 | 0.661 | |

| Cost Category Weight (%) | Structure | 23 | 20.00 | 12.70 | 32.70 | 540.30 | 23.49 | 5.019 | −0.237 | −0.398 |

| Architecture | 23 | 25.10 | 29.60 | 54.70 | 955.70 | 41.55 | 7.751 | −0.128 | −1.420 | |

| Technical Installations | 23 | 24.90 | 9.50 | 34.40 | 532.60 | 23.16 | 6.822 | −0.425 | −0.449 | |

| Site Overheads | 23 | 12.50 | 7.50 | 20.00 | 263.40 | 11.45 | 2.988 | 1.598 | 2.854 | |

| Total Cost Index (-) | 21 | 21 | 2.11 | 0.19 | 2.29 | 21.00 | 0.126 | 0.333 | 0.501 | |

| Margin Index (-) | 21 | 21 | 1.96 | 0.36 | 2.32 | 21.00 | 0.134 | 0.375 | 0.501 | |

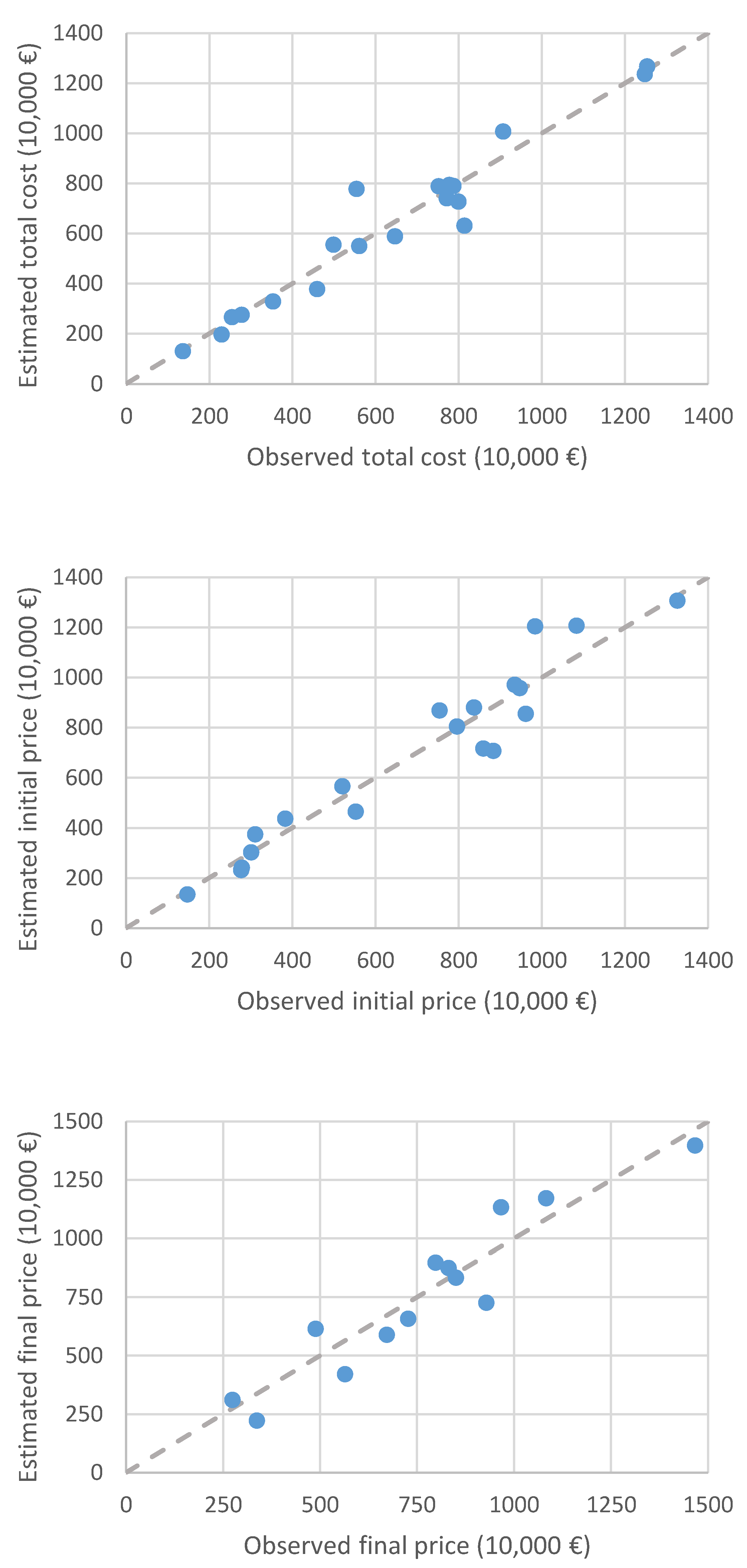

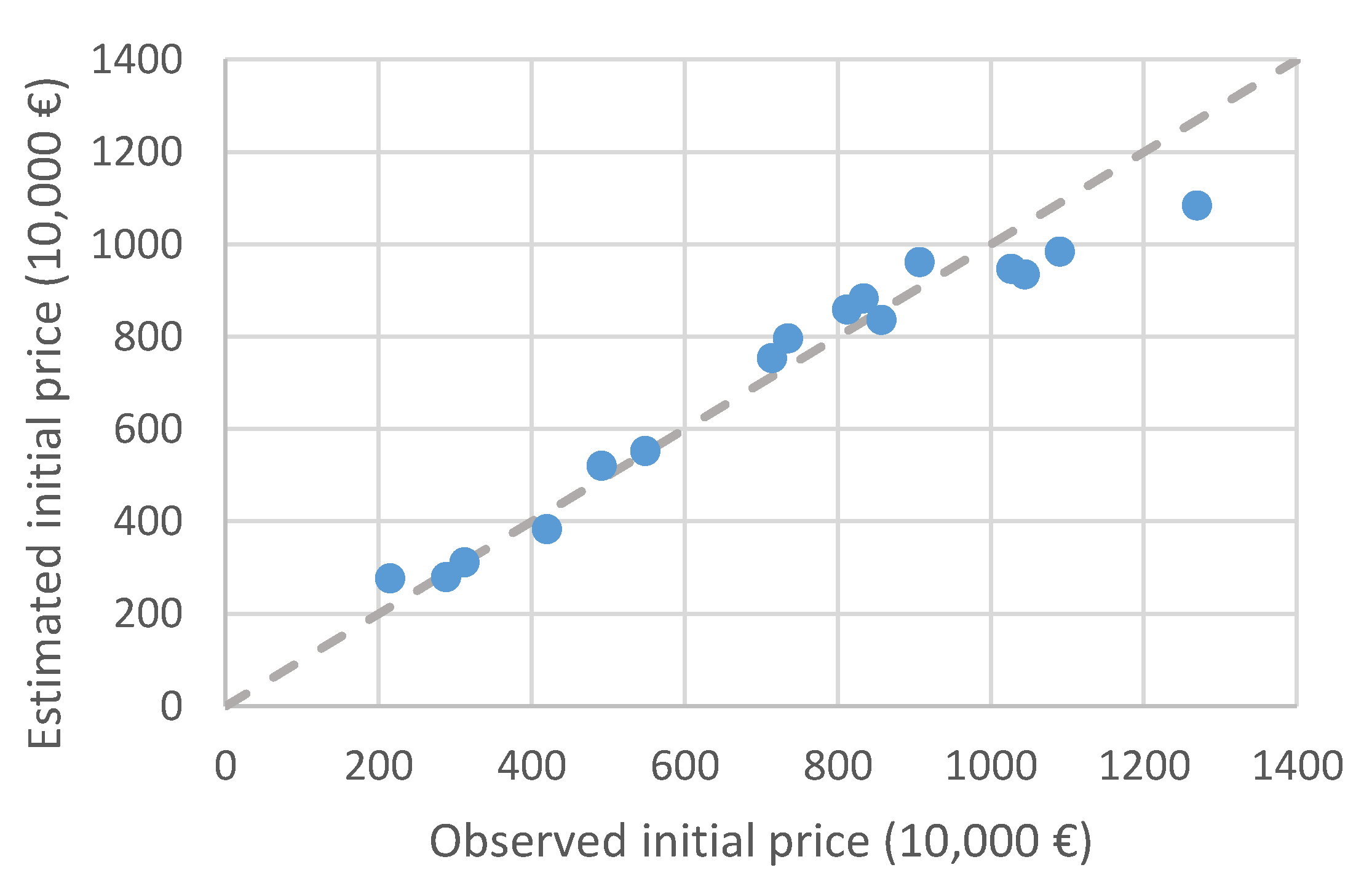

| Price (-) | Initial | 22 | 19,367,364.57 | 1,477,203.03 | 20,844,567.61 | 185,850,166.26 | 8,447,734.83 | 5,107,220.52 | 0.873 | 0.610 |

| Final | 16 | 19,159,444.23 | 2,746,435.50 | 21,905,879.73 | 155,809,085.39 | 9,738,067.84 | 5,404,338.41 | 0.970 | 0.421 | |

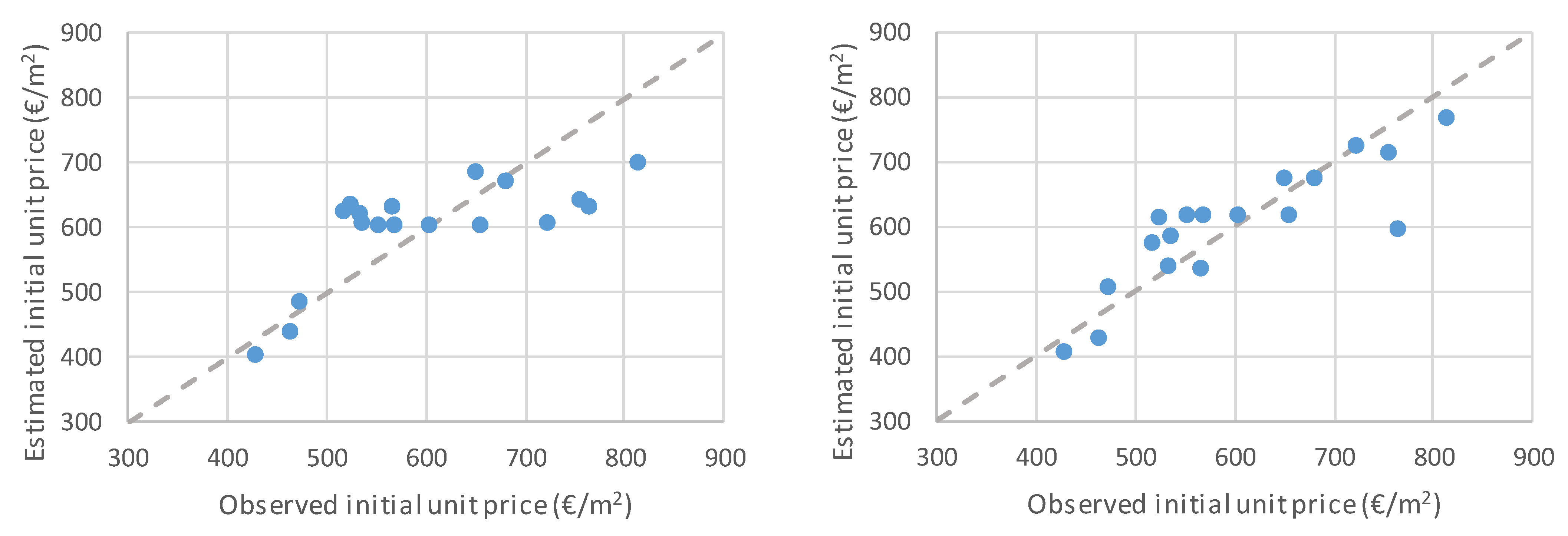

| Unit Price (-) | Initial | 22 | 1401.44 | 429.25 | 1830.69 | 15,022.83 | 682.86 | 288.56 | 3.239 | 12.577 |

| Final | 16 | 1441.43 | 402.96 | 1844.39 | 11,576.50 | 723.53 | 343.78 | 2.563 | 7.779 | |

| Cost Deviation (%) | 15 | 15 | 38.06 | −13.41 | 24.66 | 57.00 | 2.153 | 69.507 | 0.580 | |

| Duration (days) | 23 | 23 | 240 | 240 | 480 | 7320 | 14.109 | 4578.656 | 0.481 | |

| Variables | Levene’s Test | t-Test | Difference | |||||||

|---|---|---|---|---|---|---|---|---|---|---|

| F | Sig. | t | Df | Sig. (2-Tailed) | Mean | Std. Error | 95% Confidence Interval | |||

| Lower | Upper | |||||||||

| Structure | EVA | 0.018 | 0.894 | 2.176 | 19 | 0.042 | 4.557 | 2.094 | 0.174 | 8.940 |

| EVNA | 2.177 | 18.834 | 0.042 | 4.557 | 2.093 | 0.173 | 8.941 | |||

| Architecture | EVA | 0.007 | 0.935 | −5.043 | 19 | 0.000 | −11.906 | 2.361 | −16.848 | −6.965 |

| EVNA | −5.043 | 18.801 | 0.000 | −11.906 | 2.361 | −16.852 | −6.961 | |||

| Technical Installations | EVA | 1.459 | 0.242 | 4.970 | 19 | 0.000 | 9.801 | 1.972 | 5.673 | 13.929 |

| EVNA | 5.070 | 17.367 | 0.000 | 9.801 | 1.933 | 5.729 | 13.873 | |||

| Site Overheads | EVA | 3.285 | 0.086 | −1.802 | 19 | 0.087 | −1.725 | 0.957 | −3.727 | 0.278 |

| EVNA | −1.866 | 13.814 | 0.083 | −1.725 | 0.924 | −3.710 | 0.261 | |||

| Unit Cost | EVA | 0.941 | 0.346 | −2.042 | 17 | 0.057 | −86.404 | 42.314 | −175.679 | 2.871 |

| EVNA | −2.174 | 16.949 | 0.044 | −86.404 | 39.749 | −170.286 | −2.522 | |||

| Initial Unit Price | EVA | 0.174 | 0.681 | −2.222 | 18 | 0.039 | −100.576 | 45.273 | −195.692 | −5.460 |

| EVNA | −2.222 | 17.920 | 0.039 | −100.576 | 45.273 | −195.722 | −5.430 | |||

| Final Unit Price | EVA | 0.054 | 0.821 | −1.412 | 12 | 0.183 | −106.575 | 75.453 | −270.974 | 57.823 |

| EVNA | −1.443 | 11.650 | 0.175 | −106.575 | 73.854 | −268.029 | 54.878 | |||

| Variables | Levene’s Test | t-Test | Difference | |||||||

|---|---|---|---|---|---|---|---|---|---|---|

| F | Sig. | t | df | Sig. (2-Tailed) | Mean | Std. Error | 95% Confidence Interval | |||

| Lower | Upper | |||||||||

| All buildings | ||||||||||

| Structure | EVA | 2.616 | 0.122 | −0.653 | 19 | 0.521 | −1.924 | 2.944 | −8.085 | 4.238 |

| EVNA | −0.445 | 3 | 0.683 | −1.924 | 4.325 | −14.782 | 10.935 | |||

| Architecture | EVA | 0.026 | 0.874 | 1.349 | 19 | 0.193 | 5.919 | 4.387 | −3.262 | 15.100 |

| EVNA | 1.187 | 4 | 0.301 | 5.919 | 4.988 | −7.919 | 19.757 | |||

| Technical Installations | EVA | 3.737 | 0.068 | −1.141 | 19 | 0.268 | −4.199 | 3.680 | −11.901 | 3.504 |

| EVNA | −2.048 | 17 | 0.056 | −4.199 | 2.050 | −8.523 | 0.126 | |||

| Site Overheads | EVA | 1.252 | 0.277 | −0.203 | 19 | 0.841 | −0.268 | 1.316 | −3.021 | 2.486 |

| EVNA | −0.322 | 11 | 0.753 | −0.268 | 0.832 | −2.090 | 1.554 | |||

| Unit Cost | EVA | 0.055 | 0.818 | 1.566 | 17 | 0.136 | 83.700 | 53.461 | −29.092 | 196.492 |

| EVNA | 1.610 | 5 | 0.169 | 83.700 | 51.981 | −50.578 | 217.979 | |||

| Initial Unit Price | EVA | 0.290 | 0.597 | 2.396 | 18 | 0.028 | 133.254 | 55.626 | 16.388 | 250.119 |

| EVNA | 2.392 | 5 | 0.066 | 133.254 | 55.701 | −13.522 | 280.029 | |||

| Final Unit Price | EVA | 0.938 | 0.352 | 1.959 | 12 | 0.074 | 152.192 | 77.701 | −17.105 | 321.488 |

| EVNA | 2.284 | 8 | 0.052 | 152.192 | 66.628 | −1.443 | 305.826 | |||

| Office Buildings | ||||||||||

| Structure | EVA | 1.605 | 0.241 | −1.536 | 8 | 0.163 | −4.719 | 3.072 | −11.802 | 2.364 |

| EVNA | −2.222 | 8 | 0.058 | −4.719 | 2.124 | −9.633 | 0.195 | |||

| Architecture | EVA | 3.441 | 0.101 | 1.216 | 8 | 0.259 | 4.424 | 3.638 | −3.966 | 12.813 |

| EVNA | 1.703 | 8 | 0.127 | 4.424 | 2.597 | −1.566 | 10.414 | |||

| Technical Installations | EVA | 3.395 | 0.103 | 0.829 | 8 | 0.431 | 2.014 | 2.431 | −3.592 | 7.620 |

| EVNA | 0.980 | 6 | 0.366 | 2.014 | 2.055 | −3.049 | 7.078 | |||

| Site Overheads | EVA | 4.993 | 0.056 | −2.723 | 8 | 0.026 | −1.719 | 0.631 | −3.175 | −0.263 |

| EVNA | −2.075 | 2 | 0.148 | −1.719 | 0.828 | −4.695 | 1.257 | |||

| Unit Cost | EVA | 6.878 | 0.039 | 2.612 | 6 | 0.040 | 98.267 | 37.628 | 6.195 | 190.340 |

| EVNA | 3.385 | 5 | 0.022 | 98.267 | 29.034 | 21.891 | 174.643 | |||

| Initial Unit Price | EVA | 10.343 | 0.012 | 3.140 | 8 | 0.014 | 150.429 | 47.907 | 39.956 | 260.901 |

| EVNA | 4.614 | 8 | 0.002 | 150.429 | 32.605 | 74.662 | 226.195 | |||

| Final Unit Price | EVA | 2.021 | 0.228 | 2.465 | 4 | 0.069 | 181.754 | 73.733 | −22.961 | 386.469 |

| EVNA | 2.465 | 3 | 0.088 | 181.754 | 73.733 | −49.712 | 413.220 | |||

| Variables | Structure | Architecture | Technical Installations | Site Overheads | Total Cost | Initial Price | Final Price | Unit Cost | Initial Unit Price | Final Unit Price | Cost Deviation | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Structure | Correlation | −0.425 ** | 0.005 | −0.135 | 0.340 * | 0.417 * | 0.376 | −0.270 | −0.153 | −0.221 | −0.013 | |

| Sig. (2-tailed) | 0.007 | 0.976 | 0.397 | 0.042 | 0.010 | 0.062 | 0.107 | 0.347 | 0.273 | 0.951 | ||

| N | 21 | 21 | 21 | 19 | 20 | 14 | 19 | 20 | 14 | 13 | ||

| Architecture | Correlation | −0.543 ** | 0.053 | −0.216 | −0.253 | −0.143 | 0.322 | 0.253 | 0.319 | −0.077 | ||

| Sig. (2-tailed) | 0.001 | 0.739 | 0.196 | 0.119 | 0.477 | 0.054 | 0.119 | 0.112 | 0.714 | |||

| N | 21 | 21 | 19 | 20 | 14 | 19 | 20 | 14 | 13 | |||

| Technical Installations | Correlation | −0.302 | 0.205 | 0.221 | −0.011 | −0.216 | −0.200 | −0.209 | −0.128 | |||

| Sig. (2-tailed) | 0.057 | 0.221 | 0.173 | 0.956 | 0.196 | 0.218 | 0.298 | 0.542 | ||||

| N | 21 | 19 | 20 | 14 | 19 | 20 | 14 | 13 | ||||

| Site Overheads | Correlation | 0.413 * | 0.483 ** | −0.331 | 0.012 | 0.005 | −0.044 | 0.297 | ||||

| Sig. (2-tailed) | 0.014 | 0.003 | 0.100 | 0.944 | 0.974 | 0.826 | 0.160 | |||||

| N | 19 | 20 | 14 | 19 | 20 | 14 | 13 | |||||

| Underground Floors | Correlation | 0.336 | 0.062 | −0.109 | −0.314 | 0.108 | 0.280 | 0.238 | −0.088 | −0.140 | −0.089 | 0.149 |

| Sig. (2-tailed) | 0.079 | 0.744 | 0.568 | 0.102 | 0.596 | 0.142 | 0.296 | 0.664 | 0.463 | 0.695 | 0.514 | |

| N | 18 | 18 | 18 | 18 | 16 | 18 | 13 | 16 | 18 | 13 | 13 | |

| Above Ground Floors | Correlation | −0.286 | 0.380 * | −0.063 | −0.089 | −0.090 | −0.064 | 0.082 | 0.008 | −0.049 | 0.151 | 0.162 |

| Sig. (2-tailed) | 0.106 | 0.031 | 0.719 | 0.615 | 0.638 | 0.726 | 0.696 | 0.966 | 0.785 | 0.469 | 0.456 | |

| N | 19 | 19 | 19 | 19 | 17 | 18 | 14 | 17 | 18 | 14 | 13 | |

| Total Floors | Correlation | −0.098 | 0.327 | −0.132 | −0.183 | −0.036 | 0.021 | 0.211 | −0.072 | −0.104 | 0.053 | 0.184 |

| Sig. (2-tailed) | 0.587 | 0.069 | 0.461 | 0.313 | 0.853 | 0.907 | 0.325 | 0.710 | 0.561 | 0.806 | 0.389 | |

| N | 18 | 18 | 18 | 18 | 16 | 18 | 13 | 16 | 18 | 13 | 13 | |

| Underground Area | Correlation | 0.558 ** | −0.495 ** | 0.286 | −0.273 | 0.579 ** | 0.663 ** | 0.473 * | −0.520 ** | −0.389 * | −0.516 * | −0.051 |

| Sig. (2-tailed) | 0.000 | 0.002 | 0.070 | 0.085 | 0.001 | 0.000 | 0.019 | 0.002 | 0.016 | 0.010 | 0.807 | |

| N | 21 | 21 | 21 | 21 | 19 | 20 | 14 | 19 | 20 | 14 | 13 | |

| Above Ground Area | Correlation | 0.431 ** | −0.100 | −0.005 | −0.327 * | 0.739 ** | 0.691 ** | 0.758 ** | −0.246 | −0.216 | −0.231 | 0.000 |

| Sig. (2-tailed) | 0.007 | 0.526 | 0.976 | 0.040 | 0.000 | 0.000 | 0.000 | 0.141 | 0.183 | 0.250 | 1.000 | |

| N | 21 | 21 | 21 | 21 | 19 | 20 | 14 | 19 | 20 | 14 | 13 | |

| Total Area | Correlation | 0.539 ** | −0.362 * | 0.171 | −0.350 * | 0.743 ** | 0.800 ** | 0.714 ** | −0.427 * | −0.358 * | −0.407 * | 0.000 |

| Sig. (2-tailed) | 0.001 | 0.022 | 0.277 | 0.027 | 0.000 | 0.000 | 0.000 | 0.011 | 0.027 | 0.043 | 1.000 | |

| N | 21 | 21 | 21 | 21 | 19 | 20 | 14 | 19 | 20 | 14 | 13 | |

| Area Ratio | Correlation | 0.539 ** | −0.362 * | 0.171 | −0.350 * | 0.743 ** | 0.800 ** | 0.714 ** | −0.427 * | −0.358 * | −0.407 * | 0.000 |

| Sig. (2-tailed) | 0.001 | 0.022 | 0.277 | 0.027 | 0.000 | 0.000 | 0.000 | 0.011 | 0.027 | 0.043 | 1.000 | |

| N | 21 | 21 | 21 | 21 | 19 | 20 | 14 | 19 | 20 | 14 | 13 | |

| Parameter | B | Robust Std. Error a | t | Sig. | 95% Confidence Interval | |

|---|---|---|---|---|---|---|

| Lower Bound | Upper Bound | |||||

| Initial Price | ||||||

| Above Ground Area (AGA) | 735.860 | 138.565 | 5.311 | 0.000 | 443.512 | 1028.207 |

| Underground Area (UGA) | 462.428 | 121.467 | 3.807 | 0.001 | 206.155 | 718.701 |

| Area X Crisis | −102.426 | 36.276 | −2.824 | 0.012 | −178.961 | −25.890 |

| Final Price | ||||||

| Above Ground Area | 1393.707 | 399.891 | 3.485 | 0.005 | 513.554 | 2273.860 |

| Underground Area | 232.331 | 127.608 | 1.821 | 0.096 | −48.531 | 513.194 |

| Area X Type | −181.507 | 118.842 | −1.527 | 0.155 | −443.077 | 80.062 |

| Parameter | B | Robust Std. Error a | t | Sig. | 95% Confidence Interval | |

|---|---|---|---|---|---|---|

| Lower Bound | Upper Bound | |||||

| Intercept | 503.309 | 36.238 | 13.889 | 0.000 | 425.022 | 581.596 |

| Above Ground Floors 1.011 | −160.284 | 30.403 | −5.272 | 0.000 | −225.966 | −94.602 |

| Total Floors 1.608 | 17.286 | 3.129 | 5.524 | 0.000 | 10.525 | 24.046 |

| Floor Ratio | 117.935 | 25.915 | 4.551 | 0.001 | 61.949 | 173.920 |

| Economic Crisis = 0 | 211.752 | 36.914 | 5.736 | 0.000 | 132.005 | 291.499 |

| Economic Crisis = 1 | 0.000 | |||||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Monteiro, F.P.; Sousa, V.; Meireles, I.; Oliveira Cruz, C. Cost Modeling from the Contractor Perspective: Application to Residential and Office Buildings. Buildings 2021, 11, 529. https://doi.org/10.3390/buildings11110529

Monteiro FP, Sousa V, Meireles I, Oliveira Cruz C. Cost Modeling from the Contractor Perspective: Application to Residential and Office Buildings. Buildings. 2021; 11(11):529. https://doi.org/10.3390/buildings11110529

Chicago/Turabian StyleMonteiro, Francisco Pereira, Vitor Sousa, Inês Meireles, and Carlos Oliveira Cruz. 2021. "Cost Modeling from the Contractor Perspective: Application to Residential and Office Buildings" Buildings 11, no. 11: 529. https://doi.org/10.3390/buildings11110529